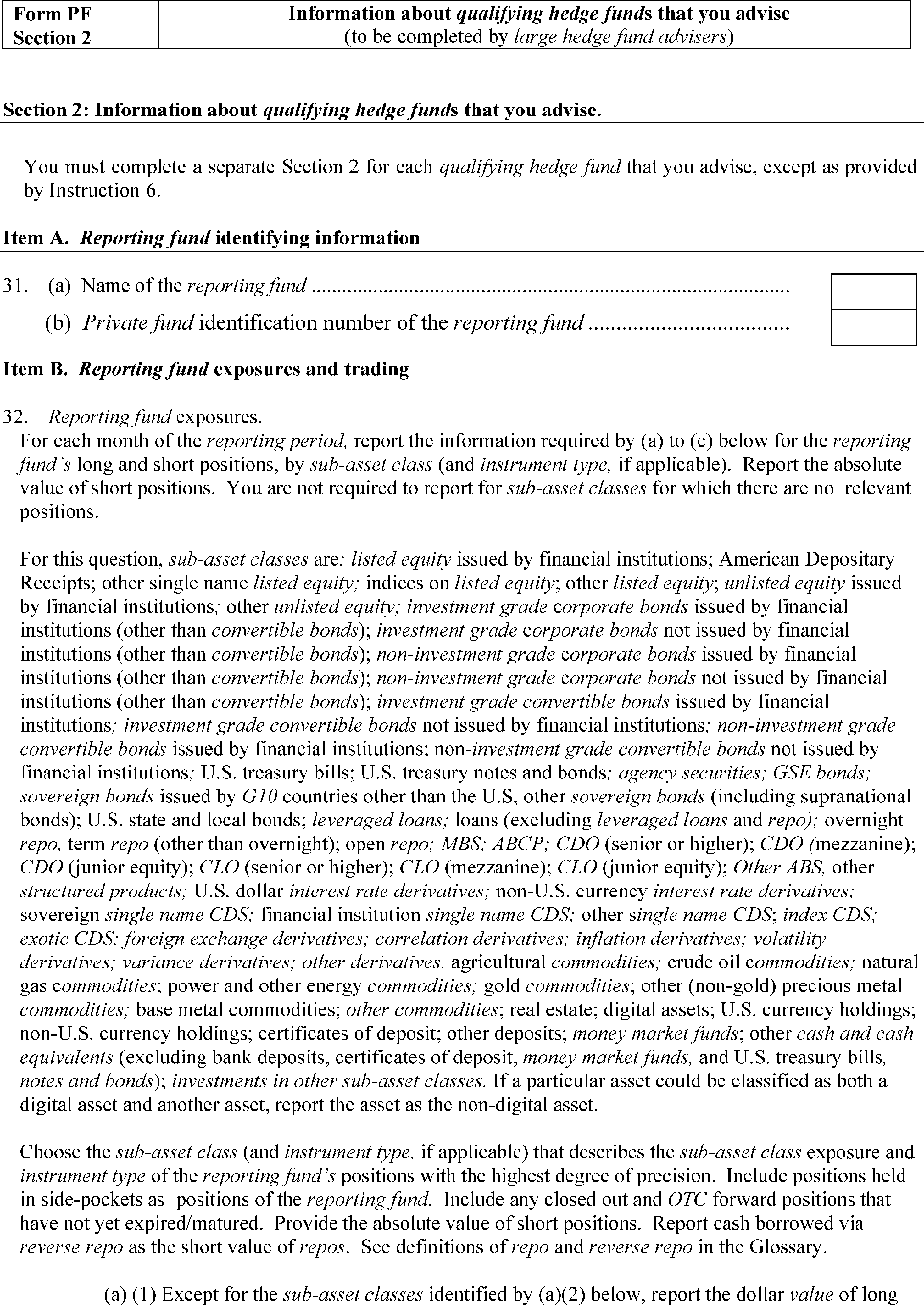

The Commodity Futures Trading Commission (the "CFTC") and the Securities and Exchange Commission (the "SEC") (collectively, "we" or the "Commissions") are proposing to amend For...

Commodity Futures Trading Commission and Securities and Exchange Commission.

ACTION:

Joint proposed rules.

SUMMARY:

The Commodity Futures Trading Commission (the “CFTC”) and the Securities and Exchange Commission (the “SEC”) (collectively, “we” or the “Commissions”) are proposing to amend Form PF, the confidential reporting form for certain SEC-registered investment advisers to private funds, including those that also are registered with the CFTC as a commodity pool operator (a “CPO”) or a commodity trading advisor (a “CTA”). The proposed amendments would eliminate certain filing and reporting obligations, streamline certain requirements, and make corrections and other revisions. The proposed amendments are designed to eliminate certain burdens, among other things.

DATES:

This proposal was published in the

Federal Register

on April 24, 2026. Comments should be received on or before June 23, 2026.

ADDRESSES:

Comments may be submitted by any of the following methods.

CFTC:

Comments may be submitted to the CFTC by any of the following methods.

CFTC Comments Portal: https://comments.cftc.gov.

Follow the instructions for submitting comments through the website.

Mail:

Christopher Kirkpatrick, Secretary of the Commission, Commodity Futures Trading Commission, Three Lafayette Centre, 1155 21st Street NW, Washington, DC 20581.

Hand Delivery/Courier:

Follow the same instructions as for Mail above.

Please submit your comments using only one method. To avoid possible delays with mail or in-person deliveries, submissions through the CFTC website are encouraged. “Form PF” must be in the subject field of comments submitted via email, and clearly indicated on written submissions. All comments must be submitted in English, or if not, accompanied by an English translation. Comments will be posted as received to

www.cftc.gov.

You should submit only information that you wish to make available publicly. If you wish the CFTC to consider information that may be exempt from disclosure under the Freedom of Information Act, a petition for confidential treatment of the exempt information may be submitted according to the established procedures in 17 CFR 145.9.

The CFTC reserves the right, but shall have no obligation, to review, prescreen, filter, redact, refuse, or remove any or all of your submission from

www.cftc.gov

that it may deem to be inappropriate for publication, including, but not limited to, obscene language. All submissions that have been redacted or removed that contain comments on the merits of the rulemaking will be retained in the public comment file and will be considered as required under the Administrative Procedure Act and other applicable laws, and may be accessible under the Freedom of Information Act, 5 U.S.C. 552,

et seq.

(“FOIA”).

SEC:

Comments may be submitted by any of the following methods:

Send an email torule-comments@sec.gov.

Please include File Number S7-2026-13 on the subject line.

Paper Comments

Send paper comments to Secretary, Securities and Exchange Commission, 100 F Street NE, Washington, DC 20549-1090.

All submissions should refer to File Number S7-2026-13. This file number should be included on the subject line if email is used. To help the Commission process and review your comments more efficiently, please use only one method of submission. The Commission will post all comments on the Commission's website (

https://www.sec.gov/rules-regulations/rulemaking-activity). Do not include personal identifiable information in submissions; you should submit only information that you wish to make available publicly. We may redact in part or withhold entirely from publication submitted material that is obscene or subject to copyright protection.

Studies, memoranda, or other substantive items may be added by the Commission or staff to the comment file during this rulemaking. A notification of the inclusion in the comment file of any such materials will be made available on the Commission's website. To ensure direct electronic receipt of such notifications, sign up through the “Stay Connected” option at

www.sec.gov

to receive notifications by email.

CFTC:

Michael Ehrstein or Elizabeth Groover, Special Counsels, at (202) 418-6700, Commodity Futures Trading Commission, Three Lafayette Centre, 1155 21st Street NW, Washington, DC 20581.

SEC:

Alexis Palascak, Janet Jun, and Daniel Levine, Senior Counsels; Adele Kittredge Murray, Private Funds Attorney Fellow; or Robert Holowka, Acting Assistant Director, Investment Adviser Regulation Office, at (202) 551-6787, Division of Investment Management, Securities and Exchange Commission, 100 F Street NE, Washington, DC 20549-8549.

SUPPLEMENTARY INFORMATION:

The CFTC and SEC are requesting public comment on the following under the Investment Advisers Act of 1940 [15 U.S.C. 80b] (“Advisers Act”).[1]

A. Increase the Filing Threshold for All Form PF Filers

B. Increase the Reporting Threshold for Large Hedge Fund Advisers

C. Disregarded Feeder Funds

D. Eliminate the Look Through Requirement

E. Trading Vehicles

F. Eliminate Form PF Question 23(c) Volatility Reporting

G. Eliminate Certain Trading and Clearing Reporting

( printed page 22233)

H. Eliminate Form PF Question 32(b)(2) Adjusted Exposure Reporting Based on Internal Methodology

I. Eliminate Form PF Question 34 Monthly Asset Turnover Reporting

J. Simplify Industry Concentration Reporting in Form PF Question 36

K. Eliminate Certain Questions Concerning Qualifying Hedge Funds' Exposures to Reference Assets

L. Simplify Large Hedge Fund Adviser Counterparty Exposure Reporting

M. Eliminate Rehypothecation Reporting

N. Amendments to Large Hedge Fund Adviser Current Reporting

1. Modify the Current Reporting Filing Deadline

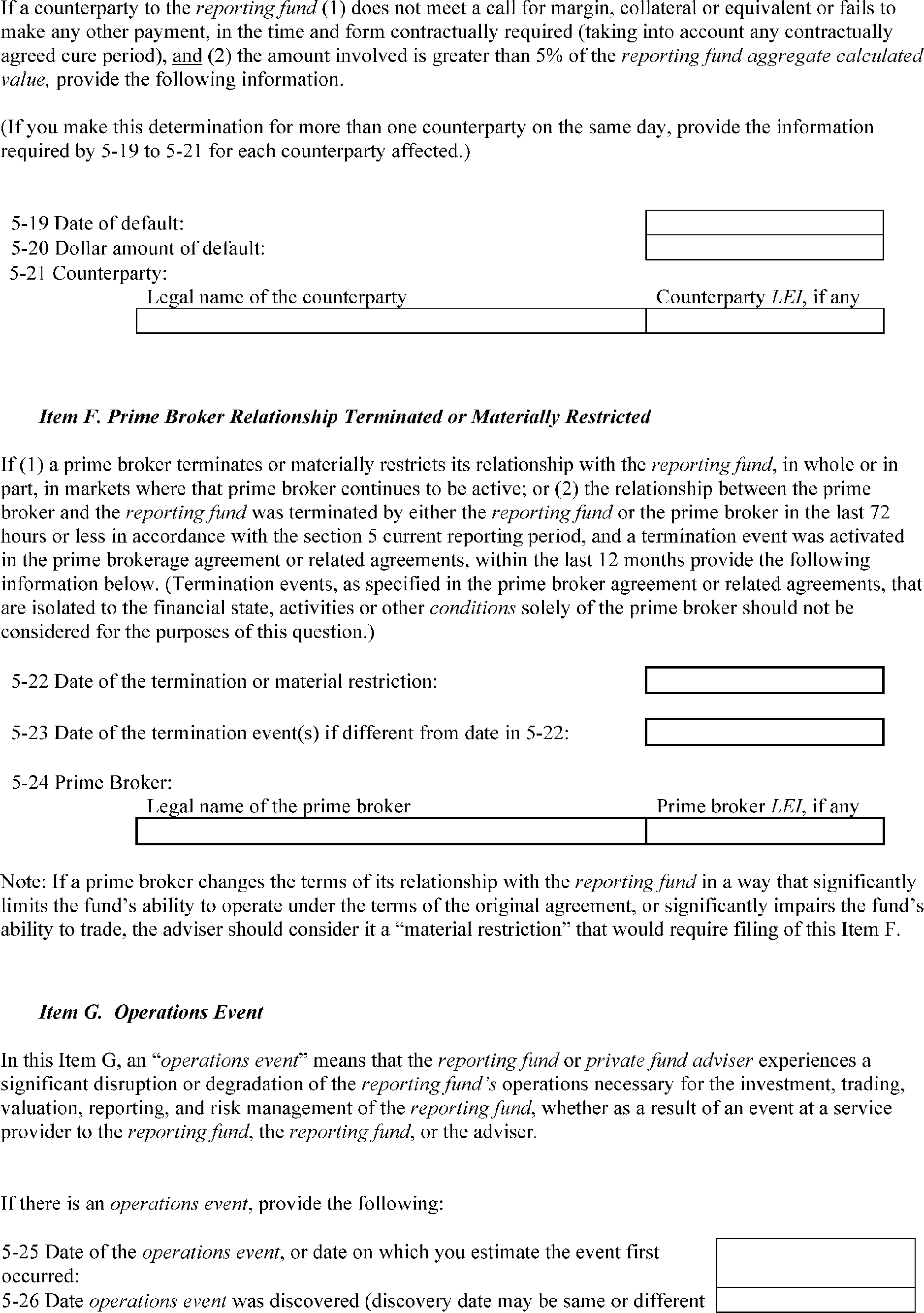

2. Eliminate Current Reporting for Notice of Margin Default or Determination of Inability To Meet a Call for Margin, Collateral or Equivalents

