Securities and Exchange Commission

- [Release No. 34-104779; File No. SR-CboeBZX-2026-011]

Pursuant to Section 19(b)(1) of the Securities Exchange Act of 1934 (the “Act”),[1] and Rule 19b-4 thereunder,[2] notice is hereby given that on January 29, 2026, Cboe BZX Exchange, Inc. (the “Exchange” or “BZX”) filed with the Securities and Exchange Commission (the “Commission”) the proposed rule change as described in Items I, II, and III below, which Items have been prepared by the Exchange. The Commission is publishing this notice to solicit comments on the proposed rule change from interested persons.

I. Self-Regulatory Organization's Statement of the Terms of Substance of the Proposed Rule Change

Cboe BZX Exchange, Inc. (the “Exchange” or “BZX”) proposes to adopt fees for new logical ports in connection with a new connectivity offering on its equity options platform. The text of the proposed rule change is provided in Exhibit 5.

The text of the proposed rule change is also available on the Commission's website ( https://www.sec.gov/rules/sro.shtml), the Exchange's website ( https://www.cboe.com/us/equities/regulation/rule_filings/bzx/), and at the principal office of the Exchange.

II. Self-Regulatory Organization's Statement of the Purpose of, and Statutory Basis for, the Proposed Rule Change

In its filing with the Commission, the Exchange included statements concerning the purpose of and basis for the proposed rule change and discussed any comments it received on the proposed rule change. The text of these statements may be examined at the places specified in Item IV below. The

( printed page 6708)Exchange has prepared summaries, set forth in sections A, B, and C below, of the most significant aspects of such statements.

A. Self-Regulatory Organization's Statement of the Purpose of, and Statutory Basis for, the Proposed Rule Change

1. Purpose

The Exchange proposes to amend its fee schedule to adopt fees for Unitized Logical Ports, a new connectivity offering for its equity options platform (“BZX Options”) and adopt new Average Daily Quote and Average Daily Order fees.[3]

Unitized Port Fees

By way of background, Exchange Members may interface with the Exchange's Trading System [4] (hereinafter, “System”) by utilizing either the Financial Information Exchange (“FIX”) protocol or the Binary Order Entry (“BOE”) protocol. The Exchange further offers a variety of logical ports,[5] which provide users of these ports with the ability within the Exchange's System to accomplish a specific function through a connection, such as order entry, data receipt or access to information. For example, such ports include Logical Ports,[6] Purge Ports,[7] and Ports with Bulk Quoting Capabilities [8] (“Bulk Ports”). By way of further background, each of these ports corresponds to a single running order handler. Each order handler processes the messages it receives from these ports from the connected Members. This processing includes determining whether the message contains the required information to enter the System, whether the message parameters satisfy port-level ( i.e., pre-trade) risk controls, and where to send that message within the System ( i.e., to which matching engine [9] ). Once an order handler completes the processing of a message, it sends that message to the appropriate matching engine.

Historically, all order handlers connect to all matching engines. That is, under the BOEv2 and FIX protocols,[10] Members were able to access all symbols from a single logical port since each port corresponds to a single order handler that conveniently connects to all matching engines (“convenience layer”). Although the Exchange configures the software and hardware for its order handlers in the same manner, there can be a natural variance in the amount of time it takes individual order handlers to process messages of the same type under this architecture. Factors that contribute to this differentiation in processing times include the availability of shared resources (such as memory), which is impacted by (among other things) then-current message rates, the number of active symbols ( i.e., classes), and recent messages for a symbol. This natural differentiation in processing times inherently may cause some messages to be sent from an order handler to a matching engine ahead of other messages that the Exchange's System may have received earlier on a different order handler.

The Exchange recently implemented a new architecture and protocol which includes, among other things, a single gateway per matching engine (“unitized layer”), which renders the above-described natural variance of order handler processing irrelevant for Members that connect to the unitized order handler.[11] More specifically, effective August 19, 2024, the Exchange implemented this new unitized access architecture and a new version of its Binary Order Entry (BOE) protocol [12] (“BOEv3”), which also resulted in the adoption of new logical port types (“Unitized Logical Ports”), for which the Exchange is now seeking to establish fees.[13] Under the new unitized BOEv3 architecture, a single BOEv3 order handler corresponds to a single matching engine and all message traffic (including FIX and BOEv3 convenience layer port traffic)[14] passes through this unitized BOEv3 order handler before reaching that order handler's corresponding matching engine.[15] If a Member desires to access this unitized layer of the BOEv3 architecture, the Member would need to obtain a Unitized Logical Port for each corresponding matching engine(s) that process the symbol(s) that Member desires to trade.[16]

BOEv3 Unitized Logical Ports provide an expedited processing path to a single matching engine over that of other inbound paths on a best-efforts basis. Under routine circumstances, the System will process pending purge messages from BOEv3 Unitized Logical Ports before processing other inbound paths. Exceptions to this approach exist with regard to various message traffic ( printed page 6709) and rate controls that are incorporated into the BOEv3 architecture. To illustrate how BOEv3 processes inbound messages, consider the following simplified example: (1) process pending purge messages from BOEv3 Unitized Logical Ports; (2) process all other pending messages from BOEv3 Unitized Logical Ports; (3) process pending messages from convenience ports.

