Small Business Lending Under the Equal Credit Opportunity Act (Regulation B)

The Consumer Financial Protection Bureau (CFPB or Bureau) proposes revisions to certain provisions of Regulation B, subpart B, implementing changes to the Equal Credit Opportuni...

The Consumer Financial Protection Bureau (CFPB or Bureau) proposes revisions to certain provisions of Regulation B, subpart B, implementing changes to the Equal Credit Opportunity Act made by section 1071 of the Dodd-Frank Wall Street Reform and Consumer Protection Act. The Bureau is reconsidering coverage of certain credit transactions and financial institutions; the small business definition; inclusion of certain data points and how others are collected; and the compliance date. The CFPB believes these proposed changes would streamline the rule, reduce complexity for lenders, and improve data quality, advancing the purposes of section 1071 and complying with recent executive directives.

DATES:

Comments must be received on or before December 15, 2025.

ADDRESSES:

You may submit comments, identified by Docket No. CFPB-2025-0040 or RIN 3170-AB40, by any of the following methods:

Mail/Hand Delivery/Courier:

Comment Intake—1071 Reconsideration NPRM, c/o Legal Division Docket Manager, Consumer Financial Protection Bureau, 1700 G Street NW, Washington, DC 20552.

Instructions:

The CFPB encourages the early submission of comments. All submissions should include the agency name and docket number or Regulatory Information Number (RIN) for this rulemaking. Because paper mail is subject to delay, commenters are encouraged to submit comments electronically. In general, all comments received will be posted without change to

https://www.regulations.gov.

All submissions, including attachments and other supporting materials, will become part of the public record and subject to public disclosure. Proprietary information or sensitive personal information, such as account numbers or Social Security numbers, or names of other individuals, should not be included. Submissions will not be edited to remove any identifying or contact information.

In 2010, Congress passed the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act). Section 1071 of that Act [1]

amended the Equal Credit Opportunity Act (ECOA) [2]

to require that financial institutions collect and report to the CFPB certain data regarding applications for credit for women-owned, minority-owned, and small businesses. Section 1071's statutory purposes are to (1) facilitate enforcement of fair lending laws, and (2) enable communities, governmental entities, and creditors to identify business and community development needs and opportunities of women-owned, minority-owned, and small businesses. Section 1071 directs the CFPB to prescribe such rules and issue such guidance as may be necessary to carry out, enforce, and compile data pursuant to section 1071.

The CFPB worked toward a section 1071 rulemaking for a number of years and has sought public comment from stakeholders numerous times. The CFPB held a field hearing on May 10, 2017, and published a request for information regarding the small business lending market.[3]

On July 22, 2020, the CFPB issued a survey to collect information about potential one-time costs to financial institutions to prepare to collect and report data on small business lending.

On September 15, 2020, the CFPB released an Outline of Proposals Under Consideration and Alternatives Considered pursuant to the Small Business Regulatory Enforcement Fairness Act of 1996 (SBREFA). On October 15, 2020, the CFPB convened a Small Business Review Panel for the section 1071 rulemaking, and the Panel met with small entity representatives (SERs). The Panel Report, publicly released on December 15, 2020, was the culmination of the SBREFA process for the section 1071 rulemaking and included feedback from SERs and written feedback from other stakeholders as well.

On October 8, 2021, the CFPB published in the

Federal Register

a proposed rule (2021 proposed rule) amending Regulation B to implement changes to ECOA made by section 1071 of the Dodd-Frank Act.[4]

The comment period for the proposed rule closed on January 6, 2022.

The CFPB received approximately 2,100 comments on the proposal during the comment period. Approximately 650 of these comments were unique, detailed comment letters representing diverse interests. These commenters included lenders such as banks and credit unions, community development financial institutions (CDFIs), community development companies, Farm Credit System (FCS) lenders, online lenders, and others; national and regional industry trade associations; software vendors; business advocacy groups; community groups; research, academic, and other advocacy organizations; Members of Congress; Federal and State government offices/agencies; small businesses; and individuals.

On May 31, 2023, the CFPB published a final rule in the

Federal Register

to implement section 1071 by adding subpart B to Regulation B (2023 final rule).[5]

Further details about section 1071, small business lending market dynamics, and the CFPB's rulemaking process leading up to the 2023 final rule can be found in the preamble to the 2023 final rule.

On July 3, 2024, the CFPB published in the

Federal Register

an interim final rule (2024 interim final rule)[6]

to extend

( printed page 50953)

the rule's compliance dates in accordance with orders issued by the United States District Court for the Southern District of Texas.[7]

Challenges to the 2023 final rule filed by various plaintiffs remain ongoing in three jurisdictions; each of those courts stayed the rule's compliance deadlines for some market participants.[8]

However, the courts did not stay the compliance dates for those who are not plaintiffs or intervenors in those cases.

On June 18, 2025, the CFPB published in the

Federal Register

an interim final rule (2025 interim final rule) to extend compliance deadlines by approximately one year[9]

to facilitate consistent compliance across all covered financial institutions. The CFPB sought comment on the 2025 interim final rule.

On October 2, 2025, the CFPB published in the

Federal Register

a final rule (2025 compliance date final rule) that confirmed its findings in the 2025 interim final rule and determined upon a review of comments received that no further substantive changes were necessary.[10]

The CFPB received 20 comments in response to the 2025 interim final rule. Most commenters addressed the 2025 interim final rule itself. Other comments addressed provisions of the 2023 final rule not addressed by the 2025 interim final rule, some of which are discussed below.

Based on reactions to the 2023 final rule, including continued feedback from stakeholders and the ongoing litigation, the CFPB now believes that at the onset of a potentially long-term data collection regime, it should start with more modest requirements, focusing on core lending products, lenders, and data. The CFPB preliminarily believes that that reaction to the 2023 final rule, practically speaking, was in part based on its expansive approach, appearing to seek broad coverage of lenders, products, and information collected.[11]

The CFPB does not believe that alignment with the statutory purposes of section 1071 requires the use of its discretionary authority to collect data with such a breadth of scope.

The CFPB now believes that the 2023 final rule should have given more weight to qualitative differences among certain types of lenders and the likelihood that smaller lenders would face difficulties addressing the complexity of a rule of broad scope, both of which could potentially diminish the quality of the data they collect.

The CFPB believes, based on this experience, that a longer-term approach to advance the statutory purposes of section 1071 would be to commence the collection of data with a narrower scope to ensure its quality and to limit, as much as possible, any disturbance of the provision of credit to small businesses. The statutory purposes of the rule are not well served by an expansive rule that could create disruptions in small business lending markets.

Rather, the CFPB now believes that an incremental approach may better serve the statutory purposes of section 1071 in the long term. Such an approach would start with core lending products, core providers, and core data points. This approach would comply with section 1071 and further its statutory purposes but reduce the rule's initial impact on small businesses and lenders. Over time, as the CFPB and financial institutions learn from early iterations of data collections, the CFPB could consider amending the rule.

The gradual development of data collection under the Home Mortgage Disclosure Act (HMDA) [12]

and its implementing Regulation C [13]

over the past 50 years provides precedent for an incremental approach. Congress passed HMDA in 1975,[14]

and the Board Governors of the Federal Reserve System (Board) promulgated implementing regulations in 1976, requiring the collection of relatively few data points from relatively few lenders. At various points, HMDA amendments passed by Congress, among other things, expanded the breadth of financial institutions covered, as well as the number of data points collected from those reporting institutions.[15]

Over time, rulemakings by the Board and the CFPB implemented these amendments, added and removed data points, and expanded and contracted the scope of Regulation C.[16]

The CFPB believes that it should approach the section 1071 data collection regime as a longer-term project akin to HMDA. The CFPB believes that it is a proper use of its authority under 15 U.S.C. 1691c-2 to reconsider several portions of the 2023 final rule to commence data collection with a focus on core lending products, core lenders, and mostly statutory data points. The CFPB believes that this incrementalist approach—starting with a more modest rule with a limited set of products, lenders, or data points—will serve the long-term interests of section 1071.

In addition, on January 20, 2025, the President issued Executive Order (E.O.) 14168, “Defending Women From Gender Ideology Extremism and Restoring Biological Truth to the Federal Government” (Defending Women E.O.).[17]

That order, among other things, directs Federal agencies to remove references and questions discussing gender identity. The order also identifies a binary of male/female sex, directing agencies to use those terms when seeking information about an individual's sex.

