Department of Justice

Antitrust Division

Notice is hereby given pursuant to the Antitrust Procedures and Penalties Act, 15 U.S.C. 16(b)-(h), that a proposed Final Judgment, Stipulation, and Competitive Impact Statement have been filed with the United States District Court for the Middle District of North Carolina in United States of America et al. v. RealPage, Inc. et al., Civil Action No. 1:24-cv-00710. On January 7, 2025, the United States filed a Complaint alleging that RealPage, Inc., along with six landlords, violated Section 1 of the Sherman Act, 15 U.S.C. 1, by unlawfully agreeing to share and use landlords' competitively sensitive information and agreeing to use RealPage's software to align pricing among competing landlords. The Complaint also alleges that RealPage violated Section 2 of the Sherman Act, 15 U.S.C. 2, by monopolizing or attempting to monopolize the commercial revenue management software market for conventional multifamily rental housing by preventing other software providers from effectively competing with products that do not harm the competitive process. The proposed Final Judgment, filed on November 24, 2025, seeks to stop the exchange of competitively sensitive data among competing landlords through RealPage and to deter exchanges of such data by other means, such as in revenue management meetings attended by competitors. RealPage must also ensure that certain features of RealPage's revenue management software do not facilitate an alignment of pricing among competing landlord users. RealPage must establish an antitrust compliance policy and cooperate with the United States in this litigation.

Copies of the Complaint, proposed Final Judgment, and Competitive Impact Statement are available for inspection on the Antitrust Division's website at https://www.justice.gov/atr and at the Office of the Clerk of the United States District Court for the Middle District of North Carolina. Copies of these materials may be obtained from the Antitrust Division upon request and payment of the copying fee set by Department of Justice regulations.

Public comment is invited within 60 days of the date of this notice. Such comments, including the name of the submitter, and responses thereto, will be posted on the Antitrust Division's website, filed with the Court, and, under certain circumstances, published in the Federal Register . Comments should be submitted in English and directed to Danielle Hauck, Acting Chief, Technology and Digital Platforms Section, Antitrust Division, Department of Justice, 450 Fifth Street NW, Suite 7100, Washington, DC 20530 (email address: ATR.Public-Comments-Tunney-Act-MB@usdoj.gov).

Suzanne Morris,

Deputy Director Civil Enforcement Operations, Antitrust Division.

In The United States District Court for the Middle District of North Carolina

UNITED STATES OF AMERICA, U.S. Department of Justice, Antitrust Division, 950 Pennsylvania Avenue NW, Washington, DC 20530, STATE OF NORTH CAROLINA, 114 W Edenton Street, Raleigh, NC 27603, STATE OF CALIFORNIA, 300 South Spring Street, Suite 1702, Los Angeles, CA 90013, STATE OF COLORADO, 1300 Broadway, 7th Floor, Denver, CO 80203, STATE OF CONNECTICUT, 165 Capitol Avenue, Hartford, CT 06106, STATE OF ILLINOIS, 115 S LaSalle St., Floor 23, Chicago, IL 60603, COMMONWEALTH OF MASSACHUSETTS, One Ashburton Place, 18th Floor, Boston, MA 02108, STATE OF MINNESOTA, 445 Minnesota Street, St. Paul, MN 55101, STATE OF OREGON, 100 SW Market St., Portland, OR 97201, STATE OF TENNESSEE, P.O. Box 20207, Nashville, TN 37202, and STATE OF WASHINGTON, 800 Fifth Avenue, Suite 2000, Seattle, WA 98104-3188, Plaintiffs, v. REALPAGE, INC., 2201 Lakeside Blvd., Richardson, TX 75082, CAMDEN PROPERTY TRUST, 11 Greenway Plaza, Ste. 2400, Houston, TX 77046, CORTLAND MANAGEMENT, LLC, 3424 Peachtree Rd., Ste. 300, Atlanta, GA 30326, CUSHMAN & WAKEFIELD, INC., 225 W Wacker Dr., Ste. 3000, Chicago, IL 60606, GREYSTAR REAL ESTATE PARTNERS, LLC, 465 Meeting St., Ste. 500, Charleston, SC 29403, LIVCOR, LLC, 233 South Wacker Dr., Ste. 4700, Chicago, IL 60606, PINNACLE PROPERTY MANAGEMENT SERVICES, LLC, 2401 Internet Blvd., Ste. 110, Frisco, TX 75034, and WILLOW BRIDGE PROPERTY COMPANY, LLC, 2000 McKinney Ave., Ste. 1100, Dallas, TX 75201, Defendants.

AMENDED COMPLAINT

Case No. 1:24-cv-00710-LCB-JLW

JURY TRIAL DEMANDED

Table of Contents

I. Introduction

II. RealPage's Revenue Management Software Is Fueled by Nonpublic, Competitively Sensitive Information Shared by Landlords

A. Landlords Agree To Share Nonpublic, Competitively Sensitive Transactional Data With RealPage for Use in Generating Competitors' Pricing Recommendations

B. AIRM and YieldStar Users Agree With RealPage To Use the Software To Align Pricing

C. RealPage's Transactional Data Is Fundamentally Different From Other Data Available to Landlords

D. RealPage Revenue Management Software Uses Nonpublic, Competitively Sensitive Data To Recommend Prices

1. AIRM and YieldStar Leverage Competitively Sensitive Data To Generate Price Recommendations

(a) AIRM Model Training Relies on Competitively Sensitive Data To Generate Learned Parameters

(b) AIRM and YieldStar Incorporate Competitors' Nonpublic Data To Generate Floor Plan Price Recommendations

(c) AIRM and YieldStar Use Competitors' Nonpublic Data—Including Data on Future Occupancy—To Determine Unit-Level Prices

2. LRO Relies Primarily on Landlords To Input Data on Competitors

E. RealPage Uses Multiple Mechanisms To Increase Compliance With Price Recommendations

1. AIRM and YieldStar Make It Easy To Accept Recommendations and More Difficult and Time-Consuming To Decline

2. RealPage Pushes Clients To Adopt Auto-Accept Settings That Automatically Approve Recommendations

3. RealPage Pricing Advisors Provide a “Check and Balance” on Property Managers To Increase Acceptance of Recommendations

4. Pricing Recommendations Heavily Influence Landlords' Behavior

III. Coordination Among Competing Landlords is a Feature of This Industry

A. Rental Housing is a Necessity for Millions of Americans

B. The Multifamily Property Industry Is Rife With Cooperation Among Ostensible Competitors

1. At the Local Level, the Multifamily Property Industry Comprises a Small Number of Large Landlords Managing Buildings With Different Owners

2. Landlords Regularly Discuss Competitively Sensitive Topics With Their Competitors and Swap Information

3. At RealPage User Group Meetings, Landlords Discuss Competitively Sensitive Topics

C. RealPage Uses Nonpublic Information To Allow Landlords To More Easily Compare Units on an Apples-to-Apples Basis

IV. RealPage Harms the Competitive Process and Renters By Entering Into Unlawful Agreements With Landlords To Share and Exploit Competitively Sensitive Data

A. AIRM and YieldStar Have the Purpose and Effect of Distorting the Competitive Pricing of Apartments

B. AIRM and YieldStar Impose Multiple Guardrails Intended To Artificially Keep Prices High or Minimize Price Decreases

C. AIRM and YieldStar Harm the Competitive Process by Discouraging the Use of Discounts and Price Negotiations

D. AIRM and YieldStar Increase and Maintain Landlords' Pricing Power by ( printed page 56287) Using Competitors' Data To Manage Lease Expirations

E. No Procompetitive Benefit Justifies, Much Less Outweighs, RealPage's Use of Competitively Sensitive Data To Align Competing Landlords

V. RealPage Uses Landlords' Competitively Sensitive Data To Maintain Its Monopoly and Exclude Commercial Revenue Management Software Competitors

A. Landlords Are Drawn to RealPage Because of Access to Nonpublic Transactional Data That Is Used To Increase Landlords' Revenue

B. RealPage's Collection and Use of Competitively Sensitive Data Excludes Competition in Commercial Revenue Management Software

VI. Relevant Markets

A. Conventional Multifamily Rental Housing Markets

1. Product Markets

(a) Conventional Multifamily Rentals Are Distinct From Other Types of Multifamily Housing

(b) Single-Family Housing Is Not a Reasonable Substitute to Multifamily Rentals

(c) Conventional Multifamily Rental Units With Different Bedroom Counts Are Relevant Product Markets

2. Geographic Markets

(a) RealPage-Defined Submarkets Identify Relevant Geographic Markets

(b) Core-Based Statistical Areas (CBSAs) Are Relevant Geographic Markets

B. Commercial Revenue Management Software Market

1. Product Market

2. Geographic Market

VII. Jurisdiction, Venue, and Commerce

VIII. Violations Alleged

IX. Request for Relief

X. Demand for a Jury Trial

Appendix A: Submarkets

Appendix B: Submarkets By Bedroom Count

I. Introduction

1. Renters are entitled to the benefits of vigorous competition among landlords. In prosperous times, that competition should limit rent hikes; in harder times, competition should bring down rent, making housing more affordable. RealPage has built a business out of frustrating the natural forces of competition. In its own words, “a rising tide raises all ships.” This is more than a marketing mantra. RealPage sells software to landlords that collects nonpublic information from competing landlords and uses that combined information to make pricing recommendations. In its own words, RealPage “ helps curb [landlords'] instincts to respond to down-market conditions by either dramatically lowering price or by holding price when they are losing velocity and/or occupancy. . . . Our tool [ ] ensures that [landlords] are driving every possible opportunity to increase price even in the most downward trending or unexpected conditions ” (emphases added).

