The Securities and Exchange Commission ("Commission") is proposing amendments to allow companies to file semiannual reports on new Form 10-S in lieu of quarterly reports on Form...

The Securities and Exchange Commission (“Commission”) is proposing amendments to allow companies to file semiannual reports on new Form 10-S in lieu of quarterly reports on Form 10-Q to meet their interim reporting obligations under the Securities Exchange Act of 1934 (“Exchange Act”). The Commission is also proposing changes to the financial statement requirements of Regulation S-X to facilitate semiannual reporting and to simplify rules regarding the age of financial statements.

DATES:

Comments should be received on or before July 6, 2026.

ADDRESSES:

Comments may be submitted by any of the following methods:

Send an email torule-comment@sec.gov.

Please include File Number S7-2026-15 on the subject line.

Paper Comments

Send paper comments to Vanessa A. Countryman, Secretary, Securities and Exchange Commission, 100 F Street NE, Washington, DC 20549-1090.

All submissions should refer to File Number S7-2026-15. This file number should be included on the subject line if email is used. To help the Commission process and review your comments more efficiently, please use only one method of submission. The Commission will post all comments on the Commission's website

https://www.sec.gov/comments/s7-2026-15/semiannual-reporting#no-back.

Do not include personally identifiable information in submissions; you should submit only information that you wish to make available publicly. The Commission may redact in part or withhold entirely from publication submitted material that is obscene or subject to copyright protection.

Studies, memoranda, or other substantive items may be added by the Commission or staff to the comment file during this rulemaking. A notification of the inclusion in the comment file of any such materials will be made available on the Commission's website. To ensure direct electronic receipt of such notifications, sign up through the “Stay Connected” option at

www.sec.gov

to receive notifications by email.

Mark Saltzburg, Senior Special Counsel, Office of Rulemaking, Division of Corporation Finance, at (202) 551-3430, or Ryan Milne, Associate Chief Accountant, Office of Chief Accountant, Division of Corporation Finance, at (202) 551-3400, U.S. Securities and Exchange Commission, 100 F Street NE, Washington, DC 20549.

SUPPLEMENTARY INFORMATION:

The Commission is proposing to amend or add the following rules and forms:

( printed page 24969)

( printed page 24970)

Table of Contents

I. Introduction

II. Background

III. Discussion of Proposed Amendments

A. Proposed Amendments for Semiannual Reporting

B. Proposed Amendments to Regulation S-X

C. Proposed Amendments Regarding Transition Reports

D. Proposed Technical Amendments

E. General Request for Comment

IV. Other Matters

V. Economic Analysis

A. Introduction

B. Broad Economic Considerations

C. Baseline

D. Benefits and Costs

E. Anticipated Effects on Efficiency, Competition, and Capital Formation

F. Reasonable Alternatives

G. Request for Comment

VI. Paperwork Reduction Act Analysis

A. Summary of the Collections of Information

B. Estimated Paperwork Burden Effects of the Proposed Amendments

C. Incremental and Aggregate Burden and Cost Estimates

D. Request for Comment

VII. Congressional Review Act

VIII. Initial Regulatory Flexibility Act Analysis

A. Reasons for, and Objectives of, the Proposed Action

B. Legal Basis

C. Small Entities Subject to the Proposed Rules and Amendments

D. Reporting, Recordkeeping, and Other Compliance Requirements

E. Duplicative, Overlapping or Conflicting Federal Rules

F. Significant Alternatives

G. Request for Comment

Statutory Authority

I. Introduction

We are proposing amendments to provide all companies subject to reporting obligations under Exchange Act Section 13(a) or 15(d) (“Exchange Act reporting companies”) [4]

that file

( printed page 24971)

quarterly reports the option of filing interim reports on a semiannual basis. Currently, Exchange Act reporting companies must file quarterly reports on Form 10-Q pursuant to 17 CFR 240.13a-13 (“Exchange Act Rule 13a-13”) or 17 CFR 240.15d-13 (“Exchange Act Rule 15d-13”), with certain exceptions.[5]

Pursuant to these rules, Exchange Act reporting companies file with the Commission three quarterly reports on Form 10-Q each fiscal year, with the fourth fiscal quarter subsumed within the reporting company's annual report on Form 10-K. The proposed amendments to Exchange Act Rules 13a-13 and 15d-13, if adopted, would allow Exchange Act reporting companies electing to do so to file semiannual reports on new Form 10-S in lieu of quarterly reports on Form 10-Q. Our proposal would provide an Exchange Act reporting company with the flexibility to determine the frequency of interim reporting that best suits its particular circumstances, such as its ability to bear the costs of preparing the quarterly reports, the stage of its business development, and the expectations of its investors, without undermining fundamental investor protections. Providing such regulatory flexibility could reduce the regulatory burden of being a reporting company, which could potentially influence a company's decision to become or remain a reporting company and encourage more companies to go or remain public. These proposed amendments would not substantively affect investment companies except for business development companies and face-amount certificate companies.[6]

We are also proposing amendments to the financial statement requirements of 17 CFR part 210 (“Regulation S-X”)—including to 17 CFR 210.3-01 (“Rule 3-01”), 17 CFR 210.3-12 (“Rule 3-12”), and 17 CFR 210.8-08 (“Rule 8-08”)—to facilitate semiannual reporting and to simplify rules regarding the age of financial statements in registration statements and other Commission filings.

II. Background

Companies subject to Exchange Act Sections 13(a) and 15(d) must file periodic and other reports as prescribed in Commission rules. Exchange Act reporting companies have been required to file annual reports on Form 10-K since 1935 [7]

as well as current reports on Form 8-K for certain material events since 1936.[8]

In 1946, the Commission required certain reporting companies to file quarterly reports on Form 8-K to disclose, among other things, the dollar amount of gross sales (less discounts, returns, and allowances) and operating revenue.[9]

In 1953, the Commission ended this quarterly reporting requirement,[10]

and, in 1955, it adopted rules requiring semiannual interim reports pursuant to Rules X-13A-13 and X-15D-13.[11]

These rules required one semiannual report to be filed each fiscal year by Exchange Act reporting companies on a new Form 9-K.[12]

Semiannual reports on Form 9-K, which were due 45 days after the end of the reporting period, did not require the narrative disclosures mandated by Form 10-Q and provided only limited disclosures typically associated with an income statement.[13]

After 15 years of this semiannual reporting system, the Commission rescinded semiannual reports on Form 9-K in 1970 and instead required quarterly reporting pursuant to amended Rules 13a-13 and 15d-13.[14]

The rules required Exchange Act reporting companies to file three quarterly reports on Form 10-Q each fiscal year.[15]

When it proposed the quarterly report on Form 10-Q, the Commission explained that the new report would “provide detailed information as a back-up to information released pursuant to timely disclosure policies” and would provide “uniform standards” for all Exchange Act reporting companies.[16]

The Commission's move towards a quarterly reporting requirement was also consistent with the recommendation of the 1969 Wheat Report, which

( printed page 24972)

concluded “that a regular, quarterly report would be more useful than the present, irregular 8-K report.” [17]

Although the Commission has amended Form 10-Q and requirements in connection with quarterly reporting over time,[18]

the Commission has not changed this cadence of quarterly interim reporting since it was adopted in 1970.

Form 10-Q today requires more detailed information than the rescinded semiannual report on Form 9-K. Form 10-Q requires financial statements (inclusive of footnote disclosures) for the covered quarterly period that are prepared in accordance with United States (“U.S.”) generally accepted accounting principles (“U.S. GAAP”),[19]

have been reviewed by an independent public accountant (but are not required to be audited),[20]

and are data tagged using inline XBRL.[21]

It also requires narrative disclosures regarding:

Management's discussion and analysis of financial condition and results of operations (“MD&A”); [22]

Material changes to the procedures by which security holders may recommend nominees to the registrant's board of directors; [29]

Disclosure of director or officer adoptions or terminations of certain plans for the purchase or sale of registrant securities; [30]

Exhibits required under Item 601 of Regulation S-K; [31]

and

Certifications by the principal executive and financial officers as exhibits.[32]

Form 10-Q reports are filed electronically with the Commission through its EDGAR system. The deadline for filing Form 10-Q with the Commission is 40 or 45 days after the end of a fiscal quarter, depending on the filer status of the reporting company.[33]

Finally, securities exchange listing standards generally do not mandate a particular frequency of interim reporting. Instead, they refer generally to compliance with Commission rules requiring interim reports (with at least one exchange making specific reference to quarterly reports on Form 10-Q),[34]

require availability of interim reports,[35]

or require quick dissemination of quarterly earnings information to the market.[36]

Certain companies that are not subject to Section 13(a) or Section 15(d) already report on a semiannual basis under the Commission's rules,[37]

and certain other

( printed page 24973)

companies are exempt from quarterly reporting but furnish semiannual information pursuant to other requirements such as exchange listing standards.[38]

Several foreign jurisdictions also require semiannual reporting of financial information (but not quarterly reporting).[39]

