Securities and Exchange Commission

- [Release No. 34-105501; File No. SR-Phlx-2026-29]

Pursuant to Section 19(b)(1) of the Securities Exchange Act of 1934 (“Act”),[1] and Rule 19b-4 thereunder,[2] notice is hereby given that on May 5, 2026, Nasdaq PHLX LLC (“Phlx” or “Exchange”) filed with the Securities and Exchange Commission (“Commission”) the proposed rule change as described in Items I and II below, which Items have been prepared by the Exchange. The Commission is publishing this notice to solicit comments on the proposed rule change from interested persons.

I. Self-Regulatory Organization's Statement of the Terms of Substance of the Proposed Rule Change

The Exchange proposes to amend Options 9, Section 13 to increase the position and exercise limits [3] for options on iShares Bitcoin Trust ETF (“IBIT”).

The text of the proposed rule change is available on the Exchange's website at https://listingcenter.nasdaq.com/rulebook/phlx/rulefilings, and at the principal office of the Exchange.

II. Self-Regulatory Organization's Statement of the Purpose of, and Statutory Basis for, the Proposed Rule Change

In its filing with the Commission, the Exchange included statements concerning the purpose of and basis for the proposed rule change and discussed any comments it received on the proposed rule change. The text of these statements may be examined at the places specified in Item IV below. The Exchange has prepared summaries, set forth in sections A, B, and C below, of the most significant aspects of such statements.

A. Self-Regulatory Organization's Statement of the Purpose of, and Statutory Basis for, the Proposed Rule Change

1. Purpose

The Exchange proposes to amend Options 9, Section 13, Position Limits, and Options 9, Section 15, Exercise Limits, for options on IBIT. The Exchange also proposes a technical amendment to Options 6C, Section 3, Proper and Adequate Margin. Each change is discussed below.

Position and Exercise Limits

Nasdaq ISE, LLC (“ISE”) recently received approval to increase the position and exercise limits for options on IBIT to 1,000,000 contracts on the same side of the market.[4] IBIT is an Exchange-Traded Fund (“ETF”) that holds Bitcoin and is listed on The Nasdaq Stock Market LLC.[5] Options on IBIT are listed pursuant to Options 4, Section 3(h)(vi).[6] On September 20, 2024, ISE received approval to list options on IBIT.[7] The position and exercise limits for IBIT options are currently set as stated in Options 9, Sections 13 and 15.[8]

Position limits, and exercise limits, are designed to limit the number of options contracts traded on the exchange in an underlying security that an investor, acting alone or in concert with others directly or indirectly, may control. These limits, which are described in Options 9, Sections 13 and 15, are intended to address potential manipulative schemes and adverse market impacts surrounding the use of options, such as disrupting the market in the security underlying the options. Position and exercise limits must balance concerns regarding mitigating potential manipulation and the cost of inhibiting potential hedging activity that could be used for legitimate economic purposes.

To achieve this balance, the Exchange proposes to increase the position limits and exercise limits for options on IBIT to 1,000,000 contracts by noting the proposed position limit in Options 9, Section 13(a), which then reflects the exercise limits in Options 9, Section 15. The position limit for options on IBIT is currently set pursuant to Options 9, Section 13(g) where the largest in capitalization and the most frequently traded stocks and ETFs have an option position limit of 250,000 contracts (with adjustments for splits, re-capitalizations, etc.) on the same side of the market; and smaller capitalization stocks and ETFs have position limits of 200,000, 75,000, 50,000 or 25,000 contracts (with adjustments for splits, recapitalizations, etc.) on the same side of the market. The Exchange notes that the proposed position limits and exercise limits for options on IBIT are consistent with existing position limits and exercise limits for options on iShares MSCI Emerging Markets, iShares China Large-Cap ETF and iShares MSCI EAFE ETF.

Composition and Growth Analysis for Underlying ETFs

As stated above, position (and exercise) limits are intended to prevent the establishment of options positions that can be used or might create incentives to manipulate the underlying market so as to benefit options positions. The Commission has recognized that these limits are designed to minimize the potential for mini-manipulations and for corners or squeezes of the underlying market, as well as serve to reduce the possibility ( printed page 30009) for disruption of the options market itself, especially in illiquid classes.[9]

Per the Commission, “rules regarding position and exercise limits are intended to prevent the establishment of options positions that can be used or might create incentives to manipulate or disrupt the underlying market so as to benefit the options positions.” [10] For this reason, the Commission requires that “position and exercise limits must be sufficient to prevent investors from disrupting the market for the underlying security by acquiring and exercising a number of options contracts disproportionate to the deliverable supply and average trading volume of the underlying security.” [11] The Exchange has observed an ongoing increase in demand in options on IBIT in 2025.[12] The Exchange believes the current position limit and exercise limit of 250,000 contracts (the highest position limit available pursuant to Options 9, Section 13 and exercise limit pursuant to Options 9, Section 15) will impede trading activity and strategies of investors, such as use of effective hedging vehicles or income generating strategies ( e.g., buy-write or put-write), and the ability of Market Makers to make liquid markets with tighter spreads in IBIT options.

