Enhancement of Emerging Growth Company Accommodations and Simplification of Filer Status for Reporting Companies

The Securities and Exchange Commission ("Commission") proposes amendments to streamline filer statuses for Securities Exchange Act of 1934 ("Exchange Act") reporting companies i...

The Securities and Exchange Commission (“Commission”) proposes amendments to streamline filer statuses for Securities Exchange Act of 1934 (“Exchange Act”) reporting companies into two primary categories: large accelerated filers and non-accelerated filers. The Commission further proposes to raise the threshold and seasoning requirements for large accelerated filer status and extend certain existing accommodations and scaled disclosures, including those for smaller reporting companies and emerging growth companies, to all non-accelerated filers, while continuing to require compliance with non-scaled disclosure from large accelerated filers. The Commission also proposes to extend the deadlines to file periodic reports for the smallest non-accelerated filers, as measured by total assets. Finally, the Commission also proposes to update the rules that define which issuers are considered small entities for purposes of the Regulatory Flexibility Act (“RFA”).

DATES:

Comments should be received on or before July 20, 2026.

ADDRESSES:

Comments may be submitted by any of the following methods:

○ Send an email to

rule-comment@sec.gov.

Please include File Number S7-2026-18 on the subject line.

Paper Comments

○ Send paper comments to Vanessa A. Countryman, Secretary, Securities and Exchange Commission, 100 F Street NE, Washington, DC 20549-1090.

All submissions should refer to File Number S7-2026-18. This file number should be included on the subject line if email is used. To help the Commission process and review your comments more efficiently, please use only one method of submission. The Commission will post all comments on the Commission's website (

https://www.sec.gov/comments/s7-2026-18/enhancement-emerging-growth-company-accommodations-simplification-filer-statusreporting-companies). Do not include personally identifiable information in submissions; you should submit only information that you wish to make available publicly. The Commission may redact in part or withhold entirely from publication submitted material that is obscene or subject to copyright protection.

Studies, memoranda, or other substantive items may be added by the Commission or staff to the comment file during this rulemaking. A notification of the inclusion in the comment file of any such materials will be made available on the Commission's website. To ensure direct electronic receipt of such notifications, sign up through the “Stay Connected” option at

www.sec.gov

to receive notifications by email.

Nabeel Cheema, Special Counsel, and Stephanie Sullivan, Associate Chief Accountant, Division of Corporation Finance, at (202) 551-3430, and Angela Mokodean, Senior Special Counsel, Division of Investment Management, at (202) 551-6792, U.S. Securities and Exchange Commission, 100 F Street NE, Washington, DC 20549.

SUPPLEMENTARY INFORMATION:

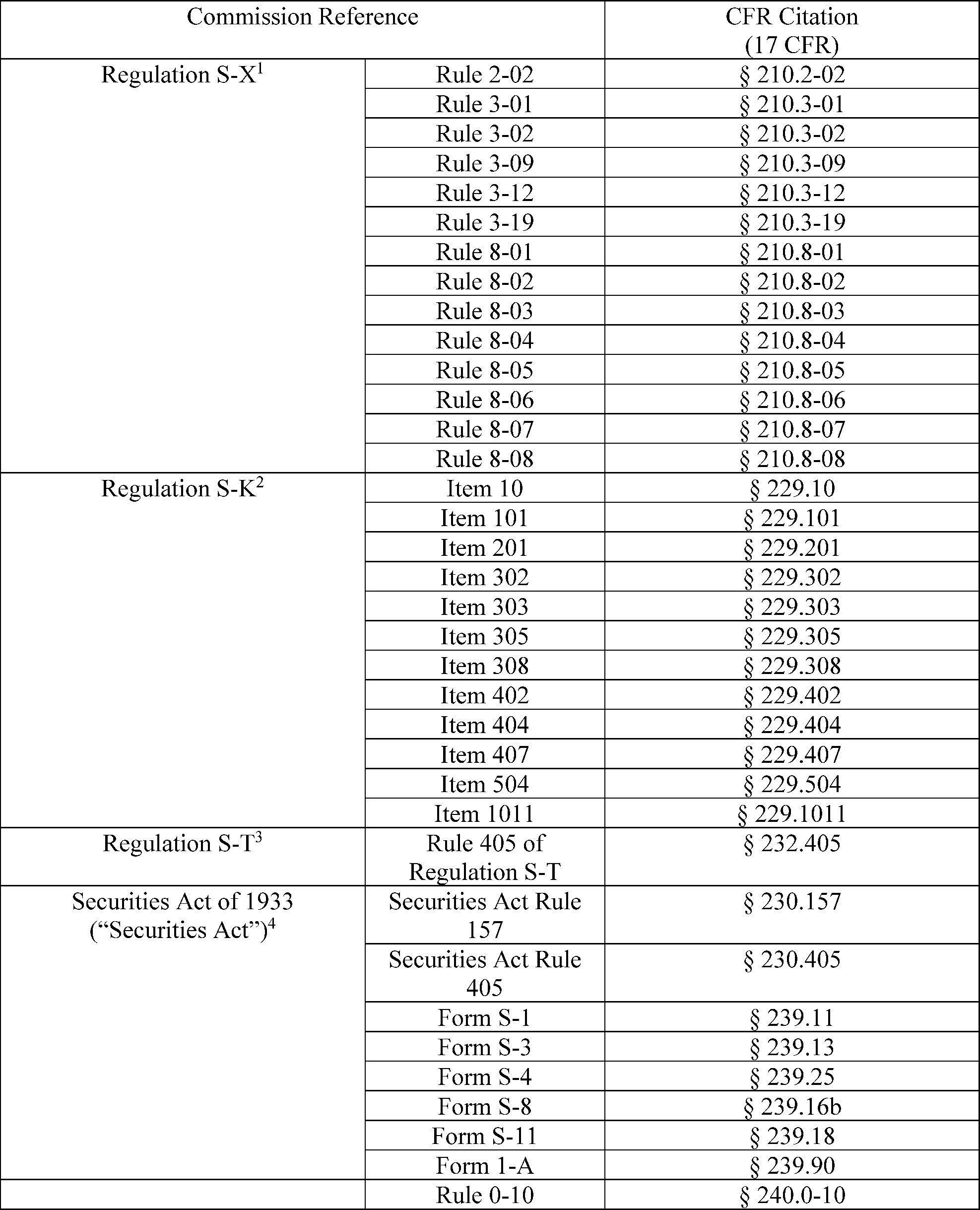

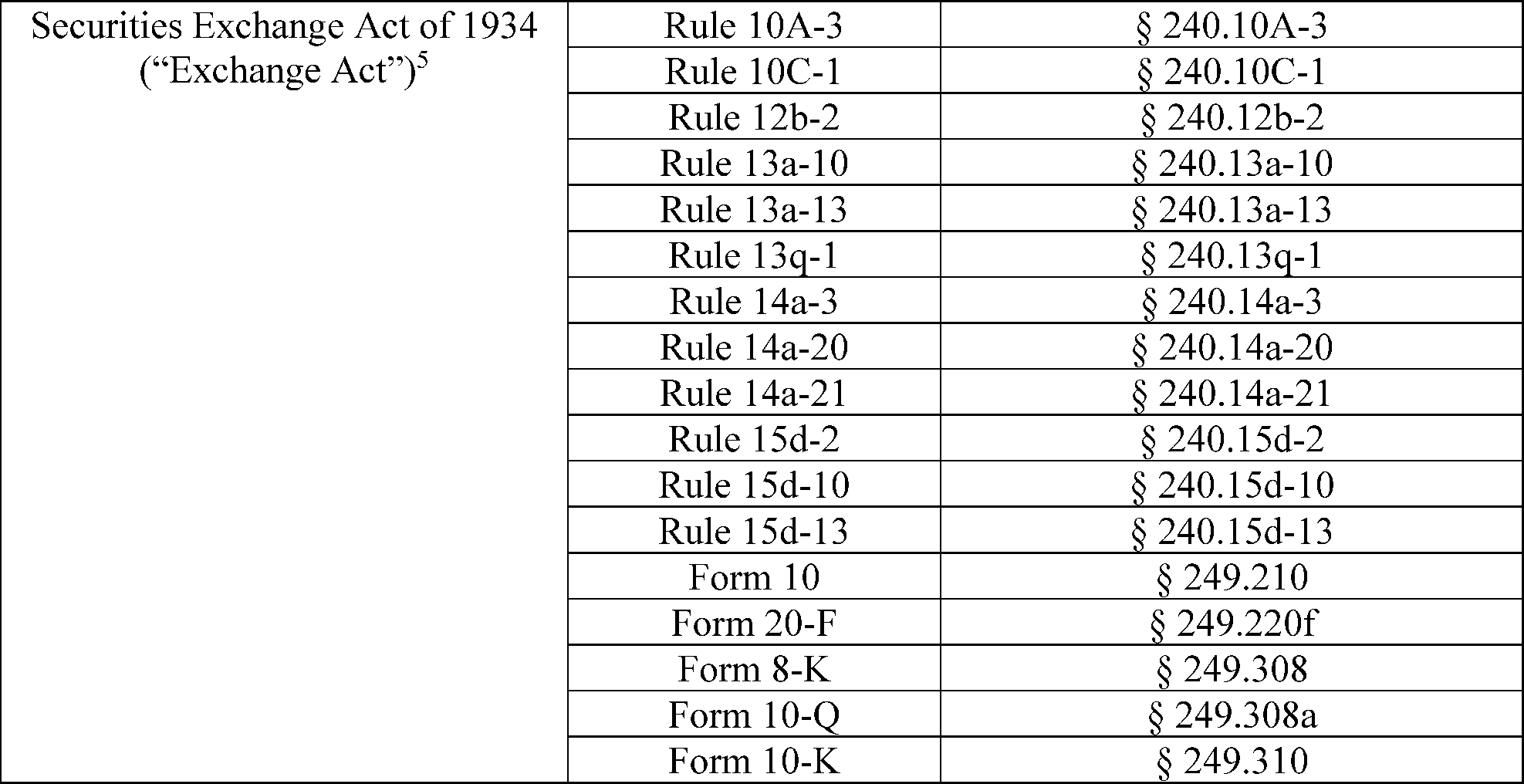

The Commission is proposing to amend or add the following rules and forms:

( printed page 30087)

( printed page 30088)

