Patient Protection and Affordable Care Act, HHS Notice of Benefit and Payment Parameters for 2027; and Basic Health Program

This final rule contains provisions to improve implementation of the Patient Protection and Affordable Care Act, including payment parameters and provisions related to the HHS-o...

Centers for Medicare & Medicaid Services (CMS), Department of Health and Human Services (HHS).

ACTION:

Final rule.

SUMMARY:

This final rule contains provisions to improve implementation of the Patient Protection and Affordable Care Act, including payment parameters and provisions related to the HHS-operated risk adjustment and risk adjustment data validation (HHS-RADV) programs, as well as 2027 user fee rates for issuers offering qualified health plans (QHPs) through Federally-facilitated Exchanges (FFEs) and State-based Exchanges on the Federal platform (SBE-FPs). This final rule also includes provisions related to civil money penalties (CMPs) for noncompliant issuers and other responsible entities; standards governing agents, brokers, and web-brokers; the expansion and codification of hardship exemption eligibility; implementation of the State Exchange Improper Payment Measurement (SEIPM); provider access standards and essential community provider standards for QHP certification; QHP certification of non-network plans; a prohibition on issuers from including routine non-pediatric dental services as an Essential Health Benefit (EHB); requirements related to defrayal for the cost of any State-required benefits in addition to the EHB; cost-sharing flexibilities for catastrophic and individual market bronze plans; establishment of catastrophic plans with plan terms of up to 10 consecutive plan years; QHP issuer quality improvement strategies (QISs); and revisions affecting which enrollees are included in Federal Basic Health Program (BHP) payment calculations to States. This final rule also includes amendments to implement certain provisions of the Working Families Tax Cut (WFTC) legislation.

DATES:

These regulations are effective on July 20, 2026.

FOR FURTHER INFORMATION CONTACT:

Jeff Wu, (301) 492-4305, Rogelyn McLean, (410) 786-1524, Grace Bristol, (410) 786-8437, for general information.

Ayesha Anwar, (301) 448-3625, or Joshua Paul, (301) 492-4347, for matters related to HHS-operated risk adjustment and HHS-operated risk adjustment data validation.

Aaron Franz, (410) 786-8027 for matters related to user fees.

Brian Gubin, (410) 786-1659, for matters related to agent, broker, and web-broker guidelines.

Zarin Ahmed, (301) 492-4400, for matters related to enrollment of qualified individuals into QHPs and termination of Exchange enrollment or coverage for qualified individuals.

Hannah Armbruster Hill, (301) 492-4343, for matters related to certification standards for QHPs, cost-sharing requirements, and the Actuarial Value Calculator.

Kelly Carda, (312) 886-5210, or Cassandra Thompson, (667) 414-0870, for matters related to Provider Access standards.

Ariana Koenitzer, (410) 786-0724, or Samantha Nguyen Kella, (816) 426-6339, for matters related to Essential Community Provider Standards.

Ariana Koenitzer, (410) 786-0724, or Cassandra Thompson, (667) 414-0870, for matters related to QHP Certification of Non-Network Plans.

Nikolas Berkobien, (667) 290-9903, for matters related to standardized plan options, non-standardized plan option limits and exceptions.

Jenny Chen, (301) 492-5156, or Shilpa Gogna, (301) 492-4257, for matters related to State Exchange and State Exchange Blueprint requirements.

Rebecca Braun-Harrison, (667) 290-8846, or Nia Blasingame, (470) 890-4178, for matters related to civil money penalties of issuers and non-Federal governmental group health plans.

Preeti Hans, (301) 492-5144, for matters related to the Quality Improvement Strategy.

Mary Beth Hance, 410-786-4299, for matters related to the Basic Health Program.

Christina Whitefield, (301) 492-4172, for matters related to the medical loss ratio (MLR) program.

David Mlawsky, (410) 786-6851, for matters related to catastrophic plans with multi-year plan terms.

Jessica Veffer, (301) 492-4827, for matters related to expanding hardship exemptions for individuals ineligible for APTC or CSRs due to projected household income.

SUPPLEMENTARY INFORMATION:

I. Executive Summary

We are finalizing changes to the provisions and parameters implemented through prior rulemaking to implement the Patient Protection and Affordable Care Act and are also finalizing updates to implement new provisions.[1]

These requirements are published under the authority granted to the Secretary of HHS (the Secretary) by the Affordable Care Act and the Public Health Service (PHS) Act.[2]

In this document, we are finalizing changes related to some of the Affordable Care Act provisions and parameters we previously implemented under the authority granted to the Secretary by Public Law (Pub. L.) 119-21, which CMS refers to as the Working Families Tax Cut (WFTC) legislation.[3]

Our goal with these requirements is providing quality, more affordable coverage to consumers while minimizing administrative burden and ensuring program integrity. The changes finalized in this rule are also intended to enhance the role of States in these programs, provide issuers and States with additional flexibilities, reduce unnecessary regulatory burden on interested parties, and improve affordability.

II. Background

A. Legislative and Regulatory Overview

Title I of the Health Insurance Portability and Accountability Act of 1996 (HIPAA) added a new title XXVII to the PHS Act to establish various reforms to the group and individual health insurance markets. These provisions of the PHS Act were later augmented by other laws, including the Affordable Care Act. Subtitles A and C of title I of the Affordable Care Act reorganized, amended, and added to the provisions of part A of title XXVII of the PHS Act relating to group health plans and health insurance issuers in the group and individual markets. The term “group health plan” includes both insured and self-insured group health plans.

In the upcoming sections, we summarize sections of the PHS Act,

( printed page 29527)

Affordable Care Act, and WFTC legislation that are relevant to this final rule.

Section 1301(a)(1)(B) of the Affordable Care Act directs all issuers of qualified health plans (QHPs) to cover the Essential Health Benefit (EHB) package described in section 1302(a) of the Affordable Care Act, including coverage of the services described in section 1302(b) of the Affordable Care Act, adherence to the cost-sharing limits described in section 1302(c) of the Affordable Care Act, and meeting the Actuarial Value (AV) levels established in section 1302(d) of the Affordable Care Act. Section 2707(a) of the PHS Act, which is effective for plan or policy years beginning on or after January 1, 2014, extends the requirement to cover the EHB package to non-grandfathered individual and small group health insurance coverage, irrespective of whether such coverage is offered through an Exchange. In addition, section 2707(b) of the PHS Act directs non-grandfathered group health plans to ensure that cost sharing under the plan does not exceed the limitations described in section 1302(c)(1) of the Affordable Care Act.

Section 1302 of the Affordable Care Act provides for the establishment of an EHB package that includes coverage of EHB (as defined by the Secretary), cost-sharing limits, and AV requirements. The law directs that EHB be equal in scope to the benefits provided under a typical employer plan, and that they cover at least the following 10 general categories: ambulatory patient services; emergency services; hospitalization; maternity and newborn care; mental health and substance use disorder services, including behavioral health treatment; prescription drugs; rehabilitative and habilitative services and devices; laboratory services; preventive and wellness services and chronic disease management; and pediatric services, including oral and vision care.

Section 1302(b)(4)(A) through (D) of the Affordable Care Act establish that the Secretary must define EHB in a manner that: (1) reflects appropriate balance among the 10 categories; (2) is not designed in such a way as to discriminate based on age, disability, or expected length of life; (3) takes into account the health care needs of diverse segments of the population; and (4) does not allow denials of EHB based on age, life expectancy, disability, degree of medical dependency, or quality of life.

Section 1302(e) of the Affordable Care Act establishes standards for catastrophic plans to be offered in the individual market and states that the only individuals who are eligible to enroll in catastrophic coverage are individuals who: (1) are under the age of 30 before the beginning of the plan year; (2) have been certified as exempt from the individual responsibility requirement because coverage is unaffordable; or (3) have been certified as experiencing a hardship for obtaining coverage under a qualified health plan (QHP).

Section 1311(c) of the Affordable Care Act provides the Secretary the authority to issue regulations to establish criteria for the certification of QHPs. Among the criteria for certification that the Secretary must establish by regulation is that QHPs ensure a sufficient choice of providers (section 1311(c)(1)(B) of the Affordable Care Act) and include essential community providers that serve predominately low-income, medically underserved individuals (section 1311(c)(1)(C) of the Affordable Care Act). Section 1311(d)(4)(A) of the Affordable Care Act requires the Exchange to implement procedures for the certification, recertification, and decertification of health plans as QHPs, consistent with guidelines developed by the Secretary under section 1311(c) of the Affordable Care Act. Section 1311(e)(1) of the Affordable Care Act grants the Exchange the authority to certify a health plan as a QHP if the health plan meets the Secretary's requirements for certification issued under section 1311(c) of the Affordable Care Act, and the Exchange determines that making the plan available through the Exchange is in the interests of qualified individuals and qualified employers in the State. Section 1311(c)(6)(C) of the Affordable Care Act directs the Secretary to require an Exchange to provide for special enrollment periods (SEPs) and section 1311(c)(6)(D) of the Affordable Care Act directs the Secretary to require an Exchange to provide for American Indians and Alaska Natives (AI/AN), as defined by section 4 of the Indian Health Care Improvement Act.

Section 1311(d)(3)(B) of the Affordable Care Act permits a State, at its option, to require QHPs to cover benefits in addition to EHB. This section also requires a State to make payments, either to the individual enrollee or to the issuer on behalf of the enrollee, to defray the cost of these additional State-required benefits.

Section 1312(c) of the Affordable Care Act generally requires a health insurance issuer to consider all enrollees in all health plans (except grandfathered health plans) offered by such issuer to be members of a single risk pool for each of its individual and small group markets. States have the option to merge the individual and small group market risk pools under section 1312(c)(3) of the Affordable Care Act.

Section 1312(e) of the Affordable Care Act provides the Secretary with the authority to establish procedures under which a State may allow agents or brokers to (1) enroll qualified individuals and qualified employers in QHPs offered through Exchanges and (2) assist individuals in applying for advance payments of the premium tax credit (APTC) and cost-sharing reductions (CSRs) for QHPs sold through an Exchange.

Sections 1313 and 1321 of the Affordable Care Act provide the Secretary with the authority to oversee the financial integrity of State Exchanges, their compliance with HHS standards, and the efficient and non-discriminatory administration of State Exchange activities. Section 1313(a)(5)(A) of the Affordable Care Act provides the Secretary with the authority to implement any measure or procedure that the Secretary determines is appropriate to reduce fraud and abuse in the administration of the Exchanges. Section 1321 of the Affordable Care Act provides for State flexibility in the operation and enforcement of Exchanges and related requirements.

Section 1321(a) of the Affordable Care Act provides broad authority for the Secretary to establish standards and regulations to implement the statutory requirements related to Exchanges, QHPs and other components of title I of the Affordable Care Act, including such other requirements as the Secretary determines appropriate. When operating an FFE under section 1321(c)(1) of the Affordable Care Act, HHS has the authority under sections 1321(c)(1) and 1311(d)(5)(A) of the Affordable Care Act to collect and spend user fees. Office of Management and Budget (OMB) Circular No. A-25 Revised establishes Federal policy regarding user fees and specifies that a user charge will be assessed against each identifiable recipient for special benefits derived from Federal activities beyond those received by the public.[4]

Section 1321(d) of the Affordable Care Act provides that nothing in title I of the Affordable Care Act must be construed to preempt any State law that does not prevent the application of title I of the Affordable Care Act. Section 1311(k) of the Affordable Care Act specifies that Exchanges may not establish rules that

( printed page 29528)

conflict with or prevent the application of regulations issued by the Secretary.

Section 1331 of the Affordable Care Act provides States with an option to establish a BHP. In the States that elect to operate a BHP, the BHP makes affordable health benefits coverage available for individuals under age 65 with household incomes between 133 percent and 200 percent of the FPL who are not otherwise eligible for Medicaid, the Children's Health Insurance Program (CHIP), or affordable employer-sponsored coverage, or for noncitizens whose income is equal to or below 200 percent of FPL but are ineligible for Medicaid benefits that at a minimum consist of the EHB described in section 1302(b) of the Affordable Care Act. For those States that have expanded Medicaid coverage under section 1902(a)(10)(A)(i)(VIII) of the Social Security Act (the Act), the lower income threshold for BHP eligibility is effectively 138 percent of the FPL due to the application of a required 5 percent income disregard in determining the upper limits of Medicaid income eligibility (section 1902(e)(14)(I) of the Act).

Section 1343 of the Affordable Care Act establishes a permanent risk adjustment program to provide payments to health insurance issuers that attract higher-than-average risk enrollees, such as those with chronic conditions, funded by charges collected from those issuers that attract lower-than-average risk enrollees, thereby reducing incentives for issuers to avoid higher-risk enrollees. Section 1343(b) of the Affordable Care Act provides that the Secretary, in consultation with States, shall establish criteria and methods to be used in carrying out the risk adjustment activities under this section. Consistent with section 1321(c) of the Affordable Care Act, the Secretary is responsible for operating the HHS risk adjustment program in any State that fails to do so.[5]

Section 1401(a) of the Affordable Care Act added section 36B to the Internal Revenue Code (the Code), which, among other things, requires that a taxpayer reconcile APTC for a year of coverage with the amount of the premium tax credit (PTC) the taxpayer is allowed for the year.

Section 1402 of the Affordable Care Act provides for, among other things, reductions in cost sharing for EHB for qualified low- and moderate-income enrollees in silver-level QHPs offered through the individual market Exchanges. This section also provides for reductions in cost sharing for American Indians and Alaska Natives (AI/AN) enrolled in QHPs at any metal level.

Section 1411(f) of the Affordable Care Act requires the Secretary, in consultation with the Secretary of the Treasury and the Secretary of Homeland Security, and the Commissioner of Social Security, to establish procedures for hearing and making decisions governing appeals of Exchange eligibility determinations. Section 1411(f)(1)(B) of the Affordable Care Act requires the Secretary to establish procedures to redetermine eligibility on a periodic basis, in appropriate circumstances, including eligibility to purchase a QHP through the Exchange and for APTC and CSRs.

Section 1411(g) of the Affordable Care Act allows the use of applicant information only for the limited purpose of, and to the extent necessary for, ensuring the efficient operation of the Exchange, including by verifying eligibility to enroll through the Exchange and for APTC and CSRs, and limits the disclosure of such information.

Section 1413 of the Affordable Care Act directs the Secretary to establish, subject to minimum requirements, a streamlined enrollment process for enrollment in QHPs and all insurance affordability programs.

Section 2718 of the PHS Act, as added by the Affordable Care Act, generally requires health insurance issuers to submit an annual medical loss ratio (MLR) report to HHS and provide rebates to enrollees if the issuers do not achieve specified MLR thresholds.

Section 5000A of the Code, as added by section 1501(b) of the Affordable Care Act, requires individuals to have minimum essential coverage (MEC) for each month, qualify for an exemption, or make an individual shared responsibility payment. Under the Tax Cuts and Jobs Act, which was enacted on December 22, 2017, the individual shared responsibility payment is reduced to $0, effective for months beginning after December 31, 2018. Notwithstanding that reduction, certain exemptions are still relevant to determine whether individuals aged 30 and above qualify to enroll in catastrophic coverage under §§ 155.305(h) and 156.155(a)(5).

Section 5000A(e) of the Code defines exemptions from the individual shared responsibility penalty. Section 5000A(e)(5) of the Code defines a hardship exemption as a situation in which an individual experiences difficulty obtaining QHP coverage and provides the HHS Secretary the authority to determine whether an individual has experienced a hardship.

Section 71301 of the WFTC legislation amends 26 U.S.C. 36B(e), effective for plan years beginning on or after January 1, 2027, to provide that a PTC is allowed for the coverage of a lawfully present non-citizen only if the non-citizen is an “eligible alien.”

Section 71302 of the WFTC legislation removes subparagraph (B) of 26 U.S.C. 36B(c)(1), eliminating PTC eligibility for lawfully present individuals with income below 100 percent of the FPL who are ineligible for Medicaid due to their immigration status. Section 71302 is effective for taxable years beginning after December 31, 2025.

Section 71303 of the WFTC legislation, effective to taxable years beginning after December 31, 2027, amends the definition of coverage month such that it would be imprudent to maintain a 2-year failure to file and reconcile (FTR) policy for 2028 and beyond, but it would not be legally prohibited to do so.

Section 71304 of the WFTC legislation amends section 36B of the Code, effective for plan years beginning after December 31, 2025, such that a plan is not considered a QHP, and therefore no PTC is allowed for coverage under the plan, if the plan is enrolled in through a special enrollment period (SEP) that is based solely on the relationship of an individual's expected income to the FPL and not on a change in circumstance (an “income-based SEP”). This provision is effective January 1, 2026.

Section 71305 of the WFTC legislation eliminates, effective for taxable years beginning after December 31, 2025, APTC repayment limits and requires individuals whose APTC exceeds their PTC to increase their tax liability by the amount of the excess.