As noted above, to access the BOEv3 architecture a Member must obtain a Unitized Logical Port for each corresponding matching engine(s) that processes the symbol(s) the Member desires to trade. The three new port types that have been adopted are: (1) BOE Unitized Logical Ports,[17] (2) Bulk Unitized Logical Ports,[18] and (3) Purge Unitized Logical Ports [19] (collectively, “Unitized Logical Port”). With the exception of Exchange Options Market Makers [20] (hereinafter, “Market Makers”) who may only quote via a BOE Bulk Unitized Logical Port,[21] use of the unitized architecture and purchase of a Unitized Logical Port is completely voluntary, and Members ( i.e., non-Market Makers) are not required, or under any regulatory obligation, to utilize them.

The Exchange proposes to establish fees for the new Unitized Logical Ports, which can be purchased on an individual basis ( i.e., capable of accessing a specified matching engine (“Matching Unit”)) [22] and/or as a set (“Unitized Logical Port Set”) ( i.e., will include the total number of ports needed to connect to each available Matching Unit). The proposed fees for Unitized Logical Ports purchased individually and as sets are as follows:

| BOE Unitized Logical Port | $350/port/month. |

| Bulk Unitized Logical Port | $550/port/month. |

| Purge Unitized Logical Port | $400/port/month. |

| BOE Unitized Logical Port (Set) | $2,500/month for 1st and 2nd port set. $3,000/month for 3rd-14th port set. $3,500/month for 15th-30th port set. |

| Bulk Unitized Logical Port (Set) | $5,500/month for 1st and 2nd port set. $6,000/month for 3rd-14th port set. $6,500/month for 15th-30th port set. |

| Purge Unitized Logical Port (Set) | $2,500/month for 1st and 2nd port set. $3,000/month for 3rd-14th port set. $3,500/month for 15th-30th port set. |

The proposed fees for Unitized Logical Port Sets are progressive. For example, if a User were to purchase 11 BOE Unitized Logical Port Sets, it will be charged a total of $32,000 per month ($2,500 * 2 + $3,000 * 9). As is the case today for existing logical ports, the monthly fees are assessed and applied in their entirety and are not prorated. The Exchange notes the current standard fees assessed for existing logical ports will remain applicable and unchanged,[23] and Members are still able to purchase and utilize such ports if they choose to do so. The proposed fees for Unitized Logical Port Sets will be assessed per set, per Port Type. As an example, if a Member requests three BOE Unitized Logical Port Sets, one Bulk Unitized Logical Port Set, and one Purge Unitized Logical Port Set, the firm would be charged $8,000 ($2,500 + $2,500 + $3,000) for the three BOE Unitized Logical Port Sets, $5,500 for the one Bulk Unitized Logical Port Set, and $2,500 for the one Purge Unitized Logical Port Set.[24]

Since the Exchange has a finite amount of capacity, it also proposes to prescribe a maximum limit on the number of Unitized Logical Ports that may be purchased and used on a per Member, per Matching Unit basis. The purpose of establishing these limits is to manage the allotment of Unitized Logical Ports in a fair and reasonable manner while preventing the Exchange from being required to expend large amounts of resources in order to provide an unlimited capacity to its matching engines. The Exchange previously proposed to provide that the two structures ( i.e., individual unitized ports or unitized port sets) can be combined for up to a maximum of 20 Unitized Logical Ports per Member, per Matching Unit, per type of Unitized Logical Port.[25] The Exchange noted at the time it adopted this maximum that it would continue monitoring interest by all Members and system capacity availability with the goal of increasing these limits to meet Members' needs if and when the demand is there and/or the Exchange is able to accommodate such demand.[26] Since then, the Exchange has determined that it is able to accommodate an increased cap relative to current demand and available to the Exchange's matching engine and order handler capacity. As such, the Exchange proposes to increase the maximum to 30 Unitized Logical Ports per Member, per Matching Unit, per port type. As an example, a Member may request 12 BOE Unitized Logical Port Sets and 18 individual BOE Unitized Logical Ports for Matching Unit 1, providing a total max of 30 BOE Unitized Logical Ports on Matching Unit 1 specifically. This would result in having 30 BOE Unitized Logical Ports on Matching Unit 1 and 12 BOE Unitized Ports on all additional Matching Units as part of the 12 BOE Unitized Logical Port Sets requested. Additionally, a firm may request 30 Bulk Unitized Logical Port Sets and 30 ( printed page 6710) Purge Unitized Logical Port Sets as those would constitute different port types.[27] The Exchange believes the proposed cap will be sufficient for the vast majority of Members, as the Exchange understands that at this time, no Member desires more than the current cap. The Exchange notes that it will continue to monitor interest in Unitized Logical Ports and system capacity availability with the goal of further increasing these limits to meet Members needs if and when the demand is there, and the Exchange is able to accommodate it. Additionally, Members will still be able to utilize the existing logical port connectivity offerings with no maximum limit in addition to their Unitized Logical Port allocation.[28] As further discussed below, the Exchange's pricing for these new Unitized Logical Ports are less than or comparable to similar offerings from other exchanges.[29]

Average Daily Quotes and Average Daily Order Fees

The Exchange also proposes to adopt Average Daily Order (“ADO”) and Average Daily Quote (“ADQ”) fees. “ADO” represents the total number of orders for the month, divided by the number of trading days. “ADQ” represents the total number of quotes for the month, divided by the number of trading days.[30] When measuring a Member's ADO orders and cancel/replace modify orders which submit a bid or offer and do not include cancels, are included. To measure a Member's ADQ, quotes and quote updates which submit a bid or offer and do not include cancels, are included. Further, ADO will include orders submitted by a Member from all logical port types ( i.e., non-unitized logical ports and Unitized Logical Ports).[31] Each Member may submit up to 2,000,000 average daily orders or up to 250,000,000 average daily quotes per calendar month without incurring any ADO or ADQ fees, respectively. In the event that the average number of quotes per trading day during a calendar month submitted exceeds 250,000,000, each incremental usage of up to 20,000 average daily quotes will incur an additional fee as set forth in the table below. Similarly, in the event that the average number of orders per trading day during a calendar month submitted exceeds 2,000,000, each incremental usage of up to 1,000 average daily orders will incur an additional ADO fee as set forth in the table below. A Member's ADO and ADQ will be aggregated together with any affiliated Member sharing at least 75% common ownership.

