Securities and Exchange Commission

- 17 CFR Parts 229, 230, 239, 240, and 249

- [Release Nos. 33-11391; 34-104102; File No. S7-2025-04]

- RIN 3235-AN52

AGENCY:

Securities and Exchange Commission.

ACTION:

Concept release; request for comments.

SUMMARY:

The Securities and Exchange Commission (“Commission”) is publishing this concept release to solicit comments on whether to amend the asset-level disclosure requirements for residential mortgage-backed securities in Item 1125 of Regulation AB and whether to revise generally the definition of “asset-backed security” and/or other definitions in Item 1101 of Regulation AB. The Commission is considering these steps to expand issuer and investor access to the registered asset-backed securities markets and facilitate enhanced capital formation and liquidity while maintaining appropriate investor protections.

DATES:

Comments should be received on or before December 1, 2025.

ADDRESSES:

Comments may be submitted by any of the following methods:

Electronic Comments

- Use the Commission's internet comment form (https://www.sec.gov/comments/s7-2025-04/s7-2025-04); or

- Send an email torule-comments@sec.gov. Please include File Number S7-2025-04 on the subject line.

Paper Comments

- Send paper comments to Vanessa A. Countryman, Secretary, Securities and Exchange Commission, 100 F Street NE, Washington, DC 20549-1090.

All submissions should refer to File Number S7-2025-04. This file number should be included on the subject line if email is used. To help the Commission process and review your comments more efficiently, please use only one method of submission. The Commission will post all comments on the Commission's website ( https://www.sec.gov/comments/s7-2025-04/s7-2025-04). Do not include personally identifiable information in submissions; you should submit only information that you wish to make available publicly. The Commission may redact in part or withhold entirely from publication submitted material that is obscene or subject to copyright protection.

FOR FURTHER INFORMATION CONTACT:

Arthur Sandel, Special Counsel, or Kayla Roberts, Acting Chief, in the Office of Structured Finance, Division of Corporation Finance, at (202) 551-3850, Securities and Exchange Commission, 100 F Street NE, Washington, DC 20549.

Table of Contents

I. Introduction

II. Asset-Level Disclosures for Residential Mortgage-Backed Securities

A. Background

B. Recent Developments

C. Potential Changes to RMBS Asset-Level Disclosure Requirements

D. Request for Comment

III. Disclosure of Certain Sensitive RMBS Asset-Level Data

A. Background

B. Potential Regulatory Response

C. Request for Comment

IV. Definition of Asset-Backed Security Generally

A. Background

B. Potential Changes to Regulation AB Definitions ( printed page 47255)

C. Request for Comment

V. General Request for Comment

VI. Regulatory Planning and Review

VII. Conclusion

I. Introduction

Securitization serves a vital role in the U.S. capital markets and the U.S. economy. As a method of financing in which financial assets are pooled and converted into instruments that may be offered and sold in the capital markets, securitization helps provide entities, such as banks, operating companies, and other non-depository financial institutions, with access to lower-cost capital to make loans to borrowers or otherwise finance operations.[1] This process, in turn, promotes necessary market liquidity and facilitates capital formation in critical economic sectors, such as housing and consumer lending. For investors, asset-backed securities (“ABS”) may offer attractive yields and an opportunity to diversify fixed-income portfolios with a range of credit quality. A more liquid registered ABS market should further increase opportunities for capital formation while also reducing borrowing costs for assets routinely financed by U.S. households, corporations, and small businesses, such as automobiles and residential and commercial real estate.

From its origins in the earliest mortgage-backed securities transactions of the 1970s, the modern ABS market gained traction in the 1980s and 1990s and, since then, the Commission has adopted a series of disclosure rules and forms to establish comprehensive registration and ongoing reporting requirements. In 2004, the Commission adopted Regulation AB,[2] establishing for the first time a comprehensive registration, disclosure, and ongoing reporting regime for ABS under the Securities Act of 1933 [3] (the “Securities Act”) and the Securities Exchange Act of 1934 [4] (the “Exchange Act”).[5] As we discuss in more detail in section IV.A below, the availability of this tailored regime was intentionally limited only to the types of securitizations that meet the definition of ABS in Item 1101(c) of Regulation AB.[6]

Following the financial crisis of 2007-2009 (the “Financial Crisis”), Congress enacted the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”).[7] The Dodd-Frank Act added a new statutory definition of “asset-backed security” [8] and included mandates for the Commission to adopt rules and regulations intended to address concerns in the securitization market including, in relevant part, a lack of transparency about the assets underlying ABS.[9] In 2014, the Commission adopted significant revisions to its registration, disclosure, and reporting regime for ABS, including amendments to Regulation AB (colloquially, “Regulation AB II”), in part to implement several of these Dodd-Frank Act mandates.[10] As discussed in sections II and III below, one such amendment adopted by the Commission in Regulation AB II was the new requirement that ABS issuers disclose asset-level data for all assets underlying registered residential mortgage-backed securities (“RMBS”) and certain other asset classes.[11]

In developing these specialized registration and reporting requirements, the Commission and its staff have regularly engaged with securitization market participants to identify areas for regulatory enhancements or modifications to address the changing needs of the market while supporting capital formation and investor protection. Market trends and developments since the adoption of Regulation AB II (such as new and expanding asset classes) have prompted us to assess whether the current framework for registration and reporting is serving the needs of the current ABS market.[12] Because, as discussed in more detail in section II.A below, a robust registered ABS market offers benefits such as increased transparency and protections, greater liquidity, and potentially lower costs of capital, this assessment includes consideration of whether there are any regulatory impediments to issuer and investor access to the registered ABS market.

As part of this assessment, the Commission is considering and seeks public input on whether certain modifications may be warranted with respect to the current asset-level disclosure requirements for RMBS under Item 1125 of Regulation AB, including whether and how to address potential disclosure of certain sensitive RMBS asset-level data. In sections II and III, we review the background of the existing asset-level disclosure requirements and discuss certain challenges reported by RMBS market participants, including some of their recent efforts to identify potential solutions to these challenges. Related to these considerations, we also discuss certain RMBS asset-level data points that raise privacy and confidentiality concerns for consumers and request feedback regarding whether we should reconsider our current approach to address such concerns. We set forth our objectives to reduce costs and regulatory obstacles to registration of RMBS offerings with the goal of facilitating public offerings of RMBS and increasing liquidity in the registered RMBS market. We seek input on potential solutions that balance the interests of all RMBS market participants, including investors.

