Securities and Exchange Commission

- [Release No. 34-101901; File No. 4-698]

I. Introduction

On March 27, 2024, and pursuant to Section 11A(a)(3) of the Securities Exchange Act of 1934 (the “Exchange Act”) [1] and Rule 608 of Regulation NMS thereunder,[2] BOX Exchange LLC, Cboe BYX Exchange, Inc., Cboe BZX Exchange, Inc., Cboe C2 Exchange, Inc., Cboe EDGA Exchange, Inc., Cboe EDGX Exchange, Inc., Cboe Exchange, Inc., The Financial Industry Regulatory Authority, Inc., Investors' Exchange LLC, Long-Term Stock Exchange, Inc., MEMX LLC, Miami International Securities Exchange LLC, MIAX Emerald, LLC, MIAX PEARL, LLC, Nasdaq BX, Inc., Nasdaq GEMX, LLC, Nasdaq ISE, LLC, Nasdaq MRX, LLC, Nasdaq PHLX LLC, The Nasdaq Stock Market LLC, New York Stock Exchange LLC, NYSE American LLC, NYSE Arca, Inc., NYSE Chicago, Inc., and NYSE National, Inc. (“the Participants”) filed with the Securities and Exchange Commission (the “Commission” or the “SEC”) proposed amendments to the national market system plan governing the consolidated audit trail (the “CAT NMS Plan” or “Plan”).[3] These proposed amendments (the “Proposal”) were designed to implement certain costs saving measures,[4] including: (A) provisions that would change processing, query, and storage requirements for options market maker quotes in listed options; (B) provisions that would permit the Plan Processor [5] to move raw unprocessed data and interim operational copies of CAT Data [6] ( printed page 103034) older than 15 days to what the Participants described as a more cost-effective storage tier; (C) provisions that would permit the Plan Processor to provide an interim CAT-Order-ID [7] to regulatory users on an “as requested” basis, rather than on a daily basis; and (D) provisions that would codify and expand exemptive relief recently provided by the Commission related to certain recordkeeping and data retention requirements for industry testing data.[8] The Proposal was published for comment in the Federal Register on April 16, 2024.[9]

On July 15, 2024, the Commission instituted proceedings pursuant to Rule 608(b)(2)(i) of Regulation NMS,[10] to determine whether to disapprove the Proposal or to approve the Proposal with any changes or subject to any conditions the Commission deems necessary or appropriate after considering public comment (the “OIP”).[11]

The Participants subsequently submitted an amendment to their Proposal on September 20, 2024 (the “Amendment”), which, among other things, withdrew the proposed provisions that would have permitted the Plan Processor to provide an interim CAT-Order-ID to regulatory users on an “as requested” basis, rather than on a daily basis.[12] The Amendment was published for comment in the Federal Register on October 7, 2024.[13] On October 8, 2024, to provide sufficient time to consider the changes set forth in the Amendment and any comments received on the Amendment, the Commission extended the period within which it must conclude its proceedings to December 12, 2024.[14]

This order approves the Proposal, as modified by the Amendment (hereinafter, the “Proposal” unless otherwise noted).

II. Description of the Proposal, as Modified by the Amendment

The Commission is approving the proposed changes to the CAT NMS Plan.[15]

A. Processing, Query, and Storage Requirements for Options Market Maker Quotes in Listed Options

The Participants proposed to amend the processing, query, and storage requirements that apply to Options Market Maker [16] quotes in Listed Options [17] through the inclusion of a new Section 3.4 in Appendix D of the CAT NMS Plan. Section 6.3(d) of the CAT NMS Plan currently requires each Participant to record and electronically report to the Central Repository [18] details for all Options Market Maker quotes.[19] With respect to Options Market Maker quotes in Listed Options, Section 6.4(d)(iii) of the CAT NMS Plan states that Reportable Events [20] required pursuant to Section 6.3(d)(ii) and (iv) shall be reported to the Central Repository by an Options Exchange in lieu of the reporting of such information by the Options Market Maker.[21] Section 6.4(d)(iii) of the CAT NMS Plan also requires Options Market Makers to report to an Options Exchange the time at which a quote in a Listed Option is sent to the Options Exchange (and, if applicable, any subsequent quote modifications and/or cancellation time when such modification or cancellation is originated by the Options Market Maker), pursuant to compliance rules established by the Options Exchanges.[22] Quote sent time information must be reported to the Central Repository by the Options Exchange in lieu of reporting by the Options Market Maker.[23]

The CAT NMS Plan requires all CAT Data reported to the Central Repository to be processed and assembled to create the complete lifecycle of each Reportable Event.[24] Appendix D, Section 3 of the CAT NMS Plan states that the Plan Processor must use a “daisy chain approach,” in which a series of unique order identifiers, assigned to all order events handled by CAT Reporters,[25] are linked together by the Central Repository and assigned a single CAT-generated CAT-Order-ID that is associated with each individual order event and used to create the complete lifecycle of an order.[26] Timelines for data processing and data availability are described in Section 6.1 and Section 6.2 of Appendix D of the CAT NMS Plan.[27] The CAT NMS Plan further provides that regulators will have access to processed CAT Data through an online targeted query tool and through user-defined direct queries and bulk extract tools described in Section 8.1 and Section 8.2 of Appendix D of the CAT NMS Plan.[28]

The Participants proposed to amend the CAT NMS Plan to provide that Options Market Maker quotes in Listed Options will not be subject to any requirement to link and create an order lifecycle, and will not undergo any linkage validation, linkage feedback, or lifecycle enrichment processing, but ( printed page 103035) will undergo ingestion validation.[29] The Participants stated that, as described in Section 5.1 (Market Maker Quotes) of the Plan Participant Technical Specifications, there are two types of events used to report Options Market Maker quotes in Listed Options: Option Quote (“OQ”) events, which are used to report a new quote or a quote replacement, and Option Quote Cancel (“OQC”) events, which are used to report when a quote is canceled.[30] The Participants also stated that only OQ and/or OQC events would be subject to the amended processing, query, and storage requirements.[31] All other options events [32] would continue to be subject to the requirement to link and create an order lifecycle, would continue to undergo linkage validation, linkage feedback, and linkage enrichment processing, and would continue to be available as usual to regulatory users through existing query tools.[33] The Proposal does not alter any of the reporting obligations set forth under the CAT NMS Plan [34] including, without limitation, obligations to accurately report OQ and OQC events, obligations related to the reporting of “all Material Terms of the Order” for Options Market Maker quotes or obligations related to the reporting of the time at which a quote in a Listed Option is sent to an Options Exchange.[35]

While such reporting obligations would not be altered by proposed Section 3.4 of Appendix D, the Proposal alters the Plan Processor's obligations regarding the processing, query, and storage of Options Market Maker quotes in Listed Options. Specifically, the Plan Processor would be required by proposed Section 3.4 of Appendix D only to ingest and store Options Market Maker quotes in Listed Options.[36] Pursuant to proposed Section 3.4 of Appendix D, the Plan Processor would not be required to also link and create an order lifecycle for Options Market Maker quotes in Listed Options, and such data would not undergo any linkage validation, linkage feedback, or lifecycle enrichment processing, although it would undergo ingestion validation.[37] Proposed Section 3.4 of Appendix D would state that unlinked data for Options Market Maker quotes in Listed Options would be made available to regulators by T+1 at 12:00 p.m. Eastern Time.[38]

The Participants clarified the impact of this change by explaining that the following data elements would no longer be available for Options Market Maker quotes in Listed Options under proposed Section 3.4 of Appendix D: Derived Next Event Timestamp/Derived Next Event Epoch Timestamp, CAT Lifecycle Sequence Number, CAT Lifecycle ID ( i.e., CAT Order ID and Venue Order ID), and Derived Next Event Type Code.[39] In addition, certain processing enrichments, which the Participants characterized as “linkage metadata,” would no longer be available under proposed Section 3.4 of Appendix D: Intra Venue Link Status Code, Unlinked Indicator, Lifecycle Assembly Date, and Associated Lifecycles.[40] Nevertheless, proposed Section 3.4 of Appendix D would require the Plan Processor to provide to regulatory users, upon request, the business and technical requirements needed to re-create the eliminated data elements and/or enrichments, as well as the code the Plan Processor currently uses to derive these eliminated data elements and/or enrichments from the unprocessed Options Market Maker quotes in Listed Options.[41]

The CAT NMS Plan currently requires that the Plan Processor provide access to CAT Data to the Participants and the Commission through various query tools, including an online targeted query tool that provides authorized users with the ability to retrieve CAT Data via an online query screen that includes the ability to choose from a variety of pre-defined selection criteria and user-defined direct queries and bulk extracts that provide authorized users with the ability to retrieve CAT Data via a query tool or language that allows users to query all available attributes and data sources.[42] The online targeted query tool functionality provided by FINRA CAT, the current Plan Processor, is provided by tools that are sometimes referred to as “DIVER” or “MIRS.” “BDSQL” is the user-defined direct query tool provided by FINRA CAT, and “Direct Read” is the bulk extract tool provided by FINRA CAT.