Table of Contents

I. Introduction

A. Exchange Act Reporting Prior to 2002

B. Accelerated Filer Status; Sarbanes-Oxley Act

C. ICFR Requirements

D. Actions Related to Smaller Reporting and Emerging Growth Companies

1. Establishment of SRC Status

2. The JOBS Act and EGC Status

3. Recent Amendments and Filer Status Complexity

II. Discussion of Proposed Rules

A. Large Accelerated Filer Status Amendments

1. Public Float Threshold

2. Public Float Determination

3. Seasoning

B. Non-Accelerated Filer Amendments

1. Non-Accelerated Filer Definition

2. ICFR and the Auditor Attestation Requirement

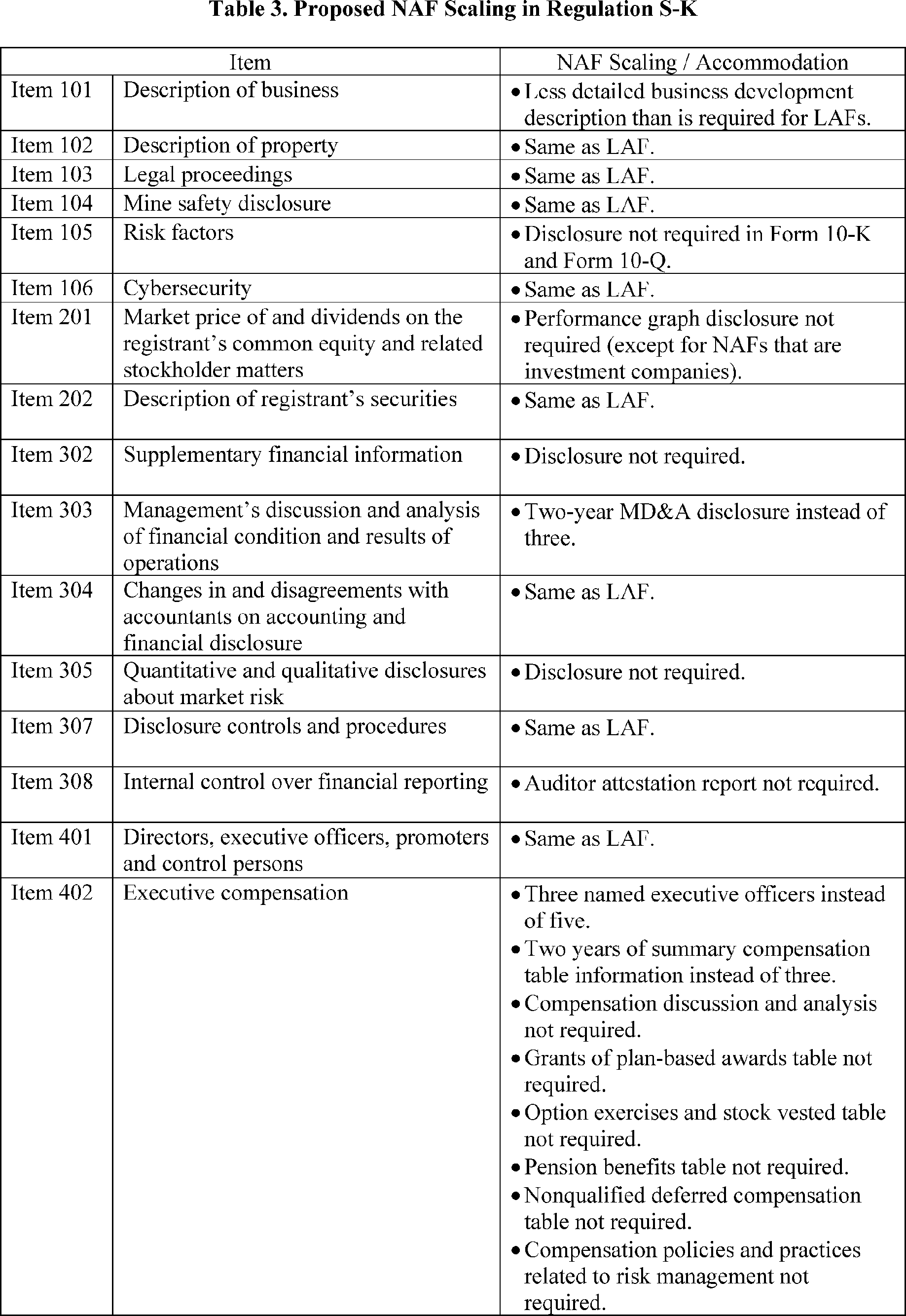

3. Extension of SRC and EGC Accommodations and Disclosure Requirements

4. Application to Other Filer Types

5. Summary of Requirements for LAFs and NAFs Under the Proposal

C. Small Non-Accelerated Filers

D. Proposed Transition Period

E. Updating Small Entity Definitions

F. Other Amendments

III. Other Matters

IV. Economic Analysis

A. Baseline and Affected Parties

1. Regulatory Baseline

2. Affected Parties

3. Registrant Characteristics

B. Economic Benefits and Costs

1. General Economic Effects of the Proposed Amendments

2. Amendments to LAF Definition

3. Exemption From ICFR Auditor Attestation

4. The Expansion of the Subset of Registrants Eligible for Extended Periodic Report Filing Deadlines

5. Extending SRC and Certain EGC Accommodations to All NAFs

6. Extending Filing Deadlines for the Smallest NAFs

7. Updating Small Entity Definition

8. Additional Considerations

9. Aggregate Monetized Benefits and Costs

C. Anticipated Effects on Efficiency, Competition, and Capital Formation

D. Reasonable Alternatives

1. LAF Public Float Threshold

2. Seasoning Requirement

3. Regulatory Accommodations for NAFs

4. SNFs

E. Request for Comment

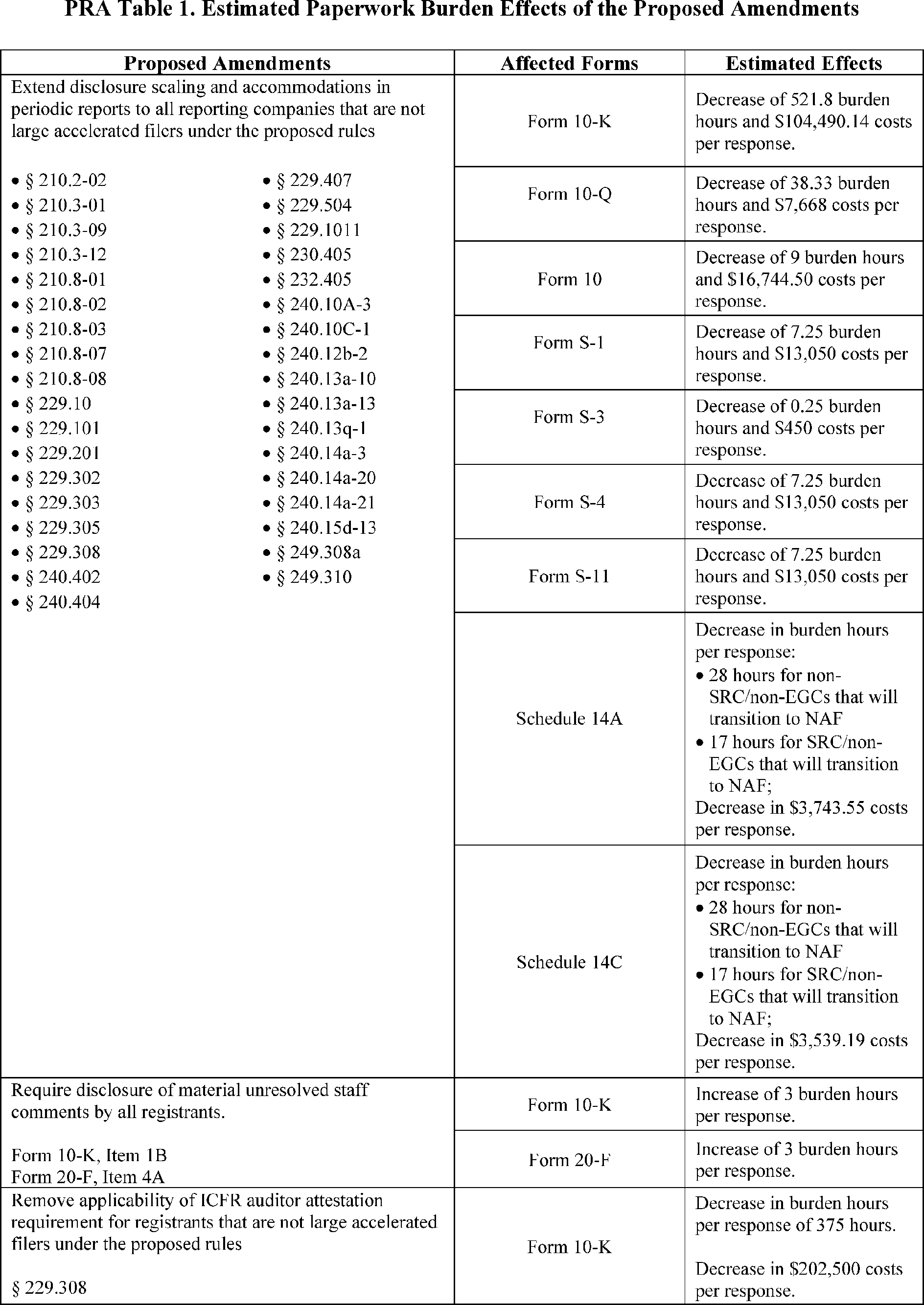

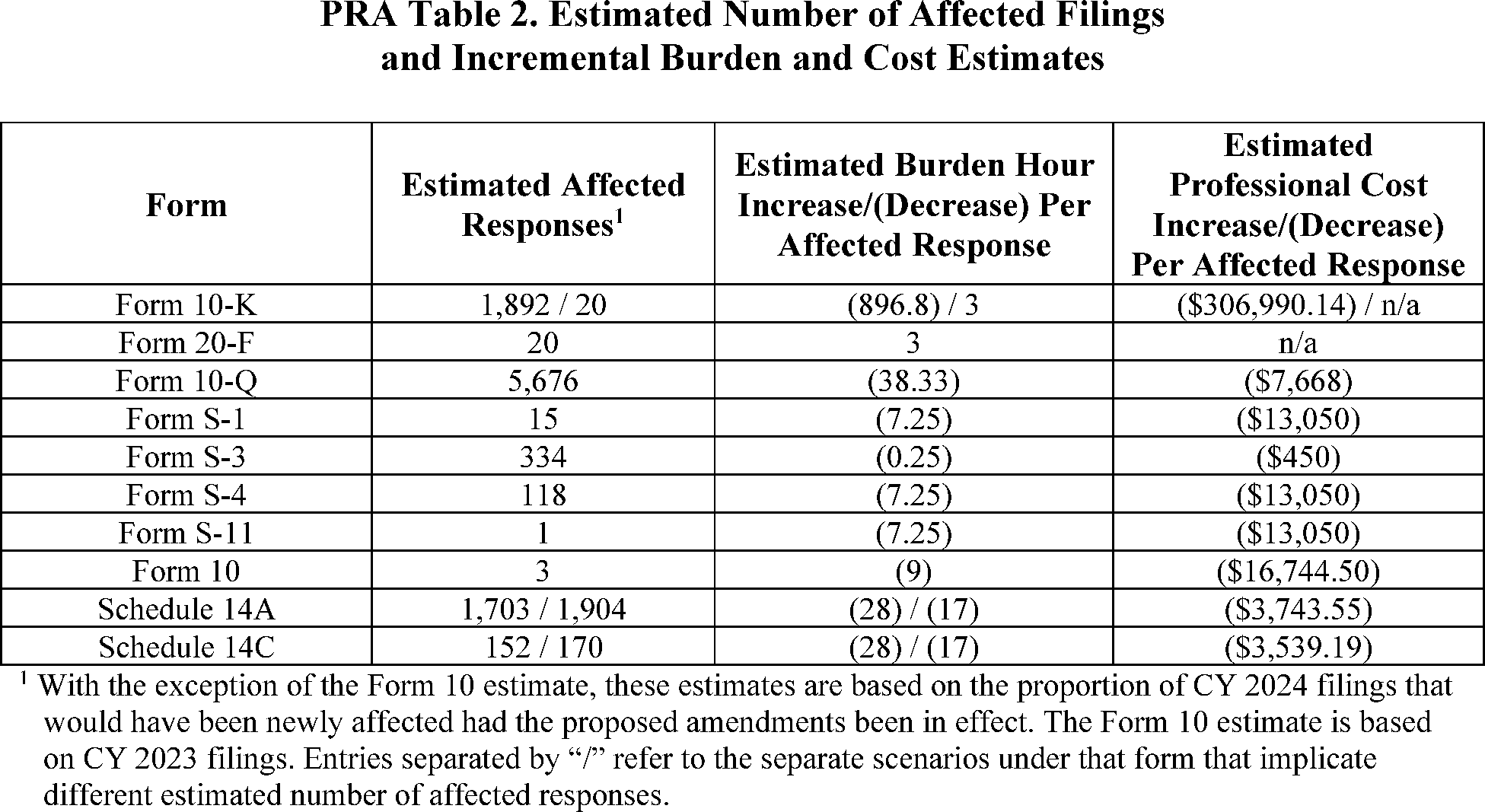

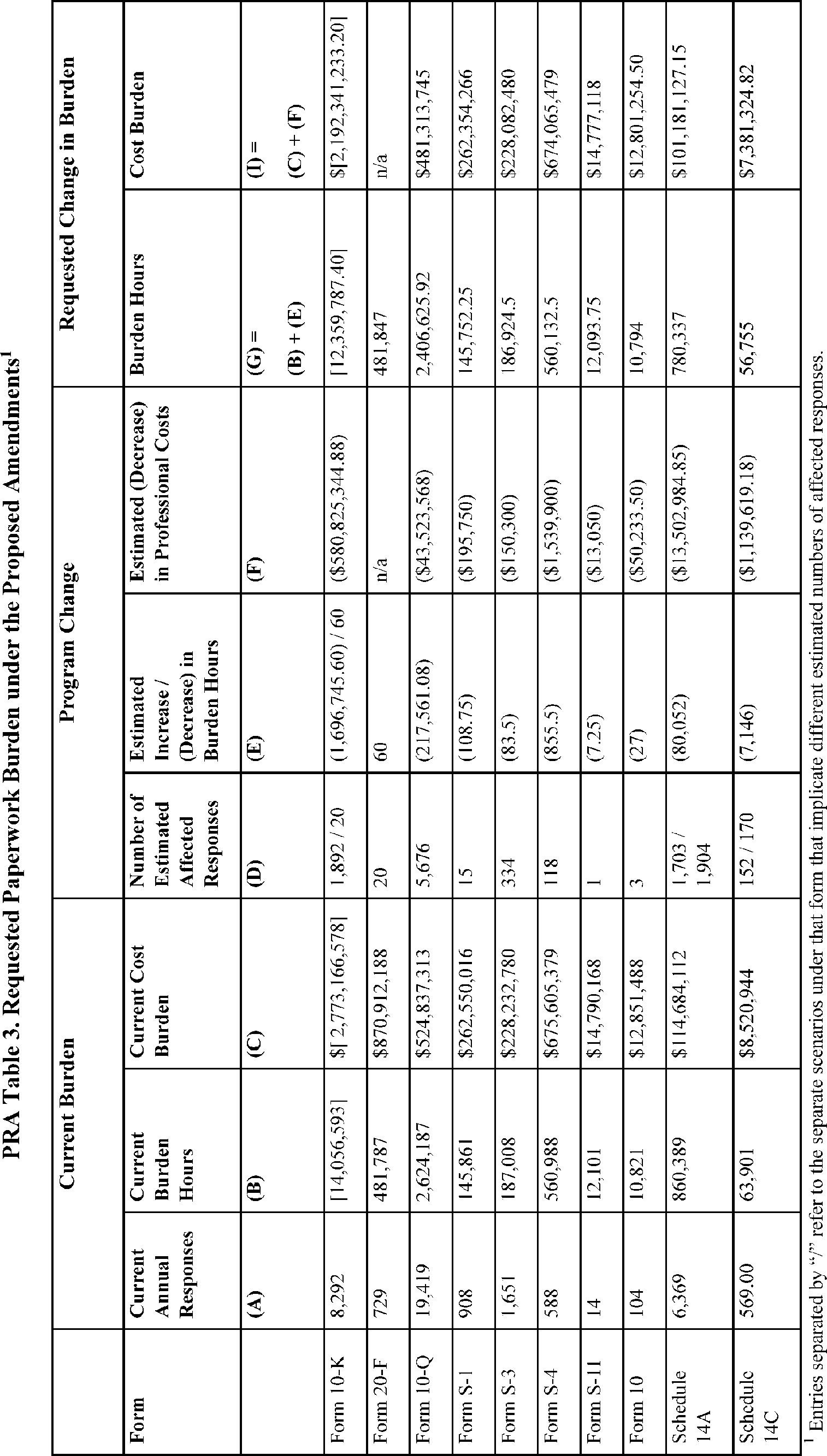

V. Paperwork Reduction Act

A. Summary of the Collections of Information

B. Estimated Paperwork Burden Effects of the Proposed Amendments

C. Incremental and Aggregate Burden and Cost Estimates