| Fee | ||||

|---|---|---|---|---|

| Tier 1 <=250,000,000 | Tier 2 >250,000,000 | Tier 3 >500,000,000 | Tier 4 >1,000,000,000 | Tier 5 >3,500,000,000 |

| ADQ Fee Rate per 20,000 ADQ | ||||

| $0.00 | $0.05 | $0.075 | $0.10 | $0.20 |

| ADO Fee Rate per 1,000 ADO | ||||

| Tier 1 <=2,000,000 | Tier 2 >2,000,000 | Tier 3 >2,500,000 | Tier 4 >3,000,000 | Tier 5 >3,500,000 |

| $0.00 | $1.00 | $1.50 | $2.00 | $2.50 |

As an example, a Member that has 510,000,000 ADQ would subsequently have 25,500 “ADQ increments” (510,000,000 ADQ/20,000 ADQ increments). While 12,500 of the 25,500 ADQ increments are free within Tier 1, 12,500 of the ADQ increments would be fee liable at $0.050 within Tier 2, while the remaining 500 ADQ increments would be fee liable at $.075 within Tier 3, resulting in a total ADQ fee of $662.50 for that month.[32]

The Exchange notes that market participants with incrementally higher ADO or ADQ are likely to require more of the Exchange's Trading System resources, bandwidth, and capacity. In this regard, higher ADO or ADQ may, in turn, create System latency and potentially impact other Members' ability to receive timelier executions. The proposed fee structure has multiple thresholds, and the proposed fees are incrementally greater at higher ADO and ADQ rates because the potential impact on Exchange Systems, bandwidth, and capacity becomes greater with increased ADO and ADQ rates. As noted above, the proposal contemplates that a Member would have to exceed the high ADO rate of 2,000,000 and a Member would have to exceed the high ADQ rate of 250,000,000 before that market participant would be charged a fee under the proposed respective tiers. The Exchange believes that it is in the ( printed page 6711) interests of all Members and market participants who access the Exchange to not allow other market participants to strain System resources, but rather encourage efficient usage of network capacity. The Exchange also believes this proposal (and in particular the proposed incrementally higher fee amounts associated with higher ADO and ADQ) will help to moderate excessive order/quote and trade activity from Members that may require the Exchange to otherwise increase its storage capacity and will encourage such activity to be submitted in good faith for legitimate purposes.

The Exchange also represents that the proposed fees are not intended to raise profits; rather, as noted above, it is intended to encourage efficient behavior so that market participants do not exhaust System resources. Moreover, the Exchange provides Members with daily reports, free of charge, which details their order and trade activity in order for those firms to be fully aware of all order and trade activity they (and their affiliates) are sending to the Exchange. This will allow Members to monitor their behavior and determine whether it is approaching any of the ADO or ADQ thresholds that trigger the proposed fees.

Lastly, the Exchange notes that other exchanges have adopted various fee programs that assess incrementally higher fees to Members that have incrementally higher order and/or quoting trading activity for similar reasons.[33]

2. Statutory Basis

The Exchange believes the proposed rule change is consistent with the Securities Exchange Act of 1934 (the “Act”) and the rules and regulations thereunder applicable to the Exchange and, in particular, the requirements of Section 6(b) of the Act.[34] Specifically, the Exchange believes the proposed rule change is consistent with the Section 6(b)(5) [35] requirements that the rules of an exchange be designed to prevent fraudulent and manipulative acts and practices, to promote just and equitable principles of trade, to foster cooperation and coordination with persons engaged in regulating, clearing, settling, processing information with respect to, and facilitating transactions in securities, to remove impediments to and perfect the mechanism of a free and open market and a national market system, and, in general, to protect investors and the public interest. Additionally, the Exchange believes the proposed rule change is consistent with the Section 6(b)(5) [36] requirement that the rules of an exchange not be designed to permit unfair discrimination between customers, issuers, brokers, or dealers. The Exchange also believes the proposed rule change is consistent with Section 6(b)(4) [37] of the Act, which requires that Exchange rules provide for the equitable allocation of reasonable dues, fees, and other charges among its Members and other persons using its facilities.

The Exchange believes the proposed fees are reasonable because Unitized Logical Ports provide a valuable service in that Unitized Logical Ports are intended to create a more consistent, and more deterministic experience for messages once received within the Exchange's System under the recently adopted unitized BOEv3 architecture. As discussed above, the new architecture (and thereby the new Unitized Logical Ports) was designed to create a more consistent and more deterministic experience for messages once received within the System, which the Exchange believes improves the overall access experience on the Exchange and will enable future system enhancements. As noted, the BOEv3 protocol and architecture, along with the three new corresponding Unitized Logical Ports, are intended to reduce the natural variance of order handler processing times for messages, and as a result reduce the potential resulting “reordering” of messages when they are sent from order handlers to matching engines. The adoption of the unitized BOEv3 structure (including the corresponding new Unitized Ports) was a technical solution that is intended to reduce the potential of this reordering and increase determinism.[38] The Exchange believes the proposed fees are also reasonable to offset costs incurred in order to build out an entirely new unitized architecture.

