Staff Report on the Definitions of “Security-Based Swap Dealer” and “Major Security-Based Swap Participant”

The Securities and Exchange Commission directed staff to prepare and is now publishing a report examining the effect and application of the definitions of "security-based swap d...

The Securities and Exchange Commission directed staff to prepare and is now publishing a report examining the effect and application of the definitions of “security-based swap dealer” and “major security-based swap participant.” Those definitions include an exception from designation as a security-based swap dealer for an entity that engages in a de minimis quantity of security-based swap dealing, as well as separate thresholds below which an entity would not become a major security-based swap participant. As provided in the Commission's rules, nine months after publication of this report and after considering any public comments received, the Commission may by order either terminate the phase-in period for the de minimis thresholds, thereby allowing thresholds of $3 billion for credit default swaps that constitute security-based swaps and $150 million for non-credit default swaps that constitute security-based swaps to take effect and replace the current phase-in thresholds of $8 billion and $400 million, respectively, or propose different thresholds through rulemaking; however, the Commission has issued an order providing a temporary exemption that has the effect of continuing to apply the phase-in thresholds of $8 billion and $400 million until May 8, 2028. The public is invited to comment on all aspects of this report, which may inform the Commission's consideration of potential changes to the de minimis exception and the rules further defining the terms “security-based swap dealer” and “major security-based swap participant.”

DATES:

Comments should be submitted on or before July 6, 2026.

ADDRESSES:

Comments may be submitted by any of the following methods:

Send an email torule-comments@sec.gov.

Please include file number S7-2026-14 on the subject line.

Paper Comments

Send paper comments in triplicate to Secretary, Securities and Exchange Commission, 100 F Street NE, Washington, DC 20549-1090.

All submissions should refer to File Number S7-2026-14. This file number should be included on the subject line if email is used. To help the Commission process and review your comments more efficiently, please use only one method of submission. The Commission will post all comments on the Commission's website (

https://www.sec.gov/comments/s7-2026-14/staff-report-definitions-security-based-swap-dealer-major-security-based-swap-participant). Do not include personal identifiable information in submissions; you should submit only information that you wish to make available publicly. We may redact in part or withhold entirely from publication submitted material that is obscene or subject to copyright protection.

FOR FURTHER INFORMATION CONTACT:

Laura Compton, Senior Special Counsel, Amy Butler, Financial Analyst, or Alexandra Oprea, Special Counsel, Office of Derivatives Policy, Division of Trading and Markets, at (202) 551-5870 or

derivativespolicy@sec.gov,

Securities and Exchange Commission, 100 F Street NE, Washington, DC 20549-8549.

SUPPLEMENTARY INFORMATION:

Pursuant to Rule 3a71-2A(c) [1]

under the Securities Exchange Act of 1934,[2]

the Commission is publishing for public comment the staff report on the definitions of “security-based swap dealer” and “major security-based swap participant.”

By the Commission.

Dated: April 29, 2026.

J. Matthew DeLesDernier,

Deputy Secretary.

Appendix A

Definitions of “Security-Based Swap Dealer” and “Major Security-Based Swap Participant”: A Report by Staff of the Securities and Exchange Commission

Table of Contents

I. Table of Citations

II. Introduction

III. SBS Transaction Reports

IV. Staff Findings and Requests for Comment

A. Security-Based Swap Dealers

1. Definition of “Security-Based Swap Dealer”

2. Methodology for Identifying New Trade Activity

3. Analysis of the Definition of “Security-Based Swap Dealer”

a. Overall SBS Market Activity

i. SBS Market Activity Reviews in 2024 and 2011

ii. Estimates of Potential SBS Dealing Activity in 2024 and 2011

b. CDS De Minimis Threshold

i. CDS Market Participants' Activity

ii. Impact of Exclusions on CDS Activity

iii. $8 Billion Phase-In CDS De Minimis Threshold

iv. $3 Billion Scheduled CDS De Minimis Threshold

v. Alternative CDS De Minimis Thresholds

c. Non-CDS De Minimis Threshold

i. Non-CDS Market Participants' Activity

ii. Impact of Exclusions on Non-CDS Activity

iii. $400 Million Phase-In Non-CDS De Minimis Threshold

iv. $150 Million Scheduled Non-CDS De Minimis Threshold

v. Alternative Non-CDS De Minimis Thresholds

d. Hypothetical Total CDS and Non-CDS SBS De Minimis Thresholds

e. Special Entity SBS De Minimis Threshold

i. Market Participants' Activity With Likely Special Entities

ii. Impact of Exclusions on Activity With Likely Special Entities

iii. $25 Million Special Entity SBS De Minimis Threshold

iv. Alternative De Minimis Thresholds for Special Entity SBS

f. Retrospective Impact Analysis

i. Effects on Competition and Market Access

ii. Effects on Investor Protection

4. Requests for Comment

B. Major Security-Based Swap Participants

1. Definition of “Major Security-Based Swap Participant”

a. Major SBS Categories

b. Substantial Position and Substantial Counterparty Exposure

c. Hedging or Mitigating Commercial Risk

d. Financial Entity

e. Highly Leveraged

f. Attribution Rules for SBS Positions

2. Methodology for Identifying Potential MSBSP Status

a. Estimates of Open SBS Positions

b. Comparison to Safe Harbors

3. Analysis of the Definition of “Major Security-Based Swap Participant”

a. Characteristics of SBS Positions

b. Retrospective Impact Analysis

4. Requests for Comment

C. Scope and Quality of SBS Transaction Reports

1. Gaps in Data Elements of SBS Transaction Reports

2. Data Quality Observations Regarding SBS Transaction Reporting

3. Requests for Comment

Annex

I. Additional Methodology for Analysis of New Trade Activity

A. Identifying New Trade Activity Events

B. Determining the Notional Amount for Each New Trade Activity Event

( printed page 24039)

II. Additional Methodology for Analysis of Open SBS Positions

A. Identifying Open SBS Positions

B. Determining the Notional Amount of Each Open SBS Position

I. Table of Citations

Below is a table of citations to the Securities Exchange Act of 1934 (“Exchange Act”) [3]

rules referenced in this staff report:

Commission reference

CFR citation

(17 CFR)

Rule 3a67-1

§ 240.3a67-1

Rule 3a67-1(a)(1)

§ 240.3a67-1(a)(1)

Rule 3a67-1(a)(2)

§ 240.3a67-1(a)(2)

Rule 3a67-1(a)(2)(i)

§ 240.3a67-1(a)(2)(i)

Rule 3a67-1(a)(2)(ii)

§ 240.3a67-1(a)(2)(ii)

Rule 3a67-1(a)(2)(iii)

§ 240.3a67-1(a)(2)(iii)

Rule 3a67-1(b)

§ 240.3a67-1(b)

Rule 3a67-2(a)

§ 240.3a67-2(a)

Rule 3a67-2(b)

§ 240.3a67-2(b)

Rule 3a67-3(a)

§ 240.3a67-3(a)

Rule 3a67-3(b)

§ 240.3a67-3(b)

Rule 3a67-3(b)(1)

§ 240.3a67-3(b)(1)

Rule 3a67-3(b)(2)

§ 240.3a67-3(b)(2)

Rule 3a67-3(b)(3)

§ 240.3a67-3(b)(3)

Rule 3a67-3(b)(4)

§ 240.3a67-3(b)(4)

Rule 3a67-3(c)

§ 240.3a67-3(c)

Rule 3a67-3(c)(1)

§ 240.3a67-3(c)(1)

Rule 3a67-3(c)(2)

§ 240.3a67-3(c)(2)

Rule 3a67-3(c)(2)(i)(A)(1)

§ 240.3a67-3(c)(2)(i)(A)(1)

Rule 3a67-3(c)(2)(i)(A)(2)

§ 240.3a67-3(c)(2)(i)(A)(2)

Rule 3a67-3(c)(2)(i)(B)

§ 240.3a67-3(c)(2)(i)(B)

Rule 3a67-3(c)(2)(i)(C)

§ 240.3a67-3(c)(2)(i)(C)

Rule 3a67-3(c)(2)(i)(D)

§ 240.3a67-3(c)(2)(i)(D)

Rule 3a67-3(c)(2)(ii)

§ 240.3a67-3(c)(2)(ii)

Rule 3a67-3(c)(3)(i)(A)

§ 240.3a67-3(c)(3)(i)(A)

Rule 3a67-3(c)(3)(i)(B)

§ 240.3a67-3(c)(3)(i)(B)

Rule 3a67-3(c)(3)(ii)

§ 240.3a67-3(c)(3)(ii)

Rule 3a67-3(d)

§ 240.3a67-3(d)

Rule 3a67-3(e)

§ 240.3a67-3(e)

Rule 3a67-4(a)(1)

§ 240.3a67-4(a)(1)

Rule 3a67-4(a)(2)

§ 240.3a67-4(a)(2)

Rule 3a67-4(b)(1)

§ 240.3a67-4(b)(1)

Rule 3a67-4(b)(2)

§ 240.3a67-4(b)(2)

Rule 3a67-5

§ 240.3a67-5

Rule 3a67-5(a)

§ 240.3a67-5(a)

Rule 3a67-6

§ 240.3a67-6

Rule 3a67-6(a)

§ 240.3a67-6(a)

Rule 3a67-6(b)

§ 240.3a67-6(b)

Rule 3a67-7

§ 240.3a67-7

Rule 3a67-7(a)

§ 240.3a67-7(a)

Rule 3a67-7(b)

§ 240.3a67-7(b)

Rule 3a67-8(b)

§ 240.3a67-8(b)

Rule 3a67-9

§ 240.3a67-9

Rule 3a67-9(a)(1)

§ 240.3a67-9(a)(1)

Rule 3a67-9(a)(1)(i)

§ 240.3a67-9(a)(1)(i)

Rule 3a67-9(a)(2)

§ 240.3a67-9(a)(2)

Rule 3a67-9(a)(2)(i)

§ 240.3a67-9(a)(2)(i)

Rule 3a67-9(a)(3)(i)(A)

§ 240.3a67-9(a)(3)(i)(A)

Rule 3a67-9(a)(3)(i)(B)

§ 240.3a67-9(a)(3)(i)(B)

Rule 3a67-9(b)

§ 240.3a67-9(b)

Rule 3a67-10(a)(1)

§ 240.3a67-10(a)(1)

Rule 3a67-10(a)(2)

§ 240.3a67-10(a)(2)

Rule 3a67-10(a)(3)

§ 240.3a67-10(a)(3)

Rule 3a67-10(a)(4)

§ 240.3a67-10(a)(4)

Rule 3a67-10(b)(1)

§ 240.3a67-10(b)(1)

Rule 3a67-10(b)(2)

§ 240.3a67-10(b)(2)

Rule 3a67-10(b)(3)

§ 240.3a67-10(b)(3)

Rule 3a67-10(b)(3)(i)(A)

§ 240.3a67-10(b)(3)(i)(A)

Rule 3a67-10(b)(3)(ii)

§ 240.3a67-10(b)(3)(ii)

Rule 3a67-10(c)

§ 240.3a67-10(c)

Rule 3a67-10(c)(1)(i)

§ 240.3a67-10(c)(1)(i)

Rule 3a67-10(c)(1)(ii)

§ 240.3a67-10(c)(1)(ii)

Rule 3a67-10(c)(2)

§ 240.3a67-10(c)(2)

Rule 3a71-1

§ 240.3a71-1

Rule 3a71-1(a)

§ 240.3a71-1(a)

Rule 3a71-1(b)

§ 240.3a71-1(b)

Rule 3a71-1(c)

§ 240.3a71-1(c)

Rule 3a71-1(d)

§ 240.3a71-1(d)

Rule 3a71-1(d)(1)

§ 240.3a71-1(d)(1)

Rule 3a71-1(d)(2)

§ 240.3a71-1(d)(2)

Rule 3a71-2

§ 240.3a71-2

Rule 3a71-2(a)

§ 240.3a71-2(a)

Rule 3a71-2(a)(1)

§ 240.3a71-2(a)(1)

Rule 3a71-2(a)(1)(i)

§ 240.3a71-2(a)(1)(i)

Rule 3a71-2(a)(1)(ii)

§ 240.3a71-2(a)(1)(ii)

Rule 3a71-2(a)(1)(iii)

§ 240.3a71-2(a)(1)(iii)

Rule 3a71-2(a)(2)

§ 240.3a71-2(a)(2)

Rule 3a71-2(a)(2)(i)

§ 240.3a71-2(a)(2)(i)

Rule 3a71-2(a)(2)(ii)

§ 240.3a71-2(a)(2)(ii)

Rule 3a71-2(a)(2)(ii)(B)

§ 240.3a71-2(a)(2)(ii)(B)

Rule 3a71-2(a)(2)(iii)

§ 240.3a71-2(a)(2)(iii)

Rule 3a71-2(a)(3)

§ 240.3a71-2(a)(3)

Rule 3a71-2A

§ 240.3a71-2A

Rule 3a71-2A(a)(1)

§ 240.3a71-2A(a)(1)

Rule 3a71-2A(a)(2)

§ 240.3a71-2A(a)(2)

Rule 3a71-2A(a)(3)

§ 240.3a71-2A(a)(3)

Rule 3a71-2A(a)(4)

§ 240.3a71-2A(a)(4)

Rule 3a71-2A(a)(5)

§ 240.3a71-2A(a)(5)

Rule 3a71-2A(a)(6)

§ 240.3a71-2A(a)(6)

Rule 3a71-2A(b)

§ 240.3a71-2A(b)

Rule 3a71-2A(c)

§ 240.3a71-2A(c)

Rule 3a71-3(a)(1)

§ 240.3a71-3(a)(1)

Rule 3a71-3(a)(2)

§ 240.3a71-3(a)(2)

Rule 3a71-3(a)(3)

§ 240.3a71-3(a)(3)

Rule 3a71-3(a)(4)

§ 240.3a71-3(a)(4)

Rule 3a71-3(b)

§ 240.3a71-3(b)

Rule 3a71-3(b)(1)

§ 240.3a71-3(b)(1)

Rule 3a71-3(b)(1)(i)

§ 240.3a71-3(b)(1)(i)

Rule 3a71-3(b)(1)(ii)

§ 240.3a71-3(b)(1)(ii)

Rule 3a71-3(b)(1)(iii)

§ 240.3a71-3(b)(1)(iii)

Rule 3a71-3(b)(1)(iii)(A)(

1)

§ 240.3a71-3(b)(1)(iii)(A)(

1)

Rule 3a71-3(b)(1)(iii)(B)

§ 240.3a71-3(b)(1)(iii)(B)

Rule 3a71-3(b)(2)

§ 240.3a71-3(b)(2)

Rule 3a71-3(b)(2)(i)

§ 240.3a71-3(b)(2)(i)

Rule 3a71-3(b)(2)(ii)

§ 240.3a71-3(b)(2)(ii)

Rule 3a71-3(b)(2)(iii)

§ 240.3a71-3(b)(2)(iii)

Rule 3a71-3(d)

§ 240.3a71-3(d)

Rule 3a71-4

§ 240.3a71-4

Rule 3a71-5

§ 240.3a71-5

Regulation SBSR

§§ 242.900 through 242.909

Rule 901(c)(1)

§ 242.901(c)(1)

Rule 901(d)(2)

§ 242.901(d)(2)

Rule 901(d)(5)

§ 242.901(d)(5)

II. Introduction

Staff of the Securities and Exchange Commission (“Commission”) prepared this report to examine the effect and application of the definitions of “security-based swap dealer” and “major security-based swap participant,” as directed in Rule 3a71-2A.[4]

Title VII of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (“Title VII” and the “Dodd-Frank Act”) [5]

provided the Commission with regulatory authority over security-based swaps (“SBS”), the Commodity Futures Trading Commission (the “CFTC”) with regulatory authority over swaps, and the Commission and the CFTC (together, the “Commissions”) jointly with regulatory authority over mixed swaps.[6]

As a result, security-based swap dealers (“SBSDs”) and major security-based swap participants (“MSBSPs,” and together with SBSDs, “SBS Entities”) became subject to regulation by the Commission.

In 2012, as directed by the Dodd-Frank Act, the Commissions jointly adopted rules further defining the terms “security-based swap dealer” and “major security-based swap participant.” [7]

Those rules provided an exception from designation as an SBSD for an entity that engages in a de minimis quantity of SBS dealing, which the rules defined as $3 billion, subject to a phase-in level of $8 billion, with regard to credit default swaps (“CDS”) that constitute SBS; $150 million, subject to a phase-in level of $400 million, with regard to non-CDS that constitute SBS; and $25 million with regard to all SBS in which the counterparty is a special entity to whom the Dodd-Frank Act extends additional protections.[8]

Those rules also defined separate thresholds below which an entity would not become an MSBSP, requiring a daily average aggregate uncollateralized outward exposure of less than $1 billion in any major SBS category (with some market participants able to deduct from this exposure certain positions held for hedging or mitigating risk) and less than $2 billion for all SBS positions and a daily average aggregate uncollateralized outward exposure plus daily average aggregate potential outward exposure of less than $2 billion in any major SBS category

( printed page 24040)

(again, with some market participants able to deduct from this exposure certain positions held for hedging or mitigating risk) and less than $4 billion for all SBS positions.[9]

The Commissions adopted those rules after considering available 2011 transaction and position data for single-name CDS transactions and estimates for non-CDS markets based on more limited 2011 position data.[10]

This available 2011 data did not yet include information from the SBS transaction reporting that would later be required under the Title VII regulatory framework. To help the Commission evaluate the practical implications and effects of the definitions of “security-based swap dealer” and “major security-based swap participant” following implementation of the Title VII regulatory framework, the Commission in Rule 3a71-2A directed staff to complete and publish for public comment a report on these definitions after additional SBS data became available pursuant to other Title VII rules.[11]

That additional data began to become available when market participants commenced reporting information about their SBS transactions (the “SBS transaction reports”) on November 8, 2021,[12]

known as the data collection initiation date, and in the initial phase of reporting that followed became more consistent as market participants and the Commission implemented this new reporting requirement.