Over the years, the Commission at times has reassessed the current periodic reporting system, its impact on Exchange Act reporting companies, and potential alternatives including semiannual reporting. Most recently, as part of the Commission's disclosure effectiveness review, the Commission issued two releases that addressed and requested public comment on the frequency of interim reporting.[40]

In July 2019, the Commission also held a roundtable that discussed issues including the frequency of periodic reporting.[41]

The Commission received significant public feedback as a result of these recent efforts, including from companies and their representative organizations, asset managers and institutional investors, investor groups and individual investors, accounting firms, law firms, and other market participants.[42]

Commenters expressed a wide variety of views about the frequency of interim reporting requirements,[43]

with some supporting the current frequency but others recommending less-frequent interim reporting, such as semiannual reports, due to concerns about compliance costs and short-termism.[44]

Finally, the concept of semiannual reporting was recently discussed at: a meeting of the Commission's Investor Advisory Committee; [45]

the Commission's

45th Annual Small Business Forum

(and the prior year's forum); [46]

and the Commission's 2025

Small Cap Policy Roundtable.[47]

III. Discussion of Proposed Amendments

Interim reports provide investors with material information about the financial performance of their companies during a fiscal year. Yet quarterly reporting may not be the ideal interim reporting frequency for every Exchange Act reporting company, given the varied circumstances each company faces. We are proposing rule and form amendments to provide all Exchange Act reporting companies with the

( printed page 24974)

option of filing semiannual reports on new Form 10-S in lieu of quarterly reports on Form 10-Q. The flexibility provided under our proposed amendments would enable all Exchange Act reporting companies to choose the reporting frequency that would best serve the company and its investors. Companies that elect semiannual interim reporting may see a reduction in compliance costs of time and money, as they would incur these interim reporting costs only one time in connection with each fiscal year instead of three times in connection with each fiscal year pursuant to quarterly reporting.[48]

These companies could then choose to dedicate any compliance cost and resource savings to their business growth. Other potential benefits of semiannual reporting include: less distraction from running the day-to-day business; reallocation of attention from interim reporting to company strategy; additional time spent on new product development; and ability to engage in transactions that might not be possible when management is focused on preparing interim reports.[49]

To the extent that companies could not previously do so due to quarterly reporting, companies electing semiannual reporting may employ business strategies that may help ensure these companies' long-term viability. In particular, emerging growth companies [50]

and smaller reporting companies [51]

may value having the flexibility to select the interim reporting requirement that is most appropriate for them and their investors.[52]

Additionally, reducing the compliance costs associated with quarterly reporting may contribute to more private companies deciding to enter the public markets and more companies deciding to remain public. Further, the flexibility provided in the proposal may appeal to companies in certain industries where investors may focus more on certain business, product, or regulatory developments than interim financial results.[53]

Under the proposal, companies would have the option to elect on an annual basis to comply with the semiannual reporting requirements. Exchange Act reporting companies could continue to file quarterly reports on Form 10-Q under the proposal. Companies might continue to report quarterly, for example, where they determine that quarterly frequency is best for the company and its investors or due to factors such as expectations of investors and securities analysts, disclosure practices in a particular industry, contractual obligations, or other regulatory requirements.[54]

It is also possible some companies may view semiannual reporting as increasing the length of time that the company's directors or employees possess non-public information that may be subject to the company's closed trading windows and see quarterly reporting as a better approach for the company, because it may provide more frequent open trading windows for the company's directors and employees.

Although one result of the proposal will be a reduction in the frequency of interim reports for some Exchange Act reporting companies, we expect certain material information about these companies between interim semiannual reports and annual reports will continue to be disclosed either voluntarily or as a result of other requirements. Significant regulatory enhancements have occurred since 1970 with regard to disclosure of certain material events during interim periods. Investors currently have access to information through the current reporting system on Form 8-K regarding certain material events that is far more robust and timely than in 1970 when semiannual reports on Form 9-K were last required. Since that time, the Commission significantly accelerated that era's Form 8-K filing deadline of 10 days after the end of the month in which the applicable event occurred to the current general deadline of within four business days of the event.[55]

In addition to shortening the filing deadlines, the Commission over time significantly expanded the list of events that would trigger a filing obligation under Form 8-K and prescribed standardized disclosures that must be provided upon the occurrence of the material event, including through amendments in 2003 and 2004.[56]

In fact, several of the Form 10-Q disclosure requirements largely duplicate the Form 8-K requirements.[57]

Importantly, in 2003, the Commission added Item 2.02 as a Form 8-K filing trigger event for the furnishing of earnings releases and other material information about companies'

( printed page 24975)

results of operations and financial condition for a completed interim period.[58]

Current Item 2.02 requires reporting companies generally to furnish their quarterly earnings releases as an exhibit to Form 8-K on the Commission's EDGAR system.[59]

Many Exchange Act reporting companies hold a conference call in connection with their earnings releases. Item 2.02 provides the conference call does not need to be furnished with Form 8-K subject to certain conditions, including that the call occur within 48 hours of the earnings release, the call be accessible to the public, and the call and dial-in information be announced in advance to the public.[60]

In practice, many public companies make recordings of the call freely available on their website. Recordings of the calls are also commonly freely available on third-party platforms.

We believe that the requirements of Form 8-K elicit important disclosures about material events on a more timely basis than quarterly reports on Form 10-Q. We acknowledge, however, that quarterly earnings releases furnished with an Item 2.02 Form 8-K differ from Form 10-Q financial information because they are not required to be reviewed by an independent public accountant or to comply with the Commission's interim financial statement requirements or certain other requirements in Form 10-Q.[61]

We also acknowledge that, if a company elects to take advantage of semiannual reporting and stops reporting quarterly earnings or having quarterly earnings release conference calls, then the disclosures elicited by Item 2.02 of Form 8-K would not be available. We expect that a company's individual characteristics, facts, and circumstances will determine whether it would make quarterly earnings releases or announcements after electing to report semiannually.[62]

Regulation FD, adopted in 2000, was another significant development in the evolution of disclosure requirements for Exchange Act reporting companies. Regulation FD requires that any material non-public information selectively shared with certain enumerated persons be promptly (in the case of unintentional disclosure) or simultaneously (in the case of intentional disclosure) disclosed to the market by either furnishing or filing a Form 8-K report or disseminating the information through another method that is reasonably designed to provide broad, non-exclusionary distribution.[63]

In connection with Regulation FD, Exchange Act reporting companies may disclose material information during a fiscal year through Item 7.01 of Form 8-K.[64]

Regulation FD seeks to promote full and fair disclosure and may cause a company to disclose material information—whether on Form 8-K or through other means—at various points during a fiscal year, depending on the company and its circumstances (such as whether the company seeks to communicate previously material non-public information to analysts or other persons covered by Regulation FD). Such disclosure results in greater investor access to material information disclosed outside quarterly reports on Form 10-Q. Regulation FD and current Form 8-K disclosure requirements were either not present or less robust when the Commission last required the limited form of semiannual reporting during the period from 1955 to 1970.

Although we are proposing to amend our rules regarding frequency of interim reporting, our proposal does not include any general changes to the current regulatory requirements governing: (1) earnings releases, other than proposed technical amendments to Item 2.02 of Form 8-K to include references to semiannual periods, or (2) earnings guidance practices. Federal securities laws do not impose general duties upon Exchange Act reporting companies to announce or publish earnings, conduct earnings calls, or issue earnings guidance.[65]

We received public feedback on earnings releases and earnings guidance practice in connection with the Commission's 2016 Regulation S-K Concept Release and 2018 Request for Comment on Quarterly Earnings and Reporting, with commenters expressing a variety of views on these practices and on a wide range of related topics. Our proposal is focused on the more specific issue of the frequency of interim reporting as mandated by the Federal securities laws, with the goal of providing more flexibility with respect to this mandated disclosure. Although the proposal is not intended to change the regulatory framework for voluntary practices regarding earnings releases and guidance, we welcome comments on the impact of our proposal on these voluntary practices.

We believe our proposal represents a balanced approach of maintaining a reporting system that elicits material, timely, and regular disclosures in a manner that best suits the needs of both the company and its investors,

( printed page 24976)

promoting efficiency by reducing compliance costs, and maintaining robust investor protections. The proposal is one step in a broader Commission effort to encourage more companies to go and remain public by reducing the costs and burdens associated with Exchange Act reporting. A robust public capital market—with more emerging companies and small businesses choosing to become public companies through initial public offerings or other paths—benefits companies and investors alike. Becoming a public company provides companies with access to the public markets that allows them to raise capital to grow their businesses, a broader set of potential investors who may purchase their securities in the secondary trading market, and the benefits of transparent valuations by public markets and of a market following. For investors, public companies represent opportunities to participate in the future growth of promising companies. Initial public offerings represent liquidity opportunities for early-stage investors. Investors in public companies are protected by mandated disclosures and by liability provisions of the Federal securities laws that apply to public companies' disclosures, such as Securities Act Section 11 and Exchange Act Section 18.[66]

We are also proposing amendments to Regulation S-X. Our proposed amendments would incorporate provisions applicable to registrants that elect semiannual reporting frequency into the financial statement requirements for periodic reports. We are also proposing changes to the age of financial statement requirements in Regulation S-X to ensure that financial statements in registration statements filed by semiannual filers would not be considered “stale” under existing rules, which were built along a quarterly reporting framework, and to revise those age requirements for semiannual filers to fit with their reporting schedule. The proposed changes to the age of financial statement rules would also simplify existing rules, including by consolidating the age requirements into a single rule.