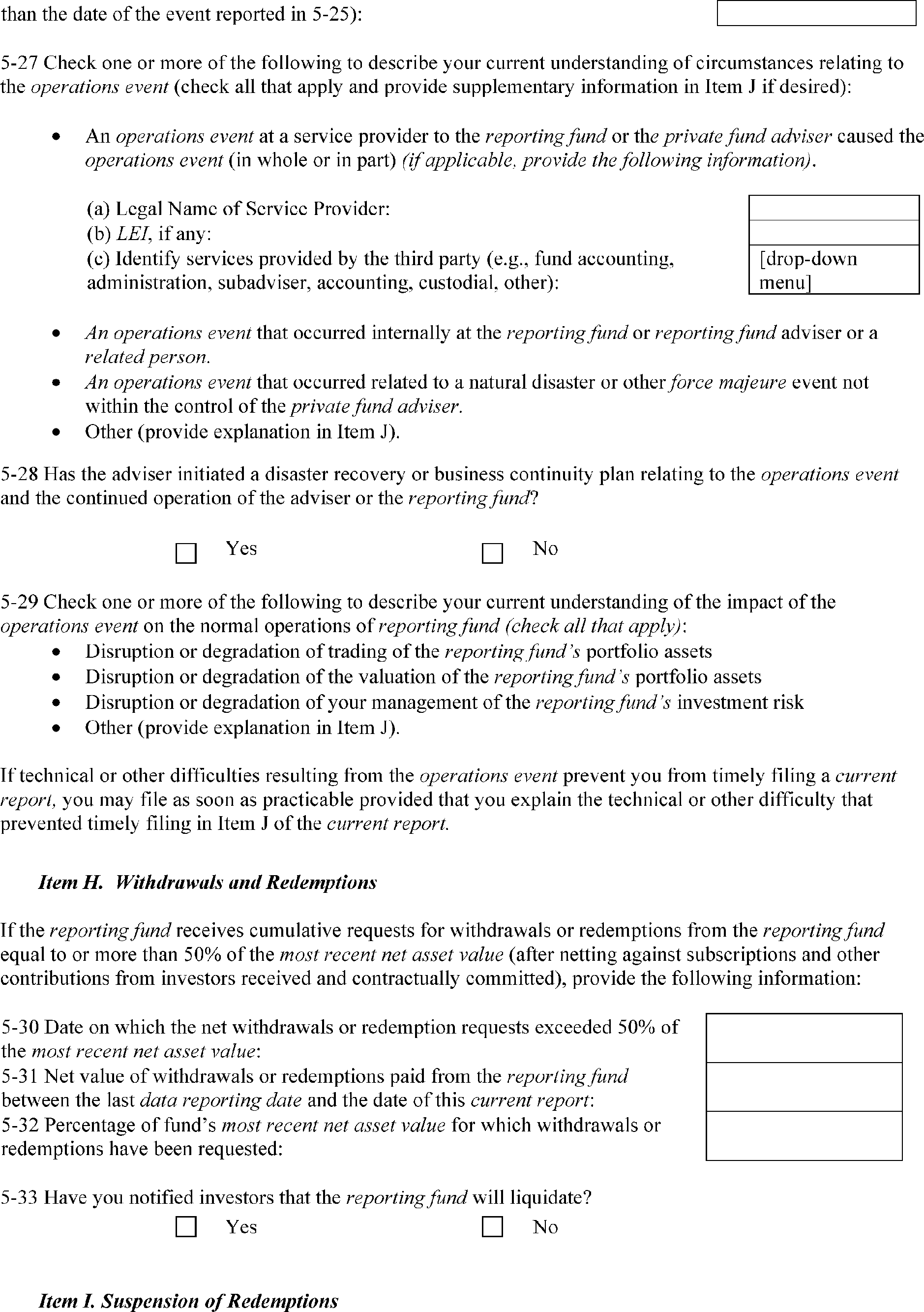

3. Streamline Reporting of “Operations Events”

4. Eliminate Current Reporting for Inability To Satisfy Redemption Requests

O. Eliminate Form PF Private Equity Quarterly Reporting in Section 6

P. Other Corrections and Revisions

Q. Request for Comments on Private Credit Reporting

R. Proposed Transition Period

III. Economic Analysis

A. Introduction

B. Baseline

1. Regulatory Baseline

2. Affected Parties

C. Benefits and Costs

1. General Considerations

2. Increase the Filing Threshold for All Form PF Filers

3. Increase the Reporting Threshold for Large Hedge Fund Advisers

4. Disregarded Feeder Funds

5. Eliminate the Look Through Requirement

6. Trading Vehicles

7. Eliminate Form PF Question 23(c) Volatility Reporting

8. Eliminate Certain Trading and Clearing Reporting

9. Eliminate Form PF Question 32(b)(2) Adjusted Exposure Netting Based on Internal Methodologies

10. Eliminate Form PF Question 34 Monthly Asset Turnover Reporting

11. Simplify Industry Concentration Reporting in Form PF Question 36

12. Eliminate Certain Questions Concerning Qualifying Hedge Funds' Exposures To Reference Assets

13. Simplify Large Hedge Fund Adviser Counterparty Exposure Reporting

14. Eliminate Rehypothecation Reporting

15. Amendments to Large Hedge Fund Adviser Current Reporting

16. Eliminate Form PF Private Equity Quarterly Reporting in Section 6

17. Other Corrections and Revisions

18. Quantification of Benefits

D. Present Values and Annualized Values of Monetized Benefits and Costs

E. Effects on Efficiency, Competition, and Capital Formation

F. Reasonable Alternatives

1. Filing Threshold

2. Reporting Threshold for Large Hedge Fund Advisers

3. Disregarded Feeder Fund

4. Industry Concentration Reporting

5. Hedge Fund Adviser Counterparty Exposure Reporting

6. Private Equity Quarterly Event Reporting

7. Private Credit Reporting

G. Request for Comment

IV. Paperwork Reduction Act

A. Form PF

1. Purpose and Use of the Information Collection

2. Confidentiality

3. Burden Estimates

B. Request for Comments

V. Regulatory Flexibility Act Certification

VI. Congressional Review Act

VII. Other Matters

VIII. Statutory Authority

I. Introduction

The Commissions are proposing to amend Form PF, the confidential reporting form that certain SEC-registered investment advisers, including those that also are registered with the CFTC as a CPO or a CTA, use to report information about the private funds they advise.[2]

Form PF is a joint form between the SEC and the CFTC with regard to sections 1 and 2. Sections 3, 4, 5 and 6 were adopted solely by the SEC. For this proposal, the SEC and the CFTC are jointly amending the joint sections of the form and the SEC is amending the SEC-only sections of the form. The proposed amendments would eliminate filing obligations for certain advisers, eliminate and streamline certain reporting requirements, and make corrections as well as other revisions. The proposed amendments are designed to eliminate certain burdens, among other things, while ensuring Form PF continues to collect information necessary and appropriate in the public interest and for the protection of investors, or for the assessment of systemic risk in the U.S. financial system by the Financial Stability Oversight Council (“FSOC”).[3]

In 2010, the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the “Dodd-Frank Act”) mandated that the SEC and the CFTC, after consultation with FSOC, jointly promulgate rules to establish the form and content of private fund reports required to be filed with the SEC under the Advisers Act, and with the CFTC by investment advisers that are registered both under the Advisers Act and the Commodity Exchange Act.[4]

The Advisers Act further mandates that an adviser must maintain records and reports for each private fund it advises, that include a description of the following: (1) the amount of assets under management and use of leverage, including off-balance-sheet leverage; (2) counterparty credit risk exposure; (3) trading and investment positions; (4) valuation policies and practices of the fund; (5) types of assets held; (6) side arrangements or side letters, whereby certain investors in a fund obtain more favorable rights or entitlements than other investors; (7) trading practices; and (8) such other information as the SEC, in consultation with FSOC, determines is necessary and appropriate in the public interest and for the protection of investors or for the assessment of systemic risk, which may include the establishment of different reporting requirements for different classes of fund advisers, based on the type or size of private fund being advised.[5]

In response to these mandates, the Commissions adopted Form PF in 2011 and have amended Form PF multiple times, including substantively in 2023 and 2024.[6]

In 2023, among other things, the SEC added requirements for (1) large hedge fund advisers to submit current reports about certain events at their qualifying hedge funds, and (2) private equity fund advisers to submit certain quarterly reports.[7]

In 2024, the Commissions comprehensively amended Form PF (the “2024 amendments”), but delayed the compliance date several times, including most recently until October 1, 2026.[8]

As a result, advisers have been

( printed page 22234)

allowed to continue to file the version of Form PF in effect before the adoption of the 2024 amendments. The Commissions delayed the compliance date to (1) address certain challenges associated with the reporting cycle timing, (2) provide the industry more time to comply with the 2024 amendments, and (3) provide the Commissions time to complete a review in accordance with a Presidential Memorandum issued by President Donald J. Trump.[9]

Specifically, on January 20, 2025, the President issued a Presidential Memorandum directing agencies to consider postponing the effective date of any rules that had been published in the

Federal Register

, or that were issued but had not yet taken effect, for the purpose of reviewing any questions of fact, law, and policy that the rules may raise. The Presidential Memorandum further provides that, for those rules that raise substantial questions of fact, law, or policy, agencies should provide notice and take further appropriate action.

In accordance with the Presidential Memorandum, the Commissions determined to conduct a comprehensive review that extended to the entire form. As a result of this comprehensive review, we are proposing several changes to Form PF that are designed to eliminate certain burdens, streamline certain requirements, and make corrections, as well as other revisions:

First, we propose to eliminate filing requirements for smaller advisers, irrespective of the categories of private funds they advise. Specifically, we propose to raise the filing threshold for all filers, from $150 million in private fund assets under management to $1 billion.[10]

We estimate that this proposed change would eliminate filing obligations for almost half of the advisers that currently must file Form PF.[11]

We further estimate that with this proposed filing threshold, Form PF would continue to obtain information on over 90 percent of private fund gross asset value that advisers report.[12]

Therefore, this proposed change is designed to eliminate filing burdens for smaller advisers, while continuing to collect data on a significant percentage of private fund assets.

Second, we propose to eliminate certain reporting requirements for smaller hedge fund advisers. Specifically, we propose to raise the reporting threshold for large hedge fund advisers from $1.5 billion in hedge fund assets under management to $10 billion.[13]

We estimate that this proposed change would eliminate certain reporting obligations for almost two-thirds of advisers that currently must report as large hedge fund advisers.[14]

We estimate that with this proposed reporting threshold, Form PF would continue to obtain information quarterly on over 80 percent of hedge fund gross asset value that advisers report.[15]

Therefore, this proposed change is designed to eliminate certain reporting burdens for smaller hedge fund advisers, while continuing to obtain information on a substantial portion of the assets of the hedge fund industry.

Third, we propose to eliminate certain requirements, including quarterly event reporting, certain current reporting, and other requirements, as well as streamline certain requirements, and make corrections and other revisions.

Table 1a summarizes the proposed changes to the filing threshold for all Form PF filers and the reporting threshold for large hedge fund advisers:

Table 1

a

—Proposal To Increase Certain Thresholds

Eliminate filing requirements for smaller advisers

We propose to increase the filing threshold for all filers from $150 million in private fund assets under management to $1 billion. (Rule 204(b)-1(a) and General Instruction 1.)

Eliminate certain reporting requirements for smaller hedge fund advisers

We propose to increase the reporting threshold for large hedge fund advisers from $1.5 billion in hedge fund assets under management to $10 billion. (General Instruction 3.)

Table 1b summarizes the proposed changes to the reporting obligations:

Table 1

b

—Proposed Changes To Reporting Obligations

Eliminate separate reporting for certain feeder funds

Currently, filers must separately report each component fund of master-feeder arrangements and parallel fund structures, except under certain limited circumstances.

We propose to eliminate this separate reporting requirement for any feeder fund that has

de minimis

holdings outside a single master fund, U.S. treasury bills, and/or cash and cash equivalents. (General Instruction 6.)

Eliminate “look through” requirements

Currently, Form PF provides instructions for where a filer should “look through” a reporting fund's investments in other private funds and entities.

We propose to eliminate the prescriptive “look through” requirements and allow filers to report indirect exposures based on reasonable estimates that are consistent with their internal methodologies and the conventions of service providers. (General Instructions 7 and 8, and conforming amendments to certain questions and asset classes in the Glossary of Terms.)

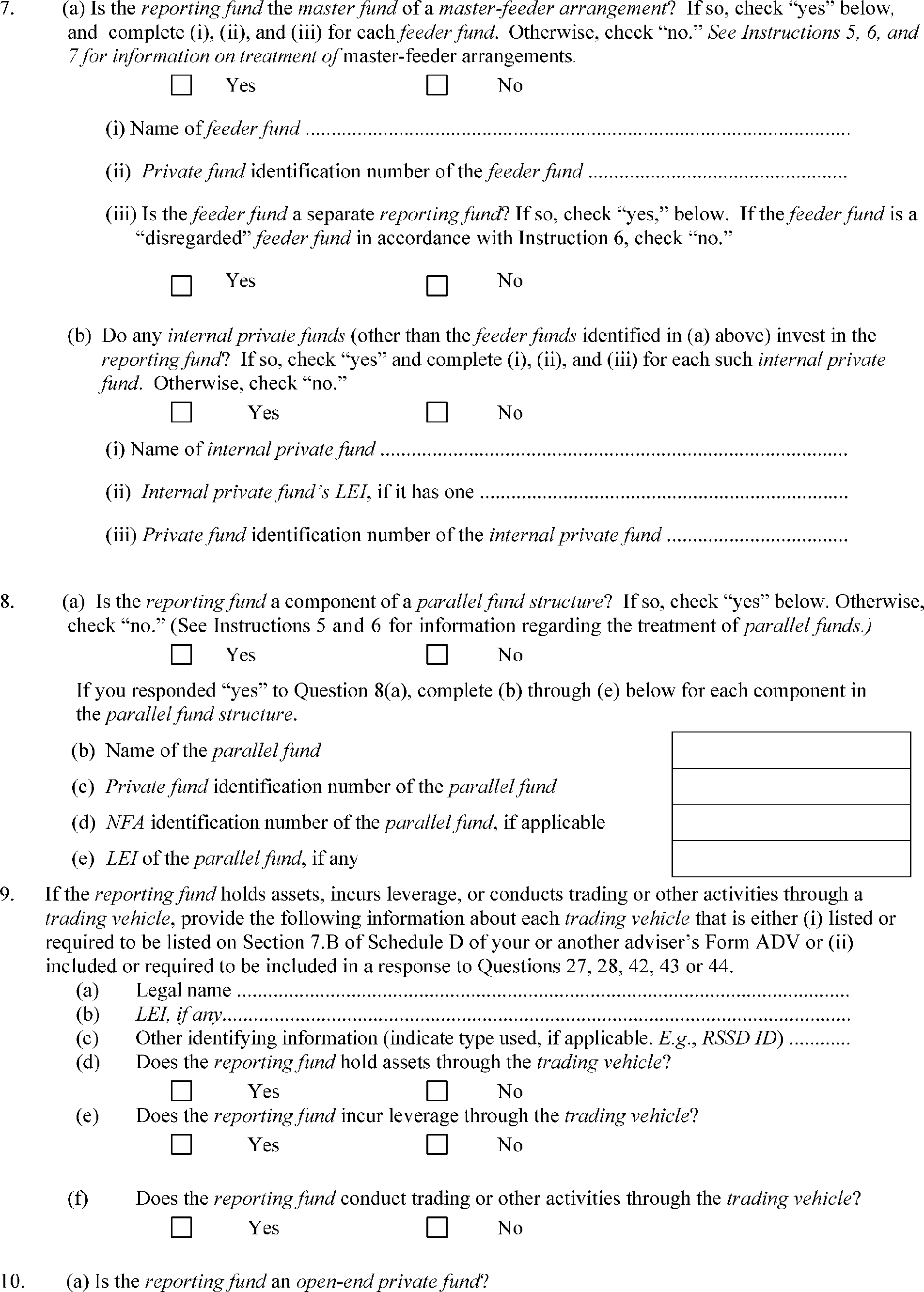

Eliminate identification requirements for certain trading vehicles

Currently, if a reporting fund holds assets, incurs leverage, or conducts trading or other activities through a trading vehicle, the adviser must provide identifying information about each such trading vehicle.

We propose to narrow the universe of trading vehicles that advisers must identify. (Question 9.)