2. In fact, as RealPage's Vice President of Revenue Management Advisory Services described, “ there is greater good in everybody succeeding versus essentially trying to compete against one another in a way that actually keeps the entire industry down” (emphasis added). As he put it, if enough landlords used RealPage's software, they would “ likely move in unison versus against each other ” (emphasis added). To RealPage, the “greater good” is served by ensuring that otherwise competing landlords rob Americans of the fruits of competition—lower rental prices, better leasing terms, more concessions. At the same time, the landlords enjoy the benefits of coordinated pricing among competitors.

3. RealPage replaces competition with coordination. It substitutes unity for rivalry. It subverts competition and the competitive process. It does so openly and directly—and American renters are left paying the price.

4. Americans spend more money on housing than any other expense. On average, American households allocate more than one-third of their monthly income to housing. Some purchase a home, while others choose to, or must, rent. A family's selection of an apartment reflects a complex set of values and criteria including comfort, safety, access to schools, convenience, and critically, affordability. To ensure they secure the greatest value for their needs, renters rely on robust and fierce competition between landlords.

5. RealPage distorts that competition. Across America, RealPage sells landlords commercial revenue management software. RealPage develops, markets, and sells this software to enable landlords to sidestep vigorous competition to win renters' business. Many of the largest landlords in the United States, including Greystar, Camden, Cortland, Cushman & Wakefield and Pinnacle, LivCor, and Willow Bridge (collectively, Defendant Landlords), which would otherwise be competing with each other, submit or have submitted on a daily basis their competitively sensitive information to RealPage.[1] This nonpublic, material, and granular rental data includes, among other information, a landlord's rental prices from executed leases, lease terms, and future occupancy. RealPage collects a broad swath of such data from competing landlords, combines it, and feeds it to an algorithm.

6. Based on this process and algorithm, RealPage provides daily, near real-time pricing “recommendations” back to competing landlords. These recommendations are based on the sensitive information of their rivals. But these are more than just “recommendations.” Because, in its own words, a “rising tide raises all ships,” RealPage monitors compliance by landlords to its recommendations. RealPage also reviews and weighs in on landlords' other policies, including trying to—and often succeeding in—ending renter-friendly concessions (like a free month's rent or waived fees) to attract or retain renters. A significant number of landlords then effectively agree to outsource their pricing function to RealPage with auto acceptance or other settings such that RealPage as a middleman, and not the free market, determines the price that a renter will pay. Competing landlords choose to share their information with RealPage to “eliminate the guessing game” about what their competitors are doing and ultimately take instructions from RealPage on how to make business decisions to “optimize”—or in reality, maximize—rents.

7. Each landlord pays steep fees to license RealPage's software. RealPage's stated goals and value proposition are not a secret. Its executives are blunt: They want landlords to “avoid the race to the bottom in down markets.” Sometimes RealPage is even more direct, acknowledging that its software is aimed at “driving every possible opportunity to increase price” or observing that among landlords, “there is a greater good in everybody succeeding versus essentially trying to compete against one another in a way that actually keeps the entire industry down.”

8. But that is not how the free market works. A free market requires that landlords compete on the merits, not coordinate pricing. Landlords should win renters by offering whatever combination of price and quality they think is most attractive. For example, landlords could lower rents or provide other financial concessions, like free months of rent, or with investments in amenities like gyms, grilling areas, or pools. Put differently, the fear of losing a renter to a competitor should motivate rival landlords to compete vigorously.

9. RealPage's revenue management software ingests on a daily basis nonpublic rental rates, future apartment availability, and changes in competitors' rates and occupancy. As competitor- ( printed page 56288) landlords increase their rents, RealPage's software nudges other competing landlords to increase their rents as well. RealPage calls this “maximiz[ing] opportunity[.]” As RealPage explained to one landlord, by using competitors' data, they can identify situations where “we may have a $50 increase instead of a $10 increase for that day.” This is what RealPage encourages as “stretch and pull pricing.”

10. RealPage allows landlords to manipulate, distort, and subvert market forces. One landlord observed that RealPage's software “can eliminate the guessing game” for landlords' pricing decisions. Discussing a different RealPage product, another landlord said: “I always liked this product because your algorithm uses proprietary data from other subscribers to suggest rents and term. That's classic price fixing. . . .” A third landlord explained, “Our very first goal we came out with immediately out of the gate is that we will not be the reason any particular sub-market takes a rate dive. So for us our strategy was to hold steady and to keep an eye on the communities around us and our competitors.”

11. RealPage's scheme not only distorts competition to the detriment of renters, but also allows it to reinforce its dominant position in the market for commercial revenue management software. By its own account, RealPage controls at least 80 percent of that market. Its dominant position is protected by substantial data advantages due to its massive reservoir of ill-gotten competitively sensitive information from competing landlords. No other revenue management company can match RealPage's access to landlords' nonpublic, competitively sensitive rental data. This is why RealPage acknowledges that it “does not have any true competitors, mainly because our data is based on real lease transaction data.” RealPage's conduct is predatory and exclusionary, which has allowed it to distort the market opportunities for honest providers of revenue management software.

12. At bottom, RealPage is an algorithmic intermediary that collects, combines, and exploits landlords' competitively sensitive information. And in so doing, it enriches itself and compliant landlords, including Defendant Landlords, at the expense of renters who pay inflated prices and honest businesses that would otherwise compete.

13. The United States, and the States of North Carolina, California, Colorado, Connecticut, Illinois, Minnesota, Oregon, Tennessee, and Washington, and the Commonwealth of Massachusetts, acting by and through their respective Attorneys General, bring this action pursuant to Sections 1 and 2 of the Sherman Act to rid markets of (i) RealPage's and Defendant Landlords' unlawful information-sharing and pricing alignment schemes, and (ii) RealPage's illegal monopoly in commercial revenue management software. In so doing, Plaintiffs seek to restore the free market to deserving individuals, families, and honest businesses.

II. RealPages's Revenue Management Software Is Fueled by Nonpublic, Competitively Sensitive Information Shared by Landlords

14. RealPage dominates the market for commercial revenue management software that landlords use to price apartments, controlling at least 80 percent of that market, according to its own estimates. RealPage currently offers three revenue management systems to landlords: YieldStar, AI Revenue Management (AIRM), and Lease Rent Options (LRO). The company's main legacy software, YieldStar, is the product of three acquisitions and subsequent internal development. Its successor, AIRM, uses much of the same codebase as YieldStar, but RealPage claims that AIRM's refined models and forecasting are more precise. RealPage acquired its other revenue management software, LRO, in 2017. RealPage has made plans to sunset both YieldStar and LRO by the end of 2024.

15. Competitively sensitive data collected from competing landlords is a critical input to RealPage's revenue management software. AIRM and YieldStar collect this data, such as rental applications, executed new leases, renewal offers and acceptances, and forward-looking occupancy, and use it to generate price recommendations for the competing landlords. This information is among the most competitively sensitive data a landlord maintains.

16. The exploitation of sensitive data from competing landlords is central to RealPage's approach. As part of pitching its software to landlords, RealPage highlights that its pricing algorithms use their competitors' data sourced directly from “lease transaction data.” RealPage describes this nonpublic data from competitors as one of three “building blocks of price” in AIRM and YieldStar. Landlords thus share their competitively sensitive information with RealPage with the understanding that RealPage's software will use the data to generate recommendations for rivals (and vice versa).

A. Landlords Agree To Share Nonpublic, Competitively Sensitive Transactional Data With RealPage for Use in Generating Competitors' Pricing Recommendations

17. RealPage amasses nonpublic, competitively sensitive data from competing landlords through use of its pricing algorithms, other rental property software, and thousands of monthly phone calls. The combined troves of nonpublic, competitively sensitive data are much more granular, sensitive, timely, and comprehensive than alternatives—and far more detailed than any data publicly available to potential renters. RealPage then uses this data in generating competitors' pricing recommendations.