As directed in Rule 3a71-2A, staff prepared this report to inform the Commission's review of the effect and application of the rules further defining the terms “security-based swap dealer” and “major security-based swap participant,” including the SBSD de minimis exception and the MSBSP thresholds, and to inform the Commission's consideration of any changes to those rules.[13]

To accomplish those goals, this report leverages the SBS market data that has emerged from the SBS transaction reports, focusing on SBS market activity during calendar year 2024 in analysis of the definition of “security-based swap dealer” and on SBS positions as of the end of that year in analysis of the definition of “major security-based swap participant.”

Section III of this report describes the SBS transaction reports that staff analyzed to prepare this report. Section IV presents staff's findings from its analysis of the SBS transaction reports.

This report includes several observations for consideration, including:

Staff estimates that in 2024 trading activity in non-CDS was much larger, both in absolute value and as compared to trading activity in CDS, than anticipated when the Commissions adopted the joint definitional rules and that there may have been less notional amount of trading activity in CDS and more notional amount of trading activity in non-CDS in 2024 than in 2011, with the caveat that these estimates are limited by significant differences in the scope of data available in 2011 as compared to 2024, as well as by issues with data quality.

○ In 2011, 1,084 single-name CDS market participants had approximately $12.6 trillion in aggregate gross notional amount of trading activity. Based on the limited information about non-CDS available to the Commission at that time, the Commission estimated that non-CDS trading activity would constitute approximately 1/20th of the aggregate gross notional amount of all SBS trading activity.

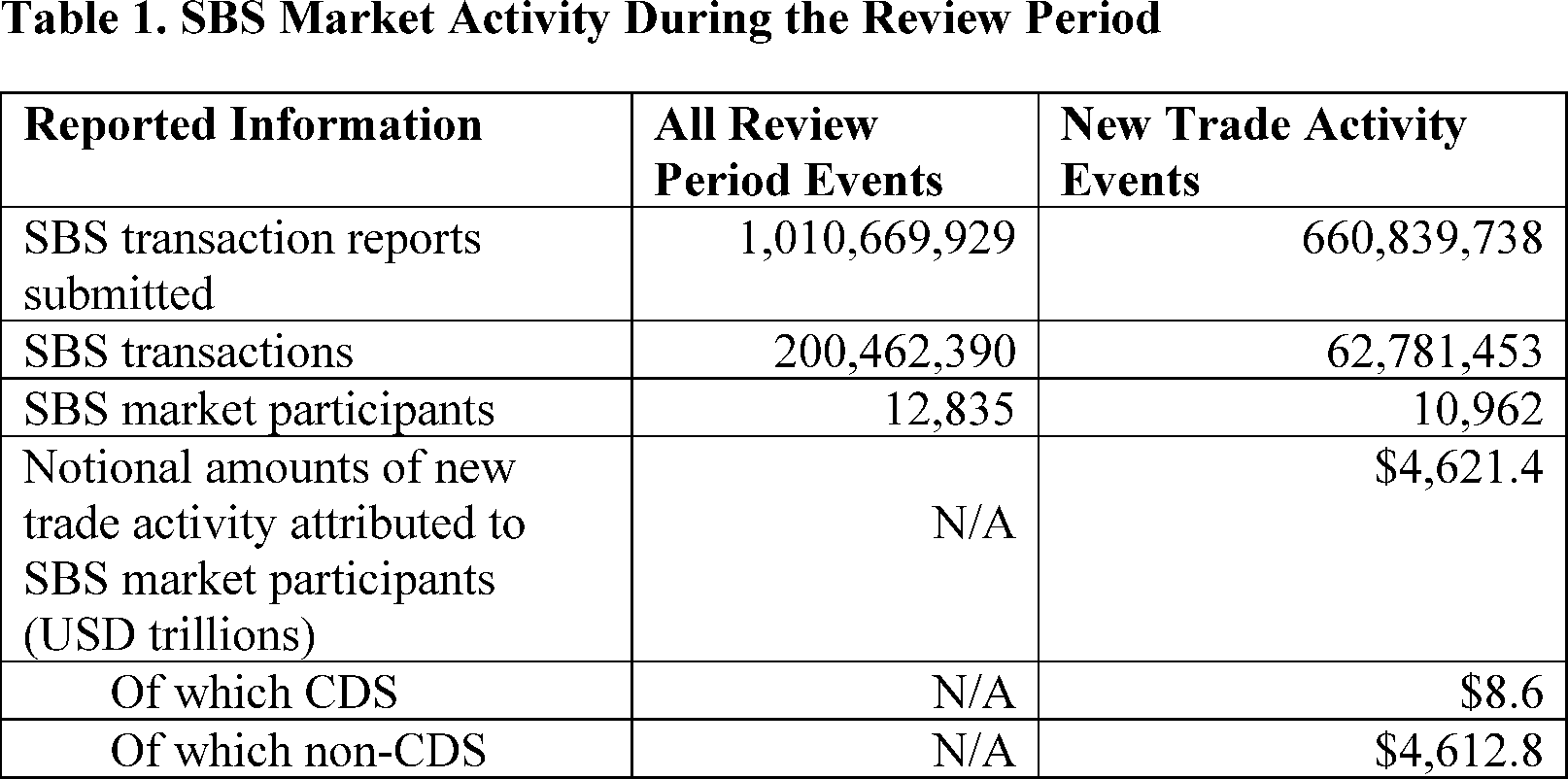

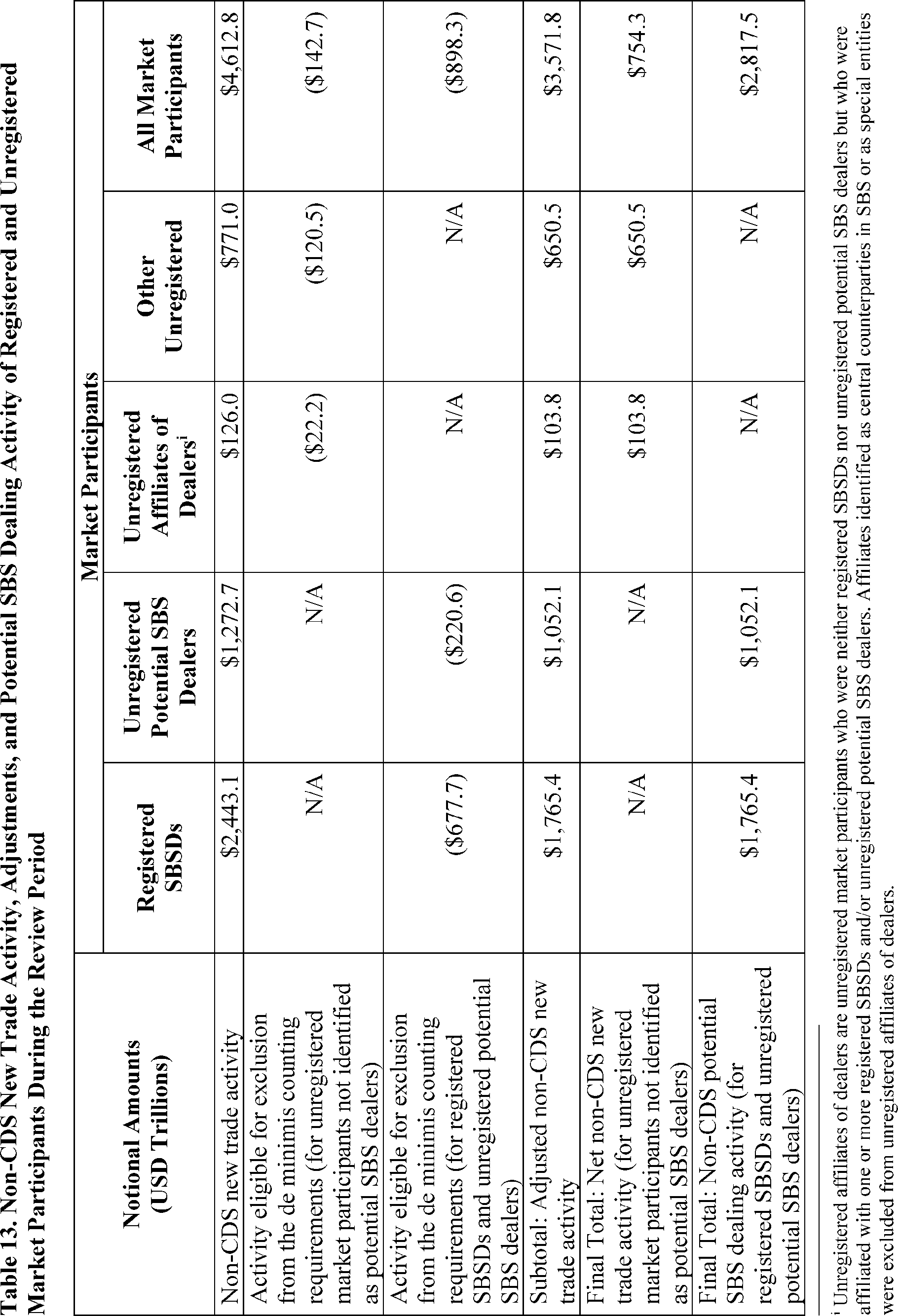

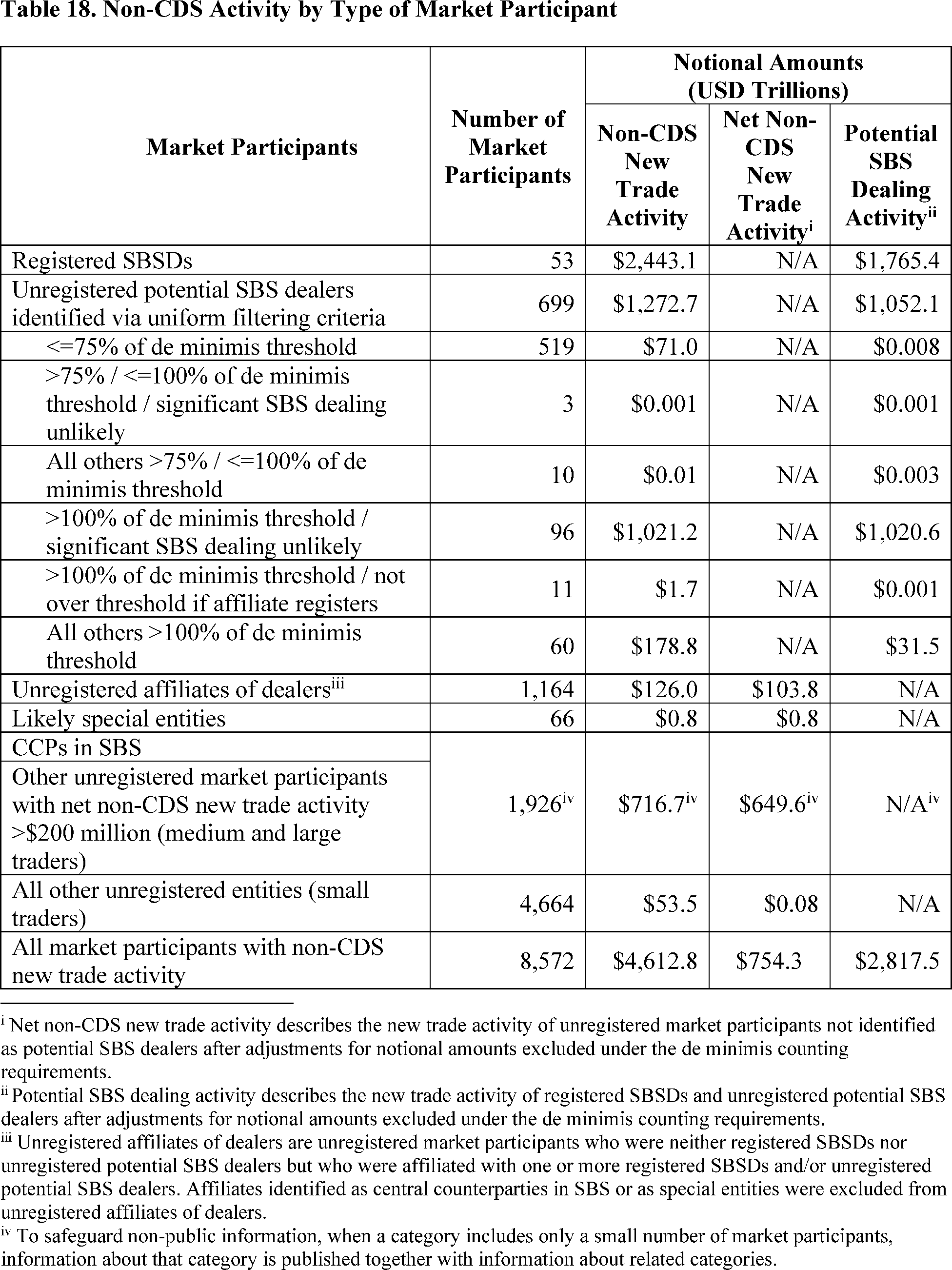

○ In 2024, 10,962 SBS market participants had a total of $4,621.4 trillion in notional amount of “new trade activity,” including 3,603 CDS market participants with approximately $8.6 trillion and 8,572 non-CDS market participants with approximately $4,612.8 trillion.

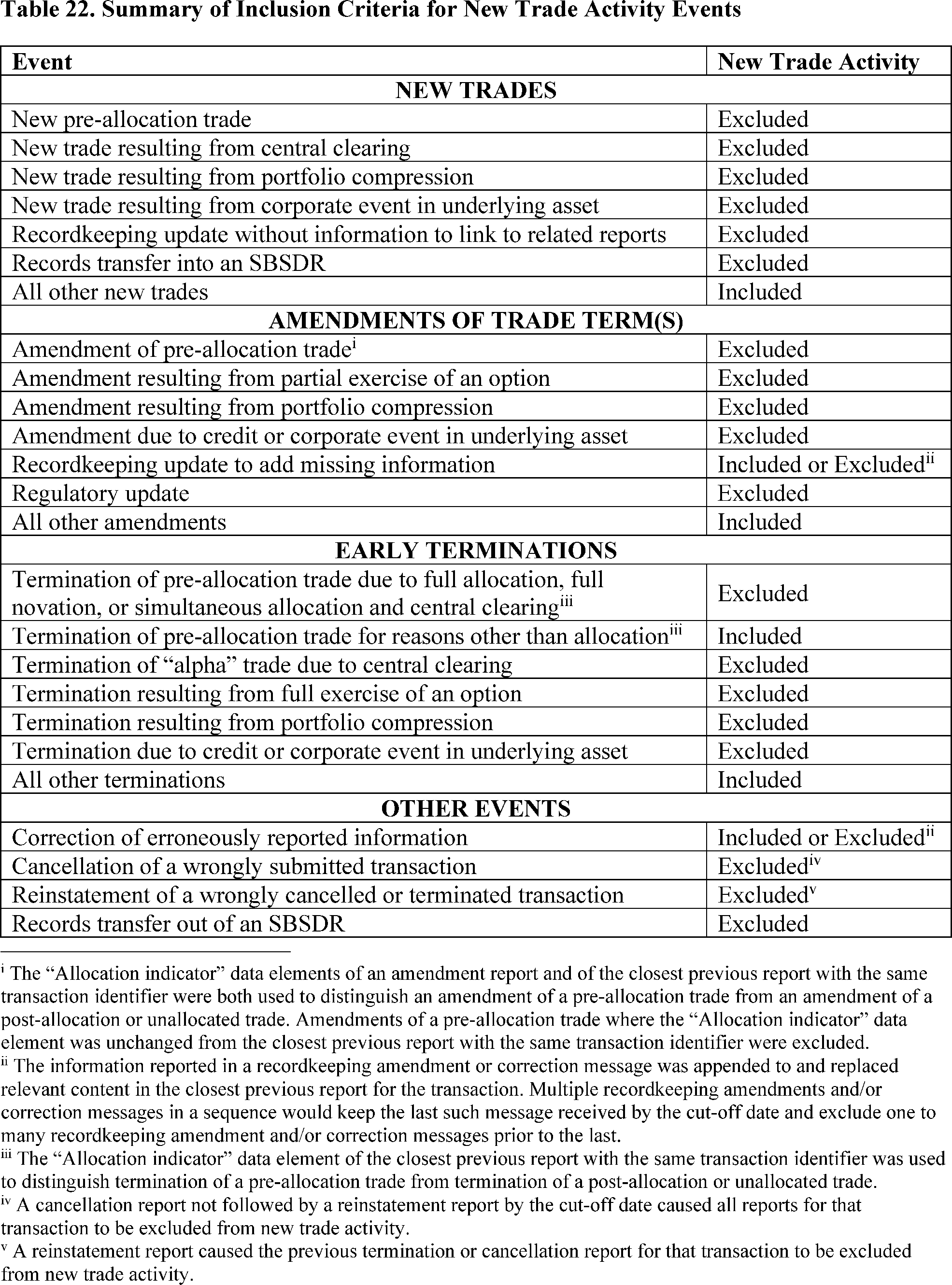

○ “New trade activity” refers to a reported event that appeared to be consistent with a new or modified investment agreement or decision between the counterparties (including reports of new trades, amendments,[14]

and terminations), as opposed to changes reflecting predetermined criteria or predetermined self-executing formulas, risk management or recordkeeping tasks, or duplicates of other reports. New trade activity includes activity that may be SBS dealing as well as activity that may not be SBS dealing and therefore should not be measured against the de minimis thresholds.[15]

Because each new trade activity event has two counterparties, attributing new trade activity to market participants doubles [16]

the total transacted notional amount of all new trade activity events.