Finally, we recognize that, if the proposal is adopted, in order to comport with semiannual reporting by public companies, it is possible that changes may be necessary or appropriate to the rules of securities exchanges [67]

or to various accounting or auditing standards.[68]

If the proposal is adopted, to facilitate any such changes, we expect the Commission staff would coordinate with accounting and auditing standard-setters, securities exchanges, and other market participants. To help inform those efforts, we are soliciting comment in this release on what changes to accounting or auditing standards or rules of securities exchanges should be made to comport with semiannual reporting.[69]

Our proposal is discussed in greater detail below. We welcome interested parties to submit comments on any aspects of the proposed rule and form amendments. When commenting, please include the reasoning in support of your position or recommendation and provide any supporting documentation or data.

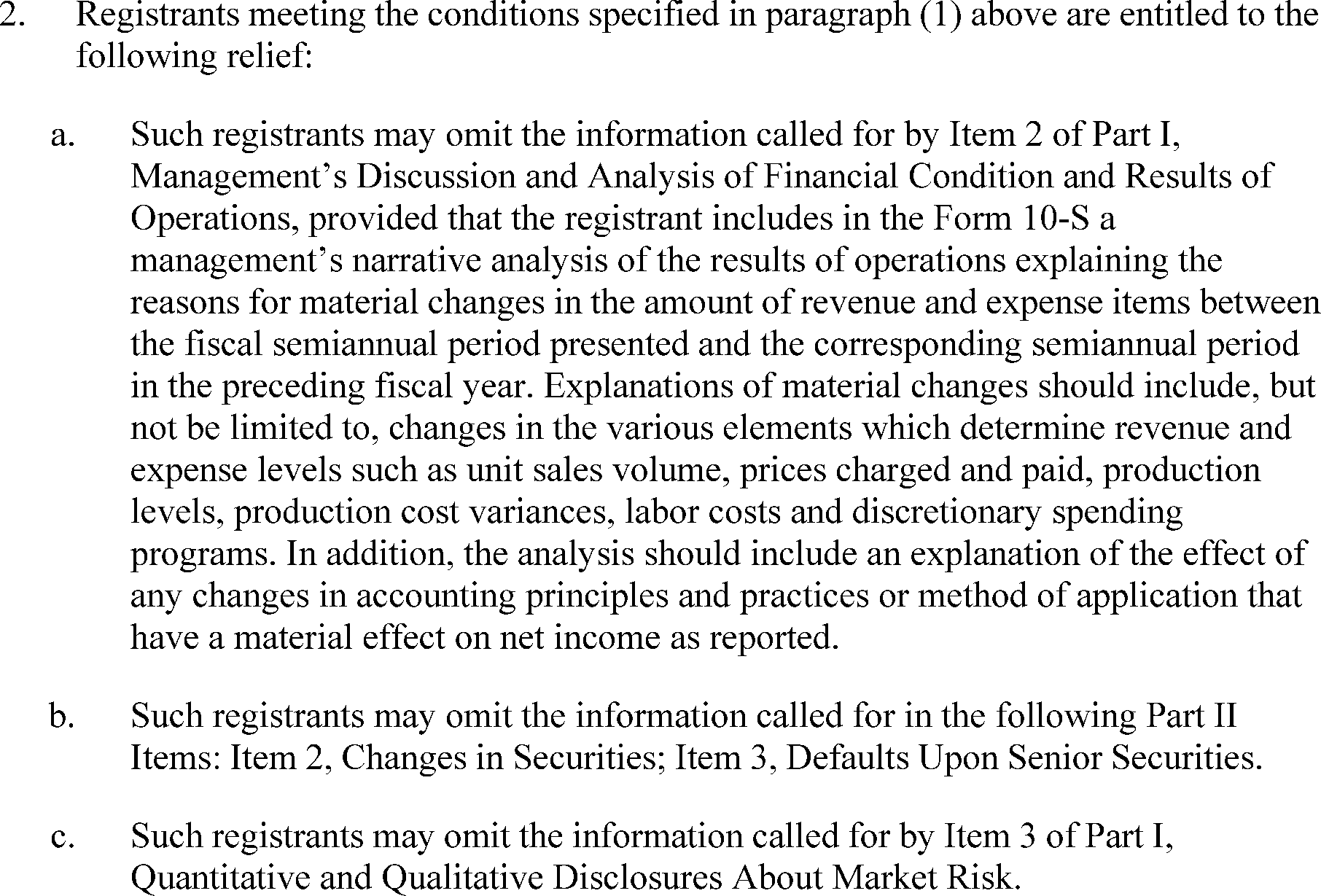

A. Proposed Amendments for Semiannual Reporting

We are proposing amendments to Exchange Act Rules 13a-13 and 15d-13 (and other relevant rules and forms that we discuss below) to change the current quarterly reporting requirements for Exchange Act reporting companies to a more flexible system that permits Exchange Act reporting companies to elect to file semiannual reports instead of quarterly reports.[70]

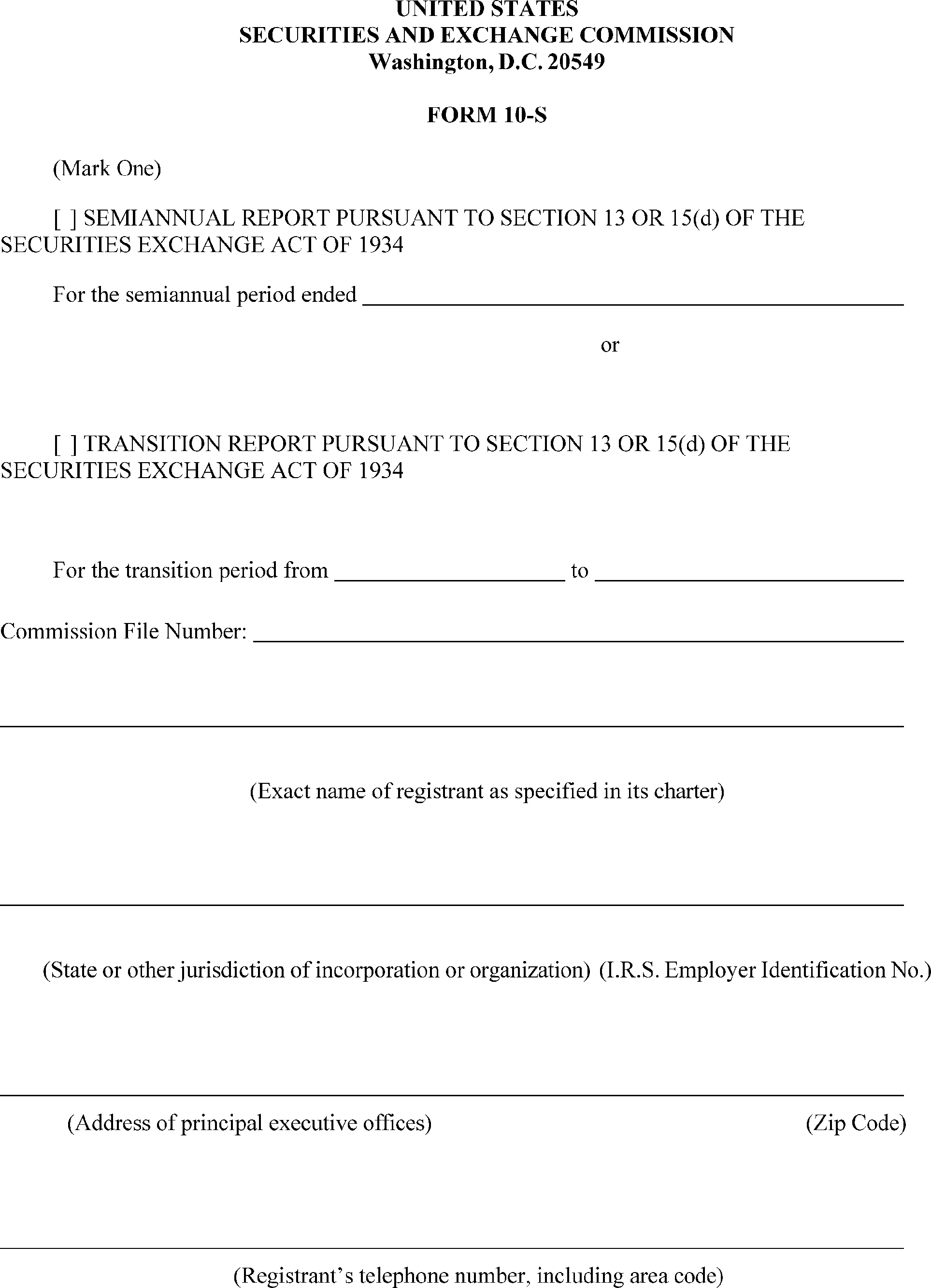

Under the proposal, an Exchange Act reporting company that elects semiannual reporting would be required to file one semiannual report and one annual report for each fiscal year. Semiannual filers would file their interim report on new Form 10-S. This form would require the same narrative disclosures and financial information as existing Form 10-Q but would cover a six-month period (rather than a fiscal quarter). The deadline for filing Form 10-S would be 40 or 45 days (depending on the company's filer status) after the fiscal year's first semiannual period end—the same as with current Form 10-Q's fiscal quarter end deadline, which would not change—while the second semiannual period would be subsumed in the annual period presented in the annual report on Form 10-K.[71]