Under proposed Section 3.4 of Appendix D, Options Market Maker quotes in Listed Options would be accessible through BDSQL and Direct Read interfaces only and would not be ( printed page 103036) accessible through DIVER.[43] In addition, the Participants stated that elimination of linkage and feedback processes would remove Options Market Maker quotes in Listed Options from certain DIVER and/or MIRS interfaces: Options Market Replay, OLA Viewer, and All-Related Lifecycle Event queries.[44] These DIVER and MIRS tools currently enable regulatory users with less expertise in sophisticated programming skills to access CAT Data. BDSQL and Direct Read—which will be the only query tools that still contain Options Market Maker quotes in Listed Options data under the Proposal—require programming skills in remote data processing and/or knowledge of structured query programming language. The Participants explained that the BDSQL and Direct Read interfaces “represent a significantly more cost-efficient method of providing access” to the relevant data,[45] insofar as the Plan Processor estimated that “the continued optimization of Options Market Maker Quotes to make them available via DIVER would cost approximately $2.8 million per year.” [46] The Participants stated that each of their regulatory groups would be able to conduct their regulatory programs accessing Options Market Maker quotes in Listed Options using only BDSQL and Direct Read and that each regulatory group supported the proposed modification.[47]

The Participants estimated that costs related to creating lifecycles for Options Market Maker quotes in Listed Options were $30 million in 2023.[48] However, the Participants acknowledged, in their Proposal, that they had already begun to implement certain measures to reduce the costs associated with lifecycle linkages for Options Market Maker quotes in Listed Options, pursuant to exemptive relief issued by the Commission in November 2023.[49] The Participants stated that the November 2023 Exemptive Relief Order allows the Plan Processor to create lifecycle linkages for Options Market Maker quotes in Listed Options only once by T+2 at 8 a.m. Eastern Time (as opposed to requiring both an interim lifecycle by T+1 at 9 p.m. Eastern Time and a final lifecycle by T+5 at 8 a.m. Eastern Time).[50] The Participants stated that they expected the above-described “single pass” approach to generating lifecycles for options quotes to result in annual savings of approximately $5.4 million upon implementation in April 2024,[51] and the Commission understands that this “single pass” functionality has now been implemented.

The Participants estimated that the Proposal would result in approximately $20 million in additional annual cost savings in the first year, such that the cost impact of Options Market Maker quotes in Listed Options on the CAT would be reduced from approximately $24.4 million (inclusive of anticipated savings resulting from the implementation of the options quotes “single pass” proposal described above) to approximately $4.0 million annually.[52]

According to the Participants, approximately $12 million of these estimated $20 million in cost savings would be attributable to “linkage processing and data processing reductions, assuming 22 processing days per month for a total of 264 processing days in a year and based on data volumes observed in the first half of 2024.” [53] Specifically, the Participants stated that “[l]inkage processing costs would be reduced from approximately $27,000 per day to $0 per day, resulting in estimated annual linkage processing savings of $7,128,000 ($27,000/day × 264 days). Data processing costs ( i.e., costs attributable to data ingestion and preparation and publication of data versions to the relevant regulatory interfaces) would be reduced from approximately $27,000 per day to $9,000 per day, resulting in estimated annual data processing savings of $4,752,000 ($18,000/day × 264 days).” [54] The Participants explained that these estimated cost savings could increase if “data volumes continue to increase as they have historically . . . .” [55] The Participants further estimated that approximately $8 million of the estimated $20 million in cost savings would be attributable to “the reduction in the storage footprint for Options Market Maker Quotes in Listed Options through the elimination of versioned quote data ( i.e., T+2 8 a.m. ET, T+5 8 a.m. ET, DIVER and OLA copies).” [56] The Participants explained that this estimate assumed a “reduction of the current production storage footprint of approximately 37.5 petabytes (PB) per month based on the data volumes from the first half of 2024 to approximately 9 PB per month” across various storage tiers.[57]

The Participants stated that one-time implementation costs, which would “generally consist of Plan Processor labor costs associated with coding and software development, as well as any related cloud fees associated with the development, testing and load testing of the proposed changes,” were expected to be “minimal relative to overall cost savings” and explained that such costs “may vary based on various factors, including the details of any requirements in any final amendment approved by the Commission and any changes in labor costs.” [58] The Participants stated that “[o]ngoing operational costs, other than cloud hosting costs” would not be affected by the proposed amendments.[59] They also stated that actual future savings could be more or less than their estimates due to changes in a number of variables on which their estimates were based, including “current CAT NMS Plan requirements; reporting by Participants, Industry Members, and market data providers; observed data rates and volumes; current storage and compute pricing discounts, compute reservations, and cost savings plans ( i.e., including savings attributable to the daily On-Demand Capacity Reservations and Compute Savings Plan); and associated cloud fees.” [60] The Participants stated that they believed that “the cost savings ( printed page 103037) estimates and assumptions [were] reasonable and provide[d] an adequate basis for the Commission to evaluate the costs and benefits” of their Proposal.[61]

Although the Participants represented that Options Market Maker quotes in Listed Options are the single largest data source for the CAT, comprising approximately 98% of all options exchange events and approximately 75% of all transaction volume stored in the CAT,[62] the Participants stated the changes set forth in the Proposal would have a limited impact on regulators.[63] The Participants stated that regulators would still have access to unlinked Options Market Maker quotes in Listed Options by T+1 at 12:00 p.m. Eastern Time under the Proposal and asserted that regulatory users would be able to derive the currently available data enrichments if needed.[64] The Participants further stated that “[l]inkage validation is not necessary for Options Market Maker Quotes because the quoteID is an effective replacement for tying quotes to trades.” [65] Since the vast majority of Options Market Maker quotes in Listed Options lifecycles consist of just two events—the quote and its subsequent cancellation—the Participants also explained that the number of Options Market Maker quotes in Listed Options that result in an execution and/or allocation in the first place would be extremely low.[66] Finally, the Participants stated that their usage data “demonstrates” that Options Market Maker quotes in Listed Options lifecycles are “very rarely accessed by regulators.” [67]

Two commenters were supportive of these aspects of the Proposal.[68] For example, SIFMA stated that the “enormity of this data set . . . has created costs and challenges far beyond those envisioned when CAT was approved.” [69] SIFMA explained that the “quote-to-trade ratio in listed options markets is so large that the operational costs of linking quotes to trades is an unreasonable burden” that had not been supported by a cost-benefit analysis.[70] Moreover, SIFMA stated that “the ratio keeps increasing, with [its] member data showing the most recent peak of 32,000 quotes per trade in the U.S. options market in December 2023,” a ratio that they stated was “nearly 4 times greater than the ratio described” in the CAT NMS Plan Approval Order.[71] SIFMA further expressed concern that there were no forces to “constrain the increase in this ratio” and asserted that “certain SEC market structure initiatives might only accelerate the increase.” [72] Given the “extremely small number of quotes” with a “corresponding trade,” SIFMA did not believe it was reasonable to spend so much on processing and storage costs for Options Market Maker quotes in Listed Options, especially if such data would continue to be reported to the CAT and if “the SEC or a Participant can use the quote data as part of its surveillance or investigation patterns, albeit with the need to perform some additional computations.” [73] FIF supported the Proposal, but suggested that the Commission go further and eliminate Options Market Maker quotes in Listed Options from the CAT altogether.[74] FIF also requested that the Commission and the Participants “conduct” and make public “a cost-benefit analysis of maintaining Options Market Maker Quotes in CAT vs. removing them from CAT.” [75]