The CFPB has consulted with the appropriate prudential regulators and other Federal agencies regarding consistency with any prudential, market, or systemic objectives administered by these agencies as

( printed page 50954)

required by section 1022(b)(2)(B) of the Dodd-Frank Act.

II. Legal Authority

The Bureau is issuing this proposed rule pursuant to its authority under section 1071. As discussed above, in the Dodd-Frank Act, Congress amended ECOA by adding section 1071, which directs the CFPB to adopt regulations governing the collection and reporting of small business lending data. Specifically, section 1071 requires financial institutions to collect and report to the CFPB certain data on applications for credit for women-owned, minority-owned, and small businesses. Congress enacted section 1071 for the purpose of (1) facilitating enforcement of fair lending laws and (2) enabling communities, governmental entities, and creditors to identify business and community development needs and opportunities of women-owned, minority-owned, and small businesses.[18]

To advance these statutory purposes, section 1071 grants the Bureau general rulemaking authority for section 1071, providing that the Bureau shall prescribe such rules and issue such guidance as may be necessary to carry out, enforce, and compile data pursuant to section 1071.[19]

Section 1071, in 15 U.S.C. 1691c-2(g)(2), also permits the Bureau to adopt exceptions to any requirement of section 1071 and to conditionally or unconditionally exempt any financial institution or class of financial institutions from the requirements of section 1071, as the Bureau deems necessary or appropriate to carry out the purposes of section 1071. The Bureau relies on its general rulemaking authority under 15 U.S.C. 1691c-2(g)(1) in this proposed rule and relies on 15 U.S.C. 1691c-2(g)(2) when proposing specific exceptions or exemptions to section 1071's requirements.

See the 2023 final rule for a more detailed discussion of the CFPB's legal authorities.[20]

III. Discussion of the Proposed Rule

A. Summary of Proposed Rule

As set out above, the CFPB now proposes to reconsider certain provisions of the 2023 final rule. The CFPB believes that a potentially long-term data collection regime should start with a focus on core lending products, lenders, small businesses, and data points. The CFPB believes in retrospect that the approach it took in the 2023 final rule—a broad initial coverage of lenders, products, small businesses and data points—was not conducive to the long-term success of the data collection regime under section 1071. The CFPB now believes that a better, longer-term approach to advance the statutory purposes of section 1071 would be to commence the collection of data with a narrower scope to ensure its quality, and to limit, as much as possible, any disturbance of the provision of credit to small businesses. The CFPB believes that such an incremental approach would also comply with section 1071 and minimize any negative initial impact on small business lending markets and on data quality. In the future, based on CFPB and industry experience during the early years of data collection, the CFPB could consider amending the rule as appropriate to further the purposes of section 1071.

The CFPB also believes that the 2023 final rule has not created significant reliance interests that would dissuade the Bureau from reconsidering its position as to certain portions of the rule. Litigation challenging provisions of the 2023 final rule and delays in the compliance dates for this rule suggest that reconsideration of the specific issues below would not meaningfully change compliance obligations.

Covered credit transactions.

The CFPB believes that the initial iterations of data collection under the rule should focus on the core, widely used lending products most likely to be foundational to small businesses' formation and operation. The CFPB therefore proposes to exclude merchant cash advances (MCAs), agricultural lending, and small dollar loans from the definition of covered credit transaction.

Covered financial institutions.

The CFPB believes that the initial iterations of data collection under the rule should focus on larger core lenders. The CFPB therefore proposes two changes to the covered financial institution definition: first, to exclude FCS lenders from coverage; and second, to raise the origination threshold from 100 to 1,000 covered credit transactions for each of two consecutive years. The CFPB is also proposing conforming changes to the bona fide error portions of the enforcement provisions in the rule.

Small business.

The CFPB believes that the focus of the rule, at least initially, should be truly small businesses. The CFPB therefore proposes to change the gross annual revenue threshold in the rule's definition of small business from $5 million or less to $1 million or less.

Data points.

The CFPB believes that the initial iterations of data collection under the rule should focus on core data points and be consistent with other executive agency directives concerning the collection of demographic data.

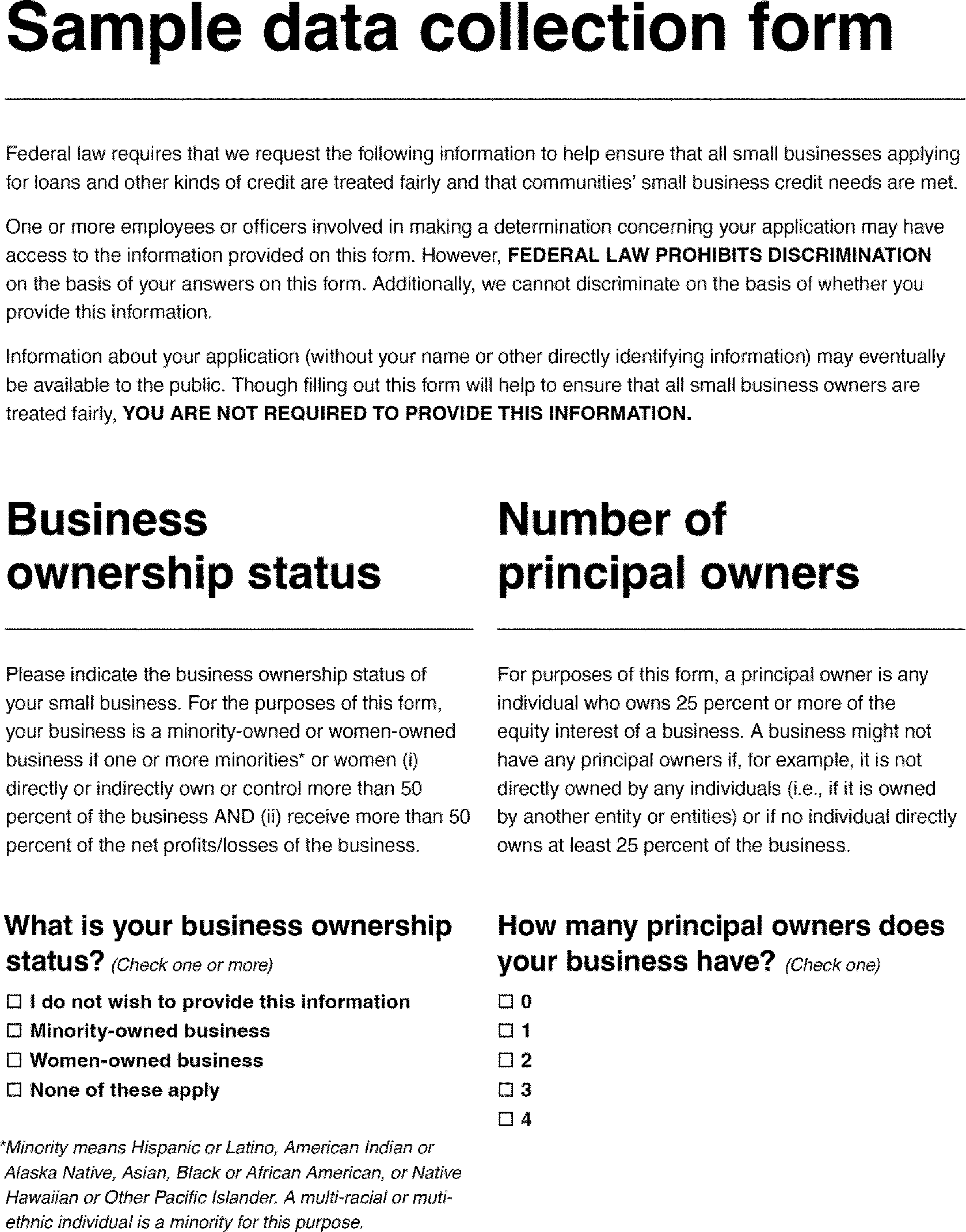

The CFPB therefore intends to focus data collection on data points specifically identified in section 1071 and a limited number of other data points needed to facilitate the collection of these statutory data points. The CFPB proposes to remove the discretionary data points for application method, application recipient, denial reasons, pricing information, and number of workers. The CFPB also proposes changes to comply with an executive branch mandate, which would result in a modification of the collection of data concerning business ownership status of small business applicants and the format of demographic data collected concerning the principal owners of a small business.

Time and manner of data collection.