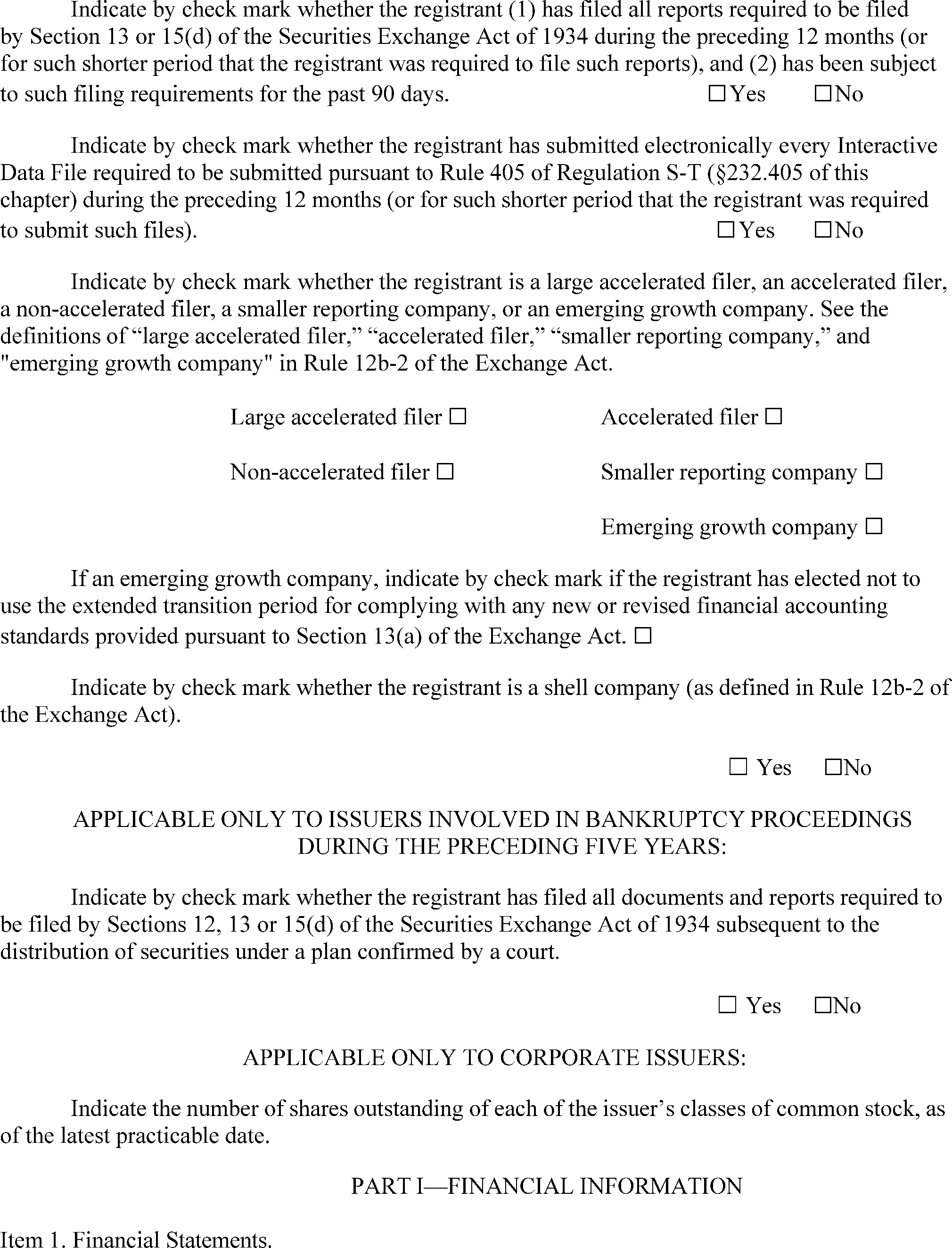

Reporting companies that do not elect to report on a semiannual basis—thereby effectively opting to report on a quarterly basis under the default rules that would apply—would continue to be required to file three quarterly reports on Form 10-Q and one annual report on Form 10-K for each fiscal year as under the current system for reporting companies. We are proposing to add a check box to the cover page of Form 10-K as the sole means by which a reporting company would indicate annually whether it is selecting a semiannual interim reporting frequency (by checking the semiannual box) or quarterly reporting (by not checking the semiannual box) and by which the reporting company would disclose the selected frequency to investors and other market participants.

( printed page 24977)

We are also proposing amendments to add a similar check box concerning the semiannual reporting election to the cover page of Securities Act registration statements on Forms S-1, S-3, S-4, and S-11 and Exchange Act registration statements on Form 10. Companies that have yet to file Exchange Act reports, such as private companies conducting initial public offerings, would make initial elections to use semiannual reporting by checking the box on the cover page of the registration statement filed.[72]

This election would determine what financial statements are required in the registration statement [73]

and indicate the company's planned interim reporting frequency to investors and other market participants.[74]

Similar to current requirements for the first quarterly report for companies that have newly become Exchange Act reporting companies,[75]

the first semiannual report on Form 10-S would be due the later of 45 days after the effective date of the registration statement or the date that Form 10-S would otherwise have been due had the company been an Exchange Act reporting company.[76]

In connection with our proposed optional semiannual reporting approach, we are proposing to add two new definitions—“quarterly filer” and “semiannual filer”—to 17 CFR 240.12b-2 (and to add two identical definitions to 17 CFR 230.405) to facilitate a number of amendments we are proposing, including a number of technical amendments to insert references to semiannual reporting in rules that currently refer to quarterly-reporting-related concepts. A “quarterly filer” would be defined as a registrant that is required to file quarterly reports on Form 10-Q, pursuant to 17 CFR 240.13a-13(a). A “semiannual filer” would be defined as a registrant that is required to file semiannual reports on Form 10-S, pursuant to 17 CFR 240.13a-13(b).

Under our proposed optional semiannual reporting approach, we are proposing to permit a change in interim reporting frequency—either from quarterly to semiannually or vice versa—to be indicated on a Form 10-K by checking the box on the cover page to file semiannually or leaving the box unchecked to file quarterly. As proposed, the determination to report semiannually or quarterly would therefore be made on an annual basis and may not be changed until the next Form 10-K annual report is filed.[77]

Companies would then be required to file interim reports based on the chosen frequency, beginning with the report for the first interim period (semiannual or quarterly) of the fiscal year in which the Form 10-K with the election was filed.[78]

For example, an Exchange Act reporting company reporting quarterly with a December 31 fiscal year-end wants to file semiannual reports on Form 10-S for the next fiscal year. The company would file its Form 10-K for fiscal year 2026 in March 2027. Under the proposal, the company would have to make its election to switch to semiannual reporting for fiscal year 2027 by checking the box for semiannual reporting on the cover page of its Form 10-K for fiscal year 2026. With this election made in fiscal year 2027 (i.e.,

when the Form 10-K for fiscal year 2026 was filed), the company would be required to report semiannually and would begin semiannual reporting by filing in August 2027 its Form 10-S for the first six-month period (ended June 30, 2027) of fiscal year 2027.[79]

Similarly, for example, an Exchange Act reporting company with a December 31 fiscal year-end that previously chose to file semiannual reports on Form 10-S as indicated in its Form 10-K for the fiscal year ended December 31, 2026 wishes to switch to quarterly reporting. The company will file its Form 10-K for fiscal year 2027 in March 2028. The reporting company would change its interim reporting frequency by leaving the box unchecked for semiannual reporting on the cover page of its Form 10-K for fiscal year 2027. With this election made in fiscal year 2028 (i.e.,

when the Form 10-K for 2027 was filed), the company would be required to report quarterly and would begin quarterly reporting by filing in May 2028 its Form 10-Q for the first quarter (ended March 31, 2028) of fiscal year 2028. In its Form 10-Q for the first quarter of fiscal year 2028, the company would be required to present statements of comprehensive income, cash flows, and changes in stockholders' equity for the first quarter of the preceding fiscal year (2027).[80]

These first quarter 2027 financial statements would have been subsumed within (but would not have been required to be separately presented in) the semiannual financial statements included in the previously filed Form 10-S covering January to June 2027. Therefore, in changing the election by leaving the box unchecked (thereby choosing to file quarterly reports on Form 10-Q for fiscal year 2028), the reporting company may need to take additional steps to prepare the financial statements for the comparable 2027 quarterly periods, including ensuring that an independent public accountant

( printed page 24978)

has reviewed the comparable quarterly periods for fiscal year 2027.[81]

Once an Exchange Act reporting company has elected its interim reporting frequency, it would be committed to that reporting frequency for the remainder of that fiscal year. This proposed approach would avoid potential investor confusion that could result if Exchange Act reporting companies were permitted to switch interim reporting frequency in the midst of a fiscal year, such as confusion over when the companies would file interim reports.