Rule 608(b)(2) states that the Commission shall approve a proposed amendment to an effective national market system plan, with such changes or subject to such conditions as the Commission may deem necessary or appropriate, if it finds that such amendment is necessary or appropriate in the public interest, for the protection of investors and the maintenance of fair and orderly markets, to remove impediments to, and perfect the mechanisms of, a national market system, or otherwise in furtherance of the purposes of the Exchange Act.[76] When evaluating the estimated cost savings of approximately $20 million annually (and potentially more if data volumes continue to increase as they have historically) in light of the reduced functionalities for Options Market Maker quotes in Listed Options,[77] the Proposal satisfies the approval standard set forth in Rule 608.[78]

In reaching this conclusion, the Commission emphasizes several important considerations. The Proposal would preserve some of the functionality that would have otherwise been available to regulators with respect to Options Market Maker quotes in Listed Options, and the Commission continues to believe that such data has substantial regulatory value.[79] ( printed page 103038) Specifically, under proposed Section 3.4 of Appendix D, regulators would still have direct access to unlinked Options Market Maker quotes in Listed Options by T+1 at 12:00 p.m. Eastern Time.[80] Regulators would also still be able to use two of the existing query tools—BDSQL and Direct Read—to access the relevant data, although access to this data through DIVER and certain MIRS interfaces would be eliminated.[81]

The Commission further understands that proposed Section 3.4 of Appendix D would also require the Plan Processor to provide regulators, on request, with the business and technical requirements needed to re-create data elements and/or enrichments that would otherwise be eliminated for Options Market Maker quotes in Listed Options, as well as the code currently used by the Plan Processor to derive those data elements and/or enrichments.[82] It may be feasible for regulators to perform such ad hoc processing of Options Market Maker Quotes in Listed Options, if they have adequate staff possessing the necessary specialized skills for this work and access to the necessary technical tools. In part, this is because lifecycles for Options Market Maker quotes in Listed Options data are generally less complex compared to lifecycles that include other CAT events, in that Options Market Maker quotes in Listed Options lifecycles usually involve only a single broker-dealer, a single exchange, an exchange quote, and a single cancel or trade event.[83] At the same time, ad hoc processing would likely require technical assistance from the Plan Processor and would impose costs on the regulator. The magnitude of this cost depends on the complexity of revising the code for regulators' systems, the frequency of updates required to maintain the code, and the chosen amount and frequency of data processed. Finally, the CAT NMS Plan will continue to obligate Participants to “adopt policies and procedures, including standards, requiring CAT Data reported to the Central Repository [to] be timely, accurate, and complete, and to ensure the integrity of such CAT Data ( e.g., that such CAT Data has not been altered and remains reliable),” [84] and each Participant's rulebook obligates its members to record and report CAT data in a manner that ensures its timeliness, accuracy, integrity and completeness.[85]

B. Storage for Raw Unprocessed Data, Interim Operational Data, and/or Submission and Feedback Files Older Than 15 Days

The CAT NMS Plan requires CAT Data to be “directly available and searchable electronically without manual intervention for at least six years” [86] and within certain query tool response times.[87] These requirements apply not only to the final corrected data version that is delivered to regulators by T+5 at 8 a.m. Eastern Time, but also to raw unprocessed data and various types of interim operational data, as well as to copies of all submission and feedback files provided to CAT Reporters as part of the correction process.[88] Specifically, with respect to raw unprocessed data and interim operational copies of data created between T+1 and T+5, Section 6.2 of Appendix D of the CAT NMS Plan provides that, prior to 12:00 p.m. Eastern Time on T+1, raw unprocessed data that has been ingested by the Plan Processor must be available to Participants' regulatory staff and the SEC, and between 12:00 p.m. Eastern Time on T+1 and T+5, access to all iterations of processed data must be available to Participants' regulatory staff and the SEC.[89]

The Participants distinguish between Raw Unprocessed Data, Interim Operational Data, and/or submission and feedback files in the Amendment, which would define Raw Unprocessed Data as “data that has been ingested by the Plan Processor and made available to regulators prior to 12:00 p.m. Eastern Time on T+1.” [90] Interim Operational Data, on the other hand, would be defined as “all processed, validated and unlinked data made available to regulators by T+1 at 12:00 p.m. ET and all iterations of processed data made available to regulators between T+1 and T+5, but excludes the final version of corrected data that is made available at T+5 at 8:00 a.m. ET.” [91] Currently, the Participants explained that such data is supplanted in all CAT query tools by the final version of corrected data that is made available to regulators at T+5 at 8:00 a.m. Eastern Time.[92] The Participants stated, however, that such data remains available to regulators after T+5 “without manual intervention” via the use of CAT data management APIs.[93]

To enable such access, Raw Unprocessed Data, Interim Operational Data, and submission and feedback files are stored in S3 Intelligent Tiers provided by the cloud service provider that currently hosts the CAT System, Amazon Web Services (“AWS”).[94] Data files that are either new or that have been recently read by a regulatory user are stored in the S3 Frequent Access tier.[95] Files that have not been read by a regulatory user for 30 days are moved to the S3 Infrequent Access tier.[96] Files that have not been read by a regulatory user for 90 days are moved to the S3 Archive Instant Access tier.[97] Once a regulatory user accesses an older file, it is moved back into the S3 Frequent Access tier.[98]

The Participants stated that regulatory users generally access the latest, corrected version of CAT data [99] and ( printed page 103039) therefore stated that Raw Unprocessed Data, Interim Operational Data, and/or submission and feedback files generally do not provide any regulatory value after the final corrected data is delivered by T+5 at 8 a.m. Eastern Time.[100] The Participants asserted that cost savings could be achieved by archiving Raw Unprocessed Data, Interim Operational Data, and/or submission and feedback files older than 15 days to a more cost-effective storage tier that is optimized for infrequent access.

Specifically, the Participants proposed to add new Section 6.3 to Appendix D of the CAT NMS Plan that would state that Raw Unprocessed Data, Interim Operational Data, and/or submission and feedback files older than 15 days may be retained in an archive storage tier that would not be directly available and searchable electronically without manual intervention and that would not be subject to any query tool performance requirements until it is restored to an accessible storage tier.[101] The Participants stated that Raw Unprocessed Data, Interim Operational Data, and/or submission and feedback files not older than 15 days, as well as all final, corrected data, would remain accessible “without manual intervention” within required query tool response times.[102]

Proposed Section 6.3 of Appendix D would also state that the Plan Processor would restore archived data to an accessible storage tier upon request to the CAT Help Desk by an authorized regulatory user from the Participants or a senior officer from the Commission.[103] The Participants explained that archived data would be restored generally within several hours or business days of a request to the CAT Help Desk that is maintained pursuant to Section 10.3 of Appendix D of the CAT NMS Plan, depending on the volume and size of the date range of the requested data restore. For example, they stated that a request to restore a single day of data may take less than 24 hours, whereas a request to restore a year's worth of data may take several days.[104] The Participants further represented that the Plan Processor would develop policies and procedures to ensure the confidentiality of any regulator requests to obtain data subject to proposed Section 6.3 of Appendix D.[105]

Accordingly, the Participants stated that they believed that the anticipated savings associated with optimizing storage costs, which they estimated as approximately $1 million in annual costs, outweighed the impact on regulatory access to this data.[106] The Participants reached their estimate by calculating the savings that would result from moving Raw Unprocessed Data, Interim Operational Data, and/or submission and feedback files from the S3 Frequent Access tier to the Glacier Deep Archive tier, “based on data volumes observed in the first half of 2024.” [107] The Participants stated that one-time implementation costs, which would “generally consist of Plan Processor labor costs associated with coding and software development, as well as any related cloud fees associated with the development, testing and load testing of the proposed changes,” were expected to be “minimal relative to overall cost savings” and explained that such costs “may vary based on various factors, including the details of any requirements in any final amendment approved by the Commission and any changes in labor costs.” [108] The Participants stated that “[o]ngoing operational costs, other than cloud hosting costs” would not be affected by the proposed amendments.[109] They also stated that actual future savings could be more or less than their estimates due to changes in a number of variables on which their estimates were based, including “current CAT NMS Plan requirements; reporting by Participants, Industry Members, and market data providers; observed data rates and volumes; current storage and compute pricing discounts, compute reservations, and cost savings plans ( i.e., including savings attributable to the daily On-Demand Capacity Reservations and Compute Savings Plan); and associated cloud fees.” [110] The Participants stated that they believed that “the cost savings estimates and assumptions [were] reasonable and provide[d] an adequate basis for the Commission to evaluate the costs and benefits” of their Proposal.[111]