( printed page 22235)

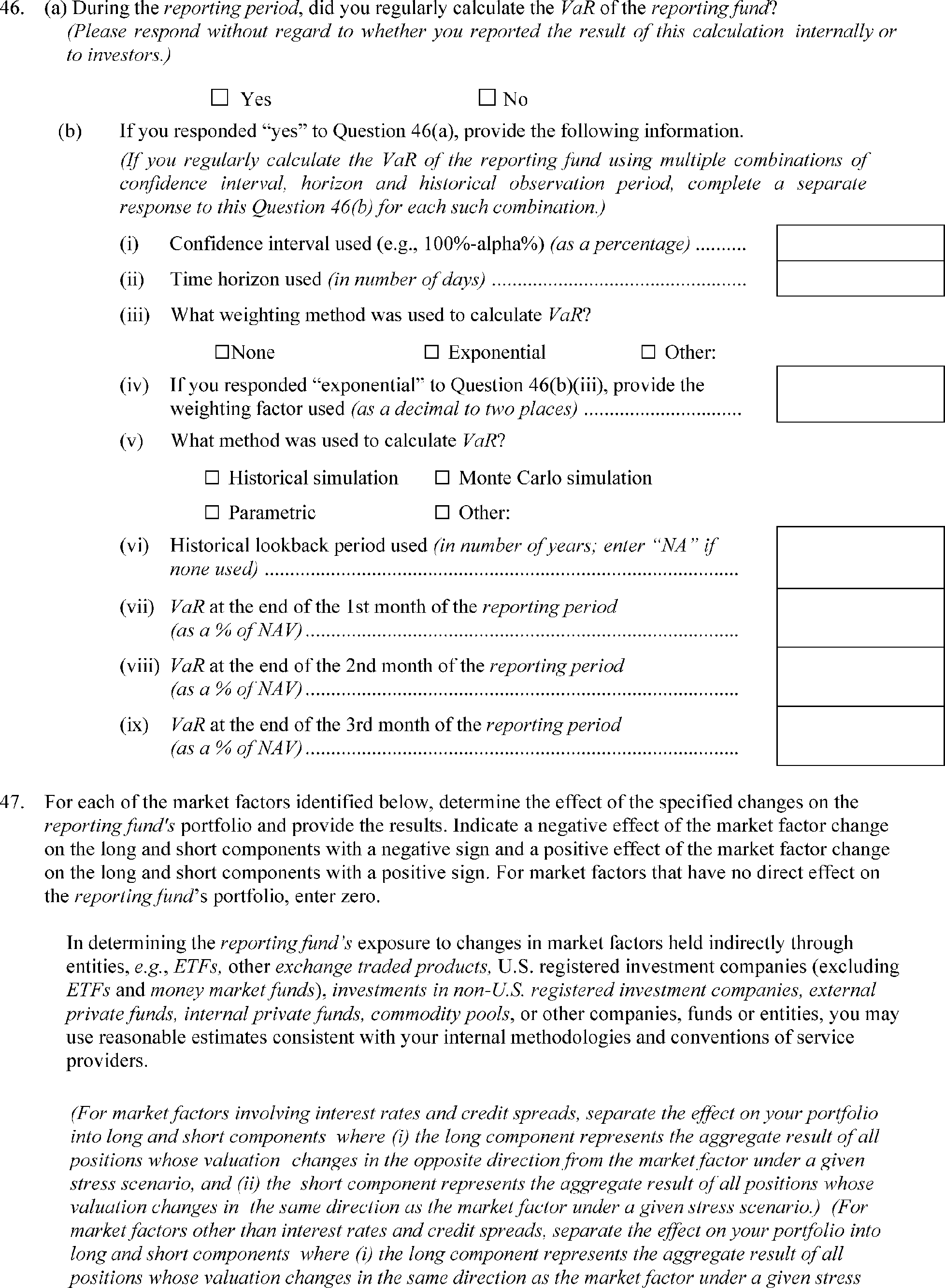

Eliminate certain performance volatility reporting requirements

Currently, if an adviser calculates a market value on a daily basis for any position in the reporting fund's portfolio, it must report certain volatility information including aggregated calculated values, monthly annualized volatility of returns, and other data associated with the daily rates-of-return.

We propose to eliminate these requirements. (Question 23(c).)

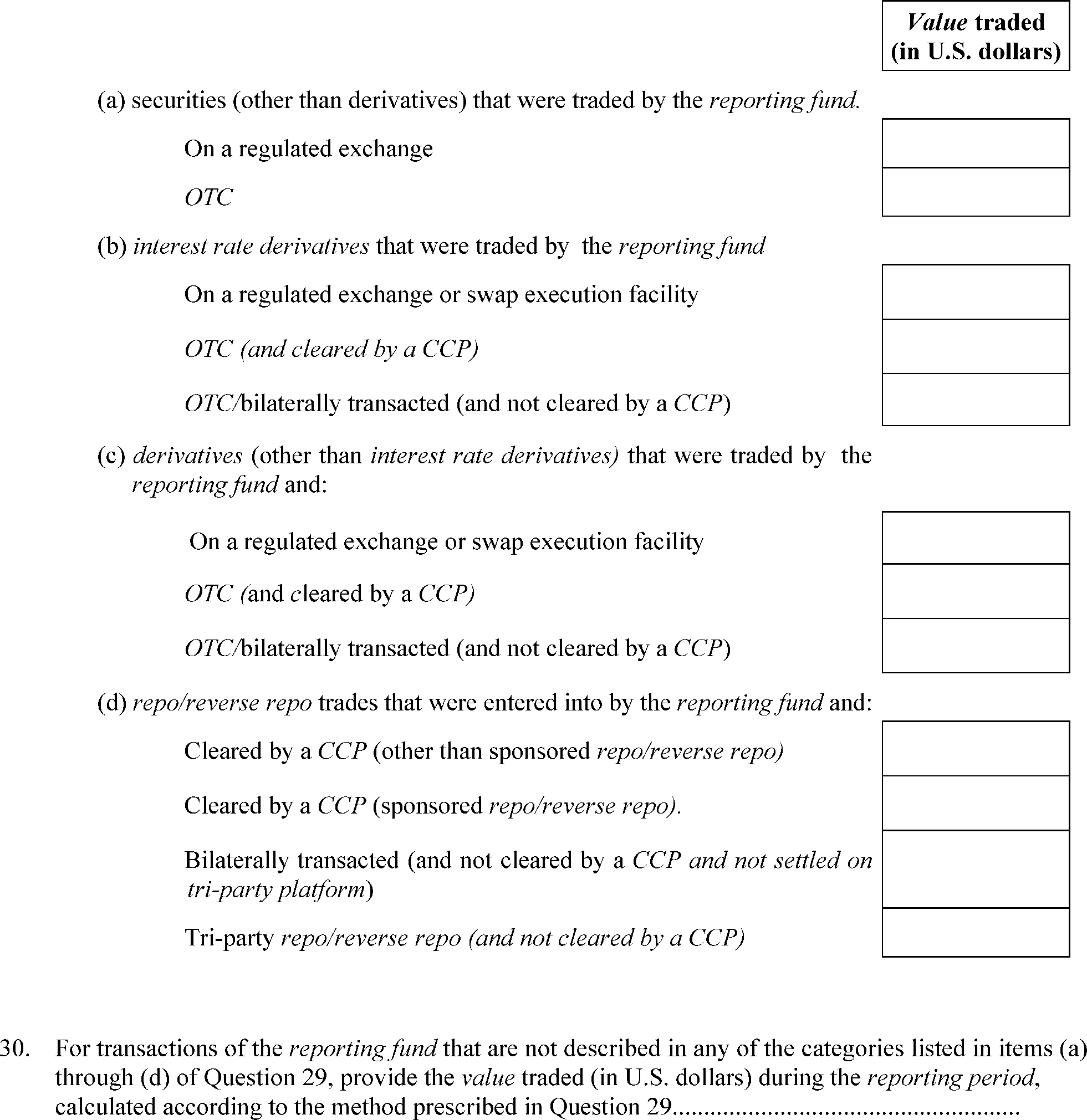

Eliminate certain trading and clearing reporting requirements

Currently, filers must report how they use trading and clearing mechanisms, including the value traded over the reporting period and the value of positions at the end of the reporting period.

We propose to eliminate the requirement to report the value of positions at the end of the reporting period. (Questions 29 and 30.)

Streamline adjusted exposure reporting

Currently, large hedge fund advisers must report their qualifying hedge funds' monthly adjusted exposures using multiple methods.

We propose to eliminate one of the methods, so advisers would no longer be required to report additional adjusted exposure based on the adviser's internal methodologies. (Question 32.)

Eliminate portfolio turnover reporting

Currently, large hedge fund advisers must report the value of their qualifying hedge funds' monthly turnover by asset class.

We propose to eliminate this question. (Question 34.)

Reduce burdens associated with reporting North American Industry Classification System (“NAICS”) codes

Currently, large hedge fund advisers must report their qualifying hedge funds' monthly industry exposures when they exceed a certain amount, using the six-digit NAICS code that best describes a company's primary business activity and principal source of revenue.

We propose to provide flexibility to allow filers to report fewer digits of the NAICS codes for industry exposures. (Question 36;

see

the Glossary of Terms (defining “NAICS code.”)

Eliminate certain reporting concerning qualifying hedge funds' monthly exposures to reference assets and, instead, include streamlined exposure reporting under an existing extraordinary loss current report trigger

Currently, large hedge fund advisers must report details about their qualifying hedge funds' monthly concentrated exposure to specific, position-level reference assets.

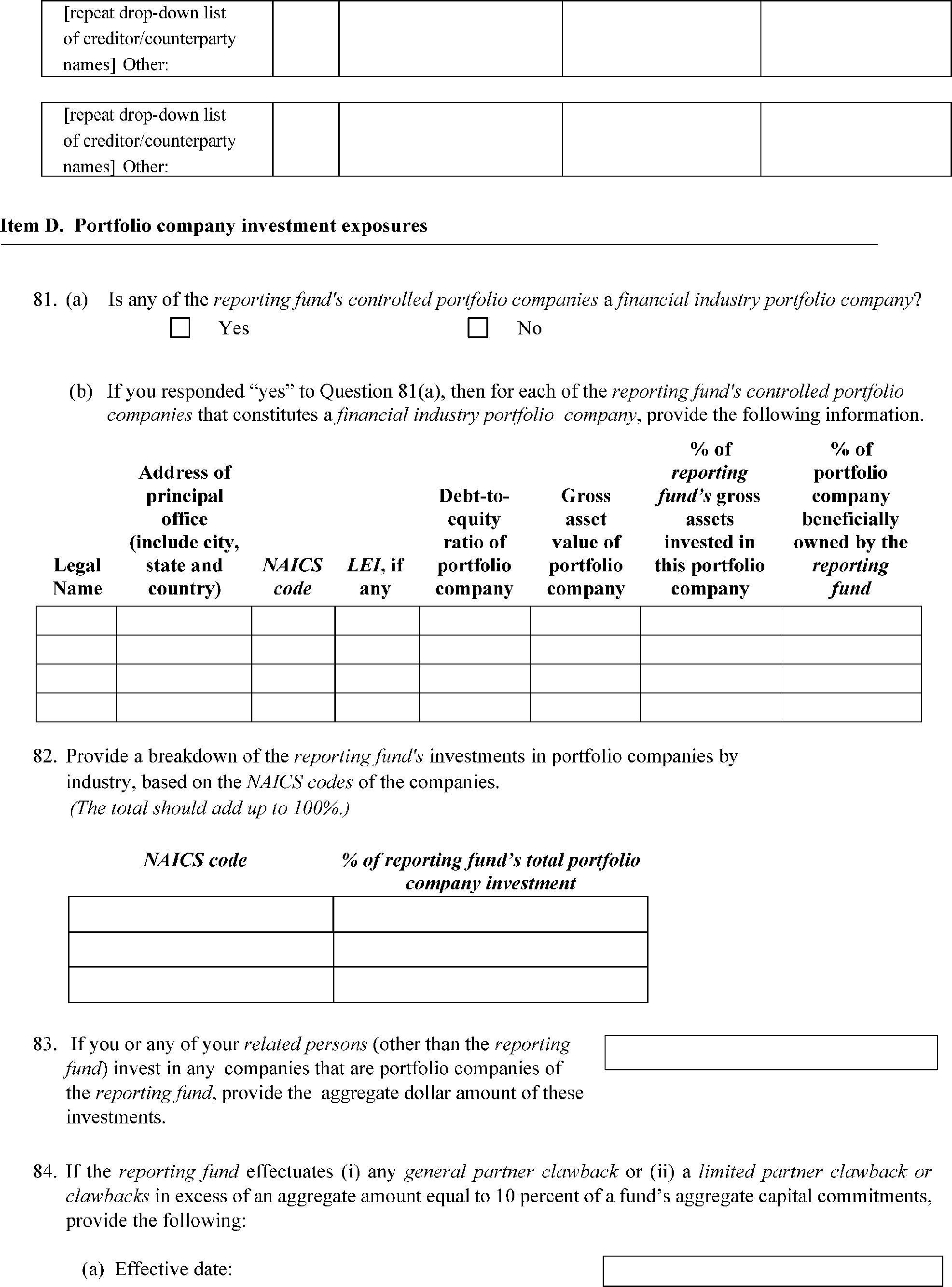

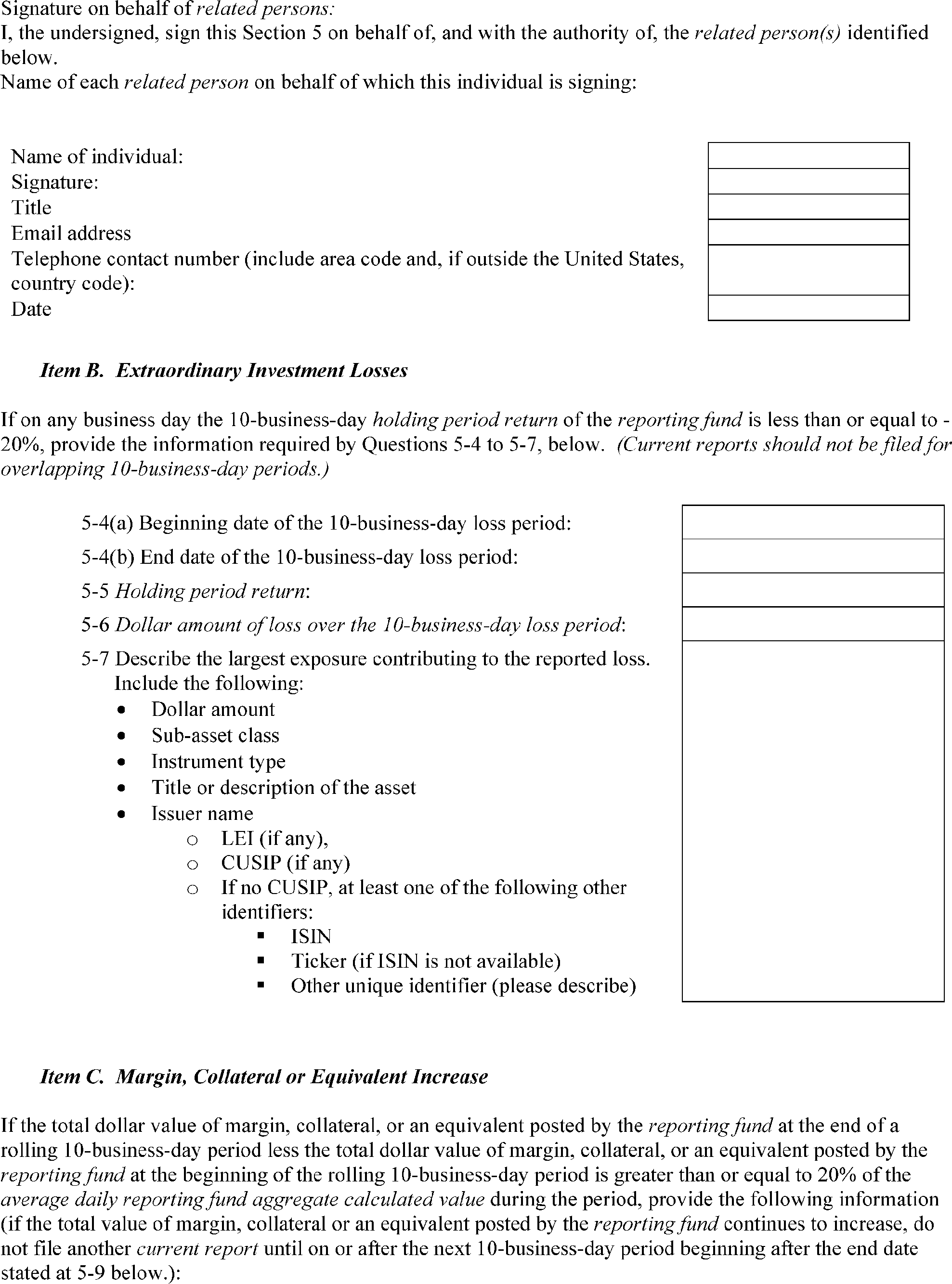

We propose to eliminate those questions. Instead, if large hedge fund advisers file a current report about their qualifying hedge funds' extraordinary investment losses, they would include a description of the largest exposure contributing to the loss. (Questions 39 and 40, and section 5, Item B.)