Section 71307 of the WFTC legislation amends the definition of “high deductible health plan” in section 223(c)(2) of the Code to include bronze and catastrophic plans available as individual coverage through an Exchange, effective for months beginning after December 31, 2025.

1. Premium Stabilization Programs

The premium stabilization programs refer to the risk adjustment, risk corridors, and reinsurance programs established by the Affordable Care Act.

6

( printed page 29529)

For past rulemaking, we refer readers to the following rules:

In the March 23, 2012Federal Register

(77 FR 17219) (Premium Stabilization Rule), we implemented the premium stabilization programs.

In the March 11, 2013Federal Register

(78 FR 15409) (2014 Payment Notice), we finalized the benefit and payment parameters for the 2014 benefit year to expand the provisions related to the premium stabilization programs and set forth payment parameters in those programs.

In the October 30, 2013Federal Register

(78 FR 65046), we finalized the modification to the HHS risk adjustment methodology related to community rating States.

In the November 6, 2013Federal Register

(78 FR 66653), we issued a correcting amendment to the 2014 Payment Notice to address how an enrollee's age for the risk score calculation would be determined under the HHS risk adjustment methodology.

In the March 11, 2014Federal Register

(79 FR 13743) (2015 Payment Notice), we finalized the benefit and payment parameters for the 2015 benefit year to expand the provisions related to the premium stabilization programs, set forth certain oversight provisions, and establish payment parameters in those programs.

In the May 27, 2014Federal Register

(79 FR 30240), we announced the fiscal year 2015 sequestration rate for the HHS-operated risk adjustment program.

In the February 27, 2015Federal Register

(80 FR 10750) (2016 Payment Notice), we finalized the benefit and payment parameters for the 2016 benefit year to expand the provisions related to the premium stabilization programs, set forth certain oversight provisions, and establish the payment parameters in those programs.

In the March 8, 2016Federal Register

(81 FR 12203) (2017 Payment Notice), we finalized the benefit and payment parameters for the 2017 benefit year to expand the provisions related to the premium stabilization programs, set forth certain oversight provisions, and establish the payment parameters in those programs.

In the December 22, 2016Federal Register

(81 FR 94058) (2018 Payment Notice), we finalized the benefit and payment parameters for the 2018 benefit year, added the high-cost risk pool parameters to the HHS risk adjustment methodology, incorporated prescription drug factors in the adult models, established enrollment duration factors for the adult models, and finalized policies related to the collection and use of enrollee-level External Data Gathering Environment (EDGE) data.

In the April 17, 2018Federal Register

(83 FR 16930) (2019 Payment Notice), we finalized the benefit and payment parameters for the 2019 benefit year, created the State flexibility framework permitting States to request a reduction in risk adjustment State transfers calculated by HHS, and adopted a new error rate methodology for HHS-RADV adjustments to transfers.

In the May 11, 2018Federal Register

(83 FR 21925), we issued a correction to the 2019 HHS risk adjustment coefficients in the 2019 Payment Notice.

On July 27, 2018, consistent with45 CFR 153.320(b)(1)(i), we updated the 2019 benefit year final HHS risk adjustment model coefficients to reflect an additional recalibration related to an update to the 2016 enrollee-level EDGE data set.[7]

In the July 30, 2018Federal Register

(83 FR 36456), we adopted the 2017 benefit year HHS risk adjustment methodology as established in the final rules issued in the March 23, 2012 (77 FR 17220 through 17252) and March 8, 2016 (81 FR 12204 through 12352) editions of the

Federal Register

. The final rule set forth an additional explanation of the rationale supporting the use of Statewide average premium in the State payment transfer formula for the 2017 benefit year, including the reasons why the program is operated by HHS in a budget-neutral manner. The final rule also permitted HHS to resume 2017 benefit year HHS risk adjustment payments and charges. HHS also provided guidance as to the operation of the HHS-operated risk adjustment program for the 2017 benefit year in light of the publication of the final rule.

In the December 10, 2018Federal Register

(83 FR 63419), we adopted the 2018 benefit year HHS risk adjustment methodology as established in the final rules issued in the March 23, 2012 (77 FR 17219) and the December 22, 2016 (81 FR 94058) editions of the

Federal Register

. In the rule, we set forth an additional explanation of the rationale supporting the use of Statewide average premium in the State payment transfer formula for the 2018 benefit year, including the reasons why the program is operated by HHS in a budget-neutral manner.

In the April 25, 2019Federal Register

(84 FR 17454) (2020 Payment Notice), we finalized the benefit and payment parameters for the 2020 benefit year, as well as the policies related to making the enrollee-level EDGE data available as a limited data set for research purposes and expanding the HHS uses of the enrollee-level EDGE data, approval of the request from Alabama to reduce HHS risk adjustment transfers by 50 percent in the small group market for the 2020 benefit year, and updates to HHS-RADV program requirements.

On May 12, 2020, consistent with § 153.320(b)(1)(i), we issued the 2021 Benefit Year Final HHS Risk Adjustment Model Coefficients on the CCIIO website.[8]

In the May 14, 2020Federal Register

(85 FR 29164) (2021 Payment Notice), we finalized the benefit and payment parameters for the 2021 benefit year, as well as adopted updates to the HHS risk adjustment models' hierarchical condition categories (HCCs) to transition to the 10th revision of the International Classification of Diseases (ICD-10) codes, approved the request from Alabama to reduce HHS risk adjustment transfers by 50 percent in the small group market for the 2021 benefit year, and modified the outlier identification process under the HHS-RADV program.

In the December 1, 2020Federal Register

(85 FR 76979) (Amendments to the HHS-Operated Risk Adjustment Data Validation Under the Patient Protection and Affordable Care Act's HHS-Operated Risk Adjustment Program (2020 HHS-RADV Amendments Rule)), we adopted the creation and application of Super HCCs in the sorting step that assigns HCCs to failure rate groups, finalized a sliding scale adjustment in HHS-RADV error rate calculation, and added a constraint for negative error rate outliers with a negative error rate. We also established a transition from the prospective application of HHS-RADV adjustments to apply HHS-RADV results to risk scores from the same benefit year as that being audited.

In the May 5, 2021Federal Register

(86 FR 24140) (part 2 of the 2022 Payment Notice), we finalized a subset of proposals from the December 4, 2020

Federal Register

(85 FR 78572) (the 2022 Payment Notice proposed rule), including policy and regulatory revisions related to the HHS-operated risk adjustment program, finalization of the benefit and payment parameters for the 2022 benefit year, and approval of

( printed page 29530)

the request from Alabama to reduce HHS risk adjustment transfers by 50 percent in the individual and small group markets for the 2022 benefit year. In addition, this final rule established a revised schedule of collections for HHS-RADV and updated the provisions regulating second validation audit (SVA) and initial validation audit (IVA) entities.

On July 19, 2021, consistent with § 153.320(b)(1)(i), we released Updated 2022 Benefit Year Final HHS Risk Adjustment Model Coefficients on the CCIIO website, announcing some minor revisions to the 2022 benefit year final HHS risk adjustment adult model coefficients.[9]

In the May 6, 2022Federal Register

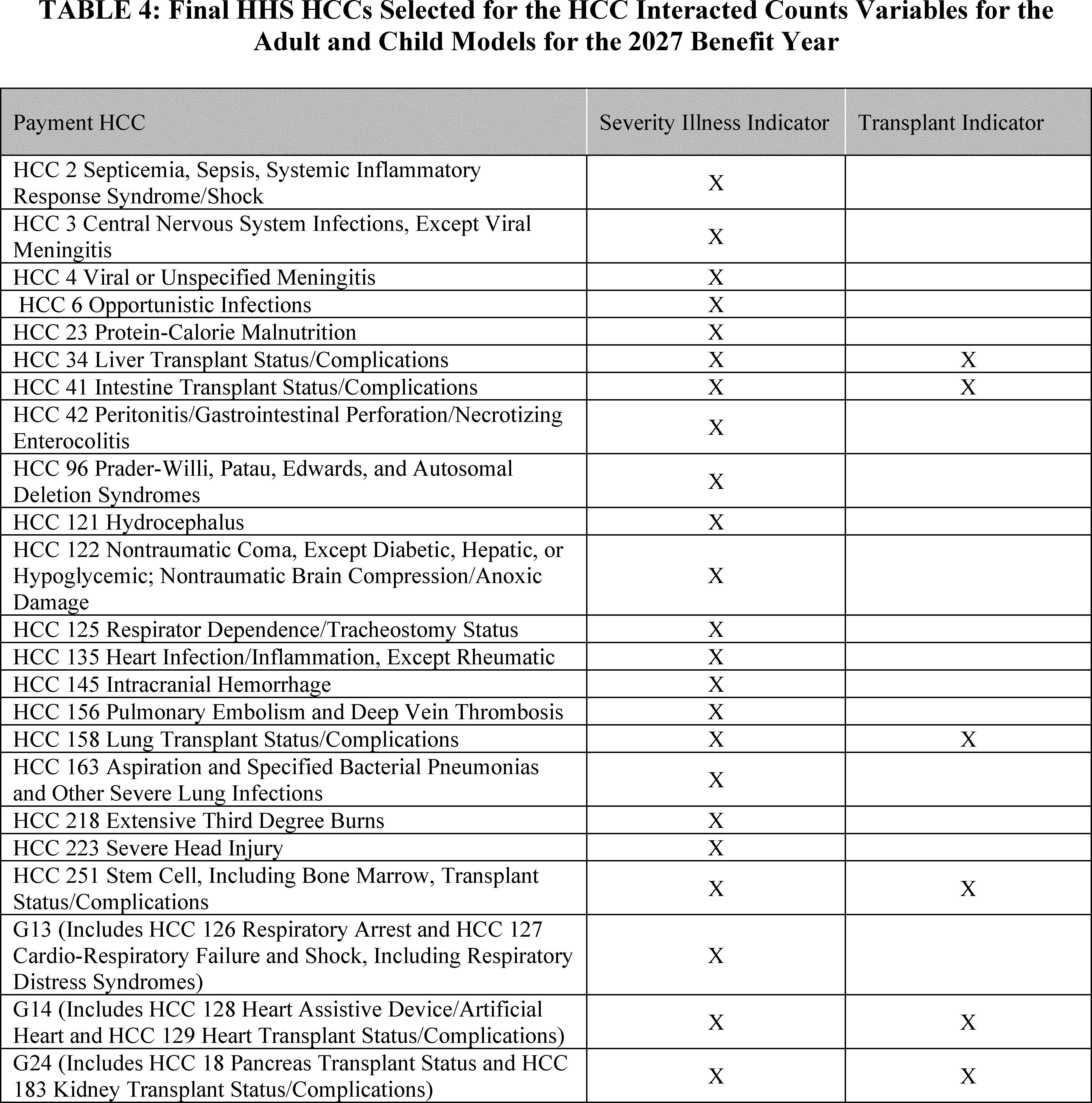

(87 FR 27208) (2023 Payment Notice), we finalized revisions related to the HHS-operated risk adjustment program, including the benefit and payment parameters for the 2023 benefit year, HHS risk adjustment model recalibration, and policies related to the collection and extraction of enrollee-level EDGE data. We also finalized the adoption of the interacted HCC count specification for the adult and child models, along with modified enrollment duration factors for the adult models, beginning with the 2023 benefit year.[10]

We also repealed the ability for States, other than prior participants, to request a reduction in HHS risk adjustment State transfers starting with the 2024 benefit year. We approved a 25 percent reduction to 2023 benefit year HHS risk adjustment transfers in Alabama's individual market and a 10 percent reduction to 2023 benefit year HHS risk adjustment transfers in Alabama's small group market. We finalized further refinements to the HHS-RADV error rate calculation methodology beginning with the 2021 benefit year.

In the April 27, 2023Federal Register

(88 FR 25740) (2024 Payment Notice), we finalized the benefit and payment parameters for the 2024 benefit year, amended the EDGE discrepancy materiality threshold and data collection requirements, and reduced the risk adjustment user fee. For the 2024 benefit year, we approved 50 percent reductions to HHS risk adjustment transfers for Alabama's individual and small group markets and repealed prior participant States' ability to request reductions of their risk adjustment transfers for the 2025 benefit year and beyond. We finalized refinements to HHS-RADV program requirements, such as shortening the window to confirm SVA findings or file a discrepancy report, changing the HHS-RADV materiality threshold for random and targeted sampling, and no longer exempting exiting issuers from adjustments to risk scores and HHS risk adjustment transfers when they are negative error rate outliers. We announced the discontinuance of the Lifelong Permanent Condition List and Non-EDGE Claims in HHS-RADV beginning with the 2022 benefit year.

In the April 15, 2024Federal Register

(89 FR 26218) (2025 Payment Notice), we finalized the benefit and payment parameters for the 2025 benefit year, including the 2025 risk adjustment models and updated the adjustment factors for the receipt of CSRs for the AI/AN subpopulation who are enrolled in zero and limited cost-sharing plans to improve prediction in the HHS risk adjustment models. In addition, we finalized that in certain cases, we may require a corrective action plan (CAP) to address an observation identified in an HHS risk adjustment program audit.

In the January 15, 2025Federal Register

(90 FR 4424) (2026 Payment Notice), we finalized the benefit and payment parameters for the 2026 benefit year, including the 2026 risk adjustment models and updated the adjustment factors, phased out the market pricing adjustment to the plan liability associated with Hepatitis C drugs, and incorporated of pre-exposure prophylaxis (PrEP) as an Affiliated Cost Factor (ACF) starting with the 2026 benefit year. Beginning with the 2025 benefit year, we excluded enrollees without HCCs from the IVA sample, removed the Finite Population Correction (FPC) from the IVA sampling methodology, and replaced the source of the Neyman allocation data used for HHS-RADV sampling with the most recent 3 consecutive years of HHS-RADV data. Beginning with the 2024 benefit year, we modified the SVA pairwise means test and increased the initial SVA subsample size. At § 156.1220(a), we established a new materiality threshold for HHS-RADV appeals.

2. Program Integrity

We have finalized program integrity standards related to the Exchanges and premium stabilization programs in two rules: the “first Program Integrity Rule” issued in the August 30, 2013

Federal Register

(78 FR 54069), and the “second Program Integrity Rule” issued in the October 30, 2013

Federal Register

(78 FR 65045). We also refer readers to the 2019 Patient Protection and Affordable Care Act; Exchange Program Integrity final rule (2019 Program Integrity Rule) issued in the December 27, 2019

Federal Register

(84 FR 71674), as well as the Patient Protection and Affordable Care Act; Marketplace Integrity and Affordability final rule (2025 Marketplace Integrity and Affordability final rule) issued in the June 25, 2025

Federal Register

(90 FR 27074).

In the May 6, 2022

Federal Register

(87 FR 27208) (2023 Payment Notice), we finalized policies to address certain agent, broker, and web-broker practices and conduct. In the April 27, 2023

Federal Register

(88 FR 25740) (2024 Payment Notice), we implemented the improper payment pre-testing and assessment (IPPTA) requirements for State Exchanges to ensure adherence to the Payment Integrity Information Act of 2019. In addition, we finalized allowing additional time for HHS to review evidence submitted by agents and brokers to rebut allegations pertaining to Exchange Agreement suspensions or terminations. We also introduced consent and eligibility application documentation requirements for agents, brokers, and web-brokers that assist Exchange consumers in FFE and SBE-FP States.

In the 2025 Payment Notice, issued in the April 15, 2024

Federal Register

(89 FR 26218), we finalized that the CMS Administrator is the entity responsible for handling requests by agents, brokers, and web-brokers for reconsideration of HHS' decision to terminate their Exchange agreement(s) for cause. We also finalized changes to §§ 155.220 and 155.221 to apply certain standards to web-brokers and Direct Enrollment (DE) entities assisting consumers and applicants across all Exchanges. In the January 15, 2025

Federal Register

(90 FR 4424) (2026 Payment Notice), we addressed our authority to investigate and undertake compliance reviews and enforcement actions occurring at the insurance agency level to hold lead agents of insurance agencies accountable. We also finalized changes to § 155.220(k)(3) to reflect our authority to suspend an agent's or broker's ability to transact information with the Exchange in certain circumstances until the incident, breach, or noncompliance are remedied or sufficiently mitigated to HHS' satisfaction.

( printed page 29531)

3. Market Rules

In the February 27, 2013

Federal Register

(78 FR 13406), we issued the health insurance market rules, including provisions related to the single risk pool. We codified that, for catastrophic plans, issuers may make a plan-specific adjustment to the market-wide index rate based on the expected impact of the specific eligibility categories for those plans. This plan-specific adjustment would be uniform across all of an issuer's catastrophic plans (that is, risk across all catastrophic plans must be pooled).