18. Data shared through YieldStar and AIRM. Each AIRM and YieldStar client agrees to share detailed data with RealPage that are private, updated nightly, and granular. The data includes lease-level information on each unit's effective rent (rent net of discounts), rent discounts, rent term, and lease status, as well as unit characteristics such as layout and amenities. It also includes the number of potential future renters who have visited a property or submitted a rental application.

19. Landlords understand that AIRM and YieldStar use their data to recommend prices not just for their own units, but also for competitors. For example, a revenue management director at Greystar testified that she understood that Greystar, and other competing landlords who used AIRM or YieldStar, agreed with RealPage to share their data, which was combined in a single data pool for use by YieldStar and AIRM. An executive at Willow Bridge noted the advantages to using YieldStar at a property if others in the property's submarket—the small geographic area around the property—also used YieldStar because “the shared data between the models at different communities can be a benefit in getting accurate transactional data on a timely basis.”

20. Landlords agree to provide this information for use by their competitors because they understand they will be able to leverage the sensitive information of their rivals in turn. In its pitch to prospective clients, RealPage describes AIRM's and YieldStar's access to competitors' granular, transactional data as a meaningful tool that it claims enables landlords to outperform their properties' competitors by 2-7%. RealPage clients receive training that highlights the role of competitors' transactional data in the price recommendation process. ( printed page 56289)

21. Data Shared Through Other RealPage Products. AIRM and YieldStar are not the only ways that RealPage shares nonpublic, competitively sensitive information among landlords. RealPage obtains the same confidential transactional data from landlords that license at least three other programs: OneSite, Performance Analytics with Benchmarking, and Business Intelligence.

22. OneSite is RealPage's property management software, which operates as the central source of data for landlords' leasing activity. Performance Analytics with Benchmarking allows landlords to compare the performance of their properties and floor plans ( e.g., a one-bedroom, one-bathroom unit) to their competitors. Business Intelligence is a data analytics tool that pulls data from a landlord's property management software and other products.

23. Each landlord using RealPage's OneSite, Business Intelligence, and Performance Analytics with Benchmarking products agrees to share its proprietary data with RealPage and agrees that RealPage's revenue management software can use the data to generate pricing recommendations. The license agreements for these products specifically identify the shared data, such as pricing information, as confidential, nonpublic information. RealPage takes this deeply confidential information and uses it to provide rent recommendations to competitors of these clients.

24. These agreements grant RealPage access to confidential information from over 16 million units across the country, including many that do not use its revenue management products. With respect to Performance Analytics with Benchmarking alone, a RealPage sales representative told a prospective client that “we have over 16 million units of data coming from various source operating systems (PMS) [property management software] into the PAB platform,” making RealPage the top choice for “transactional data benchmarking.” With properties containing approximately 3 million units using AIRM and YieldStar, these additional agreements meaningfully multiply the scale of the transactional data used by AIRM and YieldStar. This gives RealPage greater visibility, including into markets with less penetration by AIRM and YieldStar, granting even initial AIRM and YieldStar adopters in a new market the benefit of access to a significant amount of nonpublic, competitively sensitive information.

25. Landlords understand that AIRM and YieldStar will use data from these products. A revenue management director at Greystar explained that RealPage ingests transactional data from several RealPage products, besides AIRM and YieldStar, for use in revenue management. A property owner requested information from Greystar on which competing properties used revenue management software. In an internal response, the Greystar director noted that RealPage has “access to more transactional history than anyone and [is] pulling data from anyone using RealPage products which includes companies who manually price or use other revenue management firms but leveraging their BI [Business Intelligence] products.”

26. A revenue management executive at Willow Bridge asked RealPage if other specific landlords were using RealPage's non-revenue management products. The landlord's owner client was concerned about the data available to YieldStar because competing properties were unsophisticated and did not use revenue management. This executive wanted to confirm that “YieldStar will be able to leverage actual transactional data behind the scenes and not just look at offered rents for their comps.” RealPage reminded the Willow Bridge executive that RealPage collected transactional data for all users of OneSite, Business Intelligence, and Performance Analytics with Benchmarking, and reassured the executive that YieldStar had ample transactional and survey data for that area.

27. Calling Landlords. RealPage has an additional, complementary product called Market Analytics. Market Analytics compiles data from over 50,000 monthly phone calls that RealPage makes to landlords across the country. On these calls RealPage collects nonpublic, competitively sensitive information by floor plan on occupancy rates, effective rents, and concessions, as well as information on the owner, management company, and any revenue management software used at the property. These market surveys cover over 11 million units and approximately 52,000 properties. Landlords, including but not limited to those that use AIRM, YieldStar, or other RealPage products, knowingly share this nonpublic information with RealPage.

B. AIRM and YieldStar Users Agree With RealPAge To Use the Software To Align Pricing

28. In addition to agreeing to share nonpublic, competitively sensitive data with RealPage, each AIRM and YieldStar licensee agrees with RealPage to use the AIRM or YieldStar pricing software as RealPage designed it.[2] Landlords are expected to review daily AIRM or YieldStar floor plan price recommendations and use the programs to set scheduled floor plan rents or even unit-level prices.

29. While landlords may not accept every price recommendation, they use AIRM or YieldStar as their pricing software, regularly review AIRM or YieldStar floor plan recommendations, use AIRM or YieldStar to set a scheduled floor plan rent, and use AIRM or YieldStar to set unit-level prices.

30. Landlords who use AIRM and YieldStar know that others are using the same software. Some landlords track which revenue management software their competitors use, including by contacting competing properties directly and exchanging nonpublic information. Other landlords, including prospective AIRM and YieldStar users, ask RealPage whether there are existing AIRM and YieldStar users nearby before they themselves license the products.

31. An executive at Willow Bridge, for example, explained to her team how she would learn from RealPage data or from a property's website whether a property used revenue management. This information is important because properties that use revenue management tend to update prices much more frequently, and so a landlord will react differently to those price changes if it knows the competitor is using revenue management.

32. RealPage frequently tells prospective and current clients that a “rising tide raises all ships.” A RealPage revenue management vice president explained that this phrase means that “there is greater good in everybody succeeding versus essentially trying to compete against one another in a way that actually keeps the industry down.” This rising tide lifts all landlords, including but not limited to AIRM and YieldStar users.

33. In using AIRM and YieldStar, landlords expect this pricing alignment and use RealPage software in part for this reason. One landlord echoed the RealPage executive, using the phrase “a rising tide rises [sic] all ships” to explain that AIRM would move prices in a “similar manner” to how the top and bottom of the market move. Elsewhere that same landlord noted that “if everyone in the market is doing well and everyone in the market has [sic] is having the rates go up, so should ours, ( printed page 56290) right?” An employee at Willow Bridge referenced RealPage's use of the phrase “a rising tide raises all ships” to explain how AIRM would provide price recommendations that amplify market trends. Multiple landlords have expressed their preference that their competitors use YieldStar and AIRM because widespread use would benefit them all. An executive of one landlord (which itself uses YieldStar and AIRM) said in a 2021 earnings call that more sophisticated, “high-quality competition” was better for that landlord when “they all use revenue management. They are all smart. They raised rents when they should.” RealPage highlighted in promotional materials the sentiments of another landlord who noted, “It actually gives me chills to think about what a disadvantage we'd be at if we hadn't adopted YieldStar, knowing others are using it.”

C. RealPage's Transactional Data Is Fundamentally Different From Other Data Available to Landlords

34. The data that RealPage uses and supplies is unique relative to public data available to landlords on listing or property websites. As compared to public data, RealPage data is much more granular, covers a broader array of business information, and includes competitively sensitive data across several dimensions. For example:

- Information on Actual Transactions. RealPage's data include, for each lease, the unit, floor plan, listed rent, final transacted lease price (including any discounts), and lease term.

- Renewals. RealPage's data include the same information for lease renewals. Information on renewals is not listed publicly—not even asking rents—leaving a significant blind spot for landlords not using RealPage.

- Time Span. AIRM and YieldStar have access to current and historical lease data, from the previous day and going back two to three years.

- Future Demand. The shared data further includes information on tenant demand, including detailed information on inquiries and applications by potential future tenants.

- Accuracy. Landlords have greater assurance of the accuracy of the data because it comes directly from the landlords' own databases.

- Coverage. The RealPage data covers millions of units from users of its revenue management software and other products.

35. RealPage touts how its data is different. As one RealPage pitch deck put it, “we have [the] most data and the best data.” And the “[q]uality of data is best in class given that it is `lease transaction data'—this provides insight into performance data from actual signed leases, both new and renewal, net effective of concessions.” Another noted that without YieldStar “you'll be pricing your renewals in the dark without insight into actual lease transaction data that YS uses to help you make pricing decisions. This is critical to price renewals right[,] especially in a downturn.”