The Commission is also considering whether to revise generally the definition of “asset-backed security” in Item 1101(c) of Regulation AB and/or certain other definitions in Regulation AB.[13] In section IV, we review the background of the asset-backed securities definition and discuss certain challenges that may be impacting the registered ABS market. We seek public input regarding potential changes that ( printed page 47256) may facilitate expanded access to the registered ABS market.[14]

While we ask a number of general and specific questions throughout this release regarding each of these topics, we also welcome comments on any other aspects of the ABS registration and reporting regime. Interested persons are also invited to comment on whether certain specific approaches, alternative approaches, or a combination of approaches would address the items identified in this release.

II. Asset-Level Disclosures for Residential Mortgage-Backed Securities

A. Background

As discussed in section I above, in 2014, the Commission adopted significant amendments to Regulation AB and other rules governing the public offering, disclosure, and reporting regime for ABS.[15] Among the revisions, the Commission adopted Item 1125 of Regulation AB and the Appendix to Item 1125 (“Schedule AL”) [16] to implement the mandate in Securities Act section 7(c).[17] Schedule AL requires standardized asset-level disclosures for registered ABS where the underlying assets consist of residential mortgages, commercial mortgages, auto loans, auto leases, debt securities, or resecuritizations of ABS that include these asset types.[18] The Commission determined that the asset-level information required by Schedule AL would provide investors with access to more robust and standardized information necessary for investors to independently perform due diligence.[19] While the specific data requirements vary by asset class, Schedule AL generally requires information about the credit quality of obligors, the collateral related to each asset, and the performance of those assets. The information must be provided in a tagged data format using eXtensible Markup Language (“XML”) and must be filed at the time of the offering of the ABS and in ongoing reports filed with the Commission.[20]

With respect to RMBS, Item 1 of Schedule AL requires disclosure of up to 270 data points for each underlying mortgage.[21] Of these 270 RMBS data points, 165 are required to be provided only upon the occurrence of specific events or when certain specified conditions exist.[22] For example, if an underlying mortgage is a fixed-rate mortgage, the data points related to adjustable-rate mortgages need not be included in the Schedule AL data file with respect to such fixed-rate mortgage.[23]

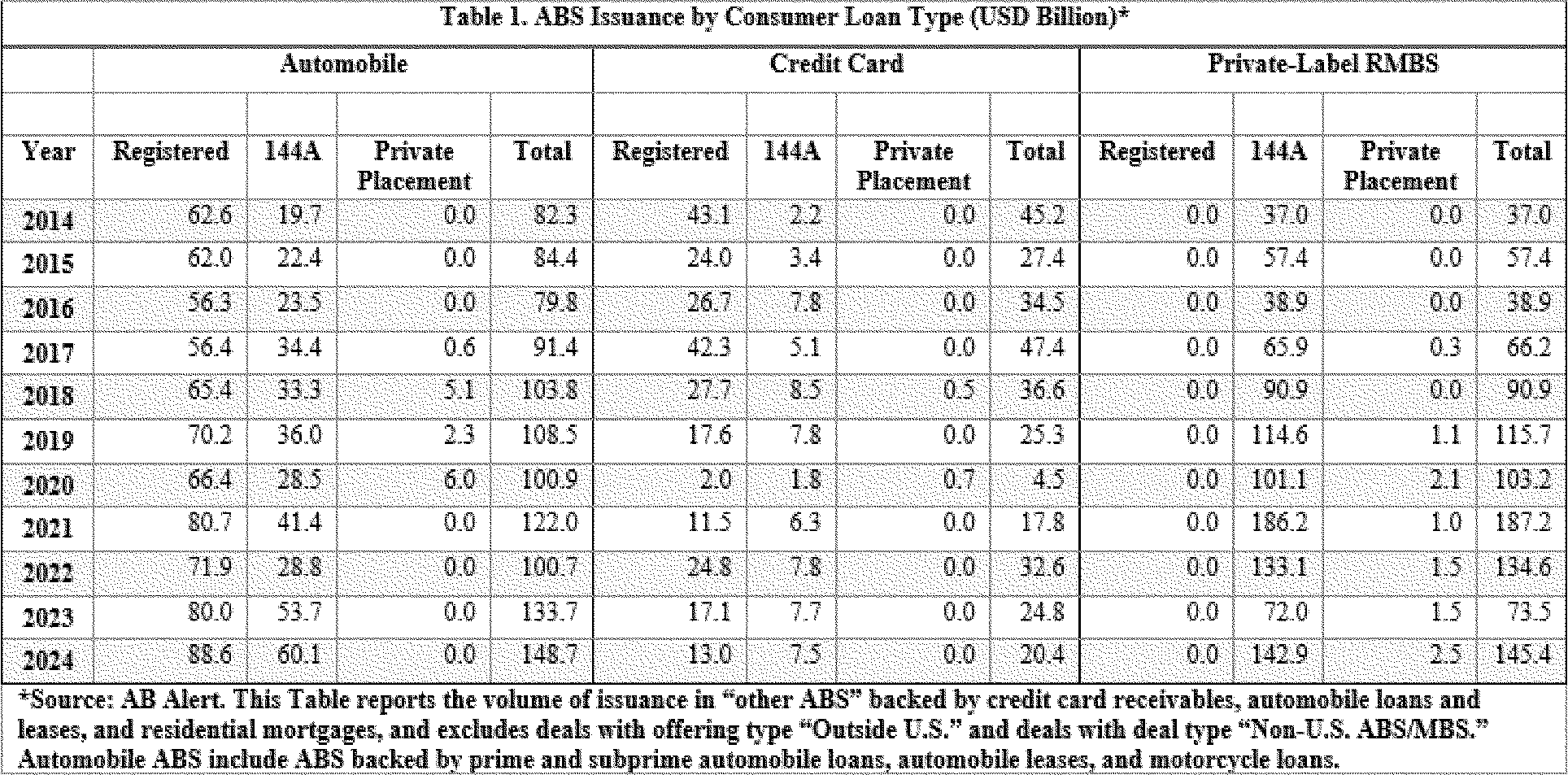

In determining which RMBS data points to adopt, the Commission considered various industry and regulatory standards developed for collection and/or presentation of asset-level data about residential mortgages, as well as suggestions from commenters.[24] Though there were many efforts by market participants to identify responses to the issues arising from the lack of transparency that was brought to light by the Financial Crisis and re-establish confidence in the market, only one issuer has publicly issued private-label RMBS ( i.e., RMBS not issued by the Agencies) since 2009,[25] and there have been no registered private-label RMBS offerings since June 2013 (pre-dating the adoption of Regulation AB II by more than a year).[26] Rather, RMBS securitizations have been concentrated in the Agencies,[27] which are exempt from the Commission's registration and reporting requirements under the Securities Act and the Exchange Act.[28] All private-label RMBS offerings since June 2013 have been unregistered, with nearly all occurring in the Rule 144A market,[29] despite investment criteria restrictions that limit the amount of Rule 144A ABS that many institutional investors can hold.[30] By contrast, as shown in Table 1, below, there has been an active registered market for ABS ( printed page 47257) backed by other consumer lending assets, such as automobile loans and leases and credit card receivables, over the same period of time.