○ Staff compared each de minimis threshold to market participants' “potential SBS dealing activity,” which refers to new trade activity, minus excluded items, of market participants that staff identified as having sufficient indicia of SBS dealing. Because the SBS transaction reports did not include definitive information about a market participant's engagement in the business of SBS dealing for a particular transaction, staff could apply criteria for these indicia of potential SBS dealing activity only at the counterparty level and not at the level of individual transactions or events. Estimates of market participants' potential SBS dealing activity thus may be exclusively SBS dealing activity, exclusively non-dealing activity, or a combination of the two. Estimates that any particular market participant engaged in potential SBS dealing activity above a de minimis threshold might reflect these limitations of available data.

○ Staff observed that market participants overall submitted significantly more substantive amendments to the terms of non-CDS transactions included in new trade activity (approximately $4,468.6 trillion, with some market participants regularly submitting multiple amendments of the same transaction each day) than they did substantive amendments to the terms of CDS transactions, and, pursuant to the methodology to measure new trade activity, each reported amendment counted as a separate new trade activity event.[17]

These substantial differences in reporting may reflect a higher volume of trading in non-CDS compared to CDS markets, a higher or lower volume of trading by individual market participants, reporting errors or inconsistencies, or a combination of these factors. To better understand the reports of

( printed page 24041)

non-CDS amendments, staff confirmed through discussion with multiple large market participants, together accounting for approximately $2,699.9 trillion in notional amount, that their reported amendments accurately reflected bona fide changes to the non-CDS trade consistent with a new or modified investment agreement or decision between the counterparties.

○ Even apart from events reported as amendments to trade terms, non-CDS events reported as new trades and early terminations consistent with a new or modified investment agreement or decision also far outpaced comparable CDS new trade activity and accounted for approximately $105.3 trillion and approximately $38.9 trillion, respectively, in notional amount of non-CDS new trade activity, compared to approximately $5.3 trillion and approximately $2.5 trillion, respectively, in notional amount of CDS new trade activity.

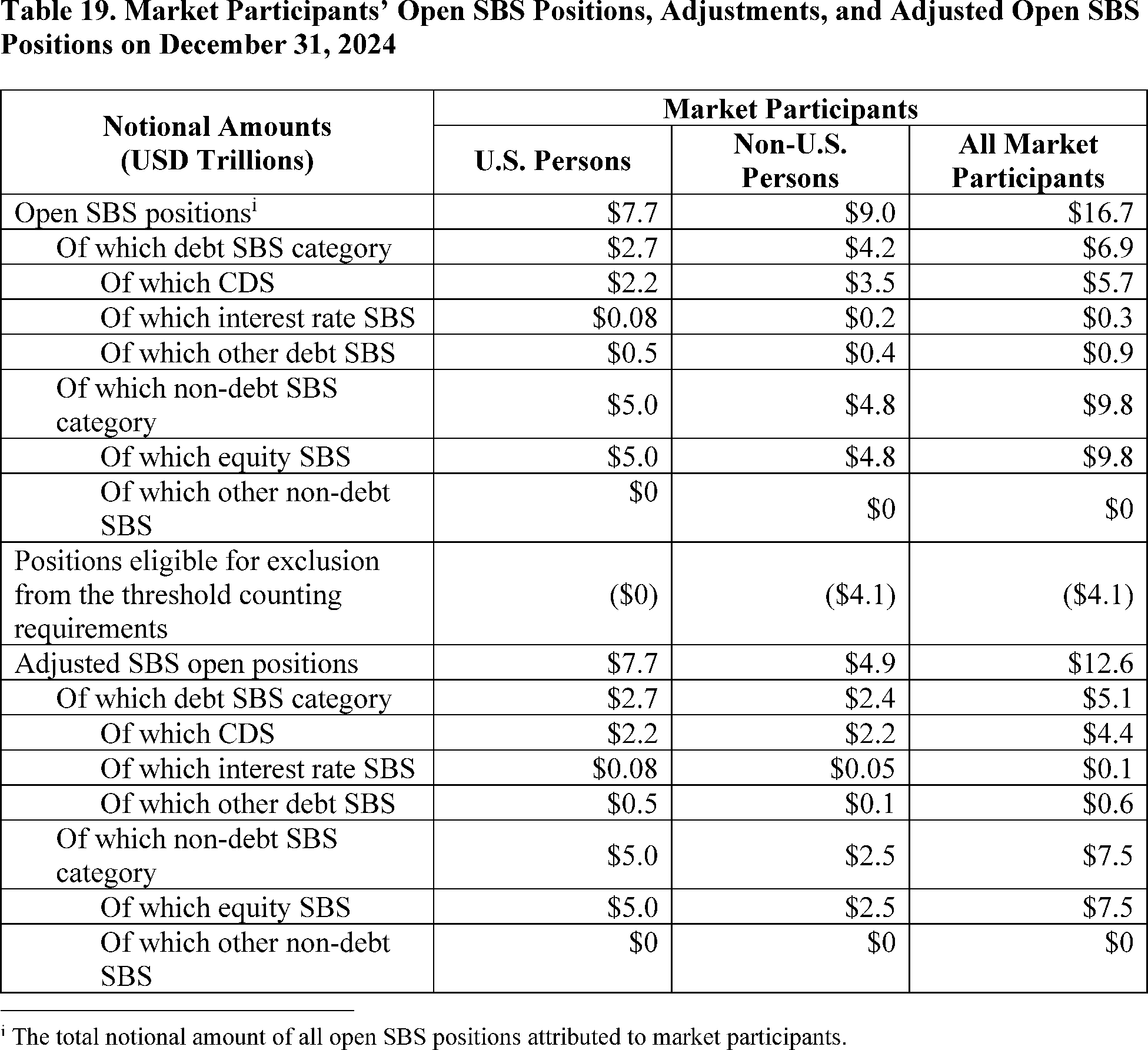

○ In contrast with this transaction-based new trade activity, the total notional amount of all open SBS positions attributed to market participants on December 31, 2024, was approximately $16.7 trillion, including approximately $5.7 trillion (34%) in CDS positions, approximately $1.2 trillion (7%) in interest rate and other non-CDS debt SBS, and approximately $9.8 trillion (59%) in equity SBS.

○ Recognizing the limitations of data scope and quality, the SBS transaction reports nevertheless suggest that non-CDS markets have become a far more significant part of the SBS market activity than previously anticipated. Over 99% of 2024 new trade activity in SBS was non-CDS, with CDS representing less than 1% of 2024 new trade activity.

See sections IV.A.3.a “Overall SBS Market Activity,” IV.B.3.a “Characteristics of SBS Positions,” and IV.C “Scope and Quality of SBS Transaction Reports” for further discussion.

Both CDS and non-CDS SBS markets appeared to be somewhat less concentrated in 2024 compared to 2011, based on 2024 CDS and non-CDS data and 2011 CDS data and non-CDS estimates.

○ In 2011, 28 single-name CDS market participants that appeared to be engaged in SBS dealing had $11.18 trillion (89%) of the $12.6 trillion in aggregate gross notional amount of trading activity by all 1,084 market participants that voluntarily reported such activity.[18]

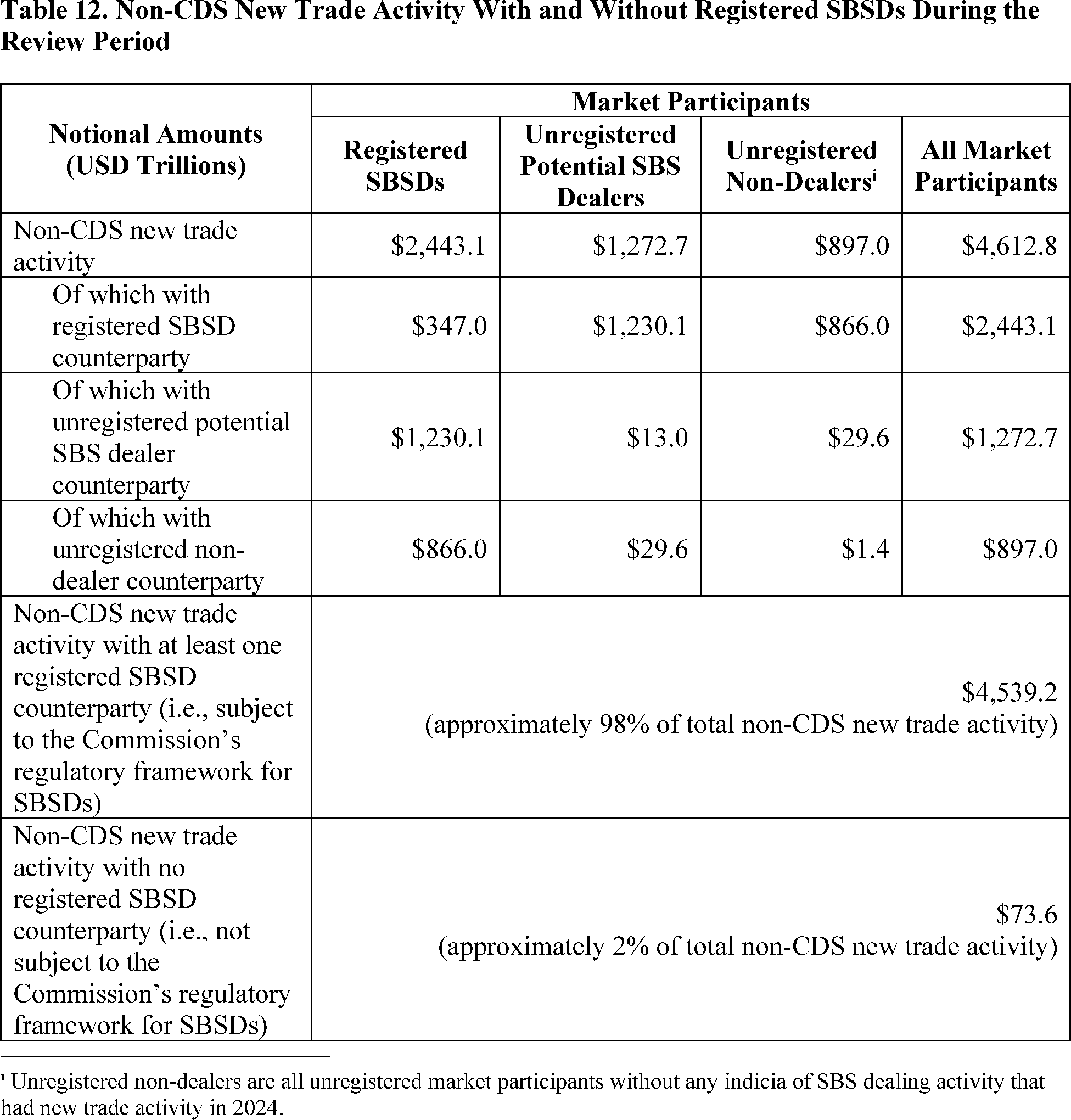

○ In 2024, 53 registered SBSDs and 853 unregistered potential SBS dealers [19]

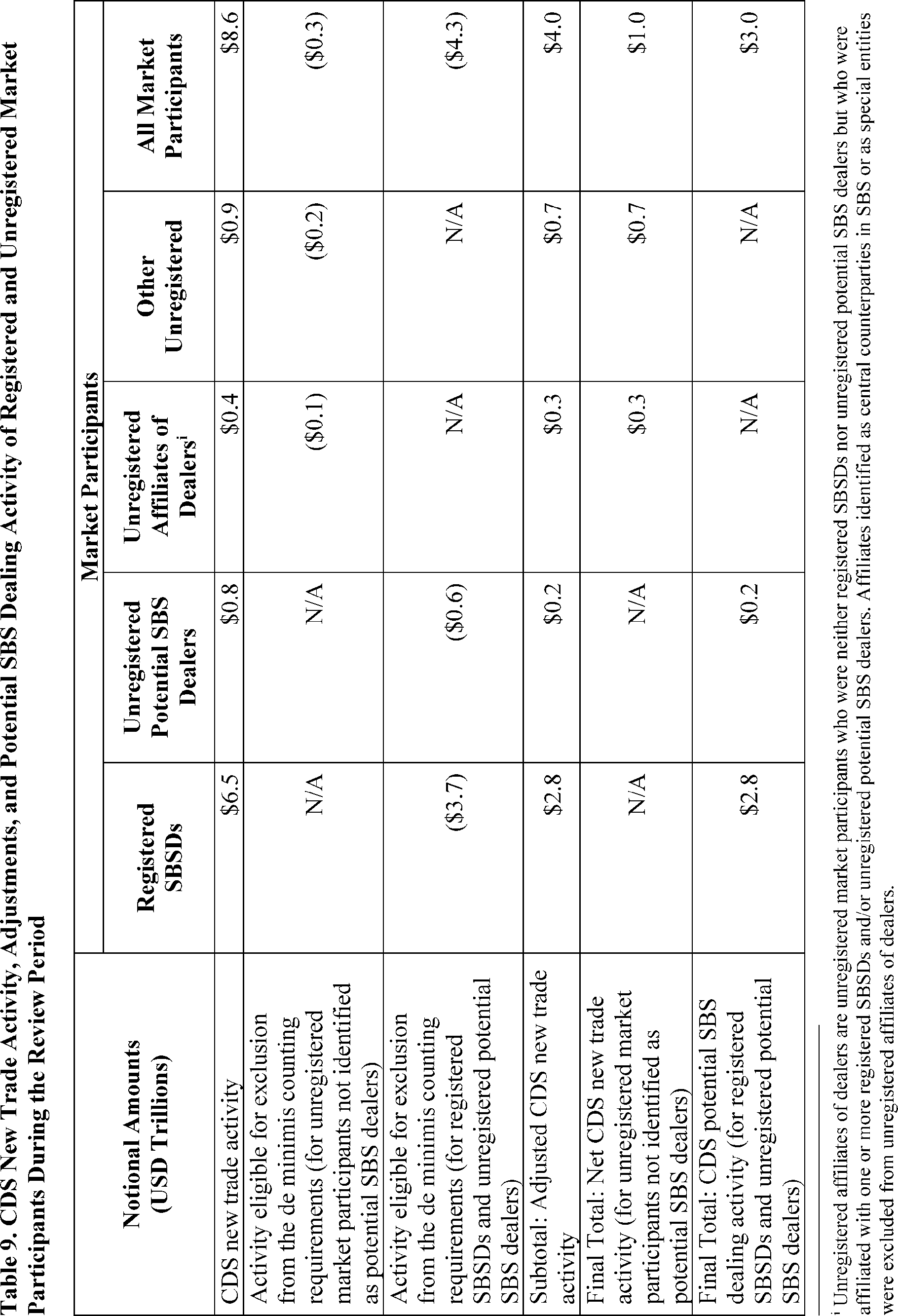

were among the 10,962 SBS market participants with new trade activity. Registered SBSDs ($2,443.1 trillion) and unregistered potential SBS dealers ($1,272.7 trillion) had a total of approximately $3,715.8 trillion (81%) of the $4,612.8 trillion in notional amount of non-CDS new trade activity. Registered SBSDs ($6.5 trillion) and unregistered potential SBS dealers ($0.8 trillion) had a total of approximately $7.3 trillion (85%) of the $8.6 trillion in notional amount of CDS new trade activity.

See sections IV.A.3.a “Overall SBS Market Activity,” IV.A.3.b.i “CDS Market Participants' Activity,” 0 “Non-CDS Market Participants' Activity,” and III.A.3.f.i “Effects on Competition and Market Access” for further discussion.

SBS markets are cross-border, with a significant number of non-U.S. market participants engaged in reported transactions.

○ Among the 53 entities registered as SBSDs on December 31, 2024, 23 (43%) were estimated to be U.S. persons and 30 (57%) were estimated to be non-U.S. persons.

○ Among 853 unregistered market participants identified (using uniform filtering criteria) as potentially engaged in SBS dealing, 325 (38%) were estimated to be U.S. persons and 528 (62%) were estimated to be non-U.S. persons.

See section IV.A.3.a “Overall SBS Market Activity” for further discussion.

The exclusions from the definition of “security-based swap dealer” [20]

are meaningful to the de minimis thresholds for CDS and non-CDS SBS but not to the de minimis threshold for SBS with special entities.

○ $4.6 trillion (54%) out of $8.6 trillion in notional amount of 2024 CDS new trade activity appeared to be eligible for one or more exclusions from potential SBS dealing activity counted toward the de minimis threshold for CDS.

○ $1,041.0 trillion (23%) out of $4,612.8 trillion in notional amount of 2024 non-CDS new trade activity appeared to be eligible for one or more exclusions from potential SBS dealing activity counted toward the de minimis threshold for non-CDS.

○ The exclusions appeared to have no impact on market participants' need to register or remain registered with the Commission as SBSDs due to SBS dealing activity with special entities.

See sections IV.A.3.b.ii “Impact of Exclusions on CDS Activity,” IV.A.3.c.ii “Impact of Exclusions on Non-CDS Activity,” and IV.A.3.e.ii “Impact of Exclusions on Activity with Likely Special Entities” for further discussion.