36. Access to this data proves important in winning over revenue management clients, including skeptical ones. One RealPage senior manager noted that a “highly suspicious CFO” was won over in part by YieldStar's “lease transaction data” that allowed his company to “achieve what his people couldn't achieve on their own.”

37. One landlord explained the benefits of YieldStar to its owner clients by calling the use of competitors' transactional data a “game changer! We have 100% truth on [competitors'] activity powering YieldStar recommendations.”

38. Another landlord's internal training presentation on YieldStar highlighted the importance of having access to competitors' transactional data:

D. RealPage Revenue Management Software Uses Nonpublic, Competitively Sensitive Data To Recommend Prices

39. AIRM and YieldStar are built upon similar code and leverage competitive data in similar ways. LRO, on the other hand, was originally developed outside of RealPage and takes a different approach.

1. AIRM and YieldStar Leverage Competitively Sensitive Data To Generate Price Recommendations

40. AIRM uses competitors' nonpublic, transactional data in three separate stages of the pricing process: (1) model training, (2) floor plan price recommendations, and (3) unit-level prices. YieldStar uses competitors' nonpublic, transactional data in stages two and three of its process.

(a) AIRM Model Training Relies on Competitively Sensitive Data To Generate Learned Parameters

41. In the first stage, RealPage trains its AIRM models using nonpublic data from OneSite and other property management software, totaling millions of executed lease transactions, new lead applications, renewal applications, and guest cards filled out by visiting potential tenants. This data is run through a machine learning model to generate learned parameters for supply and demand models that are then used for all AIRM clients across the country. Like the coefficients in a regression model, the learned parameters are applied to the data of a landlord's specific property, and to the data of its competitors, when AIRM makes pricing recommendations. RealPage generally retrains the models three to four times per year using updated nonpublic data.

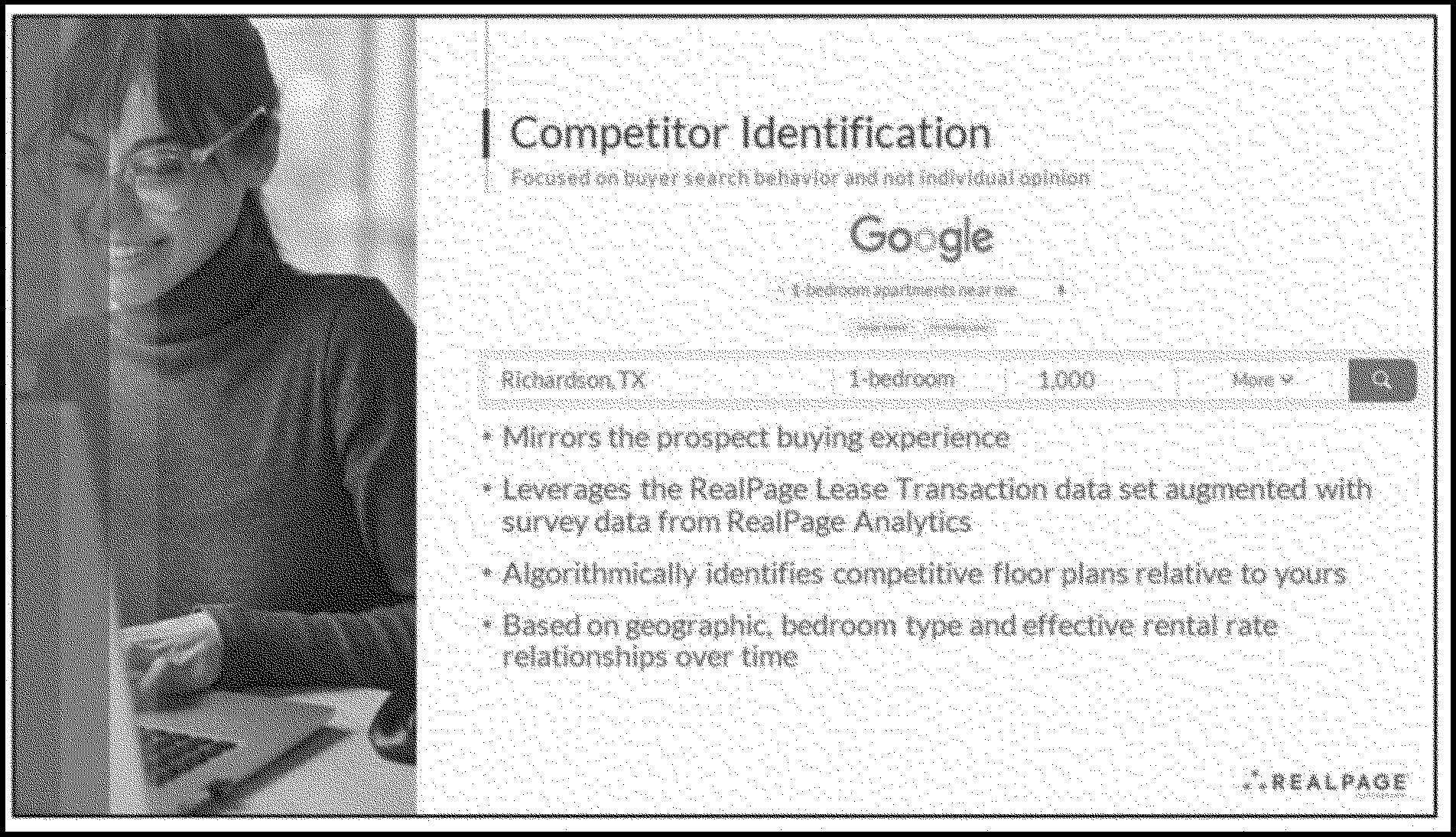

(b) AIRM and YieldStar Incorporate Competitors' Nonpublic Data To Generate Floor Plan Price Recommendations

42. In the second stage AIRM or YieldStar provides a price recommendation for every floor plan of a given property. A floor plan is a grouping of units that share similar characteristics, such as the number of bedrooms and bathrooms and square footage. Landlords define the floor plans in their buildings—for example, a large apartment building might have separate sets of floor plans for studios, one-bedroom, and two-bedroom apartments. As discussed below, AIRM and YieldStar use competitors' nonpublic, transactional data in nearly every step of setting a recommended floor plan price, including identifying peer properties, forecasting occupancy and leasing, increasing rents to match competitors' changes, and determining the magnitude of price changes.

43. Identifying Peers. First, AIRM and YieldStar use confidential transaction data to identify a property's peer properties, which include close competitors. In selecting peer properties, RealPage's algorithm generally looks for properties with similar floor plans, within close geographic proximity, and with similar effective rents over time. AIRM or YieldStar clients may review the list of peer properties and request that RealPage add or remove specific properties.