D. Request for Comment

VI. Congressional Review Act

VII. Initial Regulatory Flexibility Act Analysis

A. Reasons for, and Objectives of, the Proposed Action

B. Legal Basis

C. Small Entities Subject to the Proposed Amendments

D. Projected Reporting, Recordkeeping, and Other Compliance Requirements

E. Duplicative, Overlapping, or Conflicting Federal Rules

F. Significant Alternatives

Statutory Authority

I. Introduction

From their inception, the U.S. securities laws have sought to require full and fair disclosure by companies seeking to raise capital from investors and access the public markets.[6]

In enacting broad investor protections and disclosure requirements under the securities laws, Congress also recognized the need to take into account the burdens of registration.[7]

A core function of the Exchange Act is to extend disclosure-based investor protections that are provided for public offerings of securities under the Securities Act to post-distribution trading in the secondary markets. This is accomplished primarily by sections 12,[8]

13(a),[9]

and 15(d) [10]

of the Exchange Act, which impose periodic and current reporting requirements on companies:

( printed page 30089)

with exchange-listed securities (section 12(b)); with widely held classes of equity securities (section 12(g)); or that have completed a public offering registered under the Securities Act (section 15(d)).[11]

These registrants [12]

must file reports prescribed by the Commission, which generally include annual reports on Form 10-K and quarterly reports on Form 10-Q.[13]

With respect to investment companies, business development companies (“BDCs”) and face-amount certificate companies are also subject to these reporting requirements.[14]

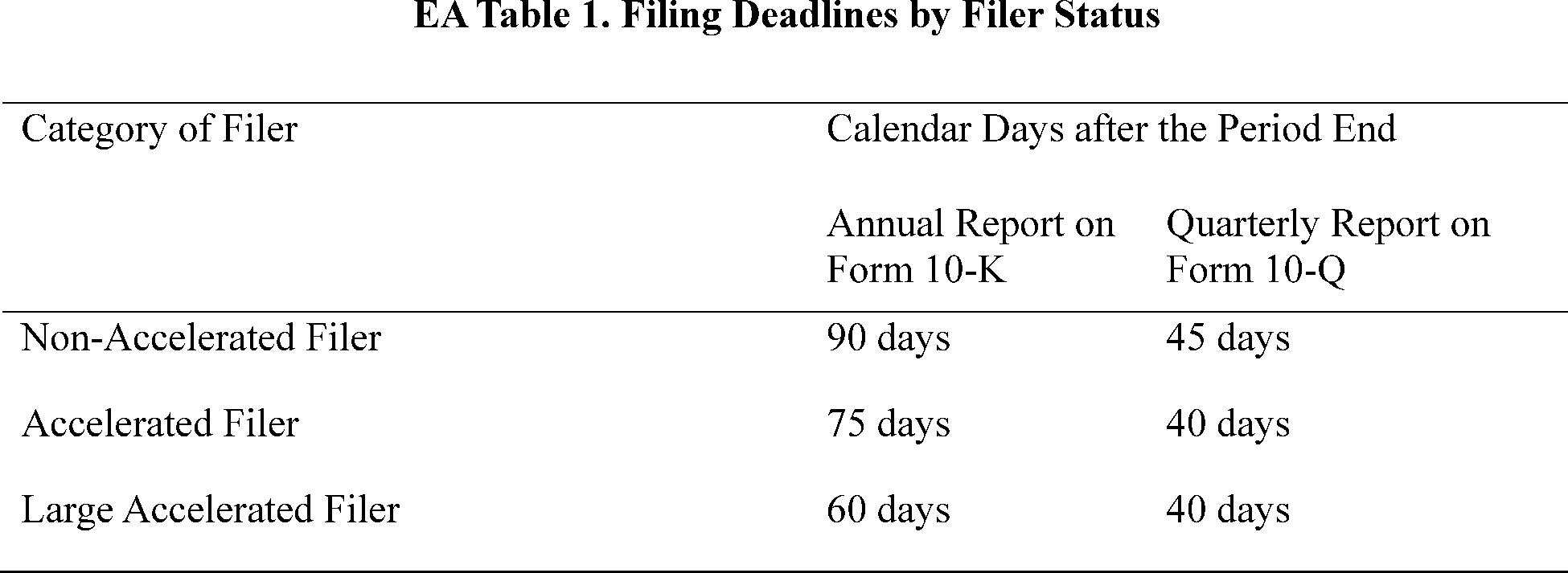

Over time, the Commission and Congress have adopted various “filer statuses” to establish tiers of registrants and offer certain accommodations by tier, including as to the timing and content of this periodic reporting. Current filer statuses include:

Large accelerated filer

(“LAF”),

accelerated filer[15]

(“AF”), and

non-accelerated filer

(“NAF”).