Although there appeared to be less concentration among market participants engaged in SBS dealing in 2024 compared to 2011, registered SBSDs nevertheless evidenced strong market participation in 2024.

○ Approximately 99% of the aggregate notional amount of all CDS new trade activity included at least one registered SBSD and thus was subject to the Commission's regulatory framework for SBSDs.

○ Approximately 98% of the aggregate notional amount of all non-CDS new trade activity included at least one registered SBSD and thus was subject to the Commission's regulatory framework for SBSDs.

○ Nearly all of the aggregate notional amount of SBS new trade activity with a market participant likely to be a special entity had a registered SBSD on the other side of the trade.

See sections IV.A.3.b “CDS De Minimis Threshold,” IV.A.3.c “Non-CDS De Minimis Threshold,” and IV.A.3.e “Special Entity SBS De Minimis Threshold” for further discussion.

Unregistered market participants appeared to make use of the de minimis exception to the definition of “security-based swap dealer” and the majority, though possibly not all, of those market participants appeared to have managed their SBS dealing to remain below the de minimis thresholds.

○ Unregistered potential SBS dealers identified through uniform filtering criteria accounted for approximately $0.2 trillion (6%) of the notional amount of potential SBS dealing activity [21]

in CDS. After excluding those below the de minimis threshold and market participants that appeared unlikely to be engaged in significant SBS dealing after manual review of additional publicly available information, staff identified three of these market participants, with potential SBS dealing activity in CDS totaling approximately $39.0 billion in notional amount, that may have surpassed the $8 billion de minimis threshold. If these three market participants had been registered as SBSDs throughout 2024, all CDS new trade activity with at least one registered SBSD counterparty would have increased by approximately $65.6 billion to approximately $8,567.1 billion.

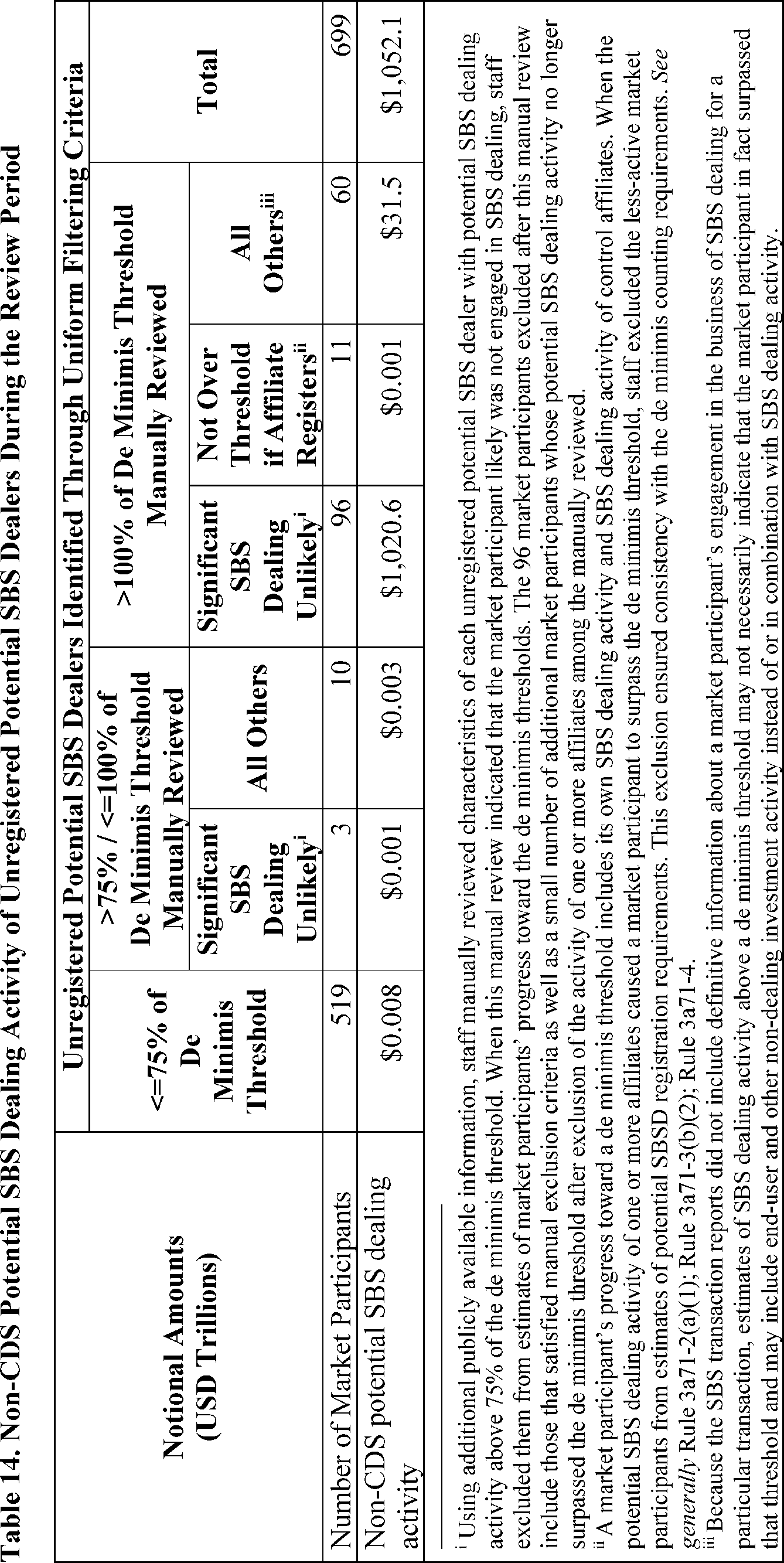

○ Unregistered potential SBS dealers identified through uniform filtering criteria accounted for approximately $1,052.1 trillion (37%) of the notional amount of potential SBS dealing activity in non-CDS. After excluding those below the de minimis threshold and market participants that appeared unlikely to be engaged in significant SBS dealing after manual review of additional publicly available information, staff identified 60 of these market participants, with potential SBS dealing activity in non-CDS totaling approximately $31.5 trillion in notional amount, that may have surpassed the $400 million de minimis threshold. If these 60 market participants had been registered as SBSDs throughout 2024, all non-CDS new trade activity with at least one registered SBSD counterparty would have increased by approximately $57.4 trillion to approximately $4,596.6 trillion.

○ Because the SBS transaction reports did not include definitive information about a market participant's engagement in the business of SBS dealing for a particular transaction, however, estimates of SBS dealing activity above a de minimis threshold may not necessarily indicate that a market participant in fact surpassed that threshold and indeed may include end-user and other non-dealing investment activity. In particular, as the uniform filtering criteria for potential SBS dealing activity could be

( printed page 24042)

applied only at the counterparty level and not at the level of individual transactions or events, all of a market participant's new trade activity net of exclusions, plus that of affiliates estimated to be engaged in SBS dealing, counted toward the de minimis thresholds. The activity of unregistered potential SBS dealers may have been exclusively SBS dealing activity, exclusively non-dealing activity, or a combination of the two.

See sections IV.A.3.b “CDS De Minimis Threshold,” IV.A.3.c “Non-CDS De Minimis Threshold,” and IV.A.3.e “Special Entity SBS De Minimis Threshold” for further discussion.

If the phase-in de minimis thresholds expire as scheduled, additional market participants may be required to register as SBSDs.

○ If the $3 billion scheduled CDS de minimis threshold had applied to the twelve-month period ended on December 31, 2024, four market participants with potential SBS dealing activity in CDS more than $3 billion and up to $8 billion, plus the three additional market participants with potential SBS dealing activity in CDS above $8 billion, may have been required to register as SBSDs.

○ If the $150 million scheduled non-CDS de minimis threshold had applied to the twelve-month period ended on December 31, 2024, 21 market participants with potential SBS dealing activity in non-CDS more than $150 million and up to $400 million, plus the 60 additional market participants with potential SBS dealing activity in non-CDS above $400 million, may have been required to register as SBSDs.

See sections IV.A.3.b.iv “$3 Billion Scheduled CDS De Minimis Threshold” and IV.A.3.c.iv “$150 Million Scheduled Non-CDS De Minimis Threshold” for further discussion.

Only limited information relevant to the MSBSP thresholds is available to the Commission.

○ Information about valuation and collateral, although reported for swap transactions, is not reported for SBS transactions and was not available to staff.[22]

That information may have allowed staff to estimate more of market participants' progress toward the MSBSP thresholds.

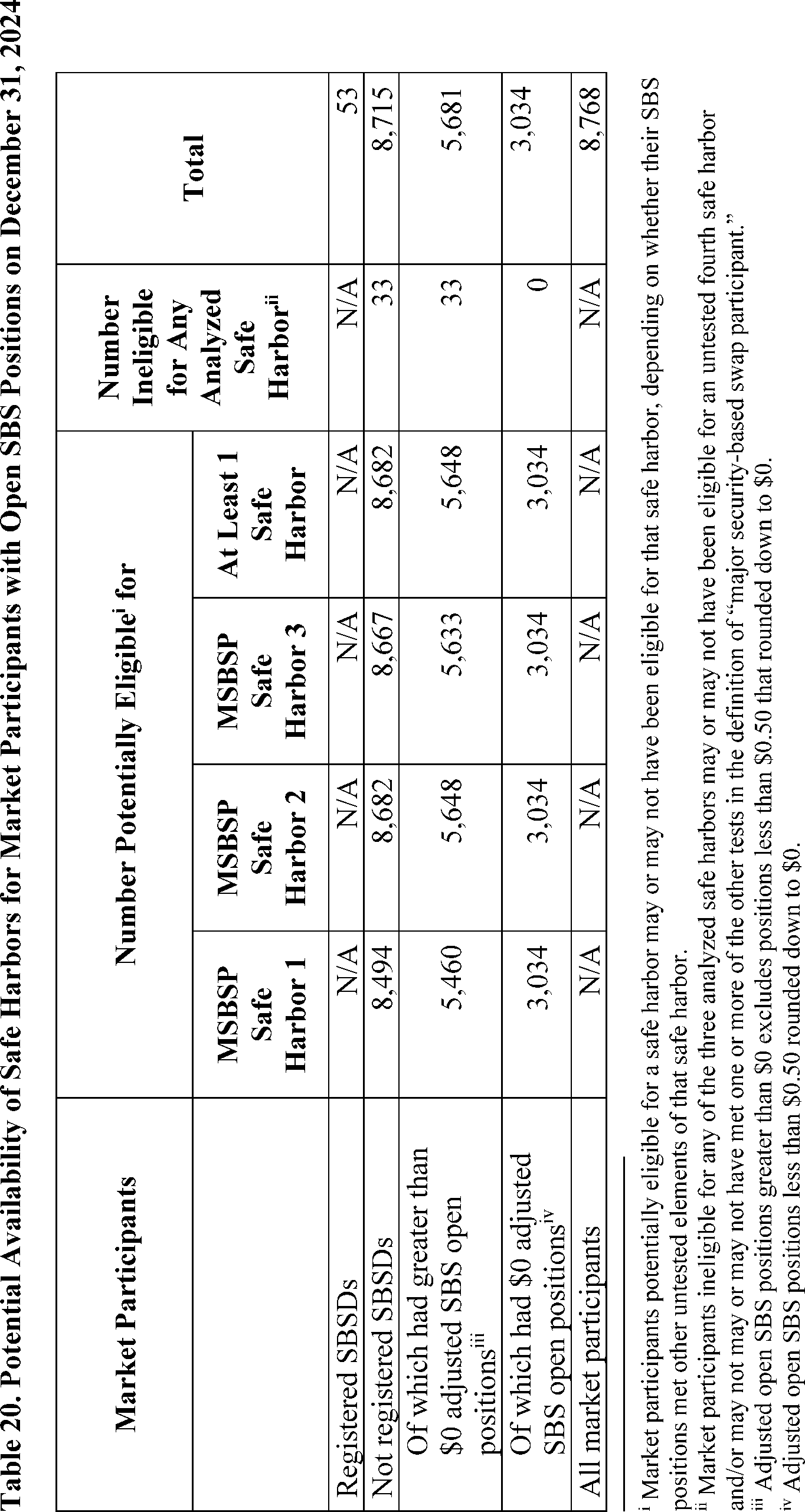

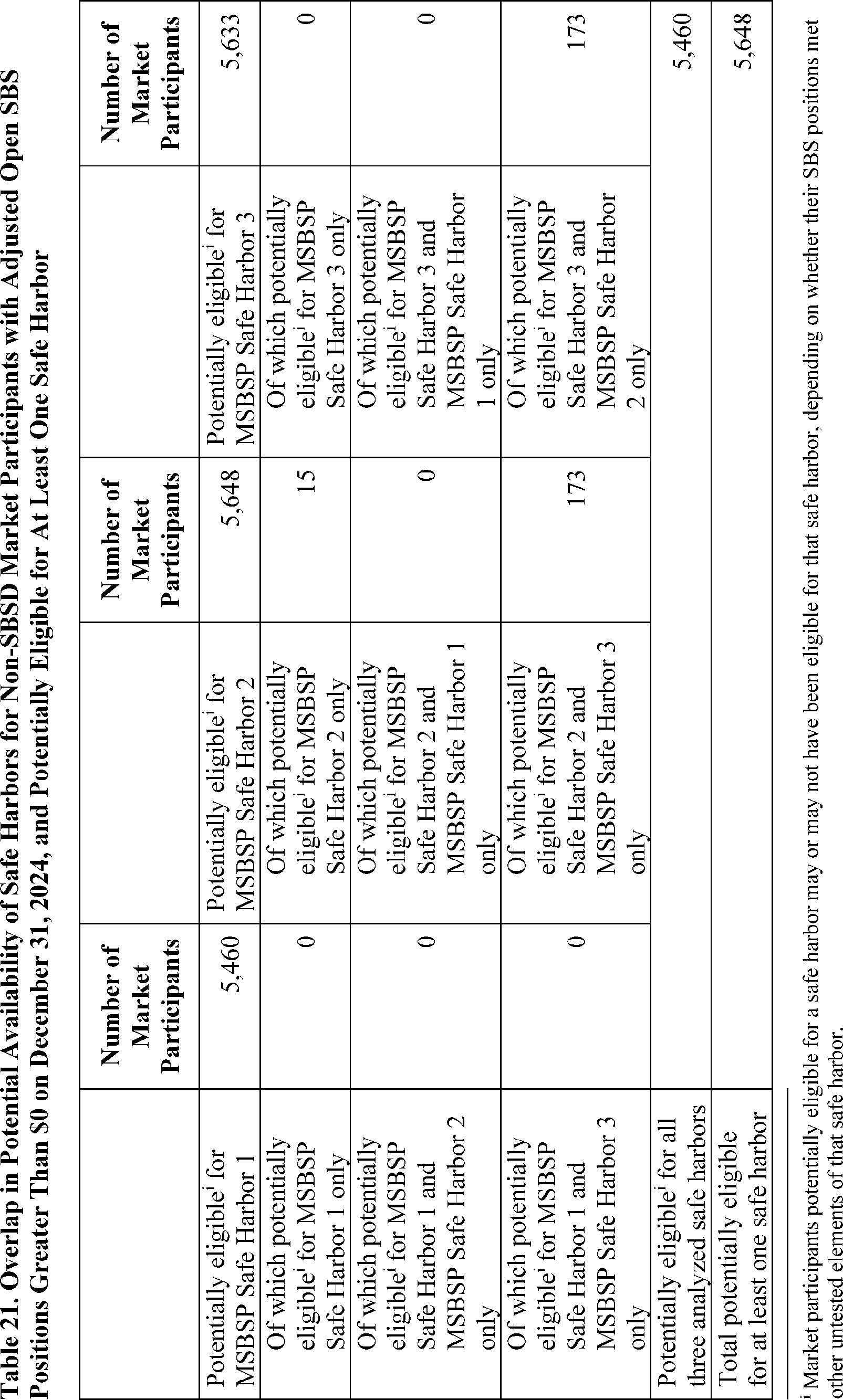

○ Thirty-three out of 8,715 unregistered market participants with open positions on December 31, 2024, did not appear to be eligible for any of the three analyzed safe harbors from the definition of “major security-based swap participant” because their positions were too large for those safe harbors, though SBS transaction report data is insufficient to determine whether those market participants should have registered as MSBSPs. These 33 market participants had a total of approximately $1.9 trillion in open positions that counted toward the MSBSP thresholds.

○ The remaining 8,682 unregistered market participants with open positions on that date did not appear to be ineligible for all three analyzed safe harbors. Additional information would be required to complete estimates of these market participants' status as MSBSPs.

○ Available data about SBS positions on December 31, 2024, did not reveal trends suggesting that market participants are managing their SBS positions in relation to the MSBSP thresholds, but available data also did not address significant aspects of those thresholds.

See section IV.B.3 “Analysis of the Definition of 'Major Security-Based Swap Participant' ” for further discussion.

Staff observed recurrent data quality issues, as well as gaps between the scope of data elements that comprise the SBS transaction reports and the definitions of “security-based swap dealer” and “major security-based swap participant,” that could have affected the accuracy of estimates of SBS dealing and MSBSP activity.

See section IV.C “Scope and Quality of SBS Transaction Reports” for further discussion.