The Exchange believes that increasing the position limit (and exercise limit) for options on IBIT to 1,000,000 contracts would enable liquidity providers to provide additional liquidity to the Exchange, as well as other options exchange on which they participate. As described in further detail below, the Exchange believes that the continuously increasing market capitalization of IBIT options, as well as the highly liquid markets for those securities, reduces the concerns for potential market manipulation and/or disruption in the underlying markets upon increasing position limits, while the rising demand for trading options on IBIT for legitimate economic purposes compels an increase in position limits (and corresponding exercise limits).

IBIT currently qualifies for a 250,000 contract position limit pursuant to the criteria in Options 9, Section 13(g)(i), which requires that, for the most recent six-month period, trading volume for the underlying security be at least 100 million shares.[13] As of February 11, 2026, ISE observed that the market capitalization for IBIT was 52,661,063,818 [14] with an average daily volume (“ADV”), for the preceding 6 months prior to February 11, 2026, of 61,803,035 shares. By comparison, on the same day, the iShares MSCI Emerging Markets (“EEM”) had an ADV of 29,459,889 shares and an AUM of 27,761,941,292 the iShares China Large-Cap ETF (“FXI”) had an ADV of 31,656,532 and an AUM of 6,594,337,253; and the iShares MSCI EAFE ETF (“EFA”) had an ADV of 17,215,037 shares and an AUM of 76,788,457,200.[15]