In that rule, we also codified that a health plan is a catastrophic plan if it: (1) meets all applicable requirements for health insurance coverage in the individual market; (2) does not offer coverage at the bronze, silver, gold, or platinum levels of coverage (3) does not provide coverage of essential health benefits until the enrolled individual reaches the annual limitation in cost sharing; and (4) covers at least three primary care visits per year before reaching the deductible. A catastrophic plan may not impose any cost-sharing requirements for preventive services identified in section 2713 of the PHS Act. We also codified the statutory eligibility criteria identified in section 1302(e)(2) of the Affordable Care Act.

We amended requirements related to index rates under the single risk pool provision in a final rule issued in the July 2, 2013

Federal Register

(78 FR 39870). In the October 30, 2013

Federal Register

(78 FR 65046), we clarified when issuers may establish and update premium rates. In the March 8, 2016

Federal Register

(81 FR 12203), we clarified single risk pool provisions related to student health insurance coverage. We finalized minor adjustments to the single risk pool regulations in the 2018 Payment Notice, issued in the December 22, 2016

Federal Register

(81 FR 94058).

4. Rate Review

In the May 23, 2011

Federal Register

(76 FR 29963) (Rate Review Rule), we implemented a rate review program. We amended the provisions of the Rate Review Rule in final rules published in the September 6, 2011

Federal Register

(76 FR 54969), the February 27, 2013

Federal Register

(78 FR 13405), the May 27, 2014

Federal Register

(79 FR 30239), the February 27, 2015

Federal Register

(80 FR 10749), the March 8, 2016

Federal Register

(81 FR 12203) and the December 22, 2016

Federal Register

(81 FR 94058).

5. Exchanges

We requested comment relating to Exchanges in the August 3, 2010

Federal Register

(75 FR 45584). We issued initial guidance to States on Exchanges on November 18, 2010. In the March 27, 2012

Federal Register

(77 FR 18310) (Exchange Establishment Rule), we implemented the Affordable Insurance Exchanges (Exchanges), consistent with title I of the Affordable Care Act, to provide competitive marketplaces for individuals and small employers to directly compare available private health insurance coverage options based on price, quality, and other factors. This included implementation of components of the Exchanges and standards for eligibility for Exchanges, as well as network adequacy and essential community provider (ECP) certification standards.

In the 2014 Payment Notice and the Amendments to the HHS Notice of Benefit and Payment Parameters for 2014 interim final rule, issued in the March 11, 2013

Federal Register

(78 FR 15541), we set forth standards related to Exchange user fees. We established an adjustment to the FFE user fee in the Coverage of Certain Preventive Services under the Affordable Care Act final rule, issued in the July 2, 2013

Federal Register

(78 FR 39869) (Preventive Services Rule).

In the 2016 Payment Notice, we also set forth the ECP certification standard at § 156.235, with revisions in the 2017 Payment Notice in the March 8, 2016

Federal Register

(81 FR 12203) and the 2018 Payment Notice in the December 22, 2016

Federal Register

(81 FR 94058).

In the 2018 Payment Notice, issued in the December 22, 2016

Federal Register

(81 FR 94058), we set forth the standards for the request for reconsideration of denial of QHP certification specific to the FFEs at § 155.1090.

In an interim final rule, issued in the May 11, 2016

Federal Register

(81 FR 29146), we made amendments to the parameters of certain SEPs (2016 Interim Final Rule).

We finalized these in the 2018 Payment Notice, issued in the December 22, 2016

Federal Register

(81 FR 94058).

In the Market Stabilization final rule, issued in the April 18, 2017

Federal Register

(82 FR 18346), we amended standards relating to SEPs and QHP certification. In the 2019 Payment Notice, issued in the April 17, 2018

Federal Register

(83 FR 16930), we modified parameters around certain SEPs. In the April 25, 2019

Federal Register

(84 FR 17454), the 2020 Payment Notice established a new SEP for certain individuals who become newly eligible for APTC.

In the May 14, 2020

Federal Register

(85 FR 29164) (2021 Payment Notice), we finalized revisions to the parameters of SEPs and the quality rating information display standards for State Exchanges and amended the periodic data matching requirements.

In the January 19, 2021

Federal Register

(86 FR 6138) (part 1 of the 2022 Payment Notice), we finalized only a subset of the proposals in the 2022 Payment Notice proposed rule. In the May 5, 2021

Federal Register

(86 FR 24140), we issued part 2 of the 2022 Payment Notice. In the September 27, 2021

Federal Register

(86 FR 53412) (part 3 of the 2022 Payment Notice), in conjunction with the Department of the Treasury, we finalized amendments to certain policies in part 1 of the 2022 Payment Notice.

In the May 6, 2022

Federal Register

(87 FR 27208), we finalized changes to maintain the user fee rate for issuers offering plans through the FFEs and maintain the user fee rate for issuers offering plans through the SBE-FPs for the 2023 benefit year. We also finalized various policies to address certain agent, broker, and web-broker practices and conduct. We also finalized updates to the requirement that all Exchanges conduct SEP verifications.

In the 2024 Payment Notice, issued in the April 27, 2023

Federal Register

(88 FR 25740), we revised Exchange Blueprint approval timelines, lowered the user fee rate for QHPs in the FFEs and SBE-FPs, and amended re-enrollment hierarchies for enrollees. We finalized a requirement that all plans seeking certification on the Exchanges utilize a provider network. We also finalized policies to update FFE and SBE-FP standardized plan options; reduce the risk of plan choice overload on the FFEs and SBE-FPs by limiting the number of non-standardized plan options that issuers may offer through Exchanges on the Federal platform; and ensure correct QHP information. In addition, we amended coverage effective date rules, lengthened the SEP from 60 to 90 days for those who lose Medicaid coverage, and prohibited QHPs on FFEs and SBE-FPs from terminating coverage mid-year for dependent children who reach the applicable maximum age. We also finalized policies on verifying consumer income and permitting door-to-door assisters to solicit consumers. We finalized provider network and ECP policies for QHPs.

( printed page 29532)

In the 2025 Payment Notice, issued in the April 15, 2024

Federal Register

(89 FR 26218), we required a State seeking to operate a State Exchange to first operate an SBE-FP for at least one plan year, revised Exchange Blueprint requirements for States transitioning to a State Exchange, established additional minimum standards for Exchange call center operations, and required an Exchange to operate a centralized eligibility and enrollment platform on its website. We required State Exchanges and State Medicaid agencies to remit payment to HHS for their use of certain income data, amended re-enrollment hierarchies for enrollees enrolled in catastrophic coverage, revised the parameters around a State Exchange adopting an alternative open enrollment period, and extended the availability of an SEP for APTC-eligible qualified individuals with a projected annual household income no greater than 150 percent of the FPL. We finalized provider network adequacy policies applicable to such Exchanges for Plan Year (PY) 2026 and subsequent plan years. We finalized the policy to maintain FFE and SBE-FP standardized plan option metal levels from the 2024 Payment Notice and finalized an exceptions process to the limitation on non-standardized plan options in FFEs and SBE-FPs. We also finalized the requirement for Exchanges to provide notification to enrollees or their tax filers who have failed to file their Federal income taxes and reconcile APTC for 1 tax year.

In the 2026 Payment Notice, published in the January 15, 2025

Federal Register

(90 FR 4424), we codified a timeliness standard for State Exchanges to review and resolve enrollment data inaccuracies at § 155.400(d)(1), finalized at § 155.1000 that an Exchange may deny certification to any plan that does not meet the criteria at § 155.1000(c), and revised the standards at § 155.1090 for an issuer to request a reconsideration of a denial of certification specific to the FFEs. We also finalized publicly releasing certain data and information that State Exchanges submit to HHS, affirmed that CSR loading practices permitted by State regulators are permissible under Federal law to the extent that they are actuarially justified and the issuer does not receive reimbursement for such CSR, and finalized that we will only release a single, final version of the AV Calculator. We also updated the standardized plan option designs for PY 2026 to ensure these plans continue to have AVs within the permissible

de minimis range

for each metal level, amended § 156.201 to require issuers to meaningfully differentiate standardized plan options from one another, and finalized that HHS would conduct ECP certification reviews in States performing plan management functions beginning PY 2026. We also finalized updates affecting the exchanges in the 2025 Marketplace Integrity and Affordability final rule issued in the June 25, 2025

Federal Register

(90 FR 27074).

6. Essential Health Benefits

We established requirements relating to EHB in the Standards Related to Essential Health Benefits, Actuarial Value, and Accreditation Final Rule, which was issued in the February 25, 2013

Federal Register

(78 FR 12834) (EHB Rule). We established at § 156.135(a) that AV is generally to be calculated using the AV Calculator developed and made available by HHS for a given benefit year. In the 2015 Payment Notice (79 FR 13743), we established at § 156.135(g) provisions for updating the AV Calculator in future plan years. In the 2017 Payment Notice (81 FR 12349), we amended the provisions at § 156.135(g) to allow for additional flexibility in our approach and options for updating of the AV Calculator.

In the 2025 Payment Notice, issued in the April 15, 2024

Federal Register

(89 FR 26218), we revised § 155.170(a) to codify that benefits covered in a State's EHB-benchmark plan are not considered in addition to EHB, even if they had been required by State action taking place after December 31, 2011, other than for purposes of compliance with Federal requirements. We finalized three revisions to the standards for State selection of EHB-benchmark plans for benefit years beginning on or after January 1, 2026: revising the typicality standard at § 156.111 for States to demonstrate that their new EHB-benchmark plan provides a scope of benefits that is equal to that of a typical employer plan in the State; revising requirements such that States do not need to submit a formulary drug list as part of their application unless they are changing their prescription drug EHB; and consolidating options for States to change their EHB-benchmark plans. At § 156.115(d), we removed the prohibition on issuers from including routine non-pediatric dental services as an EHB beginning with PY 2027.

In the 2026 Payment Notice, published in the January 15, 2025

Federal Register

(90 FR 4424), we revised § 156.80(d)(2)(i) to require the actuarially justified plan-specific factors by which an issuer may vary premium rates for a particular plan from its market-wide index rate include the AV and cost-sharing design of the plan.

7. Quality Improvement Strategy

We issued regulations in § 155.200(d) to direct Exchanges to evaluate quality improvement strategies, and § 156.200(b) to direct QHP issuers to implement and report on a quality improvement strategy or strategies consistent with section 1311(g) standards as QHP certification criteria for participation in an Exchange. In the 2016 Payment Notice, issued in the February 27, 2015

Federal Register

(80 FR 10749), we finalized regulations at § 156.1130 to establish standards and the associated timeframe for QHP issuers to submit the necessary information to implement quality improvement strategy standards for QHPs offered through an Exchange. In the 2026 Payment Notice, published in the January 15, 2025

Federal Register

(90 FR 4424), we finalized sharing summary-level QIS information publicly on an annual basis beginning on January 1, 2026, with information QHP issuers submit during the PY 2025 QHP Application Period.

8. Medical Loss Ratio (MLR)

We published a request for comment on section 2718 of the PHS Act in the April 14, 2010

Federal Register

(75 FR 19297) and published an interim final rule with a 60-day comment period relating to the MLR program on December 1, 2010 (75 FR 74863). A final rule with a 30-day comment period was published in the December 7, 2011

Federal Register

(76 FR 76573). An interim final rule with a 60-day comment period was published in the December 7, 2011

Federal Register

(76 FR 76595). A final rule was published in the May 16, 2012

Federal Register

(77 FR 28790). The MLR program requirements were amended in final rules published in the March 11, 2014

Federal Register

(79 FR 13743), the May 27, 2014

Federal Register

(79 FR 30339), the February 27, 2015

Federal Register

(80 FR 10749), the March 8, 2016

Federal Register

(81 FR 12203), the December 22, 2016

Federal Register

(81 FR 94183), the April 17, 2018

Federal Register

(83 FR 16930), the May 14, 2020

Federal Register

(85 FR 29164), the May 5, 2021

Federal Register

(86 FR 24140), the May 6, 2022

Federal Register

(87 FR 27208), and the January 15, 2025

Federal Register

(90 FR 4424) and an interim final rule that was published in the September 2, 2020

Federal Register

(85 FR 54820).

( printed page 29533)

We are finalizing updates in 42 CFR 600.5 to align BHP regulations with section 71301 of the WFTC legislation. Section 71301 of the WFTC legislation amended section 36B of the Code to provide that a PTC is allowed for the QHP coverage of a lawfully present noncitizen only if he or she is an “eligible alien,” effective for plan years beginning on or after January 1, 2027. Because Federal BHP payments to States are based in part on the amount of PTC an individual enrolled in the BHP is eligible for and would have qualified for had he or she been enrolled in a QHP through an Exchange, only lawfully present noncitizens who are considered to be “eligible aliens” will generate Federal BHP payments to the State. We are finalizing a new definition of “eligible noncitizen” at 42 CFR 600.5, cross-referencing 45 CFR 155.20.

In accordance with the OMB Report to Congress on the Joint Committee Reductions for Fiscal Year 2026, the HHS-operated risk adjustment program is subject to fiscal year 2026 sequestration.[11]

Therefore, the HHS-operated risk adjustment program will sequester payments made from fiscal year 2026 resources (that is, funds collected during the 2026 fiscal year) at a rate of 5.7 percent.