Market participants often cite the RMBS asset-level disclosure requirements as a key barrier to the return of private-label RMBS issuance to the registered market.[31] Nevertheless, many market participants, including investors,[32] have expressed a desire to re-enter the registered RMBS market due to the benefits it provides, including increased liquidity and greater transparency of registered offerings and publicly available disclosure.[33] Others have emphasized the benefits of increased financing to housing markets from the broader investor base available to invest in registered RMBS offerings versus Rule 144A RMBS offerings.[34]

B. Recent Developments

In September 2019, the Treasury Department published a housing reform plan recommending that the Commission review its RMBS asset-level requirements in Schedule AL.[35] The report raised concerns that the Commission's regulations prescribing asset-level disclosures for registered RMBS might unduly restrict registered private-label RMBS issuances and contribute to a “heightened . . . competitive advantage” for the Agencies.[36] The report concluded, in part, that “[i]t is difficult to collect the required data for some of these fields—with the expense and burden of collection potentially outweighing the benefit to [private-label RMBS] investors, particularly for seasoned mortgage loans and some of the [data points] are ambiguous.” [37] The Treasury Department recommended that the Commission review the RMBS asset-level disclosure requirements to assess the number of required reporting fields and to clarify any ambiguous fields for registered private-label RMBS issuances.[38]

In October 2019, then-Chairman Jay Clayton released a statement seeking public input on the issues related to RMBS asset-level requirements.[39] As with the Treasury's housing reform ( printed page 47258) plan, the Chairman's statement highlighted the absence of registered RMBS offerings since the adoption of Regulation AB II and the dominance of the Agencies in the overall RMBS market.[40] The Chairman's statement acknowledged that there were likely a number of factors contributing to the absence of registered private-label RMBS offerings and sought public input on these various factors, including whether the RMBS asset-level disclosure requirements were a significant contributing factor.[41] Public input was limited, with only a handful of commenters responding to the Chairman's statement.[42]

One comment letter submitted by a group of four industry organizations recommended the removal of certain specific RMBS asset-level data points from Schedule AL, and the addition of other data points, to align with the asset-level disclosures used in the Rule 144A RMBS market.[43] For example, these industry organizations suggested that, to bring the Schedule AL requirements more in line with disclosures generally provided in the Rule 144A RMBS market, the Commission should remove certain information related to servicer advances (Item 1(g)(31) of Schedule AL), loans in foreclosure (Item 1(r) of Schedule AL), “real estate owned” properties (Item 1(s) of Schedule AL), information related to losses (Item 1(t) of Schedule AL), and mortgage insurance claims (Item 1(u) of Schedule AL), among several others. The industry organizations suggested various reasons for removal of specific data points, including that the information is not typically obtained or is not obtainable, the information is not verifiable, or that the information is not material. They also recommended the addition of several data points that are used in Rule 144A RMBS issuances, including detailed information related to borrower credit scores, borrower income and employment information, geographical information related to the property, property valuation information, and certain information related to the modification of the terms of a mortgage. Schedule AL currently requires much of this information,[44] but to varying degrees and levels of granularity, at least in part due to privacy and confidentiality concerns, which we discuss in section III below. Commission staff has continued to engage with industry participants to identify potential barriers to registration of RMBS offerings, as well as ways to reduce or remove those barriers, and continue to hear concerns with certain RMBS asset-level data points.[45]

C. Potential Changes to RMBS Asset-Level Disclosure Requirements

In an effort to enhance the Commission's registration, disclosure, and reporting framework for RMBS, we are soliciting public comment on whether and how any potential revisions to the RMBS asset-level disclosure requirements in Item 1 of Schedule AL could facilitate increased capital formation through registered RMBS issuances, while providing investors with information necessary to their investment decisions. In the case of RMBS, there are several factors that may be contributing to the absence of registered offerings, including the dominance of the Agencies, which may be attributed to deep market liquidity, beliefs among some market participants regarding the availability of U.S. Government guarantees, more favorable underwriting standards compared to private-label RMBS, and attractive yields and returns for investors.[46] Nevertheless, it is important to consider whether the Commission's rules may be contributing to this absence.

Securitization market conditions have changed considerably since both the Financial Crisis and the Commission's adoption of Schedule AL, including improved investor confidence in securitization markets due to increased transparency and other regulatory guardrails established in response to the crisis.[47] Despite these developments, the issuance of registered RMBS has yet to return. In light of these observations—and based on the staff's ongoing engagement with market participants to understand the circumstances contributing to this lack of public issuance—we are considering whether the required disclosure of certain RMBS data points under Schedule AL contributes to the ongoing absence of registered RMBS transactions.

The RMBS market plays a substantial role in enhancing liquidity in the residential mortgage market and reduces the cost associated with access to capital, benefitting the U.S. housing sector.[48] As some RMBS market ( printed page 47259) participants have noted, a diverse array of securitization options ( i.e., Agency RMBS, Rule 144A private-label RMBS, and registered private-label RMBS) is important for a healthy mortgage market because it provides access to a wider range of issuers and investors, reducing reliance on any one source of liquidity and contributing to lower consumer costs.[49] For these reasons, we seek to identify and address potential barriers that issuers may face when they seek to engage in registered RMBS offerings and to explore any accommodations that could facilitate public offerings of RMBS in a manner that is consistent with the Commission's statutory mandate and maintains investor protection.