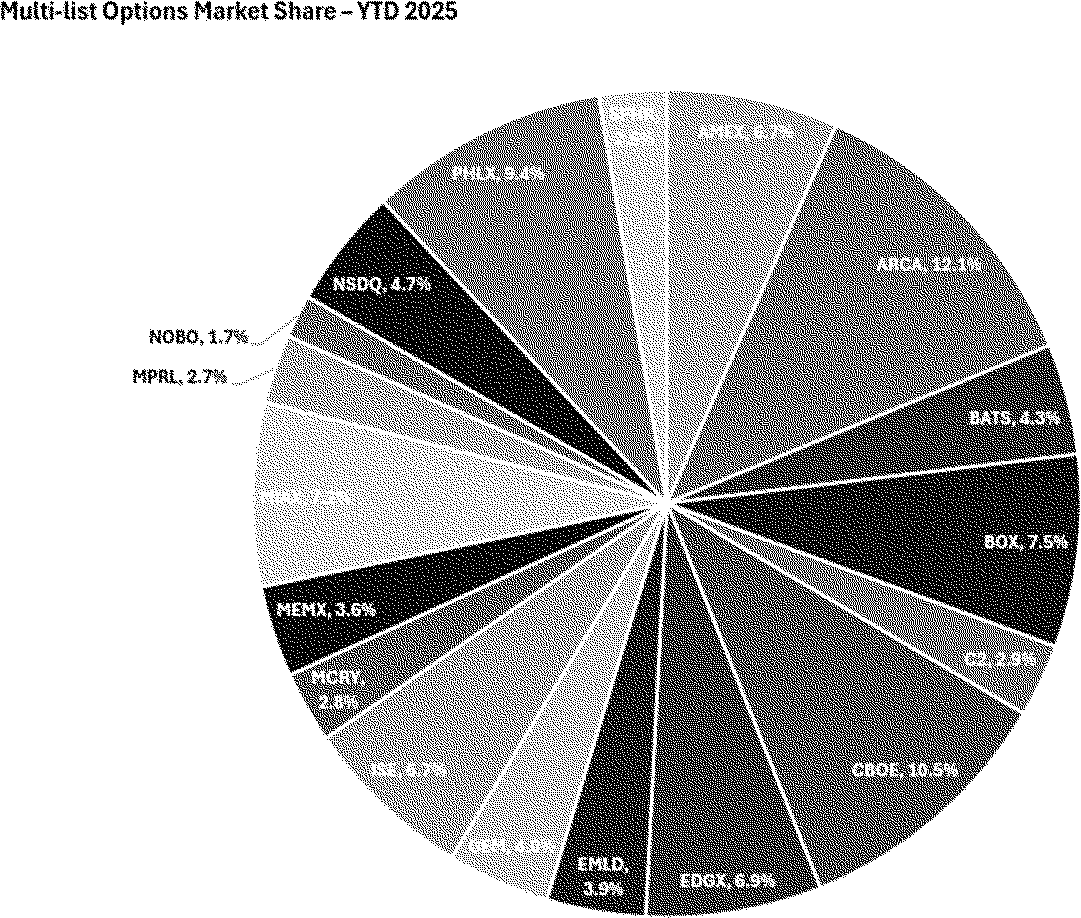

Furthermore, the Exchange also notes that it believes the proposed fees are similar to or less than fees assessed by other exchanges, for analogous connections as explained in further detail below.[39] The Exchange notes that other exchanges that offer similar pricing for similar connections have a comparable, or even lower, market share as the Exchange, as also detailed further below. Indeed, the Exchange has reviewed the U.S. options market share for each of the eighteen options markets utilizing total options contracts traded year-to-date as of the end of June 2025, as set forth in the following graph: [40]

( printed page 6712)

The Exchange (market share of 4.30%) notes that the proposed Purge Unitized Logical Port fee of $400 to connect to a matching engine is lower than fees charged by at least two other exchanges with comparable (indeed, even lower) market share, particularly by MIAX Emerald (3.90% market share) and MIAX Pearl (2.7% market share). The Exchange does note that both MIAX Emerald and MIAX Pearl offer two purge ports for a matching engine connection at a cost of $600,[41] while the Exchange offers the primary Purge Unitized Logical Port as well as a secondary Purge Unitized Logical Port for its redundant secondary data center ports for $400. The Exchange believes that the bulk of the value customers derive is not within the quantity of Purge Unitized Logical Ports a Member purchases, but the ability to connect to the specific matching engine.[42] For instance, a Member may need to purchase several convenience ports to minimize the natural variance of order handler processing times for messages, but by comparison the same Member may only need to purchase a single Unitized Logical Port to achieve the same results. For this reason, the Exchange still believes it is better priced than MIAX Emerald's and MIAX Pearl's comparable offerings.

Furthermore, even when comparing the costs of purchasing Purge Unitized Logical Ports to connect to all matching engines, the Exchange still assesses a lower fee than MIAX Pearl or MIAX Emerald. Connecting to all matching engines on MIAX Emerald or MIAX Pearl would cost $7,200, while connecting to all matching engines on BZX Options costs $2,500.[43] As noted above, while the Exchange believes the bulk of the value customers derive is the ability to connect to specific matching engines, and in this case, all matching engines, if a customer did want to have two Purge Unitized Logical Ports for all matching engines (in addition to the included secondary purge ports provided), it would cost the participant $5,000 ($2,500/set × 2)—still lower than the cost of $7,200 for two purge ports for all matching engines that MIAX Emerald and MIAX Pearl offer.