The CFPB proposes changes to the provisions on the time and manner of data collection, to remove certain requirements that are not statutorily required and appear to anticipate or presume non-compliance with the rule. The CFPB also proposes to add a provision that would emphasize for applicants their statutory rights under the rule.

Compliance dates.

Finally, in light of these other proposed changes to the rule, the CFPB proposes to extend the rule's compliance date provisions to January 1, 2028 for all financial institutions that remain covered by the rule, and to make other simplifying and streamlining changes.

The CFPB also addresses in this summary two other issues.

Privacy and data publication.

The CFPB does not address in this proposal the privacy discussions in the 2023 final rule or its statements about the eventual publication of data. The 2023 final rule did not purport to make any final or binding decisions concerning its privacy analysis, instead announcing only its “preliminary assessment of how it might appropriately assess and advance privacy interests by means of selective deletion or modification” of data. The 2023 final rule also did not reach conclusions regarding the procedural vehicle it would use to convey its decisions with respect to privacy.[21]

Nor

( printed page 50955)

has CFPB conclusively announced a timeline for the publication of application-level data, except for observing that it would need a full year's worth of data to conduct the necessary privacy analysis. The CFPB also suggested that it intended to publish aggregate data in the first year of receiving data, and before publishing any application-level data. The CFPB is currently reconsidering all of these issues and preliminary findings, will continue to engage with stakeholders, and will address these issues and findings going forward in a timely fashion.

As part of eventual data publication, as with HMDA data, the CFPB intends to note to data users that data alone are generally not used to determine whether a lender is complying with fair lending laws. The data do not include all the legitimate credit risk considerations for loan approval and loan pricing decisions. Therefore, when regulators conduct fair lending examinations, they analyze additional information before reaching a determination about an institution's compliance with fair lending laws.

Grace period.

The CFPB does not address the grace period policy statement in this proposal. The CFPB does, however, announce its intention to maintain the grace period for the same reasons articulated in the 2023 final rule, as amended by the 2025 interim final rule, and to alter the grace period to coincide with the new proposed compliance date, if it is finalized.

The Bureau seeks comments on the general approach taken in this proposal. The Bureau also seeks comment on its proposed exclusion or reconsideration of the products, lenders, small business definition, and data points identified below. Further, the Bureau requests comment on the likely change in cost and complexity of data associated with each of the specific proposed regulatory revisions identified below and whether changes to the quality of data (

e.g.,

better or worse data quality), advances or is contrary to the purposes of section 1071. Finally, the Bureau requests comment on whether the 2023 final rule has created any reliance interests not otherwise identified in this proposal.

B. Section 1002.104—Covered Credit Transactions and Excluded Transactions

The CFPB believes that at the onset of data collection under section 1071 the rule should focus on core, generally applicable, lending products that are most likely to be foundational to small businesses' formation and operation—loans, lines of credit, and credit cards—before determining whether to expand the scope of the rule to include more niche or specialty lending products. The CFPB therefore proposes to exclude MCAs, agricultural lending, and small dollar loans from the definition of covered credit transaction to better ensure the smooth operation of the initial period of data collection, while minimizing disruptions and regulatory complexity in the credit markets subject to section 1071.

1002.104(b)(7)—Merchant Cash Advance

Current § 1002.104(a) defines a “covered credit transaction” as “an extension of business credit that is not an excluded transaction under paragraph (b) of this section.” Section 1002.104(b)(1)-(6) enumerates six types of transactions that are excluded from covered credit extensions. The Bureau proposes adding MCAs to the list of excluded transactions in § 1002.104(b). Proposed § 1002.104(b)(7) would exclude MCAs, which it would define as an agreement under which a small business receives a lump-sum payment in exchange for the right to receive a percentage of the small business's future sales or income up to a ceiling amount.[22]

Consistent with this proposed new exclusion, the CFPB proposes deleting several references to MCAs, and the related term sales-based financing, in commentary.

In the 2023 final rule, the CFPB explained its belief that the statutory term “credit” in ECOA is intentionally broad so as to include a wide variety of products without specifically identifying any particular product by name, such that all credit products should be included in the rule unless the CFPB specifically excluded them and concluded that “credit” encompasses MCAs. It further explained that MCAs should not be understood to constitute factoring within the meaning of the existing commentary to Regulation B subpart A or the definition in existing comment 104(b)-1, because factoring involves entities selling an existing legal right to payment from a third party, while no such contemporaneous right exists in an MCA. The CFPB also noted its understanding that, as a practical matter, MCAs are underwritten and function like a typical loan (

i.e.,

underwriting of the recipient of the funds; repayment that functionally comes from the recipient's own accounts rather than from a third party; repayment of the advance itself plus additional amounts akin to interest; and, at least for some subset of MCAs, repayment in regular intervals over a predictable period of time), although it also implicitly acknowledged practical differences between MCAs and conventional loans by including numerous provisions intended to capture MCA-specific data.

This proposal reconsiders the CFPB's previous conclusions, as illustrated in existing comment 104(a)(1)-1, which does not exclude MCAs from the definition of “covered credit transactions” under § 1002.104(a), for several independent reasons.

First, the CFPB believes that at the onset of the data collection under section 1071 the focus should be on core lenders and products before the CFPB considers expanding the scope of the rule. MCAs are structured differently from traditional lending products; traditional lending concepts like “interest rate” do not fit the way that MCAs are priced.[23]

As a result, it is not clear that data collection on MCA transactions under section 1071 would yield information that advances section 1071's statutory purposes to the extent that some or many such transactions do not constitute credit. The CFPB believes it would advance the purposes of section 1071 at this time to exclude MCAs from the definition of covered credit transaction, and to focus on ensuring the smooth operation of data collection as to core lending products and providers most likely to be foundational to small businesses' formation and operation.

Second, the CFPB believes it erred in prematurely determining that collection of data on MCA transactions would serve section 1071's statutory purposes by concluding that all MCAs constitute credit. The 2023 final rule's one-size-fits-all approach also does not take into account the varied terms and features of MCAs across the market that may be relevant to whether the products meet the definition of “credit” under ECOA, nor did it account for the fact that MCAs

( printed page 50956)

are relatively new products whose features and practices may be evolving, including in response to State regulation. Moreover, while some State courts have analyzed whether some MCAs meet State law definitions of “debt” or “credit,” there is a dearth of case law analyzing whether MCAs meet ECOA's definition of “credit.”

Excluding MCAs from the definition of “covered credit transaction” would be consistent with the way the CFPB has already treated leases, which also present close questions as to whether they meet the definition of “credit” under ECOA. In the 2023 final rule's analysis of leases,[24]

the CFPB acknowledged that some lease transactions could constitute “credit.” But rather than include all lease transactions in the 2023 final rule to ensure coverage of those leases that did actually constitute credit and credit disguised as leases, the CFPB determined that it would be able to monitor the market for such products without including them in the 2023 final rule. The CFPB proposes taking a similar approach to MCA transactions as it did to leases.

Further, the CFPB believes that the 2023 final rule's coverage of MCAs does not take into account State law developments addressing sales-based financing. Several States have legislation and/or regulations in place addressing the MCA market and requiring providers to disclose terms such as the total cost of capital and the financing rate. Such laws provide key protections for users of MCAs and may shape MCA terms and practices in ways that bear on the question of whether they meet ECOA's definition of “credit.” [25]

While the 2023 final rule referenced these pieces of State legislation, it did not consider the extent to which the evolving landscape under State law rendered premature a determination that including MCAs in the definition of “covered credit transaction” for purposes of mandating data collection furthered section 1071's statutory purposes. The CFPB believes that it would be advantageous to observe how State laws address MCAs before the CFPB decides how, and whether, to collect data regarding MCAs pursuant to section 1071.

Finally, while the final rule cited concerns about high costs and predatory practices in the MCA market,[26]

those concerns may be addressed by Federal and State law enforcement agencies through their respective enforcement authorities.

The CFPB believes that taking into account the factors listed above, the relative novelty and evolving landscape of the MCA industry and the ongoing changes at the State level concerning the regulation of MCAs, that excluding MCA transactions from coverage under the rule at this time is necessary and appropriate to carry out the purposes of section 1071. As explained above, MCAs differ in kind from traditional lending products, such that collecting data on MCA transactions under Section 1071 may not produce information that is comparable to data collected on other types of transactions. And because MCAs have not generally been regulated as credit, many smaller MCA providers may lack the infrastructure needed to manage compliance with regulatory requirements associated with making extensions of credit. Taken together, requiring MCAs to be reported could lead to data quality issues, which would not advance the purposes of section 1071.