We recognize the possibility that a company may mistakenly leave the check box unmarked or incorrectly mark the check box (for example, a company mistakenly checking the box for semiannual reporting when it intended to be a quarterly filer or a company mistakenly leaving the check box unmarked when it intended to be a semiannual filer). We therefore propose to amend Rule 13a-13(b) and Rule 15d-13(b) to permit companies to amend their Form 10-K to correct any such inadvertent mistakes. Such corrective amendments would be required to be filed as soon as practicable after discovery of the mistake but no later than the due date by which the company's first Form 10-Q report would be required to be filed for the fiscal year in which the initial Form 10-K with the erroneous election was filed.[82]

For example, a quarterly filer with a December 31 fiscal year-end wants to continue filing quarterly reports on Form 10-Q. The company filed its Form 10-K for fiscal year 2026 in March 2027. It mistakenly marked the check box on the cover page of its Form 10-K for fiscal year 2026, thereby electing to switch to semiannual reporting for fiscal year 2027. The company would be able to correct this error by amending its Form 10-K no later than the due date for its Form 10-Q for the first quarter of fiscal year 2027.[83]

Proposed Form 10-S would require the same information as currently required by Form 10-Q but for the covered six-month period instead of a quarter.[84]

Required disclosures would include, among other things, MD&A, legal proceedings, material changes in risk factors, unregistered equity security sales and use of proceeds, defaults on senior securities, director nomination procedures, disclosure of director or officer adoptions or terminations of certain plans for the purchase or sale of registrant securities, and exhibits required under Item 601 of Regulation S-K. The financial statements for the covered semiannual period would be required to be prepared in accordance with U.S. GAAP [85]

and reviewed by an auditor (but not required to be audited).[86]

They would also be required to be data tagged using Inline XBRL. The current disclosure and certifications requirements for disclosure controls and procedures, as well as for internal control over financial reporting, would apply to proposed Form 10-S.[87]

Non-GAAP financial measures presented in proposed Form 10-S would be subject to the current requirements of Regulation G and Item 10(e) of Regulation S-K.

Request for Comment

1. The proposed amendments would allow Exchange Act reporting companies to elect to file interim reports on a semiannual basis in lieu of quarterly reports on Form 10-Q. Should companies have this option, or should all companies continue to be required to file Form 10-Q? What types of companies are likely to elect the option to file semiannual reports? Are companies in certain industries more likely than those in other industries to elect to file semiannual reports?

2. We are proposing amendments that would permit, but not require, all Exchange Act reporting companies that file Form 10-Q today to file semiannual reports. Should we instead require all companies to file semiannual reports? What would be the benefits and costs of such a mandatory approach? Would mandatory semiannual reporting, with the option to file quarterly reports, lead to more companies electing to forgo quarterly reporting?

3. Our proposal would permit semiannual reports for all Exchange Act reporting companies that file Form 10-Q today, regardless of filer status, revenues, market capitalization, or other criteria. Should the option for semiannual reporting be available only for Exchange Act reporting companies that satisfy certain criteria? If so, what criteria should be imposed and why? For example, should only emerging growth companies or smaller reporting companies be allowed to report semiannually? [88]

Should only companies below alternative quantitative or monetary thresholds be allowed to report semiannually? Should the Commission consider a pilot program to permit optional semiannual reporting for a subset of reporting companies and, if so, what would be the benefits of such a pilot program? What types of companies should be included in the pilot program?

4. Under the proposal, reporting companies currently required to file Form 10-Q would have the option

( printed page 24979)

instead to file semiannual reports on Form 10-S. Should any types of companies that currently file Form 10-Q be excluded from the option of electing semiannual reporting, such as business development companies?

5. We are proposing that the filing deadlines for semiannual reports on Form 10-S be the same as for quarterly reports on Form 10-Q. Should the filing deadline for semiannual reports on Form 10-S be longer or shorter than proposed? If so, what would be an appropriate filing deadline? Do companies need more time to prepare semiannual reports than quarterly reports and if so, why? Should smaller public companies, newly public companies, or emerging growth companies be afforded a longer filing deadline for Form 10-S to allow for additional time to consult with their accountants and advisers?

6. If adopted, would semiannual reporting have an impact on investors' ability to compare same-company performance over time? Why or why not?

7. What effect would our proposal have on investors' ability to compare the relative peer company financial performance of a quarterly filer to a semiannual filer? For example, can an investor reasonably compare a quarterly filer to a semiannual filer where the companies have the same fiscal year and the comparison is sought to be made in the second quarter (when first quarter information that would be subsumed in the semiannual filer's semiannual report on Form 10-S is not yet available) or made in the fourth quarter (when third quarter information that would be subsumed in the semiannual filer's annual report on Form 10-K is not yet available)?

8. Should the check box that indicates a company has elected semiannual reporting be added to registration statements on Forms 10, S-1, S-3, S-4, and S-11 and annual reports on Form 10-K as proposed? Should we add a similar check box to any other forms, including Forms 1-A or 8-A? If so, why?

9. Under our proposal, companies that want to file semiannual reports instead of quarterly reports would make their election by checking a box on the cover page of their annual report on Form 10-K for the most recently completed fiscal year. For investors and other market participants, this would mean that the first indication that a company will file only semiannual reports going forward will be when the company files its most recent Form 10-K. For example, under our proposal, a December 31 fiscal year-end company that files its Form 10-K for fiscal year 2026 in March 2027 would be able to cease filing quarterly reports immediately, with its next interim report being its first Form 10-S for the first six months of fiscal year 2027. Would investors and other market participants benefit from earlier notice of a company's intent to file semiannual reports instead of quarterly reports? If so, how would investors and others benefit and what would be the magnitude of any benefit? If so, what should the mechanism be for a company to provide earlier notice of intent to file semiannual reports?

10. Our proposal would require Exchange Act reporting companies that elect to file semiannual reports to continue with that interim reporting frequency for the rest of the fiscal year in which the election was made. Therefore, companies would not be allowed to file a semiannual report on Form 10-S for the first six months of a fiscal year and then file a quarterly report for the third quarter for that fiscal year. Likewise, companies would not be allowed to file a quarterly report on Form 10-Q for the first quarter of a fiscal year, file a semiannual report on Form 10-S for the first six months for that fiscal year, and not file a quarterly report on Form 10-Q for the third fiscal quarter. Would this proposed approach help avoid potential confusion that could be caused by changes in interim reporting frequency during a fiscal year? Is it necessary to add any language to the proposed rules to make more explicit the requirement to maintain the selected frequency for the full fiscal year? Rather than the proposed approach, should we allow: (1) semiannual filers and quarterly filers to make a change in interim reporting frequency during the fiscal year, or (2) only semiannual filers to switch to filing quarterly reports during the fiscal year? Should issuers that elect semiannual reporting be required to commit to that disclosure frequency for a certain period of time? Why or why not?

11. Do companies that have newly become a public company (

e.g.,

through an initial public offering, de-SPAC transaction, or direct listing) need to have greater flexibility for switching interim reporting frequency within a fiscal year? For example, a private company that elected semiannual reporting in a Form S-1 for an initial public offering could subsequently decide that quarterly reporting is preferable (

e.g.,

to promote greater trading liquidity by increasing the frequency of its interim reporting) and wish to switch to quarterly reporting for the rest of the fiscal year. Should we allow such newly public companies to switch the interim reporting frequency within a fiscal year?

12. Should correction of errors with respect to the Form 10-K check box related to semiannual reporting be permitted as we propose? Are the proposed time limits on when an error correction may be made appropriate? In addition to allowing error correction in an amended Form 10-K—or in lieu thereof—should we allow check box error correction through a Form 8-K filing?

13. We are proposing a new Form 10-S for companies that elect to file semiannual reports. Is the proposed new form needed? Should there be one form for all interim reports, regardless of whether they are for a fiscal quarter or a semiannual period? If so, why?

14. Proposed Form 10-S would mandate the same narrative and financial information as Form 10-Q, albeit for semiannual periods rather than quarterly periods. Should Form 10-S require narrative or financial information that differs from what is required in Form 10-Q? If so, please specify what information should be different and why this information is or is not needed in Form 10-S. Are there any disclosure items, such as mine safety violations, in proposed Form 10-S that should be required instead to be disclosed in other forms, such as Form 10-K, Form 8-K, or Form SD?

15. As an alternative to the proposal for optional semiannual reporting, should we instead revise the disclosure requirements of Form 10-Q to reduce the burden on reporting companies of filing this form, such as amending the current rules for the required interim financial statement review by an independent public accountant, XBRL data tagging, MD&A, information about unregistered sales of registrant securities pursuant to 17 CFR 229.701 (Item 701 of Regulation S-K), or year-to-date comparisons involving financial statements and MD&A? How should these requirements, or any other requirements of Form 10-Q, be revised? What aspects of Form 10-Q's current reporting framework are most burdensome for reporting companies?