This report is intended to inform the Commission's consideration of the definitions of “security-based swap dealer” and “major security-based swap participant.” Nine months after publication of this report and after considering any public comments received, the Commission may by order either terminate the phase-in period for the de minimis thresholds, thereby allowing thresholds of $3 billion for CDS that constitute SBS and $150 million for non-CDS that constitute SBS to take effect and replace the current phase-in thresholds of $8 billion and $400 million, respectively, or propose different thresholds through rulemaking.[23]

Rule 3a71-2 set a phase-in termination date after which the scheduled thresholds of $3 billion and $150 million would take effect, which had been November 6, 2026; however, the Commission subsequently issued an order providing a temporary conditional exemption that has the effect of continuing to apply the phase-in thresholds of $8 billion and $400 million until May 8, 2028.[24]

The public is invited to comment on all aspects of this report, which may inform the Commission's consideration of potential changes to the de minimis exception and the rules further defining the terms “security-based swap dealer” and “major security-based swap participant.”

III. SBS Transaction Reports

Regulation SBSR implements Title VII's requirement that market participants report to a security-based swap data repository (“SBSDR”) information about their SBS transactions, some of which is publicly disseminated.[25]

On November 8, 2021, market participants began to report information about their SBS transactions to SBSDRs under Regulation SBSR. Pursuant to the Commission's 2019 and 2025 compliance statements regarding these SBS transaction reports (“compliance statements”), market participants temporarily are generally able to choose not to report an SBS transaction or data element required by Regulation SBSR if the CFTC's swap reporting requirements would not require a comparable swap transaction or data element to be reported.[26]

Accordingly, the SBSDRs have prepared technical specifications for SBS transaction reports, and these SBSDR technical specifications are consistent with CFTC swap reporting requirements,[27]

including the CFTC's technical specification for swap reporting (the “CFTC Technical Specification”).[28]

Market participants prepare reports of SBS transactions pursuant to an SBSDR technical specification and submit those reports to an SBSDR. Each report typically consists of a message containing information about an event related to the SBS transaction; an SBS

( printed page 24043)

transaction could be the subject of multiple event messages.

IV. Staff Findings and Requests for Comment

A. Security-Based Swap Dealers

1. Definition of “Security-Based Swap Dealer”

Section 3(a)(71)(A) of the Exchange Act and Rule 3a71-1 define the term “security-based swap dealer” as any person who: (1) holds itself out as a dealer in SBS; (2) makes a market in SBS; (3) regularly enters into SBS with counterparties as an ordinary course of business for its own account; or (4) engages in any activity causing it to be commonly known in the trade as a dealer or market maker in SBS.[29]

The term “security-based swap dealer” does not include a person that enters into SBS for such person's own account, either individually or in a fiduciary capacity, but not as a part of regular business.[30]

An entity that meets one of the tests in the definition of “security-based swap dealer” nevertheless is excepted from that definition if it engages in a de minimis quantity of SBS dealing.[31]

Pursuant to thresholds the Commission has adopted, a person shall be deemed not to be an SBSD, and therefore is not required to register with the Commission or comply with the regulatory framework for SBSDs, if the positions connected with the person's SBS dealing activity, together with the positions connected with any SBS dealing activity of control affiliates,[32]

over the immediately preceding twelve months do not exceed an aggregate gross notional amount of:

(1) $3 billion, subject to a phase-in level [33]

of $8 billion, with regard to CDS that constitute SBS;

(2) $150 million, subject to a phase-in level of $400 million, with regard to non-CDS that constitute SBS; and

(3) $25 million with regard to all SBS in which the counterparty is a special entity to whom the Dodd-Frank Act extends additional protections.[34]

When adopting the definition of the term “security-based swap dealer,” the Commission stated that whether a person is an SBSD would depend on the relevant facts and circumstances.[35]

The Commission considered the following factors relevant for identifying SBSDs and distinguishing them from other market participants: (1) providing liquidity to market professionals or other persons in connection with SBS; (2) seeking to profit by providing liquidity in connection with SBS; (3) providing advice in connection with SBS or structuring SBS; (4) presence of regular clientele and actively soliciting clients; (5) use of inter-dealer brokers; and (6) acting as a market maker on an organized SBS exchange or trading system.[36]

In determining whether a person is an SBSD, certain SBS are not considered and thus are not “counted” toward the de minimis thresholds. These non-countable SBS include any of the person's SBS with majority-owned affiliates [37]

and the SBS of any control affiliate that is already or soon will be required to be registered with the Commission as an SBSD.[38]

U.S. persons, as well as non-U.S. persons that qualify as conduit affiliates, must otherwise count toward the de minimis thresholds all their own SBS dealing activity and any SBS dealing activity of their control affiliates.[39]

Non-U.S. persons that are not conduit affiliates, on the other hand, count only their and their control affiliates' (1) SBS entered into with a U.S. person, except for some SBS conducted through a registered SBSD's foreign branch; (2) SBS guaranteed by a U.S.-person control affiliate of the non-U.S. person; and (3) SBS that are arranged, negotiated, or executed by U.S.-located personnel of the non-U.S. person or its agent (each, an “ANE transaction”), except for certain SBS that qualify for an exception to counting these ANE transactions.[40]

However, non-U.S. persons that are not conduit affiliates do not count certain anonymous centrally cleared transactions that are platform-traded, even if they fall into one of these three countable categories.[41]

The de minimis exception strikes a balance between regulatory goals and burdens [42]

and reflects an intention to identify persons for whom regulation is warranted either “[d]ue to the nature of their interactions with counterparties” or “to promote market stability and transparency, in light of the role those persons occupy within the [SBS] markets.” [43]

The Commission crafted the de minimis exception to: (1) allow persons to accommodate existing clients that have a need for SBS in conjunction with other financial services or commercial activities without the costs of registering as an SBSD or establishing separate relationships with registered SBSDs; (2) promote competition in SBS dealing activity for persons beginning to engage in SBS dealing; (3) provide an objective test for market participants; and (4) further the interest of regulatory efficiency when the amount of a person's SBS dealing activity does not warrant regulation in comparison to the overall market for SBS.[44]

2. Methodology for Identifying New Trade Activity

Staff analyzed SBS transaction events [45]

that occurred [46]

between January 1, 2024, and December 31, 2024 (the “review period”), and were received by an SBSDR through a

( printed page 24044)

cutoff date [47]

of February 28, 2025.[48]

Any events associated with an SBS transaction [49]

that was subsequently cancelled and not reinstated by the cutoff date were excluded. Staff then identified reported events that represented new trade activity (“new trade activity”) [50]

and determined the gross notional amount [51]

associated with each new trade activity event.

Next, staff determined which of the three de minimis thresholds applied to the SBS reported in each new trade activity event. New trade activity events with a product identifier [52]

consistent with CDS were classified as CDS to which the de minimis thresholds in Rule 3a71-2(a)(1)(i) apply. New trade activity events with a product identifier consistent with any other SBS were classified as non-CDS to which the de minimis thresholds in Rule 3a71-2(a)(1)(ii) apply. SBS transaction reports do not contain information sufficient to distinguish special entity counterparties from other counterparties.[53]

Using third-party data sources, however, staff was able to identify certain counterparties as more likely than others to be special entities. New trade activity events with a counterparty that appeared likely to be a special entity were classified as the other counterparty's SBS with a special entity, to which the de minimis threshold in Rule 3a71-2(a)(1)(iii) applies.[54]

Staff used these estimates of new trade activity to review overall SBS market activity and as a starting point to identify potential SBS dealing activity over the twelve months of the review period ending on December 31, 2024 (the “measurement date”). A description of staff's methodology for identifying new trade activity events and determining their notional amounts appears in Annex section I.

3. Analysis of the Definition of “Security-Based Swap Dealer”

Staff prepared descriptive analytics of SBS market activity overall and of activity in the CDS, non-CDS and special entity SBS markets. As directed by the Commission, these descriptive analytics include staff's analysis of each significant element [55]

of the definition of “security-based swap dealer” for which data was available.[56]

The Commission also directed staff to assess whether the de minimis thresholds should be increased or decreased,[57]

and these descriptive analytics include staff's assessment of hypothetical alternative de minimis thresholds. Finally, staff retrospectively analyzed the impacts of the definition on competition, market access, and investor protection.[58]

a. Overall SBS Market Activity

i. SBS Market Activity Reviews in 2024 and 2011

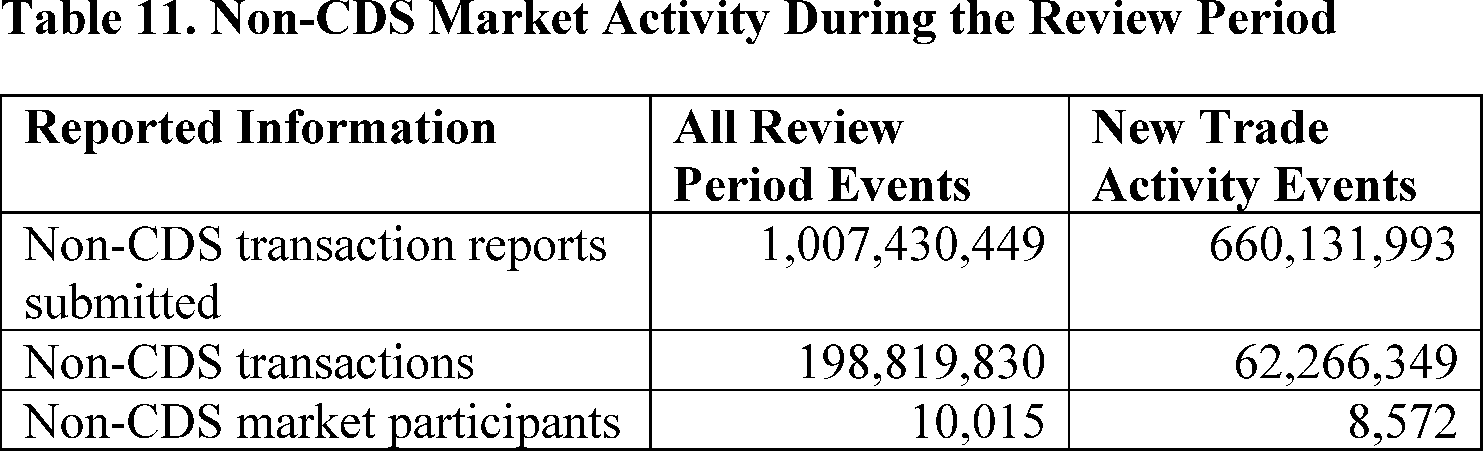

As shown in Table 1, market participants submitted to SBSDRs before the cut-off date 1,010,669,929 SBS transaction reports about events that occurred during the 2024 review period. These review period events related to 200,462,390 unique SBS transactions that involved 12,835 unique market participants and 9,191 affiliated groups.[59]

Among these were 660,839,738 unique new trade activity events related to 62,781,453 unique SBS transactions involving 10,962 unique market participants. These 10,962 unique SBS market participants included 7,736 affiliated groups of one or more market participants as of the measurement date.[60]

There was a total notional amount of approximately $2,310.7 trillion in new trade activity events during the review period. This total reflects the transacted notional amounts of the reported new trade activity events, providing a snapshot of the volume of new trade activity transactions in the SBS market at large. By contrast, when measuring market participants' progress toward the de minimis thresholds, staff took an individualized approach, analyzing each market participant's total notional amount of new trade activity. Because each new trade activity event has two counterparties, attributing new trade activity to market

( printed page 24045)

participants doubles [61]

the total transacted notional amount of all new trade activity events during the review period, resulting in approximately $4,621.4 trillion of new trade activity attributed to market participants.

The information in the 2024 SBS transaction reports differs in scope, in some cases substantially, from the 2011 data that the Commission reviewed in 2012. For SBS that are CDS, the 2011 data included a sample of “all new, risk transfer, dollar-adjusted, gold record transactions in both corporate and sovereign single-name [CDS]” submitted to the Depository Trust and Clearing Corporation's Trade Information Warehouse (“DTCC-TIW”) in 2011, as well as 2011 monthly single-name CDS position data provided by DTCC-TIW.[62]

Market participants submitted this transaction and end-of-week position data to DTCC-TIW on a voluntary basis. The transactions and positions provided to the Commission were those where at least one of the counterparties and/or the reference entity was a U.S. entity, with status as a U.S. entity determined by DTCC-TIW. The 2011 CDS data reviewed by the Commission in 2012 thus did not include transactions or positions between two non-U.S.-entity counterparties if the reference entity also was not a U.S. entity and did not provide any intra-weekly position information nor any information on the underlying security holdings of reference entities. For non-CDS SBS, available 2011 data was limited to publicly disseminated information about aggregate positions in credit and equity derivatives; transaction-level non-CDS data was unavailable.[63]

By contrast, the 2024 SBS transaction reports included all SBS reported to an SBSDR, including both CDS and non-CDS. The scope of SBS transaction reports submitted to SBSDRs may have been broader in some cases and/or narrower in other cases than the scope of the Commission's access to DTCC-TIW reports, for example because (1) the SBS transaction reports include CDS and non-CDS SBS that are subject to Title VII reporting requirements, whereas the reports to DTCC-TIW are voluntary and the DTCC-TIW SBS transaction and position data includes only single-name CDS; (2) the DTCC-TIW reports available to the Commission are those with at least one U.S.-entity counterparty or reference entity, whereas the Title VII reporting requirements apply to a different set of SBS, including SBS with a U.S.-person counterparty, SBS with a non-U.S.-person counterparty registered as an SBSD, and SBS with other U.S. jurisdictional characteristics, but not including SBS solely because of the U.S. character of the reference entity; and (3) the definition of “U.S. person” for purposes of the Title VII reporting requirements may differ from DTCC-TIW's criteria for identifying U.S. entities.

Both the number of SBS market participants and the notional amount of SBS transactions available for review were larger in 2024 compared to 2011. In 2012, the Commission reviewed 2011 trading activity of 1,084 single-name CDS market participants with approximately $12.6 trillion in aggregate gross notional amount.[64]

By contrast, the non-CDS data available to the Commission in 2011 did not include trading activity. Rather, the Commission had available to it only two limited data points about non-CDS positions: Bank for International Settlement estimates comparing the global notional amounts outstanding in equity forwards and swaps compared to credit default swaps as of June 2011 and U.S. Office of the Comptroller of the Currency data showing the notional amounts outstanding of credit and equity derivatives as of June 30, 2011, held by U.S. commercial banks and trust companies.[65]

Based on this limited non-CDS position data, the Commission estimated that non-CDS trading activity would constitute approximately 1/20th of the aggregate gross notional amount of all SBS trading activity.[66]

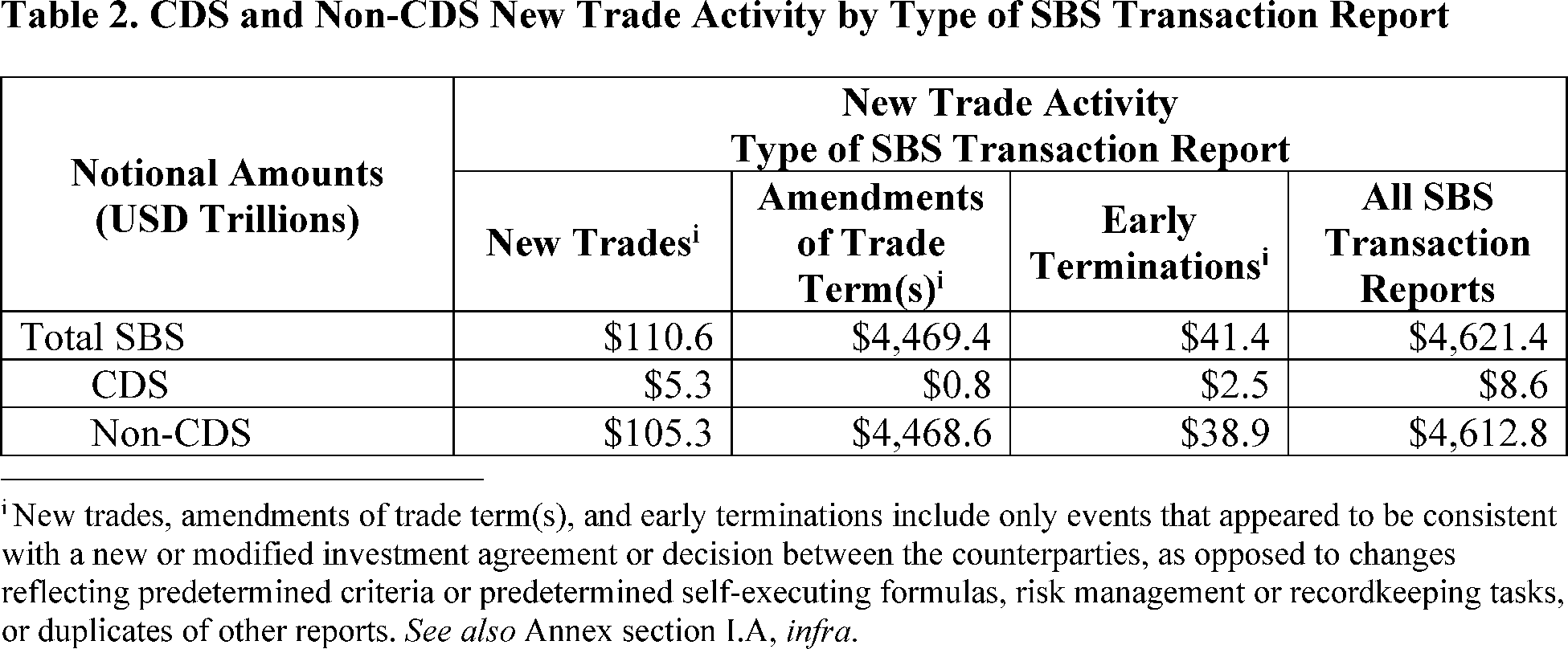

For the current analysis, staff reviewed 2024 new trade activity of 10,962 market participants with a total of approximately $4,621.4 trillion in notional amount, as reported to SBSDRs. This amount comprised $8.6 trillion in CDS new trade activity and $4,612.8 trillion in non-CDS new trade activity, including products such as equity, non-CDS debt, interest rate, and other SBS. As shown in Table 2, approximately $5.3 trillion in notional amount of 2024 CDS new trade activity (approximately 61% of all CDS new trade activity) represented events reported as new trades, compared to approximately $0.8 trillion (10%) in notional amount representing events reported as amendments to trade terms consistent with a new or modified investment agreement or decision and approximately $2.5 trillion (29%) in notional amount representing events reported as early terminations consistent with a new or modified investment agreement or decision. By contrast, a significantly larger portion of non-CDS new trade activity, approximately

( printed page 24046)

$4,468.6 trillion in notional amount (approximately 97% of all non-CDS new trade activity), represented events reported as amendments to trade terms consistent with a new or modified investment agreement or decision, with some market participants regularly submitting multiple amendments of the same transaction each day. Information in the SBS transaction reports does not indicate whether this difference may reflect actual variances in CDS and non-CDS new trade activity; inconsistencies in reporting practices across market participants, products, or scenarios; or a combination of factors.