The CFPB will continue to monitor developments in the markets for MCAs and other sales-based financing to determine whether over time a subset might be appropriately included in the definition of “covered credit transaction” for purposes of data collection.

The CFPB seeks comment on this proposed revision to the rule. It also seeks comment on topics including, but not limited to, the extent to which MCAs differ from or resemble traditional lending products; the diversity of MCA terms and practices and how they impact whether MCAs, or a subset of MCAs, meet the definition of “credit” under ECOA; whether certain types of MCAs are more or less appropriate for exclusion; and suggestions for how the 2023 final rule could be modified with respect to MCAs if the CFPB ultimately does not exclude them.

The CFPB further seeks comment on alternative definitions to the one proposed in § 1002.104(b)(7).

1002.104(b)(8)—Agricultural Lending

The CFPB proposes adding agricultural lending to the list of excluded transactions under § 1002.104(b). The CFPB proposes adding new § 1002.104(b)(8), which would define agricultural lending as a transaction to fund the production of crops, fruits, vegetables, and livestock, or to fund the purchase or refinance of capital assets such as farmland, machinery and equipment, breeder livestock, and farm real estate improvements. Consistent with this proposed addition, the Bureau proposes deleting references to agricultural credit in current commentary. This would simplify the rule by narrowing its scope to core, generally applicable, small business lending products and avoid covering a distinct and specialized lending sector that is already subject to a different regulatory reporting scheme.[27]

In the 2023 final rule, the CFPB declined to exclude agricultural credit from its definition of a “covered credit transaction.” It noted that ECOA itself has no exceptions for agricultural credit, that agricultural businesses are included in section 1071's statutory definition of small business (defined by cross-reference to the Small Business Act), and that there have been instances of discrimination in agricultural lending. It rejected comments asserting that agricultural credit is unique and not comparable to other types of small business lending, instead observing that “every small business industry has its own unique characteristics.” [28]

In response to commenters expressing concern about the impact on local community financial institutions and an outsized effect on the cost of credit for farmers, the CFPB emphasized that it was increasing its institutional coverage threshold to 100 annual originations, from the 25 originations it had originally proposed. The CFPB mentioned that many agricultural lenders have already been required to

( printed page 50957)

collect and report some form of data by HMDA, the Community Reinvestment Act (CRA), and/or the Farm Credit Administration (FCA), but did so only to note that lenders accordingly should be able to adapt to the CFPB's new data collection requirements.

The CFPB now believes that excluding agricultural lending from the definition of “covered credit transaction” would advance the statutory purposes of section 1071 at this early phase as the CFPB begins the collection of small business lending data. Most notably, typical agricultural lending differs markedly from other types of commercial lending. Agricultural loans are often secured by biological-based assets such as crops or livestock, which are subject to variables and risk from weather and disease. These characteristics create unique underwriting challenges that make such loans difficult to compare to those in other industries. The 2023 rule did not adequately consider these distinctions and the quality of data stemming from such transactions. Indeed, other data collection regimes, such as CRA regulations, appear to acknowledge categorical differences between loans to small businesses generally and loans to small farms.[29]

Second, agricultural lending is already subject to an existing Federal data collection framework, one that is tailored to this particular sector. The FCA conducts a substantial amount of agricultural lending through a nationwide network of Congressionally chartered, borrower-owned cooperatives. This system is subject to extensive oversight by the FCA. Among other things, the FCA collects demographic data including race, ethnicity, and gender from applicants as part of its program oversight, in contrast to other forms of small business lending where such data collection was not permissible under § 1002.5 of Regulation B until the promulgation of the 2023 final rule.[30]

Further, under CRA regulations, institutions must report data on lending to small farms alongside reporting their lending to small businesses. The 2023 final rule did not adequately consider these distinctions.[31]

The CFPB believes upon reconsideration that the fact that agricultural lenders are already reporting information to other agencies supports its conclusion that excluding agricultural lending is necessary or appropriate to carry out the purposes of section 1071 to avoid imposing new, overlapping reporting requirements on agricultural lenders at this point when the CFPB is commencing the collection of data under this rule. The Bureau believes that excluding agricultural lending would further the purposes of section 1071 because such an exclusion would limit potential issues with data quality. Compliance may pose greater difficulties for small agricultural lenders, which are often rural entities with less compliance infrastructure than other lenders, potentially impacting the quality of their data, and they may need to divert their limited resources from lending activities. Further, for lenders that provide both agricultural and non-agricultural loans that would still be subject to coverage, the CFPB believes that such lenders would be better situated to focusing their section 1071 reporting efforts on improving the quality of data for more core lending products.

Given these factors, the CFPB believes it would be appropriate to reconsider the rule's application to agricultural lending to focus on conventional, generally applicable small business lending at this time, and to use its exemption authority under 15 U.S.C. 1691c-2(g)(2) to exclude agricultural lending from coverage under the rule.

The CFPB seeks comment on this proposed revision to the rule. It seeks comment on topics including, but not limited to, the definition of agricultural lending; the extent to which agricultural lending differs from or resembles other types of lending; and whether specific types of agricultural lending are more or less appropriate for exclusion.

1002.104(b)(9)—Small Dollar Business Credit

The CFPB proposes adding small dollar business credit to the list of excluded transactions under § 1002.104(b). Proposed § 1002.104(b)(9) would exclude from the definition of covered credit transaction a transaction in an amount of $1,000 or less, to be adjusted for inflation over time.

In the 2023 final rule, the CFPB declined commenters' suggestions that it exempt credit transactions below a certain threshold; commenters had suggested exemption thresholds ranging from $25,000 to $10 million, on the grounds that it would help smaller institutions continue to make credit available. The CFPB explained that it was not adopting an exemption because of the significant volume of small business lending involving credit amounts below the threshold levels proposed by commenters.

The CFPB now believes that an exclusion for the smallest loans—well under the thresholds suggested by commenters in the 2023 final rule—is necessary or appropriate to carry out the purposes of section 1071. Indeed, in considering comments regarding larger exemption thresholds, the 2023 final rule did not explicitly address an exemption for loans under $1,000.

The CFPB believes that the collection of data on such loans, to the extent that they exist, are more likely to result in poor data quality for purposes of any analyses in furtherance of the statutory purposes of section 1071, given that small businesses will generally require much larger loans to begin or operate their businesses. Typically, very small loans below $1,000 would be satisfied by consumer credit options and small non-profit lenders who lack infrastructure to support regulatory compliance. Consequently, data collected from smaller transactions may not provide meaningful insight into the practices of most core lenders to small businesses.

Further, requiring data reporting on loans of $1,000 or less may make offering such small credit products uneconomical for lenders. Detailed data collection and reporting requirements are likely to impose operational complexity, which would make producing quality data difficult for smaller financial institutions. The CFPB is concerned that this could impact data quality.

Moreover, the CFPB believes, based on its experience and understanding of the markets, that many lenders treat transactions under $1,000 as consumer credit, rather than business credit. Further, $1,000 is substantially lower than loan amounts already characterized as “microloans” to businesses. The CFPB understands that loans in such amounts are not material for the small business lending markets. For example, the Small Business Administration (SBA) offers business credit that it characterizes as “microloans,” which are generally for loan amounts under $50,000 and an average loan amount of $13,000.[32]

Further, several commenters in the 2023 final rule requested that the CFPB carve out loans under $50,000 to

( printed page 50958)

$100,000 as microloans.[33]

Some State-run programs offer business credit that start at a minimum loan amount of $1,000.[34]

The CFPB believes that it seems unlikely that many such small dollar loans under $1,000 to small businesses are made, and if so the collection of such data would not advance the statutory purposes of the rule.

The CFPB seeks comment on this proposed revision to the rule. It seeks comment on topics including, but not limited to, the loan amount at which the exclusion for small dollar business credit should be set; whether the exclusion should be limited to certain types of loan products, financial institutions, or small businesses; the extent to which financial institutions lend to small businesses in amounts less than $1,000 and why they do so; and whether the exclusion should account for a lender extending multiple small dollar loans to a single small business.