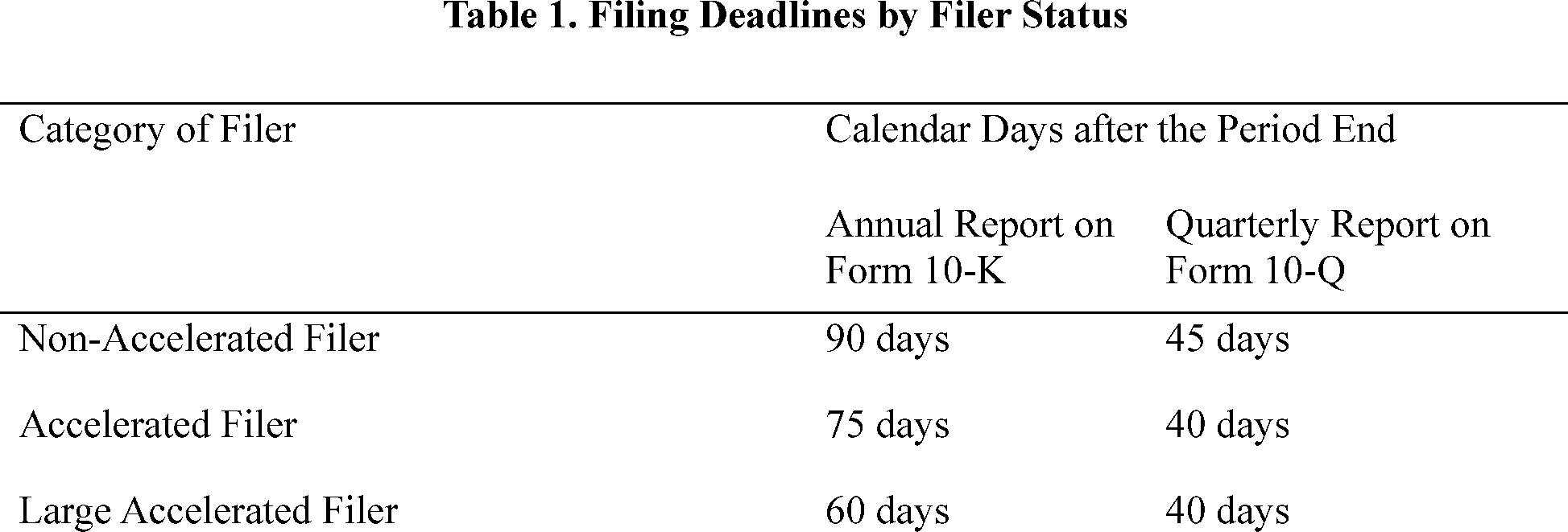

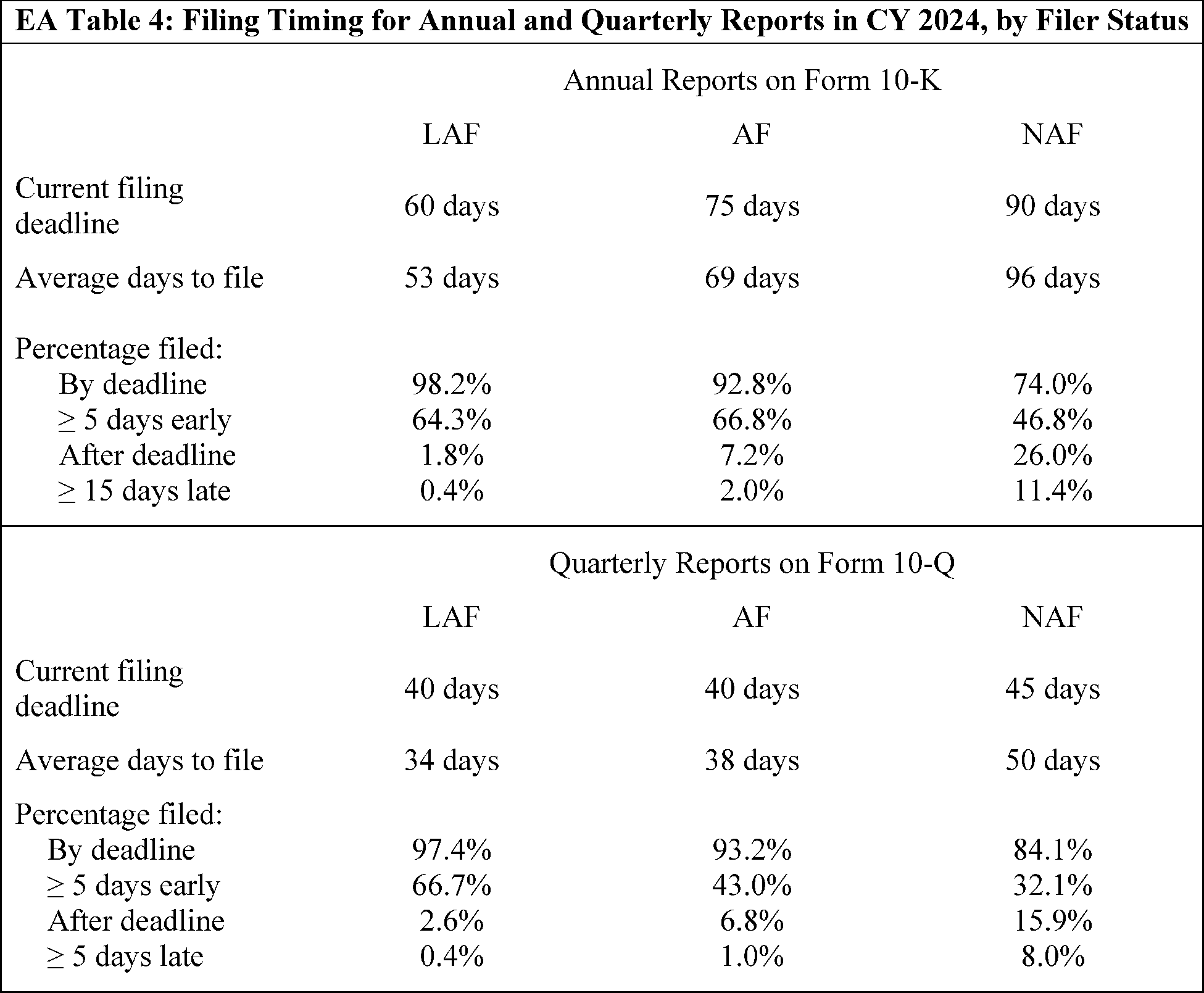

○ Filing deadlines for periodic reports depend on whether a registrant is classified as an LAF, an AF, or neither of these, which we refer to as an NAF.[16]

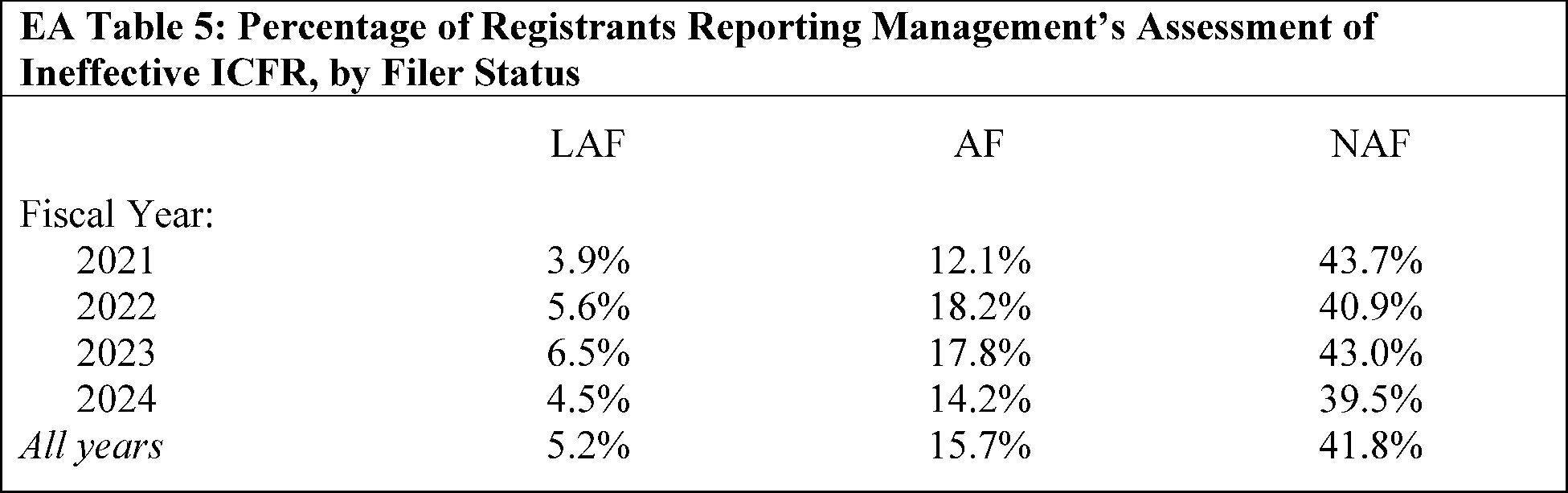

○ Only LAFs and AFs are required to have the registered public accounting firm that prepares or issues their financial statement audit report attest to, and report on, management's assessment of the effectiveness of internal control over financial reporting (“ICFR”) (“ICFR auditor attestation”) under section 404(b) of the Sarbanes-Oxley Act of 2002 (“Sarbanes-Oxley Act”).[17]

Smaller reporting company[18]

(“SRC”) is a regulatory status that applies to smaller registrants permitting those registrants to comply with a number of scaled disclosure requirements, discussed in detail below,[19]

which notably include scaled financial statement disclosure and scaled executive compensation disclosure, among other accommodations.

Emerging growth company

(“EGC”) is a statutorily-defined status that applies to registrants for the first five years after their initial public offering so long as they do not become an LAF or surpass revenue and debt issuance limitations.[20]

The EGC accommodations are described more fully below [21]

and notably include scaled financial statement disclosure in an EGC's initial public equity offering registration statement, deferred adoption of certain new or revised financial accounting standards, scaled executive compensation disclosure, and an exemption from the ICFR auditor attestation requirement.[22]

The table below lists the periodic reporting deadlines that currently apply to LAFs, AFs, and NAFs.[23]

( printed page 30090)

The filer status framework that has developed is layered and complex.[24]

Under the current system, registrants must annually reevaluate their filer status at the end of their fiscal year. To do so, they consider both their public float [25]