To better understand these non-CDS amendment reports, staff discussed them with multiple market participants that had reported among the highest total notional amounts of amendments to trade terms of non-CDS transactions. The market participants with whom staff discussed these reports together accounted for approximately $2,699.9 trillion of the approximately $4,468.6 trillion in notional amount of non-CDS new trade activity representing events reported as amendments to trade terms consistent with a new or modified investment agreement or decision. Each of these market participants confirmed that their reported amendments accurately reflected bona fide changes to the non-CDS trade consistent with a new or modified investment agreement or decision between the counterparties. Moreover, even apart from events reported as amendments to trade terms, non-CDS events reported as new trades and early terminations consistent with a new or modified investment agreement or decision also far outpaced comparable CDS new trade activity and accounted for approximately $105.3 trillion and approximately $38.9 trillion, respectively, in notional amount of non-CDS new trade activity, compared to approximately $5.3 trillion and approximately $2.5 trillion, respectively, in notional amount of CDS new trade activity.

Staff thus estimates that trading activity in non-CDS was more significant compared to trading activity in CDS in 2024 than anticipated when the Commissions adopted the joint definitional rules. In addition, there may have been less notional amount of trading activity in CDS in 2024 than in 2011 based on comparison of 2011 and 2024 transaction data,[67]

while there may have been more notional amount of trading activity in non-CDS in 2024 than in 2011 based on comparison of the 2011 estimate to 2024 transaction data. Though each of these estimates is limited by the significant differences in the scope of data available in 2011 as compared to 2024 and by the 2024 data quality issues described below, the magnitude of the differences between 2024 CDS and non-CDS new trade activity suggests that non-CDS trading activity is much larger, both in absolute value and as compared to CDS trading activity, than the limited 2011 data could have predicted at the time the Commission adopted the de minimis thresholds.

ii. Estimates of Potential SBS Dealing Activity in 2024 and 2011

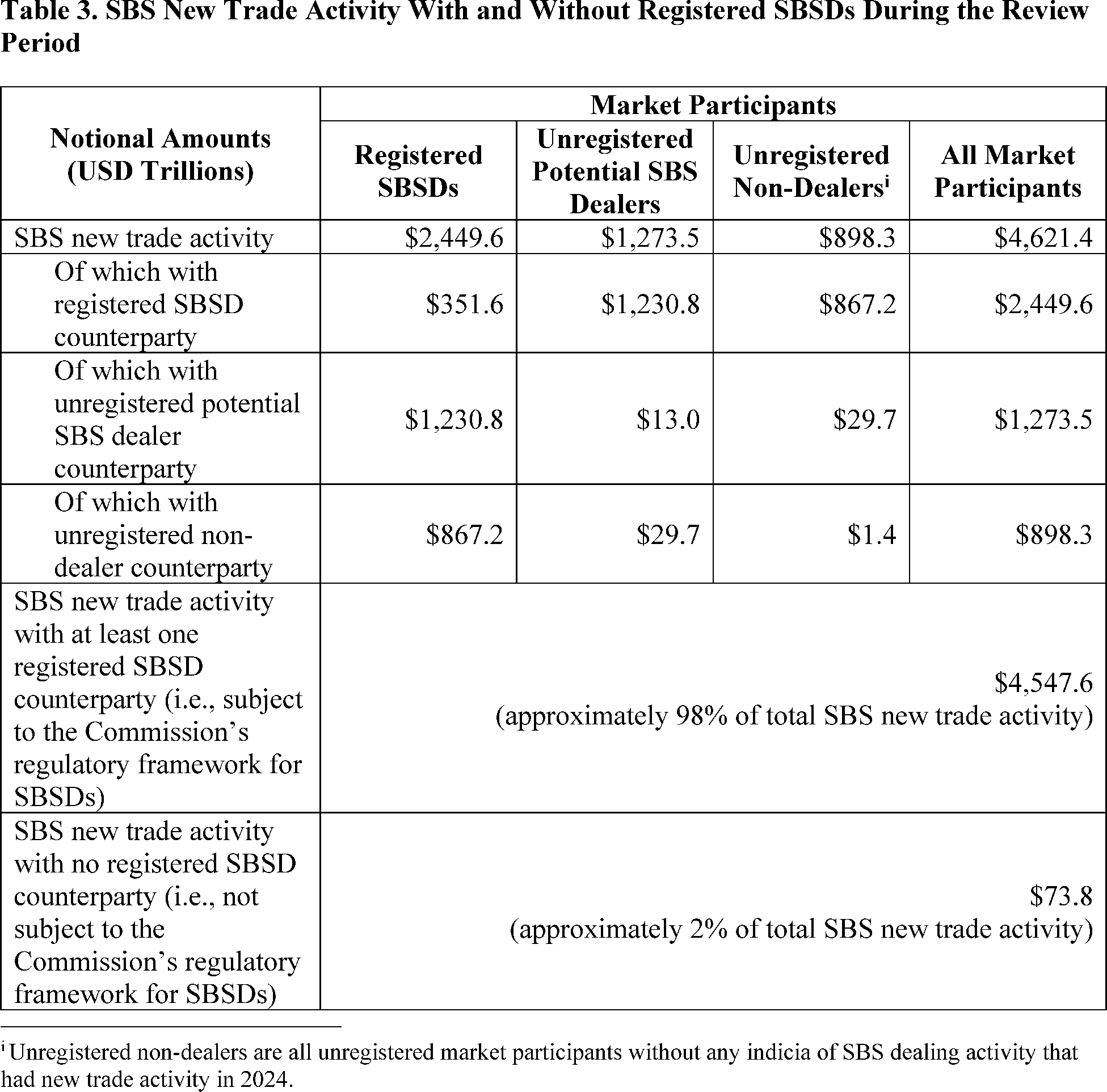

As shown in Table 3, the approximately $4,621.4 trillion in notional amount of 2024 SBS new trade activity included approximately $2,449.6 trillion in new trade activity attributed to 53 SBSDs registered with the Commission [68]

and thus subject to the Commission's regulatory framework for SBSDs. There was approximately $2,171.8 trillion [69]

in notional amount of new trade activity by unregistered market participants, including approximately $2,098.0 trillion [70]

in new trade activity with a registered SBSD. Accordingly, approximately 98% of all new trade activity events included at least one registered SBSD counterparty and thus was subject to the Commission's regulatory framework for SBSDs.

( printed page 24047)

The Commission's analysis of the 2011 trade activity of 1,084 participants in the single-name CDS market indicated a high degree of concentration among those apparently engaged in SBS dealing. From among those 1,084 market participants, 28, or approximately 3%, had three or more non-dealer counterparties; the Commission identified these 28 market participants as potential SBS dealers.[71]

In 2011, the 28 potential SBS dealers engaged in single-name CDS transactions with a total of $11.18 trillion in notional amount,[72]

or approximately 89%, out of a total of $12.6 trillion in aggregate gross notional amount of all single-name CDS transactions that the Commission reviewed.[73]

Similarly, based on available 2011 position data about other non-CDS types of SBS such as equity swaps, the Commission estimated that the 2011 non-CDS SBS markets also had a high degree of concentration among market participants apparently engaged in SBS dealing.[74]

De minimis thresholds of $8 billion [75]

and $3 billion [76]

for CDS that are SBS would have covered 99.9% and over 99.9%, respectively, of that $11.18 trillion, and would have required 23 and 25, respectively, of the 28 potential SBS dealers to register as SBSDs. The Commission expected the equity and other non-CDS SBS markets to be approximately 1/20th of the overall SBS market and set the permanent and phase-in

( printed page 24048)

de minimis thresholds at 1/20th of the CDS thresholds.[77]

Market data available today—including SBS transaction reports and third-party commercial sources—provides additional information about SBS market participants that the Commission did not have in 2012. SBS transaction reports in 2024 did not, however, include information about a market participant's engagement in the business of SBS dealing for a particular transaction or event. Though new trade activity events exclude activity particularly unlikely to be SBS dealing, they may still include non-dealing activity. A market participant's new trade activity thus may include SBS dealing transactions and/or non-dealing transactions. For purposes of this report, staff used the 2024 SBS transaction reports and third-party commercial sources [78]

to identify market participants with indicia of SBS dealing activity. Rather than limit indicia of SBS dealing activity to the number of counterparties with which a market participant transacted, staff used information about market participant characteristics, independent of the number or identity of counterparties, to identify market participants with indicia of SBS dealing. These uniform filtering criteria allowed staff to analyze a broader subset of market participants either known to be engaged or potentially engaged in SBS dealing in 2024 than was possible in 2011. Market participants with indicia of SBS dealing activity included both registered SBSDs and unregistered market participants, and staff refers to the latter as unregistered “potential SBS dealers.” Staff classified the new trade activity of registered SBSDs and unregistered potential SBS dealers (minus adjustments for activity that appeared to fit within exclusions from the de minimis counting requirements, as described below) as potential SBS dealing [79]

and thus counted that activity toward the de minimis thresholds.

As discussed above, using the 2011 single-name CDS transaction data, the Commission identified 28 potential dealers with three or more non-dealer counterparties. Based on the 2024 filtering criteria, among the 10,962 total SBS market participants with new trade activity events during the review period, 906 had indicia of SBS dealing, including 53 registered SBSDs and 853 unregistered potential SBS dealers. For broad comparison with the 2011 findings, staff reviewed the activity of these 906 market participants and found that during the review period 57 of them had three or more counterparties that were not among the 906 (that is, counterparties that were neither registered SBSDs nor unregistered potential SBS dealers).[80]

To ensure this report's broad coverage of potential SBS dealing activity, particularly by market participants who may be dealing under the de minimis thresholds, staff analyzed the activity of all 906 market participants identified as having indicia of SBS dealing.

Comparing the 2011 CDS transaction data and non-CDS estimates to 2024 CDS and non-CDS transaction data, both CDS and non-CDS SBS markets appeared to be somewhat less concentrated in 2024. In 2011, 28 of 1,084 single-name CDS market participants appeared to be engaged in SBS dealing, and these 28 potential SBS dealers accounted for approximately 89% of the aggregate gross notional amount of trading activity that the Commission reviewed. By contrast, the 53 registered SBSDs as of December 31, 2024, had approximately 53% and 853 unregistered potential SBS dealers had approximately 28% of all SBS new trade activity, for a total of approximately 81% of all SBS new trade activity in 2024. Similarly, in 2024 registered SBSDs had approximately 76% and unregistered potential SBS dealers had approximately 9% of CDS new trade activity, for a total of approximately 85% of all CDS new trade activity in 2024. Registered SBSDs had approximately 53% and unregistered potential SBS dealers had approximately 28% of non-CDS new trade activity, for a total of approximately 81% of all non-CDS new trade activity in 2024.

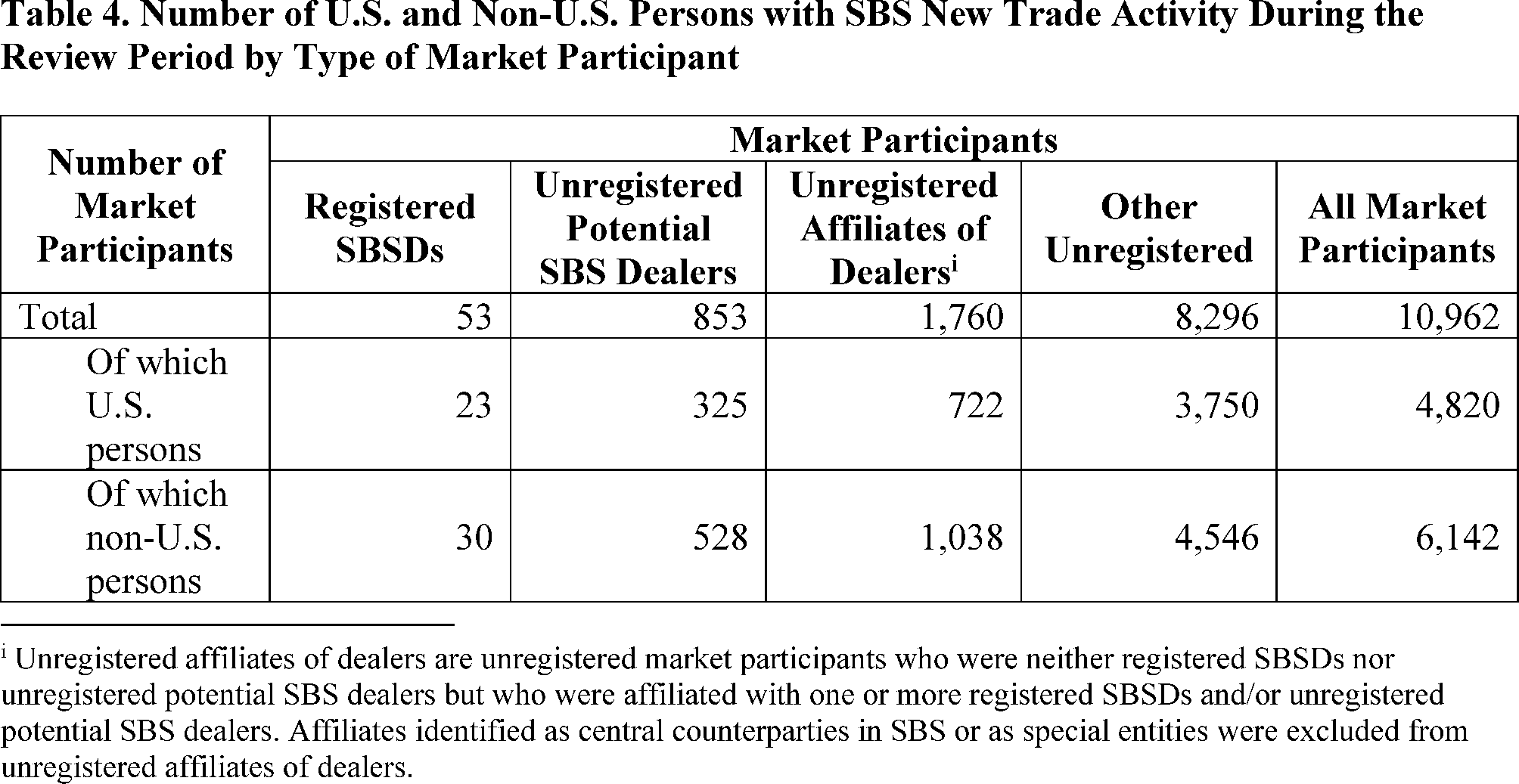

As shown in Table 4, SBS markets are cross-border, with a significant number of market participants that did not appear to be U.S. persons [81]

engaged in new trade activity during the 2024 review period. Among the 53 registered SBSDs on December 31, 2024, 23 appeared to be U.S. persons and 30 appeared to be non-U.S. persons.[82]

Among 853 unregistered potential SBS dealers, 325 appeared to be U.S. persons and 528 appeared to be non-U.S. persons. The 10,962 SBS market participants with new trade activity events during the review period also included 1,760 market participants who were neither registered SBSDs nor unregistered potential SBS dealers but who were affiliated with one or more registered SBSDs and/or unregistered potential SBS dealers (“unregistered affiliates of dealers”).[83]

Though staff did not classify unregistered affiliates of dealers as potential SBS dealers (unless an affiliate independently had indicia of SBS dealing), staff reviewed their activity separately from that of other unregistered market participants. These unregistered affiliates of dealers included 722 that appeared to be U.S. persons and 1,038 that appeared to be non-U.S. persons. Market participants that were not registered SBSDs, unregistered potential SBS dealers, or unregistered affiliates of dealers accounted for the remaining 8,296 market participants with new trade activity events during the review period and may have been end users and other investors.[84]

Among these 8,296 other unregistered market participants, 3,750 appeared to be U.S. persons and the remaining 4,546 appeared to be non-U.S. persons.