C. Section 1002.105—Covered Financial Institutions and Exempt Institutions

The CFPB believes that at the onset of data collection under section 1071 the focus should be on larger core lenders before the CFPB considers whether it would be appropriate to expand the scope of the rule to specialty lenders and smaller lenders. The CFPB therefore proposes to exclude FCS lenders from the definition of covered financial institution and proposes to raise the origination threshold from 100 to 1,000 covered credit transactions to better ensure the smooth operation of the initial period of data collection.

105(b) Covered Financial Institution—FCS Lenders

The CFPB proposes excluding FCS lenders from the “covered financial institution” definition in § 1002.105(b). Consistent with this proposed exemption, the CFPB proposes deleting several references to FCS lenders in commentary.

As with the Bureau's proposal to reconsider the treatment of agricultural transactions as covered transaction under § 1002.104(a), this proposal would simplify the rule by narrowing its scope to core small business lending practices and lenders. The proposal would also avoid imposing reporting requirements on a category of specialized lenders that are already subject to a separate regulatory reporting scheme.

The CFPB believes that an exemption for FCS lenders would advance the statutory purposes of section 1071. FCS lenders have a unique mission-driven structure, and they operate in a specific regulatory environment.

FCS lenders differ from traditional financial institutions in several significant respects. The FCS is comprised of a nationwide network of borrower-owned, cooperative institutions with a statutory mandate to provide the agricultural sector with reliable credit. FCS borrowers include agricultural and related businesses as well as rural homeowners. As owners of the FCS lending associations, these borrowers can receive patronage dividends that can reduce borrowing costs and make FCS loans difficult to compare to loans issued by non-FCS lenders. Commercial banks, by contrast, are owned by shareholders, and credit unions, while member-owned, serve a wide range of customers, provide a wide range of products and services, and lack a specific charter that is exclusively focused on agriculture. These differences between FCS lenders and other types of lenders, which the CFPB did not meaningfully address in the 2023 final rule, make it difficult to easily compare loans made by FCS lenders with those of other non-cooperative lenders.

In addition to their unique nature and mission, as described above, FCS lenders are also already subject to an existing regulatory reporting framework through the FCA, including the collection of demographic data as part of its program oversight.[35]

In issuing the 2023 final rule, the Bureau explained the decision not to categorically exempt any specific type of financial institution from the rule's coverage, stating that such exemptions “would create significant gaps in the data and would create an uneven playing field between different types of institutions.” [36]

The CFPB did not appear to meaningfully consider the extent to which FCS lending differs in kind from general-purpose lending.

However, in light of the CFPB's reconsideration of the 2023 final rule and new focus on ensuring the consistent and smooth initial collection of data from core lenders and products, the CFPB believes it would further the purposes of section 1071 to commence the data collection without including FCS lenders.

The existing reporting requirements of FCS lenders further supports excluding FCS lenders.[37]

Moreover, requiring compliance with a second set of potentially redundant reporting obligations may put FCA lenders at a competitive disadvantage relative to other lenders.

The CFPB believes that the rule's current application to FCS lenders risks imposing disproportionate regulatory complexity on them, many of which are small, rural cooperatives lacking the compliance infrastructure of large commercial lenders, which in turn risks diminishing the quality of the data they report to CFPB. Adding potentially redundant reporting requirements would do little to advance the goals of section 1071. Such a result would be counter to the Congressional goals behind the establishment of the FCS.

Based on the factors discussed above, the CFPB believes it would be appropriate to reconsider the rule's application to FCS lenders and to focus the rule's scope on conventional, general-purpose small business lending. Accordingly, the Bureau proposes to use its exemption authority under 15 U.S.C. 1691c-2(g)(2) to exclude FCS lenders.

The CFPB seeks comment on this proposed revision to the rule.

Current § 1002.105(b) defines a covered financial institution as one that has made at least 100 covered credit transactions to small businesses in each of the two preceding calendar years. The CFPB is proposing to change this definition by increasing this threshold from 100 covered credit transactions to 1,000 covered credit transactions because it believes that it would advance the statutory purposes of section 1071 to commence the data collection without including smaller lenders under a 1,000 originations threshold.

In the 2023 final rule, the CFPB explained its belief that a 100-loan origination threshold would best address widespread industry concerns regarding compliance burdens for the smallest financial institutions while also

( printed page 50959)

capturing the overwhelming majority of the small business lending market. It noted that while its original proposal of a 25-loan threshold would have yielded more data than a 100-loan threshold, the 100-loan origination threshold “massively expands data availability relative to the status quo.” [38]

The CFPB noted that a number of commenters on the 2021 proposed rule requested a higher threshold, such as 1,000 covered credit transactions. At that time, the CFPB was concerned that a threshold higher than 100 covered credit transactions would dramatically reduce the number of covered financial institutions that must report data under the rule. However, as the CFPB noted in the 2023 final rule, a large decrease in the number of covered financial institutions does not equate to a proportionately large reduction in the estimated number of small business credit applications reported.

As a result, the CFPB believes that the proposed 1,000 originations threshold is justified for several independent reasons. First, the CFPB believes that at the onset of the data collection under section 1071 the focus should be on core lenders and products before the CFPB considers whether it would be appropriate to expand the scope of the rule. The CFPB believes that larger volume lenders are core to small business lending. Current § 1002.114(b), by way of comparison, prioritized the collection of data from the largest volume lenders first because they have more resources, and because they account for the bulk of small business lending volume.[39]

Second, the proposed change better aligns with E.O. 14192,[40]

which directs Federal agencies to review regulations for regulatory burden, and is responsive to feedback received from stakeholders following publication of the 2023 final rule. The CFPB has heard repeatedly from industry stakeholders that its estimates in the 2023 final rule were wrong, and that a 100-loan origination threshold is too low and captures too many smaller institutions, which they say originate fewer small business loans and also are less able to shoulder the costs and complexity of complying with the rule due to fewer resources and staff.

The Bureau preliminarily determines that changing the originations threshold to 1,000 strikes a better balance by minimizing complexity for smaller entities while still collecting data on a large proportion of small business credit applications; indeed, as the Bureau observed with respect to the 100-loan threshold in the 2023 final rule, a 1,000-loan threshold would substantially increase data availability as compared to the status quo.

The CFPB believes a threshold of 1,000 originations, instead of 100, would be congruent with the statutory purposes of section 1071. The CFPB believes that the onset of data collection should commence with core products and lenders, as larger lenders are better resourced and can better sustain the complexities and cost of compliance with the rule. The CFPB believes that it should work with larger lenders to better understand potential difficulties associated with collecting data before considering whether to expand the rule to require that smaller lenders comply with the rule.

Further, the CFPB also notes from its research that the proposed change in the threshold for originations would result in a reduction in the number of smaller institutions covered by the rule without a proportionately large reduction in the number of loan application-level data collected by the rule.[41]

While the proposed 1,000 originations threshold would carve out a large number of mostly smaller depository institutions, the rule would still cover the vast majority of small business loan originations (well over 90 percent).

Given this the CFPB believes increasing the threshold would remove regulatory burden from small entities, and therefore the proposed change would be responsive to E.O. 14192.

The CFPB believes that increasing the threshold is necessary or appropriate to carry out the purposes of section 1071 because the complexity of compliance may pose difficulties for smaller lenders, many of which have no previous experience at all with data collection rules such as HMDA or CRA. The new compliance complexity may result in decreased data quality for those institutions, which would not advance the statutory purposes of section 1071.

The proposed change to § 1002.105(b) would, in turn, require other changes. Current § 1002.112(b) provides that a bona fide error is not a violation of ECOA or Regulation B, subpart B. The provision cross-references numerical error thresholds in current appendix F. Under appendix F, a financial institution is presumed to maintain procedures reasonably adapted to avoid errors with respect to a given data field if the number of errors found in a random sample of a financial institution's data submission for a given data field do not equal or exceed the threshold in column C of table 1 of appendix F.

The CFPB proposes revising appendix F to conform to the proposed changes to § 1002.105(b), defining “covered financial institution,” based on a revised origination threshold of 1,000 covered credit transactions. Specifically, column A of existing appendix F lists ranges of small business lending application register counts. The CFPB proposes eliminating the rows in table 1 associated with application counts under 1,000, and revising the count in what is currently the 4th row to be “1,000-100,000” rather than the current “500-100,000.” The CFPB requests comment on these proposed changes.