16. What impact would the flexibility to file semiannual reports on Form 10-S, instead of quarterly reports on Form 10-Q, have on a private company's decision to become an Exchange Act reporting company? Would more companies choose to go public under the proposed flexible approach to interim reporting? What impact would the proposed flexible approach have on existing Exchange Act reporting companies' desire to remain public companies?

( printed page 24980)

17. What impact would the proposed option to file semiannual reports on Form 10-S have on Exchange Act reporting companies' ability to focus on: (1) business operations, (2) growth, or (3) long-term business strategies? Please provide any data on the amount of employee and director time spent on preparing a quarterly report on Form 10-Q.

18. What is the likelihood that companies that elect semiannual reporting will continue to issue quarterly earnings releases (to the extent they did so previously when they reported quarterly)? Why would semiannual filers still issue earnings releases on a quarterly basis? Would this practice create any new or heightened investor protection concerns? For example, would there be any new investor protection concerns if an Exchange Act reporting company with a December 31 year-end elects to file semiannual reports and issues an earnings release for the first quarter of the fiscal year, with the semiannual report for the first six months of the fiscal year (which includes that first quarter) not due until months later (

e.g.,

in August of that fiscal year)? Would companies that currently issue quarterly earnings releases but elect to become semiannual filers change their earnings release practices either: (1) to issue earnings releases semiannually, or (2) to cease issuing earnings releases? Please provide any data or analysis regarding any experience with earnings releases in foreign jurisdictions where issuers report semiannually.

19. Our proposal generally would not change the current Item 2.02 Form 8-K furnishing requirement for earnings releases (but we are proposing technical amendments to include references to semiannual periods). Should we change these requirements generally for semiannual filers? For example, should we amend the Form 8-K requirements so that Item 2.02 Form 8-K submissions are “filed,” not “furnished,” for semiannual filers thereby subjecting the earnings release to additional liability provisions, such as Exchange Act Section 18 (and Securities Act Section 11 if incorporated into a Securities Act registration statement), given that investors could rely more heavily on earnings releases by semiannual filers due to the less frequent interim reporting by such filers as compared to quarterly filers? If we require the filing (not furnishing) of earnings releases for semiannual filers, should we require the incorporation by reference of earnings releases into Securities Act registration statements of those semiannual filers? Would requirements for semiannual filers to file (not furnish) earnings releases discourage semiannual filers from issuing earnings releases? Would requirements for semiannual filers to file (not furnish) earnings releases have an impact on companies' decisions about whether to elect quarterly or semiannual reporting? Are there particular reasons or need for the information provided in an Item 2.02 Form 8-K submission by a semiannual filer to be treated differently than a similar Item 2.02 Form 8-K submission by a quarterly filer?

20. In connection with any adoption of the proposal, should there be a new requirement for semiannual filers that announce or release earnings for the first or third quarters of their fiscal year (

i.e.,

the periods that would later be subsumed in Forms 10-S and 10-K but for which there would be no quarterly report filed with the Commission)—that financial information in any first or third quarter earnings releases be reviewed by an independent public accountant? If so, would any changes to current auditing standards (

e.g.,

governing reviews) be required?

21. For companies that issue earnings releases, would the proposed flexible approach to interim reporting have any effect on how quickly these releases would be issued after the end of the reporting period?

22. Would the option for semiannual reporting result in an overall reduction in material information for investors? Or would other regulatory requirements, such as Form 8-K filing requirements and Regulation FD, elicit sufficient information to offset the less-frequent interim reports and address any investor protection concerns? Would market forces or demands on a company's business—such as contractual obligations, investor expectations, and potential for shareholder activism—encourage semiannual filers to: (1) voluntarily disclose more information than required, (2) disclose information more frequently than is required, or (3) opt not to become semiannual filers at all?

23. With semiannual reporting, would there be an impact on investors or other market participants as a result of less frequent certifications by management relating to internal control over financial reporting and disclosure controls and procedures, as well as less frequent disclosures of changes in such controls? [89]

24. Would the nature and extent of procedures that an independent public accountant performs during a review change depending upon whether the independent public accountant is performing a review over a fiscal semiannual period or a fiscal quarterly period? Would independent public accountants conducting reviews do the same amount of work for a fiscal semiannual period as they currently do for two quarterly fiscal periods on a combined basis? Would an independent public accountant experience any impact on efficiency or economies of scale when conducting reviews and annual audits under semiannual reporting versus under quarterly reporting for the same company? Would any changes to independent public accountants' review or audit procedures or any impact on efficiency or economies of scale result in changes in costs to companies? If so, describe the impact and whether the impact could vary depending upon the size of the registrant subject to the review.

25. Would companies that elect semiannual reporting retain their independent public accountant to perform a review of their financial statements at the end of each quarter either to: (1) support financial information that is used for purposes of a quarterly earnings release (notwithstanding that, as noted above, there is no Commission requirement for a quarterly earnings release to be reviewed by an independent public accountant), or (2) guard against the possible need for a quarterly review to be performed should the company decide to change back to quarterly reporting in a future period (where that period would require comparative quarterly data for the prior year)?

26. For semiannual filers, what impact would a shift to semiannual reporting have on: (1) companies' disclosure controls and procedures, (2) companies' internal control over financial reporting, and (3) independent public accountants' strategy and approach for the annual audit of companies' internal control over financial reporting or financial statements? With semiannual reporting, is there a potential for a material increase in the risk that material misstatements (either due to error or fraud) or control deficiencies are not timely detected by or communicated to the independent public accountant thereby limiting potential remediation of these issues by the issuer? Please provide any data related to these questions.

27. Would there be reduced securities analyst coverage of Exchange Act

( printed page 24981)

reporting companies that elect the semiannual reporting option as compared to quarterly filers? Would underwriters' requests for independent public accountants to provide “comfort letters” [90]

in securities offerings (to support potential due diligence defenses) [91]

lead semiannual filers to continue to retain independent public accountants to conduct quarterly financial statement reviews? If so, are changes needed to PCAOB Auditing Standards (regarding reviews by independent public accountants)? [92]

For example, to comport with semiannual reporting, are changes needed to PCAOB Auditing Standard 6101,

Letters for Underwriters and Certain Other Requesting Parties,

to permit independent public accountants to provide comfort letters expressing negative assurance on changes subsequent to the date and period of the latest financial statements included (or incorporated by reference) in the registration statement? [93]

If semiannual filers would continue to prepare quarterly financial information or to retain independent public accountants to conduct quarterly reviews, should the Commission make any rule changes or take any other steps to address this issue?

28. Would our proposal have any impact on a semiannual filer's application of relevant accounting standards to prepare financial statements in accordance with U.S. GAAP, IFRS, or home-country GAAP? How? Are any changes to accounting standards, including U.S. GAAP or IFRS, necessary or appropriate to effectuate semiannual reporting (

e.g.,

changes to the guidance on annual impairment testing, lag reporting, earnings per share, or other topics of authoritative guidance)?

29. Are any changes to rules of securities exchanges necessary or appropriate to effectuate semiannual reporting?

30. Should we require the second semiannual period financial information (for semiannual filers) or the fourth quarter financial information (for quarterly filers) to be included in Form 10-K so investors do not need to back out this information if companies do not voluntarily provide it? Would having a longer period (six months for semiannual reports versus three months for quarterly reports) make it more difficult for investors to back out this information? Relatedly, should we require semiannual filers to break out financial statement information for the six-month period covered by Form 10-S into two three-month periods and provide similarly broken-out three-month information for the fiscal year covered by Form 10-K?

31. Many public companies have standalone insider trading policies or insider trading policies that are part of the company's code of ethics,[94]

and these policies may provide for trading windows.[95]

What impact would optional semiannual reporting have on company insider trading policies, including trading windows? For example, would companies impose longer trading blackout periods at the beginning of a semiannual period or towards the end of a semiannual period than they would impose if reporting quarterly? Even if these periods are longer, would the total number of blackout days be fewer each fiscal year for semiannual filers compared to quarterly filers given that semiannual filers would report less frequently? To the extent that there are longer blackout periods or fewer total blackout period days each year, what effects would these changes have on semiannual filers? Under our proposal, semiannual filers are allowed to voluntarily issue quarterly earnings releases. How would this affect current trading windows practices, if at all? Where a company elects to be a semiannual filer, would this be likely to have an effect on trading plans that may be adopted by companies or insiders (

e.g.,

company directors, officers, or employees) for purposes of 17 CFR 240.10b5-1 (Exchange Act Rule 10b5-1)? If so, what are the effects?

32. Would there be an increased risk of insider trading at companies that elect to report on a semiannual basis? If so, please provide the basis for this view, as well as data. Could companies enhance their insider trading policies or improve their self-enforcement of these policies to help address this concern? What other actions could companies or the Commission take to mitigate any increase in the risk of insider trading?