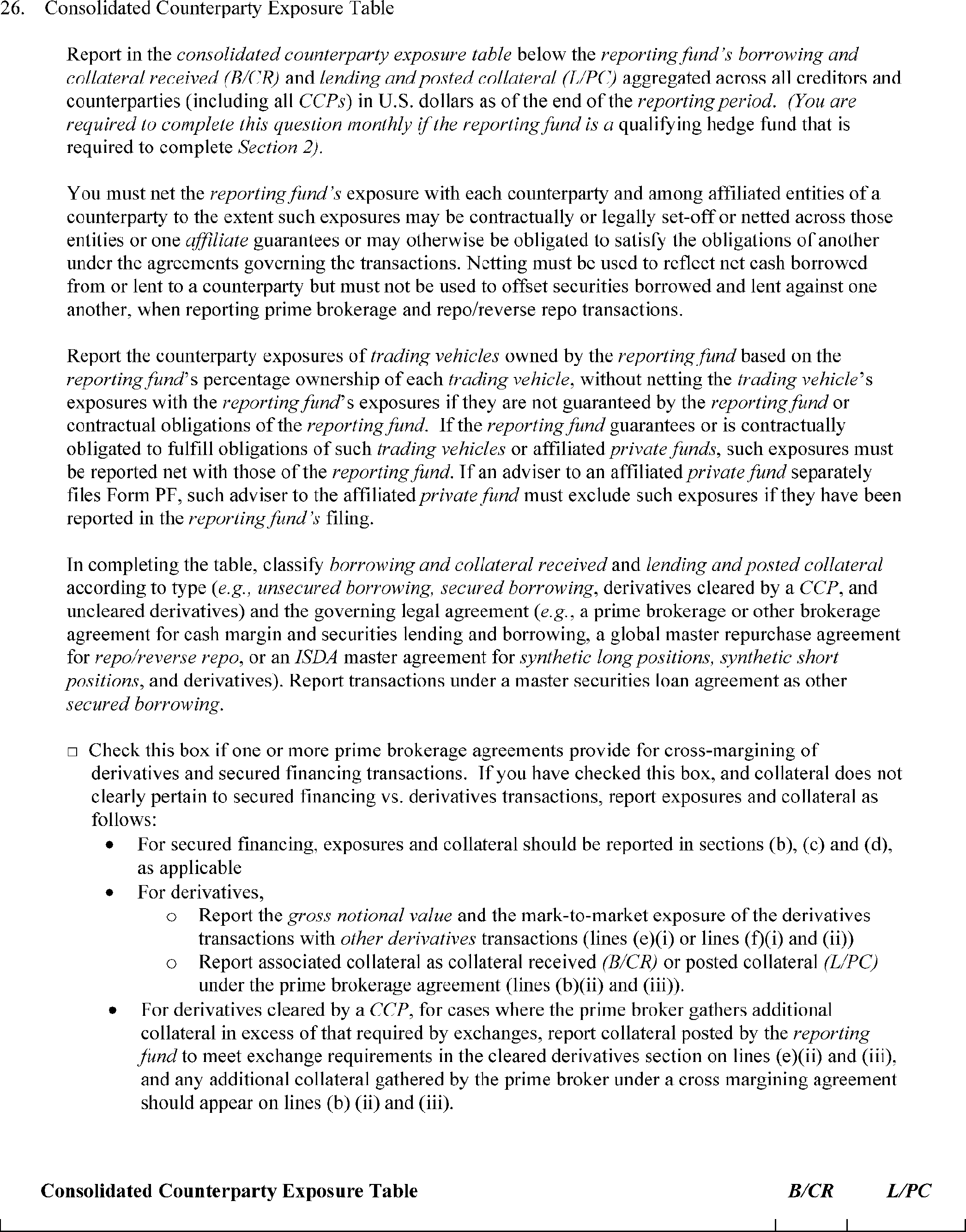

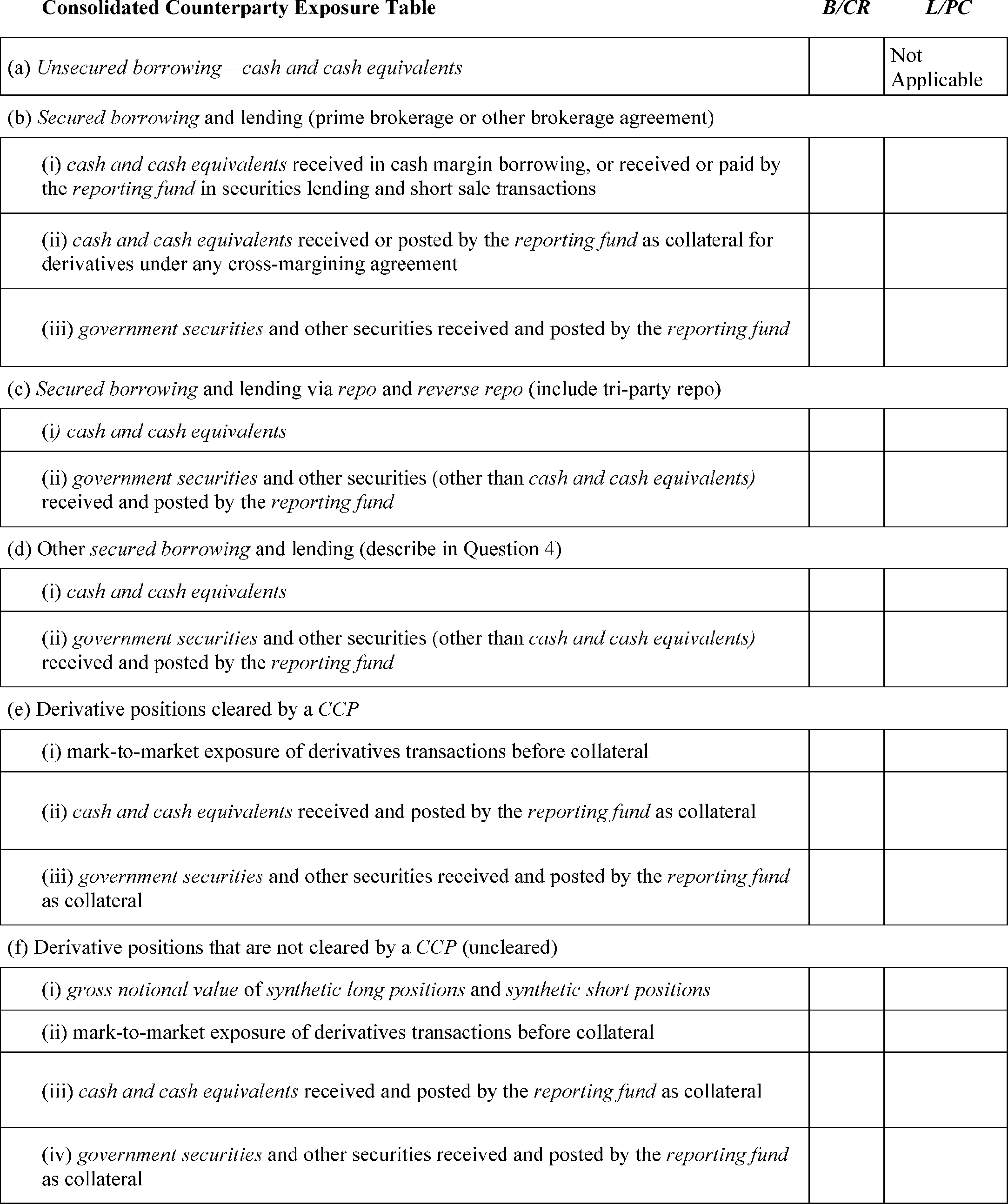

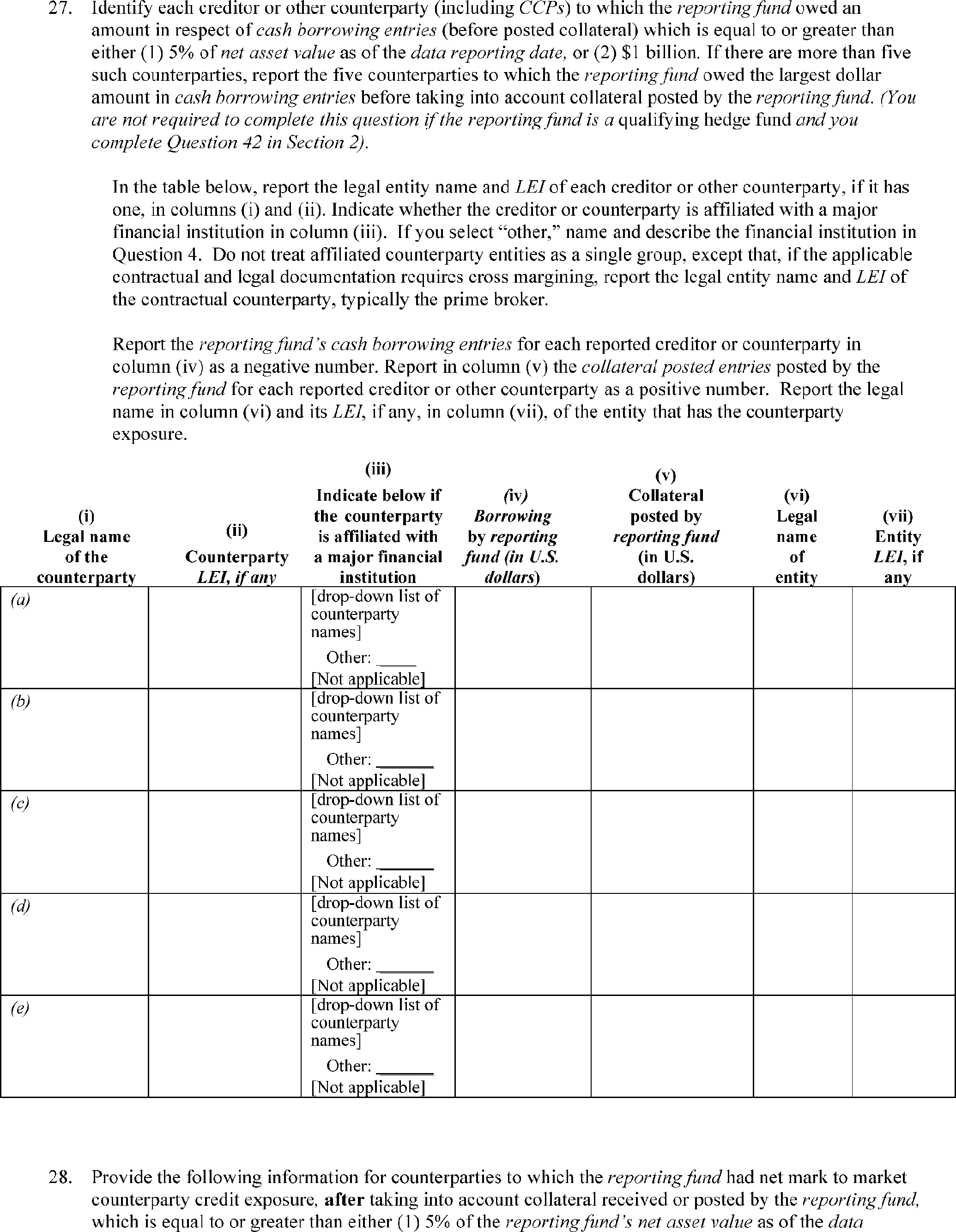

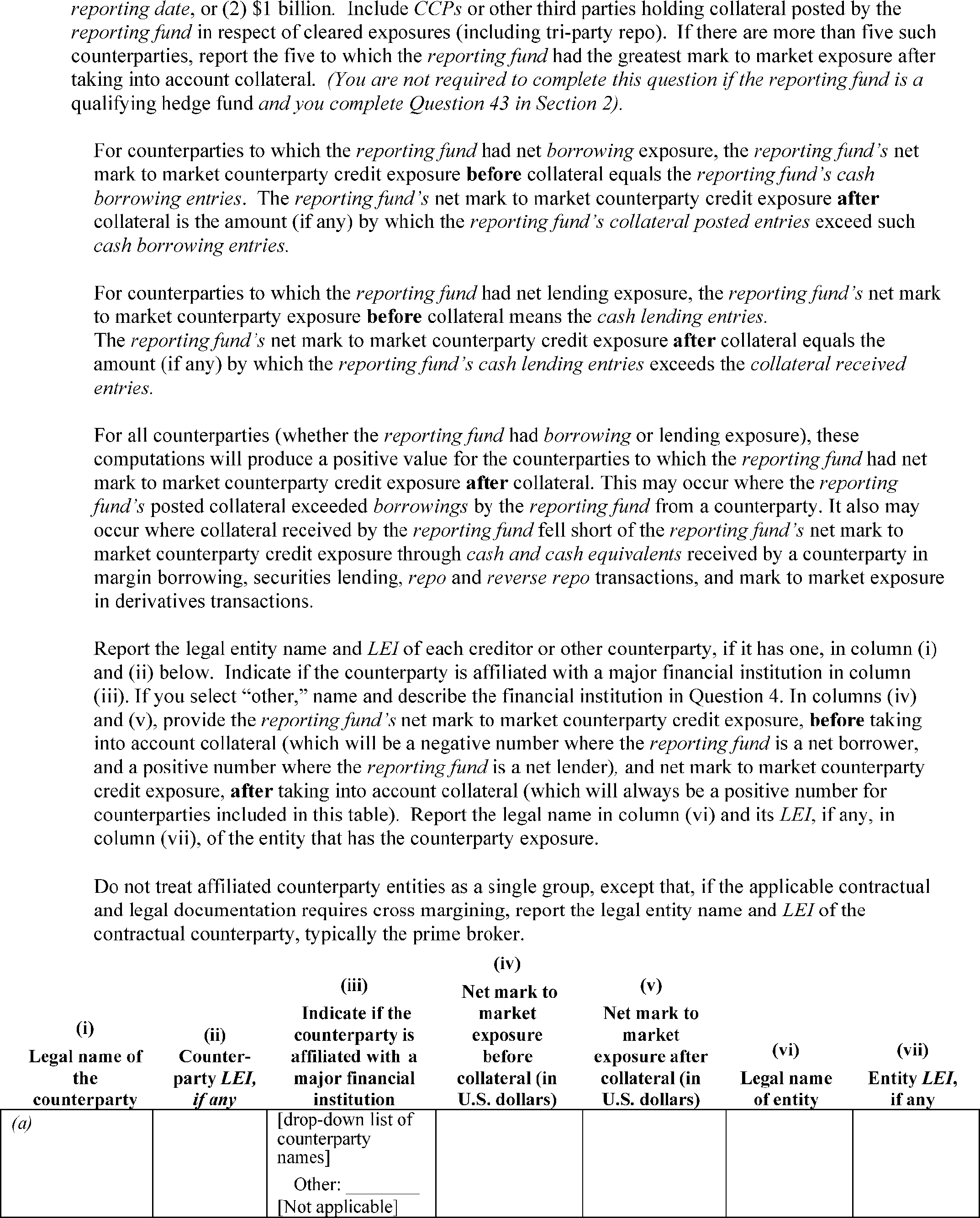

Simplify certain large hedge fund counterparty exposure reporting

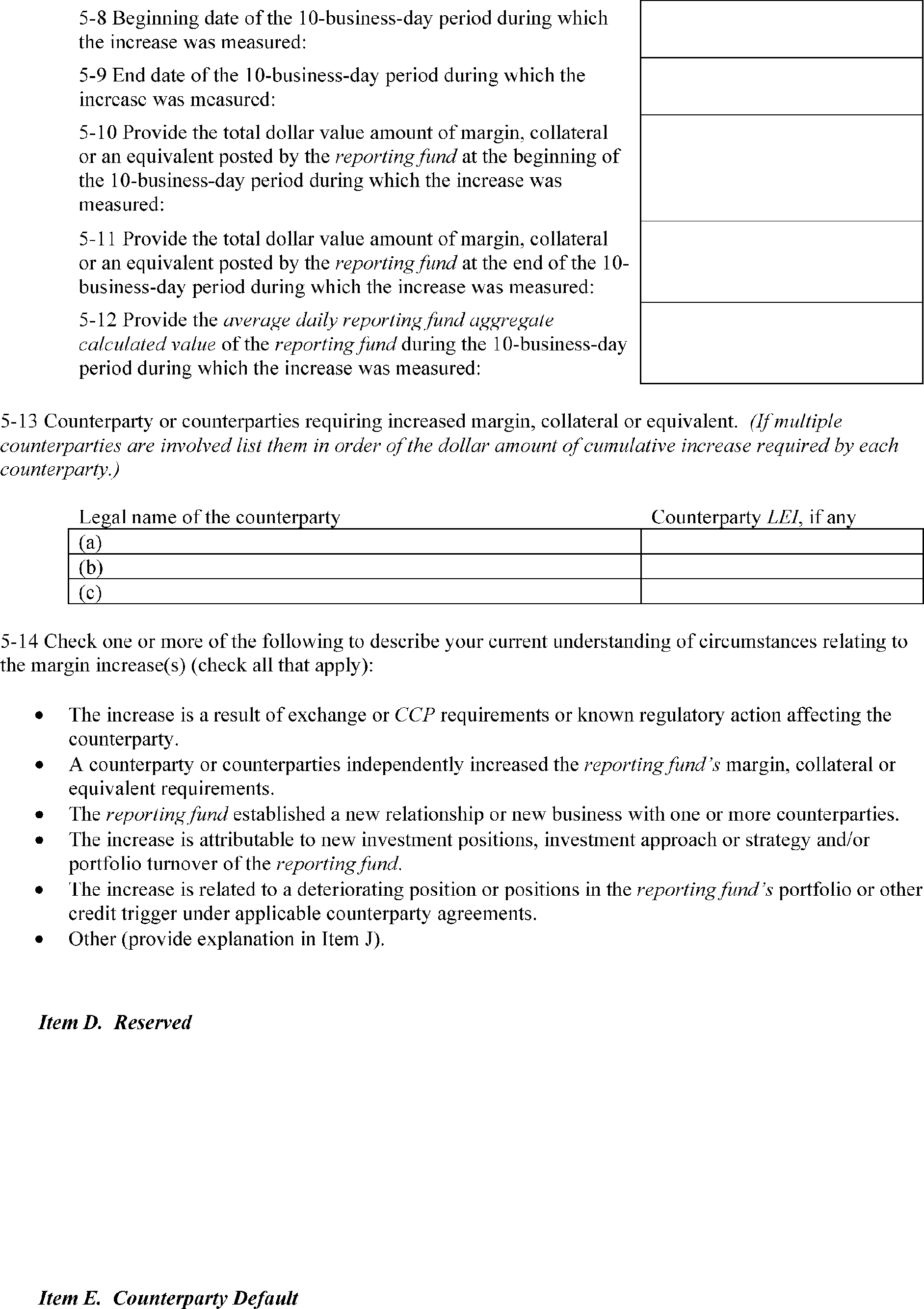

Currently, large hedge fund advisers must report in a consolidated counterparty exposure table their qualifying hedge funds' borrowing, collateral received, lending, and posted collateral, all aggregated across all counterparties as of the end of each month.

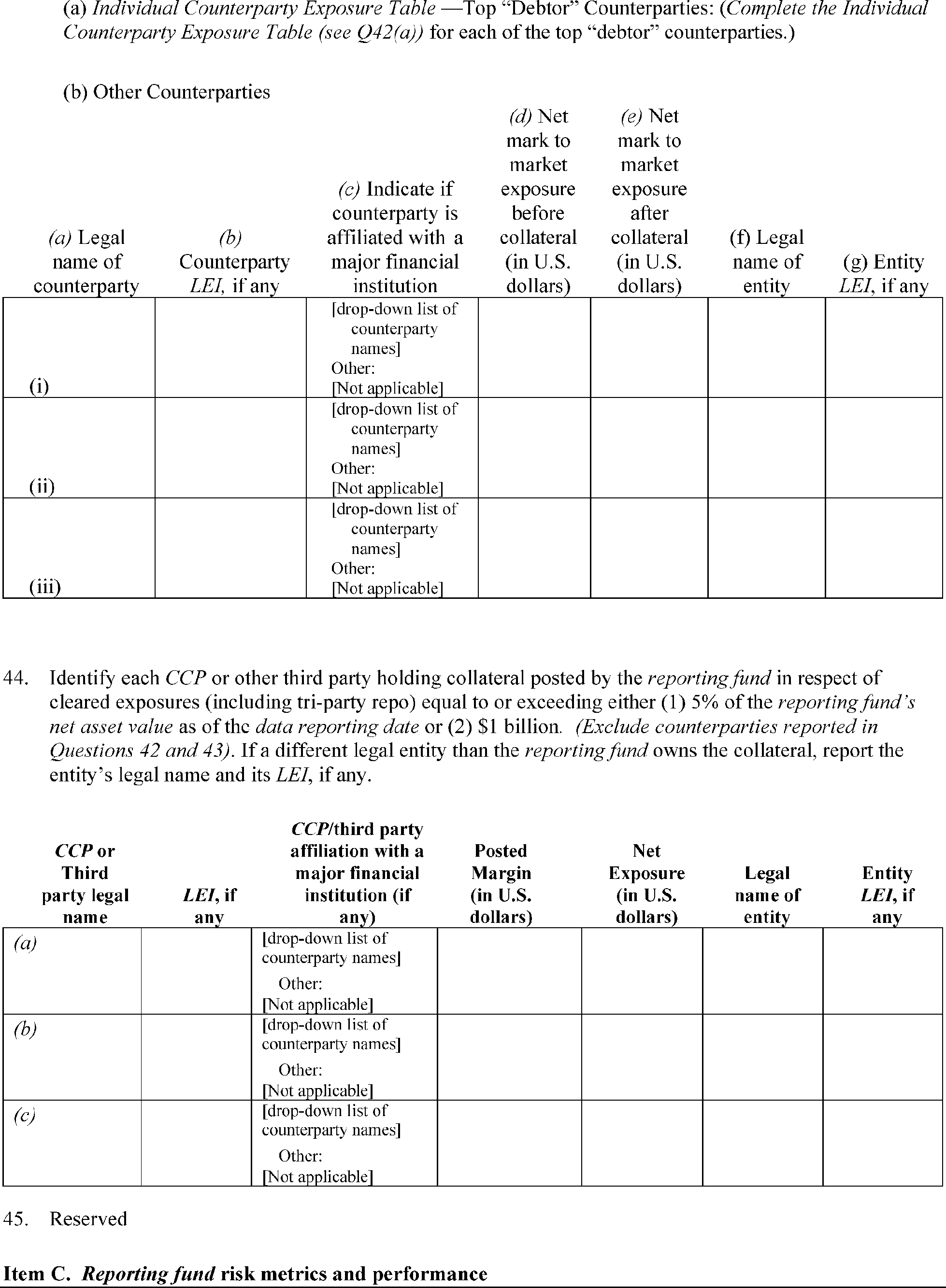

We propose to eliminate this table and direct large hedge fund advisers to: (1) complete the more simplified table in Question 26 for their qualifying hedge funds; and (2) report all borrowings to significant counterparties under Questions 42 and 43, and (3) categorize significant borrowing entries in Question 42. (Questions 41 and 42, and conforming amendments to Questions 18, 26, 43, and the Glossary of Terms.)

Eliminate rehypothecation reporting

Currently, large hedge fund advisers must report the total amount of collateral posted by counterparties to the qualifying hedge fund that may be and has been rehypothecated by the qualifying hedge fund.

We propose to eliminate these questions. (Question 45.)

Modify the current reporting trigger for all current reports

Currently, section 5 requires large hedge fund advisers to file a current report “as soon as practicable, but no later than 72 hours” upon the occurrence of certain events at their qualifying hedge fund.