The CFPB seeks comment on this proposed revision to the rule, in particular whether an originations threshold at 200, 500, 2,000, or some other number would be appropriate, and whether the associated changes to appendix F are appropriate.

D. Section 1002.106—Business and Small Business

106(b) Small Business

Current § 1002.106(b)(1) defines “small business” and provides, among other criteria, that a business is small if its gross annual revenue for its preceding fiscal year is $5 million or less. Section 1002.106(b)(2) provides procedures for inflation adjustments to that threshold. For the reasons discussed below, the CFPB is proposing to reduce the gross annual revenue threshold from $5 million or less to $1 million or less.

In the 2023 final rule, the CFPB explained that its definition reflected the need for financial institutions to apply a simple, broad definition of a small business across industries. It also explained its belief that a $5 million gross annual revenue threshold strikes the right balance in terms of broadly covering the small business financing market while meeting the SBA's criteria for an alternative size standard. It noted that it did not propose a $1 million gross annual revenue threshold out of concern that such a threshold likely would not satisfy the SBA's requirements for an alternative size standard across industries, while also observing that a $1 million threshold would better align with existing Regulation B adverse action notification requirements. It also concluded that a $1 million threshold would exclude many businesses that should be characterized as small.

The CFPB will retain the use of a simple, broad definition of a small business across industries but is

( printed page 50960)

proposing to change the gross annual revenue threshold from $5 million or less to $1 million or less, and to make conforming changes throughout the regulatory text and commentary. The CFPB is seeking SBA approval for this alternate small business size standard pursuant to the Small Business Act.[42]

Since the 2023 final rule was published, the President issued E.O. 14192.[43]

As part of the CFPB's review of the 2023 final rule under this order, the CFPB identified that a $1 million threshold would help reduce regulatory burden on financial institutions because it would better align with other existing financial regulatory requirements and standard financial industry practices related to small businesses.

Specifically, the CFPB believes several independent reasons justify a change of the gross annual revenue threshold to $1 million. First, as noted by commenters on the CFPB's 2021 proposed rule, a $1 million threshold would align with certain metrics in CRA regulations. Several CRA tests analyze lending to “smaller businesses” with $1 million or less in revenues.[44]

The CFPB finalized the $5 million threshold in the 2023 final rule, and the Federal agencies responsible for implementing the CRA proposed and subsequently finalized amendments to their small business revenue threshold to $5 million, to conform with the CFPB's rule implementing section 1071, and to use data collected pursuant to that rule. Since then, however, the CRA agencies have proposed withdrawing those revisions, which never entered into force. The CRA agencies proposed reverting back to a $1 million or less definition, and no longer using section 1071 data in certain CRA tests concerning small businesses.[45]

The CFPB believes that it should follow suit to reduce avoidable regulatory complexity for regulated entities by sharing where possible a uniform size standard with other Federal agencies.

Second, the CFPB also believes that the revised threshold in proposed § 1002.106(b) would be more consistent with Regulation B, subpart A, further helping to reduce regulatory burden pursuant to E.O. 14192.[46]

As noted in the 2023 final rule, Regulation B, subpart A uses a $1 million revenue threshold to determine what kind of adverse action notice a business credit applicant receives; those under the threshold receive a notification similar to one a consumer would receive.[47]

As a result, many covered financial institutions likely already apply a $1 million threshold to determine which businesses are small. Here, the CFPB believes that using an existing size standard would reduce regulatory complexity for covered financial institutions.

Third, as many financial institutions have worked on implementing the 2023 final rule, the Bureau has received more feedback, including from a number of community banks and trade groups representing larger institutions, that a $1 million revenue threshold would more closely align with their internal thresholds that separate small and medium-sized businesses within their own institutions.

The CFPB notes that the 2023 final rule adopted a $5 million threshold in significant part because it believed that a $1 million threshold, discussed as an alternative to the $5 million threshold, would not satisfy the SBA's requirements for an alternative size standard and would exclude too many businesses designated as small under the SBA's size standards. Whether an alternative size standard satisfies the requirements for an alternative size standard is within the SBA's purview to determine, and as noted above the CFPB is seeking SBA approval for its proposed $1 million threshold.

Further, as commenters initially stated, a $1 million threshold would cover most (over 95 percent) of small businesses as defined by the SBA size standards in effect at the time of the 2021 proposed rule. The CFPB estimated in the 2023 final rule that among non-agricultural industries over 1.5 million small businesses (27 percent) would not be covered by an alternative $1 million gross annual revenue threshold.[48]

The CFPB is now reconsidering the data provided by commenters and its final rule estimate. In any case, the CFPB believes that a change to $1 million is consistent with the alignment goals noted above given the E.O.s discussed throughout, even if a 27 percent decline in small business coverage would result. At a $1 million threshold, the proposed rule would still cover a supermajority of small businesses that the 2023 final rule covers.

The CFPB is proposing conforming changes also to the inflation adjustment provision in § 1002.106(b)(2), to require adjustment in $100,000 increments (rather than $500,000) every five years after 2030 (rather than 2025). The CFPB is concerned that, given the proposed change to a $1 million revenue threshold, inflation adjustments in $500,000 increments would not be granular enough for this provision to meaningfully track inflation.

The Bureau seeks comment on the proposed changes to § 1002.106(b)(1) and (b)(2), including whether revenue thresholds of $500,000, $2 million, $3 million, or some other amount would be appropriate.

E. Section 1002.107—Compilation of Reportable Data

107(a) Data Format and Itemization

107(a) Discretionary Data Points

Section 1071 provides for two types of data points, those statutorily required under ECOA section 704B(e) and those promulgated based on Bureau discretion provided for in ECOA section 704B(e)(2)(H), which are sometimes referred to as discretionary data points, and which the Bureau has authority to add if the “Bureau determines [they] would aid in fulfilling the purposes of this section.” In the 2023 final rule, the Bureau finalized several discretionary data points, determining the additional data would aid in fulfilling the purposes of section 1071 of the Dodd-Frank Act, as required by ECOA section 704B(e)(2)(H). The discretionary data points were for pricing information, time in business, North American Industry Classification System (NAICS) code, number of workers, application method, application recipient, denial reasons, and number of principal owners. The Bureau considered the additional operational complexity and

( printed page 50961)

potential reputational harm described by commenters that collecting and reporting these data points could impose on financial institutions, but determined that the costs were only incremental and that the data points were designed to minimize additional compliance burden.[49]

Notably, in the 2023 final rule the Bureau declined to add other discretionary data points sought by commenters, because the decision whether to include a discretionary data point necessarily also involves considering the relative utility of a data point and the operational complexity of adding it. For that reason, in 2023 the Bureau stated that it was adopting a “limited number of data points . . . that it believes will offer the highest value in light of section 1071's statutory purposes,” and it rejected additional data points on the grounds that they would pose “operational complexities.” [50]

For example, the Bureau declined to include a data point on credit scores, even though the data would be useful for fair lending analyses, due to the complexity and operational difficulty of doing so.[51]

In other words, to be included as a discretionary data point, a data point implicitly must satisfy two independent tests: (1) whether the data point would aid in fulfilling the purposes of section 1071,

and

(2) whether the CFPB believes based on the record before it that it is appropriate to adopt as a discretionary data point given factors such as operational cost and regulatory complexity. Accordingly, if the Bureau now believes that the relative utility of the data is not strong enough to justify the additional operational complexity for financial institutions, that is sufficient reason to propose removing the discretionary data point, even if the discretionary data point would otherwise advance the purposes of the statute.

After the publication of the 2023 final rule, two factors prompted reconsideration of the discretionary data points by the Bureau. First, as discussed above, pursuant to E.O.s. 14192 and 14219 (“Ensuring Lawful Regulation and Implementing the President's `Department of Government Efficiency' Deregulatory Agenda”), the Bureau is reviewing the 2023 final rule as part of its effort to streamline and simplify regulations.[52]

The Bureau believes that removing some of the discretionary data points would meet the goals of these E.O.s. Second, subsequent to the publication of the 2023 final rule and through the implementation process, the Bureau received additional feedback about the number of data points total, and the logistical challenges associated with implementing some or all of the discretionary data points. The implementation feedback provided by stakeholders further supports reconsideration of certain discretionary data points, and the Bureau now believes that the 2023 final rule did not adequately consider the extent to which the value of the data point justifies the additional operational complexity in obtaining it.