( printed page 24049)

To estimate potential SBS dealing activity, staff adjusted new trade activity of each of the 906 market participants with indicia of SBS dealing (

i.e.,

the 853 unregistered potential SBS dealers and the 53 registered SBSDs), consistent with the de minimis threshold counting requirements in Rule 3a71-3(b)(1). Starting with a market participant's new trade activity, staff subtracted any events where its counterparty was either the same person or an affiliate of the market participant on the date of the event, approximating the inter-affiliate exclusion from the de minimis counting requirements.[85]

For non-U.S.-person market participants only, staff further subtracted any events where the market participant's counterparty was also a non-U.S. person [86]

on the last day of the review period,[87]

and any events related to a transaction that was both traded on a platform and either actually or intended to be centrally cleared,[88]

approximating the additional exclusions from the de minimis counting requirements for non-U.S. persons. The result after these adjustments was the market participant's potential SBS dealing activity before aggregation with any potential SBS dealing activity of its affiliates.[89]

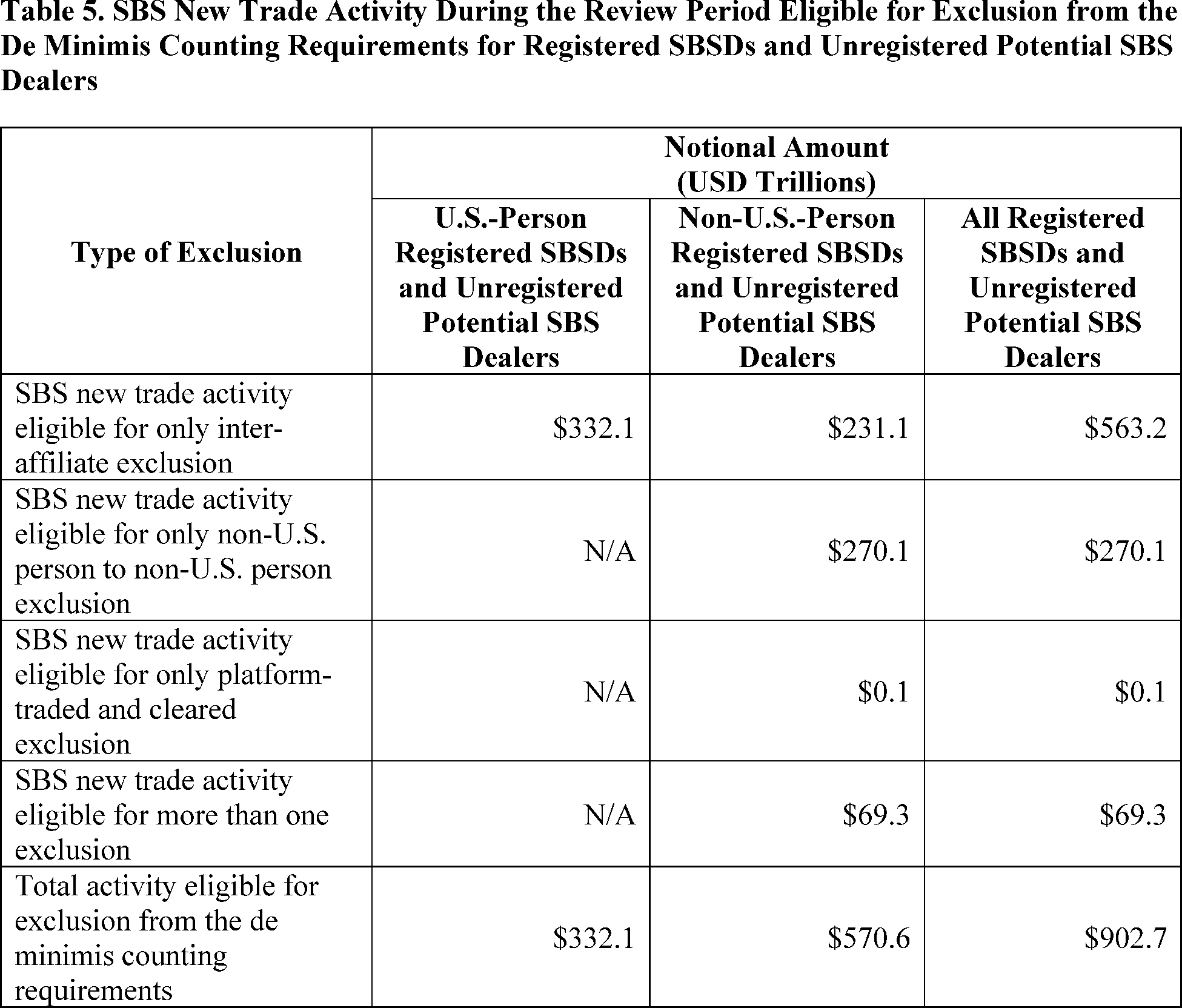

As shown in Table 5, the 23 U.S.-person registered SBSDs and 325 U.S.-person unregistered potential SBS dealers together had approximately $332.1 trillion in notional amount that appeared to be eligible for exclusion from the de minimis counting requirements. By comparison, the 30 non-U.S. person registered SBSDs and the 528 non-U.S.-person unregistered potential SBS dealers together had approximately $570.6 trillion in notional amount that appeared to be eligible for exclusion from the de minimis counting requirements. Some new trade activity events of these non-U.S. persons appeared to be eligible for more than one exclusion from these counting requirements. Of the approximately $570.6 trillion in notional amount of these market participants' new trade activity eligible for exclusion, approximately $69.3 trillion in notional amount appeared to be eligible for more than one exclusion.

( printed page 24050)

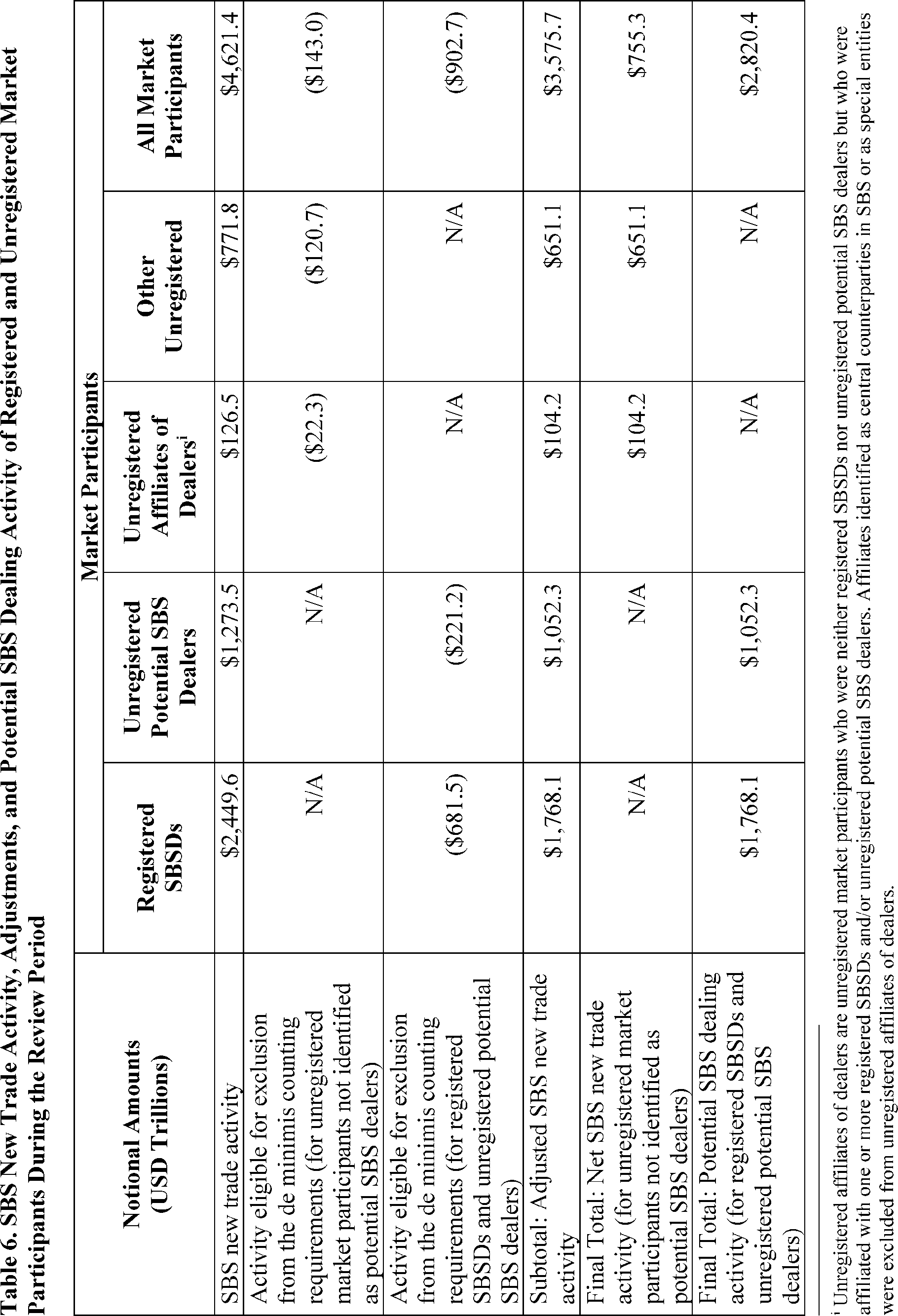

To aid comparison across all market participants, staff also adjusted the new trade activity of market participants that did not appear to be engaged in SBS dealing to exclude activity that appeared to be eligible for exclusion from the de minimis counting requirements. As shown in Table 6, after excluding $1,045.7 trillion [90]

in notional amount from new trade activity, all SBS market participants had $3,575.7 trillion in adjusted new trade activity during the review period that counted toward the de minimis thresholds. Approximately 49% of that adjusted new trade activity, or approximately $1,768.1 trillion, belonged to registered SBSDs and thus appeared to be SBS dealing activity. Of the approximately $1,807.6 trillion [91]

of adjusted new trade activity belonging to unregistered market participants during the review period, approximately $1,052.3 trillion belonged to unregistered potential SBS dealers and appeared to be SBS dealing activity. The remaining approximately $755.3 trillion [92]

belonged to market participants that did not appear to be engaged in SBS dealing and thus may have been non-dealing activity by end users and other investors. All potential SBS dealing activity during the review period totaled

( printed page 24051)

$2,820.4 trillion in notional amount. Registered SBSDs accounted for approximately 63% of this potential SBS dealing activity, while unregistered potential SBS dealers accounted for approximately 37%.

( printed page 24052)

The de minimis counting requirements also direct any person that engages in its own SBS dealing activity to count toward the de minimis thresholds certain SBS dealing

( printed page 24053)

activity of the person's control affiliates.[93]

For market participants identified as registered SBSDs or unregistered potential SBS dealers, staff estimated aggregate SBS dealing activity of that market participant and any of its affiliates that were also identified as registered SBSDs or unregistered potential SBS dealers. Staff used this estimate of aggregate SBS dealing activity to compare each of these market participants' progress toward the de minimis thresholds.

b. CDS De Minimis Threshold

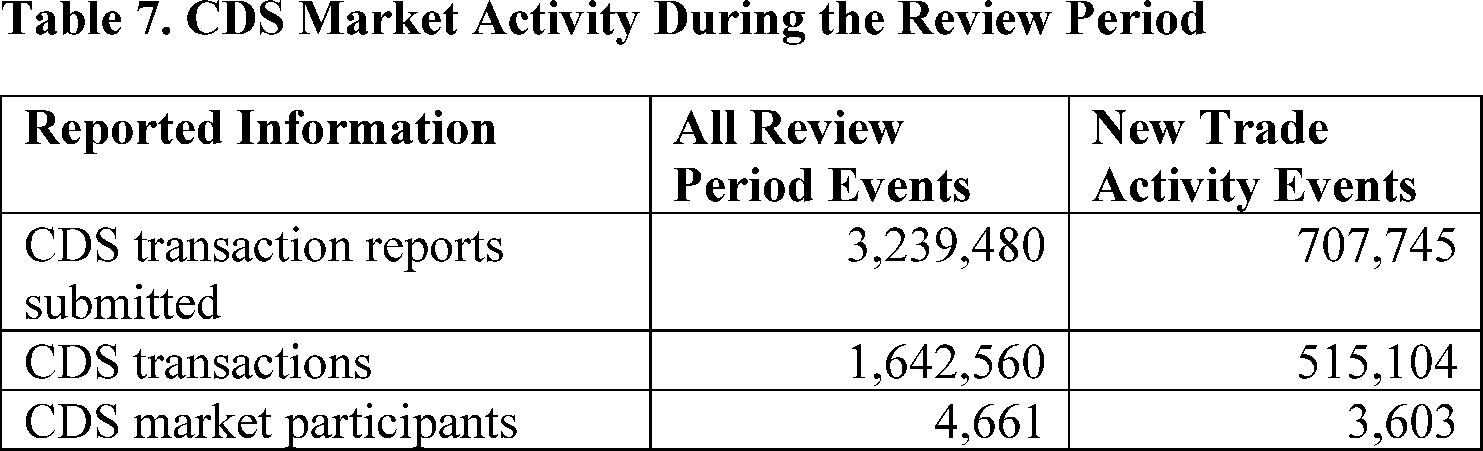

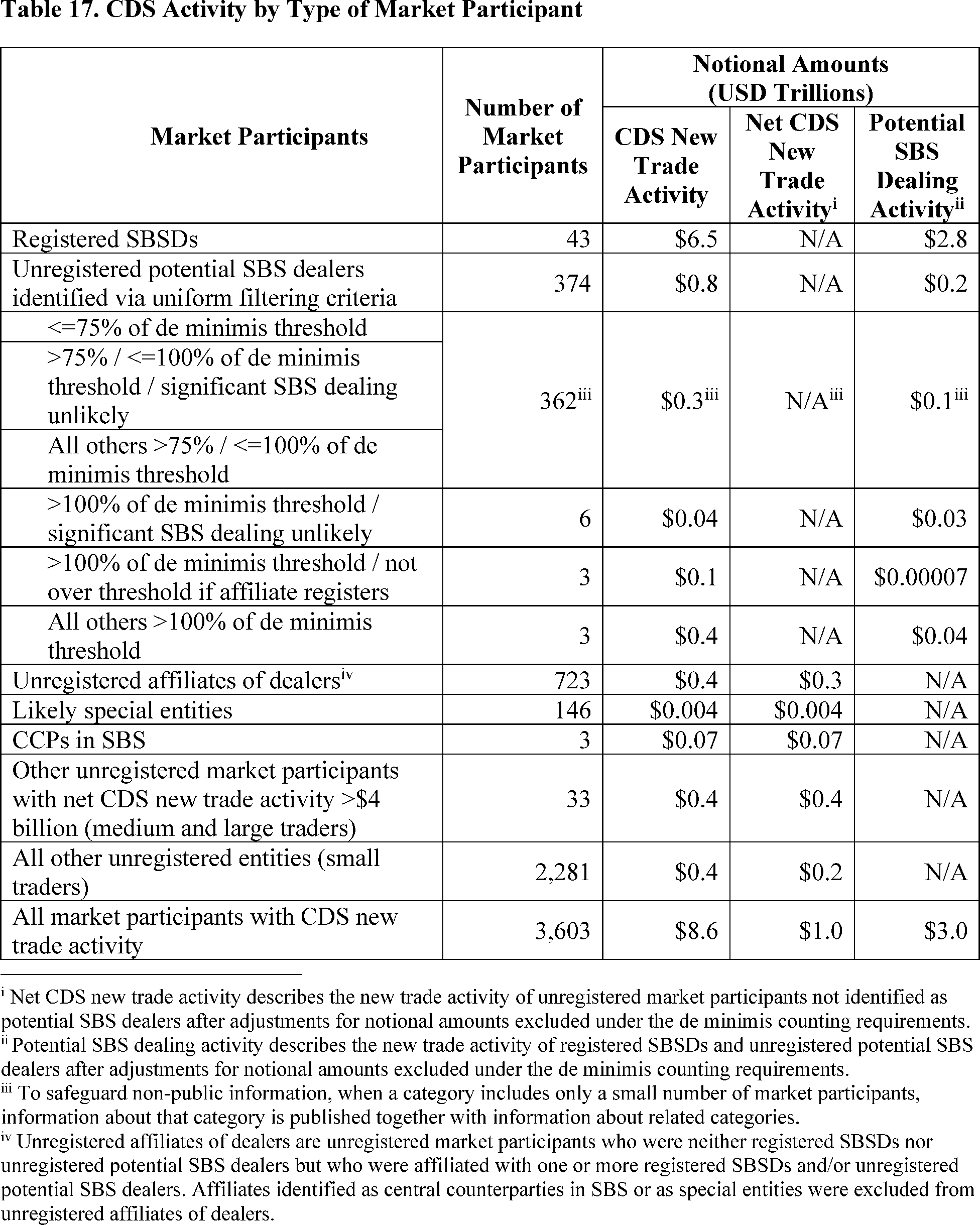

As shown in Table 7, market participants submitted to SBSDRs before the cut-off date SBS transaction reports on 707,745 unique new trade activity events related to 515,104 unique CDS transactions involving 3,603 unique CDS market participants.[94]

Staff evaluated the impact of the current $8 billion and scheduled $3 billion CDS de minimis thresholds on market participants' CDS new trade activity and potential SBS dealing activity in CDS and also assessed hypothetical alternative de minimis thresholds in the amounts of $1 billion, $5 billion, and $15 billion.[95]

Analysis of SBS transaction reports revealed that market participants are using the exclusions from the definition of “security-based swap dealer” and that, at the current $8 billion de minimis threshold, 43 market participants registered as SBSDs on the measurement date were on at least one side of 99% of CDS new trade activity in 2024. A lower de minimis threshold of $1 billion, $3 billion, or $5 billion could add additional registered SBSDs, while a higher $15 billion de minimis threshold may create eligibility for some currently registered SBSDs to de-register.