33. How would the proposed flexible approach to semiannual reporting affect the competitiveness of U.S. reporting companies vis-a-vis foreign competitors? For Exchange Act reporting foreign companies that would

( printed page 24982)

not be foreign private issuers (which report semiannually as discussed above) and that would report quarterly under the current system, would the proposed option to report semiannually make these foreign companies more likely to list on a U.S. exchange? What would be the competitive implications of the proposed optional semiannual reporting approach between U.S. reporting companies (which report quarterly under the current system) and foreign private issuers (which report semiannually under the current system as a practical matter)? Should there be different periodic reporting for foreign private issuers compared to domestic issuers? Why or why not?

34. If the proposal is adopted, what should be the compliance date for the proposed amendments? If the proposal is adopted, is there a need for a transition period and, if so, what should be the length of the period?

B. Proposed Amendments to Regulation S-X

We are proposing amendments to various rules in Regulation S-X that would incorporate semiannual reporting and simplify the rules with respect to the age of financial statements. Specifically, the proposed amendments would:

simplify Rule 3-01 and Rule 8-08 by reorganizing each and consolidating the requirements of Rule 3-12 regarding the age of financial statements in a registration or proxy statement into the balance sheet requirements of Rule 3-01;

revise the age requirements to incorporate semiannual reporting through the introduction of a revised model for determining the age of interim financial statements; and

revise other rules in Regulation S-X to incorporate semiannual reporting.

1. Streamlining Age of Financial Statements Requirements

To simplify our rules and effectuate our proposed optional semiannual reporting approach, we are proposing amendments to Rules 3-01 and 8-08 of Regulation S-X so that each amended rule clearly sets forth the requirements for annual financial statements and interim financial statements. The proposed amendments would consolidate the requirements of Rule 3-12 into Rule 3-01 and eliminate Rule 3-12.

Currently, Rule 3-01 governs the date of audited and interim balance sheets required to be included in filings as of the filing date.[96]

The requirements for statements of comprehensive income, cash flows, and changes in stockholders' equity—set out in current 17 CFR 210.3-02 (Rule 3-02 of Regulation S-X) and 17 CFR 210.3-04 (Rule 3-04 of Regulation S-X)—are derived from dates of annual and interim balance sheets required by Rule 3-01.[97]

While current Rule 3-01 addresses the dates of the balance sheets as of the filing date, current Rule 3-12 addresses the age of financial statements as of the effective date of a registration statement or mailing of a proxy statement.[98]

Notwithstanding this difference, application of the two rules currently results in age requirements that are aligned: if a registrant were to apply current Rule 3-01's filing date age requirements to a registration statement at the date of effectiveness (or a proxy statement at the mailing date), the resulting financial statement requirements would be no different than if Rule 3-12 were applied. Our proposed consolidation of Rules 3-01 and 3-12 would streamline Regulation S-X, making the age of financial statement requirements easier to apply. To clarify the dual purpose of Rule 3-01 as proposed to be revised, we are proposing new Rule 3-01(a), which would provide that the date of the most recent balance sheet included in a registration or proxy statement must be updated to comply with that section's requirements as if the effective date of the registration statement, or proposed mailing date in the case of a proxy statement, were the filing date.

Further, we are proposing several amendments to streamline and reorganize Rule 3-01 as well as integrate Rule 3-12 into Rule 3-01.

We are proposing to place the rules regardingannual

balance sheets in Rule 3-01(b). We do not propose any substantive amendments to the rules regarding annual balance sheets. Proposed Rule 3-01(b) would require audited balance sheets as of the end of the two most recently completed fiscal years, which would be the same as current Rule 3-01(a).

The current exceptions to current Rule 3-01(a) applicable to filings other than on Form 10-K would be included in proposed Rules 3-01(b)(1) and (b)(2).

○ Proposed Rule 3-01(b)(1), which would be the same as current Rules 3-01(b) and 3-12(b), would permit that if the filing is made no more than 45 days after the end of the registrant's fiscal year, the audited balance sheets may be as of the end of the two fiscal years preceding the most recently completed fiscal year and must include an additional balance sheet as of an interim date specified in proposed paragraph (c)(1), as described further below.

○ Proposed Rule 3-01(b)(2), which would be the same as current Rules 3-01(c) and 3-12(b), would permit that—if the filing is made more than 45 days but no more than 59 days (for large accelerated filers, as defined in § 240.12b-2 of this chapter), 74 days (for accelerated filers, as defined in § 240.12b-2 of this chapter), or 89 days (for all other registrants) after the end of the registrant's most recently completed fiscal year—so long as three conditions are met, the registrant may apply proposed paragraph (b)(1), which means that, in this situation, the audited balance sheets may also be as of the end of the two fiscal years preceding the most recently completed fiscal year and the filing must include an additional balance sheet as of an interim date specified in proposed paragraph (c)(1).[99]

We do not propose any changes to the three conditions.

Proposed Rule 3-01(b)(3), which would be similar to the second sentence of current Rule 3-01(a), would require the filing of an audited balance sheet dated as of a date not more than 134 days before the date of the filing if the

( printed page 24983)

registrant was not in existence as of the end of its fiscal year.

Proposed Rule 3-01(b)(4), which would be the same as Rules 3-01(b) and 3-12(c),[100]

would require that, notwithstanding the requirements of this section, the filing must be updated with audited financial statements for the most recently completed fiscal year if they become available prior to the filing date.

The proposed amendments to Rules 3-01 and 8-08 reflect the replacement of references to filing dates from the current text of “within” a certain number of days after a milestone (

e.g.,

filing date or end of the fiscal year or quarter) to “more than” or “no more than” a certain number of days.[101]

We believe this change will clarify the filing requirements and ensure alignment of financial statement updating dates with the Forms 10-K, 10-Q, and 10-S filing deadlines. A registration or proxy statement filed on the same date a periodic report is due would be required to include the financial statements required in that periodic report. We are making similar clarifying amendments to Exchange Act Rules 13a-13 and 15d-13.

We are proposing to place the rules regarding an

interim

balance sheet in Rule 3-01(c).

Proposed Rule 3-01(c)(1) would require that, when an audited balance sheet for the most recently completed fiscal yearis not included in

the filing, the interim balance sheet must be as of the end of the third fiscal quarter of the most recently completed fiscal year for quarterly filers or as of the end of the first fiscal semiannual period of the most recently completed fiscal year for semiannual filers. This proposed rule would be similar to current Rule 3-01(b) and Rule 3-12(b), except that it would require a semiannual filer to file an interim balance sheet as of the end of its semiannual period.

Proposed Rule 3-01(c)(2) would set forth requirements for an interim balance sheet when an audited balance sheet for the most recently completed fiscal yearis included in

the filing. We discuss proposed Rule 3-01(c)(2)'s requirements for an interim balance sheet for the current fiscal year in detail in Section III.B.2 below on determining the age of interim financial statements.

Proposed Rule 3-01(c)(3) would be substantively unchanged from current requirements in Rules 3-01(f) and 3-12(a) and would provide that an interim balance sheet provided in accordance with proposed Rule 3-01(c) need not be audited and need not be presented in greater detail than is required by § 210.10-01.

We are proposing to renumber current Rule 3-01(g), regarding registered management investment companies, as Rule 3-01(d). Likewise, we are proposing to renumber current Rule 3-01(h), regarding foreign private issuers, as Rule 3-01(e)(1). We are proposing to incorporate current Rule 3-12(f) regarding financial statements of a foreign business into proposed Rule 3-01(e)(2).

We are proposing to delete current Rule 3-01(d), which requires—when filings are made after 45 days but within a number of days of the end of the registrant's fiscal year based on its filer status and the three conditions in Rule 3-01(c) are not met—that balance sheets for the two most recently completed fiscal years must be included. We believe current Rule 3-01(d) is redundant with current Rule 3-01(a) and is unnecessary to include in Rule 3-01 as proposed to be revised, because we believe it is clear if the required conditions in current Rule 3-01(c) are not met, then the registrant must provide the balance sheet for the two most recently completed fiscal years as required by current Rule 3-01(a) and as would be required by proposed Rule 3-01(b)(2).

We do not propose to integrate current Rule 3-12(d) into Rule 3-01 as proposed to be revised, as we believe it would be redundant with proposed Rule 3-01(b). Current Rule 3-12(d) requires the age of the registrant's most recent audited financial statements included in a registration statement filed under the Securities Act or filed on Form 10 under the Exchange Act to be no more than one year and 45 days old at the date the registration statement becomes effective if the registration statement relates to the security of an issuer that was not subject, immediately before the time of filing the registration statement, to the reporting requirements of Exchange Act Section 13 or 15(d). Because a registrant in this situation would not satisfy the first of the three conditions in proposed Rule 3-01(b)(2), it would be required to file an annual balance sheet for the most recently completed fiscal year, which would be as of a date more current than one year and 45 days.