Given this new information, the Bureau proposes to remove the discretionary data points for application method, application recipient, denial reasons, pricing, and number of workers in § 1002.107(a)(3), (4), (11), (12), (16), as well as the relevant commentary, and to make conforming changes throughout.

The data points identified for removal are not statutorily required and are not otherwise relied upon by or intertwined with the statutorily required data points.[53]

In any case, because the identified data points were finalized pursuant to the Bureau's discretionary authority under 15 U.S.C. 1691c-2(e)(2)(H), it is also within the bounds of that discretion to remove these data points. The CFPB believes that their removal at this time, at the start of a potentially long-term data collection regime, would advance the longer-term statutory purposes of the rule. Stakeholders attempting to implement the rule have suggested the addition of data points beyond those statutorily required had led to unnecessary complexity in implementing the 2023 final rule, and that such complexity might reduce data quality and lead to additional errors. The CFPB preliminarily concludes that initiating the data collection with an expansive rule that covered more data points would tend to make the initial collections more complicated and result in lesser data quality and integrity.

The CFPB believes it prudent to focus on the collection of a more limited number of core data points (the statutory data points and a limited number of other data points needed to facilitate the collection of these statutory data points) to avoid complexity in the initial implementation of a rule to implement section 1071. This in turn would make it more likely that covered financial institutions face a smoother transition in the initial years of the rule in ramping up to the accurate, recurring collection of data.[54]

Application method.

The 2023 final rule required financial institutions to collect data on whether applications were submitted in person, by phone, online, or by mail. It explained its belief that this data will improve the market's understanding of how different types of applicants apply for credit and provide additional context for the business and community development needs of particular geographic regions. The Bureau now believes that this information is of relatively low value in furthering the purposes of section 1071 while adding to the overall complexity of a lengthy data collection, and thus should not be included. Upon reconsideration, the Bureau believes that in the 2023 final rule, it had underestimated the potential complexity of this data point. The Bureau acknowledged that many lenders do not already collect this data point as such, and that many small business applicants have multiple interactions across the different methods listed (in-person, telephone, online) during the application process. However, current § 1002.107(a)(3) does not seem to address this but rather appears to reduce the potentially complex set of interactions to identifying only one means of collecting a covered application. The logic of the 2023 final rule justifying this provision suggests the futility of collecting this data point without capturing the full scope of interaction between applicant and lender for purposes of this rule. The Bureau believes, as a result, that at this time, this data point should be removed because its utility does not outweigh the cost and complexity of collecting it.

Application recipient.

In the 2023 rule, the Bureau required financial institutions to collect data on application method—whether the applicant submitted the covered application directly to the financial institution or its affiliate, or whether the applicant submitted the covered application indirectly to the financial institution via a third party. It explained

( printed page 50962)

that this discretionary data point will improve the market's understanding of how small businesses interact with financial institutions when applying for credit, such as whether financial institutions making credit decisions are directly interacting with the applicant and/or generally operating in the same community as the applicant. The Bureau now believes that this information is of relatively low value in furthering the purposes of section 1071 while adding to the overall complexity of a lengthy data collection. Upon reconsideration, the Bureau believes that in the 2023 final rule, it overestimated the utility and underestimated the cost and complexity of this data point. The justification for this data point in the 2023 final rule suggested that it would help determine whether lenders were operating in the communities with applicants but did not offer details on why a data point on third-party submissions would advance such an understanding, above and beyond the other data points more apparently targeted to identify community development needs, such as census tract. Further, in response to a comment that lenders do not track data on application submissions by third parties because such data played no role in underwriting decisions, the Bureau summarily replied that it did not believe it would be difficult for lenders to track this information. The Bureau believes that submissions through third parties may not always be identified as such, and that its statement in the 2023 final rule justifying the inclusion of this data point did not account for this. The Bureau as a result believes that at the start of a potentially long-term data collection regime that this data point should be removed.

Denial reasons.

The Bureau explained in the 2023 rule that data on denial reasons will allow data users to better understand the rationale behind denial decisions, help identify potential fair lending concerns, and provide financial institutions with data to evaluate their business underwriting criteria and address potential gaps as needed. As the Bureau acknowledged in the 2023 rule, reasons for denial data could be harmful or sensitive for applicants or related natural persons. The Bureau now believes that the sensitivity of this information, combined with its addition to the overall complexity of a lengthy data collection, justifies proposing to remove it from the discretionary data points. The 2023 final rule did not explain how the marginal or added usefulness of denial reasons would justify the added cost and complexity above and beyond the collection of data on denials, already captured by the mandatory “type of action taken” data point. Further, to the extent that this data point was intended to assist lenders to analyze their own fair lending concerns, as the 2023 final rule stated, the data point is redundant as lenders already possess this information. To the extent that this data point was intended to assist applicants, under subpart A of Regulation B they are already able to access a statement of denial reasons. Section 1002.9(a)(3) in subpart A already requires lenders to inform applicants for business credit with $1 million or less in gross annual revenue of their right to receive a statement of denial reasons upon request. Upon reconsideration, the Bureau believes that it is sufficient at this time to collect data on denials via the action taken data point, as required under 15 U.S.C. 1691c-2(e)(2)(D), and that this data point should not be included at the start of a potentially long-term data collection regime.

Pricing.

In the 2023 rule, the Bureau required reporting of an array of different pricing data: interest rate; total origination charges; broker fees; the total amount of all non-interest charges that are scheduled to be imposed over the first annual period; for a merchant cash advance or other sales-based financing transaction, the difference between the amount advanced and the amount to be repaid; and information about any applicable prepayment penalties. It explained its belief that because price-setting is integral to the functioning of any market, any analysis of the small business lending market—including to enforce fair lending laws or identify community and business development opportunities—would be less meaningful without this information. The 2023 rule acknowledge the potential complexity of collecting this data, and commenters noted the risk that it could reveal confidential business information or lead to incorrect inferences about discrimination. The Bureau now believes that the potential risk of harm to applicants and the substantial complexity of the data collection justify removing it from the discretionary data points. While the Bureau acknowledged comments “about the harmful consequences of potentially misleading data,” the Bureau addressed this concern in the 2023 final rule by stating that it would note “when disclosing the 1071 data that the data alone generally do not offer proof of compliance with fair lending laws.” [55]

The Bureau upon reconsideration believes that such a statement may not be sufficient to address concerns about the misuse of pricing data. In adopting the pricing data point, the Bureau assumed that community groups would use data responsibly but did not address how other members of the public with access to the data might use it.[56]

Further, the 2023 final rule stated that “the 1071 data need not reflect every determinant of credit pricing to provide value to users” but also acknowledged the relevant and importance of credit score of principal owners to “explain[] pricing differences between transactions.” [57]

That is, the Bureau believes that the publication of pricing information absent certain other information may be incomplete and give rise to incorrect inferences concerning discrimination; however, the collection of sufficient data points to correct potentially erroneous inferences may make the data collection unduly complex. This combination of difficulties leads the Bureau to believe that this data point should not be included at the start of a potentially long-term data collection regime.

Number of workers.

The 2023 rule required financial institutions to report the number of workers in ranges, and stated that data on the number of persons working for a small business applicant will provide data users and relevant stakeholders with a better understanding of the job maintenance and creation that small business credit provides. The Bureau now believes that this information is of relatively low value in furthering the purposes of section 1071 while adding to the overall complexity of a lengthy data collection. First, in the 2023 final rule, the Bureau acknowledged that “[t]he majority of small businesses are run by a single owner.” Given the proposed change to § 1002.106(b), revising the definition of small business to those businesses with $1 million or less in gross annual revenue, fewer small businesses with employees would be covered under the rule. Second, as acknowledged in the 2023 final rule, small businesses may encounter difficulties in providing this information to financial institutions, especially small businesses that use contractors, temporary or gig workers, or seasonal workers, or those that cycle through employees frequently. While the Bureau simplified a covered financial institution's reporting requirements for this data point, the Bureau believes that even as simplified this data point's complexity outweighs its potential utility. That is, the Bureau

( printed page 50963)

now believes that it would be difficult to ensure consistency in reporting this data point across a variety of different small business applicants, making it likely that the data collected would be of poor quality or otherwise difficult to interpret. Further, the 2023 final rule justified this data point solely on community development grounds. It did not justify this data point on fair lending grounds because nothing in Regulation B, including subpart A, offers differential protection based on a business credit applicant's number of workers. Based on the Bureau's intention to commence this rulemaking regime focused on truly small businesses, the Bureau believes that this data point should not be included at the start of a potentially long-term data collection regime as it is not likely to result in the collection of useful data at this time.