The SEC proposes to modify the reporting trigger by removing the requirement to report as soon as practicable. Under the proposal, large hedge fund advisers would have the full 72 hours to file a current report. (Section 5.)

Eliminate current reporting for large hedge fund advisers concerning certain margin defaults

Currently, large hedge fund advisers are required to report within 72 hours if their qualifying hedge fund is in margin default or is unable to meet a call for margin, collateral, or equivalents.

The SEC proposes to eliminate this requirement. (Section 5, Item D.)

Eliminate current reporting for certain operations events

Currently, large hedge fund advisers are required to report within 72 hours if their qualifying hedge fund client experiences an operations event (

i.e.,

a significant disruption or degradation of the fund's “critical operations”). Form PF defines “critical operations” as operations necessary for (1) the investment, trading, valuation, reporting, and risk management of the reporting fund; or (2) the operation of the reporting fund in accordance with the Federal securities laws and regulations.

The SEC proposes to eliminate the second element. (Section 5, Item G, and the Glossary of Terms.)

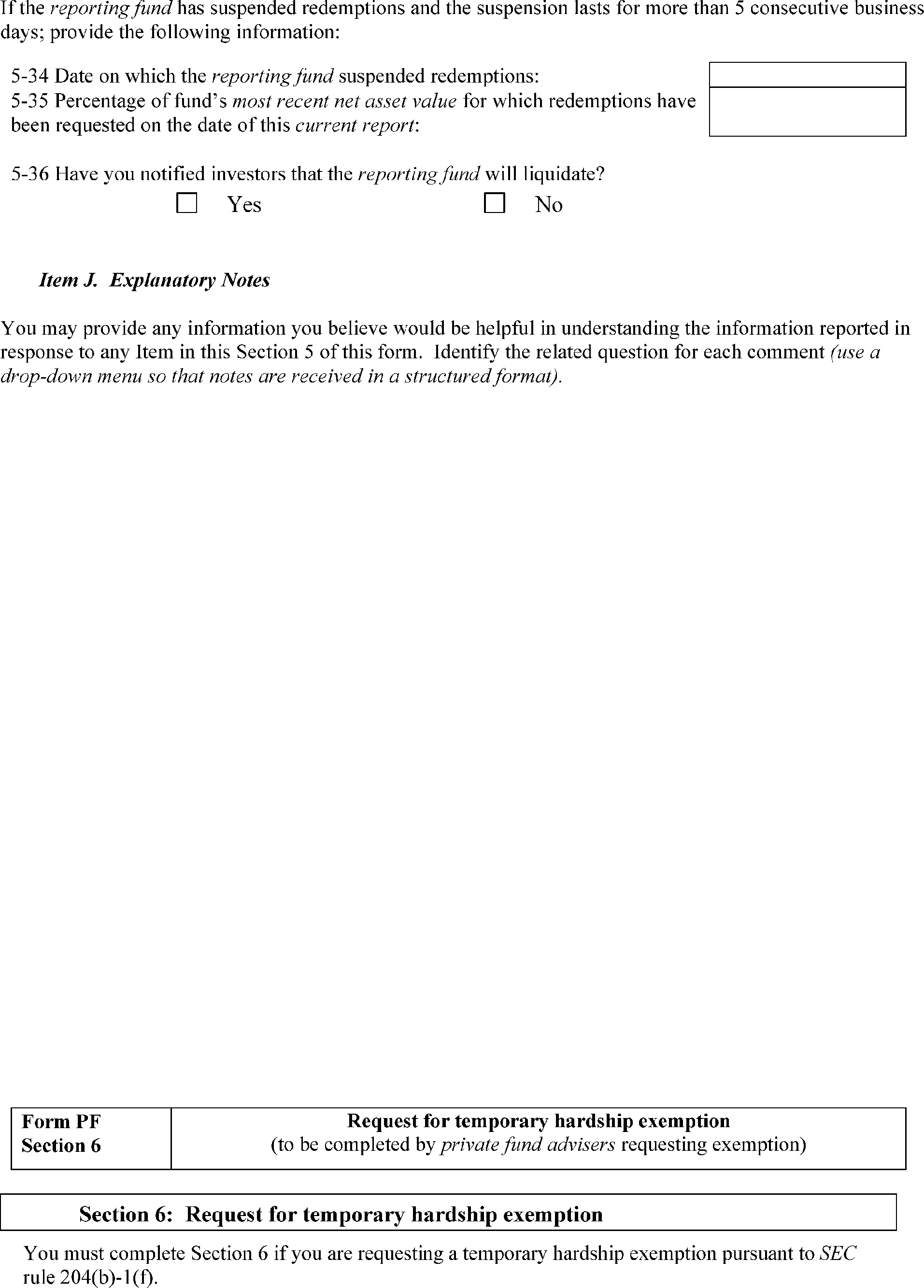

Eliminate current reporting related to the inability to satisfy redemption requests

Currently, large hedge fund advisers are required to report within 72 hours if their qualifying hedge fund (1) is unable to pay redemption requests or (2) has suspended redemptions and the suspension lasts for more than five consecutive business days.