Both commenters supported this aspect of the Proposal.[112] SIFMA further urged the Commission to consider “whether its recordkeeping requirements are appropriate” and to “embark on a more comprehensive undertaking about what other data can be moved to more cost-effective storage solutions.” [113] FIF suggested that, “[i]f the Operational Data does not provide any value to CAT Reporters [114] or to regulators after T+5, there is no reason to store this data after T+5.” [115] Conversely, if the Commission and the Participants issued a public report that “explains the regulatory value of maintaining this Operational Data,” FIF stated that it would “agree with the proposal . . . to move the Operational Data to a more cost-effective storage tier.” [116] FIF further requested that the Commission and the Participants “publish an analysis as to whether this data could be stored in tiers within AWS S3, such as Glacier or Glacier Deep Archive, that could be more cost effective than the AWS S3 Intelligent Tier, as proposed in the Participant ( printed page 103040) filing.” [117] In addition, FIF stated that “enhanced transparency regarding the operation of the CAT system is necessary and appropriate” and expressed concern that “there could be other requirements that the Commission is imposing on the . . . Participants that either do not provide regulatory value or are beyond the scope of CAT.” [118] FIF requested that the Commission “provide clarification” as to why Industry Members and their customers should be “required to incur costs for storage of data that has no regulatory value.” [119]

The Commission does not agree that Raw Unprocessed Data, Interim Operational Data, and/or submission and feedback files have no regulatory value after final data is published at 8 a.m. Eastern Time on T+5. Although the Participants have represented that Raw Unprocessed Data, Interim Operational Data, and/or submission and feedback files has not yet been accessed by regulatory users,[120] the Participants have only very recently represented to the Commission that CAT implementation is complete.[121] Current use is therefore not necessarily a reliable or dispositive reflection of the regulatory need for Raw Unprocessed Data, Interim Operational Data, and/or submission and feedback files. The Commission does agree, however, that the expected regulatory use cases involving this subset of data would likely not be time-sensitive, such that the Participants' proposal to move Raw Unprocessed Data, Interim Operational Data, and/or submission and feedback files to a more cost-effective storage tier after 15 days reflects a reasonable approach.[122] Accordingly, and pursuant to Rule 608(b)(2) under the Exchange Act, the Commission finds that it is appropriate in the public interest, for the protection of investors and the maintenance of fair and orderly markets, to remove impediments to, and perfect the mechanisms of, a national market system, or otherwise in furtherance of the purposes of the Exchange Act to approve the proposed amendments that relate to the storage of Raw Unprocessed Data, Interim Operational Data, and/or submission and feedback files.

C. Codification and Expansion of Exemptive Relief Permitting Deletion of Industry Test Data Older Than Three Months

According to the Participants, Industry Members and Participants submit data to the CAT pursuant to required and voluntary testing, feedback files related to such data, and output files that hold the detailed transactions, referred to herein as “Industry Test Data.” [123] Under Section 1.2 of Appendix D of the CAT NMS Plan, such Industry Test Data must be saved for three months.[124] Separate from this specific three-month retention requirement, Rule 17a-1 under the Exchange Act requires every national securities exchange and national securities association to keep and preserve at least one copy of all documents, including all correspondence, memoranda, papers, books, notices, accounts, and other such records as shall be made or received by it in the course of its business as such and in the conduct of its self-regulatory activity, and to keep all such documents for a period of not less than five years, the first two years in an easily accessible place, subject to the destruction and disposition provisions of Rule 17a-6 under the Exchange Act.[125] Section 9.1 of the CAT NMS Plan, the general recordkeeping provision for the CAT NMS Plan, also states, in relevant part, that the Company shall maintain complete and accurate books and records of the Company in accordance with Rule 17a-1 under the Exchange Act.[126]

The Participants explained that, on June 2, 2023, CAT LLC requested exemptive relief from Rule 17a-1 under the Exchange Act and certain provisions of the CAT NMS Plan relating to the retention of Industry Test Data beyond three months.[127] On November 27, 2023, the Commission granted the requested relief.[128] The Participants stated that their previous request for exemptive relief and the Industry Test Data Exemptive Relief Order apply only to Industry Test Data related to the CAT order and transaction system, not to the customer account and information system (“CAIS”).[129]

The Participants therefore proposed to amend Section 1.2 of Appendix D of the CAT NMS Plan to provide that test data (whether related to the CAT order and transaction system or to the CAIS) may be deleted by the Plan Processor after three months.[130] Proposed Section 1.2 of Appendix D would continue to state that operational metrics associated with industry testing (including, but not limited to, testing results, firms who participated, and amount of data reported and linked) must be stored for the same duration as the CAT production data.[131]

The Participants explained that eliminating Industry Test Data older than three months as permitted by the Industry Test Data Exemptive Relief ( printed page 103041) Order is expected to achieve approximately $1 million per year in savings.[132] According to the Participants, the proposed amendments would not generate additional cost savings beyond those achievable pursuant to the Industry Test Data Exemptive Relief Order,[133] although the Participants generally noted that actual future savings could be more or less than their estimates due to changes in a number of variables on which their estimates were based, including “current CAT NMS Plan requirements; reporting by Participants, Industry Members, and market data providers; observed data rates and volumes; current storage and compute pricing discounts, compute reservations, and cost savings plans ( i.e., including savings attributable to the daily On-Demand Capacity Reservations and Compute Savings Plan); and associated cloud fees.” [134] The Participants stated that one-time implementation costs, which would “generally consist of Plan Processor labor costs associated with coding and software development, as well as any related cloud fees associated with the development, testing and load testing of the proposed changes,” were expected to be “minimal relative to overall cost savings” and explained that such costs “may vary based on various factors, including the details of any requirements in any final amendment approved by the Commission and any changes in labor costs.” [135] The Participants stated that “[o]ngoing operational costs, other than cloud hosting costs” would not be affected by the proposed amendments.[136] The Participants stated that they believed that “the cost savings estimates and assumptions [were] reasonable and provide[d] an adequate basis for the Commission to evaluate the costs and benefits” of their Proposal.[137]

Two commenters, SIFMA and FIF, supported this aspect of the Proposal.[138] FIF further stated that it supported “deletion of all test data after one week” and requested that the Commission and the Participants “publish a cost-benefit analysis of any mandate to retain test data beyond one week,” which analysis should “identify any use cases that would involve access to test data beyond one week, including the regulatory purpose.” [139]

The Commission understands from the Participants that the primary purpose of Industry Test Data is to facilitate CAT Reporter testing needs and not to facilitate regulatory use.[140] The Commission therefore agrees with the Participants and the commenters that, in light of the approximately $1 million per year cost for retaining Industry Test Data beyond three months, the proposed approach to retention of Industry Test Data is reasonable. Accordingly, and pursuant to Rule 608(b)(2) under the Exchange Act, the Commission finds that it is appropriate in the public interest, for the protection of investors and the maintenance of fair and orderly markets, to remove impediments to, and perfect the mechanisms of, a national market system, or otherwise in furtherance of the purposes of the Exchange Act to approve the provisions of the Proposal that relate to the retention of Industry Test Data.[141]

Although the Participants did not specifically also request exemptive relief from Rule 17a-1 under the Exchange Act with respect to Industry Test Data related to the CAIS,[142] such relief is necessary in order to effectuate the Proposal, as Rule 17a-1 would otherwise require Industry Test Data related to the CAIS to be retained for a longer time period. For the above-described reasons, and consistent with its action in the Industry Test Data Retention Exemptive Relief Order, the Commission finds that it is appropriate in the public interest and consistent with the protection of investors under Section 36 of the Exchange Act,[143] as well as consistent with the public interest, the protection of investors, the maintenance of fair and orderly markets and the removal of impediments to, and the perfection of, a national market system under Rule 608(e) under the Exchange Act,[144] to grant relief that exempts each Participant from the longer recordkeeping and data retention requirements for CAIS-related Industry Test Data that otherwise would apply as set forth in Rule 17a-1 under the Exchange Act.[145]

D. Other Comments Received on the Proposal

Both commenters proposed that additional steps be taken to further manage and reduce CAT operating costs.[146] For instance, SIFMA expressed concern that the Commission, “the primary beneficiary of the CAT, . . . does not pay for it, and thus does not have a direct incentive to consider costs, or opportunities for cost savings, in connection with making decisions regarding its operation.” [147] SIFMA stated that the Commission's “rejection” of provisions that would have permitted the Plan Processor to provide an interim CAT-Order-ID to regulatory users on an “as requested” basis, rather than on a daily basis—provisions that were initially included in the Proposal,[148] but withdrawn by the Participants [149] —suggested that “costs and cost savings are not necessarily a Commission priority in connection with decision-making regarding the operation of the CAT.” [150]