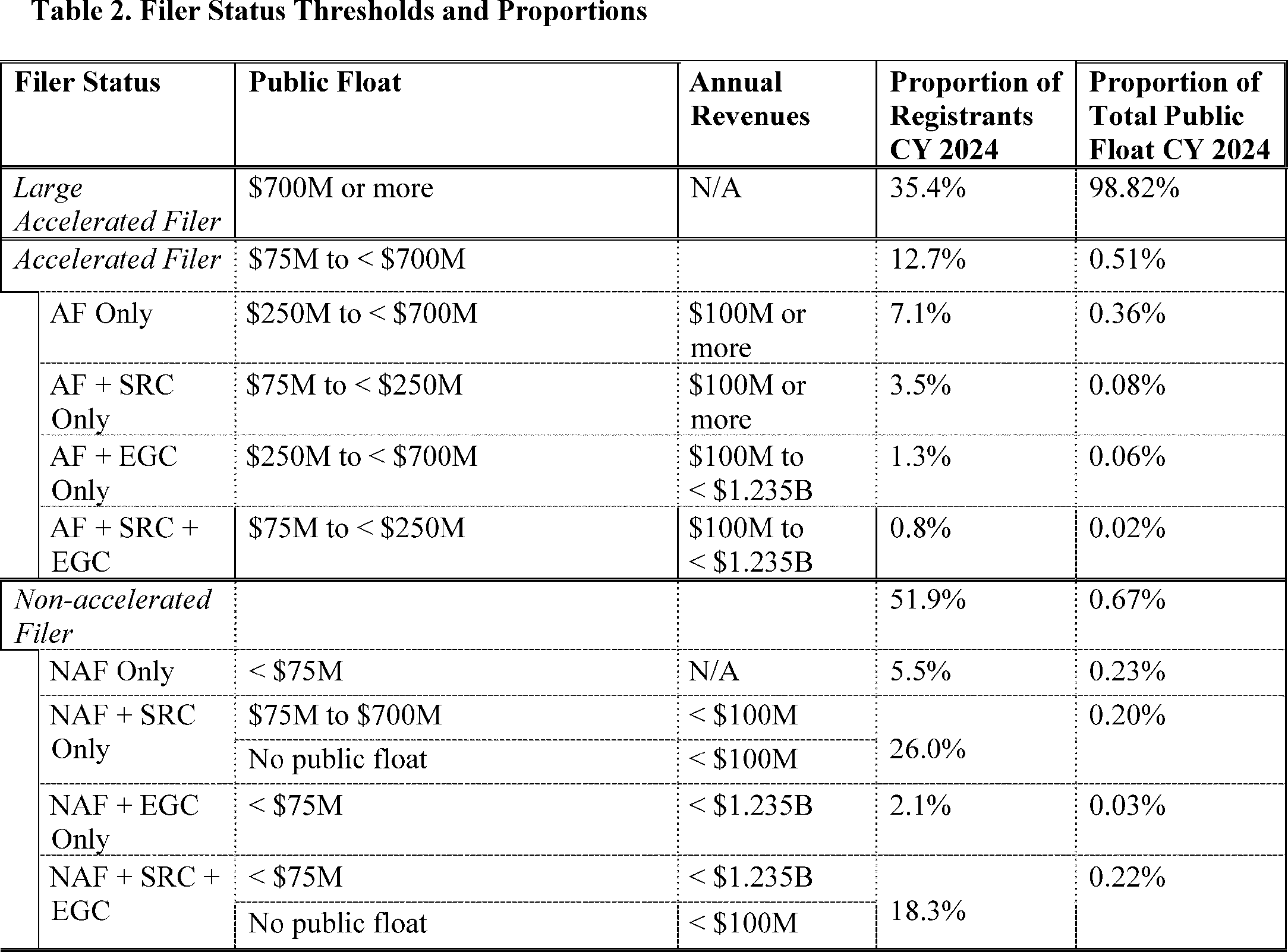

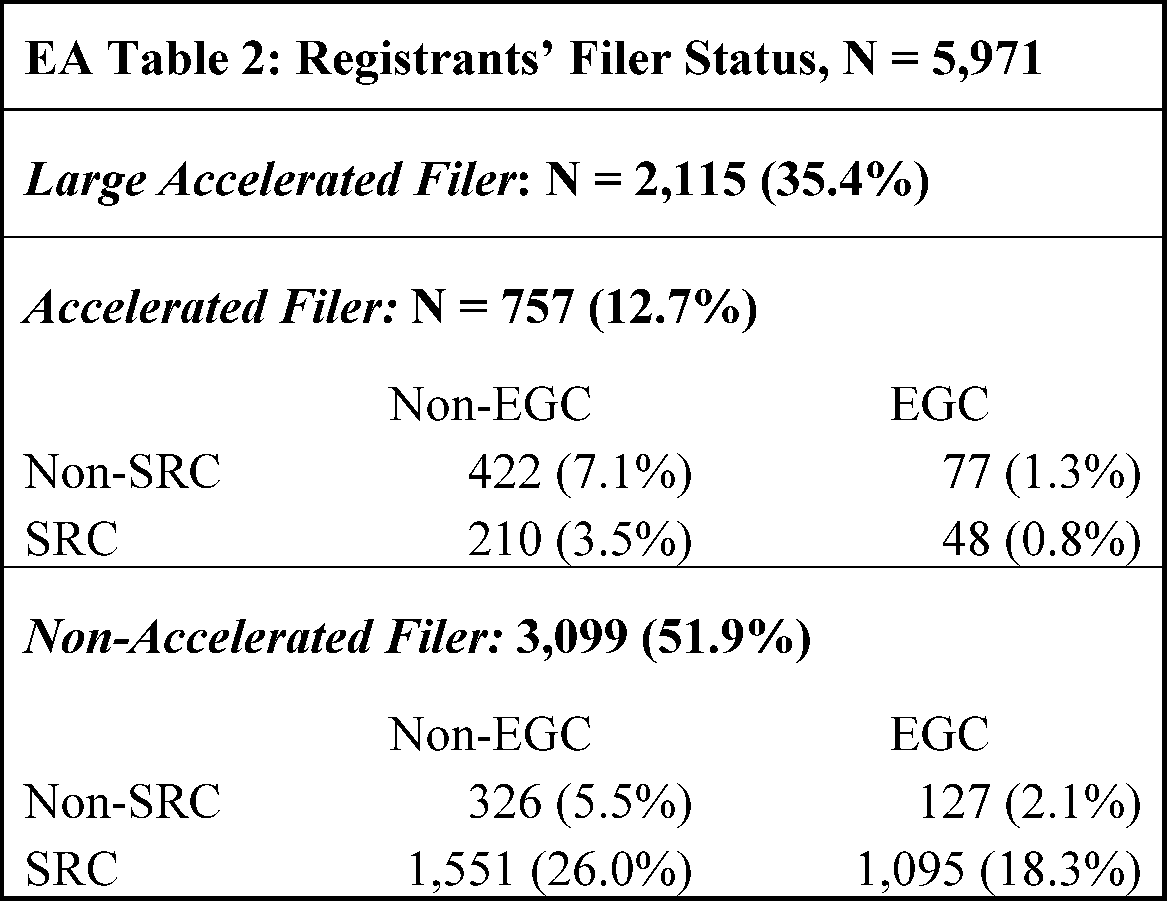

as of the end of their second fiscal quarter and their annual revenue, and compare those figures to thresholds that vary based on whether a registrant is entering or exiting a particular filer status. Additionally, registrants qualifying as EGCs must evaluate whether they met any of the disqualifying provisions of an EGC throughout the year. The table below illustrates the combinations of filer statuses that are possible today, highlights the overlap that can occur among filer statuses, and provides the entry thresholds for each status and the proportion of registrants in each permutation:[26]

The table reflects the current thresholds for initially entering into a particular status, but, under existing rules, the thresholds are often different for determining when a registrant transitions out of that status. Under current rules, LAFs transition to AF status when their public float falls below $560 million, and AFs and LAFs transition out of either such status when their public float falls below $60 million or they determine that they are eligible to use the requirements for SRCs under the revenue test in paragraph (2) or (3)(iii)(B) of the smaller reporting company definitions in 17 CFR 230.405 and 17 CFR 240.12b-2. Similarly, once a registrant exits SRC status, the registrant will only transition back into SRC status if its public float falls below $200 million, or its public float falls

( printed page 30091)

below $560 million and its revenues fall below $80 million.[27]

In addition, because the definitions for the accelerated filer statuses rely in part on SRC status, these transition thresholds also affect accelerated filer status determinations.

In addition to the complexity of the current filer status framework, we note that the number of Exchange Act reporting companies filing on domestic forms fell from 6,996 in 2004 to 5,976 in 2024.[28]

Unsurprisingly, a similar time period (2009-2017) saw significant growth in private markets, with private markets regularly outpacing public markets in capital raised.[29]

Recent studies point to a variety of conditions influencing companies that might previously have gone public to remain private, with the regulatory burdens and costs of being a public company consistently considered to be among the factors that have led to this trend.[30]

The Commission's two most recent Small Business Forums explored the obstacles facing smaller companies trying to go public. In 2025, the issues discussed included having to produce three years of audited financial statements, having to produce reports on a quarterly basis, the volume of disclosure requirements, and the complexity of the filer status framework.[31]

In 2026, many of the same themes were explored, with notable discussion on the cost of compliance with section 404(b) of the Sarbanes-Oxley Act, the impact on a registrant's ability to plan for those costs in light of an AF public float threshold that is based on a single measurement date, and the limited personnel and resources small companies can devote to such costs.[32]

Similar recommendations came out of prior years' forums and other roundtables.[33]

We are also aware of continued concerns regarding the cost of compliance with the ICFR auditor attestation requirement under section 404(b) of the Sarbanes-Oxley Act.[34]

Some comments on the 2019 Accelerated Filer Release stated that the ICFR auditor attestation requirement is the most costly aspect of being an AF and indicated that, in relative terms, it is particularly costly for low-revenue registrants.[35]

In addition, a recent Government Accountability Office (“GAO”) study found that Section 404(a) and (b) compliance costs are more burdensome in relative terms for smaller companies.[36]

At the same time, the ICFR auditor attestation requirement has benefits for investors, including that it enhances the reliability of management's disclosure related to ICFR and may help a registrant identify a significant deficiency or identify and disclose a material weakness in ICFR that had not been identified or properly characterized by management.[37]

While registration and entry into the public capital markets is not always necessary or appropriate for smaller or emerging companies,[38]

a robust pipeline of companies joining the public markets benefits investors by providing them with a more diverse set of investment opportunities and greater transparency.

( printed page 30092)

It also benefits companies in various ways, including by providing them new sources of capital at a potentially lower cost. The Commission has long considered the regulatory burdens of public company registration and ongoing compliance with the regulations that apply to public companies. Indeed, the Commission has previously taken steps with the aim of increasing the viability of entry into the public markets to more companies, by adopting simplified registration rules and processes for issuers while carefully balancing investors' need for timely and appropriate disclosure. For example, in a series of actions spanning decades, the Commission has routinely simplified and tailored smaller issuers' disclosure obligations.[39]

In 2005, the Commission reformed the securities offering process by, among other actions, liberalizing permitted offering communications, updating prospectus delivery requirements, and modernizing the shelf registration provisions.[40]

Nonetheless, changes in the securities laws have resulted in an increasingly complicated regulatory framework that warrants reconsideration, including a reassessment of whether the disclosure burdens faced by registrants are properly balanced with the corresponding benefits to investors and markets.

We are therefore proposing amendments to our regulations to rationalize the existing Exchange Act filer status framework, which will simplify reporting and disclosure requirements and reduce burdens on most reporting companies, while continuing to seek full and fair disclosure for investors. To provide context to our proposed amendments, we briefly trace the evolution of the current filer status framework below.