The SEC proposes to eliminate the first element. (Section 5, Item I.)

Eliminate quarterly event reporting for all private equity fund advisers

Currently, all private equity fund advisers must submit quarterly reports about adviser-led secondary transactions, general partner removals, termination of investment periods, and fund terminations.

The SEC proposes to eliminate this requirement. (Section 6.)

Corrections and other revisions

We propose to make corrections and other revisions to help ensure filers clearly understand Form PF requirements.

Request for comments on private credit reporting

We are requesting comment on whether to modify the information that advisers must report about private credit funds.

The Commissions have consulted with FSOC to gain input on this proposal, and to help ensure that Form PF continues to provide FSOC with information it needs to carry out its monitoring obligations and its assessment of systemic risk while also not requiring the reporting of information that is not useful to FSOC in carrying out these responsibilities.

II. Discussion

A. Increase the Filing Threshold for All Form PF Filers

The Commissions propose to increase Form PF's filing threshold for all filers. Currently, SEC-registered advisers must

( printed page 22236)

file Form PF if they and their related persons, collectively, had at least $150 million in private fund assets under management as of the last day of their most recently completed fiscal year.[16]

We propose to increase this filing threshold from $150 million to $1 billion.[17]

When the Commissions adopted Form PF in 2011, the Commissions set a filing threshold of $150 million in private fund assets under management, which aligned with the private fund adviser registration exemption that the Dodd-Frank Act created.[18]

The Commissions stated that the filing threshold, based on an adviser's private fund assets under management, would adequately differentiate between advisers with only smaller funds and those with significant fund assets.[19]

Since then, Form PF has provided the Commissions with a greater ability to analyze and understand data on private fund advisers. With over a decade of experience reviewing Form PF data, we can more accurately determine an appropriate filing threshold for assessing systemic risk. Indeed, Form PF data show that the private fund industry has grown dramatically. For example, from 2013 to the first quarter of 2025, the aggregated private fund gross asset value that advisers reported on Form PF more than tripled, from $8 trillion to over $25 trillion.[20]

As Table 2 shows, we estimate that the proposed filing threshold would continue to allow Form PF to obtain information on approximately 94 percent of the most recent aggregate private fund gross asset value reported, while reducing the percentage of advisers that are required to file by almost half. Therefore, this proposed change is designed to better differentiate those advisers with significant private fund assets, consistent with the Commissions' original intent for the filing threshold.[21]

Table 2—Comparing the Current Filing Threshold to the Proposed Filing Threshold 1

Current

$150 million

threshold

(%)

Proposed

$1 billion

threshold

(%)

Impact 2

Percent of All SEC-Registered Advisers to Private Funds

70

40

43% fewer advisers would file.

Percent of All Private Funds Reported by SEC-Registered Advisers 3

83

68

18% fewer private funds' data would be reported.

Percent of Private Fund Gross Assets Reported by SEC-Registered Advisers 3

96

94

2% less gross asset value would be reported.

Notes:

1. Form PF data as of the first quarter of 2025 and Form ADV data as of December 2024.

3. Denominators for the Current Threshold Column and the Proposed Threshold Column calculations include private funds reported on Form PF and Form ADV by SEC-Registered Advisers.

In determining how to propose re-calibrating the filing threshold, the Commissions considered the alternatives outlined in Table 3 and the distribution of private fund assets across advisers with the goal of ensuring coverage of a significant percentage of private fund industry managed assets, while at the same time minimizing filing burdens on private fund advisers where their smaller size may both disproportionately increase the burdens of reporting and reduce their likelihood of having a meaningful effect on the assessment of systemic risk.[22]

As evidenced by Table 3, the percentage of private fund gross assets reported by SEC-registered advisers is concentrated with the largest private fund advisers (measured by assets) of the private fund industry as a whole, which would allow us to raise the reporting threshold while maintaining substantial reporting coverage of the private fund industry by assets. However, setting the threshold too high has the potential to narrow the field of reporting advisers to a degree that they skew or fail to represent the range of private fund strategies and activities that may materially inform systemic risk assessment and investor protection efforts. Therefore, as Table 3 highlights, the proposed filing threshold is designed to strike a balance between reducing the percentage of advisers that would be required to file, and the associated burdens, while helping ensure that Form PF would continue to collect information about a significant percentage of private fund gross assets appropriately to inform the assessment of systemic risk.

By increasing the Form PF filing threshold as proposed, the burdens of Form PF's section 1 collection of information would be more focused on advisers that manage private fund assets representing a significant percentage of the private fund industry and, thus, providing a diverse and representative view of private fund advisers for systemic risk assessment, while recognizing that Form PF can be burdensome for smaller advisers that the Commissions understand generally have fewer resources available to fulfil the reporting requirements of Form PF and who are less likely to have systemic risk impact.

As Table 3 indicates, by raising the filing threshold to $1 billion, we would be able to maintain insight into the potential systemic risk implications of private funds while eliminating filing burdens for many advisers.

( printed page 22237)

Table 3—Alternative Filing Thresholds 1

Filing threshold

Percent of all SEC-registered advisers to private funds

Percent of all private funds reported by SEC-registered

advisers 2

Percent of private fund gross assets reported by SEC-

registered advisers 2

Current $150 Million

70

83

96

Alternative $250 Million

64

83

96

Alternative $500 Million

53

76

95

Proposed $1 Billion

40

68

94

Alternative $2 Billion

30

60

91

Alternative $3 Billion

25

55

89

Alternative $4 Billion

22

51

87

Notes

1

Form PF Data as of the First Quarter of 2025 and Form ADV data as of December 2024.

2

Denominators for the calculations include private funds reported on Form PF and Form ADV by SEC-Registered Advisers.

SEC-registered advisers that would no longer meet the Form PF filing threshold, and as a result, would no longer be required to report on Form PF, would nonetheless continue to publicly report certain information about their private funds on 17 CFR 279.1 (Form ADV), as all SEC-registered advisers of such funds are required to do. Form ADV, which is publicly available, provides the SEC and investors with information about advisers (including private fund advisers) and the funds they manage, and is designed to provide the SEC with information necessary to its investor protection efforts. In contrast, Form PF is primarily designed to facilitate FSOC's assessment of systemic risk, although it is available to assist the Commissions in their regulatory programs for the protection of investors.[23]

Accordingly, the proposed changes would not eliminate all private fund data reporting for the affected advisers. Any SEC-registered adviser that would no longer be required to file Form PF would nonetheless continue to report information about its private funds on Form ADV.[24]

We request comment on the proposed change to the filing threshold:

1. Should the Commissions increase the filing threshold for all private fund advisers as proposed? If not, should the current filing threshold be kept constant, increased less than the proposed threshold, or increased more than the proposed threshold? Should the Commissions adopt any of the alternative thresholds presented in Table 3? For example, should the Commissions adopt a filing threshold of $250 million, $500 million, $2 billion, or $3 billion? If the threshold should be changed, what is the appropriate threshold and why?

2. Would the proposal to increase the filing threshold sufficiently alleviate burdens on private fund advisers? Please provide quantitative and qualitative data to support your conclusion.

3. Would the proposed filing threshold result in Form PF collecting information about the private fund industry necessary and appropriate in the public interest and for the protection of investors, or for the assessment of systemic risk?

4. Should the Commissions also adopt a filing threshold that adjusts for inflation? If the Commissions should adopt an inflation adjustment for the filing threshold, how should the Commissions measure the inflation adjustment? For example, should the Commissions measure the inflation adjustment from the time of the filing threshold's original adoption in 2011, or from the date the inflation adjustment would be adopted, or from another date? Is there a price index, such as the Personal Consumption Expenditures Chain-Type Price Index, the Consumer Price Index for All Urban Consumers, the Producer Price Index, or the GDP Price Deflator, that would be best suited for this adjustment? Would using a securities market index such as the S&P 500 or the NYSE Composite Index, which is not based on inflation, be a better way to adjust the filing threshold on an ongoing basis? At what cadence should the inflation be adjusted? For example, yearly, or every ten years, or any other cadence?

B. Increase the Reporting Threshold for Large Hedge Fund Advisers

The Commissions also propose to increase Form PF's reporting threshold for large hedge fund advisers. Currently, to qualify as a large hedge fund adviser, a Form PF filer and its related persons must have, collectively, at least $1.5 billion in hedge fund assets under management as of the last day of any month in the fiscal quarter immediately preceding their most recently completed fiscal quarter and manage a qualifying hedge fund.[25]

We propose to increase the large hedge fund reporting threshold from $1.5 billion to $10 billion.[26]

If an adviser qualifies as a large hedge fund adviser, it must file section 1 quarterly, instead of annually as it would if it were a hedge fund adviser that did not qualify as a large hedge fund adviser.[27]

Section 1a requires all advisers to report general identifying information about themselves and the private funds they advise, including a breakdown of regulatory assets under management and net assets under management. Section 1b requires all advisers to report information about each private fund they advise, including the following: (1) the private fund type; (2) assets, financing, and investor concentration; and (3) performance. Section 1c requires all advisers to report information about each hedge fund they advise, including the following: (1) investment strategies; (2) exposures; (3) counterparties; and (4) trading and clearing mechanisms.

If an adviser qualifies as a large hedge fund adviser, it also must file Form PF section 2 quarterly with respect to each qualifying hedge fund that it advises, including the following: (1) identifying information; (2) exposures and trading; (3) risk metrics and performance; (4) financing information; and (5) investor information.[28]

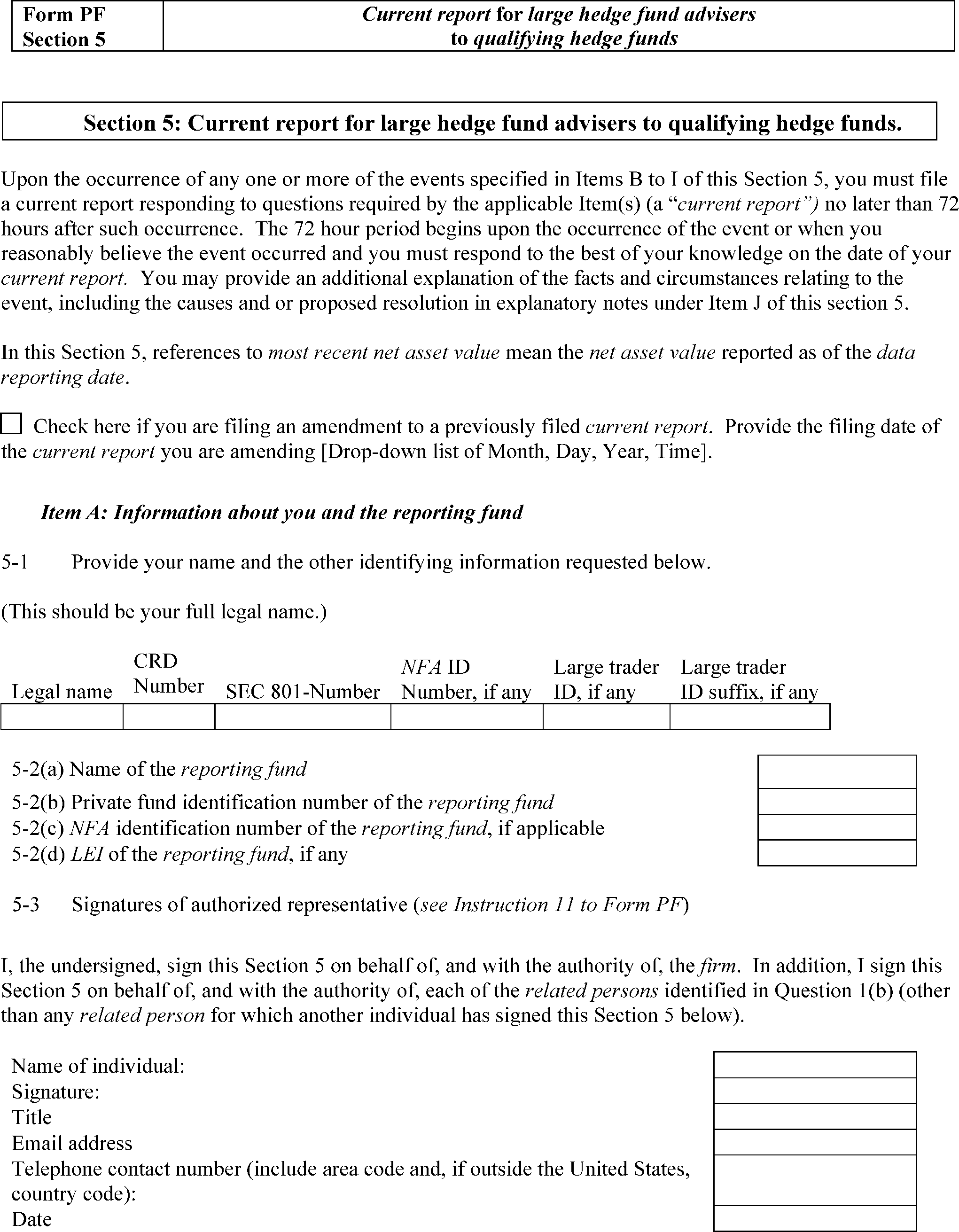

If an adviser qualifies as a large hedge fund adviser, it is also subject to Form PF Section 5 reporting, which requires a large hedge fund adviser to report information as soon as practicable, but no later than 72 hours upon the occurrence of certain events at qualifying hedge funds it advises,

( printed page 22238)

including the following: (1) extraordinary investment losses; (2) margin, collateral, or equivalent increases; (3) notice of margin default or determination of inability to meet a call for margin, collateral, or equivalents; (4) counterparty defaults; (5) prime broker relationships that have been terminated or materially restricted; (6) operations events; (7) withdrawals and redemptions; and (8) if the qualifying hedge fund is unable to satisfy redemptions or suspends redemptions.

Therefore, an adviser that would no longer qualify as a large hedge fund adviser under the proposed threshold would file section 1 annually, instead of quarterly, and would not file section 2 or be subject to section 5 current reporting, absent any other requirements.[29]

While the quarterly section 1, quarterly section 2, and section 5 current reporting are important for the largest hedge fund advisers that are more likely to be systemically important, they can impose disproportionate burdens on smaller advisers that are less likely to be systemically important.[30]

Any SEC-registered adviser would continue to report information about its private funds on Form ADV.[31]

When Form PF was originally adopted, the Commissions stated that the reporting thresholds were designed so that the group of large private fund advisers (including large hedge fund advisers) filing Form PF would be relatively small in number but would represent a substantial portion of the assets of their respective industries.[32]

At that time, the Commissions estimated that advisers each managing at least $1.5 billion in hedge fund assets represented over 80 percent of the U.S. hedge fund industry based on assets under management.[33]

As Table 4 shows, we estimate that the proposed higher threshold would still result in Form PF obtaining information quarterly on over 80 percent of hedge fund gross asset value that advisers report, while reducing the percentage of advisers that are required to file as large hedge fund advisers by almost two-thirds. Therefore, the proposed change is designed to continue to obtain information on a substantial portion of the assets of the hedge fund industry, consistent with the Commission's original intent for the large hedge fund reporting threshold, while reducing burdens on hedge fund advisers.