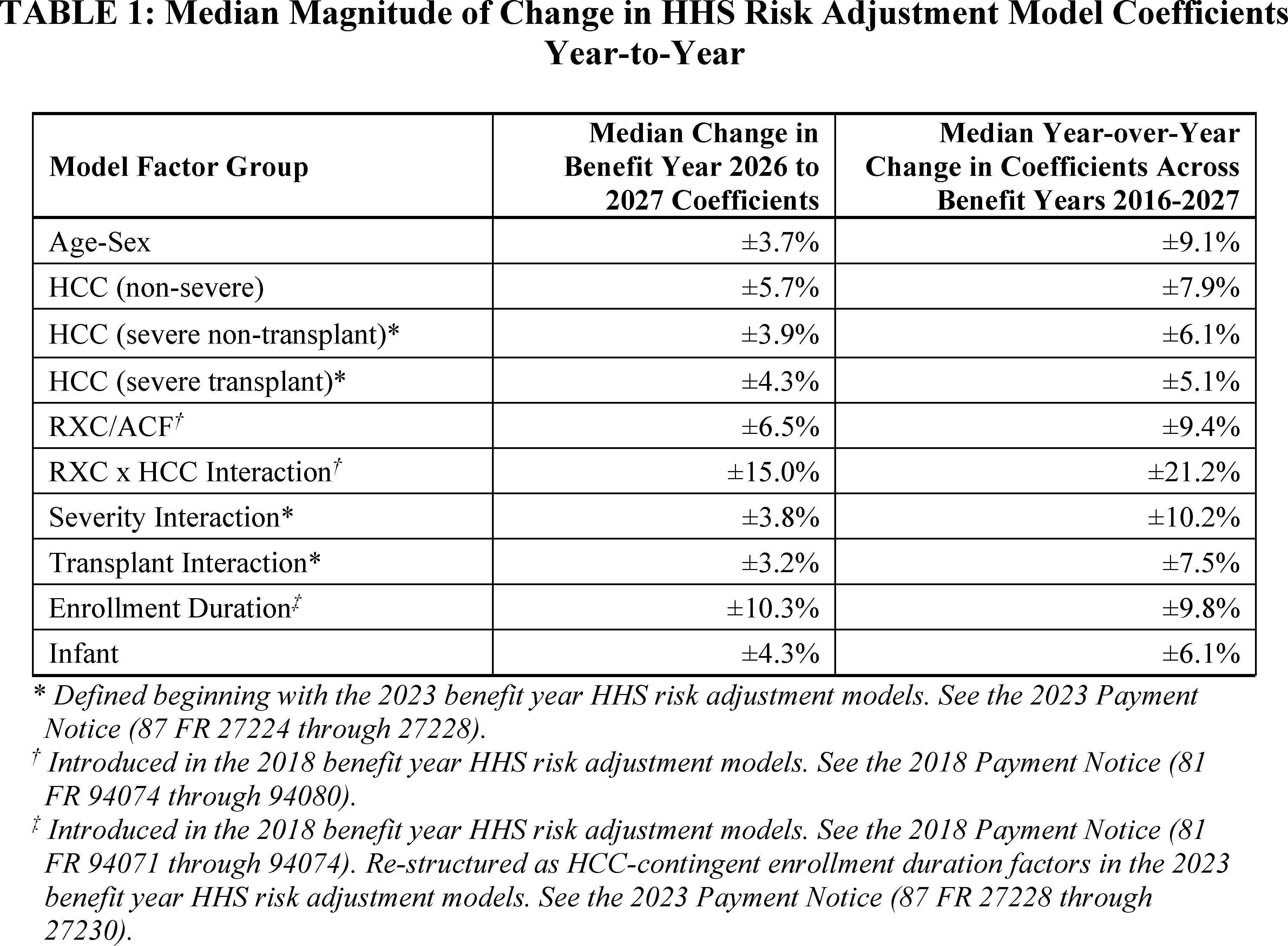

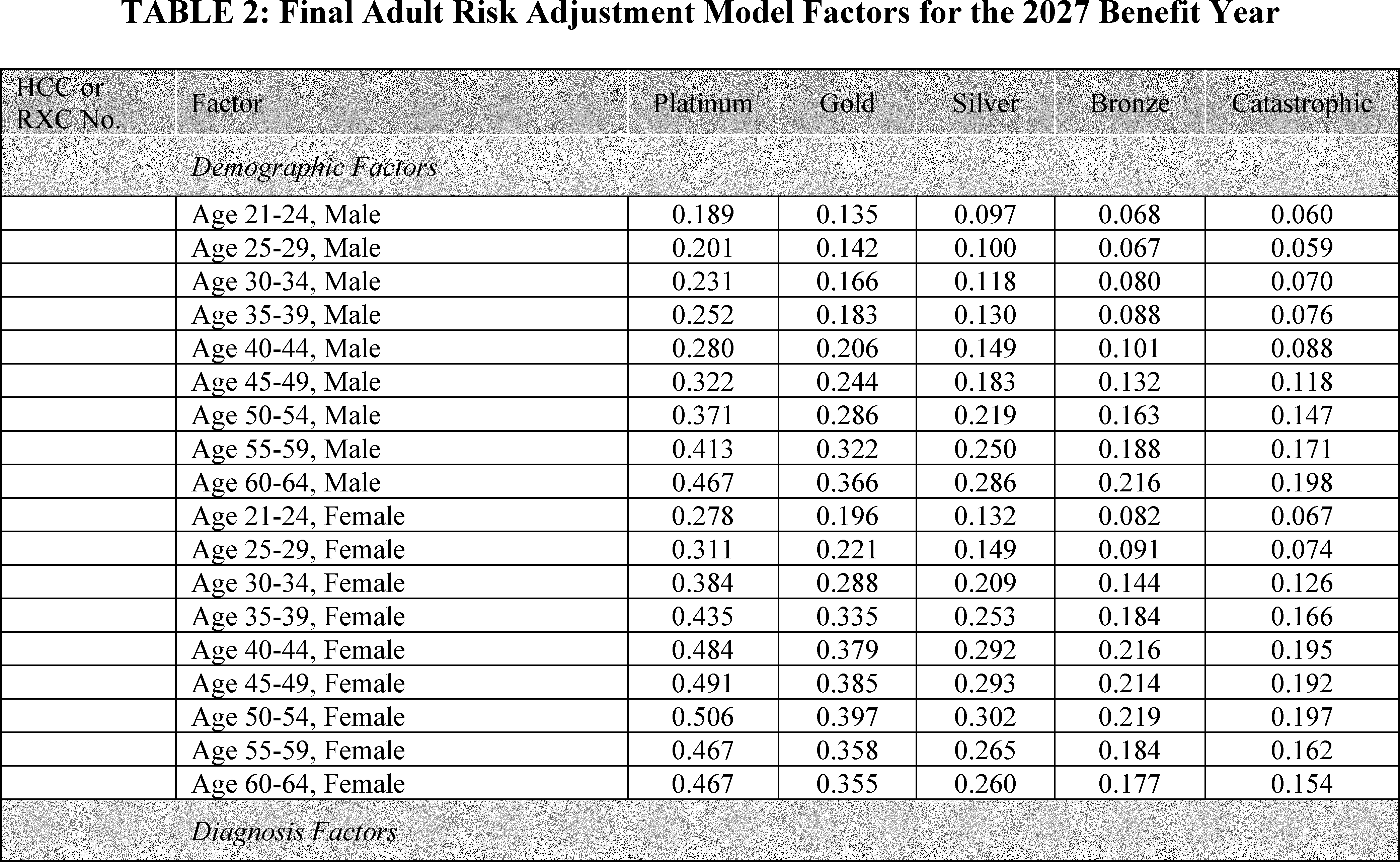

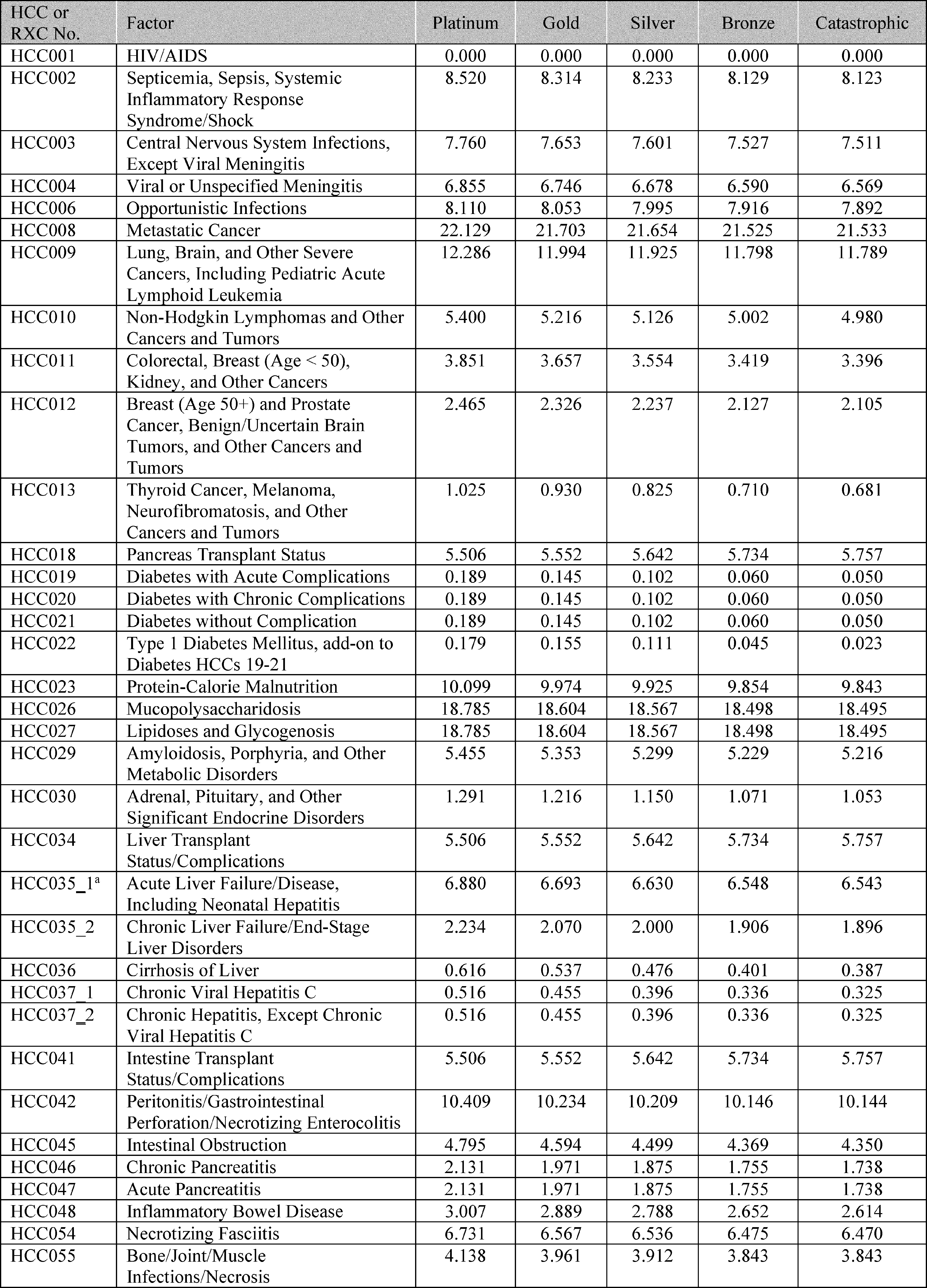

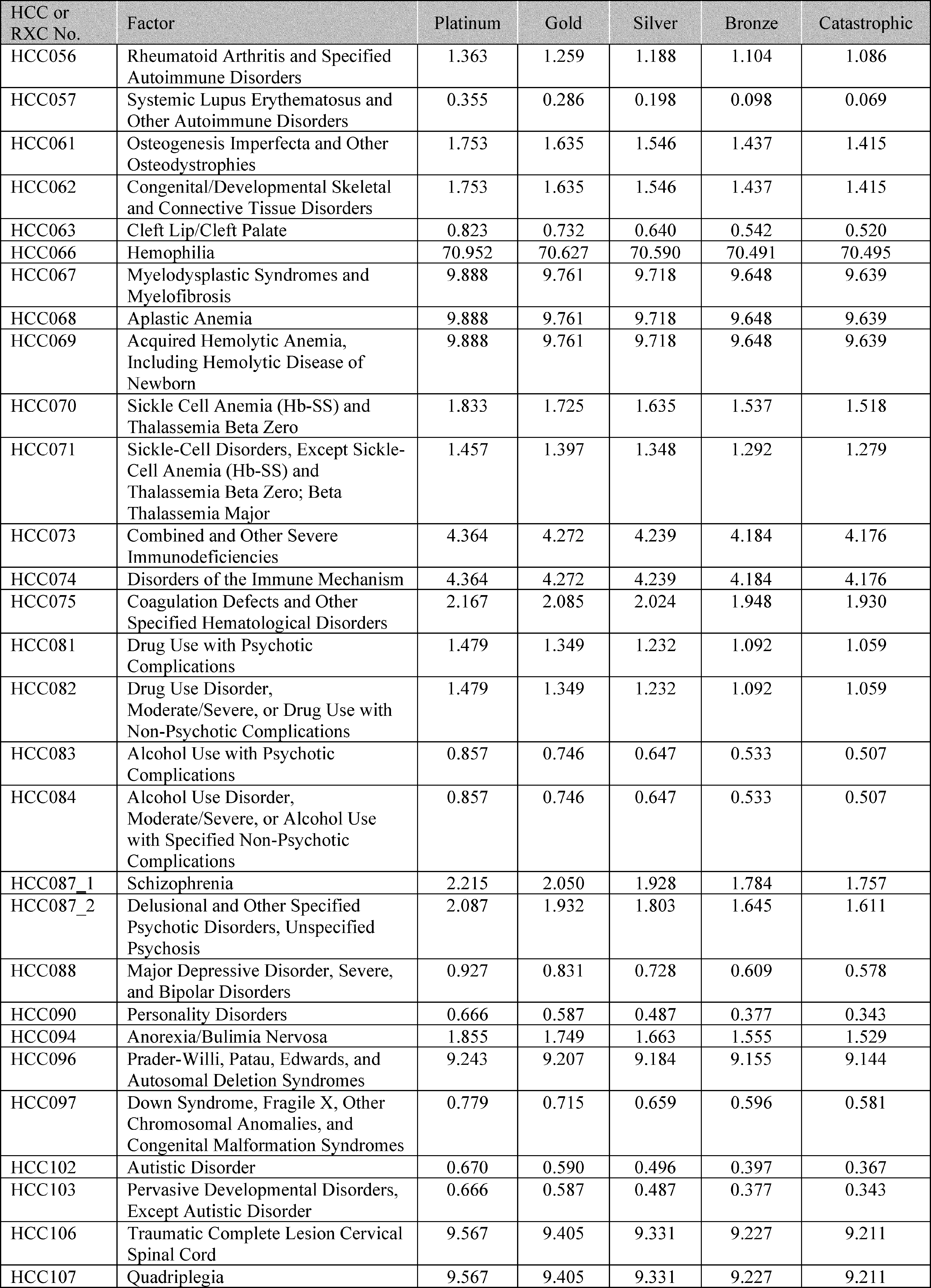

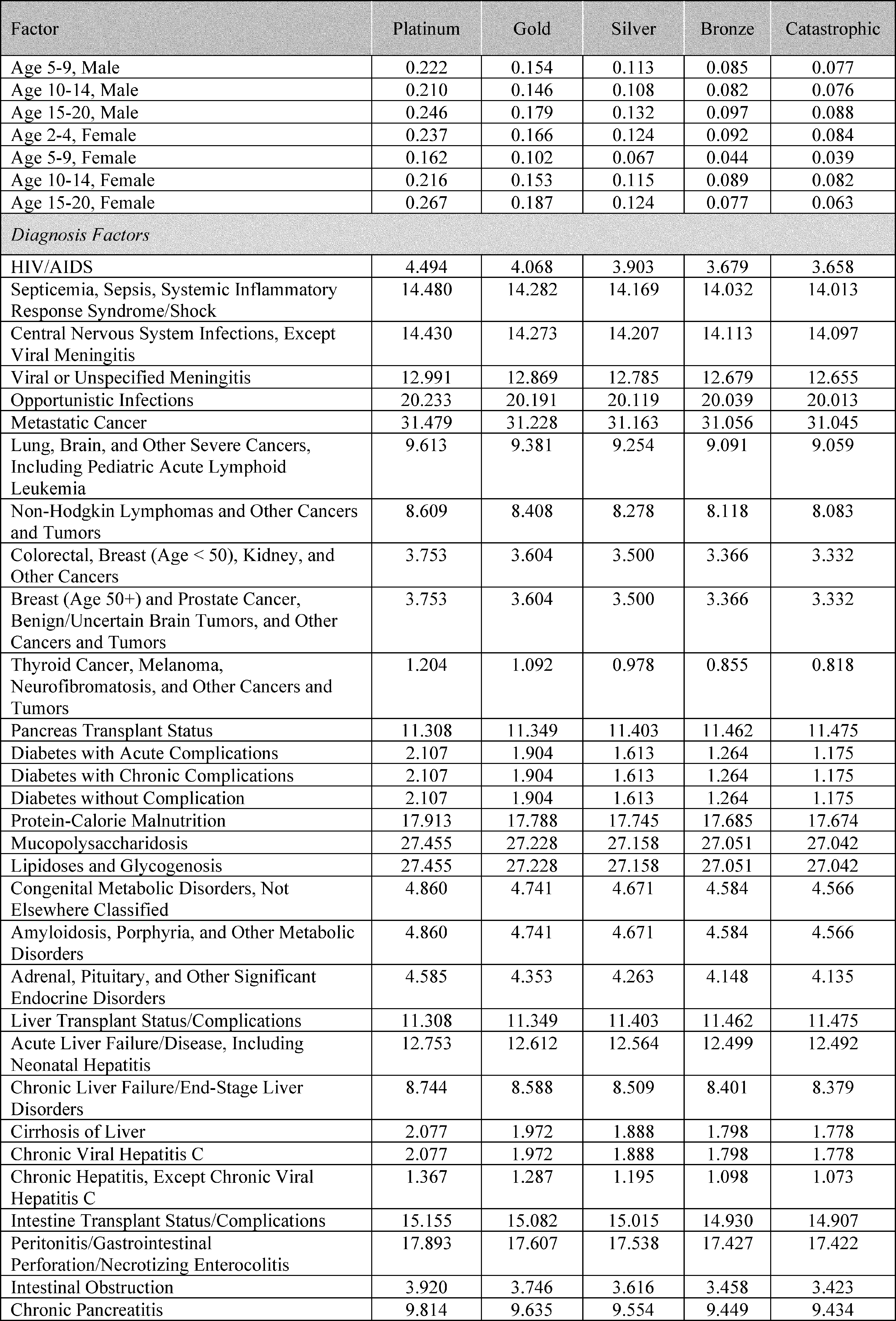

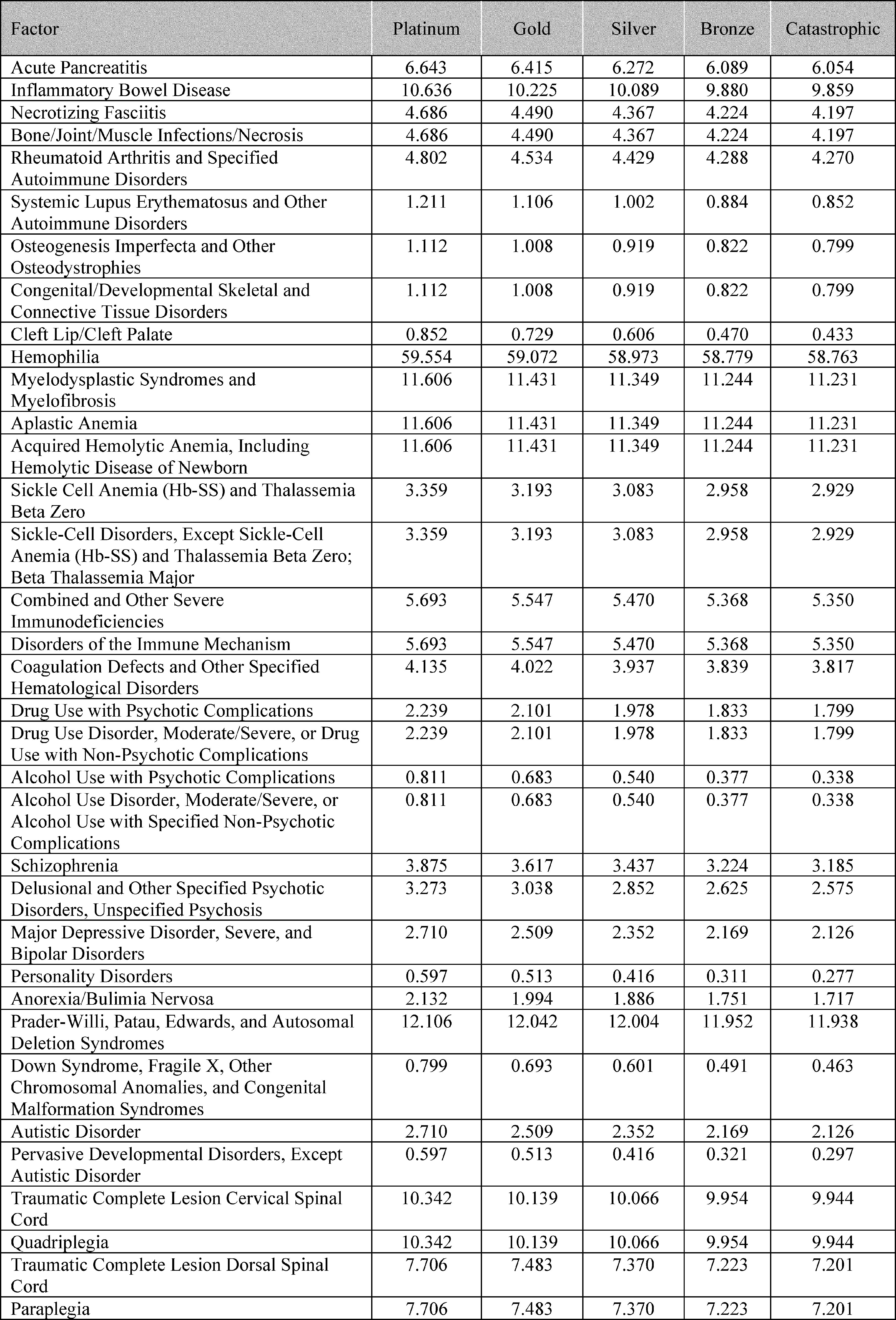

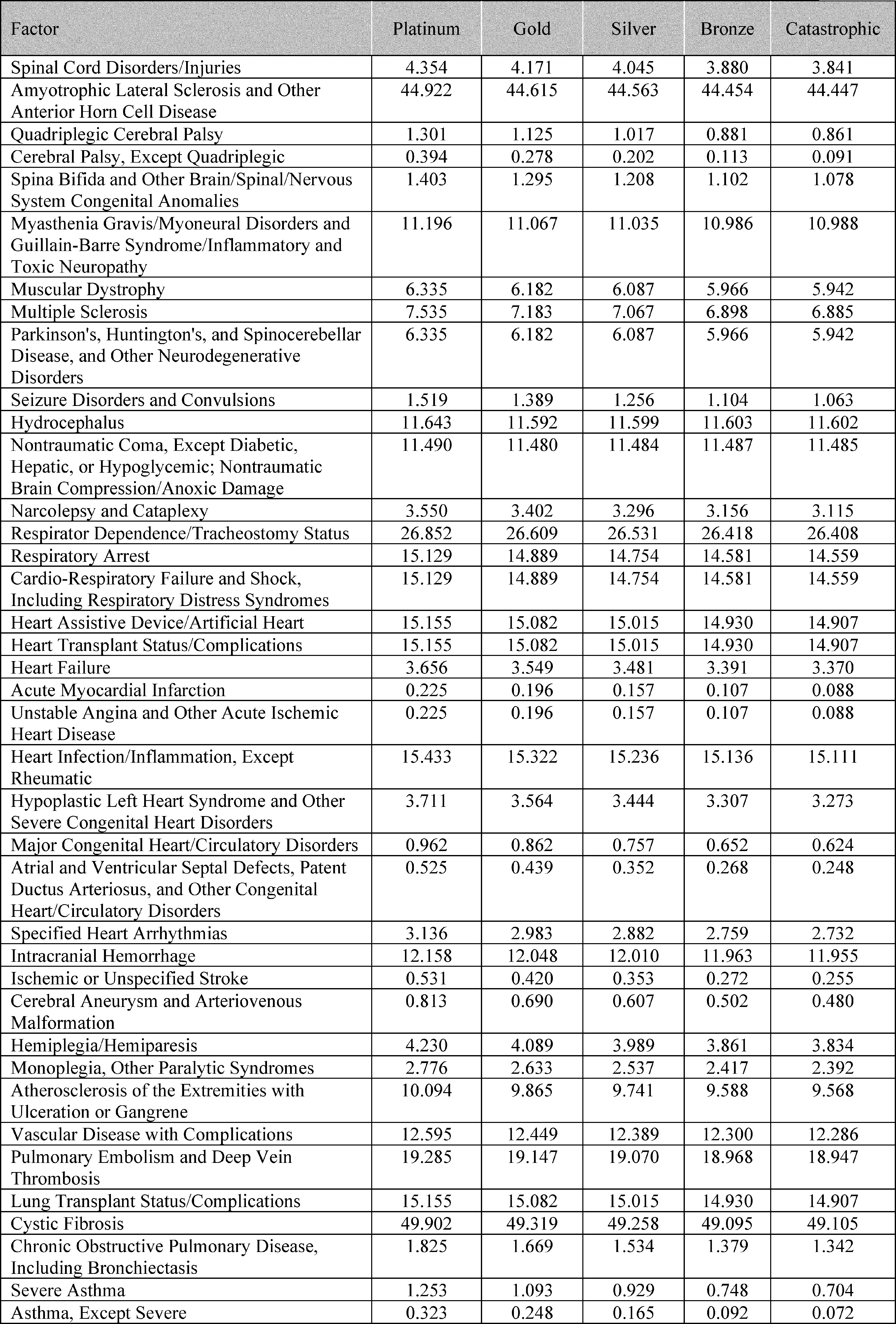

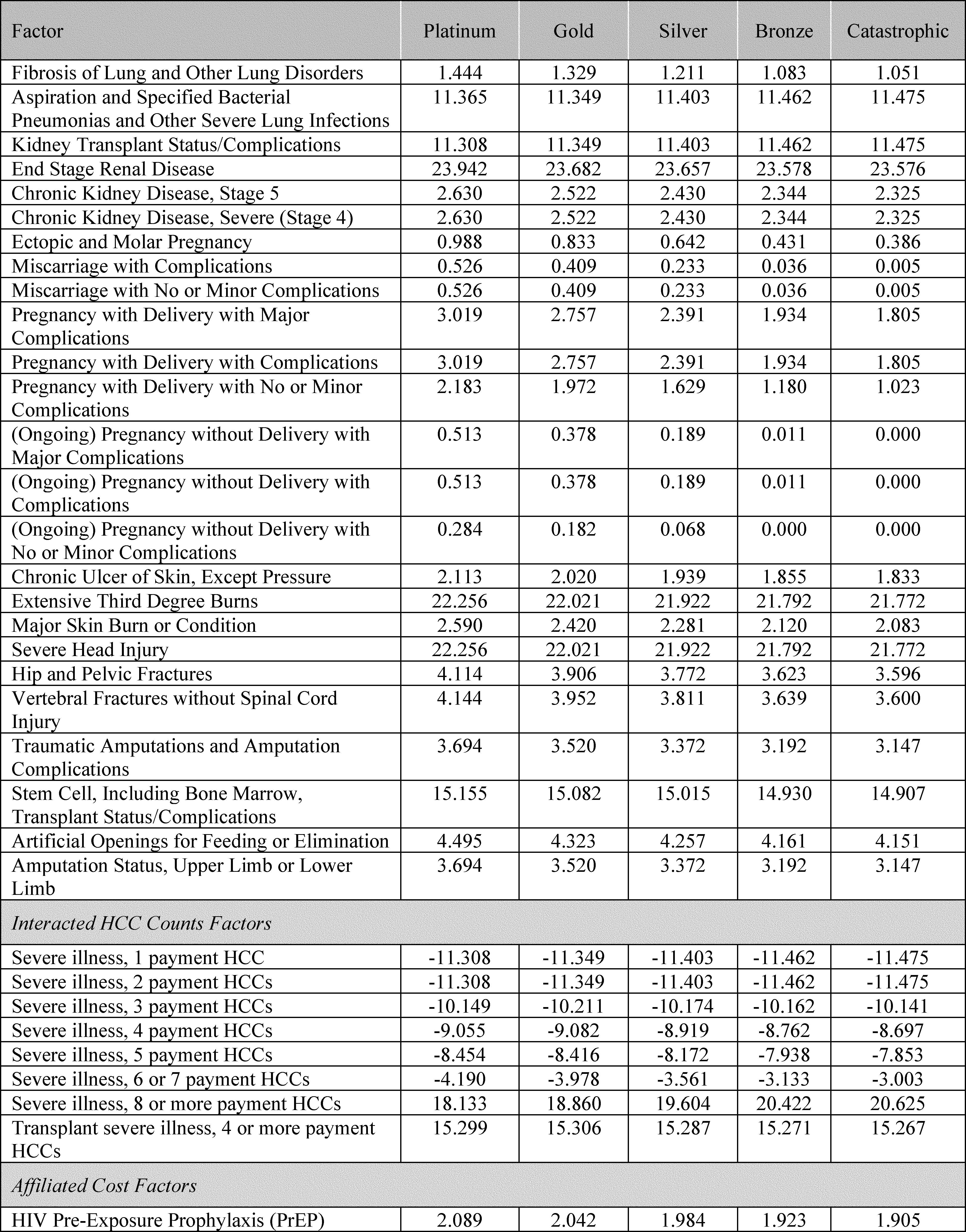

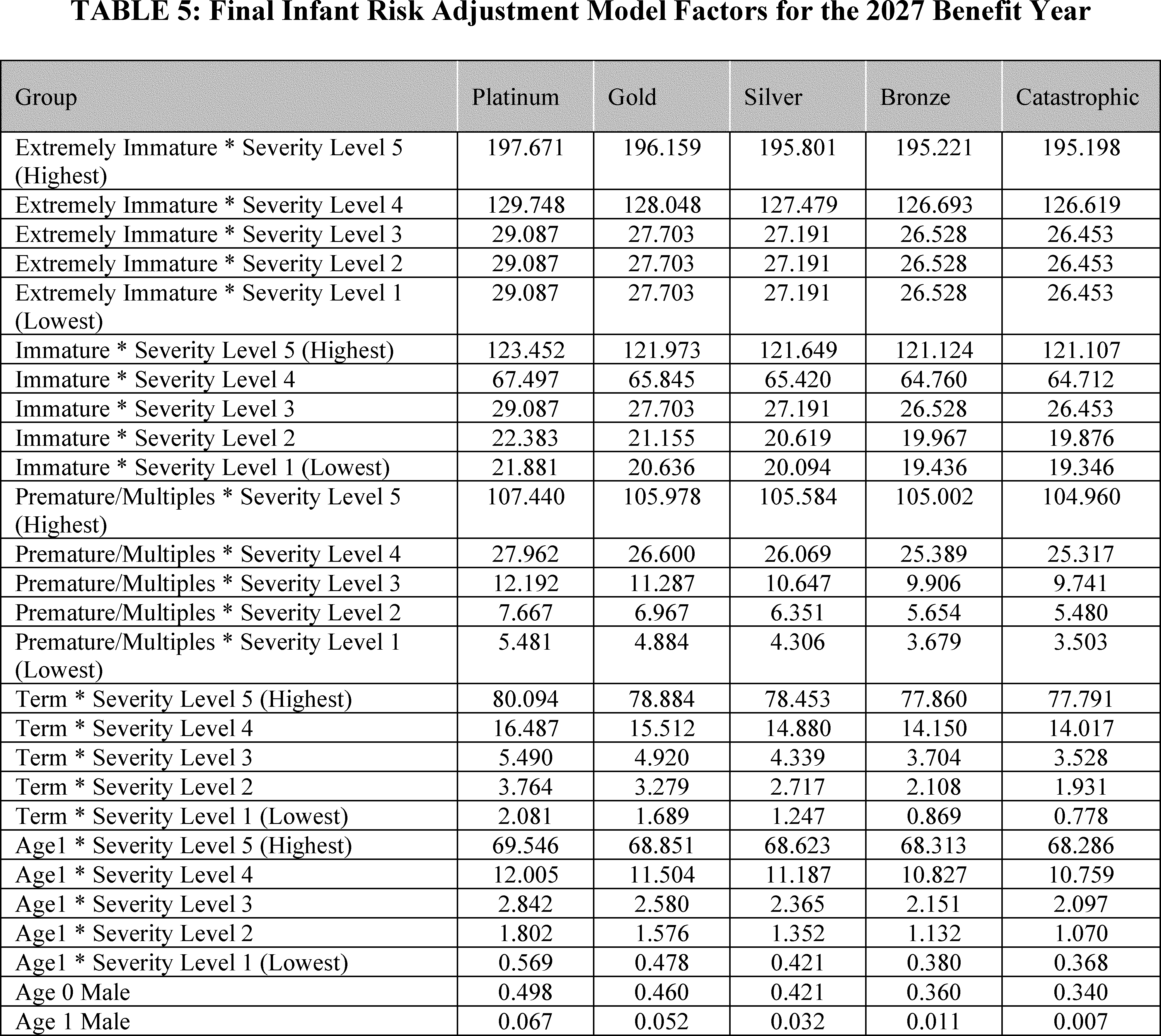

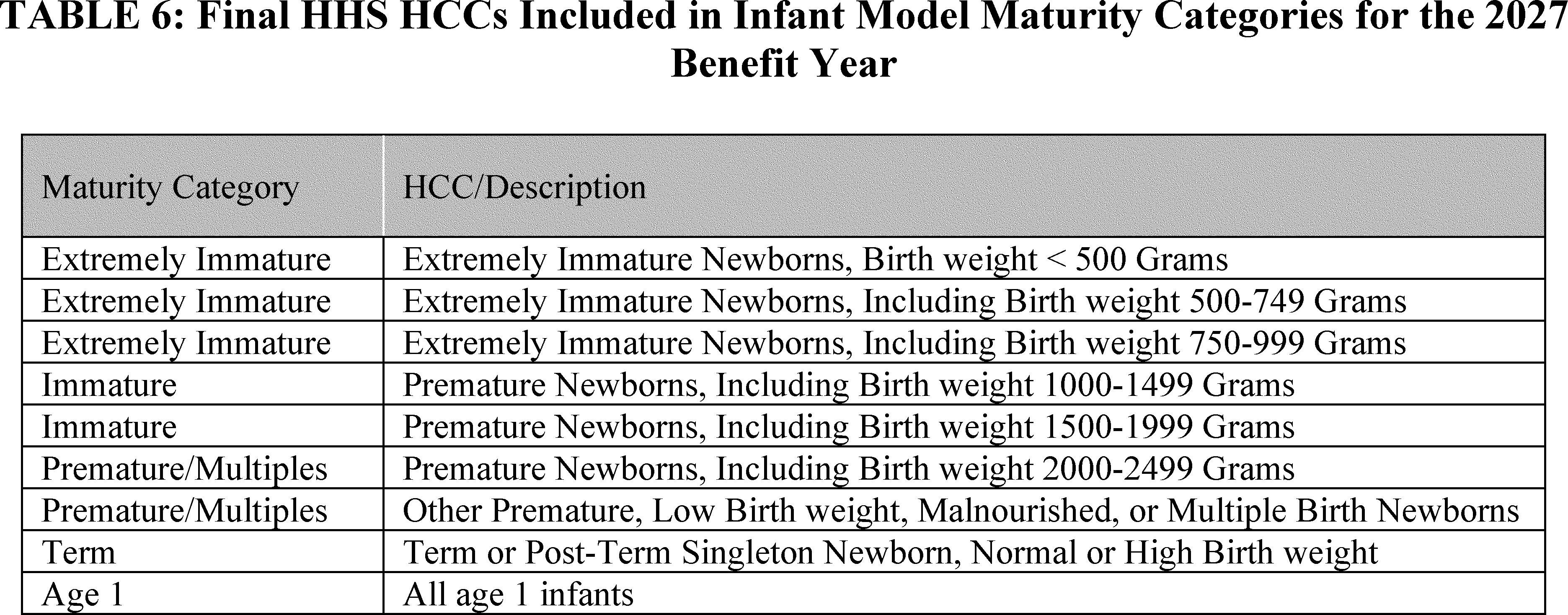

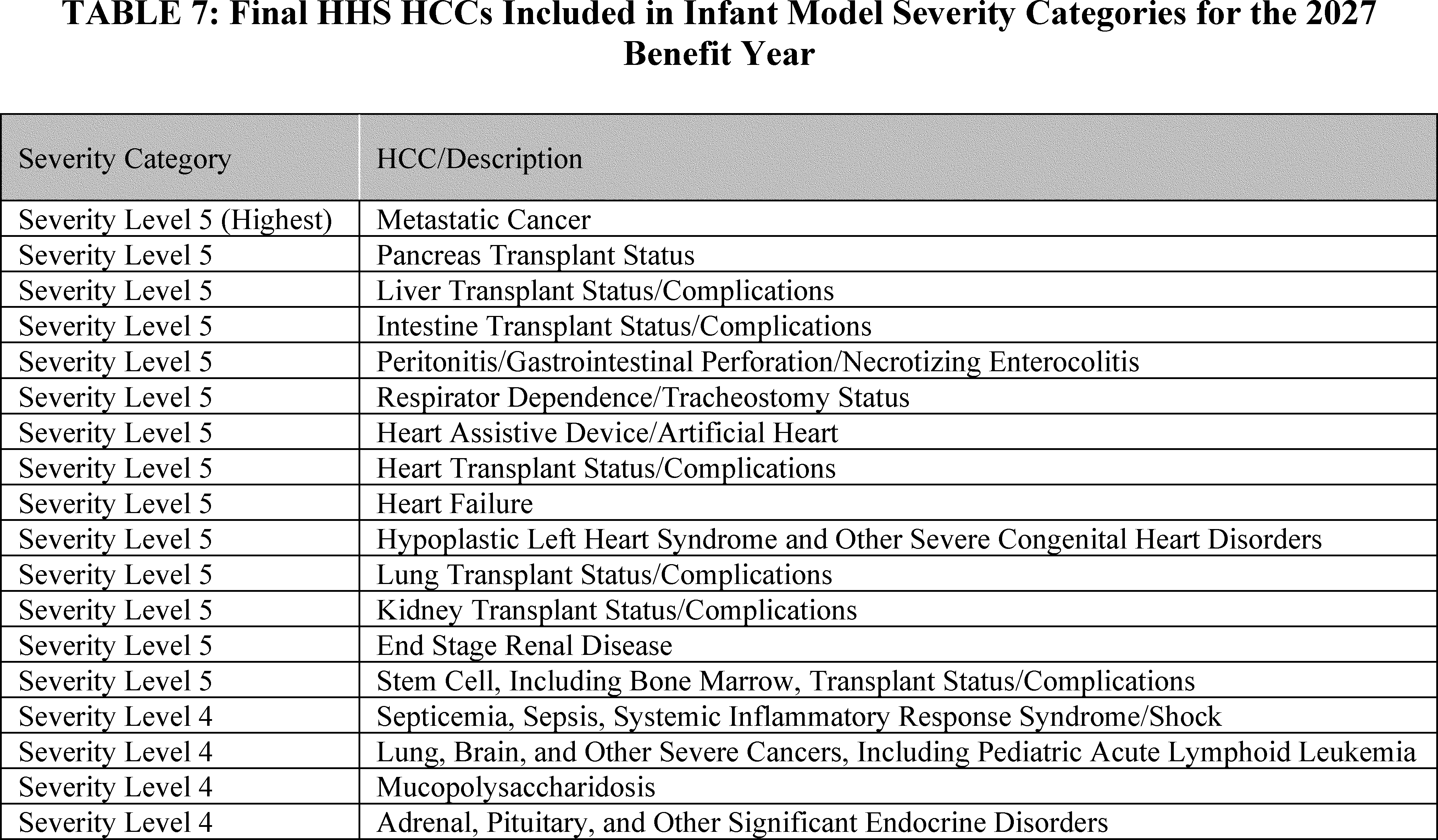

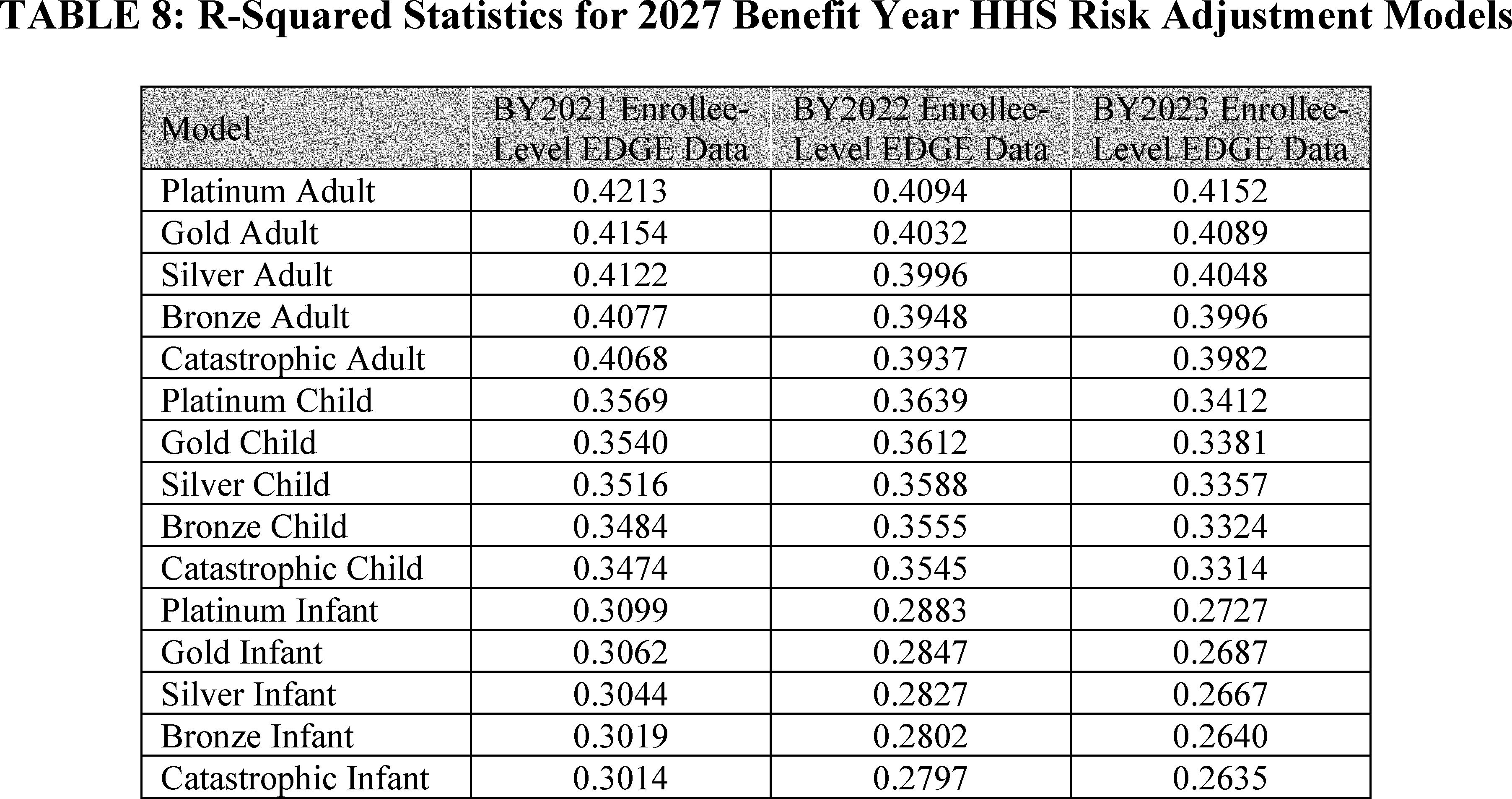

We are finalizing our proposal to recalibrate the 2027 benefit year HHS risk adjustment models using the 2021, 2022, and 2023 benefit year enrollee-level EDGE data. We are also finalizing a risk adjustment user fee rate for the 2027 benefit year of $0.18 per member per month (PMPM).

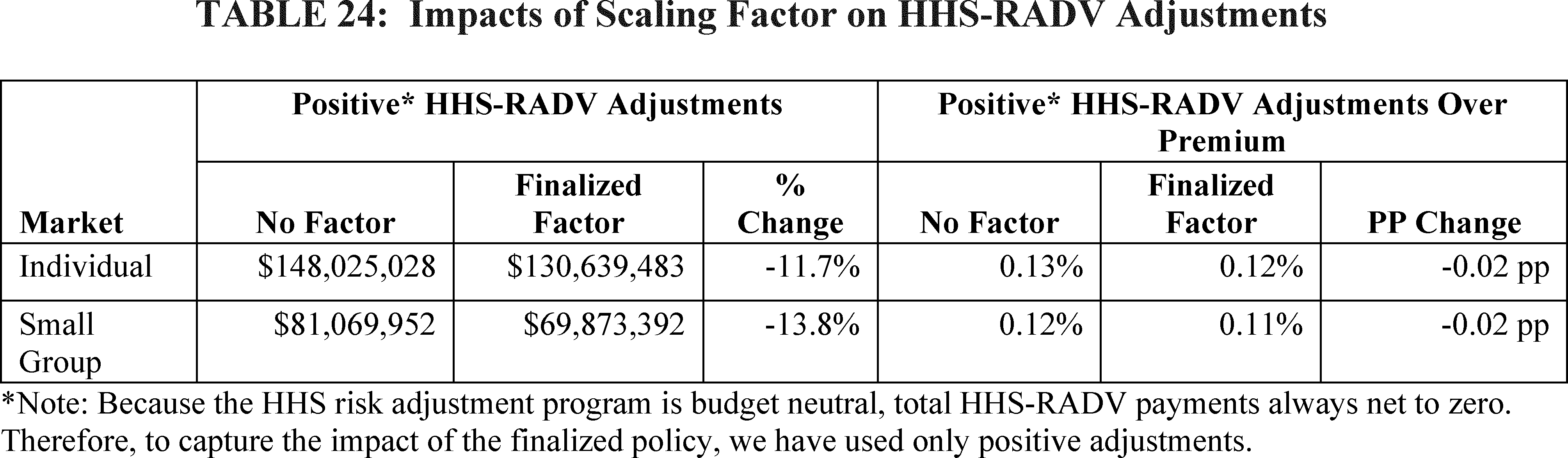

We are finalizing our proposal to modify one intermediate step of the HHS-RADV error estimation methodology starting with 2025 benefit year HHS-RADV to add an additional scaling factor to appropriately estimate the proportion of the issuer's total plan liability risk score (PLRS) that is HCC-related after the removal of no-HCC enrollees from the IVA sample beginning with 2025 benefit year HHS-RADV, as finalized in the 2026 Payment Notice (90 FR 4424).

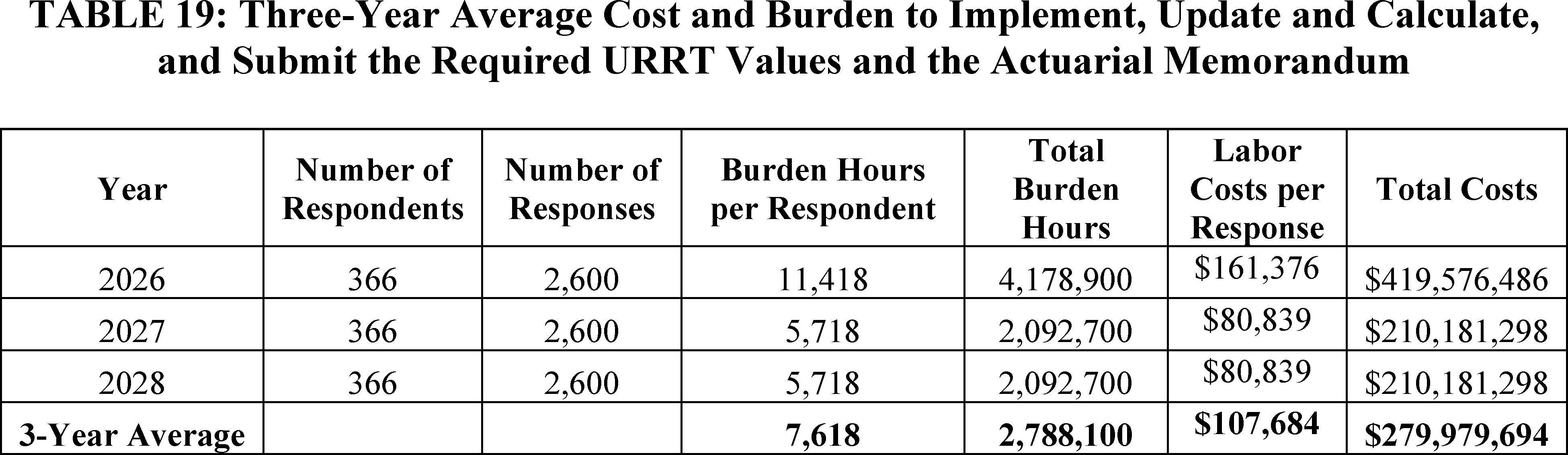

We are finalizing our proposal to require issuers that intend to load rates to account for unpaid CSRs for the applicable rating year to submit certain information related to CSR loading in their Unified Rate Review Templates (URRTs) and the Actuarial Memoranda for each filing year in which CSRs are not funded beginning with PY 2027 rate filings.[12]

We are finalizing our proposal to remove the requirement at § 155.105(b)(4) that a State seeking to operate a State Exchange must first operate an SBE-FP for at least one plan year.