While not as closely comparable, MIAX Emerald and MIAX Pearl both offer Full Service MEI Ports (analogous to the Exchange's Bulk Port offering) and Limited Service MEI Ports (analogous to the Exchange's BOE Port offering) that are based on the lesser of a participant's per class basis or percentage of total national average daily volume measurement. For each matching engine a participant connects to (based on their activity), they receive two Full Service MEI Ports and four Limited Service MEI Ports.[44] Based on publicly available information, MEI ports provide market makers direct connections to each matching engine for high-speed mass quoting.[45] A Full Service MEI Ports support all input message types, and Limited Service MEI Ports support all message types except bulk quotes.

Notably, MIAX Emerald and MIAX Pearl offer their Full Service MEI Ports and Limited Service MEI Ports only to market makers on those respective exchanges, and non-market maker members are not permitted to purchase MEI connections. As such, when comparing the Unitized Logical Port fees assessed to Market Makers by the Exchange to the Full Service MEI and Limited Service MEI Ports assessed to market makers by MIAX Emerald and MIAX Pearl, the Exchange believes that its proposed fee for Unitized Logical Ports is reasonable and justified by the value derived by Options Market Makers purchasing these connections in being able to connect directly to a certain matching engine.

Specifically, presuming a participant is quoting up to 10 classes for MIAX Pearl or 5 classes for MIAX Emerald (the lowest available tier for each exchange), they are connecting to fewer matching engines than another participant who may be quoting over 100 classes (the highest tier available for both MIAX Pearl and MIAX Emerald). In comparing the monthly cost using the pricing of the lowest tiers for MIAX Pearl and MIAX Emerald, the Exchange presumes an estimated comparable connection of ( printed page 6713) connecting to 3 different matching engines at a cost of $550 per Bulk Port per matching engine and $350 per BOE Port per matching engine.[46] This equates to $7,500 (($350 * 4 Ports * 3 matching engines) + ($550 * 2 Ports * 3 matching engines) per month for BZX Options, and $5,000 per month for both MIAX Pearl and Emerald. For the highest tier, the Exchange presumes that if a participant was quoting over 100 classes, they are likely connecting to all matching engines. In this case, it costs a participant $12,000 per month for MIAX Pearl, $20,500 per month for MIAX Emerald, and $22,000 ($5,500 * 2 Bulk Sets) + ($2,500 * 2 BOE Sets (Tier 1)) + ($3,000 * 2 BOE Sets (Tier 2)) per month for BZX Options to connect to all matching engines.

While the Exchange is priced higher in these specific examples, it again believes the value comes from the ability to connect to additional matching engines as opposed to the quantity of ports itself and participants of the Exchange are able to determine their number of desired ports as opposed to having a set package based on their Exchange activity. For example, a participant of BZX Options can have similar matching engine connectivity to the lowest tier of MIAX Emerald or MIAX Pearl by connecting to three matching engines (using the same presumed number as above) by purchasing three Bulk Ports for a cost of $1,650 per month, substantially less than the fixed costs of $5,000 per month of MIAX Emerald and MIAX Pearl. Additionally, a participant on BZX Options is able to connect to all matching engines for a price of $5,500 per month by purchasing a Bulk Set as opposed to the fixed cost of MIAX Emerald and MIAX Pearl at $20,000 per month and $12,000 per month, respectively. Furthermore, MIAX Emerald does allow participants to purchase additional Limited Service ports at a price of $420 per month, higher than the Exchange's comparable offering of $350 per month for a BOE port. While it is challenging to compare the exact pricing on these products, the Exchange believes that it is priced comparably, if not lower than MIAX Pearl and MIAX Emerald.

The Exchange acknowledges that the above comparability analysis does not consider the fees assessed to non-Options Market Makers on the Exchange relative to non-market makers on MIAX Emerald or MIAX Pearl. This is due, however, to the fact that MIAX Emerald and MIAX Pearl do not permit non-market makers to purchase MEI ports (the closest comparable product to BZX's Unitized Logical Ports). Presumably, MIAX Emerald and MIAX Pearl limit such participants to use of only MIAX's FIX ports. Importantly, unlike MIAX Emerald and MIAX Pearl, the Exchange permits its Members ( i.e., non-Market Makers) to purchase a Unitized Logical Port, should such Member deem the use of such connection to be beneficial to their trading strategy. Additionally, Members ( i.e., non-Market Makers) may instead elect to purchase Exchange BOE convenience or FIX Ports, or a combination of Unitized Logical Ports, BOE convenience and FIX ports. Furthermore, Members and Market Makers are free to choose to purchase Unitized Logical Ports in sets or by individual ports (dependent on the firm's matching engine needs, which may be based on products it trades, strategies, or other business needs). As such, the Exchange's offering is both more widely available and provides Members and Market Makers with more flexibility and customization in contrast to MIAX's strict matching engine connectivity based on the classes a Market Maker is quoting in and its rigid fee structure.