As such, we are requesting input as to whether a reconsideration of the RMBS asset-level disclosure requirements is warranted to assess whether certain data points continue to be necessary for independent investor due diligence under current market conditions. We are also soliciting public comment about ways to enhance and revise the asset-level disclosure requirements of Schedule AL to reduce or remove any potential barriers to registration of RMBS offerings. In considering potential revisions to our rules, it would be helpful to understand which data points are possible to obtain, even if not typically or easily obtained, versus which data points are impossible to obtain, and the separate reasons for each.[50] As we consider potential approaches, it will be helpful to have a better understanding regarding the level of difficulty for disclosure of various data points and the related reasons and impacts. Likewise, it will be helpful to understand what asset-level data is necessary for the investor to independently perform due diligence on RMBS, consistent with the mandate in Securities Act section 7(c). In each case, a clear and demonstrable rationale for a suggested approach would allow us to evaluate more effective and tailored solutions. We welcome and encourage market participants and other interested persons to submit their views on potential regulatory changes discussed above or on any alternative that they deem appropriate.

D. Request for Comment

1. To what extent, if at all, are the Commission's asset-level disclosure requirements adopted in 2014 contributing to the lack of registered RMBS issuances? What are the costs and other related burdens associated with providing asset-level disclosures for registered RMBS offerings?

2. To what extent have other factors contributed to the absence of registered RMBS offerings? Which are the most salient factors? To what extent, if at all, has the Rule 144A market also contributed to the lack of registered RMBS issuances and if so, why?

3. Are there differences in transaction costs for registered RMBS relative to Rule 144A RMBS offerings? For example, are there differences in costs associated with reporting frequency, making filings on EDGAR, or costs related to the administration of the deals, such as those related to transaction parties? Is there quantitative data available underlying such cost comparisons? Are there any parallels to other quantitative data sets?

4. Are there any RMBS data points in Schedule AL for which the Commission's rationale articulated in the 2014 Regulation AB II Adopting Release is no longer relevant in today's market?

5. Should the RMBS asset-level disclosure requirements in Schedule AL be conformed to the practices of private-label RMBS issuers offering securities in the Rule 144A market?

6. Should any RMBS data points in Schedule AL be revised? Should any data points be removed? If so, which specific data points should be revised or removed and why? Should any RMBS data points not in Schedule AL be added? If so, which specific data points should be added and why?

7. Are there any RMBS data points in Schedule AL that are not necessary or are overly burdensome to obtain? If so, could any such data points be revised or should they be removed from Schedule AL? Are such data points overly burdensome to obtain for newly issued mortgages, or only for legacy mortgages, and if the latter, of what vintage? Which data points are possible to obtain, even if not typically or easily obtained, versus which data points are impossible to obtain and why? Please specify the data points and provide a detailed explanation of the reasons why they should be revised or removed.

8. Are there any definitions in Schedule AL regarding specific RMBS data points that are ambiguous or confusing? Why or why not? If so, how can such definitions be revised to provide clarity? Is there interpretive guidance that the Commission could provide to help clarify any data points?

9. Should we consider alternative reporting frequencies for ongoing disclosures and/or allowing summary reporting for certain credit events required to be disclosed by Schedule AL? Why or why not?

10. Should the Schedule AL data points be rearranged or modified in such a way that would more clearly delineate when and under what circumstances each data point is required to be provided ( i.e., at offering and/or at the time of filing each Form 10-D)? If so, what clarifying changes to the structure of Schedule AL or the definitions of specific data points would be helpful in this regard?

11. Should the response codes for specific RMBS data points in Schedule AL be revised? If so, which ones and why? Should we consider providing greater use of response codes such as “not applicable,” “not available,” “not obtainable,” or “unknown”? Should we require additional explanatory information regarding such responses and, if so, where?

12. Should we consider a “provide-or-explain” regime? [51] Under a provide-or-explain regime, an issuer may omit any asset-level data point, provided the issuer identifies the omitted field and explains why the data was not disclosed.

- If so, what limits should we place on a provide-or-explain regime? What impact could a provide-or-explain regime have on investor protection, market transparency, and investors' ability to analyze data using models or other technologies?

13. What impacts would there be on standardization of RMBS asset-level data if we were to allow a provide-or-explain regime? How could a provide-or-explain disclosure regime be structured so as to be consistent with ( printed page 47260) Securities Act section 7(c)? Please explain.

14. What asset-level data is necessary for investors to independently perform due diligence on RMBS offerings, consistent with the mandate in Securities Act section 7(c)? Are there data points in current Schedule AL upon which investors do not rely? Would the elimination of any of the RMBS data points in Schedule AL be reasonably expected to adversely affect investors' ability to analyze the quality and performance of the underlying assets? If so, which specific data points should not be eliminated and why?

15. Are there any RMBS data points in Schedule AL that are duplicative? If so, identify the data points and explain why. Would it be beneficial to issuers and investors to remove duplicative data points?

16. Some RMBS data points request the results of calculations, such as debt-to-income ratios. Can these ratios otherwise be calculated from data provided in other asset-level data points? Are these calculations overly burdensome to perform? Should we permit these data points to be excluded from the asset-level data file?

III. Disclosure of Certain Sensitive RMBS Asset-Level Data

A. Background

Throughout the Regulation AB II proposal process, the Commission was sensitive to the possibility that certain asset-level disclosures may raise concerns about an underlying obligor's personal privacy.[52] In particular, the Commission noted that asset-level data points requiring disclosures about the geographic location of the collateralized property and obligors' credit scores, income, and debt may raise privacy concerns.[53] The Commission also recognized, however, that information about obligors' credit scores, employment status, and income would permit investors to perform better risk and return analysis of the underlying assets and, therefore, of the ABS.[54] In an effort to balance individual privacy concerns with the needs of investors to have access to detailed financial information about the obligors, the Commission proposed a series of data points that required information presented in ranges and coded responses rather than specific values. One such example of this effort is the approach taken with respect to the data point requiring disclosure of the geographic location of the property.[55]

The Commission originally proposed that a property's location be provided by Metropolitan Statistical Area, Micropolitan Statistical Area, or Metropolitan Division (collectively, “MSA”) [56] in lieu of the narrower geographic delineation of zip codes.[57] Commenters' responses to this proposal were mixed, with some noting that such an approach would greatly reduce transparency [58] and one stating its belief that limiting geographic information to MSA could result in lower pricing for new RMBS offerings, potentially resulting in higher costs for consumers of residential mortgage loans.[59] According to these commenters, zip codes were preferable as they could provide further information for a property, including, for instance, whether a property is in a flood plain or earthquake zone.[60] Other commenters highlighted the potential privacy risks posed by zip codes, including that they can be used with other public databases to match a property with a specific borrower.[61]