We are finalizing our proposal to amend § 155.106(a)(2) to rescind the requirement that as part of a State's activities for its establishment of a State Exchange, the State must provide supporting documentation demonstrating progress toward meeting or implementing State Exchange Blueprint requirements, given preexisting processes per the State Blueprint Application [13]

for CMS to collect supporting documentation from a State as part of a State Exchange implementation efforts.

We are finalizing our proposal to amend § 155.170 with a modification to provide that beginning with PY 2028, a State-required benefit will be considered “in addition to EHB” (and thus not EHB) if it is required by a State action taking place after December 31, 2011; applicable to the small group and/or individual markets; specific to required care, treatment, or services; and not required by State action for purposes of compliance with Federal requirements. Under this finalized policy, such State-required benefits will be considered in addition to EHB regardless of whether the required benefits are embedded in the State's EHB-benchmark plan. Further, we finalize that States must make payments in accordance with § 155.170(b) to defray the cost of any State-required benefits in addition to the EHB. We are also finalizing revisions to the regulatory text at § 156.115(a) to align with this finalized policy.

We are not finalizing amendments to § 155.205(b) to amend the requirement that a State Exchange operate a centralized eligibility and enrollment consumer interface on the Exchange's website for an individual to submit a single streamlined eligibility application and subsequently select a QHP following a determination of eligibility. However, we may consider finalizing this proposal, with or without modifications, in the 2028 Payment Notice rulemaking cycle or another appropriate rulemaking vehicle, and, if so, will respond to comments then.