As an additional point of comparison for non-market makers, the Exchange notes the FIX port fees it charges it Members, relative to those charged by MIAX Emerald and MIAX Pearl for their non-market maker members.[47] Specifically, the Exchange charges its Members $750 per month, per convenience port (which may be FIX or BOE). MIAX Emerald [48] utilizes a progressive fee schedule for its FIX ports and charges its members a fee of $550 per month, per port, for the first FIX port; $350 per month, per port, for ports two through five; and $150 per month, per port, for each FIX port above five. MIAX Pearl [49] also utilizes a progressive fee schedule for its FIX ports, and charges its members $275 per month, per port, for the first FIX port; $175 per month, per port, for FIX ports two through five; and $75 per month, per port, for each sixth or more FIX port. While purchasing six FIX ports on the Exchange ($4,500) [50] would cost more than purchasing six FIX ports on MIAX Emerald ($3,100) [51] or MIAX Pearl ($1,225),[52] the Exchange again notes that its Members are, unlike MIAX Emerald and MIAX Pearl members, permitted to purchase BOE ports, FIX ports, or Unitized Logical Ports, or a combination of the three, depending on their needs and strategy. In this regard, unlike MIAX Emerald and MIAX Pearl the Exchange's Unitized Logical Port solution and its related benefits are available to all Members, and at a lower cost than that assessed to Members for a single FIX port ($750 for one FIX port, per month vs. $350 for one BOE Unitized Logical Port). Therefore, while FIX ports on the Exchange are more expensive than those on MIAX Emerald and MIAX Pearl, the Exchange's port offerings as a whole provide Members and Market Makers with more flexibility in how to manage their Exchange access and better configure their connectivity costs based on their needs The Exchange also emphasizes that the use of the Unitized Logical Ports is not necessary for trading on the Exchange and, as noted above, is entirely optional (other than Market Makers which must utilize a Unitized Logical Port for quoting). The Exchange notes the following usage stats, current as of September 25, 2025:

• Convenience Ports (FIX or BOEv3)

○ 57% of Members still utilize a convenience layer port (FIX or BOEv3), in addition to or in lieu of Unitized Ports. On average, Market Makers utilize 44 convenience ports.

• BOEv3 Unitized Logical Port

○ Market Makers constitute 71% of all BOEv3 Unitized Logical Port usage, compared to 29% of Members ( i.e., non-Market Makers).

○ Market Makers constitute 70% of all BOEv3 Unitized Logical Port sets usage, while Members ( i.e., non-Market Makers) constitute 30% of BOEv3 Unitized Logical Port sets usage.

• BOEv3 Unitized Logical Purge Port

○ Market Makers constitute 100% of all BOEv3 Unitized Logical Purge Port usage, and 100% of BOEv3 Unitized Logical Purge Port set usage. ( printed page 6714)

• BOEv3 Unitized Logical Bulk Port

○ Market Makers constitute 99% of all BOEv3 Unitized Logical Bulk Port Usage, while Members ( i.e., non-Market Makers) constitute 1%.

○ Market Makers constitute 99% of all BOEv3 Unitized Logical Bulk Port set usage, while Members ( i.e., non-Market Makers) constitute 1% of BOEv3 Unitized Logical Bulk Port set usage.

The Exchange believes that the above statistics demonstrate that the use of Unitized Logical Ports and their associated fees are not mandatory per se. Indeed, Market Makers and Members alike are free to continue to utilize convenience ports for their message traffic as they best see fit, and may continue to access the Exchange through existing logical port offerings at existing rates. The Exchange believes that it is a Member's specific business needs that will drive its decision whether to use Unitized Logical Ports in lieu of, or in addition to, existing logical ports (or, as emphasized, not use them at all). If a Member finds little benefit in having these ports based on its business model and trading strategies, or determines the Unitized Logical ports are not cost-efficient for its needs, or does not provide sufficient value to the firm, such Member may continue connecting to the Exchange in the manner it does today, unchanged. Moreover, the Exchange believes that providing Members the option of purchasing Unitized Logical Ports individually or in sets provides Members further flexibility and an opportunity for cost savings for those Members that wish to only trade a subset of classes. The Exchange has seen firms take advantage of individually priced Unitized Logical Ports when their needs do not require connectivity to all matching engines—further allowing its Members to pay reduced fees relative to a Unitized Logical Port set.

Furthermore, the Exchange notes that undertaking a technological innovation, such as offering a new connectivity option for Members (of which, 57% still utilize at least one FIX or BOEv3 Port through the convenience layer), requires costs and resource allocation. In fact, as the Exchange previously noted, such innovation has improved the infrastructure for all Members of the Exchange. Such innovation is a part of what allows the Exchange to continue to provide access to markets in times of heightened volatility with zero downtime. The new Chairman of the Securities Exchange Commission, Paul Atkins, even recently heighted the importance of innovation by stating “. . . we are getting back to our roots of promoting, rather than stifling, innovation. The markets innovate, and the SEC should not be in the business of telling them to stand still.” [53] In order for exchanges to continue to provide greater options through technological innovation and, in turn, work to improve the resiliency of markets, exchanges must have reasonable certainty around their ability to set fees.

The Exchange also believes that the proposed Unitized Logical Port fees are equitable and not unfairly discriminatory because they continue to be assessed uniformly to similarly situated users in that all Members who choose to purchase Unitized Logical Ports will be subject to the same proposed tiered fee schedule. Moreover, Members purchasing Unitized Logical Ports will only do so if they find a benefit and sufficient value in such ports as all Members can otherwise continue to use the preexisting logical connectivity options.[54] As such, Members can choose whether to purchase Unitized Logical Ports based on their respective business needs.

The proposed ascending tier structure for Unitized Logical Port Sets is reasonable, equitable and not unfairly discriminatory as it is designed to encourage market participants to be efficient with their respective Unitized Logical Port usage. It also is designed so that Members that use a higher allotment of the Exchange's system resources pay higher rates, rather than placing that burden on market participants that have more modest needs. The Exchange believes the proposed ascending fee structure is therefore another appropriate means, in conjunction with an established Unitized Logical Port limit, to manage this finite resource (system capacity) and ensure it is apportioned fairly.