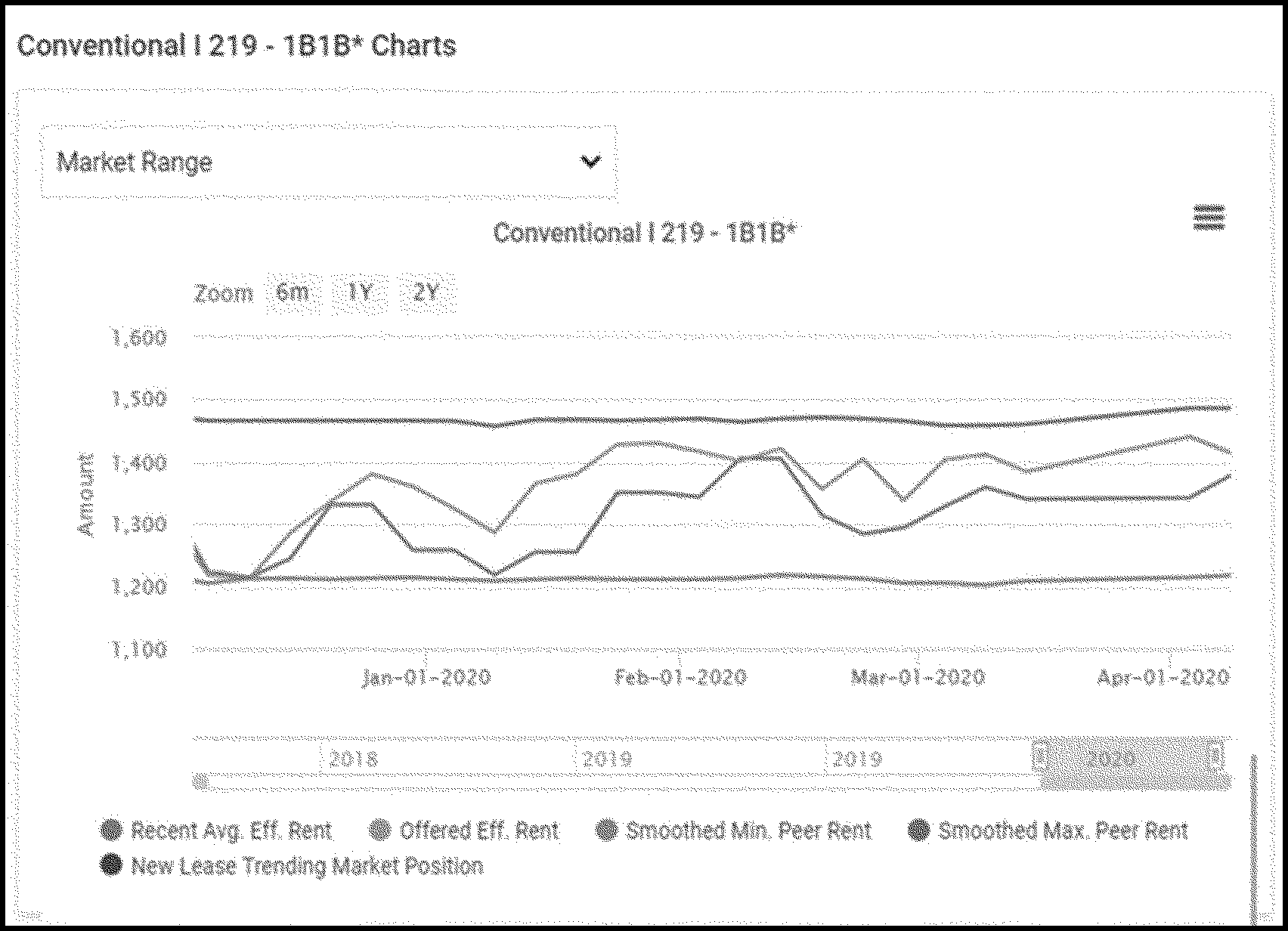

44. AIRM or YieldStar then uses the nonpublic data from competitors' executed leases to generate a market range chart for each floor plan. This chart identifies a “smoothed” market minimum effective rent and market maximum effective rent. The market minimum is a hard floor. AIRM and YieldStar will not recommend a rent below the market minimum. On the other hand, the market maximum is a “soft ceiling,” and the programs will recommend prices above the ceiling.

45. The client has access to the market range chart within the AIRM and YieldStar interfaces. As shown below, for each floor plan the client can see the smoothed market minimum and market maximum and where the client's own floor plan sits within the market range.

46. Forecasting Occupancy and Leasing. Every night, for each participating property, AIRM applies the model's learned parameters to that property's internal transactional data to forecast the number of expected vacancies and expected lease applications for a certain period into the future. AIRM may also use competitors' data to adjust the projected supply.

47. AIRM or YieldStar then determines whether actual leasing for a floor plan is on track to meet predicted leasing. To do so, it creates a forecast of the number of leases over time, using nonpublic lease and application data from the subject property, and potentially from so-called surrogate properties (similar properties in the surrounding area).[3] When there is an imbalance between a property's actual and forecasted leasing, it recommends a price change.

48. Changing Rents to Match Competitors. Even when a property's supply and demand are balanced, RealPage's software will still recommend a price change, based on competitors' nonpublic data, when it determines that the market is moving. For example, if the minimum and maximum of the competing floor plans' effective rents increase, it will recommend a price increase to maintain the floor plan's market position (its price position relative to its competitors).

49. Determining Magnitude of Price Changes. Once AIRM or YieldStar has determined that it will recommend a price increase or a price decrease, it again uses competitors' transactional data to determine how much the price should move and provide a floor plan price recommendation. It uses nonpublic transactional data from peer properties, in addition to data from the subject property and surrogate properties, to generate a market response curve—analogous to a market demand curve—for every floor plan. This demand curve provides an estimate of how demand for particular apartments would change in response to changes in rents, a measure that RealPage calls elasticity. In other words, it uses competitors' nonpublic transactional data to calculate how many leases the property will likely gain or lose for a particular floor plan, for every price point along the curve. Using this data, AIRM or YieldStar can determine how much the price can increase and still achieve the target number of leases, or by how little price can decrease to maintain a target occupancy.

50. RealPage describes elasticity as a pivotal input into balancing supply and demand and, therefore, price.

51. The use of surrogate properties in this pricing process has the potential to push convergence on price even further. As two properties' surrogate sets become closer—and therefore their respective demand curves become more similar—AIRM and YieldStar will generate increasingly similar prices for the two properties. And the use of surrogates is common. One of the largest landlords in the country, for example, uses surrogates at over 80% of its properties.

52. This process repeats for every floor plan in the client's property, every night. A new floor plan price recommendation is generated daily.

(c) AIRM and YieldStar Use Competitors' Nonpublic Data—Including Data on Future Occupancy—To Determine Unit-Level Prices

53. A property manager at the landlord reviews each floor plan recommendation daily and enters the floor plan price. AIRM and YieldStar then use the floor plan price to generate prices for every unit within the floor plan. The unit price is shown in a pricing matrix, which provides the price for each combination of start date and lease term. To generate the price for an individual unit, the floor plan price is adjusted to account for unit-specific factors such as amenities ( e.g., a desirable view, the floor level, or an in-unit washer and dryer), staleness ( i.e., how long that specific unit has been vacant), and the timing of lease expirations. AIRM and YieldStar again use competitors' nonpublic data during this step in at least two ways.

54. First, AIRM and YieldStar use data on competitors' supply of multifamily housing to adjust recommendations to limit “exposure” with a feature called lease expiration management. Exposure refers to the number of units that are available for lease. Managing lease expirations is an important element of revenue management software. If too many leases expire and the corresponding units become available at the same time, supply increases and rents for those units will tend to drop. This process will also tend to repeat itself as the same units will become available at the same time a year later for leases with a standard twelve-month term.

55. The objective of expiration management is to smooth out this exposure so that landlords, as explained by one RealPage employee, “remain in a position of pricing power.” For example, if AIRM or YieldStar sees that a large number of units will likely be available in twelve months, it will increase the price recommendation for a twelve-month lease relative to price recommendations for leases of other terms, such as 11 months or 13 months, in order to nudge potential renters to accept those terms. Expiration management can only raise prices—AIRM does not lower a unit's price if the lease term would fall in an underexposed period.

56. This calculation does not rely only on the predicted future supply for the client's property. For any landlord who uses a “market seasonality” setting, AIRM and YieldStar also rely on competitors' transactional data and the supply for those competitors—including the supply of competitors' existing leases that expire in the future. AIRM and YieldStar thus work to manage lease expirations for the client's units based on how competitors' supply will change. RealPage strongly recommends to landlords that they use market seasonality.

57. The use of competitors' nonpublic data in expiration management to fill out the pricing matrix occurs regardless of whether the landlord accepts the AIRM or YieldStar recommendation. Thus, even if a landlord were to override every price recommendation, its rental prices would still be influenced by nonpublic information about its competitors' supply.

58. Second, AIRM and YieldStar include an amenity optimization feature. By pricing specific amenities within units, landlords can avoid making wholesale pricing changes to a floor plan if a specific unit fails to lease. Within the amenity analysis, AIRM and YieldStar provide market values for specific amenities to landlords, allowing them to compare their perceived value of an amenity with the nonpublic valuation of their competitors. The peer data include the market minimum and maximum value for specific amenities.

2. LRO Relies Primarily on Landlords To Input Data on Competitors

59. RealPage's LRO also provides pricing recommendations to users. Each week, LRO users manually input competitor information into the system that they have obtained from public websites or more questionable means, such as communicating directly with their competitors.

60. A small number of LRO users subscribe to a feature called AutoComp. With this feature, RealPage provides ( printed page 56293) information on competitors' rents, traffic, and occupancy. This information comes from market surveys that RealPage compiles using call centers to call competitor properties. Landlords may use LRO without using AutoComp.

E. RealPage Uses Multiple Mechanisms To Increase Compliance With Price Recommendations

61. AIRM and YieldStar provide daily price recommendations. RealPage has taken multiple steps to increase compliance with AIRM and YieldStar price recommendations. It designed AIRM and YieldStar to make it much easier to accept recommendations than to decline them. It built an auto-accept function and pushes clients to adopt it and increase its role. And its pricing advisors encourage landlords to follow AIRM and YieldStar pricing recommendations. Among their duties, pricing advisors review any request to override a price recommendation.