We are not finalizing our proposal at § 155.221(k) that State Exchanges may elect a new EDE option (SBE-EDE option), in which a State Exchange could seek HHS approval to allow web-brokers to operate enrollment websites as the exclusive pathway through which consumers can apply, receive an eligibility determination from the Exchange, and purchase an individual market QHP offered through the Exchange with APTC and CSRs, if otherwise eligible. However, we may consider finalizing this proposal, with or without modifications, in the 2028 Payment Notice rulemaking cycle or another appropriate rulemaking vehicle.

We are finalizing changes to the existing regulatory authority under § 155.220(j)(2)(ii) and (iii) to require agents, brokers, and web-brokers to use an HHS-approved and -created consumer consent form to meet the eligibility application review requirements and consumer consent documentation requirements.[14]

We will delay the effective date of requiring the HHS-approved and -created consumer consent form so that it is required for enrollments for plan years beginning on or after January 1, 2028, including enrollments under § 155.335(j). Our finalized policy will eliminate the current flexibility, which allows agents, brokers, and web-brokers to use their own standards and templates for documentation requirements, and instead sets a universal standard that requires agents, brokers, and web-brokers to use the HHS-approved and -created consumer consent form.[15]

We considered commenters' suggestion to allow previously signed consent forms to remain valid after the effective date of these policies, but we are not adopting that approach because standardizing the use of the HHS-approved and -created consumer consent form will help ensure consumers and consumers' representatives are provided with all the necessary information before providing consent, and that HHS consistently applies the consumer consent and eligibility application review

( printed page 29534)

documentation requirements uniformly among agents, brokers, and web-brokers moving forward. We are also finalizing our proposal to revise § 155.220(j)(2)(ii) and (j)(2)(iii) to clarify what constitutes a consumer “taking an action” for eligibility application review and confirmation and providing consumer consent.