In contrast, MIAX's structure limits its offering to a specific subset of participants, Market Makers, and allocates its ports based on quoting. In contrast, the Exchange and its participants are free to utilize this product at their required level of consumption. Furthermore, the Exchange already assesses higher fees to those that consume more Exchange resources for the existing non-Unitized Bulk Ports.[55] The proposed limit on Unitized Logical Ports is also reasonable, equitable and not unfairly discriminatory as the Exchange believes that it is in the interests of all Members and market participants who access the Exchange to not allow Members to exhaust System resources, but to encourage efficient usage of network capacity. The Exchange also notes that the new BOEv3 unitized architecture is subject to software limitations on the number of sessions that can be created on any one unitized process. Consideration was given to this limitation as well as to the amount of ports firms had indicated they would need prior to the implementation of Unitized Logical Ports.

The Exchange believes the proposed ADO and ADQ fees are reasonable as Members that do not exceed the high thresholds of 2,000,000 ADO and 250,000,000 ADQ will not be charged any fee under the proposed tiers. The Exchange notes that in establishing the proposed thresholds, it evaluated average ADO and ADQ rates over several months and the thresholds were designed to protect the Exchange's Matching Engines from being adversely impacted from sustained and excessive orders/quotes throughout the course of a given month. Further, the Exchange considered the highest levels of ADO and ADQ rates amongst firms and from there, reviewed what would be considered an unreasonable threshold even at the highest levels. The ADQ thresholds are also designed to ensure Market Makers quoting activity, which acts as an important source of liquidity, is not impeded by the proposal.[56] In fact, when setting these thresholds, the Exchange reviewed to ensure that these levels would not prohibit Market Makers from meetings quoting obligations.

The Exchange also believes it is reasonable, equitable and not unfairly discriminatory to assess higher fees when a Member has higher ADO and ADQ rates because the potential impact on exchange systems, bandwidth and capacity becomes greater with increased ADO and ADQ rates. In this regard, the fees are designed to apply only to those Members whose message traffic is noticeably beyond the proposed ADO and ADQ rates. In particular, the proposed fee amounts that correspond to higher ADO and ADQ rates are designed to incentivize Members to reduce excessive order and quoting trade activity that the Exchange believes ( printed page 6715) can be detrimental to all market participants at those levels and encourage such activity to be made in good faith and for legitimate purposes. As of the end of August 2025, the Exchange notes that all but one Member fell within the proposed ADO Tier 1, resulting in that one single Member being assessed additional ADO fees. With regards to ADQ, 9 Members fell into Tier 1 and were not assessed any additional ADQ fees. Additionally, 4 Members fell into Tier 2, 2 Members fell into Tier 3, 2 Members fell into Tier 4, and 1 Member fell into Tier 5, and were assessed related ADQ fees.[57]

Importantly, as noted above, the Exchange believes that it is in the interests of all Members and market participants who access the Exchange to not allow Members to exhaust System resources, but to encourage efficient usage of network capacity. The Exchange therefore also believes that the proposed fees are one method of facilitating the Commission's goal of ensuring that critical market infrastructure has “levels of capacity, integrity, resiliency, availability, and security adequate to maintain their operational capability and promote the maintenance of fair and orderly markets.” [58] Furthermore, the Exchange believes adopting the proposed ADO and ADQ fees are reasonable as unfettered usage of System capacity and network resource consumption can have a detrimental effect on all market participants who access and use the Exchange. As discussed above, high ADO and ADQ rates may adversely impact system resources, bandwidth, and capacity which may, in turn, create latency and impact other Members' ability to receive timely executions.

Moreover, the Exchange believes that the proposed ADO and ADQ fees are equitable and not unfairly discriminatory because they will be assessed uniformly to similarly situated users in that all Members that exceed the thresholds in connection with ADO and ADQ will be assessed the proposed ADO and ADQ rates. Regarding ADO and ADQ, no market participant is assessed any fees unless it exceeds the proposed thresholds. The Exchange also believes it is equitable and not unfairly discriminatory to assess incrementally higher fees to Members that have higher ADO and ADQ rates because the potential impact on exchange systems, bandwidth and capacity becomes greater with increased ADO and ADQ.

Furthermore, the Exchange believes it is equitable and not unfairly discriminatory to aggregate Members trading activity with any affiliated Member sharing at least 75% common ownership [59] in order to prevent members from shifting their order flow or quoting activity to other affiliates in order to circumvent the ADO and ADQ thresholds.

The Exchange lastly believes that its proposal is reasonable, equitably allocated and not unfairly discriminatory because it is not intended to raise revenue for the Exchange; rather, it is intended to encourage efficient behavior so that Members do not exhaust System resources. Moreover, as noted above, competing options exchanges similarly assess fees to deter Members from over utilizing their respective systems by having excessive order and/or quoting trading activity.[60]

Finally, the Exchange notes that it operates in a highly competitive market in which market participants can readily direct order flow to competing venues if they deem fee levels at a particular venue to be excessive or incentives to be insufficient. The Exchange is only one of 18 options exchanges which market participants may direct their order flow and/or participate on, and it represents a small percentage of the overall market.[61] When determining reasonable prices, the Exchange must ensure these are competitive prices in order to maintain market share, as uncompetitive pricing, or prices that Members deem to be excessive, can lead Members to take their order flow to other exchanges.