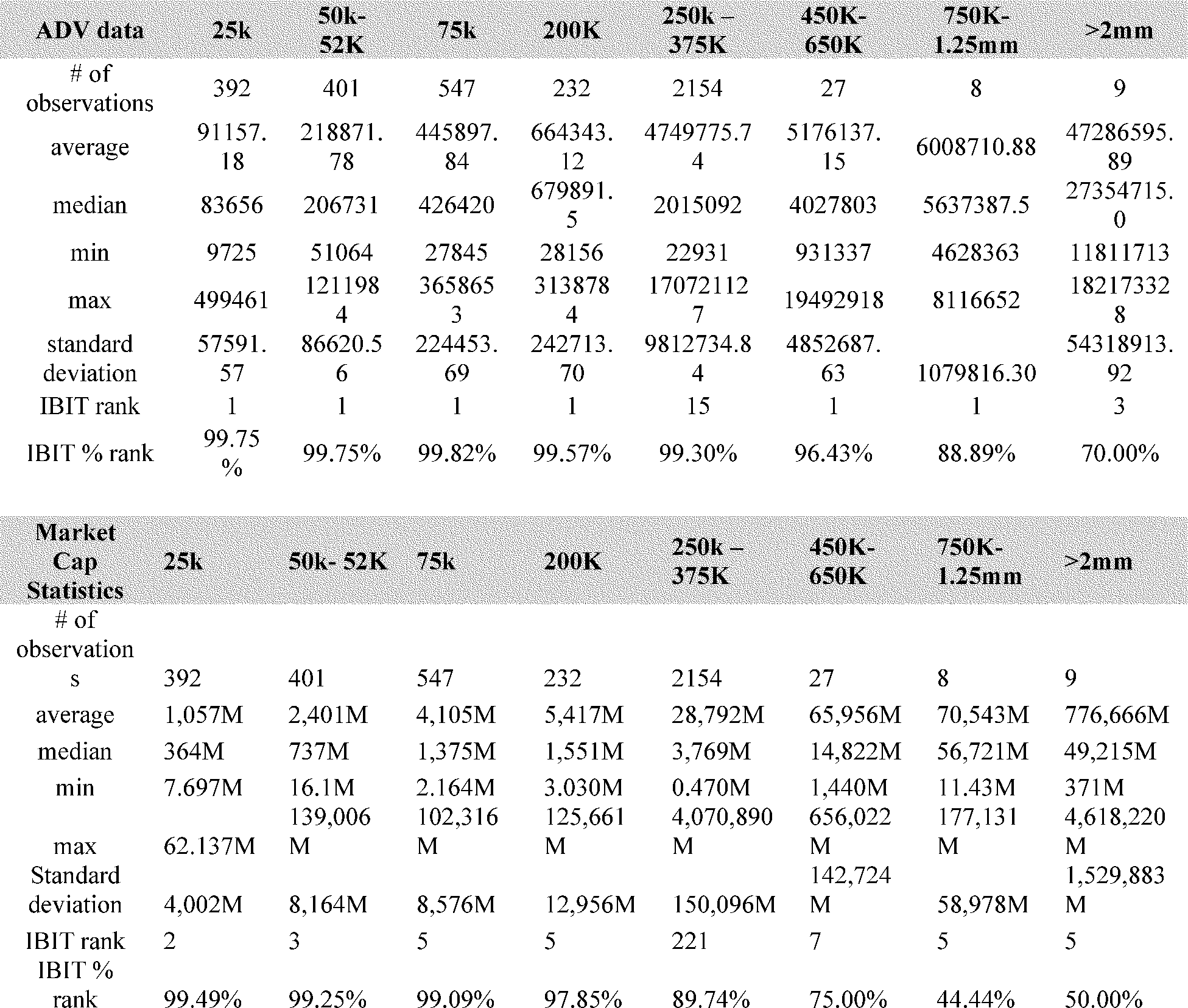

In addition to IBIT's Options 9, Section 13(g)(i) eligibility for 1,000,000 contracts, ISE performed additional analysis with respect to IBIT. First, ISE considered IBIT's market capitalization and ADV, and prospective position limit in relation to other securities. In measuring IBIT against other securities, ISE aggregated market capitalization and volume data for securities that have defined position limits utilizing data from The Options Clearing Corporation (“OCC”).[16] This pool of data took into consideration 3,797 options on single stock securities, excluding broad based ETFs.[17] Next, the data was aggregated based on market capitalization and ADV and grouped by option symbol and position limit utilizing statistical thresholds for ADV, based on 180 days, and market capitalization that were one standard deviation [18] above the mean for each position limit category ( i.e. 25,000; 50,000 to 52,000; 75,000; 200,000; 250,000 to 375,000; 450,000 to 650,000; 750,000 to 1,250,000; and greater than or equal to 2,000,000).[19] This exercise was performed to demonstrate IBIT's position limit relative to other options symbols in terms of market capitalization and ADV. For reference, the market capitalization for IBIT was $52,661,063,818 [20] with an ADV, for the preceding 180 days prior to February 11, 2026, of 61,803,035 shares.

( printed page 30010)

Based on the above table, if IBIT were compared to the 10 stocks that had position limits of 750,000 contracts to 1.25 million contracts it would have ranked in the 45th percentile for market capitalization and the 89th percentile for ADV.