SIFMA therefore suggested that the Commission and the Participants should “assess their own CAT usage patterns and needs to identify further cost saving measures.” [151] SIFMA further stated that the CAT “should be operated to meet the reasonable and legitimate needs of regulators, and not as a monolith to address any regulatory use case regardless of the costs.” [152]

SIFMA stated that the “Commission's action in connection with Amendment No. 1 to the proposed Cost Savings Amendment” demonstrated the need for the Participants and the Commission to “provide Industry Members with a more meaningful opportunity to contribute their experience and expertise to the CAT's budget setting and cost savings processes.” [153] Specifically, SIFMA recommended that the Participants establish a separate working group that includes Industry Members to focus on ways the CAT System can be made more efficient from a cost perspective while still achieving its goals, rather than relying on the existing Cost Management Working Group, which is comprised solely of Participant members.[154] “Without more direct involvement by Industry Members in the CAT budgeting process,” SIFMA stated that “there is an insufficient structural framework and incentives to bring CAT costs under control.” [155]

FIF expressed similar concerns.[156] Noting that the Participants have recently estimated “total CAT operating expenses of $248,846,076 for 2025,” FIF stated that this “14.8% increase over the estimated CAT operating expenses for 2024” was “not sustainable over the long-term.” [157] FIF stated that it was “imperative that the Commission take steps to manage CAT operating costs,” including approval of the Proposal and other recommendations made by FIF in their comment letters that were not included in the Proposal.[158] FIF further requested that the Commission “publish a report setting forth the factors giving rise to the significant estimated cost increase for 2025 and whether these factors will continue to apply year-over-year for the foreseeable future.” [159] FIF stated that the Commission “should not impose CAT reporting requirements that are beyond the scope of Commission Rule 613 and the CAT NMS Plan” and that “[p]roposed changes to current CAT processing or reporting requirements that could involve further significant increases in CAT operating costs should be subject to an appropriate cost-benefit analysis that is included as part of a CAT NMS Plan amendment.” [160]

Contrary to the assertions of SIFMA, both the Commission and the Participants have demonstrated their commitment to reducing CAT costs where appropriate—and even where there is some amount of regulatory loss—as evidenced by the very existence of the cost savings measures proposed by the Participants and approved herein by the Commission.[161] The Participants have already formed a Cost Management Working Group comprised of senior members of the Participants that works to find and address cost management needs,[162] and the findings of this group are discussed with the Industry Members that sit on the CAT's Advisory Committee.[163] There are also meaningful and reasonable constraints set on the CAT budgeting process, including a process that gives Industry Members a chance to review and publicly comment on the CAT's budget and that requires Commission review of CAT funding.[164] And the Commission agrees with FIF that any amendments to the requirements of Rule 613 and/or the CAT NMS Plan must be pursued either: (1) through a Commission-led rule-making process that includes public notice and comment and economic analysis; or (2) through the amendment process set forth under Rule 608, which would require the Participants to file with the Commission a proposed amendment to the CAT NMS Plan, subject that amendment to public notice and comment, and generally require approval by the Commission and a consideration of the impact of the amendment on efficiency, competition, and capital formation.[165]

In determining whether any particular cost savings amendment meets the approval standard set forth in Rule 608(b)(2), the Commission evaluates and balances many factors, including the amount of costs savings as well as the potential downstream harms to investors and the U.S. financial markets that could result from less effective regulatory oversight by the SROs and the Commission. The Commission emphasizes that its approval of the specific cost savings amendments that the Participants have proposed for consideration in this proceeding does not foreclose future consideration of additional cost savings amendments and analyses, including the withdrawn interim CAT-Order-ID proposal and the other measures suggested by commenters.[166]

III. Efficiency, Competition, and Capital Formation

A. Introduction

In determining whether to approve an amendment to the CAT NMS Plan and whether that amendment is in the public interest, Rule 613 requires the Commission to consider the impact of that amendment on efficiency, competition, and capital formation.[167] ( printed page 103043) The Participants stated that their proposed amendments “will have a positive impact on competition, efficiency, and capital formation.” [168] The Commission has analyzed the potential impacts of the Proposal.

Based on its analysis, and after considering potential sources of imprecision in the Participants' estimates, the Commission concludes that savings in operating costs will enhance the operational efficiency of CAT,[169] while the changes to CAT Data will lessen some regulatory efficiencies. These changes to regulatory efficiencies, however, are likely to be limited for regulatory activities using small samples of data but potentially more significant for certain time-sensitive regulatory activities using large amounts of data. Effects on market efficiency, competition, and capital formation, stemming from the impacts of the Proposal on regulatory and operational efficiencies, will likely be second-order and limited.

B. Baseline

In analyzing the impact of the Proposal on efficiency, competition and capital formation, the Commission considered the current CAT Data [170] as the baseline. Specifically, the baseline consists of the current properties, and the actual and potential regulatory usages of the CAT Data, in the absence of the Proposal. CAT Data was intended to make possible reconstruction of market events,[171] market analysis and research that inform policy decisions, regulatory activities such as market surveillance, examinations and investigations, and more efficient execution of numerous other regulatory functions.[172] In the CAT NMS Plan Approval Order, the Commission explained how investors benefit from the CAT-enabled improvements to such regulatory activities.[173]

The first provision of the Proposal focuses on Options Market Maker quotes in Listed Options. Along with their lifecycle linkages and associated derived fields, Options Market Maker quotes in Listed Options are currently accessible via an online targeted query tool, called DIVER. Alternatively, regulatory users with specialized knowledge of remote data processing and the structured query programming language (“SQL”) can use BDSQL to construct and run their own complex queries.[174]

The Participants stated that, while the Options Market Maker quotes in Listed Options constitute the largest component of CAT Data,[175] only a small fraction of them end in an execution or allocation.[176] In addition, the Proposal stated that “the vast majority of Options Market Maker Quote lifecycles consist of just two events—the quote and its subsequent cancellation,” [177] which suggests that these quotes have simple lifecycles.