A. Exchange Act Reporting Prior to 2002

The Commission adopted the “integrated disclosure system” in 1982 following several years of analysis of the disclosure rules under the Securities Act and the Exchange Act.[41]

Prior to the adoption of the integrated disclosure system, separate disclosure regimes applied to Securities Act registration statements and Exchange Act registration and periodic reporting, which often resulted in overlapping and duplicative requirements. At the time the integrated disclosure system was adopted, the Commission stated that the “goal of the Commission's integrated disclosure program has been to revise or eliminate overlapping or unnecessary disclosure and dissemination requirements wherever possible, thereby reducing burdens on registrants while at the same time ensuring that security holders, investors and the marketplace have been provided with meaningful nonduplicative information upon which to base investment decisions.” [42]

Under the integrated disclosure system, most registration and reporting forms under the Securities Act and the Exchange Act refer to common disclosure requirements codified in Regulation S-K and Regulation S-X. In recognition of the difficulties that smaller issuers were facing in accessing the capital markets, the Commission adopted Regulation S-B in 1992, an integrated disclosure system tailored specifically to a set of “small business issuers,” as defined by revenues and public float, and provided specialized forms under the Securities Act and Exchange Act that referenced simplified disclosure requirements for these issuers.[43]

As a result of these accommodations, prior to 2002, there were effectively two Exchange Act filer statuses: a “default” category of issuers that filed periodic reports on Forms 10-K and 10-Q under Regulation S-K, and a small business issuer category that filed periodic reports on Forms 10-KSB and 10-QSB under Regulation S-B. Commission rules applied uniform filing deadlines to all Exchange Act reporting companies' periodic reports: 90 days after fiscal year end for annual reports, and 45 days after quarter end for quarterly reports.

B. Accelerated Filer Status; Sarbanes-Oxley Act

Following a series of corporate and accounting scandals in the early 2000s that led to financial restatements and bankruptcies and resulted in significant adverse effects on shareholders, the Commission established “accelerated filer” status by adopting accelerated filing deadlines for certain registrants. Congress subsequently enacted the Sarbanes-Oxley Act,[44]

which included ICFR requirements intended to improve the accuracy and reliability of corporate disclosures.

The Commission's adoption of AF status was motivated in part by advances in communication technology and companies' growing practice of releasing quarterly earnings well before the Form 10-Q deadline.[45]

The new “accelerated filer” status therefore accelerated the periodic report filing deadlines for registrants with a public float of $75 million or more, who had been subject to Exchange Act reporting requirements for at least 12 months, and had previously filed at least one annual report.[46]

In acting to further categorize the filer statuses in this way, the Commission sought to “balance the market's need for information with the time companies need to prepare that information without undue burden.” [47]

The Commission again amended the filer status rules in 2005 by introducing the LAF status.[48]

The Commission sought to avoid applying the shortest filing deadlines to registrants with less than $700 million in public float by further dividing filers into LAFs

( printed page 30093)

(registrants with $700 million or more in public float) and AFs (registrants with at least $75 million in public float but less than $700 million). All remaining registrants with less than $75 million in public float have become known as NAFs. While the Commission acknowledged the incremental benefit of more timely accessibility to periodic reports, it was concerned with the added burdens associated with the increased acceleration of the deadlines.[49]

The Commission determined to limit the shortest deadlines to the largest registrants, reasoning that LAFs, “are more likely than smaller companies to have a well-developed infrastructure and financial reporting resources to support further acceleration of the annual report deadline.” [50]

As a result of this and later developments,[51]

under the current definition in Rule 12b-2, an LAF is a registrant that: (1) has a public float of $700 million or more, as of the last business day of its most recently completed second fiscal quarter, calculated using either the closing price or the average of the bid and ask prices that day; (2) has been subject to the requirements of Exchange Act section 13(a) or 15(d) for at least 12 calendar months; (3) has filed at least one annual report pursuant to the Exchange Act; and (4) is not eligible to be an SRC under the SRC revenue test. LAFs' periodic reporting deadlines are 60 days for Form 10-K, and 40 days for Form 10-Q, while AFs' deadlines are 75 and 40 days, respectively; and the deadlines for NAFs remain at 90 and 45 days, respectively.[52]

C. ICFR Requirements

In 2002, less than two months before the Commission adopted the rules for AFs, Congress enacted the Sarbanes-Oxley Act.[53]

One aspect of the Sarbanes-Oxley Act's reforms was the adoption of section 404. Section 404(a) mandates Commission rules requiring Exchange Act reporting companies to include in their annual reports an internal control report that states the responsibility of management for establishing and maintaining ICFR and that contains an assessment of the effectiveness of the registrant's ICFR as of the end of each fiscal year.[54]

Section 404(b) requires that each registered public accounting firm that prepares or issues the registrant's financial statement audit report attest to, and report on, management's assessment of the effectiveness of the ICFR.[55]

As discussed below, Congress took further action in the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (“Dodd-Frank Act”) [56]

and the Jumpstart Our Business Startups (“JOBS”) Act,[57]

to exempt from section 404(b): (1) any registrant that is not an LAF or an AF and (2) any registrant that is an EGC, respectively.

As mandated by section 404, the Commission adopted rules in 2003 requiring registrants that are subject to Exchange Act reporting requirements to include in their annual reports a report of management on the registrant's ICFR and an attestation report by the registrant's auditors on management's assessment of the internal controls.[58]

Although section 404 generally requires and directs the Commission to adopt rules regarding ICFR that apply to every issuer that is required to file reports pursuant to Exchange Act section 13(a) or 15(d), registered investment companies (“RICs”) under section 8 of the Investment Company Act [59]

are specifically exempted from section 404 by section 405.[60]

In addition, the Commission's rules implementing section 404 exempted other types of issuers, such as asset-backed issuers, from the ICFR obligations.[61]

The Commission also determined that FPIs and Canadian multijurisdictional disclosure system (“MJDS”) issuers must have their management assess and report annually on the effectiveness of their ICFR as of the end of their fiscal year and include an auditor attestation report on ICFR in their annual report form if the FPI or MJDS issuer is an AF or LAF, other than an EGC.[62]

BDCs, however, are subject to the rules adopted by the Commission to implement section 404.[63]

Through a series of actions from 2003 through 2009, the Commission delayed compliance with section 404 for NAFs, acknowledging that “non-accelerated filers, including smaller companies and foreign private issuers, may have greater difficulty in preparing the management report on internal control over financial reporting.” [64]

Ultimately, Congress

( printed page 30094)

enacted section 989G of the Dodd-Frank Act, which added section 404(c) to the Sarbanes-Oxley Act to exempt issuers that are neither LAFs nor AFs, as defined by the Commission, from the ICFR auditor attestation requirement of section 404(b).[65]

Section 404(c) also directed the Commission to conduct a study to determine how the Commission could reduce the burden of complying with the section 404(b) ICFR auditor attestation requirement for companies with public float between $75 million and $250 million. Congress further extended relief from section 404(b) in the JOBS Act when it exempted EGCs from the requirement.[66]

In April 2011, the Commission staff published the required study and recommendations relating to section 404(b).[67]

The study found that, while initial implementation of section 404 resulted in a steep increase in audit fees, there was a statistically significant decrease in compliance costs (including audit fees) for registrants subsequent to the issuance of PCAOB Auditing Standard No. 5 [68]

and related Commission guidance [69]

on management's report on ICFR. Based on the study's findings, the staff did not recommend changing the scope of the ICFR auditor attestation requirement at that time, but encouraged activities to further improve the effectiveness and efficiency of implementation of the ICFR requirements.[70]

As discussed in more detail below, the Commission modified the definition of AF in 2020 to exclude a registrant that is eligible to be an SRC and has annual revenues of less than $100 million.[71]

In excluding low-revenue SRCs from AF status, the Commission also exempted those registrants from the ICFR auditor attestation requirement. In the adopting release, the Commission found that the ICFR auditor attestation requirement is disproportionately costly to small issuers, noting that the fixed costs of compliance are not scalable for smaller issuers and that low-revenue issuers have limited access to internally generated capital such that the costs may more directly constrain their ability to invest and hire.[72]

Commentators and registrants continue to express concerns regarding the costs of implementation of section 404 and the disproportionate effect on smaller issuers.[73]

D. Actions Related to Smaller Reporting and Emerging Growth Companies

1. Establishment of SRC Status

Through the course of implementing the enhanced disclosure and other requirements of the Sarbanes-Oxley Act, the Commission recognized the increased regulatory burden faced by registrants.[74]

This eventually led in 2007 to the Commission reworking its regulatory framework for smaller registrants by establishing the “smaller reporting company” filer status.[75]

As part of the revisions, the Commission rescinded Regulation S-B and the “small business issuer” definition.[76]

Under the 2007 rules, all filers that were not AFs or LAFs—

i.e.,

those with less than $75 million in public float [77]

—were designated as SRCs, and granted most of the scaled disclosure accommodations that had previously been provided to “small business issuers.” [78]

The SRC definition excludes asset-backed issuers, RICs, BDCs, and majority-owned subsidiaries of issuers that do not qualify as an SRC. Additionally, FPIs are not eligible to use the requirements for SRCs unless they use the forms and rules designated for domestic issuers and provide financial statements prepared in accordance with U.S. Generally Accepted Accounting Principles (“U.S. GAAP”).[79]

The revised streamlined regulatory framework moved all disclosure requirements back into Regulation S-K and Regulation S-X, consolidated smaller issuers and NAFs into the same filer status, and expanded the number of registrants eligible to use scaled disclosure requirements.[80]

The

( printed page 30095)

amendments effectively established a three-tier filer status framework:

LAFs having a public float of $700 million or more, subject to the most accelerated filing deadlines and the most comprehensive disclosure requirements;

AFs having a public float of $75 million or more, but less than $700 million, subject to less accelerated filing deadlines and the most comprehensive disclosure requirements; and

SRCs having a public float of less than $75 million (or, if without a calculable public float, annual revenues below $50 million), subject to non-accelerated filing deadlines and scaled disclosure requirements.