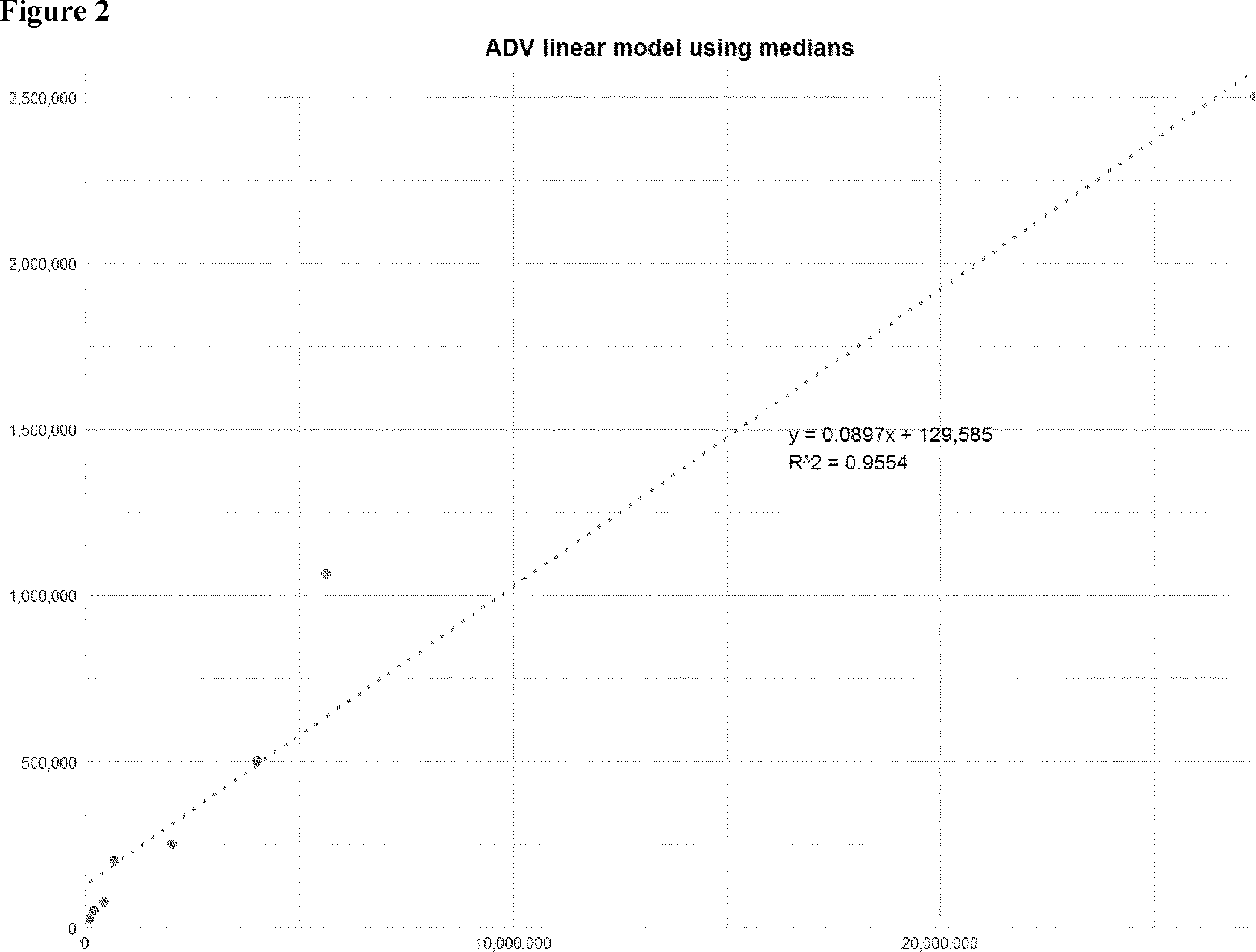

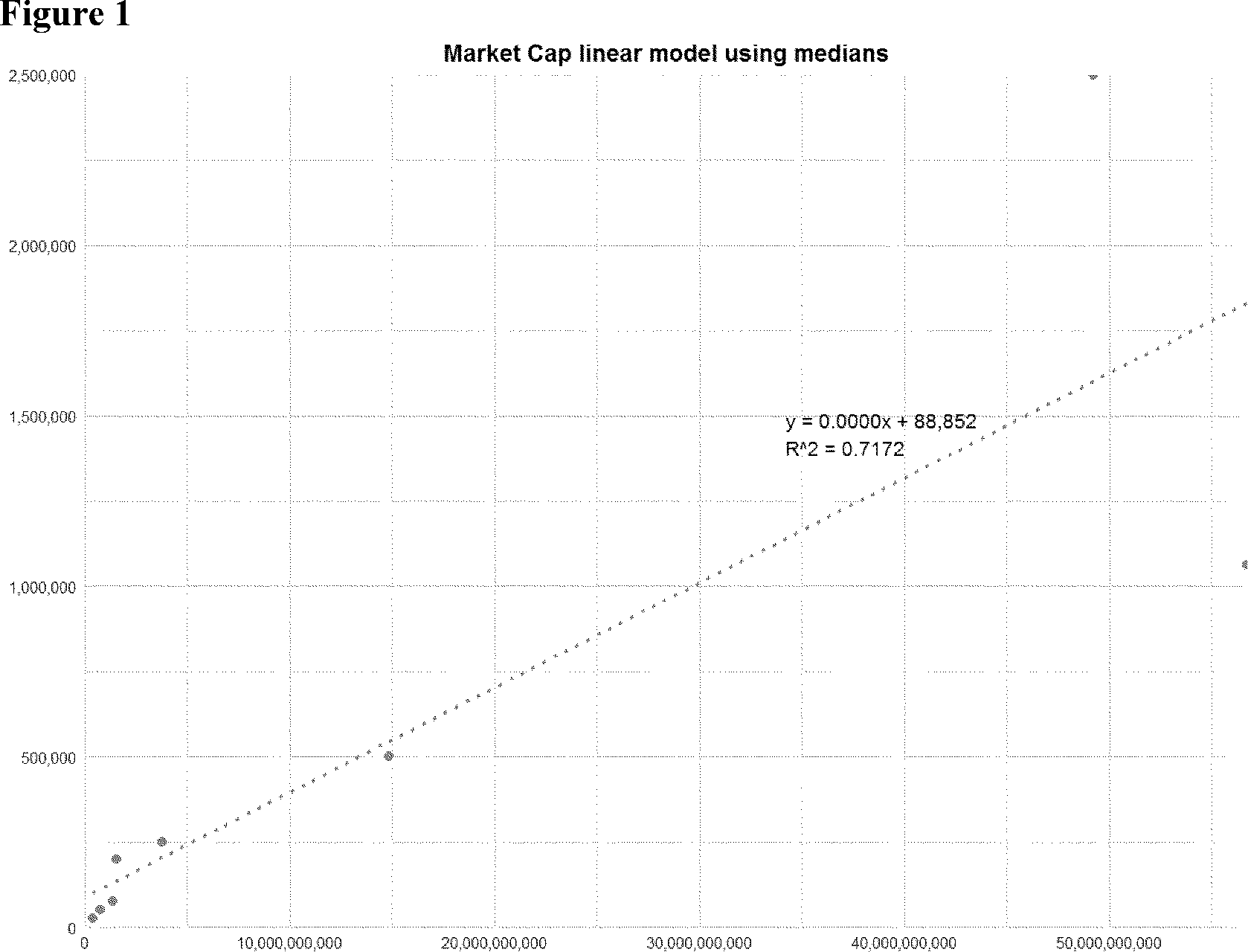

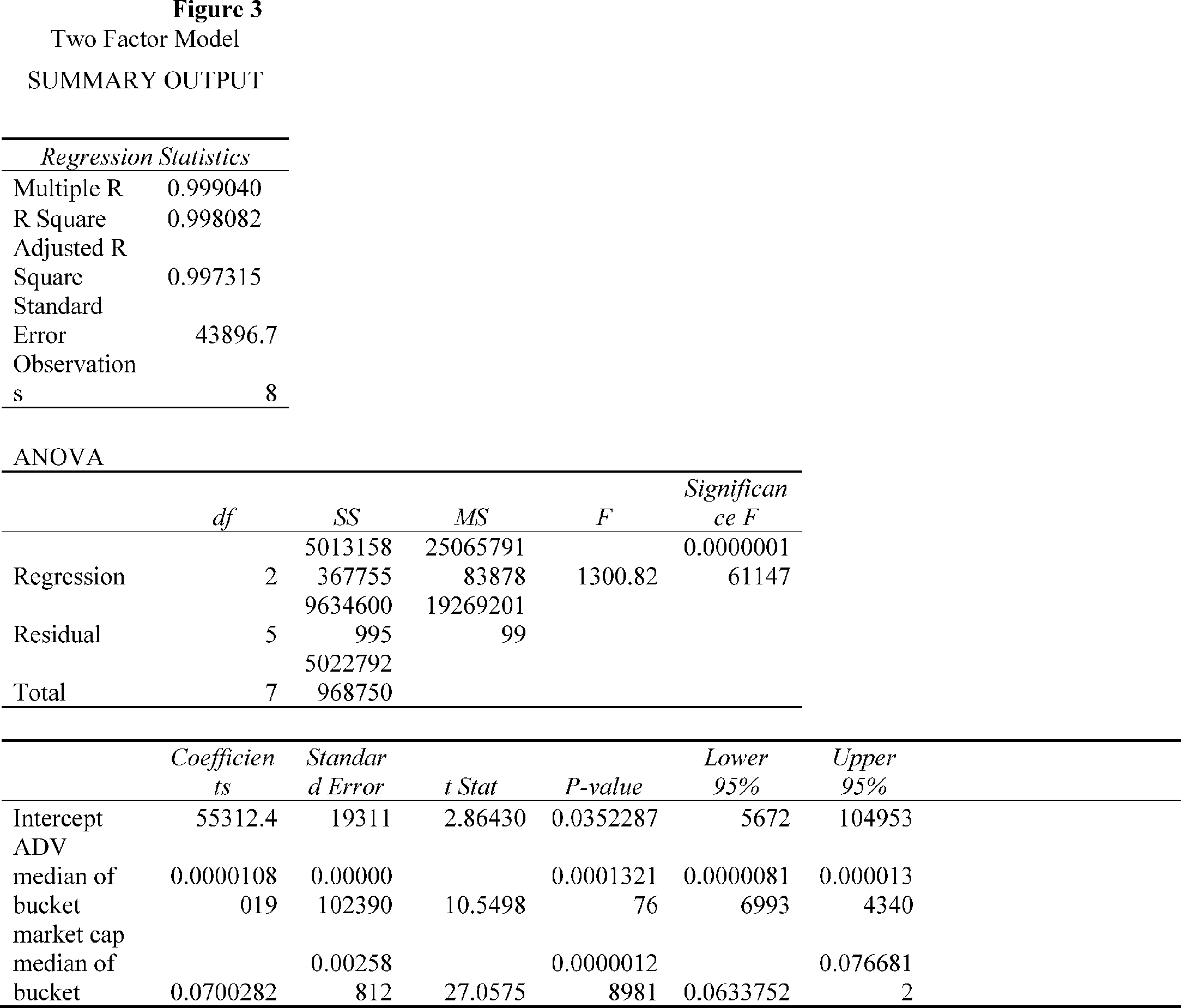

ISE also analyzed the position limits for IBIT by regressing the median elements from each bucket of market capitalization and 180-day ADV of all non-ETF equities, against their respective position limit figures. From this regression, ISE was able to determine the implied coefficients to create a formulaic method for determining an appropriate position limit.[21] ISE utilized a linear model approach which incorporated the median metric from each bucket given the data at both the lower end of each position limit bucket and the higher end of each position limit bucket could be considered significant outliers, thereby skewing the results. Below are various linear models utilizing market capitalization and ADV as well as a two-factor model to determine the appropriate coefficients when both metrics are incorporated into the same model.[22]

( printed page 30011)

Figure 1 utilized IBIT's market capitalization of 52,661,063,818 to arrive at a modeled position limit of 1,707,654.

Figure 2 utilized IBIT's ADV of 61,803,035 to arrive at a modeled position limit of 5,672,081. Based on the aforementioned analysis, ISE noted that the proposed 1,000,000-contract position and exercise limits are appropriate.

Figure 3 shows the results of constructing a two-factor model that employed both metrics (180-day ADV and market capitalization). The result was a modeled position limit of 4,952,107.[23]

Second, ISE reviewed IBIT's data relative to the market capitalization of the entire Bitcoin market in terms of exercise risk and availability of deliverables. As of February 11, 2026, there were approximately 20.5 million Bitcoins in circulation.[24] At a price of $66,938,[25] that equates to a market capitalization of greater than $1.374 trillion US. If a position limit of 1,000,000 contracts were considered, the exercisable risk would represent 7.474% [26] of the shares outstanding of IBIT. Since IBIT has a creation and redemption process managed through the issuer, the position limit was compared to the total market capitalization of the entire Bitcoin market and in that case, the exercisable risk for options on IBIT represented 0.278% of all Bitcoin outstanding.[27] Assuming a scenario in which all options on IBIT shares were exercised given the proposed 1,000,000-contract position limit (and exercise limit), it would have a virtually unnoticed impact on the entire Bitcoin market. This analysis demonstrates that the proposed 1,000,000 per same side position and exercise limit is appropriate for options on IBIT given its liquidity.