We are finalizing several new provisions at § 155.220(j)(3) to establish more robust standards of conduct related to the marketing practices of agents, brokers, and web-brokers which would include examples of prohibited marketing practices. Furthermore, we are finalizing our proposal to require agents, brokers, and web-brokers to provide HHS marketing documentation in response to monitoring, audit, and enforcement activities. We also are finalizing our proposal to notify agents, brokers, and web-brokers that they may be held responsible for marketing content created, written, released, or otherwise produced by an entity on their behalf.

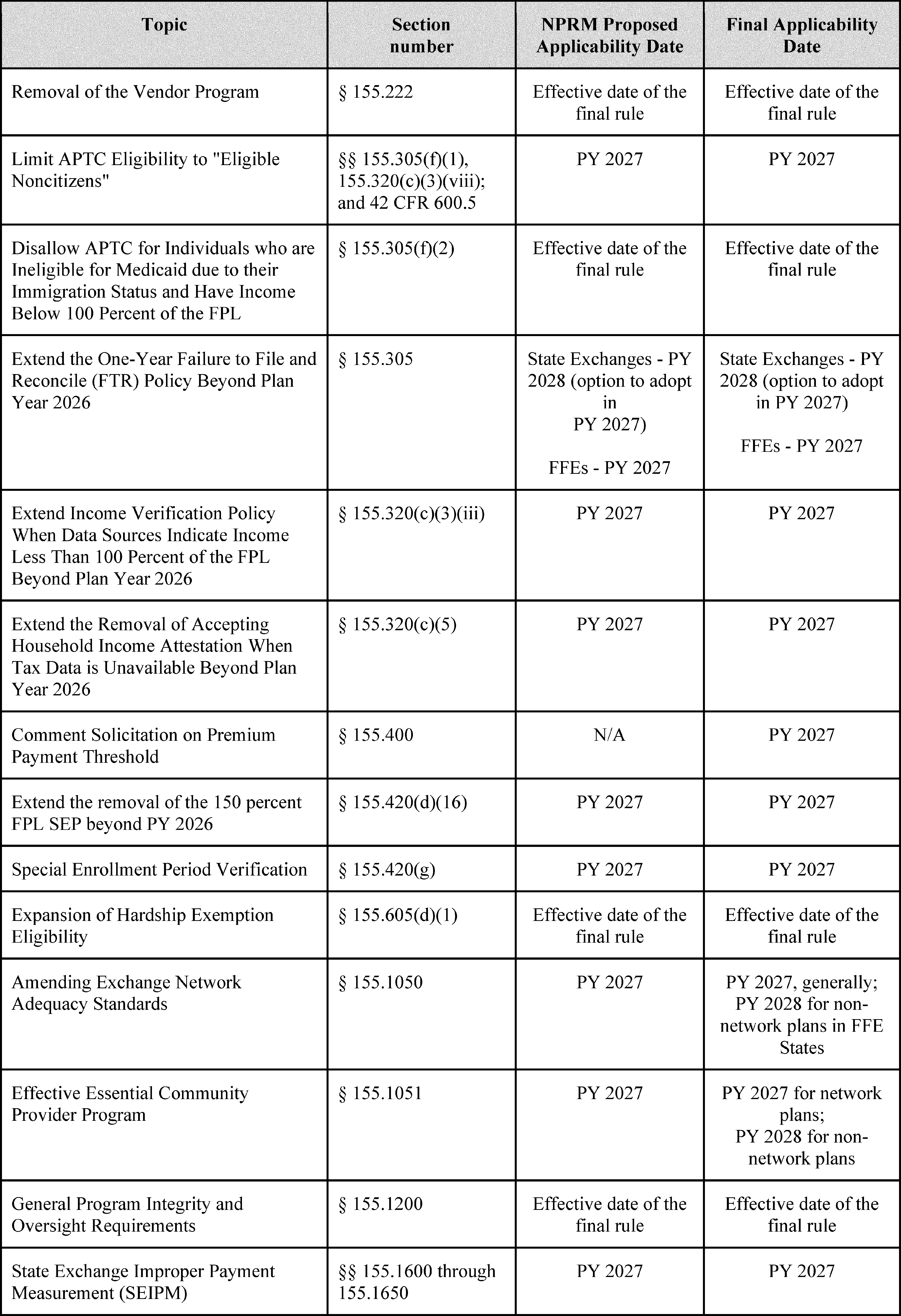

We are finalizing our proposal to discontinue the vendor program, which allows for certain training and information verification functions to be provided by HHS-approved vendors. To accomplish this, we are removing § 155.222.

We are finalizing updates in §§ 155.20, 155.305(f)(1), and 155.320 to align Exchange regulations with section 71301 of the WFTC legislation. Section 71301 of the WFTC legislation amended section 36B of the Code to provide that PTC is allowed for the QHP coverage of a lawfully present noncitizen only if such noncitizen is an “eligible alien.” It also makes conforming amendments to section 1411 of the Affordable Care Act requiring Exchanges to verify applicants' “eligible alien” status effective for plan years beginning on or after January 1, 2027. We are finalizing a new definition in § 155.20, updating our APTC eligibility regulations at § 155.305(f)(1), and adding to our verification regulations in § 155.320 to align Exchange eligibility and verification rules with section 71301 of the WFTC legislation. This finalized policy will also impact Federal payments to States effective January 1, 2027, for individuals enrolled in the BHP who are lawfully present noncitizens but are not “eligible aliens,” as Federal BHP payments attributable to these enrollees will cease beginning January 1, 2027.

To align Exchange regulations with section 71302 of the WFTC legislation, we are finalizing our proposal to remove § 155.305(f)(2) and make conforming updates to §§ 155.320(c)(3)(iii)(A) and 155.420(d)(13). Section 71302 of the WFTC legislation amended section 36B(c) of the Code to provide that PTC is no longer allowed for noncitizens lawfully present in the United States who were ineligible for Medicaid due to their immigration status and have household income below 100 percent of the FPL. Removing § 155.305(f)(2) and updating § 155.320(c)(3)(iii)(A) will align Exchange APTC eligibility and verification rules with section 71302 of the WFTC legislation. This finalized policy will also impact Federal payments to States for individuals enrolled in the BHP who are ineligible for Medicaid due to their immigration status and with household income below 100 percent of the FPL, for whom Federal payments to States are also no longer allowed.

We are finalizing our proposal to revise the failure to file and reconcile process at § 155.305(f)(4) such that Exchanges on the Federal platform will conduct the 1-year policy beginning in PY 2027. State Exchanges will have the option to conduct either the 1-year or 2-year policy in PY 2027 but will be required to conduct the 1-year policy beginning in PY 2028. Under the 1-year policy, an Exchange must determine a tax filer ineligible for APTC if: (1) HHS notifies the Exchange that the tax filer (or their spouse if the tax filer is a married couple) received APTC for a prior year for which tax data will be utilized for verification of income, and (2) the tax filer or tax filer's spouse did not comply with the requirement to file a Federal income tax return and reconcile APTC for that year. This finalized policy, which Exchanges on the Federal platform plan to adopt a year early, will align with the statutory requirement in section 71303 of the WFTC legislation that effectively requires Exchanges to follow the 1-year policy as a requirement for a month to be a coverage month under section 36B of the Code as of PY 2028. We are also finalizing our proposal to remove the notice requirement at § 155.305(f)(4)(ii) for PY 2027 to conform with the notice policy under the PY 2026 policy.

We sought comment on considerations for future policy development and implementation under section 71303 of the WFTC legislation, which imposes new requirements on Exchanges related to eligibility verification. Specifically, we sought comment on: operational considerations for interested parties; effective rollout and communications; required timelines for interested parties to comply with the law; anticipated complexity, costs, burden, enrollment impacts; and any State-specific considerations. We will take comments we received into consideration for any potential guidance or rulemaking.

We are finalizing our proposal to revise § 155.320(c) such that all Exchanges are required to continue conducting the income verifications changes introduced in the 2025 Marketplace Integrity and Affordability final rule (90 FR 27074) in PY 2027 and beyond, effectively removing the requirement to stop both income verification policies starting in PY 2027. Specifically, we are updating § 155.320(c)(3)(iii) and § 155.320 (c)(3)(vi)(C)(2) to extend the requirement indefinitely to create income data matching issues (DMIs) when trusted data sources indicate that projected consumer household income is under 100 percent of the FPL. Additionally, we are removing § 155.320(c)(5), which outlines the requirement to accept the annual household income attestation when no tax data is returned for a household.

We sought comment on whether we should regulate the option for issuers to implement the fixed-dollar and/or gross percentage-based premium payment thresholds in § 155.400(g) for PY 2027 and beyond. Currently, issuers are only able to implement a net premium percentage-based premium threshold for PY 2026, and effective January 1, 2027, issuers will be able to implement the fixed-dollar and/or either net or gross premium percentage-based thresholds, which was finalized in the 2025 Marketplace Integrity and Affordability final rule. After consideration of public comments and for reasons outlined in the proposed and final rule, we are finalizing for all Exchanges the removal of the fixed-dollar and gross-premium threshold flexibilities.

We are finalizing our proposal to remove § 155.420(d)(16) such that Exchanges will continue to be prohibited from offering the 150 percent FPL SEP in PY 2027 and beyond, in alignment with section 71304 of the WFTC legislation. We are finalizing our proposal to make conforming amendments at §§ 155.420(a)(4)(ii)(D), 155.420(b)(2)(vii), and 155.420(a)(4)(iii).

We are finalizing our proposal to revise § 155.420(g) to remove the restriction for Exchanges on the Federal platform to only conduct Special Enrollment Period Verification (SEPV) for Loss of Minimum Essential Coverage (MEC). We also are finalizing our proposal to require Exchanges on the Federal platform to conduct SEPV for at least 75 percent of new enrollments. These policies were finalized in the 2025 Marketplace Affordability and Integrity final rule but were stayed in

( printed page 29535)

City of Columbus et al.

v.

Kennedy et al.[16]

We are therefore finalizing these provisions as we reproposed in the 2027 Payment Notice proposed rule.

We are finalizing our proposal to amend § 155.605 to codify and expand hardship exemption eligibility. Specifically, this finalized policy will allow individuals who are ineligible for APTC or CSRs due to projected household income below 100 percent or above 250 percent of the FPL to qualify for a hardship exemption under § 155.605(d)(1)(iii). This change will allow individuals aged 30 and older who receive this hardship exemption to enroll in catastrophic coverage, if otherwise eligible.

We are finalizing, for plan years beginning on or after January 1, 2027, our proposal to amend § 155.1050(a)(2) to remove the requirements at § 155.1050(a)(2)(i) and (ii) that State Exchanges and SBE-FPs establish and impose quantitative time and distance network adequacy standards that are at least as stringent as standards for QHPs participating on the FFEs and to no longer require State Exchanges and SBE-FPs to conduct quantitative network adequacy reviews to evaluate a plan's compliance with certain network adequacy standards under § 156.230 prior to certifying any plan as a QHP. Instead, we are finalizing our proposal to restore the requirement at § 155.1050(a)(2) that State Exchanges and SBE-FPs ensure that each QHP provides sufficient access to providers in a manner that meets applicable standards consistent with § 156.230(a)(1)(ii) and (a)(1)(iii) for network plans, or for plan years beginning on or after January 1, 2027, § 156.236(a) for non-network plans if such plans are allowed to be offered through the Exchange, as applicable.

We also are finalizing, with minor modification, at new § 155.1050(d) our proposal to defer provider access reviews of QHP issuers, with or without a provider network, applying for certification as a QHP to be offered through the FFE, to the FFE States that elect to conduct such reviews, should the FFE State demonstrate sufficient authority and the technical capacity to conduct such reviews by satisfying the applicable criteria to be considered to have an Effective Provider Access Review Program under § 155.1050(d)(2) through (d)(4). We note that provisions related to non-network plans will be implemented beginning January 1, 2028.

We are finalizing, with modification, our proposal to implement new requirements for an Effective Essential Community Provider (ECP) Review Program by adding § 155.1051. Under this finalized policy, FFE States may elect to conduct their own ECP certification reviews of issuers, with or without a provider network, that are applying for certification to be offered as a QHP through an FFE, including in States performing plan management. To conduct their own reviews, we are finalizing that FFE States will be required to demonstrate that they have sufficient authority and the technical capacity to conduct these reviews by satisfying the applicable criteria to be considered to have an Effective ECP Review Program under § 155.1051. We note that provisions related to non-network plans will be effective beginning on or after January 1, 2028.

We are finalizing our proposal to amend § 155.1200(d) and add new paragraph (e) to permit State Exchanges to satisfy certain requirements of the independent external programmatic audit, as outlined in paragraph (d), by completing the SEIPM process that will be established at 45 CFR 155, subpart Q.

We are finalizing our proposal to add new subpart Q (§§ 155.1600 through 1650) to establish the SEIPM program. The Payment Integrity Information Act of 2019 (PIIA) requires Federal agencies to annually review, measure, and report on the programs they administer that have been determined to be susceptible to significant improper payments. To satisfy the requirements of the PIIA, we are finalizing our proposal to measure improper payments of APTC that are administered by State Exchanges and to annually report statistically valid improper payment estimates in the HHS Agency Financial Report.

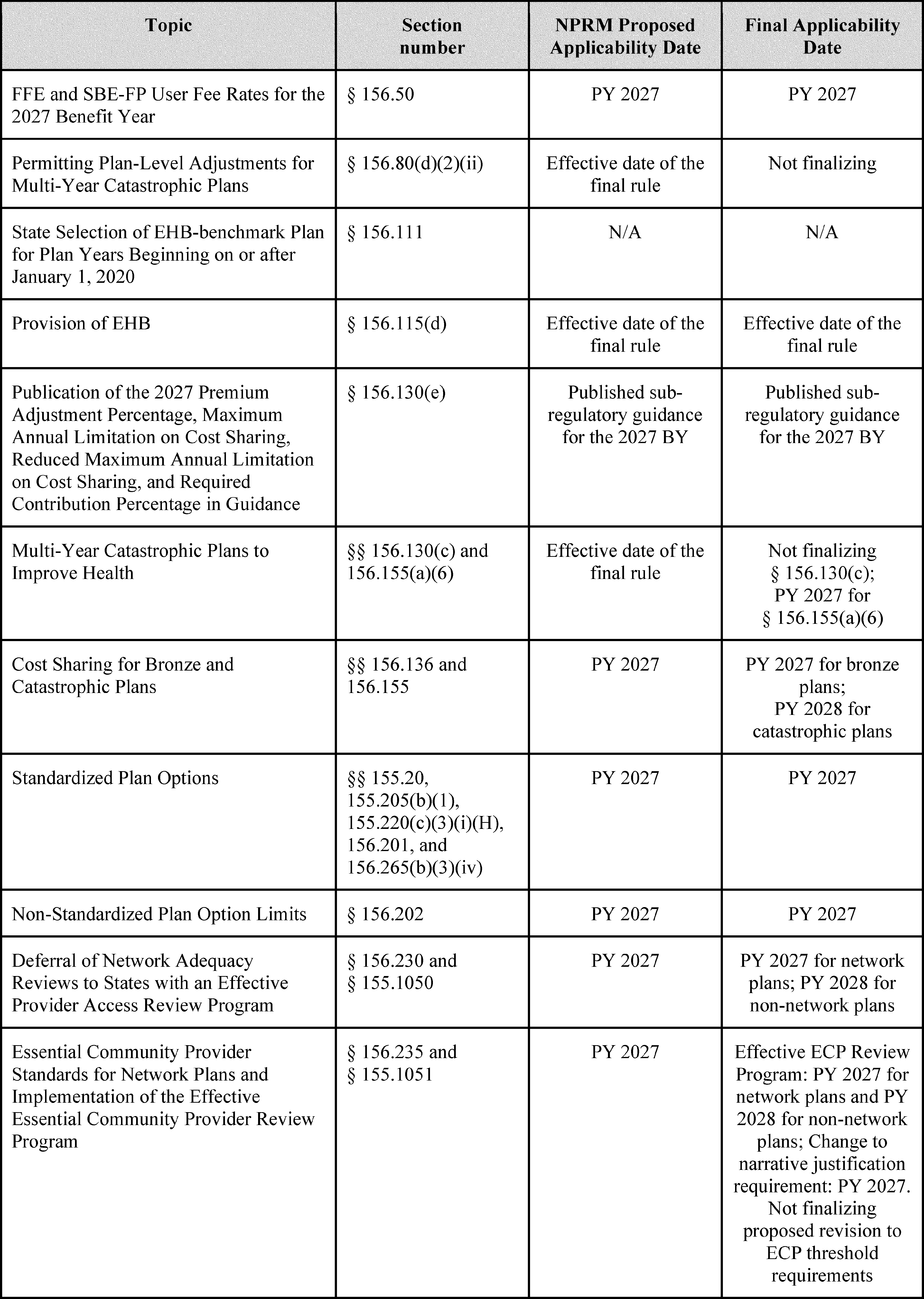

We are finalizing 2027 benefit year FFE and SBE-FP user fee rates of 1.9 percent and 1.5 percent of total monthly premiums, respectively.