In February 2014, the Division of Corporation Finance issued a staff memorandum detailing how disclosure of certain asset-level data requirements combined with other publicly available sources of consumer information would allow the identity of the obligors in ABS pools to be uncovered or re-identified and the potential implications of such an outcome.[62] The 2014 Staff Memorandum also presented a potential approach of making certain asset-level data available to investors and potential investors through an issuer-sponsored website, rather than on EDGAR.[63] The 2014 Staff Memorandum suggested that such a website would allow issuers the flexibility to determine the procedures and controls best suited to protecting asset-level data while allowing investor access to the data necessary for any investment decisions. Also in February 2014, the Commission re-opened the comment period for the 2010 Regulation AB II Proposing Release and the 2011 Regulation AB II Re-Proposing Release to solicit public comment on the privacy considerations and website approach detailed in the 2014 Staff Memorandum.[64]

As detailed in the 2014 Regulation AB II Adopting Release, only a few commenters supported the use of such a website, citing concerns that it could increase the legal and reputational risks to issuers and may cause issuers to take on liability under any applicable privacy laws.[65] Other commenters noted ( printed page 47261) concerns that websites pose technological risks and that any issues could have negative market impacts.[66] The Commission went on to detail a series of options considered before finally adopting Item 1(d)(1) of Schedule AL, which requires disclosure of a two-digit zip code for the geographic location of individual properties underlying an RMBS offering to mitigate privacy and re-identification risk.[67] To provide guidance with respect to the FCRA implications of the proposed asset-level disclosure requirements, the Consumer Financial Protection Bureau (“CFPB”) issued a letter to the Commission explaining its view that, if the Commission made certain determinations related to the disclosure of the asset-level information at issue, which excluded direct identifiers, the Commission would not become a consumer reporting agency by requiring, obtaining, and disseminating such information and an issuer would not become a consumer reporting agency by disclosing such information to investors or filing it with the Commission pursuant to the Commission's regulatory requirement.[68]

In his 2019 statement regarding RMBS asset-level disclosure requirements, then-Chairman Clayton specifically requested feedback on issues related to five-digit zip code and other privacy concerns.[69] Chairman Clayton noted the Commission staff's understanding that issuers of unregistered RMBS provide five-digit zip codes to investors rather than the two-digit zip code required under Schedule AL and that issuers address privacy concerns by limiting the use and dissemination of zip codes, including via the use of end-user agreements. Chairman Clayton requested feedback regarding the impact of the zip codes on registered RMBS offerings, the role and value of zip codes in risk and return analysis related to RMBS offerings, and whether there were alternatives to zip codes that would accommodate privacy concerns while still meeting the needs of investors.[70]

In response to this request, one commenter noted that there should be alignment between the asset-level data disclosure provided in registered and unregistered RMBS offerings, but that, in the meantime, issuers of registered RMBS offerings should provide the five-digit zip code to investors of record, with the EDGAR filing displaying only three-digit zip codes.[71] Another commenter stated that filing data on EDGAR should be limited to three-digit zip codes, with processes in place to allow public disclosure of a zip code to be further limited.[72] This commenter proposed an approach already used for Rule 144A RMBS issuances: a “click-through” agreement through which investors can access asset-level data ( e.g., through a permissioned website) after providing representations regarding the use and redistribution of such data.

The Securities Industry and Financial Markets Association (“SIFMA”) has made available a model click-through agreement.[73] The agreement places several limitations on users, including on the use of the data, disclosure of the data, and communications with any obligors. The agreement also requires users to represent that, where they do disclose the data, those with access to the data are informed that it is confidential and that they are subject to confidentiality and security obligations. Users must further represent that they will treat the information as personally identifiable under all applicable laws and that, commensurate with the type of user and relative to the nature and scope of their activities, they have reasonable safeguards to protect the confidentiality of the asset-level data.[74]

B. Potential Regulatory Response

As discussed in section II above, we are considering possible approaches to facilitate issuer participation in registered RMBS offerings, including a reconsideration of the issuer-sponsored websites discussed above. We understand there is a difference between the information investors receive in unregistered transactions, such as those conducted pursuant to Rule 144A, and disclosures required in a public offering through registered transactions. From staff discussions with RMBS market participants, we are aware that there are certain data point categories provided in Rule 144A RMBS transactions that, if included in registered RMBS transactions, would pose privacy concerns, including property address and other geographical property information, borrower credit scores, property valuation, and underwriting details. We also acknowledge that asset-level information is important to an investor's analysis in making investment decisions about the RMBS transaction. As such, providing that information to investors and promoting capital formation may involve considering potential alternative approaches, such as the use of a website separate from EDGAR, managed or sponsored by the issuer, consistent with current practices for unregistered private-label RMBS issuances.

At the time Regulation AB II was proposed, commenters generally opposed the use of a website for storing asset-level data, leading to its exclusion from the final rule.[75] However, commenters responding to the 2019 Chairman's Statement indicated that the use of a website would be more consistent with the approach currently utilized for unregistered RMBS issuances.[76]

Given the passage of time and evolution of industry practice, we are interested in market participants' views on whether an issuer-sponsored website as summarized in the Regulation AB II Adopting Release and the 2014 Staff Memorandum may be an alternative worth considering. Such a website could allow issuers to manage access to, ( printed page 47262) and protection of, asset-level data for investors. This could be done by leveraging existing technology and procedures that are currently used for unregistered RMBS issuances, which would also help provide consistency with current industry practices and legal requirements. We recognize that the concerns raised during the proposal of Regulation AB II may persist but, given that such websites are currently in use for unregistered RMBS issuances, this approach may provide a potential solution to balance the market concerns with respect to both individual privacy and consistency in investor access to certain information between registered and unregistered markets, and therefore we seek public comment on its regulatory viability. We also seek public input on any other potential approaches that could address privacy and confidentiality concerns related to the disclosure of certain sensitive asset-level information.

C. Request for Comment

17. Are issuers forgoing registered RMBS offerings because they cannot provide investors with sensitive asset-level information, such as five-digit zip code, due to privacy and re-identification concerns? If so, please identify the asset-level requirements that contain such sensitive information and that are causing or contributing factors in issuers' decisions to forgo registered RMBS offerings.

18. What methods of disclosing zip codes, obligor credit scores, and other sensitive asset-level data would best balance providing investors with sufficiently granular geographical and obligor financial information while also addressing privacy concerns?