At the time of initial adoption of SRC status, LAFs and AFs were generally subject to the same disclosure requirements as each other. SRCs, however, were (and currently remain) permitted to avail themselves of certain scaled disclosure accommodations, which currently include:

To provide two (instead of three) years of audited financial statements, and prepare their financial statements in accordance with Article 8 of Regulation S-X; [81]

To provide two (instead of three) years of summary compensation table information and tabular and other compensation disclosure for three (instead of five) named executive officers;

To omit the compensation discussion and analysis, compensation policies and practices related to risk management, pay ratio disclosure, grants of plan-based awards table, pension benefits table, option exercises and stock vested table, and nonqualified deferred compensation table; [82]

To provide scaled golden parachute and pay versus performance disclosure; [83]

To omit disclosure relating to risk factors in periodic reports; [84]

a stock performance graph; [85]

quantitative and qualitative disclosure about market risk; [86]

supplementary financial information relating to the disclosure of material quarterly changes and information about oil and gas activities; [87]

policies and procedures for the review, approval, or ratification of related party transactions; [88]

and certain payments made by resource extraction issuers; [89]

and

To provide a simplified description of business.[90]

By contrast, Item 404 of Regulation S-K, which addresses related-party transaction disclosure, includes in Item 404(d) certain requirements for SRCs that are more rigorous than those for other filers,[91]

namely:

Rather than a flat $120,000 threshold for the disclosure of related-party transactions, the threshold is the lesser of $120,000 or one percent of total assets;

Disclosures are required about underwriting discounts and commissions where a related person is a principal underwriter or a controlling person or member of a firm that was or is going to be a principal underwriter;

Disclosures are required about the issuer's parent(s) and their basis of control; and

An additional year of disclosures is required regarding transactions with related persons.[92]

2. The JOBS Act and EGC Status

In 2012, Congress enacted the JOBS Act, which established a new “emerging growth company,” or EGC, filer status and provided disclosure and other accommodations to EGCs.[93]

Currently, a company qualifies as an EGC if it has total gross revenues of less than $1.235 billion during its most recently completed fiscal year and continues to qualify as an EGC until the earliest of: (1) the last day of the fiscal year of the issuer during which it has total annual gross revenues of $1.235 billion or more; (2) the last day of its fiscal year following the fifth anniversary of the first sale of its common equity securities pursuant to an effective registration statement; (3) the date on which the issuer has, during the previous three-year period, issued more than $1 billion in nonconvertible debt; or (4) the date on which the issuer is deemed to be an LAF (as defined in Exchange Act Rule 12b-2).[94]

Congress supplemented the JOBS Act by enacting the Fixing America's Surface Transportation (“FAST”) Act,[95]

which provided for targeted additional accommodations for EGCs and required the Commission “to further scale or eliminate requirements of Regulation S-K, in order to reduce the burden on emerging growth companies, accelerated filers, smaller reporting companies, and other smaller issuers, while still providing all material information to investors.” [96]

EGC status provides a registrant with accommodations that lower the costs and burdens of registration and reporting and is generally seen as an “on-ramp” for newly public companies to ease the burdens of transitioning from a private to a public company.[97]

While there are overlaps between the EGC and SRC populations and their respective accommodations, EGCs are entitled to a similar but distinct set of accommodations. EGCs are:

( printed page 30096)

Exempt from the ICFR auditor attestation requirement,[98]

the requirement to hold shareholder advisory votes on executive compensation,[99]

pay ratio disclosure,[100]

and pay versus performance disclosure; [101]

Permitted to provide two (instead of three) years of audited financial statements in the registration statement for an initial public offering of common equity securities, and to defer compliance with new or revised financial accounting standards until a company that is not an issuer is required to comply with such standards, if such standard applies to private companies; [102]

Permitted to provide executive compensation disclosure to match the information required from issuers with less than $75 million in public float (the SRC threshold at the time of adoption of the JOBS Act); [103]

and

Permitted to submit certain draft registration statements to the Commission on a confidential basis.[104]

3. Recent Amendments and Filer Status Complexity

While a registrant cannot be both an EGC and an LAF,[105]

as shown in the table in section I above, a registrant can be both an EGC and an SRC, or both an EGC and an AF. When the Commission updated the SRC, AF, and LAF thresholds in 2018, the SRC public float threshold was raised to $250 million, and the SRC revenue threshold was raised to $100 million.[106]

Along with the increase of these thresholds, the Commission removed the automatic exclusion of SRCs from the definition of AF and LAF. As a result of these changes, SRCs went from being exclusively NAFs to a separate, additional status (like EGC status) that could attach to either NAFs or AFs. Further, SRCs can also be EGCs, and these statuses involve largely overlapping but distinct obligations and accommodations.

When adopting the 2018 amendments to the SRC definition, the Commission acknowledged the “regulatory complexity” created by this potential overlap between the SRC and AF definitions.[107]

Subsequently, in 2020, the Commission adopted amendments to the definitions of AF and LAF seeking to tailor the types of issuers included in those filer statuses.[108]

The rules, as amended, now exclude low-revenue SRCs (those with under $100 million in annual revenues and either no public float or a public float of less than $700 million) from the definitions of AF and LAF, increasing the number of registrants that qualify as NAFs.[109]

As NAFs, these registrants, among other things, are not required to obtain an ICFR auditor attestation. The amendments were intended to thereby reduce compliance costs for these registrants while maintaining investor protections by more appropriately tailoring the types of registrants that are included in the categories of AF and LAF.[110]

While the amendments increased the number of SRCs that qualify as NAFs, the Commission determined not to fully align the statuses.[111]

The Commission acknowledged that such alignment would promote greater regulatory simplicity and reduce friction or confusion associated with registrants' determination of their filer status or reporting regime.[112]

It expressed concerns, however, that such alignment could result in adverse effects on the reliability of the financial statements and the ability of investors to make informed investment decisions about those issuers.[113]

Thus, the amendments reduced the overlap between AF status and SRC status by including low-revenue SRCs as NAFs (

i.e.,

those with a public float of $75 million or more but less than $250 million, regardless of annual revenues, and those with public float of less than $700 million and annual revenues of less than $100 million), but added an additional determination for SRC status.

We are proposing to revise the current rules to streamline and further scale disclosure and reporting requirements. Among our objectives is to reduce compliance costs and create a more attractive on-ramp for newly public companies, thereby reducing regulatory impediments that may be deterring companies from participating in the public market and encouraging more companies to go and stay public, while ensuring that investors have the information necessary to inform their investment and voting decisions.

II. Discussion of Proposed Rules

As detailed above, the Commission's rules currently set forth five filer statuses that correspond to varying levels of disclosure and other requirements, which are sometimes overlapping and often complex for issuers to determine.[114]

LAFs are subject to the most stringent requirements, and NAFs that are also both SRCs and EGCs are afforded the most accommodations. LAFs in 2024 accounted for 35.4 percent of registrants and 98.8 percent of total market public float.[115]

In contrast, in 2024, while NAFs, including NAFs that are also SRCs or EGCs (or both), accounted for 51.9 percent of registrants, they accounted for only 1.2 percent of total market public float.[116]

We are proposing amendments with the goal of streamlining the overlapping Exchange Act filer statuses and further

( printed page 30097)

scaling disclosures and other accommodations while ensuring that investors continue to receive timely and material information. To do so, the proposed amendments seek to align disclosure and other reporting requirements and reporting deadlines with registrants' public float. As a result of the proposed amendments, companies that collectively make up the majority of the U.S. equity market capitalization would be subject to the most comprehensive requirements and earliest filing deadlines, while all other issuers would be afforded the proposed scaled disclosure and other accommodations. The proposed amendments would provide for simplified compliance and reduced costs for a majority of registrants. Additionally, we are proposing to extend the filing deadlines for the smallest companies in order to reduce the burden on these companies and further accommodate their ability to efficiently comply with Exchange Act reporting. As described in more detail below, the proposed amendments would:

Revise the LAF filer status to:

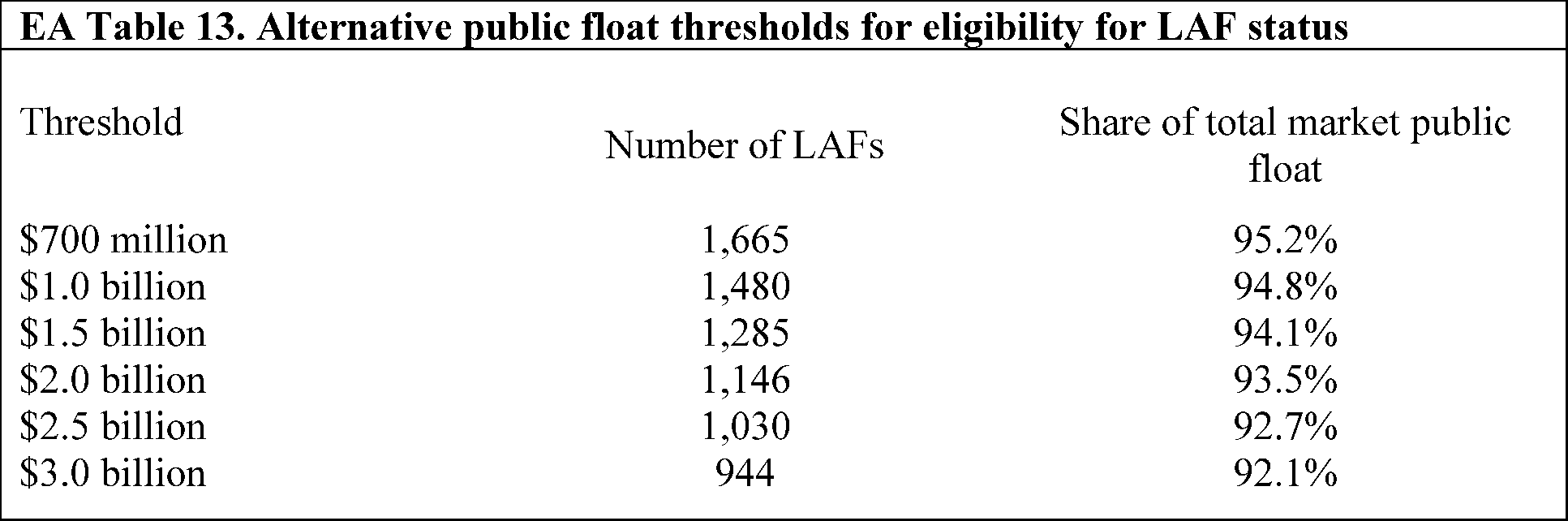

○ Raise the threshold for becoming an LAF from the current $700 million to $2 billion in public float, which would represent 93.5 percent of the current total market public float; [117]

○ Establish a new, more stable, public float calculation window that provides for the determination of public float based on the average price of the registrant's voting and non-voting common equity held by non-affiliates over the last 10 trading days of the second quarter of a registrant's fiscal year; [118]

○ Establish that a registrant will only transition into or out of a status after the registrant has been above or below the public float threshold for two consecutive years; [119]

and

○ Increase the seasoning threshold for becoming an LAF to 60 consecutive calendar months.[120]

Establish the NAF filer status and consolidate and extend to NAFs currently available scaled disclosure and other accommodations by:

○ Establishing an NAF definition that encompasses all registrants that are not LAFs; [121]

and

○ Applying to NAFs the current disclosure requirements applicable to SRCs and EGCs, including not requiring an ICFR auditor attestation.[122]

Extend to NAFs the requirement currently applicable to LAFs and AFs to disclose on Form 10-K or Form 20-F the substance of material unresolved staff comments regarding the registrant's periodic or current reports received at least 180 days before a registrant's fiscal year end.[123]

Eliminate AF and SRC filer statuses as unnecessary in light of the amendments described above.[124]