We paused review of State applications to select EHB-benchmark plans in accordance with § 156.111. We are reviewing section 1302 of the Affordable Care Act and are considering future rulemaking to revise § 156.111 and EHB standards more broadly.

We are finalizing our proposal to revise § 156.115(d) to prohibit issuers from including routine non-pediatric dental services as an EHB.

We are finalizing, with modification, our proposals to amend the requirements for catastrophic plans in § 156.155. We specify that, effective for plan years beginning on or after January 1, 2027, a catastrophic plan has a plan term of either 1 plan year, or of multiple consecutive plan years not to exceed 10 plan years, and that catastrophic plans with terms of at least 2 consecutive plan years may utilize value-based insurance designs to provide benefits before reaching the deductible, pursuant to guidelines issued by the Secretaries of HHS, Labor, and the Treasury under section 2713(c) of the PHS Act. We are not finalizing our proposal to amend § 156.80 to permit issuers of multi-year catastrophic plans to make a plan-level adjustment to the index rate that reflects the length of the entire plan term. We also are not finalizing our proposal to amend § 156.130 to specify that, in the case of a catastrophic plan with a consecutive multi-year term, the annual limitation on cost sharing for the initial plan year of the contract may apply on an annual basis, or on average over the life of the contract.

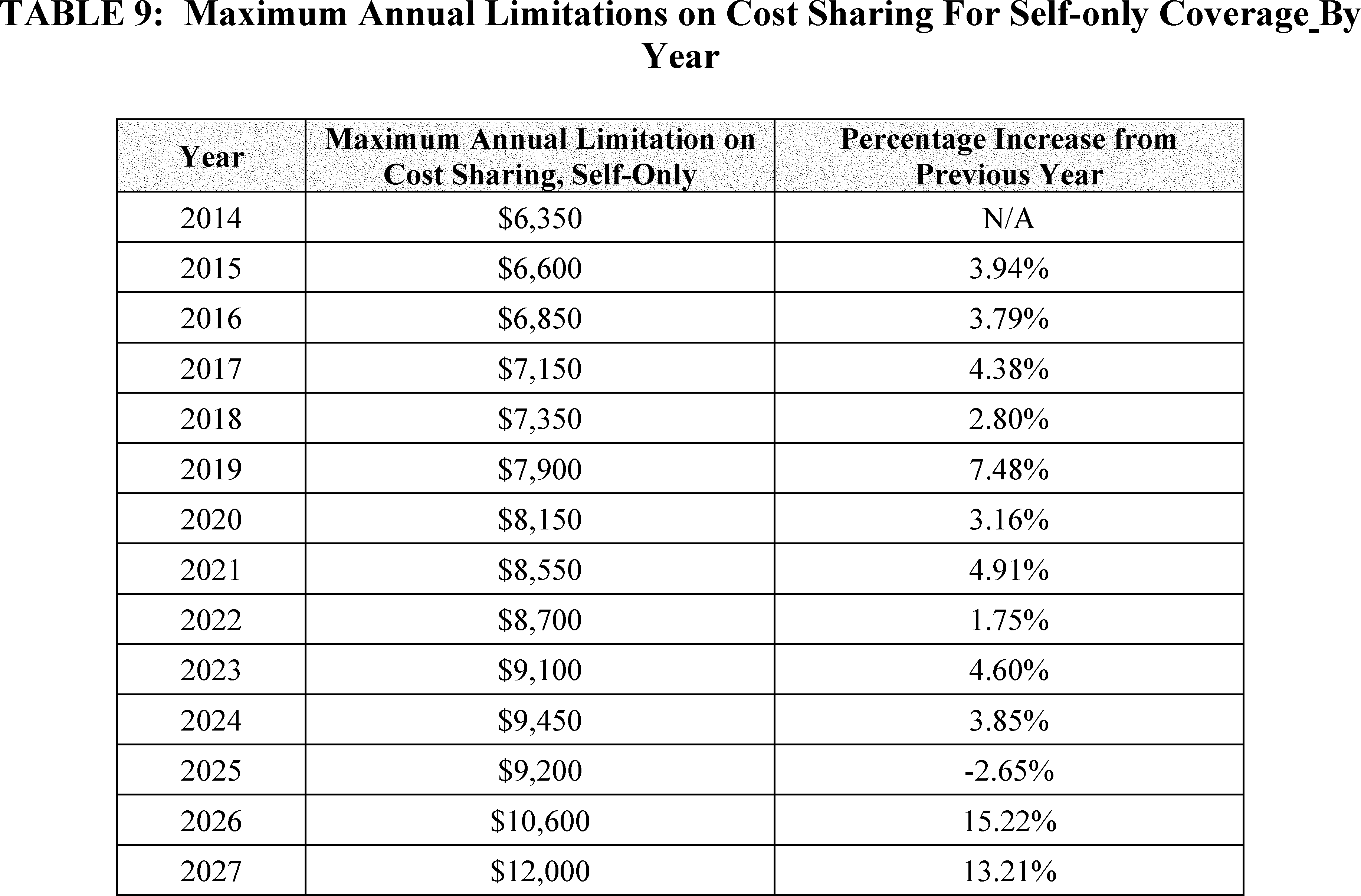

To address an issue that has arisen in the implementation of section 1302(c) through (e) of the Affordable Care Act, we are finalizing changes to (1) the permissible cost-sharing parameters for individual market bronze plans through new § 156.136 effective beginning PY 2027, with modification to specify that such plans are permitted to exceed the standard annual limitation on cost sharing by up to 130 percent of the standard annual limitation on cost sharing, and (2) the required cost-sharing parameters for catastrophic plans through revisions to § 156.155(a)(3) with a modification to have the revisions to § 156.155(a)(3) be effective beginning PY 2028.

We are finalizing our proposal to remove the following from our regulations effective beginning in PY 2027: the definition of “standardized options” at § 155.20; all requirements pertaining to standardized plan options at § 156.201; the differential display of standardized plan options on

HealthCare.gov

at § 155.205(b)(1); the corresponding standardized plan option differential display requirements for approved web-broker and QHP issuer enrollment partners using a DE pathway to facilitate consumer enrollment through an FFE or SBE-FP at §§ 155.220(c)(3)(i)(H) and 156.265(b)(3)(iv); the annual design and publication of these standardized plan options in the applicable Payment Notice for each plan year; and non-standardized plan option limits and exceptions at § 156.202.

We are finalizing our proposal to revise the network adequacy and ECP standards at §§ 156.230 and 156.235 to make clear that these sections contain the provider access standards for all individual market QHPs and stand-alone dental plans (SADPs) and all

( printed page 29536)

Small Business Health Options Program (SHOP) QHPs across all QHP issuers that use a network of providers. We also are finalizing our proposal to revise these sections to remove the requirement that all QHPs must use a network of providers.

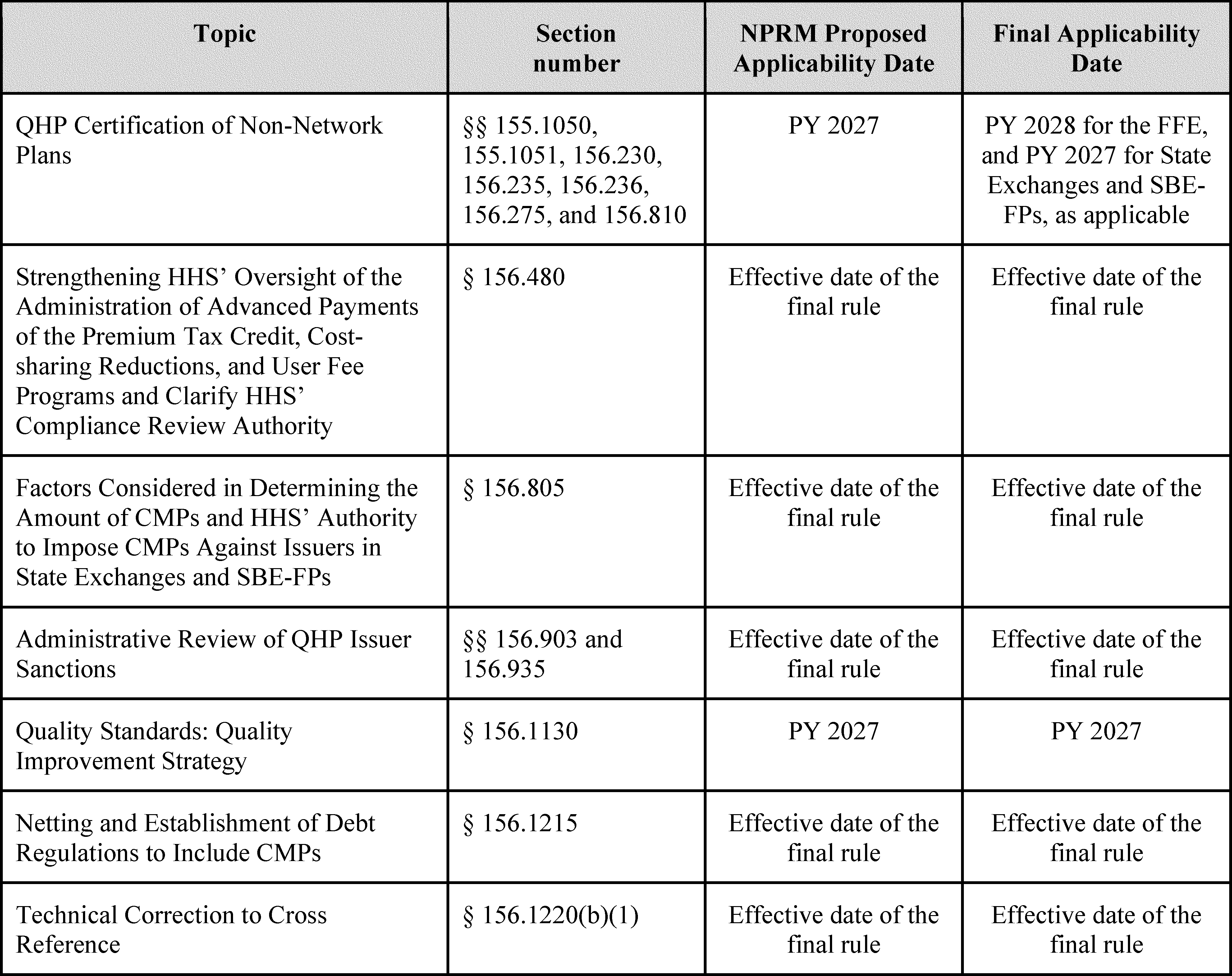

Additionally, we are finalizing our proposal to revise § 156.230 to provide that HHS will continue to conduct network adequacy reviews using standards described at § 156.230 for QHP issuers that use a provider network in FFE States that do not elect to conduct such reviews, or in FFE States that HHS has determined do not satisfy the criteria to be considered to have an Effective Provider Access Review Program, as described at § 155.1050(d). We also are finalizing our proposal to add new § 156.236 to allow plans that do not use a network (non-network plans) to receive QHP certification, effective beginning in PY 2028, by demonstrating that they ensure a sufficient choice of providers that accept the non-network plan's benefit amount as payment in full, and reasonable and timely access to ECPs that accept the plan's benefit amount as payment in full. As finalized, § 156.236 will set forth provider access and ECP requirements for assessing whether non-network plans provide sufficient choice of providers.

For PY 2027 and subsequent plan years, we are finalizing, with modification, our proposed changes to the QHP certification requirements for ECPs included within a network plan issuer's provider network. First, we are not finalizing our proposal to reduce the minimum percentage requirement from 35 to 20 percent for both medical QHP and SADP issuers. Second, we are finalizing our proposal to modify the narrative justification requirements at §§ 156.235(a)(3) and 156.235(b)(3) to be consistent with systems changes and existing QHP issuer ECP data submission requirements as part of ECP certification reviews.

We are finalizing our proposal to modify § 156.480(c) to clarify HHS' authority to audit or conduct a compliance review of an issuer that offers a QHP through an Exchange for the purposes of administering and providing oversight of the APTC, CSR, and user fee programs. We are also finalizing that HHS may conduct a compliance review to assess issuers' compliance with requirements related to these programs as needed or on an annual basis rather than only on an ad hoc basis.

We are finalizing our proposal to amend § 156.805(b) to reiterate in § 156.805(b) that in determining the amount of CMPs, in addition to the factors HHS takes into account when determining a CMP amount listed in § 156.805(b)(1) through (3), HHS will identify the lawful purpose or purposes of the CMP. We are also finalizing our proposal to amend the introductory text of § 150.317 to make corresponding edits for the factors HHS, through CMS, considers when determining the amount of CMPs as enforcement remedies against issuers more broadly or other responsible entities, such as a non-Federal governmental plan sponsor that is subject to applicable PHS Act requirements. In addition, we are finalizing our proposal to amend § 156.805(f) to reiterate that HHS has the authority to impose CMPs against issuers in a State Exchange or SBE-FP for an identified violation of any Exchange requirements applicable to issuers offering a QHP in an Exchange, when a State notifies HHS that it is not enforcing these requirements or HHS determines that a State is failing to substantially enforce these requirements.

We are finalizing our proposal to amend § 156.903 to provide the option for an administrative law judge (ALJ) to issue subpoenas, upon his or her own motion or at the request of a party, if reasonably necessary for the full presentation of a case and to add procedures governing the process for issuing subpoenas. We are also finalizing our proposal to amend § 156.935 to ensure that the discovery provisions set forth therein do not apply to administrative appeals of proposed CMPs for violations identified through audits of the APTC, CSR, or user fee programs conducted in accordance with § 156.480(c).

We are finalizing our proposal to require QHP issuers to submit QISs addressing any two of the five topic areas listed in section 1311(g)(1) of the Affordable Care Act, without mandating which specific topics areas a QHP issuer will be required to address to meet the QIS statutory certification requirement, beginning with PY 2027.

We are finalizing our proposal to amend § 156.1215(b) to provide that CMPs assessed against health coverage issuers and their affiliates under the same taxpayer identification (TIN) number will be subject to netting as part of HHS' integrated monthly payment and collection cycle. We are also finalizing our proposal to amend § 156.1215(c) to provide that any amount owed to the Federal Government by an issuer and its affiliates for unpaid CMP amounts, after HHS nets amounts owed by the Federal Government, will be the basis for calculating the debt.

We are finalizing a technical correction to update a cross reference in § 156.1220.

We sought comment on the impact of the Federal MLR standard on individual market stability and whether HHS should use its authority under section 2718(b)(1)(A)(ii) of the PHS Act and § 158.301 to adjust the Federal MLR standard in a State to promote individual market stability. We also solicited comment on whether and how to amend regulations allowing States to request an adjustment to the MLR standard in their individual market to reduce burden and encourage States to request adjustments, as appropriate, in their State markets. We will take comments we received into consideration as we continue to consider potential adjustments to the Federal MLR standard for particular States' individual health insurance markets.

III. Summary of the Proposed Provisions, Public Comments, and Responses to Comments on the Proposed Rule

A. Part 150—CMS Enforcement in Group and Individual Insurance Markets

1. Factors CMS Uses To Determine the Amount of a Civil Money Penalty (CMP) (§ 150.317)

In the 2027 Payment Notice proposed rule (91 FR 6292, 6327), to align with the proposal discussed in section III.E.14. of the proposed rule, which would reiterate in § 156.805(b) what factors HHS considers when determining the amount of CMPs as enforcement remedies against QHP issuers in Exchanges, we proposed a conforming amendment to § 150.317 introductory text to clarify that HHS, through CMS, will identify the lawful purpose or purposes of the penalty, and take into account the enumerated factors as appropriate for the circumstances. In proposing the conforming edits to § 150.317, we did not propose other changes to the legal bases and procedural processes for imposing CMPs.

We requested comment on this proposal.

After consideration of comments and for the reasons outlined in the proposed rule and section III.E.14. of this final rule, including our responses to comments, we are finalizing as proposed an amendment to the introductory text of § 150.317 to make

( printed page 29537)

corresponding edits for the factors HHS considers when determining the amount of CMPs as enforcement remedies against issuers more broadly or other responsible entities, such as a non-Federal governmental plan sponsor that is subject to applicable PHS Act requirements. We summarize and respond to public comments received on the proposed conforming amendment for the factors HHS considers when determining the amount of CMPs as enforcement remedies at § 156.805(b) in section III.E.14. of this final rule.