19. Should we consider adding data points used in Rule 144A private-label RMBS transactions that may include sensitive information to Schedule AL? If so, which data points should be added and what steps should be taken to address privacy or confidentiality concerns?

- If any of the sensitive information is not currently considered by market participants to be necessary for investors to independently perform due diligence, please elaborate as to why such information is provided to investors in connection with a Rule 144A private-label RMBS issuance.

20. Are the legal and reputational concerns under privacy laws that were identified in connection with the adoption of Regulation AB II still relevant? How have Rule 144A private-label RMBS issuers mitigated those concerns? Have there been breaches in data and privacy protections resulting in harm to obligors? To what extent and how frequently do issuers update their data and privacy protections in response to emerging cybersecurity threats and breaches?

21. Are there other legal or reputational concerns, such as with respect to Regulation FD or other Federal or State securities laws, that RMBS issuers would have if we permit disclosures of certain information via an issuer-sponsored website (or other alternative method) rather than being publicly disseminated via filings on EDGAR? Would Commission rules or guidance establishing what information may or must be disclosed in this manner mitigate any of those concerns?

22. Please describe the websites currently used to provide RMBS asset-level data to investors and potential investors. How is access managed? Is access limited only to potential investors, investors, and the issuer? How is access managed to reflect secondary market transactions? For instance, how is it updated to reflect when investors may no longer hold an applicable investment? What are the challenges issuers have faced in maintaining these websites?

23. Do the websites continue to use click-through agreements consistent with the model click-through agreement provided by SIFMA? Have there been important changes to usage rights, representations, or limitations?

24. Do RMBS issuers maintain websites specific to their own issuances, or are there any third-party websites, whether affiliated or unaffiliated with the RMBS issuers, currently in use that allow investors to access data across issuances? If such websites have been utilized or considered, what challenges do they pose? How have those challenges been addressed? To what extent do liability concerns impact issuers' use of issuer-maintained websites or third-party websites, respectively?

- Do RMBS issuers delegate the responsibility and obligations to establish, maintain, and manage access to such websites to other transaction parties such as the sponsor, servicer, trustee, or custodian (whether affiliated or unaffiliated with the RMBS issuers)? Why or why not? To what extent do liability concerns impact issuers' decisions to delegate these obligations? Is there a standard market practice with respect to the security provided when issuers delegate their obligations to other transaction parties? If so, what are the standard liability provisions under these arrangements in the event of a data breach?

25. Should we permit RMBS issuers to use issuer-sponsored websites in connection with registered RMBS offerings? If so, should we permit RMBS issuers to delegate the responsibility and obligations to establish, maintain, and manage access to such websites to other transaction parties such as the sponsor, servicer, trustee, or custodian (whether affiliated or unaffiliated with the RMBS issuers)? Why or why not?

26. Have investors in unregistered RMBS offerings expressed concerns with the amount of asset-level data typically provided on the website? Have investors expressed concerns with the approach taken in providing the data, or on the attendant access restrictions?

27. Should we require the RMBS issuer to undertake in the offering materials and transaction documents that it will identify and make available the sensitive asset-level information provided on the website? Should we consider requiring that RMBS issuers make certain representations in their filings on EDGAR related to the disclosure of sensitive information?

28. If we require undertakings, representations, and/or certifications by the RMBS issuer as to the sensitive asset-level data provided on its website, what should those obligations include? Should the Commission provide standard language for such undertakings, representations, and/or certifications?

- For example, should we require undertakings, representations, and/or certifications that a website will be/has been established, that a website will continue to be maintained for the life of the deal, and that access to such website has been granted to all prospective/purchasing/current investors (and will continue to be granted) subject to certain specified conditions? Why or why not? Are there other representations and/or certifications that we should consider? If so, please specify.

- Should RMBS issuers be required to represent that such information will be provided to any investor or prospective investor upon request, similar to the standard used in Rule 144A? Would it be appropriate to require that the sensitive RMBS asset-level information that is disclosed outside of EDGAR be incorporated by reference into the issuer's disclosures that are publicly filed on EDGAR?

- When and how frequently should any such undertakings, representations, and/or certifications be required? For example, should they be required with the offering materials (either at the time that the preliminary prospectus is required to be filed pursuant to ( printed page 47263) Securities Act Rule 424(h) [77] or at the time that the final prospectus is required to be filed pursuant to Securities Act Rule 424(b) [78] ), with each distribution report filed on Form 10-D,[79] and/or with the annual report filed on Form 10-K? Please specify why your recommendation as to timing and frequency would be appropriate.

29. Have there been recent technological or other advances in the production and analysis of property data that have lessened reliance on the RMBS asset-level data that has previously raised privacy concerns, including zip codes?

30. When investors in, or assets of, a given unregistered RMBS issuance are located outside the United States, what is the general approach for addressing any cross-border privacy considerations? For instance, when a property and/or obligor may be situated outside the United States and foreign privacy laws constrain the dissemination of asset-level information beyond what is contemplated by U.S. privacy laws, what sorts of restrictions are put in place?

31. Are there alternative approaches to providing RMBS investors with access to sensitive asset-level information that would minimize the re-identification risks discussed above? Please describe the alternative(s) and explain why it would be preferable to the issuer-sponsored website approach discussed in this release.

IV. Definition of Asset-Backed Security Generally

A. Background

When the Commission adopted Regulation AB in 2004, it defined “asset-backed security” to demarcate the securities and offerings to which the rules would apply for purposes of registration, disclosure, and reporting under the Securities Act and the Exchange Act.[80] Specifically, Item 1101(c) of Regulation AB (the “Regulation AB ABS Definition”) defines “asset-backed security” as a “security that is primarily serviced by the cash flows of a discrete pool of receivables or other financial assets, either fixed or revolving, that by their terms convert into cash within a finite time period, plus any rights or other assets designed to assure the servicing or timely distributions of proceeds to the security holders. . .” with certain conditions and limitations added with respect to lease assets, transaction parties, non-performance, delinquencies, master trusts, and revolving asset pools.[81]