Third, ISE reviewed the proposed position limit by comparing it to position limits for derivative products ( printed page 30013) regulated by the Commodity Futures Trading Commission (“CFTC”). While the CFTC, through the relevant Designated Contract Markets, only regulates options positions based upon delta equivalents (creating a less stringent standard), ISE examined equivalent bitcoin futures position limits. In particular, ISE looked to the CME bitcoin futures contract [28] that had a position limit of 2,000 futures.[29] On February 11, 2026, CME bitcoin futures settled at $67,71570,406.33.[30] On February 11, 2026, IBIT settled at $38.29, which would equate to greater than 17,684,774 shares of IBIT if the CME notional position limit were utilized. Since substantial portions of any distributed options portfolio are likely to be out of the money on expiration, an options position limit equivalent to the CME position limit for bitcoin futures (considering that all options deltas are <=1.00) should be a bit higher than the CME implied 176,848 limit. Of note, unlike options contracts, CME position limits are calculated on a net futures-equivalent basis by contract and include contracts that aggregate into one or more base contracts according to an aggregation ratio(s).[31] Therefore, if a portfolio includes positions in options on futures, CME would aggregate those positions into the underlying futures contracts in accordance with a table published by CME on a delta equivalent value for the relevant spot month, subsequent spot month, single month and all month position limits.[32] If a position exceeds position limits because of an option assignment, CME permits market participants to liquidate the excess position within one business day without being considered in violation of its rules. Additionally, if at the close of trading, a position that includes options exceeds position limits for futures contracts, when evaluated using the delta factors as of that day's close of trading, but does not exceed the limits when evaluated using the previous day's delta factors, then the position shall not constitute a position limit violation. Based on the aforementioned analysis, ISE noted that the proposed 1,000,000-contract position and exercise limits are appropriate.

Fourth, ISE analyzed a position limit and exercise limit of 1,000,000 for IBIT options against other options on ETFs with an underlying commodity, namely SPDR Gold Shares (“GLD”), iShares Silver Trust (“SLV”), and ProShares Bitcoin ETF (“BITO”).[33] GLD had a float of 377 million shares [34] and a position limit of 250,000 contracts. SLV had a float of 552 million shares [35] and a position limit of 250,000 contracts. Finally, BITO had 200.89 million shares outstanding [36] and a position limit of 250,000 contracts. As previously noted, position limits and exercise limits are designed to limit the number of options contracts traded on the exchange in an underlying security that an investor, acting alone or in concert with others directly or indirectly, may control. A position limit exercise in GLD would represent 6.63% of the float of GLD; a position limit exercise in SLV would represent 4.53% of the float of SLV; and a position limit exercise of BITO would represent 12.44% of the float of BITO. In comparison, a 1,000,000-contract position limit in IBIT options would represent 7.474% [37] of the float of IBIT. Consequently, the 1,000,000-contract proposed IBIT options position and exercise limits are more conservative than the standards applied to GLD, SLV and BITO, and appropriate.

Fifth, ISE noted that IBIT began trading in penny increments as of January 2, 2025 pursuant to the Penny Interval Program.[38] The Commission noted that evidence and analysis provided in connection with the Penny Pilot demonstrated that the Pilot benefitted investors and other market participants in the form of narrower spreads.[39] The most actively traded options classes are included in the Penny Program based on certain objective criteria (trading volume thresholds and initial price tests). As noted in the Penny Approval Order, the Penny Program reflects a certain level of trading interest (either because the class is newly listed or a class has experienced significant growth in investor interest) to quote in finer trading increments, which in turn should benefit market participants by reducing the cost of trading such options.[40] IBIT options are among a select group of products that have achieved a certain level of liquidity, which has garnered them the ability to trade in finer increments. Failing to increase position and exercise limits for IBIT options, which trade in finer increments, may artificially inhibit liquidity and create price inefficiency. Options on iShares MSCI Emerging Markets, iShares China Large-Cap ETF and iShares MSCI EAFE ETF also trade in penny increments based on their liquidity.

IBIT options have more than sufficient liquidity to garner an increased position and exercise limit of 1,000,000 contracts. Any concerns related to manipulation and protection of investors are mollified by the significant liquidity provision in IBIT. As a general principle, increases in active trading volume and deep liquidity of the underlying securities do not lead to manipulation and/or disruption.

Increasing the position (and exercise) limits for IBIT options would lead to a more liquid and competitive market environment for IBIT options, which will benefit customers that trade these options. Further, the reporting requirement for such options would remain unchanged. Thus, the Exchange will still require that each member that maintains positions in impacted options ( printed page 30014) on the same side of the market, for its own account or for the account of a customer, report certain information to the Exchange. This information includes, but would not be limited to, the options' positions, whether such positions are hedged and, if so, a description of the hedge(s). Market Makers would continue to be exempt from this reporting requirement, however, the Exchange may access Market Maker position information.[41] Moreover, the Exchange's requirement that members file reports with the Exchange for any customer who held aggregate large long or short positions on the same side of the market of 200 or more option contracts of any single class for the previous day will remain at this level and will continue to serve as an important part of the Exchange's surveillance efforts.[42]

The Exchange also has no reason to believe that the growth in trading volume in IBIT will not continue. Rather, the Exchange expects continued options volume growth in IBIT as opportunities for investors to participate in the options markets increase and evolve. The Exchange believes that the current position and exercise limits in IBIT options are restrictive and will hamper the listed options markets from being able to compete fairly and effectively with the over-the-counter (“OTC”) markets. OTC transactions occur through bilateral agreements, the terms of which are not publicly disclosed to the marketplace. As such, OTC transactions do not contribute to the price discovery process on a public exchange or other lit markets. The Exchange believes that without the proposed changes to position and exercise limits for IBIT options, market participants will find the 250,000-contract position limit an impediment to their business and investment objectives as well as an impediment to efficient pricing. As such, market participants may find the less transparent OTC markets a more attractive alternative to achieve their investment and hedging objectives, leading to a retreat from the listed options markets, where trades are subject to reporting requirements and daily surveillance.