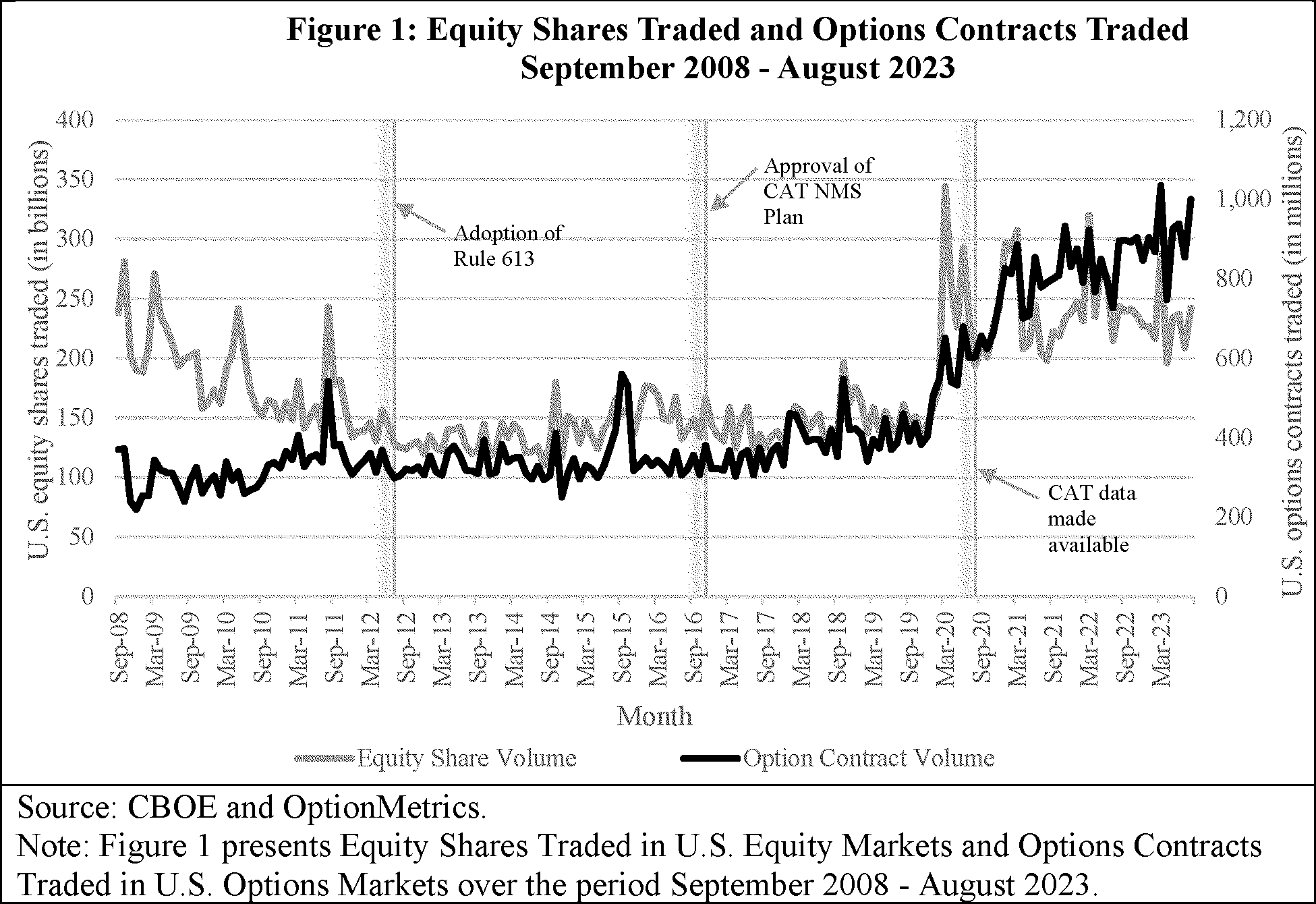

Figure 1 shows the backdrop of the evolution of Options Market Maker quotes in Listed Options, which is that the options market has experienced noticeable overall growth. As Figure 1 shows, the volumes in both the equity and the options markets (equity shares traded and options contracts traded, respectively) have markedly increased since early 2020. While volume growth has somewhat stagnated in the equity market since 2021, volume has continued to grow in the options market. Between 2016 and 2022, the volume of equity shares traded increased by 61 percent and options contracts traded increased by 153 percent.

Table 1 presents an analysis of CAT Data from the first quarter of 2024. It shows that, approximately 90 percent of all options-related events and 80 percent of all events in CAT are Options Market Maker quotes in Listed Options,[178] which include both OQ and OQC events.[179] OQ events account for approximately 72 percent of all options-related events and 63 percent of all events in CAT.

Further analysis of options trades associated with Options Market Maker quotes in Listed Options, in the options market data from Q1-2024,[180] showed that the number of option trades associated with Options Market Maker quotes in Listed Options as percent of CAT OQ events is small, 0.001 percent or less.[181] The analysis, however, also shows that a substantial portion of all options trades, approximately 20 percent, is associated with Options Market Maker quotes.

An analysis of lifecycles of Options Market Maker quotes in selected Listed Options shows that at least for some options on some days these lifecycles can be more complex than suggested by the Participants.[182] For these selected Options, 63 percent of the Options Market Maker quotes had a lifecycle with two events, while almost 10 percent had lifecycles that included five or more events.

The second provision of the Proposal involves Raw Unprocessed Data, Interim Operational Data and/or submission and feedback files data. These data are currently available without “manual intervention” for at least six years within certain query tools.[183] These data are currently stored within the Central Repository via AWS S3-FA storage tier for the first 30 days, in the S3-Infrequent Access tier for the next 60 days, and in the S3-Archive Instant Access tier thereafter.[184] Access to such data prior to the availability of final data can improve the timeliness of regulatory activities for those regulators who do not already have such data.[185]

The third provision of the Proposal relates to the retention of Industry Test Data.[186] Industry Members and Participants submit data to CAT pursuant to both required and voluntary testing; CAT retains the Industry Test Data in connection with such testing. Industry Test Data associated with CAIS is required to be retained for six years whereas CAT LLC was previously permitted to eliminate Industry Test Data related to the CAT order and transaction system after three months.[187] The Participants proposed that test data (whether related to the CAT order and transaction system or to the CAIS) may be deleted by the Plan Processor after three months.

C. Efficiency

The Commission analyzed three types of efficiency impacts from the Proposal: operational efficiency in terms of cost savings of operating the Central Repository; [188] regulatory efficiency in terms of the impact of changes in CAT Data on regulatory activities; and market efficiency in the form of second order impacts on the market.

As discussed further below, cost savings in operating the Central Repository represent an enhancement of the operational efficiency of CAT. The changes to CAT Data from the Proposal will lessen some regulatory efficiencies by delaying certain regulatory activities. While these inefficiencies could be relatively more significant for certain time-sensitive regulatory activities involving large amounts of data, in general, these inefficiencies are likely to be limited.[189] Effects on market efficiency, competition, and capital formation, which stem from the aforementioned impacts of the Proposal on regulatory and operational efficiencies, will likely be second-order and, hence, also limited.

1. Operational Efficiency

The Proposal will result in operational cost savings, net of implementation costs, of operating the Central Repository, which will reduce the CAT Fees borne by Participants, Industry Members, and investors (through pass-throughs). The Participants' estimates of cost savings could be imprecise, however. The actual cost savings could differ from the projected cost savings for several reasons including: (1) assumptions used to generate estimates, (2) uncertainty in the future direction of a number of factors, (3) implementation costs, which are not included in the estimates, (4) some of the cost savings representing costs transferred to regulators, and (5) potential interactions of the Proposal with a recent regulatory change. These issues could mean that the Participants' estimates are somewhat over-estimated or, alternatively, potentially considerably underestimated, depending upon the assumptions and methodologies used.

a. Estimated Cost Savings, Methodologies and Assumptions

The Proposal will result in meaningful cost savings even when considering some of the alternate methodologies and assumptions discussed below. The Participants estimate that the cost savings will be $21 million in the first year, which is 11 percent of the total operating costs of CAT in 2023.[190] The Participants state ( printed page 103046) that they believe their assumptions and estimates are reasonable.[191] The Commission acknowledges the necessity of using simplifying assumptions to generate estimates and that such assumptions can affect the precision of the estimates. The Commission has considered the methodologies and assumptions and concludes that there are at least three issues that could affect the magnitude of the cost estimates—two relating to the volume of CAT Data affected and one relating to a processing cost assumption. However, the cost savings will be meaningful regardless of these issues.

The Participants' cost estimates [192] are generated using current costs. Specifically, the Participants state that, among other things, cost savings estimates are based on “observed data rates and volumes; current discounts, reservations and cost savings plans; and associated cloud fees.” [193] The Commission agrees that using current costs to generate cost savings estimates is reasonable and recognizes that the cost savings in the future could change depending on factors discussed in the next section.[194]

The Participants' storage cost saving estimates are annual cost savings for the first year. However, the CAT NMS Plan requires the storage of six years of data, so the maximum annual cost savings would not be achieved in the first year.[195] Indeed, the Proposal will result in additional potential annual cost savings each year until the Proposal affects the annual storage of six years of data. Based on the current assumptions, the cost savings could eventually reach $48 million per year for the provision on Options Market Maker quotes in Listed Options.[196] Likewise, the storage cost savings from the provision on Raw Unprocessed, Interim Operational Data and/or submission and feedback files could reach $6 million per year to account for a baseline of storing six years of data in an S3 storage tier.[197] These additional annual cost savings would not be expected in full until six years after the implementation of the Proposal.

The Participants' estimates may also not account for the one-time cost savings for affected historical data. The primary historical CAT Data affected by the Proposal are the Raw Unprocessed, Interim Operational Data and/or submission and feedback files.[198] All Raw Unprocessed, Interim Operational Data and/or submission and feedback files older than 15 days will be moved to a cheaper storage tier, including historical data. However, the Participants describe the cost savings estimates as “annual,” [199] suggesting that they do not account for historical data. We estimate that including historical data could add up to $4 million in one-time cost savings.[200]

The Participants, however, likely over-estimated the $12 million estimate in annual processing cost savings from the provision on Options Market Maker quotes in Listed Options. To generate this estimate, the Participants apparently assumed that the per message linkage costs of options events were the same as those for equities events,[201] but this is unlikely.[202] As the CAT Funding Model Approval Order discusses, the linkage processing of equities orders is generally more complex than the linkage processing of options orders.[203] Further, Options Market Maker quotes in Listed Options have mostly simple lifecycles.[204] However, the volume of the Options Market Maker quotes in Listed Options data suggests that they will still account for a large proportion of overall linkage processing costs.[205] Therefore, while the cost savings could be less than $12 million, they will likely still be large.