The origins of the Regulation AB ABS Definition can be traced back to 1992, when the Commission amended Form S-3 [82] to permit shelf registration of offers and sales of ABS.[83] At that time, the Commission envisioned a broad definition, stating that “[a] broad standard has been adopted in order to provide sufficient flexibility and to accommodate future developments in the asset-backed marketplace.” [84] The definition, however, was used only for purposes of Form S-3 eligibility. When the Commission later adopted the Regulation AB ABS Definition, it noted that moving the definition from the registration form to Regulation AB meant that any security meeting the general definition would be eligible for the new disclosure and reporting regime, regardless of the form used for registration.[85] The Commission made clear, however, that the substance of the definition itself would remain largely unchanged,[86] stating that it “continue[d] to believe the ABS regulatory regime [being adopted] should be appropriately limited to a definable group of asset-backed securities.” [87] For example, the Commission's emphasis on discrete pools meant excluding managed pool structures, such as collateralized loan obligations (“CLOs”).[88] Similarly, the emphasis on the activities of the issuing entity being limited to owning and holding one asset pool and issuing securities backed by that pool meant excluding series trust structures, where a single issuing entity issues separate series of ABS backed by separate asset pools.[89] The Commission's concerns about payments not being based primarily on the performance of assets in an underlying pool in synthetic securitizations meant excluding these securitizations.[90] Recognizing that other structures and securities may develop in the future, the Commission explained that the Regulation AB ABS Definition was not designed to limit the public offering of securities that fell outside its parameters; [91] rather, ABS that fall outside the parameters of Regulation AB, such as ABS structured as a series trust, do not qualify to rely on the registration and reporting regime created by Regulation AB.[92]

In 2010, section 941(a) of the Dodd-Frank Act [93] added a separate statutory definition of “asset-backed security” as section 3(a)(79) of the Exchange Act (the “Exchange Act ABS Definition”).[94] The Exchange Act ABS Definition defines “asset-backed security” as “a fixed-income or other security collateralized by any type of self-liquidating financial asset (including a loan, a lease, a mortgage, or a secured or unsecured receivable) that allows the holder of the security to receive payments that depend primarily on cash flow from the asset. . .” and explicitly includes managed pool structures, such as CLOs. While the two definitions share similarities ( i.e., that the securityholder receives payments that primarily depend on cash flows from self- ( printed page 47264) liquidating financial assets underlying the ABS), there are key differences—specifically, the inclusion of managed pool and series and master trust structures in the Exchange Act ABS Definition. Therefore, the Exchange Act ABS Definition is broader ( i.e., encompasses more types of ABS) than the Regulation AB ABS Definition, and any ABS that satisfy the Regulation AB ABS definition also meet the Exchange Act ABS Definition.

B. Potential Changes to Regulation AB Definitions

The Regulation AB ABS Definition was adopted prior to the enactment of the Dodd-Frank Act and, as noted above, was intended to identify ABS that satisfied certain core principles that the Commission determined should be met in order to be eligible for the specialized registration and reporting regime under Regulation AB.[95] The Exchange Act ABS Definition is used primarily in various Commission rules arising from the Dodd-Frank Act, such as the credit risk retention rule under Exchange Act section 15G,[96] which requires the securitizer of ABS to retain a portion of the credit risk associated with the underlying assets, and Securities Act Rule 192,[97] which was adopted by the Commission pursuant to Securities Act section 27B [98] and prohibits certain material conflicts of interest. As a result, the overall regulatory regime for ABS is governed by two different regulatory standards which serve distinct purposes. This dynamic has resulted in market participants needing to analyze the nuances of each definition to determine whether various ABS structures satisfy only the Exchange Act ABS Definition, both definitions, or neither definition, and what the ramifications might be.

As the ABS market continues to evolve in response to macroeconomic changes and market trends and innovations, ABS transactions have become more diverse and complex, both structurally and in the types of assets that are securitized. For example, since the Exchange Act ABS Definition was enacted in 2010 (and since the Regulation AB ABS Definition was adopted in 2004), we have observed the introduction of new asset classes, such as cell phone payment plan securitizations, as well as the proliferation of others, such as public utility securitizations.[99]

Public utility securitizations are a helpful example of both the impact of the differing definitions on the market and how the evolution of the ABS market over time indicates that a reconsideration of the current regulatory framework may be warranted.[100] These transactions are generally structured in one of two ways: using a stand-alone trust for each issuance of ABS; or using a single series trust that issues multiple series of ABS, each of which is backed by a separate pool of assets, from the same trust. In 2004, the Commission intentionally chose to exclude series trust ABS from the specialized regulatory regime in Regulation AB.[101] Today, this exclusion means that public utility securitizations could be subject to different registration, disclosure, and reporting obligations depending on their structure. As a result, investors in public utility securitizations structured as series trusts could receive different sets of disclosures, reporting frequency, and other regulatory requirements from those available in stand-alone trust issuances, despite the securities themselves having nearly identical features and risk profiles.

However, the concerns informing this decision ( e.g., that an investor may need to analyze potential risks from a wholly separate and unrelated transaction created after its original investment) [102] may no longer be so salient that the structure should continue to be disqualifying.[103] Aside from the difference in the structure of the issuance trust, the key features of these offerings are the same and satisfy the “core principles” of the ABS definition as set out by the Commission in 2004 as well as the elements of the Exchange Act ABS Definition.[104] For example, in ( printed page 47265) public utility securitizations, the asset that collateralizes the ABS is the property right to assess and collect charges paid by utility customers, up to a specified total amount, within a specified time period that is not to exceed the final maturity date of the bonds issued to investors. This property right, therefore, is a “self-liquidating financial asset” because it establishes: (1) the total amount to be raised by the charges, thereby converting the property right into that dollar amount in cash; and (2) the finite time period by which that property right must convert to cash.

Another core principle of both ABS definitions—that payments to the securityholders depend primarily on cash flows from the underlying self-liquidating financial asset—is also present, regardless of structure. Whether an offering employs a stand-alone trust or a series trust, the financing order establishing the property right requires that the property right be transferred to a bankruptcy-remote special purpose vehicle ( i.e., the trust) as a true sale. The securityholders rely only on the cash flow from this property right for payment, not on the performance of the utility company itself and, in the event of bankruptcy of the utility company, payments on the public utility securitizations would continue independent of the utility's continued participation or existence.[105]

Because the key features of these offerings are otherwise the same, whether the offering is both Exchange Act ABS and Regulation AB ABS (and therefore eligible for the specialized registration, reporting, and disclosure regime in Regulation AB) or solely Exchange Act ABS (and therefore not eligible for the Regulation AB regime) is entirely dependent on the structure of the transaction. This has the practical effect of preventing an issuer of an offering structured as a series trust from accessing the registered ABS market. Recognizing this fact, and in response to a request from issuers in this asset class,[106] Commission staff has advised issuers of public utility securitizations structured using a series trust to follow the regulatory regime in Regulation AB since 2007.[107]

We have also observed that there appears to be some continued market confusion with respect to the differences, overlap, and purpose of the Regulation AB ABS Definition and the Exchange Act ABS Definition.[108] Given the evolution of the ABS market in general since the Regulation AB ABS Definition was adopted, the similarities between the two definitions, and the resulting potential ambiguity in the market, we are seeking public comment about whether we should amend the definition of ABS in Regulation AB to better align with the Exchange Act ABS Definition, as well as consider potential updates to other related definitions. Such revisions may bring clarity and uniformity to the current ABS regulatory regime and remove potentially unnecessary definitional and/or structural impediments to accessing the registered market for ABS issuers and investors, while providing sufficient flexibility and accommodating future developments in the ABS market.