1. AIRM and YieldStar Make It Easy To Accept Recommendations and More Difficult and Time-Consuming To Decline

62. Every morning, the landlord's property manager chooses whether to accept the floor plan price recommendation, keep the previous day's rent, or override the recommendation. These options are the same for new leases and renewal leases. RealPage makes it easier and faster for a client to accept a recommendation than to decline it. When accepting recommendations, the manager can choose to do a bulk acceptance—she can accept all or multiple floor plan recommendations at once. But she cannot do the same when overriding, or rejecting, the recommendation.

63. Instead, for every recommendation that she does not accept—whether overriding or keeping the previous day's rent—the property manager must provide “specific business commentary” for diverging from the recommendation. This justification, RealPage instructs, should not be a mere preference for another price but must be based on a factor that the model cannot account for, such as local construction or renovations occurring in the building. It must be a “strong sound business minded approach.”

64. The property manager knows that these recommendation rejections and accompanying justifications will be sent to a RealPage pricing advisor.[4] If the pricing advisor disagrees with the rejection or justification, the disagreement is escalated for resolution to a landlord's regional manager, who typically supervises the property manager.

65. As one client who complained to RealPage explained, RealPage's design is “trying to persuade [clients] to take the recommendations (almost like we made it hard to do anything but).”

2. RealPage Pushes Clients To Adopt Auto-Accept Settings That Automatically Approve Recommendations

66. AIRM and YieldStar each include auto-accept functions. This functionality automatically accepts price recommendations falling within certain parameters. By default, AIRM and YieldStar set auto-accept parameters of a 3% daily change and an 8% weekly change. The landlord can change these parameters, disable or enable auto-accept, and even enable partial auto-accept. With partial auto-accept, if the recommendation exceeds the auto-accept parameters, the recommendation is accepted as far as the parameter permits. For example, if the auto-accept daily change limit is 4% and the price recommendation is 5%, using partial auto-accept will result in an increase of 4%. By enabling auto-accept, a landlord functionally delegates pricing authority to RealPage (within the bounds of the daily and weekly limits).

67. As part of the onboarding process, internal RealPage guidance states, “AUTO ACCEPT should be confirmed as `on' with parameters in place.” Internal AIRM training explained that RealPage wanted to “widen auto accept parameters” by introducing the feature and then “creating enough trust so that over time we have client[s] that are willing to let auto accept run with very wide parameters . . . AKA—accept all recommendations.” RealPage trains pricing advisors to have an “accountability conversation” or a “refresher on short term vs long term goals” for clients that show less tolerance for increasing auto-accept parameters.

68. Even if a landlord does not want to use auto-accept, RealPage trains its advisors to convince the landlord to turn it on with 0% limits—a setting whereby auto-accept will never accept price changes. The reason? So that it is no longer a question of whether the client turns on auto-accept, but only a matter of convincing them to widen the parameters and further delegate pricing decisions. RealPage instructs its advisors on best practices: “[I]f a partner is not ready to use auto acceptance, are they ready to use revenue management?”

3. RealPage Pricing Advisors Provide a “Check and Balance” on Property Managers To Increase Acceptance of Recommendations

69. RealPage offers landlords pricing advisory services. Landlords typically have an assigned pricing advisor, unless the client has internal revenue managers that were certified by RealPage. Pricing advisors play an important role in the daily review of pricing recommendations. Landlords' property managers are asked to review recommendations every morning by 9:30 a.m. After their review, a pricing advisor accepts agreed-upon pricing within an hour and escalates any disputes to the landlord's regional manager.

70. If a property manager disagrees with the direction of a recommended price change— e.g., the manager wants to implement a price decrease when the model recommends a price increase—the RealPage pricing advisor escalates the dispute to the manager's superior. As a pricing advisor manager explained in a client training, the advisor would “stop the process and reach out to our partners”—the property manager's supervisors—to “talk about this further.” The advisors, the manager elaborated, are part of a system of “checks and balances.” The client confirmed the value of this system to stop property managers from acting on emotions, which could limit RealPage's influence on their pricing.

71. Beyond the daily interactions between pricing advisors and their own property managers, clients agree to make meaningful changes when they use RealPage's pricing advisory services. Under the specifications for this service, clients agree to use AIRM or YieldStar exclusively to give quotes to potential renters, further tying landlords' pricing decisions to RealPage's software. Clients also agree to change their commission programs for leasing agents to “ensure these programs motivate sales behavior that is consistent with the objectives of revenue growth.” And clients further agree to revenue growth as the official metric to evaluate AIRM and YieldStar, as opposed to occupancy rates.

72. RealPage imposes additional requirements on landlords who want to use internal or in-house revenue management advisors with YieldStar or AIRM (rather than use RealPage pricing advisors). RealPage requires these ( printed page 56294) landlords' employees go through RealPage certification. Certification is a multiday course in which landlords are trained—at times in the same session—on AIRM and YieldStar use and best practices, according to RealPage. Certification includes observing and leading pricing calls with property managers and passing a written exam. This certification program facilitates the landlords' agreements with RealPage to align pricing by ensuring that landlords' internal revenue managers are trained and tested to use AIRM and YieldStar in the same way.

4. Pricing Recommendations Heavily Influence Landlords' Behavior

73. RealPage defines an acceptance as where the final floor plan price is within 1% of the recommended floor plan price. According to that definition, the average acceptance rate across all landlords nationally for new leases between January 2017 and June 2023 is between 40-50%. But RealPage itself recognizes that acceptance rates are not necessarily the best measure of its influence; one employee explained that the spread between a floor plan recommendation and the final scheduled floor plan price is more useful for measuring model adoption—and therefore influence—than the binary accept/reject decision that the RealPage-defined acceptance rate reflects. Widening the definition of acceptance even slightly to account for partial acceptances illustrates the influence of recommendations: nearly 60% of final floor plan prices are within 2.5% of RealPage's recommendation, and more than 85% are within 5% of RealPage's recommendation.

74. RealPage's preferred measure of acceptance understates the influence of RealPage's price recommendations and the effect of competitors' data. AIRM and YieldStar use competitors' nonpublic transactional data to adjust unit-level pricing, after a floor plan recommendation has been accepted or rejected. RealPage's metric does not capture the cumulative effect of rate acceptances over time. Nor do they capture when a client is influenced by and partially accepts a recommendation.

III. Coordination Among Competing Landlords Is a Feature of This Industry

75. Several characteristics of apartment-rental markets make it easier for landlords to coordinate with, or accommodate, each other. Rental housing is a necessity for many Americans, meaning that demand is inelastic—that is, changes in rent produce relatively small changes in the number of renters. There is significant concentration among landlords in local markets, and these landlords engage in widespread, regular communications with one another. And RealPage makes rental units more comparable to each other in AIRM and YieldStar, allowing landlords to track one another more easily. These industry characteristics exacerbate the harm to the competitive process—and ultimately to renters—from the exchange of nonpublic, competitively sensitive data through RealPage and the use of the AIRM and YieldStar models.

A. Rental Housing Is a Necessity for Millions of Americans

76. Shelter is a basic, foundational necessity of life. And for tens of millions of Americans, conventional multifamily apartment buildings are the only reasonable option for much of their lives. Many renters cannot afford the significant down payment needed to purchase a single-family home, among other requirements.

77. Demand for apartments is relatively inelastic. Rising rents have disproportionately affected low-income residents: The percentage of income spent on rent for Americans without a college degree increased from 30% in 2000 to 42% in 2017. In 2021, the proportion of severely burdened households—households spending more than half of their income on gross rent—was 25%, or approximately 10.4 million households, an increase in approximately 1 million households since 2019. By 2022, this number increased to 12.1 million households. For college graduates, the percentage of income spent on rent increased from 26% to 34% from 2000 to 2017.

B. The Multifamily Property Industry Is Rife With Cooperation Among Ostensible Competitors

78. Within particular metropolitan areas and neighborhoods, the multifamily property industry is concentrated and replete with competitively sensitive discussions among ostensible competitors. Landlords have agreed with one another to share nonpublic, sensitive information, both indirectly through RealPage software and directly outside of RealPage's software. RealPage facilitates some of these discussions, while others are made directly between competing landlords. These discussions supplement and reinforce the indirect information sharing among landlords that occurs through AIRM and YieldStar. As a result of this coordination, RealPage's pricing algorithms are even more likely to restrain, rather than promote, competition.

1. At the Local Level, the Multifamily Property Industry Comprises a Small Number of Large Landlords Managing Buildings With Different Owners

79. In 595 zip codes with at least 1,000 total multifamily units across 125 core-based statistical areas, five or fewer landlords manage more than 50% of the multifamily units. Within the submarkets alleged in this complaint, there are at least 214 zip codes, each with at least 1,000 total multifamily units, in which five or fewer landlords manage more than half of those units. Similarly, within the ten core-based statistical areas alleged in the complaint, there are 144 zip codes, each with at least 1,000 total multifamily units, in which five or fewer landlords manage more than half of those units.