Table 4—Comparing the Current Large Hedge Fund Reporting Threshold to the Proposed Reporting Threshold 1

Current

$1.5 billion

threshold

(%)

Proposed

$10 billion

threshold

(%)

Impact 2

Percent of SEC-registered advisers reporting as large hedge fund advisers

26

9

65% fewer advisers would be required to report as large hedge fund advisers.

Percent of hedge funds reported by large hedge fund advisers related to those reported by all SEC-registered advisers 3

49

34

Data on 31% fewer hedge funds would be reported under the large hedge fund adviser requirements, and instead would be reported under other requirements, as applicable.

Percent of hedge fund gross assets reported by large hedge fund advisers related to those reported by all SEC-registered advisers 3

92

81

12% less of hedge fund gross asset value would be reported under the large hedge fund adviser requirements, and instead would be reported under other requirements, as applicable.

Notes:

1. Form PF data as of the first quarter of 2025 and Form ADV data as of December 2024.

3. Denominators for the Current Threshold Column and the Proposed Threshold Column calculations include hedge funds reported on Form PF and Form ADV by SEC-Registered Advisers.

We chose the proposed reporting threshold in light of the alternatives outlined below in Table 5, with the goal of helping ensure that Form PF would continue to collect information necessary and appropriate in the public interest and for the protection of investors, or for the assessment of systemic risk, while reducing burdens on hedge fund advisers.[34]

As in the past, the proposed amended reporting threshold is designed so that the group of large hedge fund advisers filing Form PF would be relatively small in number but represent a substantial portion of hedge fund assets.[35]

In determining where to propose re-calibrating the reporting threshold, the Commissions considered the alternatives outlined in Table 5 and the distribution of hedge fund assets with the goal of ensuring coverage of a substantial portion of hedge fund assets, while at the same time minimizing filing burdens on hedge fund advisers where their smaller size may both increase the burdens of reporting and reduce their likelihood of having a meaningful effect on the assessment of systemic risk.

As evidenced by Table 5, the percent of hedge fund gross assets reported by SEC-registered hedge fund advisers is concentrated at the largest hedge fund advisers, which would allow us to raise the reporting threshold while maintaining substantial reporting coverage of the hedge fund industry assets. However, setting the threshold too high has the potential to narrow the field of large hedge fund advisers to a degree that they skew or fail to represent the range of hedge fund strategies and activities that may materially inform systemic risk assessment. As a result, FSOC and the Commissions could miss emerging trends in the hedge fund industry. Furthermore, too few hedge fund advisers subject to quarterly reporting, instead of annual reporting, as well as enhanced Form PF reporting in sections 2 and 5, could result in

( printed page 22239)

FSOC and the Commissions being alerted in a less timely manner to certain events that may indicate significant stress at a hedge fund that could signal risk in the broader financial system. Therefore, as Table 5 highlights, the proposed reporting threshold is designed to strike the appropriate balance between reducing the percentage of hedge fund advisers that would be required to file as large hedge fund advisers, while helping ensure that Form PF would continue to collect information on a substantial portion of the assets of the hedge fund industry.

In addition, the SEC is proposing to require its staff to report to the SEC on each filing and reporting threshold in the form, assessing whether any should be adjusted, approximately five years after the compliance date for the amendments to the form and approximately every five years thereafter.[36]

These staff reports would help the SEC periodically evaluate the continued appropriateness of the filing and reporting thresholds in all respects, including whether proposing revisions to the thresholds would be appropriate. In producing this report, the staff would be directed to consider data collected by the SEC pursuant to Form PF, as well as any other applicable information as the staff may determine to be appropriate for its analysis. As the private fund adviser industry grows and changes, such a report and related review would be designed to ensure that the form continues to impose minimal filing burdens for small advisers, while continuing to collect data on a significant percentage of private fund assets.[37]

Table 5—Alternative Large Hedge Fund Reporting Thresholds 1

Reporting threshold

Percent of all

SEC-registered

advisers to

hedge funds

Percent of all

hedge funds

reported by

SEC-registered

advisers 2

Percent of

hedge fund

gross assets

reported

quarterly by

SEC-registered

advisers 2

Percent of hedge

fund gross

assets reported

as QHFs by

SEC-registered

advisers 23

Current $1.5 Billion

26

49

92

84

Alternative $2 Billion

22

47

91

83

Alternative $3 Billion

19

44

90

82

Alternative $5 Billion

14

41

86

79

Alternative $7.5 Billion

11

37

83

76

Proposed $10 Billion

9

34

81

74

Alternative $15 Billion

7

29

77

70

Alternative $20 Billion

6

27

74

68

Notes:

1. Form PF Data as of the First Quarter of 2025 and Form ADV data as of December 2024.

2. Denominators for the calculations include hedge funds reported on Form PF and Form ADV by SEC-Registered Advisers.

3. Reported by SEC-registered advisers for qualifying hedge funds (QHFs) on Form PF section 2.

We request comment on the proposed change to the large hedge fund reporting threshold:

5. Should the Commissions increase the large hedge fund adviser reporting threshold, as proposed? If not, should the current reporting threshold be kept constant, increased less than the proposed threshold, or increased more than the proposed threshold? Instead of the proposed reporting threshold, should the Commissions adopt one of the alternative thresholds listed in Table 5? For example, should the Commissions adopt a reporting threshold of $2 billion, $3 billion, $15 billion, or $20 billion? If the threshold should be changed, what is the appropriate threshold and why?

6. Would the proposal to increase the reporting threshold sufficiently alleviate burdens on hedge fund advisers? Please provide quantitative and qualitative data.

7. Would the proposed reporting threshold result in Form PF collecting information about the hedge fund industry necessary and appropriate in the public interest and for the protection of investors, or for the assessment of systemic risk?

8. The SEC is proposing to require its staff to report to the SEC on each filing and reporting threshold in the form, assessing whether any should be adjusted, approximately five years after the compliance date for the amendments to the form and approximately every five years thereafter. Alternatively, should the Commissions adopt a large hedge fund adviser reporting threshold that adjusts for inflation? If so, should the Commissions adopt the same inflation adjustment for all or just certain reporting thresholds in Form PF, or only for the large hedge fund adviser threshold? If the Commissions should adopt an inflation adjustment for any reporting threshold on Form PF, how should the Commissions measure the inflation adjustment? For example, should the Commissions measure the inflation adjustment from the time of the reporting threshold's original adoption in 2011, or from the date the inflation adjustment would be adopted, or from another date? Is there a price index, such as the Personal Consumption Expenditures Chain-Type Price Index, the Consumer Price Index for All Urban Consumers, the Producer Price Index, or the GDP Price Deflator, that would be best suited for this adjustment? Would using a securities market index such as the S&P 500 or the NYSE Composite Index, which is not based on inflation, be a better way to adjust the reporting threshold on an ongoing basis? At what cadence should the inflation be adjusted? For example, yearly, or every ten years, or any other cadence?

9. Should the Commissions increase the qualifying hedge fund threshold? Why or why not? What is the appropriate qualifying hedge fund threshold (

e.g.,

a net asset value of $750 million or $1 billion)? The qualifying hedge fund threshold is based on net asset value, while the large hedge fund adviser threshold is based on gross asset

( printed page 22240)

value. Under the proposed amendments this construction would have two results: (1) it identifies and requires more detailed and frequent reporting for hedge fund advisers that manage several large hedge funds and (2) it identifies and requires more detailed and frequent reporting for hedge fund advisers that manage hedge funds with significant use of leverage. Is there an alternative approach to ensure hedge funds using significant leverage are reporting in the more detailed section 2 on a quarterly basis? If we increased the qualifying hedge fund threshold, should we change the threshold to measure on a gross asset value basis so that it does not disproportionately eliminate more frequent and detailed reporting from more leveraged hedge funds?

10. Should the Commissions increase the large liquidity fund adviser threshold? Why or why not? If so, what is the appropriate threshold for large liquidity fund advisers (

e.g.,

$2 billion, $3 billion, $5 billion)?

11. Should the Commissions increase the large private equity fund adviser threshold? Why or why not? If so, what is the appropriate threshold for large private equity fund advisers (

e.g.,

$3 billion, $5 billion)?

C. Disregarded Feeder Funds

The Commissions propose to allow advisers not to separately report feeder funds with minimal holdings outside of a feeder fund's interest in a master fund. Specifically, the Commissions propose to revise General Instruction 6 to permit advisers to treat a feeder fund as “disregarded” if it invests not more than five percent of its gross asset value in investments that are not in a single master fund, U.S. treasury bills, and/or cash and cash equivalents.[38]

This proposed change is designed to reduce filing burdens on advisers and better balance against the need for the Commissions and FSOC to understand the reporting fund's structure and the risk exposure of its component funds.[39]

Prior to the 2024 amendments, Form PF provided advisers with flexibility to respond to questions regarding master-feeder arrangements and parallel fund structures, either in the aggregate or separately, as long as they did so consistently throughout Form PF. This resulted in some advisers reporting in aggregate and some advisers reporting separately, and consequently, obscured risk profiles (

e.g.,

with respect to leverage, counterparty exposure, investor liquidity) and created difficulties when comparing complex structures.[40]

In 2024, the Commissions adopted amendments to Form PF that generally require separate reporting for every component fund of a master-feeder arrangement and parallel fund structure.[41]

By prescribing the way advisers report master-feeder arrangements and parallel fund structures, the 2024 amendments were intended to provide the Commissions and FSOC with better insight into the risks and exposures of these arrangements. The 2024 amendments, however, required disregarded feeder funds to be aggregated in the reporting about master-feeder arrangements and parallel fund structures. Defined in General Instruction 6 as a feeder fund that invests all of its assets in a single master fund, U.S. treasury bills,[42]

and/or cash and cash equivalents, a “disregarded feeder fund” effectively invests only through its associated master fund, and the Commissions stated that separate reporting of these funds is not necessary for data analysis purposes because it would not convey additional information about their exposures.[43]

Since the adoption of the 2024 amendments, industry members have highlighted the significance of the burdens associated with disaggregating feeder funds in their reporting.[44]

In communications with the SEC staff, several filers have stated that many private funds utilize complex master-feeder arrangements, and that separate reporting of feeder funds without additional exceptions would cause substantial burdens because it requires the collection of many more data points about many more fund entities in these private fund structures.[45]

Some filers said feeders that hold minimal holdings outside of the master fund should be disregarded, as the

de minimis

amount of these outside assets do not alter the risk picture of the feeder. These filers stated that disaggregated reporting does not reflect how advisers typically manage risk and liquidity for these funds, and that reporting instructions should align with advisers' typical risk management practices in order to result in meaningful and accurate data.[46]

In response to these concerns, we are proposing to change General Instruction 6 to allow advisers to aggregate in their reporting about master-feeder arrangements feeder funds that hold a

de minimis

amount of investments outside of the master fund.[47]

Under the proposed change to General Instruction 6, advisers would be able to treat a feeder fund that invests not more than five percent of its gross asset value [48]

in other investments that are not in a single master fund, U.S. treasury bills, and/or cash and cash equivalents, as a disregarded feeder fund. Accordingly, advisers would be permitted to aggregate such feeder funds in their reporting about master-feeder arrangements on Form PF. In our view, five percent is an appropriate threshold because it parallels the threshold used in other parts of Form PF to represent a fund's material exposure and a level of exposure that could be significant enough to present broader systemic risk and contagion risk.[49]

The proposed change seeks to better align the Form PF reporting requirements with the way advisers typically track and manage the risk profile of feeder funds while preserving the Commissions and FSOC's ability to obtain a clear understanding of fund structures and the risk exposure of their component funds.[50]

We request comment on the proposed change to General Instruction 6:

( printed page 22241)

12. Would the proposed change to General Instructions 6 sufficiently alleviate burdens on private fund advisers?

13. Would the proposed change to General Instruction 6 result in the collection of information about private fund structures and the risk exposure of their component funds necessary and appropriate in the public interest and for the protection of investors, or for the assessment of systemic risk?

14. Would the proposed change to General Instruction 6 result in certain feeder funds that are necessary to assess systemic risk not being identified in the form? If so, how?

15. Is five percent the appropriate threshold for disregarding feeder funds with minimal holdings outside of the master fund? Why or why not? What other percentages (

e.g.,

three percent, ten percent) or methods should the Commissions consider for purposes of identifying disregarded feeder funds that are not necessary and appropriate for the assessment of systemic risk? For example, should we allow filers to treat any feeder fund as disregarded if the filer does not separately consider the feeder fund and its exposures for its risk management purposes? Should we allow, as was the case prior to the 2024 amendments, filers to choose whether to respond to questions in the aggregate or separately, as long as they did so consistently through Form PF? Why or why not?

16. Is “gross asset value,” as defined in the Form PF Glossary of Terms, the appropriate denominator for disregarding feeder funds with minimal holdings outside of the master fund? Why or why not? What alternatives should the Commissions consider as the denominator for purposes of disregarding feeder funds that are not necessary and appropriate for the assessment of systemic risk?

17. Are there types of investments or features of feeder funds that should be considered in permitting aggregation?

18. Is the proposed change to the definition of disregarded feeder fund in General Instruction 6 sufficiently clear? Would this raise any questions about how to determine which feeder funds should be disregarded for purposes of General Instruction 6? Should we provide any additional clarification regarding which feeder funds should be disregarded for purposes of General Instruction 6?

D. Eliminate the Look Through Requirement

The Commissions propose changes to Form PF that would allow advisers to report indirect exposures based on reasonable estimates that are consistent with their internal methodologies and the conventions of service providers when responding to certain questions that currently require looking through the reporting fund's investments. Specifically, the Commissions propose to eliminate from General Instructions 7 and 8 the prescriptive requirement that advisers “look through” the reporting fund's investments when reporting indirect exposures and to instead allow advisers to rely on reasonable estimates consistent with their internal methodologies and conventions of service providers when reporting indirect exposures.[51]

The Commissions also propose conforming amendments to the instructions for Questions 32, 33, 35, 36, and 47, and to amend the definitions of certain asset classes in the Glossary of Terms, to allow advisers to report indirect exposures consistent with the amended General Instructions 7 and 8. These changes are intended to reduce and better balance the filing burdens on advisers against the need to obtain clear and comparable data across advisers.

In 2024, the Commissions adopted amendments to General Instructions 7 and 8 to provide that, when responding to questions, advisers generally must not “look through” a reporting fund's investments in other funds or entities (other than a trading vehicle), unless the question instructs the adviser to report exposure obtained indirectly through the reporting fund's positions in such other funds or entities. In reporting indirect exposures of the reporting fund in response to certain questions (Questions 32, 33, 35, 36 and 47), General Instruction 7 requires advisers to “look through” the reporting fund's investments in internal private funds and external private funds. Likewise, General Instruction 8 requires advisers to “look through” the reporting fund's investments in other funds or entities when reporting indirect exposures in response to those same questions.