C. Request for Comment

32. Are there any challenges to market participants associated with having more than one definition of “asset-backed security” in the Federal securities laws? If so, what are the challenges? Are there any potential benefits to retaining the current Regulation AB ABS Definition as is that could be lost if we make changes? What are those benefits?

33. Should we amend the Regulation AB ABS Definition to cross-reference, or otherwise incorporate, the Exchange Act ABS Definition? What are the advantages or disadvantages of consolidating the two definitions?

- If we amend the Regulation AB ABS Definition in this way, should we revise either Item 1101(c)(2) or Item 1101(c)(3) to be consistent with the additional features and structures (such as active pool management and the use of series trusts) included in the Exchange Act ABS Definition? Are there any conditions or limitations in Item 1101(c)(2) and/or Item 1101(c)(3) that we should retain as still applicable and/or because they would still be appropriate for registered offerings? If so, please specify what should be retained, deleted, and/or revised and why.

34. As an alternative to the approach described in question 33, should we replace the entirety of the Regulation AB ABS Definition with the Exchange Act ABS Definition? Would replacing the entirety of the Regulation AB ABS Definition with the Exchange Act ABS Definition create a definition of “asset-backed security” that is too broad for purposes of Regulation AB? If so, what conditions and limitations would be necessary or beneficial?

35. Should we consider expanding the Regulation AB ABS Definition to conform with the recently adopted definition of “asset-backed security” in Securities Act Rule 192, which references the Exchange Act ABS Definition but also includes synthetic and hybrid cash/synthetic securitizations? Why or why not?

36. Are there any potential regulatory impacts to market participants that would result from revising the Regulation AB ABS Definition?

- For example, would revising the Regulation AB ABS Definition cause any consequences for issuers who have historically offered, or would offer, securities in reliance on Regulation A,[109] which excludes “asset-backed securities as such term is defined in Item 1101(c) of Regulation AB” from eligibility? [110]

- What impacts, if any, would incorporating the Exchange Act ABS Definition into Regulation AB have on market participants who are subject to regulation under the Investment Company Act of 1940? Should managed pool structures such as CLOs be permitted (but not required) to register ABS offerings pursuant to Regulation AB? What impacts, if any, would such a registered ABS offering have on a pool's ability to rely on the exclusions set forth in sections 3(c)(1) or 3(c)(7) of the Investment Company Act?

- Should we also consider revising the definition of “asset-backed securities” in Rule 902(a)(2) of Regulation S [111] to further harmonize the definitions across the Federal securities laws? What impacts, if any, ( printed page 47266) would such a change have for issuers and/or offerings of ABS offered and sold pursuant to Regulation S?

- While any potential changes to the Regulation AB ABS Definition would not change the statutory definition of “asset-backed security” referenced in Exchange Act section 3(a)(62)(A)(iv), would revising the Regulation AB ABS Definition have any impact for a credit rating agency registered, or seeking to be registered, as a nationally recognized statistical rating agency (“NRSRO”) in the issuers of asset-backed securities category of credit ratings pursuant to Exchange Act Rule 17g-1? [112] Could revising such definition have any impact for NRSROs not registered in the issuers of asset-backed securities category or for users of credit ratings?

37. Are there other definitions under Item 1101 of Regulation AB that we should consider amending to expand issuer and investor access to the registered ABS markets and facilitate enhanced capital formation and liquidity while maintaining appropriate investor protections?

- For example, do the definitions for the various ABS transaction participants—such as asset-backed issuer, depositor, issuing entity, sponsor, and originator—still accurately describe these parties' roles and responsibilities in contemporary securitization transactions? If not, what changes would be beneficial?

- Would any new definitions be necessary or beneficial?

- Is there interpretive guidance that could help clarify any definitions?

38. What additional or alternative disclosures should we consider in light of any revisions to the Regulation AB ABS Definition or other definitional changes discussed above? What specialized disclosures may be necessary or appropriate regarding asset classes or structures that may be new to shelf registration or registration in general?

39. Are there any additional features of, or developments in, the ABS market that we should take into account in considering potential regulatory changes?

V. General Request for Comment

We request and encourage any interested person to submit comments on any aspect of this concept release, other matters that might have an impact on the topics discussed in this concept release, and any suggestions for additional changes. We are also soliciting comment on any other aspect of asset-backed securities regulations that commenters believe may be improved, including additional amendments to Regulation AB that should be considered. Please be as specific as possible in your discussion and analysis of any additional issues. We particularly welcome comments on any costs, burdens, or benefits that may result from possible regulatory responses related to the items identified in this release or otherwise proposed by commenters.

VI. Regulatory Planning and Review

This concept release and request for comments is a significant regulatory action under Executive Order 12866, as amended, and has been reviewed by the Office of Management and Budget.

VII. Conclusion

We are interested in the public's views regarding the matters discussed in this concept release. We recognize the public interest is served by opportunities to invest in a variety of securities, including asset-backed securities and, in this regard, we seek the public's input on ways to reduce the barriers to entering the registered ABS market, expand registration, and increase liquidity in the ABS market in general. For RMBS market participants, in particular, reducing barriers may result in a wider investor base, which could potentially increase financing available for housing markets, while also renewing opportunities for investors to benefit from the publicly available disclosure and greater transparency that registered offerings provide. We encourage all interested parties to submit comments on the topics being considered in this concept release. If possible, please reference the specific question numbers or sections of the release when submitting comments.

By the Commission.

Dated: September 26, 2025.

J. Matthew DeLesDernier,

Deputy Secretary.