80. The same landlord often oversees nearby properties with different owners. In at least 502 zip codes, at least one landlord using AIRM or YieldStar oversees properties with different owners.

81. There is also overlap among RealPage pricing advisor assignments. In at least 683 zip codes, within 96 core-based statistical areas, a RealPage pricing advisor has responsibility for properties managed by different landlords. RealPage takes no steps to avoid assigning the same pricing advisor to properties with different owners, even if those properties compete with each other or are RealPage-mapped competitors.

2. Landlords Regularly Discuss Competitively Sensitive Topics With Their Competitors and Swap Information

82. Landlords regularly solicit and obtain nonpublic information about inquiries by prospective renters, occupancy, and rents from their direct competitors. Although this information is not as accurate or thorough as the transactional-level data shared with AIRM and YieldStar, it is nonetheless sensitive competitive information.

83. Landlords collect this information through a variety of means, including weekly phone calls, emails, and in-person visits. Some landlords also share information on their local geographic markets through shared Google Drive documents. One RealPage employee explained to his colleagues, reflecting on his former time working at a landlord, that these weekly inquiries “required cooperation among the comp[etitor]s but wasn't hard to get that.” In June 2023, a senior director at Cushman & Wakefield admitted that ( printed page 56295) “this practice has been prevalent in our industry for a long time.”

84. Landlords not only knew of these so-called “market surveys,” but expected their property managers to participate. As a manager of Cushman & Wakefield's revenue management department explained, “we have always expected our properties to continue doing a traditional market survey[,]” which “gives us insight into the very specific handful of competitors closest to the subject property.”

85. At a February 2020 industry event, representatives from Cushman & Wakefield and two other landlords shared tips on collecting information on concessions and net effective rents from competitors. The suggestions included bi-weekly and monthly meetings with competitors, sponsored “cocktail hours for regional competitors to share info and build relationships and rapport,” and using Google Drive documents to share information on a weekly basis. Building relationships with competitors to get accurate data was “critical.” The representatives cautioned that the collected data was used to make “major decisions about pricing,” so the landlord employees collecting data should be trained accordingly to ask such questions as “are you seeing a slow down?” and “are you adjusting pricing?”

86. Some landlords engage in even more sensitive communications about price, demand, and market conditions. These communications are not isolated instances at a specific property. Rather, they are conversations at the corporate revenue management level about strategies and approaches to market conditions that apply to the landlords' business across all markets.

87. For example, in January 2018, Willow Bridge's director of revenue management reached out to Greystar's director of revenue management and asked about Greystar's use of auto accept in YieldStar. In response, Greystar's director provided Greystar's standard auto-accept settings, including daily and weekly limits and for which days of the week auto accept was used. The Greystar director, explaining why she provided this information, testified that the Willow Bridge director was a “colleague,” even though Willow Bridge was a competitor to Greystar.

88. In March 2020, Cushman & Wakefield's director of revenue management reached out to Willow Bridge's director of revenue management. The Cushman & Wakefield director wanted to hold a call among revenue management executives at multiple landlords to discuss market conditions, use of YieldStar, and strategy plans. The Willow Bridge director agreed and suggested a small number of landlords to invite to keep the group “tight.” The directors agreed to reach out to Greystar, as well as several other landlords.

89. Also in March 2020, a senior executive at Greystar obtained a copy of Willow Bridge's sensitive strategic plans regarding the COVID-19 pandemic. The plans included Willow Bridge's corporate protocols for concessions, rent increases, and lease terms. The plans recommended that property managers work closely with YieldStar and LRO to preserve rent integrity. The Greystar executive forwarded Willow Bridge's plans to executives at Cushman & Wakefield and another landlord. All four landlords compete with one another.

90. In September 2020, Camden's director of revenue management reached out to Greystar's director of its internal revenue management team. Camden asked Greystar—a direct competitor—what increases on renewal pricing Greystar had seen in August and offered what it had seen. Greystar's director replied with information not only on August renewals, but also on how Greystar planned to approach pricing in the upcoming quarter. Greystar's director further disclosed its practices on accepting YieldStar rates and use of concessions. As the conversation continued, the two competitors shared additional highly-sensitive information on occupancy—including in specific markets—demand, and the strategic use of concessions.

91. At the same time, Camden's director emailed a revenue management executive at LivCor and asked how LivCor was faring on raising renewal rates. He explained his request by noting that Performance Analytics provided some good data, but it was “hard to see what our competitors are signing today.” The two executives shared information about their respective renewal increases. After the Camden executive passed this information along internally, he continued his outreach with several other landlords and with the LivCor executive—who in the meantime had reached out to three other landlords about their renewal rates. Camden's internal team decided to raise a renewal cap to get to the same renewal gains as LivCor.

92. Camden's director received competitively sensitive information from at least four competitors. Another senior executive at Camden asked him to compile the information so it could be shared internally. That executive noted the usefulness of the competitors' information and the need to take advantage of the shared information while it was fresh.

93. In June 2021, Willow Bridge's head of revenue management emailed Greystar's revenue management director. She proposed collaborating with Greystar to convince a client to move all of its properties, including those managed by Willow Bridge and those managed by Greystar, to AIRM. But she also noted that, in thinking about “the larger picture as well,” it could be useful to “coordinate with the other companies that we often share business with” to prepare to move their clients to AIRM as well. Greystar responded favorably to transitioning the joint client to AIRM.

94. In November 2021, a revenue management executive at LivCor emailed an executive at Camden to propose a call to discuss Camden's “renewal philosophy,” for the purpose of informing how LivCor calculated renewal increases. The two spoke that day. The following day, another LivCor executive—who was included on the call—thanked the Camden executive for the opportunity to “connect on industry best practices” and asked another “operational question” about implementing “larger renewal increases.” The executives exchanged emails over the next few months, including discussing their respective strategies on maximum increases to lease renewal prices. They shared not only their increase limits in specific markets but also what price increases they were able to achieve. For example, in April 2022, the executive at LivCor reached out to Camden to share that “my current thinking (not sure it's right, just where my mind is at) is . . . prices for almost everything are up 20%. Therefore, unless there is a good reason not to, should we be increasing rates on rentable items by 20%?” The Camden executive responded, “I like your thinking.” He continued, “Typically, we lean into the demand signals to inspire a price increase. . . . I'm divided on whether the default increase should be 20% or closer to the 10%. . . . Curious what your thoughts are!?”

95. In September 2021, a property manager at Cortland explained to a colleague that the manager had called two competitors and received from them pricing information on two-bedroom and three-bedroom units. The property manager asked for the information to decide how to act on YieldStar's price recommendations.

96. Landlords also engage in group discussions with local and national competitors about sensitive topics. For example, for a number of months in ( printed page 56296) 2020, dozens of “high-level participants” from competing landlords participated in weekly “multifamily leadership huddle” videoconferences. The organizer informed participants that “the goal of the call is to share information about what our companies are doing, share some collateral and resources,” and then—perhaps recognizing the problematic nature of these calls—he claimed that “then we hang up and make our own decisions.”

97. In one such call in April 2020 with over 100 attendees, participants discussed a number of topics, including “pricing and renewal strategies.” Several senior landlord executives, including a Greystar senior managing director and a CEO of another landlord, participated and shared their practices on new leases and renewals, use of renter payment plans, and use of YieldStar and other revenue management software. On a similar call in October 2020, participants discussed current and forecast rent prices, renewal strategies, and use of concessions. A Willow Bridge employee forwarded a colleague notes from the call, and he specifically highlighted information about a competitor's use of concessions.

98. These conversations among competing landlords have extended from the national level to local markets across the country. For example, in Minnesota, property managers from Cushman & Wakefield, Greystar, and other landlords regularly discussed competitively sensitive topics, including their future pricing. When a property manager from Greystar remarked that another property manager had declined to fully participate due to “price fixing laws,” the Cushman & Wakefield property manager replied to Greystar, “Hmm . . . Price fixing laws huh? That's a new one! Well, I'm happy to keep sharing so ask away. Hoping we can kick these concessions soon or at least only have you guys be the only ones with big concessions! It's so frustrating to have to offer so much.” The property managers from Greystar and Cushman & Wakefield continued to discuss competitively sensitive topics. For example, in response to Greystar's tipoff that it had reduced concessions and “hop[ed] the Spring/Summer market allow us to pull further back on concessions,” the Cushman & Wakefield property manager replied, “That's great news and I love hearing about the concessions being pulled back. We have done the same and hoping the rest of the market follows suit.” These communications between RealPage users that are ostensibly competitors are examples of the industry-wide coordination that magnifies the anticompetitive effects of RealPage's software.