The Participants did not estimate any cost savings from the provision on CAIS test data but reiterated the $1 million cost savings from the prior related exemptive relief.[206] We expect these test data to have a small storage footprint. While the cost savings will be positive, they are unlikely to increase the approximate magnitude of the cost savings from the prior exemptive relief.

b. Future Magnitude of Cost Savings

The Participants recognize that the actual future cost savings could differ from the estimates because of uncertainty in several factors.[207] These factors include the number of exchanges, Plan requirements, data rates and volumes, discounts, reservations and cost savings plans, and cloud fees.[208] The Participants also state that future cost savings could be greater than ( printed page 103047) the estimates as data volumes grow over time.[209] The Participants produce cost savings estimates that apply only to the first year of implementation.[210] However, the cost savings estimated for the first year may not continue at the same level for at least two reasons: (1) changes in the costs of cloud computing, and (2) changes in the frequency of regulatory requests to have data restored.

Cost savings (and CAT operational costs) could decline as cloud computing evolves. The storage and computing services industries, technologically, are among the most rapidly evolving industries. In some estimates, the costs of host computer and storage services have steadily declined.[211] Similar trends can be observed in the pricing of some of the cloud storage products.[212] The Participants' estimated cost savings of $21 million are based on the current cloud computing and storage costs.[213] Therefore, declines in cloud computing costs could result in smaller than expected future cost savings.

On the other hand, if message traffic keeps increasing, then, despite the rapid technological advancements, the future cost savings could be higher than those estimated for the first year.[214] Indeed, one new options exchange has started operations since the publication of the Notice, likely resulting in a higher volume of Options Market Maker quotes in Listed Options.[215] In addition, one new equities exchange has been approved since the costs were estimated, potentially increasing the storage footprint of Raw Unprocessed Data, Interim Operational Data, and/or submission and feedback files.[216]

Cost savings from the provision on Raw Unprocessed, Interim Operational Data and/or submission and feedback files will be reduced by any data requests by regulators to restore such data.[217] Participants state that retrieving data from Glacier Deep Archive storage is costly and the costs are a function of the size of the data being pulled in addition to the speed with which the request must be fulfilled.[218] This $1 million savings is also based, in part, on an expectation of usage of Raw Unprocessed, Interim Operational Data and/or submission and feedback files older than 15 days that matches the previous four years.[219] According to the Participants, these data were not used during the development of the CAT NMS Plan over the last four years.[220]

c. Implementation Costs

The Amendment states that “the one-time implementation costs are expected to be minimal relative to overall cost savings.” [221] While the Participants do not estimate implementation costs, the Commission can compare anticipated implementation activity to that of recent Commission final rules that include estimates for such activity. According to the Participants, “[o]ne-time implementation costs will generally consist of Plan Processor labor costs associated with coding and software development, as well as any related cloud feed associated with the development, testing and load testing of the proposed changes.” [222] The Participants state that, “[o]ngoing operational costs, other than cloud hosting costs,” will not be affected by the proposed amendments.[223] The Commission agrees that the implementation costs seem minimal relative to overall cost savings.

The Proposal will result in costs to the Plan Processor with respect to developing policies and procedures, revising and testing coding changes, and revising user manuals and training materials. Policies and procedures will dictate how the Plan Processor responds to requests to restore the operational data and ensure confidentiality in the request.[224] Implementing the Proposal will also require changes to programming code to change the processing of affected CAT Data. Finally, user manuals and training will have to be revised to ensure they reflect the CAT Data and access for regulators after the Proposal.

Table 2 shows ranges of implementation costs for implementation activities in recent Commission final rules. The Commission expects the Proposal to fall near the lower end of these ranges, and possibly below them. The estimates for developing policies and procedures in Table 2 apply to policies and procedures that codify business practices,[225] which would be a bigger effort than the policies and procedures for fulfilling requests to restore data. Second, the Commission expects the coding changes necessary to implement the Proposal to involve fewer labor hours than the comparison rules for revising code in Table 2.[226] Finally, while the recent Commission final rules surveyed did not separately itemize the costs of revising user manuals and training (and thus are not included in Table 2), the Commission expects that the costs will be lower than the costs of developing policies and procedures.

The Commission understands, from Staff discussions with the Participants, that moving data to Glacier Deep Archive is a service provided by the cloud provider and, thus, costs are unaffected by the Proposal. In addition, the proposed amendments will not involve any costs of building security for the Glacier Deep Archive because the Plan Processor has already built such security measures.

As for ongoing implementation costs, the Proposal could result in ongoing costs related to an increase in help desk demands to assist regulatory staff requesting assistances in linking Options Market Maker quotes in Listed Options lifecycles, and restoration of Raw Unprocessed, Interim Operational Data and/or submission and feedback files older than 15 days.

d. Cost Transfers to Regulators

Regulators may undertake activities to mitigate the impact of the proposed amendments on regulatory activities and, as a result, incur costs. For regulatory activity that necessitates lifecycle information for Options Market Maker quotes in Listed Options, regulators could reduce the impact of the Proposal by revising lifecycle-producing code from the Plan Processor to apply it to their systems, maintaining such code over time, and processing data with that code.[227] The cost of applying and maintaining the code as well as processing data with the code is a cost transfer from the Company to regulators. The magnitude of this cost depends on the complexity of revising the code for regulators' systems, the frequency of updates required to maintain the code, and the chosen amount and frequency of data processed. In addition, regulators could incur staffing costs to mitigate the loss of data in DIVER and MIRS query tools [228] and to request restorations of Raw Unprocessed, Interim Operational Data and/or submission and feedback files older than 15 days. The costs incurred by regulators would reduce the cost savings of the proposed amendments. However, cost savings would still be meaningful after taking these transfers into consideration.

e. Interaction With Tick Size Adopting Release

One commenter stated that the rules and amendments proposed in the Tick Size Proposing Release [229] (the “Proposed Tick Size Rules”) had “the potential to significantly expand the amount of quoting activity in the . . . listed options markets,” [230] implying that the costs of linking Options Market Maker quotes in Listed Options would increase following the implementation of the Proposed Tick Size Rules. The commenter did not provide an explanation as to why they expected the Proposed Tick Size Rules would increase Options Market Maker quotes in Listed Options, and while the Commission has considered this potential interaction, it finds the connection is unclear. Regardless, the cost savings in the Proposal will still be meaningful as to all Options Market Maker quotes in Listed Options.

2. Regulatory efficiency

Regulatory efficiency refers to the efficiency of regulatory activities conducted by SROs and/or the Commission necessary to protect investors, maintain fair, orderly, and efficient markets, and facilitate capital formation.[231] In analyzing how the Proposal will impact regulatory efficiency, the Commission assessed how the Proposal will impact regulatory activities.

The Commission identified regulatory inefficiencies resulting from the Proposal. Most of these regulatory inefficiencies are transitional.[232] The other regulatory inefficiencies will be permanent in nature and will occur each time certain regulatory use cases arise.[233] The Commission concludes that the regulatory inefficiencies will have a limited overall impact.

a. Options Market Maker Quotes in Listed Options

The Participants state that the provision of the proposed amendments involving Options Market Maker quotes in Listed Options will have a “limited impact on the regulatory function of the CAT.” The Commission expects that this provision will delay potential regulatory activities involving lifecycle linkages for Options Market Maker quotes in Listed Options and reduce the ( printed page 103049) accessibility of Options Market Maker quotes in Listed Options.[234] The Commission expects the mitigation mechanisms— e.g., the provision of code from the Plan Processor and the use of the quoteID field—to partially alleviate the delays created by the Proposal.[235] The removal of Options Market Maker quotes from DIVER will result in certain regulatory inefficiencies; most of these inefficiencies, however, will dissipate in the long run.[236]

(i) Cessation of Processing of Options Market Maker Quotes by the Plan Processor

The loss of the linkage processing and derived fields specified in the Proposal could adversely affect investigations, examinations, or market analyses that rely on the lifecycle information in Options Market Maker data in CAT.[237] When the Plan Processor ceases lifecycle processing on Options Market Maker quotes in Listed Options, CAT Data will no longer include a CAT-Lifecycle-ID. The absence of CAT-Lifecycle-IDs for Options Market Maker quotes will delay any regulatory activities involving order linkages for Options Marker Maker quotes in Listed Options.[238] Lack of lifecycle linkages would also preclude derived fields such as Derived Next Event Timestamp (and Type Code) from being used by regulators to make regulatory activities, such as order book reconstructions, easier and faster.