B. Self-Regulatory Organization's Statement on Burden on Competition

The Exchange does not believe that the proposed rule change to adopt fees for Unitized Logical Ports will impose any burden on intramarket competition that is not necessary in furtherance of the purposes of the Act because the proposed fees for will apply equally to all similarly situated Members. As discussed above, Unitized Logical Ports are optional [62] and Members may choose to utilize Unitized Logical Ports or not, based on their views of the additional benefits and added value provided by these ports. The Exchange believes the proposed fees will be assessed proportionately to the potential value or benefit received by Members with a greater number of Unitized Logical Ports and notes that Members may determine to cease using Unitized Logical Ports should they determine that they are no longer receiving value from these ports. As discussed, Members can also continue to access the Exchange through existing Logical Ports, which fees are not changing. Moreover, while the NYSE Arca Marketplace (“Arca”) and Nasdaq Stock Market, LLC (“Nasdaq”) do not have offerings directly comparable to Unitized Logical Ports, the Exchange notes that Arca's and Nasdaq's port fees are higher than those of the Exchange. Specifically, the Exchange notes that Arca charges a fee of $621 per quoting/order entry port, [63] ( printed page 6716) and Nasdaq assess its members a fee of $575 per FIX order entry port.[64] In both cases, Arca and Nasdaq's port fees are more expensive than the proposed fees for a single BOE Unitized Logical Port ($350/port/month), a single Bulk Unitized Logical Port ($550/port/month), and a single Purge Unitized Logical Port ($400/port/month).

Similarly, the Exchange does not believe that the proposed rule change to adopt ADO and ADQ fees will impose any burden on intramarket competition that is not necessary in furtherance of the purposes of the Act because such fees will apply equally to all similarly situated Members. Particularly, the proposed fees apply uniformly to all Members, in that any Member who exceeds the ADO and/or ADQ Tier 1 thresholds will be subject to a fee under the proposed corresponding tiers. The Exchange believes that the proposed change neither favors nor penalizes one or more categories of market participants in a manner that would impose an undue burden on competition. Rather, the proposal seeks to benefit all market participants by encouraging the efficient utilization of the Exchange's network while taking into account the important liquidity provided by its Members. As discussed above potential impact on exchange systems, bandwidth, and capacity becomes greater with increased ADO and ADQ rates. Accordingly, the Exchange believes that the proposed ADO and ADQ fees do not favor certain categories of market participants in a manner that would impose a burden on competition.

Next, the Exchange believes the proposed rule change does not impose any burden on intermarket competition that is not necessary or appropriate in furtherance of the purposes of the Act. As previously discussed, the Exchange operates in a highly competitive market, including competition for order flow. Market Participants have numerous alternative venues that they may participate on, including 17 other options exchanges (including 3 other Cboe-affiliated options exchanges), as well as off-exchange venues, where competitive products are available for trading. Indeed, participants can readily choose to submit their order flow to other exchange and off-exchange venues if they deem fee levels at those other venues to be more favorable. Moreover, the Commission has repeatedly expressed its preference for competition over regulatory intervention in determining prices, products, and services in the securities markets. Specifically, in Regulation NMS, the Commission highlighted the importance of market forces in determining prices and SRO revenues and, also, recognized that current regulation of the market system “has been remarkably successful in promoting market competition in its broader forms that are most important to investors and listed companies.” [65] The fact that this market is competitive has also long been recognized by the courts. In NetCoalition v. Securities and Exchange Commission , the D.C. Circuit stated as follows: “[n]o one disputes that competition for order flow is `fierce.' . . . As the SEC explained, `[i]n the U.S. national market system, buyers and sellers of securities, and the broker-dealers that act as their order-routing agents, have a wide range of choices of where to route orders for execution'; [and] `no exchange can afford to take its market share percentages for granted' because `no exchange possesses a monopoly, regulatory or otherwise, in the execution of order flow from broker dealers'. . . .”.[66] Accordingly, the Exchange does not believe its proposed change imposes any burden on competition that is not necessary or appropriate in furtherance of the purposes of the Act.

C. Self-Regulatory Organization's Statement on Comments on the Proposed Rule Change Received From Members, Participants, or Others

The Exchange neither solicited nor received comments on the proposed rule change.

III. Date of Effectiveness of the Proposed Rule Change and Timing for Commission Action

The foregoing rule change has become effective pursuant to Section 19(b)(3)(A) of the Act [67] and paragraph (f) of Rule 19b-4 [68] thereunder. At any time within 60 days of the filing of the proposed rule change, the Commission summarily may temporarily suspend such rule change if it appears to the Commission that such action is necessary or appropriate in the public interest, for the protection of investors, or otherwise in furtherance of the purposes of the Act. If the Commission takes such action, the Commission will institute proceedings to determine whether the proposed rule change should be approved or disapproved.

IV. Solicitation of Comments

Interested persons are invited to submit written data, views and arguments concerning the foregoing, including whether the proposed rule change is consistent with the Act. Comments may be submitted by any of the following methods:

Electronic Comments

- Use the Commission's internet comment form (https://www.sec.gov/rules/sro.shtml); or

- Send an email torule-comments@sec.gov. Please include file number SR-CboeBZX-2026-011 on the subject line.

Paper Comments

- Send paper comments in triplicate to Secretary, Securities and Exchange Commission, 100 F Street NE, Washington, DC 20549-1090.

All submissions should refer to file number SR-CboeBZX-2026-011. This file number should be included on the subject line if email is used. To help the Commission process and review your comments more efficiently, please use only one method. The Commission will post all comments on the Commission's internet website ( https://www.sec.gov/rules/sro.shtml). Copies of the filing will be available for inspection and copying at the principal office of the Exchange. Do not include personal identifiable information in submissions; you should submit only information that you wish to make available publicly. We may redact in part or withhold entirely from publication submitted material that is obscene or subject to copyright protection. All submissions should refer to file number SR-CboeBZX-2026-011 and should be submitted on or before March 5, 2026.

For the Commission, by the Division of Trading and Markets, pursuant to delegated authority.[69]

Sherry R. Haywood,

Assistant Secretary.