The Exchange believes that the existing surveillance procedures and reporting requirements at the Exchange are capable of properly identifying disruptive and/or manipulative trading activity. The Exchange also represents that it has adequate surveillances in place to detect potential manipulation, as well as reviews in place to identify continued compliance with the Exchange's listing standards. These procedures monitor market activity via automated surveillance techniques to identify unusual activity in both options and the underlyings, as applicable. The Exchange also notes that large stock holdings must be disclosed to the Commission by way of Schedules 13D or 13G,[43] which are used to report ownership of stock which exceeds 5% of a company's total stock issue and may assist in providing information in monitoring for any potential manipulative schemes. Further, the Exchange believes that the current financial requirements imposed by the Exchange and by the Commission adequately address concerns regarding potentially large, unhedged positions in equity options. Current margin and risk-based haircut methodologies serve to limit the size of positions maintained by any one account by increasing the margin and/or capital that a member must maintain for a large position held by itself or by its customer.[44] In addition, Rule 15c3-1 [45] imposes a capital charge on members to the extent of any margin deficiency resulting from the higher margin requirement.

Technical Amendments

The Exchange proposes to combine the rule text in Options 9, Section 13(n)(i)(f) and (g) and to re-letter Options 9, Section 13(n)(i)(h) as “g.”

Margin

Currently, Options 6C, Section 3, Proper and Adequate Margin, provides at subparagraph (b) that a member organization must elect to be bound by the initial and maintenance margin requirements of either the Chicago Board Options Exchange (“CBOE”) or New York Stock Exchange (“NYSE”) as the same may be in effect and amended from time to time. The Exchange proposes to update Cboe's name from “Chicago Board Options Exchange” to “Cboe Exchange, Inc.”

2. Statutory Basis

The Exchange believes that its proposal is consistent with Section 6(b) of the Act,[46] in general, and furthers the objectives of Section 6(b)(5) of the Act,[47] in particular, in that it is designed to prevent fraudulent and manipulative acts and practices, to promote just and equitable principles of trade, to foster cooperation and coordination with persons engaged in regulating, clearing, settling, processing information with respect to, and facilitating transactions in securities, to remove impediments to and perfect the mechanism of a free and open market and a national market system, and, in general, to protect investors and the public interest. Additionally, the Exchange believes the proposed rule change is consistent with the Section (6)(b)(5) [48] requirement that the rules of an exchange not be designed to permit unfair discrimination between customers, issuers, brokers, or dealers.

The Exchange believes that increasing the position limit and exercise limit for options on IBIT to 1,000,000 contracts is consistent with the Act. This proposal will remove impediments to and perfect the mechanism of a free and open market and a national market system, and, in general, protect investors and the public interest, because it will provide market participants with the ability to more effectively execute their trading and hedging activities. Also, based on current trading volume, the resulting increase in the position (and exercise) limits for IBIT options may allow Market Makers to maintain their liquidity in these options in amounts commensurate with the continued high consumer demand in IBIT options. The increased position and exercise limits may also encourage other liquidity providers to continue to trade on the Exchange rather than shift their volume to OTC markets, which will enhance the process of price discovery conducted on the Exchange through increased order flow. Further, this amendment would allow institutional investors to utilize IBIT options for prudent risk management purposes.

In addition, the Exchange believes that the current liquidity in IBIT will ( printed page 30015) continue to mitigate concerns regarding potential manipulation of IBIT options and/or disruption of IBIT upon amending the table of position limits in Options 9, Section 13 and the exercise limits in Options 9, Section 15.

Comparing IBIT's data relative to the market capitalization of the entire Bitcoin market in terms of exercise risk and availability of deliverables, ISE was able to conclude that if a position limit of 1,000,000 contracts were considered, the exercisable risk would represent 7.474%[49] of the shares outstanding of IBIT. Since IBIT has a creation and redemption process managed through the issuer (whereby Bitcoin is used to create IBIT shares), the position limit could be compared to the total market capitalization of the entire Bitcoin market and in that case, the exercisable risk for options on IBIT would represent less than 0.278% of all Bitcoin outstanding.[50] This analysis demonstrated that a 1,000,000 contracts position and exercise limits would be appropriate.

Comparing a position limit of 1,000,000 for IBIT options against other options on ETFs with an underlying commodity, namely GLD, SLV and BITO, a position limit exercise in GLD represents 6.63% of the float of GLD, a position limit exercise in SLV represents 4.53% of the float of SLV, and a position limit exercise of BITO represents 12.44% of the float of BITO. In comparison, a 1,000,000-contract position limit in IBIT options would represent 7.474%[51] of the float of IBIT. Consequently, a 1,000,000 IBIT options position limit is generally aligned with the standards applied to GLD, SLV and BITO, and appropriate.

ISE notes that IBIT began trading in penny increments on January 2, 2025 pursuant to the Penny Interval Program.[52] The Commission noted that evidence and analysis provided in connection with the Penny Pilot demonstrated that the Pilot benefitted investors and other market participants in the form of narrower spreads.[53] The most actively traded options classes are included in the Penny Program based on certain objective criteria (trading volume thresholds and initial price tests).[54] As noted in the Penny Approval Order, the Penny Program reflects a certain level of trading interest (either because the class is newly listed or because the class has experienced significant growth in investor interest) to quote in finer trading increments, which in turn should benefit market participants by reducing the cost of trading such options.[55] IBIT options are among a select group of products that have achieved a certain level of liquidity, which has garnered them the ability to trade in finer increments pursuant to the Penny Interval Program. Failing to permit IBIT options to potentially increase position and exercise limits given the trading in finer increments, may artificially inhibit liquidity and create price inefficiency for IBIT options.