Because proposed Rule 3-01 would integrate current Rule 3-12, as described above, we are proposing to eliminate Rule 3-12. We are also proposing technical amendments to rules that currently refer to Rule 3-12 to reflect its integration into Rule 3-01.[102]

Smaller reporting companies apply Rule 8-08 to determine the age of financial statements. We are proposing amendments to Rule 8-08 to conform its organization to proposed Rule 3-01, as described above.

With respect to

annual

financial statements, we are proposing to eliminate the introductory text of Rule 8-08 and revise paragraph (a) to address annual financial statements. Consistent with proposed Rule 3-01(b), proposed paragraph (a) of Rule 8-08 would require a registrant to file, in filings other than on Form 10-K, audited annual financial statements for the registrant and its predecessors, as required by Rule 8-02. We are also proposing to move current paragraph (a) to paragraph (a)(1) of Rule 8-08 and revise the rule to require that if the effective date of a registration statement or anticipated mailing date of a proxy statement is no more than 45 days after the end of the most recently completed fiscal year, the filing may include financial statements as of the end of the two fiscal years preceding the most recently completed fiscal year and for the years then ended and must include interim financial statements, the requirements for which we propose to move to a revised paragraph (b). We are proposing to move the requirements in current paragraph (b) of Rule 8-08, that address the requirements when the effective date of a registration statement or mailing date of a proxy statement is more than 45 days but not more than 90 days after the end of the most recently completed fiscal year, to a new proposed paragraph (a)(2) of Rule 8-08. The proposed amendments would not change the age of

annual

financial statements requirements for a smaller reporting company.

With respect to

interim

financial statements, we are proposing to revise paragraph (b) of Rule 8-08 to include the interim financial statement requirements. Proposed paragraph (b)(1) of Rule 8-08 would require that, if

( printed page 24984)

audited financial statements for the most recently completed fiscal year

are not included in

the filing, a quarterly filer must file interim financial statements as of the end of the third fiscal quarter of the most recently completed fiscal year and for the nine months then ended and a semiannual filer must file interim financial statements as of the end of the first fiscal semiannual period of the most recently completed fiscal year and for the semiannual period then ended. Proposed paragraph (b)(2) of Rule 8-08 would require that, if audited financial statements for the most recently completed fiscal year

are included in

a filing, the registrant must file interim financial statements as of the end of the most recently completed fiscal quarter (for quarterly filers) or semiannual period (for semiannual filers) and for the year-to-date interim period then ended that has been filed, or is required to be filed on or before the filing date, in a Form 10-Q or Form 10-S. A registrant that is not subject to Exchange Act Section 13(a) or 15(d) would apply this rule as if it were required to file Form 10-Q or Form 10-S.

These proposed interim requirements in Rule 8-08 would replicate the requirements in proposed Rules 3-01(c)(1) and (2). Proposed paragraph (b)(3) of Rule 8-08 would require that interim financial statements must be prepared and presented in accordance with Rule 8-03, which would replicate proposed Rule 3-01(c)(3).

2. Determining Age of Interim Financial Statements

As noted in Section III.B.1 above, proposed Rule 3-01(c)(2) would address age requirements for interim financial statements (and proposed Rule 8-08(b)(2) would address age requirements for smaller reporting companies). These proposed amendments would revise how the date of an interim balance sheet is determined in registration or proxy statements. Currently, Rule 3-01(e) requires that, for filings made after 129 days or 134 days (depending on filer status) after fiscal year end, the filing must include a balance sheet as of an interim date within 130 days or 135 days of the date of filing (depending on filer status). Rule 3-12 similarly requires that, if the financial statements in a filing are as of a date 130 days or 135 days (depending on filer status) or more before the date the filing is expected to become effective, or the proposed mailing date in the case of a proxy statement, the financial statements must be updated with a balance sheet as of an interim date within 130 days or 135 days (depending on filer status). Rule 8-08 contains a similar age requirement for the filing of interim financial statements in a registration or proxy statement.

Under the proposed amendments, a registrant would no longer assess the number of days from the filing date or from the effective date of the registration statement (or mailing date of a proxy statement) to the date of the most recent balance sheet to determine if the balance sheet falls within 130 days or 135 days, as applicable. Rather, under the proposed amendments to Rules 3-01(c)(2) and 8-08(b)(2), a registrant, in determining if interim financial statements are required when audited financial statements for the most recently completed fiscal year are included in the filing, would include the interim financial statements as of the end of the most recently completed fiscal quarter (for quarterly filers) or semiannual period (for semiannual filers) that has been filed, or is required to be filed on or before the filing date, in a Form 10-Q or Form 10-S.[103]

A registrant that is not subject to Exchange Act Section 13(a) or 15(d) would apply this rule as if it were required to file Form 10-Q or Form 10-S. In this regard, for a non-reporting company that filed a registration statement that has not yet become effective, these provisions of proposed Rules 3-01(c)(2) and 8-08(b)(2) (regarding the interim financial statements that would have been required in a Form 10-Q or Form 10-S) would mean that the non-reporting company must file in a registration statement the interim financial statements that would have been required in periodic reports if that non-reporting company were an Exchange Act reporting company.[104]

For example, the Form 10-Q or proposed Form 10-S for a company that is a large accelerated filer or accelerated filer would be due 40 days after the end of the interim period (or 45 days for all other registrants). For an interim period ending on June 30, the Form 10-Q or proposed Form 10-S would be due by August 10 for a large accelerated or accelerated filer (August 14 for all other registrants). Under the proposed amendments, a registration statement filed by a large accelerated or accelerated filer on August 10 (or August 14 for all other registrants) would be required to include financial statements for the interim period ended June 30.

We are proposing this change to simplify the updating requirements in current rules and to align the date upon which the interim financial statements of a quarterly filer's second quarter would be required to be updated with that of a semiannual filer's first semiannual period. In this regard, with respect to semiannual filers, if we were to simply add 90 days to the existing 135-day window, based on the application of current Rule 3-12 of Regulation S-X, the date upon which a semiannual filer would have to update its interim financial statements for the semiannual financial statements could differ by one or two days compared to the date upon which a quarterly filer would have to update its second quarter financial statements.[105]

The proposed amendments to Rule 3-01(c)(2) and 8-08(b)(2) would avoid disparate treatment between semiannual filers and quarterly filers with respect to the age of the interim financial statements requirements.

The 1980 Regulation S-X Adopting Release stated that Rule 3-12 would result in requirements for the age of financial statements in registration statements that “correspond with the requirements for quarterly data under the 1934 Act on Form 10-Q.” [106]

While the requirements correspond, they are not identical: Rule 3-12 requires updated financial statements to be as of a date within 130 days or 135 days of effectiveness (depending on filer status); while a Form 10-Q is due 40 days or 45 days after the end of the fiscal quarter (depending on filer status). As a result of this difference, under current rules, the financial statements in a registration statement or proxy statement may be

( printed page 24985)

required to be updated one or two days before those same financial statements are required to be filed on Form 10-Q. Such a difference results from the number of days in a quarter that exceeds 90 days.[107]

Our proposed rule would align the financial statement age requirements of registration statements (and proxy statements) with the filing deadlines of Form 10-Q and Form 10-S, eliminating such one- or two-day differences. Proposed Rule 3-01(c)(2) results in both quarterly filers and semiannual filers having the same date on which the financial statements would be required to be updated because both filers would determine the date from the end of their most recently completed interim period as opposed to, for example, the quarterly filer's determination being from the end of the first quarter and the semiannual filer's determination being from the end of the fiscal year.

Under the proposed amendments to Rule 3-01(c), the interim financial statement period required in a registration or proxy statement would be as of the end of a registrant's fiscal quarterly or semiannual period, as applicable. This would differ from current Rule 3-12, which permits interim financial statements as of any date so long as they cover a period within the prescribed number of days from the date of effectiveness or mailing date. We observe that virtually all registrants file interim financial statements as of the end of a quarter, since those financial statements would be filed in future Exchange Act reports on Form 10-Q. Further, registrants who wish to file interim financial statements as of a date that does not align with a quarterly or semiannual period may request a substitution of financial statements under 17 CFR 210.3-13 (Rule 3-13 of Regulation S-X). As a result, we do not expect that this aspect of the proposed amendments would result in any change in today's practice.[108]

When interim financial statements for a semiannual filer are required in a registration or proxy statement, proposed Rule 3-01(c)(2) would require those interim financial statements to be for a semiannual period. Under the proposed rules, depending on when the registration statement becomes effective or the proxy statement is mailed, an investor in a registrant that is a semiannual filer may not receive interim financial statements that are as current as would be required today. For example, if a non-reporting registrant with a calendar fiscal year that elects semiannual reporting files a registration statement as late as August 13, proposed Rule 3-01(c)(2) would not require any interim financial statements to be included in the registration statement. In contrast, under the current requirements and under the proposal for those registrants that continue to report quarterly, the filing would include interim financial statements for the first fiscal quarter. As discussed in Section I, we are proposing these amendments that may result in less current interim financial statements in a registration statement to reduce regulatory burden and align the requirements for updating interim financial statements with the requirements for periodic reporting under the Exchange Act, including the proposed semiannual reporting option.

3. Other Proposed Amendments to Regulation S-X