LGBTQI+-owned business status.

The 2023 rule required financial institutions to inquire whether a small business applicant for credit is a minority-owned, women-owned, and/or LGBTQI+-owned business. This discretionary data point is addressed in more detail below in the section on the Defending Women E.O.

The Bureau solicits comment on these proposed changes, including whether any of the identified discretionary data points should be modified or retained, in part or in full.

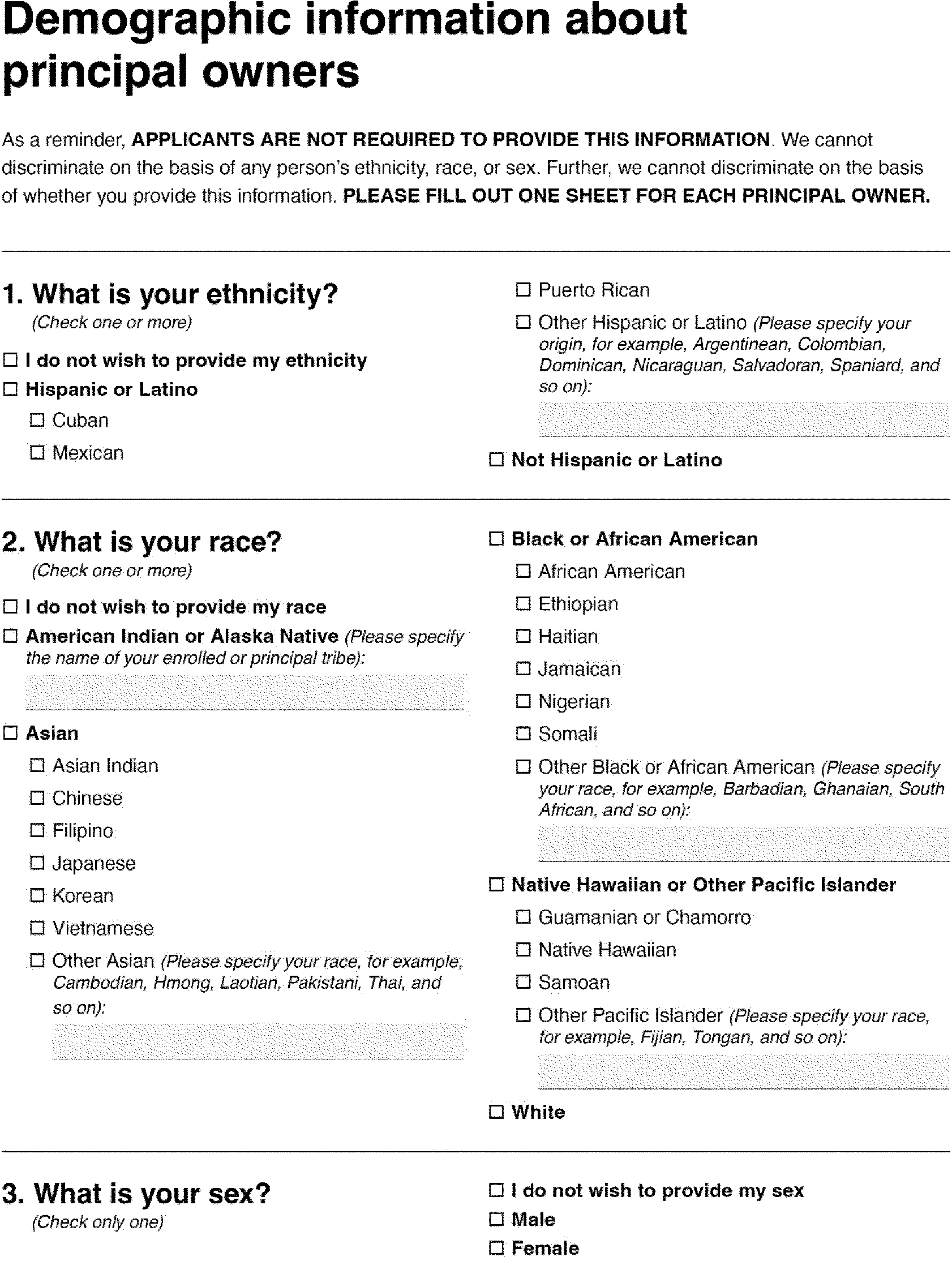

Collection of Disaggregated Ethnicity and Race Categories

Current § 1002.107(a)(19) requires the collection of both aggregate and disaggregated race and ethnicity information on principal owners of small business applicants. However, 15 U.S.C. 1691c-2(e)(2)(G) only requires covered lenders to collect and report the “race, sex, and ethnicity of the principal owners of the business.” This statutory provision does not explicitly call for the collection of disaggregated data on the race and ethnicity of principal owners. Given its concern about commencing a long-term data collection regime by asking for potentially complex and costly data points, the Bureau seeks comment on whether it should revise the rule's data collection requirements to require collection only of aggregate ethnicity and race categories.

As a result, and consistent with its reconsideration of discretionary data points, the Bureau also seeks specific comment on what utility there might be for carrying out the purposes of section 1071 in requiring the collection of disaggregated categories of ethnicity and race, in addition to the aggregate categories. The Bureau also seeks comment on the costs and burdens for financial institutions in requiring the collection of these disaggregated categories of ethnicity and race.

Defending Women E.O.

LGBTQI+-ownership.

Current § 1002.107(a)(18) requires financial institutions to inquire whether a small business applicant for credit is a minority-owned, women-owned, and/or LGBTQI+-owned business. The Bureau explained that, based on limited information available, it believed that LGBTQI+-owned businesses may experience particular challenges accessing small business credit, and used its discretionary authority under 15 U.S.C. 1691c-2(e)(2)(H) to require financial institutions to request information about whether an applicant is a LGBTQI+-owned business. In the time since the 2023 rule, the Bureau has heard repeated concerns from stakeholders, as well as members of Congress and the general public, that this question in particular is an invasion of privacy and risks damaging the relationship between small businesses and their lenders, particularly in smaller lending markets. The Bureau now believes that the sensitivities involved in this inquiry, which the 2023 rule did not address, exceed any utility this data point might provide, and that it adds to the overall complexity of a lengthy data collection.[58]

In addition, the President issued the Defending Women E.O. (E.O. 14168) on January 30, 2025, which directs Federal agencies seeking information not to discuss gender identity and to refer to sex using a binary of male/female. Consistent with this E.O. and the feedback the Bureau received from stakeholders and members of Congress and the general public described above, the Bureau is proposing to make certain conforming changes to the rule and remove or rescind provisions in the current rule that do not comply with the order. These changes generally would include (1) removing references to and questions about “LGBTQI+”-owned business status, (2) requiring financial institutions to inquire about a principal owner's sex, rather than sex/gender, and (3) providing that the sex of the principal owners be selected from a static binary response option of male/female, rather than a free-form text field.

Specifically, the proposed changes would include removing the definition related to LGBTQI+-owned business status in § 1002.102(k) and (l) and removing references to LGBTQI+-owned business status in § 1002.107(a)(18) and (19) and associated commentary, and revising how principal owners' sex is to be collected in commentary accompanying § 1002.107(a)(19). The proposed changes would also include removing references to LGBTQI+-owned business status in Regulation B, subpart A, § 1002.5(a)(4) and revising commentary accompanying § 1002.5(a)(2). The Bureau is also proposing to make conforming changes elsewhere throughout the regulatory text and associated commentary, as well as the sample form in appendix E.

The Bureau seeks comment on these proposed changes.

Sex/gender.

Current § 1002.107(a)(19) requires financial institutions to ask a small business applicant to provide its principal owners' ethnicity, race and sex. Associated commentary further explains how financial institutions are to make these requests. Commentary to current § 1002.107(a)(19) requires financial institutions, when requesting principal owners' sex, to use the term “sex/gender” and to give applicants a free-form text field to provide a response.

Commentary accompanying current § 1002.107(a)(19) requires financial institutions, when requesting principal owners' sex, to use the term “sex/gender” and to give applicants a free-form text field to provide a response. In the 2023 rule, the Bureau explained its belief that this approach would allow applicants to self-identify as they see fit. Commenters had contended, however, that the free-form text approach would inhibit data analysis.