i. CDS Market Participants' Activity

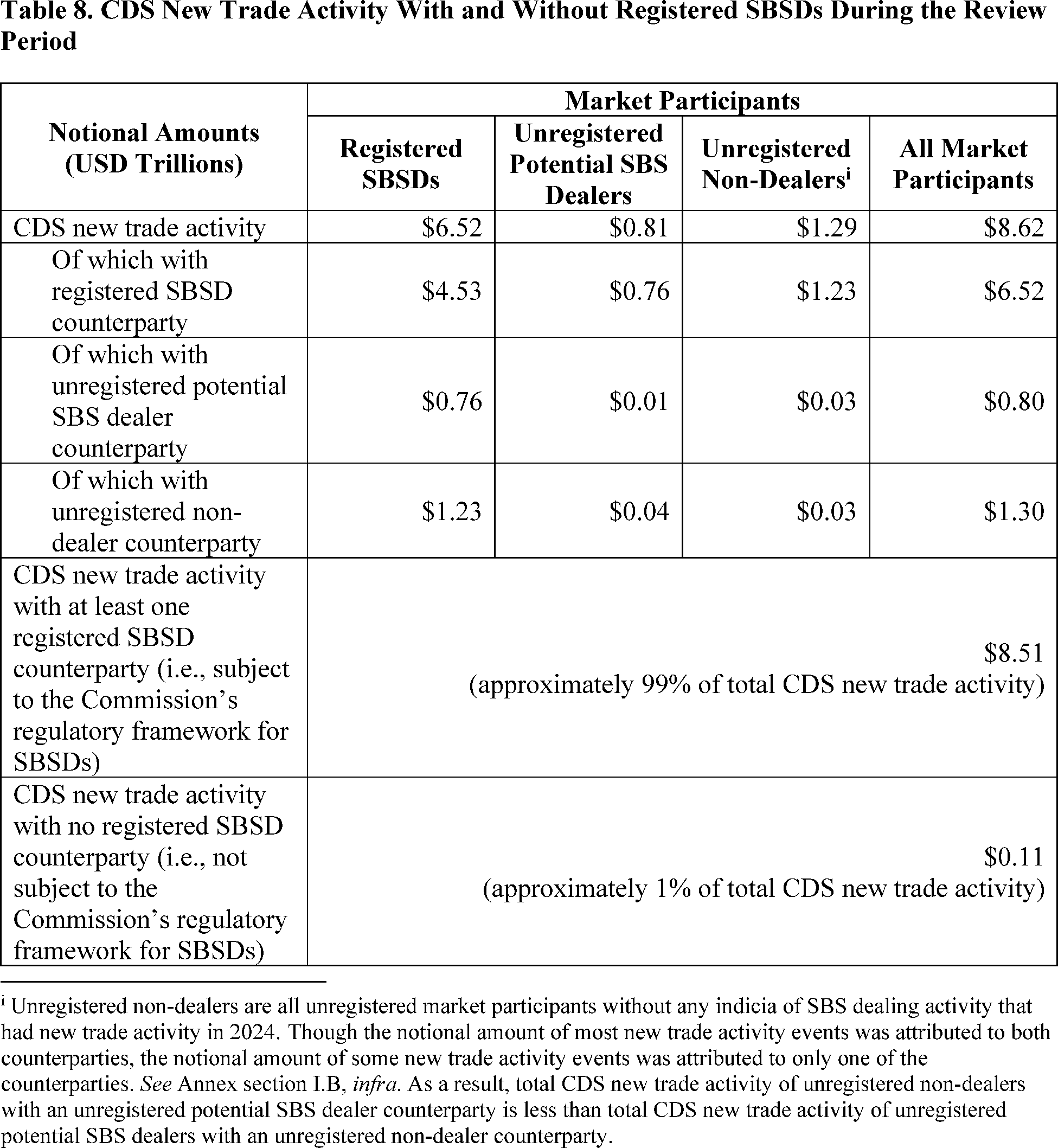

There was approximately $4.3 trillion in total notional amount of CDS new trade activity events during the review period. This total reflects the transacted notional amounts of the reported CDS new trade activity events, providing a snapshot of the volume of new trade activity transactions in the CDS market at large. After attributing the notional amounts of these CDS new trade activity events to market participants to measure their progress toward the de minimis thresholds, the total notional amount of CDS new trade activity during the review period was approximately $8.6 trillion.

As shown in Table 8, this $8.6 trillion included approximately $6.5 trillion in notional amount of CDS new trade activity by 43 registered SBSDs and thus was subject to the Commission's regulatory framework for SBSDs. There was approximately $2.1 trillion [96]

in notional amount of CDS new trade activity by unregistered market participants, including approximately $2 trillion [97]

of CDS new trade activity with a registered SBSD and approximately $115 billion [98]

of CDS new trade activity with another unregistered market participant. Accordingly, approximately 99% of CDS new trade activity events included at least one registered SBSD counterparty and thus was subject to the Commission's regulatory framework for SBSDs.

( printed page 24054)

ii. Impact of Exclusions on CDS Activity

Staff adjusted CDS new trade activity to remove activity that appeared to be eligible for an exclusion from the de minimis counting requirements.[99]

As shown in Table 9, of the approximately $8.6 trillion in notional amount of CDS new trade activity during the review period, approximately $4.6 trillion [100]

represented activity that appeared to be eligible for exclusion from the de minimis counting requirements.[101]

This excluded activity accounted for a higher proportion of CDS new trade activity of unregistered potential SBS dealers than of

( printed page 24055)

other market participants. Unregistered potential SBS dealers had approximately $619 billion in notional amount of excluded activity, or 77% of their approximately $809 billion total notional amount of CDS new trade activity. Meanwhile, approximately 57% of registered SBSDs' CDS new trade activity and 26% of all other unregistered market participants' CDS new trade activity was excluded. These results suggest that the exclusions from the definition of “security-based swap dealer” had a significant impact on CDS market participants' need to register or remain registered as SBSDs with the Commission during the review period.

After subtracting activity that appeared to be eligible for exclusion from the de minimis counting requirements, approximately $4 trillion in notional amount remained as adjusted CDS new trade activity during the review period, as shown in Table 9. Nearly three-quarters of this adjusted CDS new trade activity, or approximately $2.8 trillion, belonged to registered SBSDs and thus appeared to be SBS dealing activity. Of the approximately $1.2 trillion [102]

in notional amount of adjusted CDS new trade activity belonging to unregistered market participants, approximately $1 trillion [103]

belonged to market participants that did not appear to be engaged in SBS dealing and thus may have been non-dealing trading activity by end users and other investors. Unregistered potential SBS dealers had the remaining $190 billion, and this amount appeared to be SBS dealing activity. Registered SBSDs thus accounted for approximately 94%, or approximately $2.8 trillion, of the approximately $3 trillion total potential SBS dealing activity in CDS during the review period, while unregistered potential SBS dealers accounted for approximately 6%, or approximately $190 billion, of that total.

( printed page 24056)

( printed page 24057)

iii. $8 Billion Phase-In CDS De Minimis Threshold

Forty-three out of a total of 53 registered SBSDs had CDS new trade activity during the review period, meaning ten registered SBSDs did not have any CDS new trade activity during the review period. Twenty-seven of these 43 registered SBSDs had potential SBS dealing activity in CDS above the $8 billion de minimis threshold, while the remaining sixteen of these 43 registered SBSDs had potential SBS dealing activity in CDS at or below $8 billion. However, all 16 of these registered SBSDs had potential SBS dealing activity in non-CDS and/or SBS with counterparties likely to be special entities that surpassed one or both of the other de minimis thresholds for those transactions.

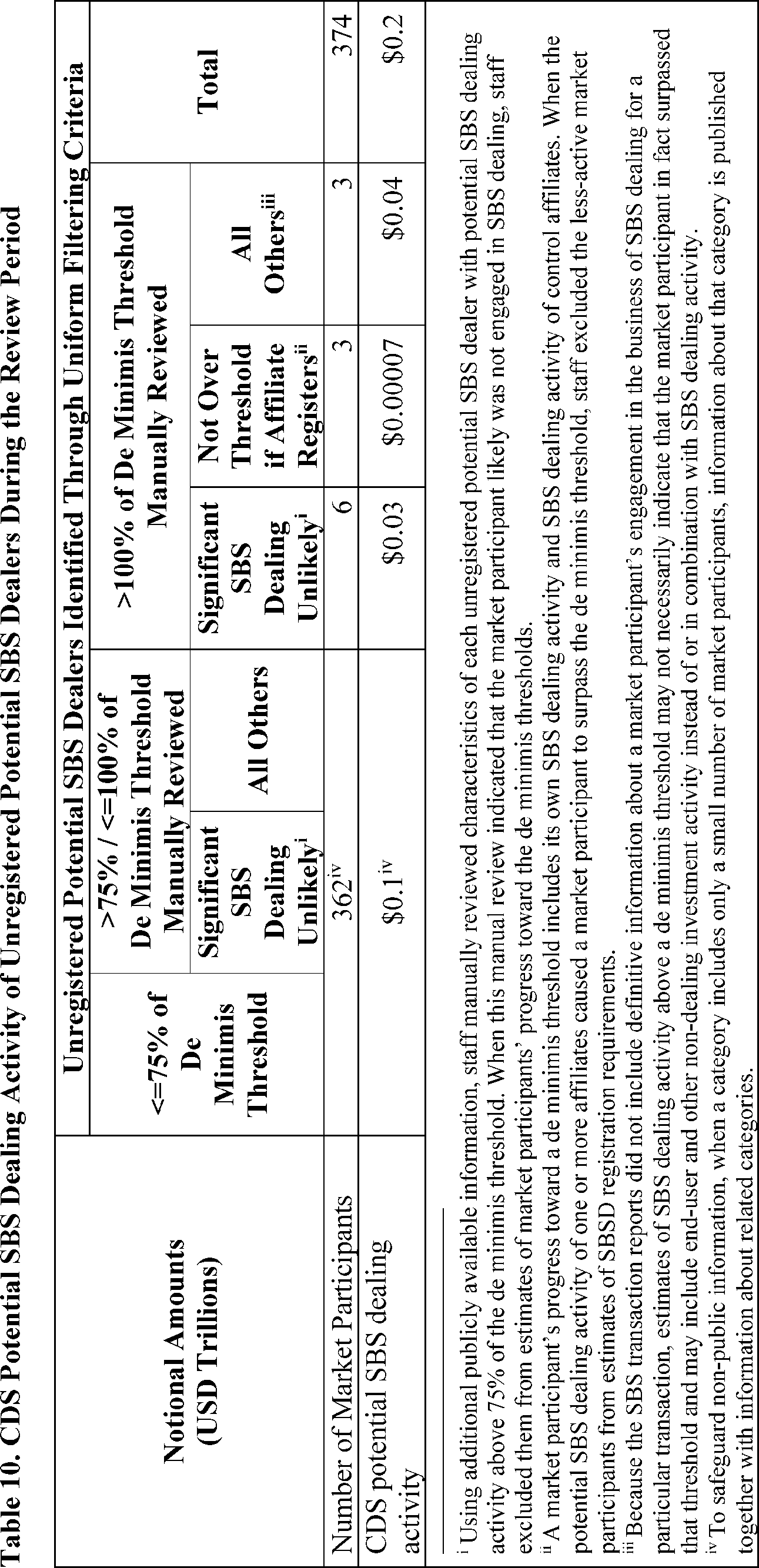

Among the 853 unregistered potential SBS dealers identified through staff's uniform filtering criteria, 374 [104]

of them, who together were members of 279 groups of one or more affiliated market participants, had CDS new trade activity and together had approximately $190 billion in potential SBS dealing activity in CDS. As shown in Table 10, twelve of these 374 unregistered potential SBS dealers initially appeared to have potential SBS dealing activity above the $8 billion threshold. Of these twelve, six were market participants that staff excluded after manual review of additional publicly available information suggested they were unlikely to be engaged in significant SBS dealing, three were market participants that would not have been required to register as SBSDs if an affiliate had done so,[105]

and three were market participants that may have been required to register as SBSDs. The six manually excluded market participants accounted for approximately $33.5 billion of the total approximately $190 billion in notional amount of potential SBS dealing in CDS by unregistered potential SBS dealers. Because the SBS transaction reports did not include sufficient information to support transaction-level estimates of SBS dealing activity, staff could estimate that these six market participants were unlikely to be engaged in significant SBS dealing activity but could not estimate the notional amount of SBS dealing activity, if any, in which they may have engaged alongside non-dealing activity. The three market participants that would not have been required to register as SBSDs if an affiliate had done so accounted for approximately $65 million in notional amount of potential SBS dealing activity in CDS. Finally, the remaining three market participants that did not meet any of these exclusion criteria had a total of approximately $39.0 billion in notional amount of potential SBS dealing activity in CDS.

Because the SBS transaction reports did not include definitive information about a market participant's engagement in the business of SBS dealing for a particular transaction, estimates of SBS dealing activity above a de minimis threshold may not necessarily indicate that a market participant in fact surpassed that threshold and indeed may include end-user and other non-dealing investment activity. In particular, as the criteria for indicia of potential SBS dealing activity could be applied only at the counterparty level and not at the level of individual transactions or events, all of these three unregistered potential SBS dealers' new trade activity net of exclusions, plus that of affiliates estimated to be engaged in SBS dealing, counted as progress toward de minimis threshold. These market participants' activity may in fact be exclusively SBS dealing activity, exclusively non-dealing activity, or a combination of the two, but the SBS transaction reports did not include sufficient information to support more granular estimates. If these three unregistered potential SBS dealers did surpass the $8 billion de minimis threshold, they would have been required to register as SBSDs or shift SBS dealing to a control affiliate [106]

that is a registered SBSD. If the three had been registered as SBSDs during the review period, all CDS new trade activity subject to the Commission's regulatory framework for SBSDs (that is, all CDS new trade activity with at least one registered SBSD counterparty) would have increased by approximately $65.6 billion, to $8,567.1 billion, and CDS new trade activity outside of that regulatory framework (that is, all CDS new trade activity with no registered SBSD) would have decreased by the same amount, to $49.4 billion.

A small number of unregistered potential SBS dealers appeared to have progressed more than 75% (more than $6 billion) toward the $8 billion threshold while remaining below that threshold. The remaining unregistered potential SBS dealers had potential SBS dealing activity at or below 75% of the $8 billion de minimis threshold.

( printed page 24058)

( printed page 24059)

These results suggest that a small but significant minority [107]

of unregistered CDS market participants may have engaged in SBS dealing activity and thus relied on the de minimis exception to the definition of “security-based swap dealer.” The vast majority, though possibly not all, of those market participants appeared to have kept their SBS dealing below the de minimis threshold, though the data do not contain information about market participants' intent in this regard.[108]

A significant portion of registered SBSDs did not participate in the CDS markets during the review period, but those that did together were counterparties to approximately 99% of CDS new trade activity.

iv. $3 Billion Scheduled CDS De Minimis Threshold

Among the 16 registered SBSDs with potential SBS dealing activity in CDS at or below the current $8 billion de minimis threshold, three surpassed the scheduled $3 billion de minimis threshold. These three registered SBSDs thus may have lost any eligibility to de-register if a $3 billion threshold had applied during the review period. The remaining 13 of those 16 registered SBSDs had potential SBS dealing activity in CDS at or below $3 billion. An additional 10 registered SBSDs did not have any CDS new trade activity during the review period. Each of these 13 registered SBSDs, as well as the 10 registered SBSDs with no CDS new trade activity during the review period, may already have been eligible to de-register on the measurement date under the current $8 billion threshold, provided that their aggregate SBS dealing activity also fell below the other applicable de minimis thresholds. Based on their estimated potential SBS dealing activity, any of these 23 registered SBSDs that were eligible to de-register under an $8 billion threshold also would have been eligible to de-register under a $3 billion threshold. None of these registered SBSDs, however, did de-register on or after the measurement date, even with a higher $8 billion threshold. Though the scheduled $3 billion de minimis threshold would not be expected to create eligibility for any registered SBSDs to de-register, the lower threshold would leave less room for de minimis SBS dealing activity and thus may make it less likely that these registered SBSDs choose to de-register.

Fifteen unregistered potential SBS dealers initially appeared to have more than $3 billion but not more than $8 billion in potential SBS dealing activity in CDS. Of those 15 unregistered potential SBS dealers, nine were market participants that staff excluded after manual review of additional publicly available information suggested they were unlikely to be engaged in significant SBS dealing, two were market participants that would not have surpassed a $3 billion de minimis threshold if an affiliate had registered as an SBSD,[109]

and four were market participants that may have been required to register as SBSDs if a $3 billion de minimis threshold had applied during the review period. The nine manually excluded market participants accounted for approximately $33 billion of the total approximately $190 billion in notional amount of potential SBS dealing in CDS by unregistered potential SBS dealers. Because the SBS transaction reports did not include sufficient information to support transaction-level estimates of SBS dealing activity, staff could estimate that these nine market participants were unlikely to be engaged in significant SBS dealing activity but could not estimate the notional amount of SBS dealing activity, if any, in which they may have engaged. The two market participants that would not have surpassed a $3 billion de minimis threshold if an affiliate had registered as an SBSD accounted for approximately $34 million in notional amount of potential SBS dealing activity in CDS. Finally, the remaining four market participants that did not meet any of these exclusion criteria had a total of approximately $19.3 billion in notional amount of potential SBS dealing activity in CDS.