Prior to the 2024 amendments, Form PF generally did not address how to report indirect exposures resulting from positions held through other entities, and advisers were not required to (although they had the option to) look through a reporting fund's investments in another entity, unless the form specifically requested information regarding that entity.[52]

As a result, some advisers were reporting indirect exposures, while others were not, leading to incomplete and unclear data, inconsistent comparisons, and less precise analysis across advisers. The 2024 amendments changed General Instructions 7 and 8 to direct advisers to report indirect exposures in response to certain questions by mandatorily looking through the reporting fund's investments in private funds and other entities. These changes were designed to promote FSOC's effective systemic risk assessments and the Commissions' investor protection efforts by reducing issues of data quality and incomparability with respect to data regarding indirect exposures of private funds.

After the adoption of the 2024 amendments, however, industry members reported that the rigid and granular reporting required via this mandatory look-through would create significant burdens and in many cases would be operationally difficult.[53]

For example, several filers noted that looking through a reporting fund's investment in an exchange-traded fund (an “ETF”) to calculate the reporting fund's indirect exposure to each underlying investment in the ETF could be particularly burdensome in instances where the ETF tracks and continuously rebalances a broad index comprising potentially hundreds of underlying investments. Other filers stated that the methodology for determining the exact composition of an index may be proprietary and not controlled by the adviser.

We also heard concerns that looking through the reporting fund's investments in other entities, such as investments in another private fund that in turn invests in portfolio companies, private credit instruments, or securitized assets, could be operationally challenging, if the adviser does not control those entities and therefore has limited access to information regarding the underlying investments, or the data that the adviser does obtain does not align with the timing and reporting requirements of Form PF.

In consideration of these concerns, we are now proposing changes to General Instructions 7 and 8 to eliminate the prescriptive requirement that advisers “look through” the reporting fund's investments when reporting indirect exposures and to instead allow advisers to report required indirect exposures based on reasonable estimates that are consistent with the adviser's internal

( printed page 22242)

methodologies and conventions of service providers. We are also proposing amendments to Questions 32, 33, 35, 36 and 47 to remove instructions that reasonable estimates used to report indirect exposures, and that indirectly held entity positions in a sub-asset class and instrument type, must “best represent” the exposure of the entity [54]

or the sub-asset class exposure of the indirectly held entity.[55]

The prescriptive look-through requirement in General Instructions 7 and 8 as well as the “best represent” standard in the specific questions' instructions for reporting indirect exposures would create burdens for advisers to conduct look-through for assessing indirect exposures even though they may reasonably and more efficiently estimate such indirect exposures in their own portfolio and risk management processes. The proposed changes are intended to provide advisers the ability to rely on reasonable estimates to report indirect exposures, provided they are consistent with their internal methodologies and the conventions of service providers.[56]

For example, with respect to a reporting fund's investment in a gold ETF, the proposed changes would allow advisers to estimate the reporting fund's exposure through an ETF more broadly (

e.g.,

“gold commodities” sub-asset class) to the extent consistent with their own portfolio and risk management processes.

Relatedly, the Commissions propose conforming amendments to align other parts of the form with the proposed General Instructions 7 and 8. The proposed changes would include conforming amendments to Question 32 and Question 47 to remove certain references to indirectly held “positions.” [57]

The Commissions also propose to revise definitions of certain asset classes in the Form PF's Glossary of Terms to explicitly subject those definitions to proposed General Instructions 7 and 8.[58]

As part of the 2024 amendments, Form PF defined these asset classes also requiring the reporting fund to look through to indirect exposures to such assets held through another entity. The proposed definitional changes are intended to allow advisers, consistent with General Instructions 7 and 8, to use their reasonable estimates that are consistent with the adviser's internal methodologies and conventions of service providers for such indirect exposures. These proposed changes would also help to resolve any inconsistencies between the instructions in the definitions of these terms and General Instructions 7 and 8.

Furthermore, the Commissions propose to make a conforming change to the definition of “reference asset” in the Form PF Glossary of Terms by removing the phrase “and do not conflict with any instructions or guidance relating to this Form,” which would be unnecessary with the proposed changes to General Instructions 7 and 8 that would allow for the use of reasonable estimates consistent with internal methodologies to report indirect exposures.[59]

Although the proposed changes to General Instructions 7 and 8 (and related conforming changes) would lead to more filers using their internal practices to report indirect exposures and to do so less precisely, thus potentially reducing the level of specificity and comparability of indirect exposures through fund or entity holdings reported by advisers on Form PF,[60]

we anticipate that these changes would not undermine FSOC's systemic risk assessment and the Commission's investor protection efforts. Based on input received from filers, we understand that the operational challenges posed by the strict look-through requirement, such as lack of the advisers' control of or access to granular position data of underlying fund or entity investments from third party entities or third party data that comports with the reporting requirements of Form PF, would likely, in practice, result in advisers having to rely on internal assumptions to comply with Form PF's requirements. As such, the prescriptive look-through requirements in General Instructions 7 and 8 would likely not achieve the intended outcome, making any greater granularity and comparability unjustified in light of the apparent significant filing burdens on advisers.[61]

Our proposal, however, would retain questions mandating the reporting of indirect exposures and thus preserve the objective of the 2024 amendments to address issues of data quality and comparability that had resulted from some advisers providing indirect exposures while others did not.

Moreover, the proposed changes would preserve FSOC's ability to assess systemic risk and the Commissions' ability to protect investors by collecting data based on advisers' portfolio risk management processes, which themselves are designed to capture material risk exposures from investments.

We request comment on the proposed changes to General Instructions 7 and 8, the definitions of certain asset classes in the Form PF Glossary of Terms, and other conforming changes:

19. Would the proposed changes to General Instructions 7 and 8, the definitions of asset classes including “reference asset,” and other conforming changes sufficiently alleviate burdens on private fund advisers?

20. Would the proposed changes to General Instructions 7 and 8 and the definitions of asset classes including “reference asset” result in the collection of information about the reporting fund's indirect exposure necessary and appropriate for investor protection and the assessment of systemic risk?

21. Should the “look through” requirement for certain, or all, questions be eliminated entirely, as proposed, and allow advisers to instead rely on reasonable estimates that are consistent with their internal methodologies and conventions of service providers? If not, why not?

22. Are certain questions easy to “look through” funds, entities and investments than others? If so, which ones and why?

23. Are there certain types of funds or entities that are easy to “look through”? If so, which ones and why?

24. Are there certain types of reference assets that are easy to report on a “look through” basis? If so, which ones and why?

25. Should the form require a “look through” for certain, or all, types of funds, entities or reference assets? If so, which ones and why?

( printed page 22243)

E. Trading Vehicles

The Commissions propose to amend Question 9 under section 1b of the Form PF to reduce the scope of trading vehicles that advisers must specifically identify. The proposed new scope focuses solely on trading vehicles that face counterparties and creditors or are reported on Form ADV as a private fund. This proposed change is intended to reduce the burdens on advisers with respect to identifying trading vehicles while still supporting the need for the Commissions and FSOC to understand the reporting fund's use of trading vehicles relevant to identifying systemic risk and investor protection efforts.[62]

Before the 2024 amendments, Form PF did not require advisers to identify trading vehicles, even though private funds often use trading vehicles to trade, incur leverage, and bear counterparty and credit exposures as part of their investment strategy.[63]

In 2024, the Commissions adopted amendments to section 1b to obtain a clear view of the reporting fund's use of trading vehicles in this manner and therefore to enhance FSOC's ability to monitor systemic risk and the Commissions' ability to protect investors by better assessing the scope of the reporting fund's position sizes and counterparty exposures that are attributable to the trading vehicle and identifying areas in need of outreach, examination or investigation. The broad definition of “trading vehicle” in the final form was intended to ensure that such trading vehicles were captured,[64]

and Question 9 was designed to obtain identifying information about any trading vehicle used by the reporting fund that met this definition.[65]

Since the adoption of the 2024 amendments, filers have highlighted the broad scope of trading vehicles that would need to be identified on the form and the significance of the burden on advisers of having to meet this requirement.[66]

Private funds may use trading vehicles for a wide variety of purposes other than trading and bearing counterparty exposure. Consequently, the broad definition of “trading vehicle,” which includes an entity that “holds assets” and conducts “other activities” as part of the reporting fund's investment activities, potentially captures passive entities (

e.g.,

tax blockers, liability blockers, aggregator vehicles used to consolidate investments from investors in private funds, passive holding companies formed to hold portfolio investments) that are commonly used by private funds for structuring, tax and/or other operational efficiencies. Many of these passive entities, however, may not otherwise actively trade nor engage in other activities directly related to the fund's counterparty or credit exposures in a manner that creates interconnectedness of the trading vehicle to the broader financial services industry, a critical part of systemic risk assessment and investor protection efforts. Some filers have expressed concern that under the current “trading vehicle” definition, they would have to report hundreds of entities in certain private fund structures, imposing significant burdens on those advisers.[67]

After considering the scope of trading vehicles that must be reported under Question 9 in light of systemic risk assessment and investor protection efforts, as well as the significance of the burdens on advisers raised by the current instructions, we propose to reduce the scope of trading vehicles that must be reported under Question 9 to focus on trading vehicles that face counterparties and creditors or are reported on Form ADV as a private fund.

Specifically, the proposed changes to Question 9 would limit trading vehicles that must be identified by name and legal entity identifier (“LEI”), if any, to those that are (i) listed or required to be listed on Section 7.B. of Schedule D of the adviser's or another adviser's Form ADV,[68]

or (ii) included or required to be included in a response to Questions 27, 28, 42, 43, or 44 of the Form PF,[69]

which require advisers to identify the relevant party (including any trading vehicles) that bears counterparty and credit exposures.[70]

The proposed changes would entail a conforming amendment to General Instruction 7 with the same instruction limiting the scope of trading vehicles that must be identified in response to Question 9 to those that are listed on the adviser's Form ADV or in response to Questions 27, 28, 42, 43 or 44. As discussed above, the broad definition of “trading vehicle” may cover passive entities commonly used in private fund structures but do not directly interact with the market in a manner that may pose systemic risk such as by trading, taking on leverage, or bearing counterparty and credit exposures. Furthermore, as emphasized by some filers, the burden on advisers of having to identify each passive entity in the reporting fund's structure that meets the broad definition of “trading vehicle” may be significant.

Although the current instructions would have provided a more comprehensive visibility into the wide variety of ways trading vehicles are incorporated into private fund structures, they would have primarily captured passive trading vehicles, and reducing the scope of trading vehicles would not materially affect the Commissions' and FSOC's systemic risk oversight and investor protection efforts. The proposed changes to Question 9 would reduce the scope of trading vehicles that advisers must identify to those that are more directly relevant and meaningful to the Commissions' and FSOC's oversight and investor protection efforts. Section 7.B. of Schedule D of Form ADV requests important information about the private funds managed by advisers but does not specify whether the private funds

( printed page 22244)

reported therein are trading vehicles. The proposed changes would therefore facilitate our staff's ability to identify trading vehicles reported on Form ADV and the scope of trading vehicles' potential effects on systemic risk and investor protection.

Furthermore, the revised Question 9 would require advisers to identify those trading vehicles that they have included in response to questions on the form that address how the reporting fund uses trading vehicles to bear counterparty and credit exposures (Questions 27, 28, 42, 43, or 44). Hence, any trading vehicle that incurs leverage or conducts trading or other activities as part of a hedge fund's investment activities resulting in significant exposure to creditors or counterparties is currently identified by advisers in those questions and would therefore continue to be included in Question 9 under the proposed change.

Trading vehicles included in response to these questions (which may overlap with those reported on Form ADV) would provide the Commissions and FSOC with transparency into the reporting fund's risk profile and interconnectedness of private funds with the broader financial services industry. Moreover, although we propose to limit the scope of trading vehicles that must be specifically identified, General Instructions 7 and 8 would continue to require advisers to look through certain trading vehicles and to their specific holdings, which would capture their counterparty and creditor exposures.[71]

These proposed changes would therefore not have a significant effect on the Commissions' and FSOC's ability to assess relevant information for purposes of their risk assessment and investor protection efforts, as the form would continue to obtain relevant information about operationally active trading vehicles that do engage in activities that could impact the broader financial services industry.[72]

We request comment on the proposed changes to Question 9 of Section 1b:

26. Would the proposed changes to Question 9 sufficiently alleviate burdens on private fund advisers?

27. Do you agree that the current definition of “trading vehicle” covers entities that do not directly interact with the market in a manner that may pose systemic risk such as by trading, taking on leverage, or bearing counterparty and credit exposures? Would the proposed changes to Question 9 result in the collection of information about trading vehicles necessary and appropriate in the public interest and for the protection of investors, or for the assessment of systemic risk?

28. Would the proposed changes to Question 9 result in certain trading vehicles that are necessary to assess systemic risk not being identified in the form? Should such trading vehicles continue to be identified in the form? If so, which ones?

29. Should we instead amend Form PF so that private fund advisers are not required to identify any trading vehicles? Is the identification of trading vehicles relevant to the assessment of systemic risk? Why or why not?

F. Eliminate Form PF Question 23(c) Volatility Reporting

The Commissions propose to eliminate Question 23(c) in its entirety for all private fund filers.[73]

Question 23(c) requires private funds to report additional performance-related information if the adviser calculates a market value on a daily basis for any position in the reporting fund's portfolio. Such information includes: (1) the “reporting fund aggregate calculated value” at the end of the reporting period; (2) the reporting fund's volatility of the natural log of the “daily rate-of-return” for each month of the reporting period; (3) whether the daily return rates are reported to current or prospective investors; and (4) whether the reporting fund had one or more days with a negative daily rate of return during the reporting period and related information.

We added Question 23(c) in the 2024 amendments to allow the Commissions and FSOC to compare return volatility more accurately across different private fund types to identify market trends, for systemic risk assessment, and for investor protection efforts.[74]

This measure quantifies the degree to which a portfolio's logarithmic returns fluctuate around their average, with higher values indicating greater risk of large gains or losses and uncertainty in an investment's value.

However, during implementation of this new question, it is our understanding that numerous advisers encountered challenges and significant costs in preparing to respond to this question. Some advisers calculate this information in the ordinary course of their business for certain funds but not all private funds, or only at the level of the master fund. Other advisers use an internal methodology that does not necessarily align with what we ask under Question 23(c), so they have had to design complicated and bespoke calculations based on approximations of the same data points. Industry members have further pointed out that there are many investing strategies involving less liquid or illiquid assets that have less volatility and could mute or otherwise skew volatility data, so capturing intra-month volatility about them is less valuable but more burdensome, even if they can be reported.

We now propose to delete Question 23(c). Based on our review, the data captured by other questions in the form can assist in contextualizing performance-related volatility, such as the monthly performance reporting in Question 23(a) and (b) or extraordinary losses reported in current reports.[75]

Although deleting Question 23(c) would result in less detailed performance-related volatility information, such that the Commissions and FSOC may lose insight into significant performance volatility swings occurring on an intra-month basis, intra-month performance-related data for less liquid or illiquid investment strategies can have limited utility when evaluating performance volatility.[76]

Further, we understand that funds are making assumptions in calculating this information, which undermines its comparability.

Given the burdens associated with calculating this information, and that information related to performance-related volatility can be gathered from other existing parts of the form, we propose to eliminate Question 23(c) from Form PF.

We request comment on the proposed removal of Question 23(c):

30. Should the Commissions eliminate Question 23(c)? Why or why not?