Finally, as discussed above, the Exchange's surveillance and reporting safeguards continue to be designed to deter and detect possible manipulative behavior that might arise from increasing or eliminating position and exercise limits in certain classes. The Exchange believes that the current financial requirements imposed by the Exchange and by the Commission adequately address concerns regarding potentially large, unhedged positions in the options on the underlying securities, further promoting just and equitable principles of trading, the maintenance of a fair and orderly market, and the protection of investors.

Technical Amendments

The Exchange's proposal to combine the rule text in Options 9, Section 13(n)(i)(f) and (g) and to re-letter Options 9, Section 13(n)(i)(h) as “g” is non-substantive. Additionally, the amendment to Options 6C, Section 3 to change Cboe's name is a non-substantive amendment.

B. Self-Regulatory Organization's Statement on Burden on Competition

The Exchange does not believe that the proposed rule change will impose any burden on competition that is not necessary or appropriate in furtherance of the purposes of the Act.

The Exchange does not believe that the proposed rule change will impose any burden on inter-market competition as the proposal is not competitive in nature. The Exchange expects that all option exchanges will adopt substantively similar proposals, such that the Exchange's proposal would benefit competition. For these reasons, the Exchange does not believe that the proposed rule change will impose any burden on competition not necessary or appropriate in furtherance of the purposes of the Act.

The Exchange's proposal does not burden intra-market competition because all members would be subject to the position limits in Options 9, Section 13 and corresponding exercise limits in Options 9, Section 15. The Exchange believes that the proposed rule change will also provide additional opportunities for market participants to continue to efficiently achieve their investment and trading objectives for equity options on the Exchange.

Technical Amendments

The Exchange's proposals to combine the rule text in Options 9, Section 13(n)(i)(f) and (g), re-letter Options 9, Section 13(n)(i)(h) as “g,” and change Cboe's name at Options 6C, Section 3 are non-substantive amendments.

C. Self-Regulatory Organization's Statement on Comments on the Proposed Rule Change Received From Members, Participants, or Others

No written comments were either solicited or received.

III. Date of Effectiveness of the Proposed Rule Change and Timing for Commission Action

Because the foregoing proposed rule change does not: (i) significantly affect ( printed page 30016) the protection of investors or the public interest; (ii) impose any significant burden on competition; and (iii) become operative for 30 days from the date on which it was filed, or such shorter time as the Commission may designate, it has become effective pursuant to Section 19(b)(3)(A)(iii) of the Act [56] and subparagraph (f)(6) of Rule 19b-4 thereunder.[57]

A proposed rule change filed pursuant to Rule 19b-4(f)(6) under the Act normally does not become operative for 30 days after the date of its filing. However, Rule 19b-4(f)(6)(iii) [58] permits the Commission to designate a shorter time if such action is consistent with the protection of investors and the public interest. The Exchange has requested that the Commission waive the 30-day operative delay so that the proposal may become operative immediately upon filing. The Commission notes that the proposal will conform the Exchange's IBIT options position and exercise limits with ISE's IBIT options position and exercise limits.[59] Therefore, the proposal raises no novel legal or regulatory issues. Thus, the Commission believes that waiver of the 30-day operative delay is consistent with the protection of investors and the public interest. Accordingly, the Commission hereby waives the 30-day operative delay and designates the proposed rule change operative upon filing.[60]

At any time within 60 days of the filing of the proposed rule change, the Commission summarily may temporarily suspend such rule change if it appears to the Commission that such action is necessary or appropriate in the public interest, for the protection of investors, or otherwise in furtherance of the purposes of the Act.

IV. Solicitation of Comments

Interested persons are invited to submit written data, views and arguments concerning the foregoing, including whether the proposed rule change is consistent with the Act. Comments may be submitted by any of the following methods:

Electronic Comments

- Use the Commission's internet comment form (https://www.sec.gov/rules/sro.shtml); or

- Send an email torule-comments@sec.gov. Please include file number SR-Phlx-2026-29 on the subject line.

Paper Comments

- Send paper comments in triplicate to Secretary, Securities and Exchange Commission, 100 F Street NE, Washington, DC 20549-1090.

All submissions should refer to file number SR-Phlx-2026-29. This file number should be included on the subject line if email is used. To help the Commission process and review your comments more efficiently, please use only one method. The Commission will post all comments on the Commission's internet website ( https://www.sec.gov/rules/sro.shtml. Copies of the filing will be available for inspection and copying at the principal office of the Exchange. Do not include personal identifiable information in submissions; you should submit only information that you wish to make available publicly. We may redact in part or withhold entirely from publication submitted material that is obscene or subject to copyright protection. All submissions should refer to file number SR-Phlx-2026-29 and should be submitted on or before June 11, 2026.

For the Commission, by the Division of Trading and Markets, pursuant to delegated authority.[61]

Sherry R. Haywood,

Assistant Secretary.