To mitigate the impact of this provision, regulators will have the option of requesting from the Plan Processor the code underlying the current linkage processing for Options Market Maker quotes in Listed Options for the purpose of creating the lifecycles and derived fields themselves.[239] While such code could be helpful, it may also need to be modified by regulators to run on their own systems. Further, the Plan Processor will not update this code over time, and thus, regulators will need to maintain it themselves.[240] Also, the processing and maintenance of lifecycle linkages of Options Market Maker quotes in Listed Options will shift from a single entity (the Plan Processor) to multiple regulators. Such decentralization could result in duplicative efforts across regulators.

The Commission recognizes that potential delays depend on how complex the linkage processes are. A simpler linkage process will reduce the inefficiencies associated with decentralization and stale code. The Participants stated that “the vast majority of options market maker quote lifecycles consist of just two events,” [241] and that “[e]xecutions that result from Options Market Maker quotes will identify the quoteId of the quote that resulted in an execution,” [242] which suggests that these quotes have simple lifecycle processing.

While the majority of lifecycles of Options Market Maker quotes in Listed Options, with or without trades, may contain only two events, a substantial number of lifecycles could be more complex.[243] The Proposal further states that a large portion of lifecycles of Options Market Maker quotes in Listed Options do not involve any execution or allocation.[244] However, regulatory activities that analyze lifecycles or reconstruct order books are not restricted to lifecycles that contain trades.

Similarly, while having a quoteID on all options events in the lifecycle of an Options Market Maker quote in Listed Options can simplify the process of linking events,[245] quote ID does not fully substitute for CAT-Lifecycle-ID in all instances. An analysis of the effectiveness of quoteID in linking trades to quotes, and linking lifecycles more generally, found that quoteID is approximately 95 percent as effective as CAT-Lifecycle-ID is.[246]

Resulting delays from the implementation of the Proposal will vary across the impacted regulatory activities. Certain analyses using high volumes of data ( e.g., the January 2021 volatility [247] ) are more likely to face a large number of disparate complexities in linkage processing, which could take more time to address. Also, in these cases, the aforementioned challenges in using quoteID and Plan Processor code could be significant if such regulatory activities are time-sensitive. The implementation of the Proposal likely will have a limited impact for regulatory activities that focus on small samples,[248] where the Plan Processor's code and quoteID may be sufficient to avoid meaningful delays associated with linkage complexities.

(ii) Loss of Options Market Maker Quotes in Listed Options in Tools Such as DIVER and MIRS

The provision of the proposed amendments involving the Options Market Maker quotes in Listed Options will also eliminate Options Market Maker quotes in Listed Options from DIVER. The Participants state that, “[t]he regulatory groups of each of the Participants have indicated that they are able to conduct their regulatory programs accessing Options Market Maker Quotations via BDSQL and/or Direct Read, and each group supports the proposed modification.” [249]

The loss of Options Market Maker quotes in Listed Options from DIVER may delay regulatory activities, at least ( printed page 103050) in the short-term. While use of DIVER does not require programming skills in remote data processing and/or knowledge of structured query programming language,[250] regulatory users seeking to access Options Market Maker quotes in Listed Options will now have to do so through BDSQL and Direct Read, which do require such specialized skills and are therefore less user-friendly.[251] This may create some inefficiencies in the short term for regulatory activities involving Option Market Maker quotes.[252] Over a longer term, however, some regulatory users may become more familiar with BDSQL and Direct Read. Further, regulators could also adjust by creating internal tools for to replicate the same targeted queries they would otherwise run on DIVER. Once the code has been written out, BDSQL would likely be less time-consuming compared to DIVER, which can offset the delays. However, this could result in another inefficiency should multiple SROs and the Commission create code to replicate the commonly-used functionality formerly centralized within DIVER.

b. Raw Unprocessed, Interim Operational Data and/or Submission and Feedback Files

Based on the potential future use of Raw Unprocessed, Interim Operational Data and/or submission and feedback files older than 15 days, as well as the Participants' statements on past use, the Commission expects the Proposal not to have a consequential negative impact on regulatory efficiency. Some future regulatory activities of SROs could depend on the use of the Raw Unprocessed, Interim Operational Data and/or submission and feedback files older than 15 days, and therefore may be affected by a delay in access to data. It could, for example, be used by SROs to investigate patterns of errors in CAT Data submissions by their members.[253] However, such regulatory activities are unlikely to be time-sensitive.

3. Market Efficiency

Market efficiency could be slightly negatively impacted by the Proposal with the impact coming from reductions in regulatory efficiency.[254] Since the impact of the Proposal on regulatory efficiency is limited, the impact on market efficiency will be minimal. There could also be minor improvements in market efficiency due to a reduction in CAT fees.[255]

D. Competition

The Participants believe that the Proposal will have a positive impact on competition.[256] The Commission expects that the Proposal is likely to result in slightly reduced CAT fees, which could dampen existing competitive advantages for some market participants relative to the baseline,[257] but this is unlikely to have a meaningful effect on competition.[258] To the extent that the Proposal results in a modest reduction in the deterrence effects of CAT and a potential increase in persistence of violative behaviors,[259] there could be a resulting small adverse effect on competition in the market for trading services.[260] None of these effects on competition, however, is likely to be meaningfully large.

E. Capital Formation

The Participants state that the Proposal will have a positive impact on capital formation.[261] While they do not explain the mechanism, they state that the savings under the proposed amendments will “inure to the benefit of all participants in the markets for NMS Securities and OTC Equity Securities, including Participants, Industry Members, and most importantly, the investors.” [262] The Commission does not expect that the cost savings will result in any meaningful positive impact on capital formation.[263] In addition, any adverse impact on capital formation resulting from the regulatory inefficiencies created by the proposed amendments will also be small.[264]

IV. Conclusion

For the reasons discussed, the Commission, pursuant to Section 11A of the Exchange Act,[265] and Rule 608(b)(2) [266] thereunder, is approving the proposed changes to the CAT NMS Plan, as those changes are set forth in the Proposal. Section 11A of the Exchange Act authorizes the Commission, by rule or order, to authorize or require the self-regulatory organizations to act jointly with respect to matters as to which they share authority under the Exchange Act in planning, developing, operating, or regulating a facility of the national market system.[267] Rule 608 of Regulation NMS authorizes two or more SROs, acting jointly, to file with the Commission proposed amendments to an effective NMS plan,[268] and further provides that the Commission shall approve an amendment to an effective NMS plan if it finds that the amendment is necessary or appropriate in the public interest, for the protection of investors and the maintenance of fair and orderly ( printed page 103051) markets, to remove impediments to, and perfect the mechanisms of, a national market system, or otherwise in furtherance of the purposes of the Exchange Act.[269]

For the reasons set forth above, the Commission finds that the proposed changes to the CAT NMS Plan, as set forth in the Proposal, meet the required standard.

It is therefore ordered, pursuant to Section 11A of the Exchange Act,[270] and Rule 608(b)(2) [271] thereunder, that such changes be, and hereby are, approved.

December 12, 2024. ( printed page 103042) ( printed page 103044)

| Jan-24 | Feb-24 | Mar-24 | |

|---|---|---|---|

| Panel A (numbers in billions) | |||

| All events in CAT (1) [= (2) + (9)] | 8,164 | 7,811 | 7,892 |

| All options-related events in CAT (2) [= (3) + (8)] | 7,166 | 6,905 | 7,039 |

| All options exchange events (3) [= (4) + (7)] | 6,817 | 6,530 | 6,655 |

| OMM a quotes in Listed Options (4) [= (5) + (6)] | 6,528 | 6,225 | 6,340 |

| Options quote (OQ) events (5) | 5,287 | 4,884 | 4,896 |

| Options quote cancel (OQC) events (6) | 1,241 | 1,341 | 1,444 |

| Other options exchange events (7) | 289 | 305 | 315 |

| Industry member options-related events (8) | 349 | 376 | 384 |

| All equities events in CAT (9) | 998 | 906 | 853 |

| Panel B (%) | |||