99. In addition to contacting each other directly, many landlords also exchange information through other intermediaries. One vendor offers a tool for landlords to exchange with one another nonpublic information on concessions, net effective rents, inquiries and visits by prospective renters, and occupancy that is pulled from each landlord's property management software. Over 150 landlords nationally have used this service, including Greystar, LivCor, and some of the other largest landlords across the country. The vendor's CEO described this as a “quid pro quo or give to get” arrangement among landlords where “if you share this data with me, I'll share the same data.” A RealPage employee noted that this vendor makes it “quicker and easier to get your market surveys.”

100. Some landlords use this direct exchange of competitively sensitive information to update competitor rents within LRO—a practice that RealPage is aware of and accepts.

101. Recently, under the scrutiny of antitrust lawsuits, some landlords have adopted internal policies prohibiting “call arounds” and other direct sharing of competitively sensitive information with direct competitors. But even assuming that their property managers fully comply with these legally unenforceable internal policies, these landlords continue to use RealPage's revenue management software.

3. At RealPage User Group Meetings, Landlords Discuss Competitively Sensitive Topics

102. RealPage holds monthly “user group” meetings attended by competing landlords that use RealPage's software. There are separate user group meetings for LRO and for YieldStar and AIRM.[5] One of RealPage's stated purposes for the user groups is to “to promote communications between users.” Attendees include a wide mix of competing landlords. For example, the June 2022 YieldStar user group included representatives from five of the largest property management companies in the country, among a larger group.

103. Recurring topics at the user group meetings include product enhancements and an “idea exchange” on potential changes to the products. The user group participants often vote on the proposals discussed in the idea exchange. But discussions have covered competitively sensitive topics, including managing lease expirations, pricing amenities, the use of concessions, pricing strategies, and how to manage properties during the COVID-19 pandemic. RealPage encouraged landlords to use the user group meetings to discuss such topics in their industry and set agendas for these meetings to aid them in doing just that, remarking that “[t]he user group is meant to be self-governed to a degree and the clients should be leading it.” These RealPage-fostered discussions among competitors enhance and facilitate the landlords' agreement with RealPage to use AIRM and YieldStar to align pricing.

104. At an April 2020 YieldStar user group meeting, the participants discussed strategies for handling the COVID-19 pandemic. In the presentation, two RealPage employees and a landlord led a group discussion of trends in rent payments and collections and provided five strategic tips. One tip encouraged landlords to “push for occupancy but don't give away the farm (pricing).” Another counseled landlords to “balance internal and external dynamics” and, referring to the nonpublic information used by YieldStar, to “use transactional market data for decision support and to know when you can be more aggressive” in pushing higher rents. Invited attendees included representatives from at least twelve landlords. At this meeting, Greystar and another landlord shared information on their usage of payment plans with tenants.

105. In May 2020, RealPage started a YieldStar user group meeting by surveying them on concessions. RealPage asked landlords how many of their properties offered concessions, whether concessions applied to new leases or renewals, and the types of concessions offered (such as discounts, gift cards, or other benefits). Invited attendees included representatives of thirteen landlords.

106. In March 2021, the user group meeting included a discussion on possible adjustments to how YieldStar calculated lease expiration premiums. A RealPage executive shared that she liked the idea of adding weekend premiums to incentivize prospective renters to move in during the week, and commented that “the rev[enue] potential would then scale up.” The LivCor representative responded in favor of weekend premiums, and another user group member suggested adding the proposal to the user group idea exchange. RealPage agreed to do so.

107. RealPage began its agenda for an April 2021 YieldStar user group meeting with “strategic insights” from a ( printed page 56297) RealPage economist. This employee shared “21 key strategic insights,” including “focus on renewals,” “be cautious with concessions,” and “drive up revenues—not just base rent.” Specifically, he urged the group to “push up new and renewal pricing where demand [is] solid” and warned against over-relying on concessions. They were instead to “trust the science” of YieldStar.

108. In May 2021, RealPage included a “Back to Basics” discussion in a YieldStar user group meeting. This discussion covered “returning to renewal increases post-COVID” and “declining concessions,” as well as eviction moratoria and areas where acceptance rates were “seeing significant uptick in past 6 months.” The meeting group chat is even more revealing. Over a period of approximately fifteen minutes, representatives from fifteen landlords shared their plans for renewal increases and their use of concessions. The questions were posed, “At what point do we go back to normal? I[f] we go back to normal[,] [i]s it now? Is anyone seeing that the model is raising rent and are you doing it?” In response, these representatives made statements on renewal increases such as “increasing, back to normal,” “major rent growth on the west coast,” “increasing the renewals,” “almost all markets we are raising rents,” “actually raising more than before covid at some,” “raising,” and “we are pushing to get back to normal. Sending increases.” A representative from LivCor stated, “increasing renewals and pushing new lease rents.”

109. The user group members were similarly open about their disinterest in concessions, signaling to each other that they do not intend to offer them or would offer them less frequently. Their pronouncements included “no consessions [sic],” “no concessions,” “considerably less concessions,” “less frequent and less aggressive,” “no concessions except in markets with a lot of lease-ups,” and “almost no concessions currently.” A representative from Willow Bridge noted concessions had “gone away a LOT. People asking for a free month on renewals and being denied, but still signing the renewal.”

110. When the discussion turned to acceptance rates, a RealPage employee stated that rates had “pretty much gone back to pre-COVID. Rate Acceptance has grown 11% over the past 6 months.” A landlord responded that they had “seen our acceptance rate increase tremendously.” Another user group member explained to the group, for “about 1/3 of the communities I manage the [YieldStar] model was too slow to respond, and we are pushing rates above market and above YS rec[ommendation].” A representative from Willow Bridge concluded, “Are we deciding as a group to remove hesitation? :).”

111. The LivCor representative who attended this May 2021 meeting testified that similar discussions happened numerous times during the COVID-19 pandemic—specifically, the beginning of 2020 through the middle of 2022. In these meetings, user group members discussed new and renewal rent increases, concessions, and renewal strategies, as well as other sensitive topics.

112. RealPage claims that this and other user group meetings were not recorded.

113. The July 2021 YieldStar user group meeting, held at RealWorld (a RealPage-hosted industry event), included a roundtable discussion among competitors. One of the discussion topics? “What is the one thing you consistently consider outside of the model when accepting or changing price and why?”

114. At the October 2021 YieldStar user group meeting, a RealPage economist gave a presentation regarding the 2022 market outlook. RealPage presented analyses on current occupancy and pricing, and on expected occupancy and rent growth in 2022 by geographic regions.

115. At the July 2022 RealWorld YieldStar user group meeting, RealPage hosted a “roundtable discussion” on market volatility and its impact on how to use revenue management, unit amenities and their impact on tenant rents, and best practices for conducting lease ups.[6]

116. RealPage recognized the sensitive nature of the information shared at these meetings. Beginning in late 2022, after public reporting about AIRM and YieldStar, RealPage added an antitrust compliance statement in the user group presentations. Among other directions, the statement instructed participants not to discuss “confidential or competitively sensitive information,” and then noted that this included “you or your competitors' prices or anything that may affect prices, such as current or future pricing strategies, costs, discounts, concessions or profit margins.” But these were the very topics of previous user group meetings, as described above, that RealPage encouraged its users to discuss. And these are the very types of nonpublic information that AIRM and YieldStar use to recommend and determine prices.

117. Landlords frequently take advantage of RealPage user group meeting invites to email each other directly. In August 2020, for example, an employee of Cortland emailed a user group invitee list and asked them to support a change to how YieldStar calculated the number of leases needed. In response, an employee of a different landlord agreed, adding that “I also rely on comparing available units to adj[usted] leases needed, to forecast leases, to gut check the pricing recs. These data points are always a factor in my pricing decisions.”

C. RealPage Uses Nonpublic Information To Allow Landlords To More Easily Compare Units on an Apples-to-Apples Basis

118. Renters typically search for a rental unit using certain key criteria, including the number of bedrooms and the location. Recognizing this market reality, RealPage enables landlords to more easily compare unit prices. When picking a property's “peer set,” RealPage matches floorplans with the same number of bedrooms that are geographically proximate. This makes it easier for landlords, through AIRM and YieldStar, to track and respond to competitors' movements at the floor plan level.

119. To account for amenities, RealPage instructs landlords to identify amenities using standardized naming conventions so that RealPage can use machine learning to group amenities together. RealPage then provides the market value for specific amenities, allowing landlords to more accurately identify and track how their competitors value these amenities and adjust their own pricing accordingly. The peer data include the market minimum and maximum value, as well as market quartile values, for specific amenities.

IV. RealPage Harms the Competitive Process and Renters by Entering Into Unlawful Agreements With Landlords To Share and Exploit Competitively Sensitive Data