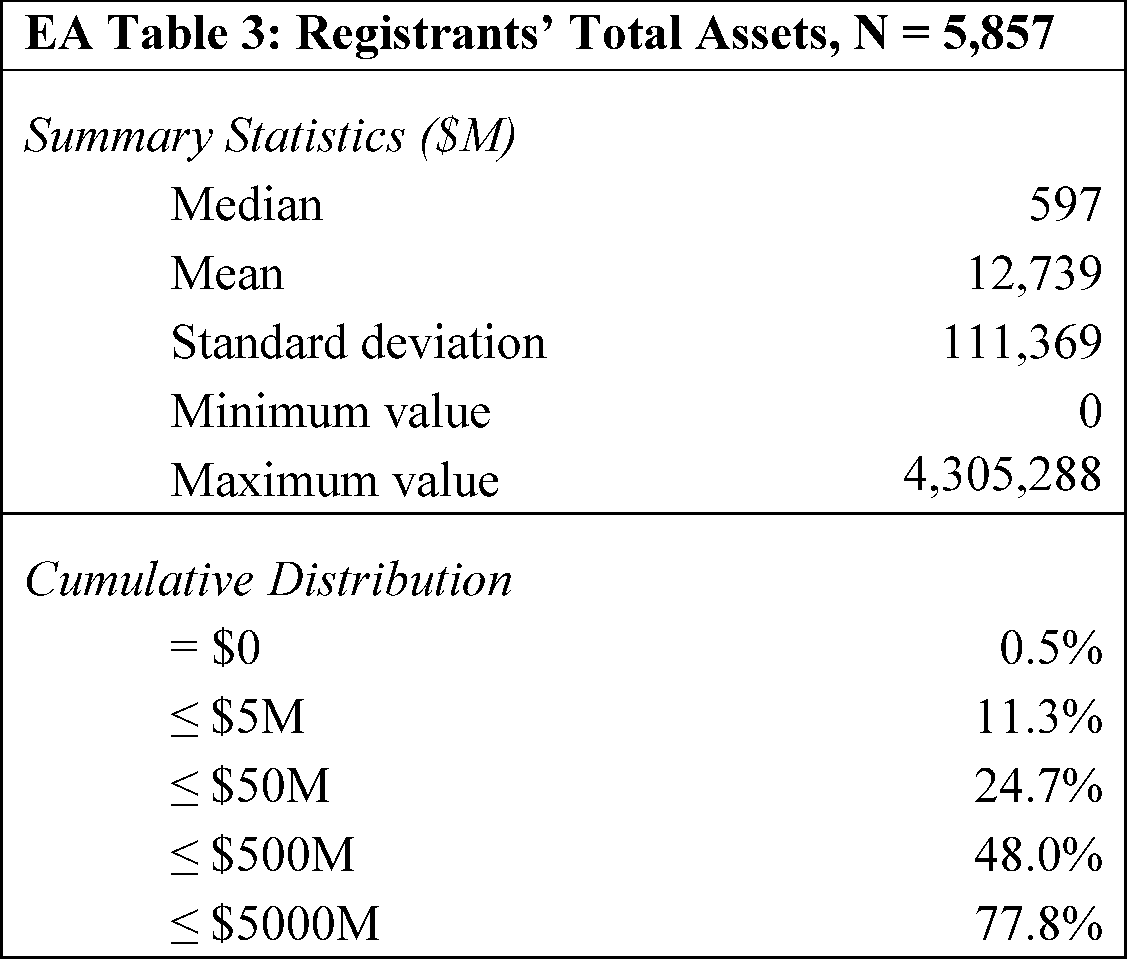

Create a sub-category consisting of the smallest NAFs (“SNFs”), comprising NAFs reporting total assets of $35 million or less as of the end of an issuer's two most recent second fiscal quarters, that would be eligible for extended deadlines for filing their Form 10-K and Form 10-Q periodic reports.[125]

Consistent with the Commission's history of considering how its regulatory regime can serve investors while avoiding unnecessary regulatory burdens to registrants, we believe the time is ripe to again rebalance the disclosure and other requirements applicable to issuers of given sizes. Evidence shows that regulatory changes over the last two decades, which increased the costs of public company reporting, have contributed to a decline in the number of public companies in the United States.[126]

We believe the proposed amendments are a meaningful step in making the public markets more attractive, which would encourage more companies to go and stay public while ensuring that investors remain equipped to make informed investment and voting decisions, which would in turn improve investment opportunities and the information available to investors in such companies.

In this regard, the proposed scaling and accommodations would in many cases apply to disclosures, such as in the area of executive compensation and corporate governance matters, where the associated potential benefits may not be commensurate with their costs to registrants. Further, we believe any loss of information and assurance or increased costs to investors in registrants that would newly receive certain accommodations would be justified by the expected reduction in costs to those registrants, as well as by effects that may encourage more companies to go and stay public, which ultimately would benefit investors in those companies.[127]

Finally, to the extent that these accommodations contribute to a company choosing to go or stay public, we also believe that is ultimately a benefit to investors, including through the resulting greater diversification and more efficient capital allocation within investor portfolios.[128]

A. Large Accelerated Filer Status Amendments

We are proposing to revise the definition of LAF to mean an issuer that as of the end of each of the issuer's two most recent second fiscal quarters, had an aggregate worldwide market value of the voting and non-voting common equity held by non-affiliates of $2 billion or more. In addition, we are proposing to extend the seasoning requirement for LAF status such that an issuer would be an NAF until it has been subject to the requirements of section 13(a) or 15(d) of the Exchange Act for a period of at least the preceding 60 consecutive calendar months.[129]

Consistent with our current rules, an issuer would be required to assess its filer status annually, as of the last day of its fiscal year.[130]

These proposed amendments would apply the LAF requirements to only the largest registrants, which comprise the vast majority of the equity market capitalization in the U.S. public

( printed page 30098)

markets, with those companies currently representing approximately 93.5 percent of total market public float.[131]

We believe that registrants with the largest U.S. equity market capitalization have a heightened investor demand for more comprehensive information sooner, and these registrants are likewise the most capable of bearing the costs and burdens of compliance with shorter disclosure deadlines and non-scaled disclosure and other requirements. We estimate these proposed conditions would result in 19.2 percent of existing Exchange Act reporting companies being LAFs, as compared to 35.4 percent today.[132]

1. Public Float Threshold

We are proposing to raise the public float threshold for purposes of determination of LAF status from $700 million to $2 billion. The Commission has historically looked to public float as a proxy for demonstrated market following [133]

and used public float in determining filer status and appropriate disclosure requirements and accommodations. When the Commission created the LAF filer status in 2005, it emphasized that “companies with a public float of $700 million or more represent nearly 95 percent of the U.S. equity market capitalization and are more closely followed by the markets and by securities analysts than other issuers,” and that “larger issuers generally have sufficient financial reporting resources and sufficiently robust infrastructures to comply with the [accelerated filing deadlines].” [134]

We continue to believe that public float is a reasonable indicator of which companies the markets follow most closely.[135]

We further believe that it is most appropriate to subject registrants with the higher public float to non-scaled disclosure requirements. In addition, we believe that companies with a public float of $2 billion or more should be sufficiently resourced to be able to comply with the highest level of burden associated with registration and the obligations of being a public company.

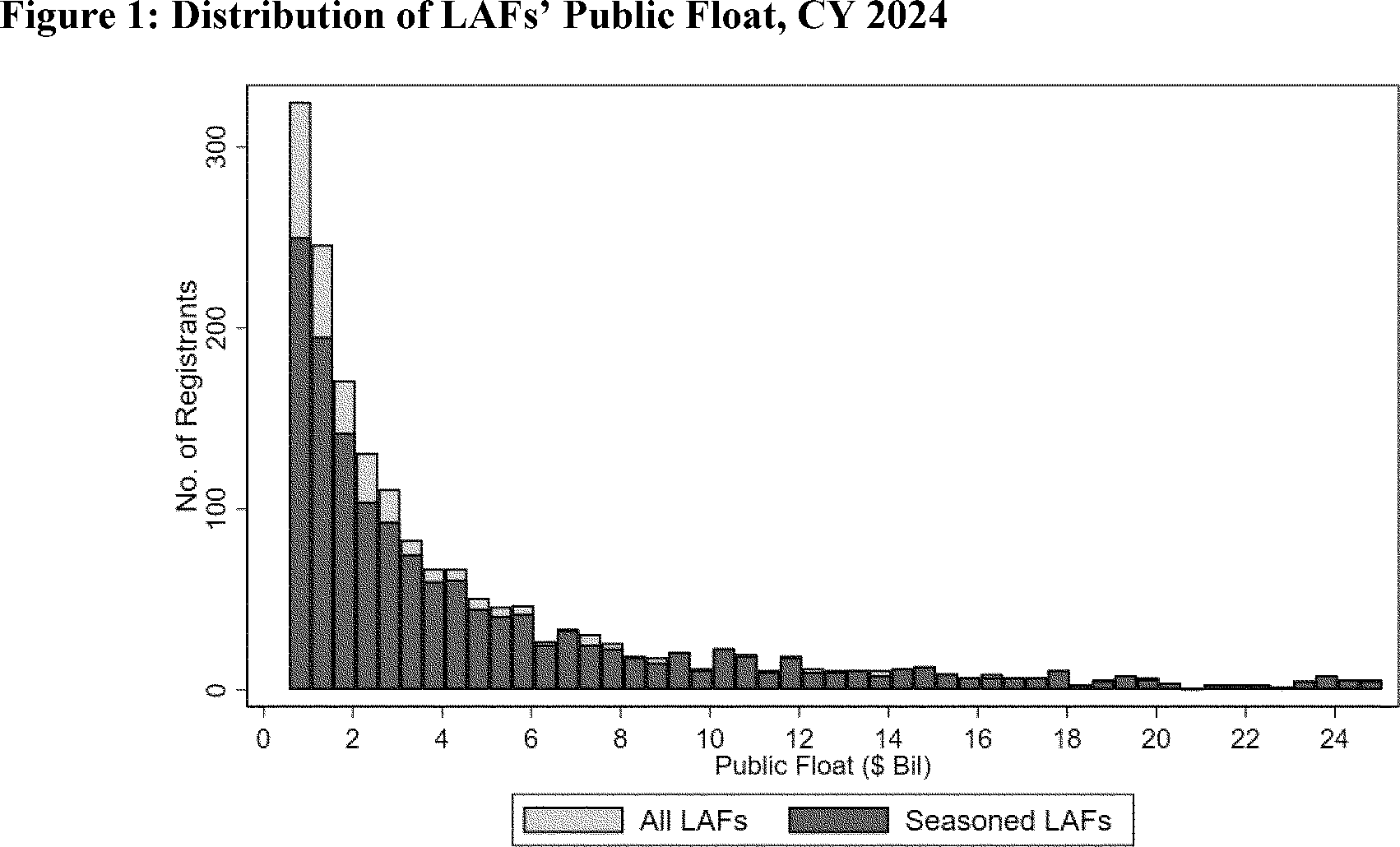

At the time the Commission adopted LAF filer status in 2005, it was estimated that “companies with a public float of over $700 million represent approximately 18 percent of the total number of companies on these markets and nearly 95 percent of the total public float on these markets.” [136]

We note that since the adoption of the LAF filer status, the $700 million threshold has not been updated. Today, we estimate that the current threshold captures 98.8 percent of total market public float and 35.4 percent of registrants.[137]

We are proposing to raise the threshold to continue to cover the largest registrants and reestablish the relationship to the number of companies covered and total market public float that existed when the filer status was adopted.[138]

We therefore propose to reestablish a public float requirement that would capture nearly 95 percent of total market public float and estimate that setting the threshold at $2 billion would capture approximately 93.5 percent of total market public float, and cover approximately 20 percent of the total number of existing registrants.

Other than the proposed single public float threshold, we are not proposing additional or alternative LAF status determination thresholds, as we believe doing so could complicate the regulatory framework without commensurate benefits.

2. Public Float Determination

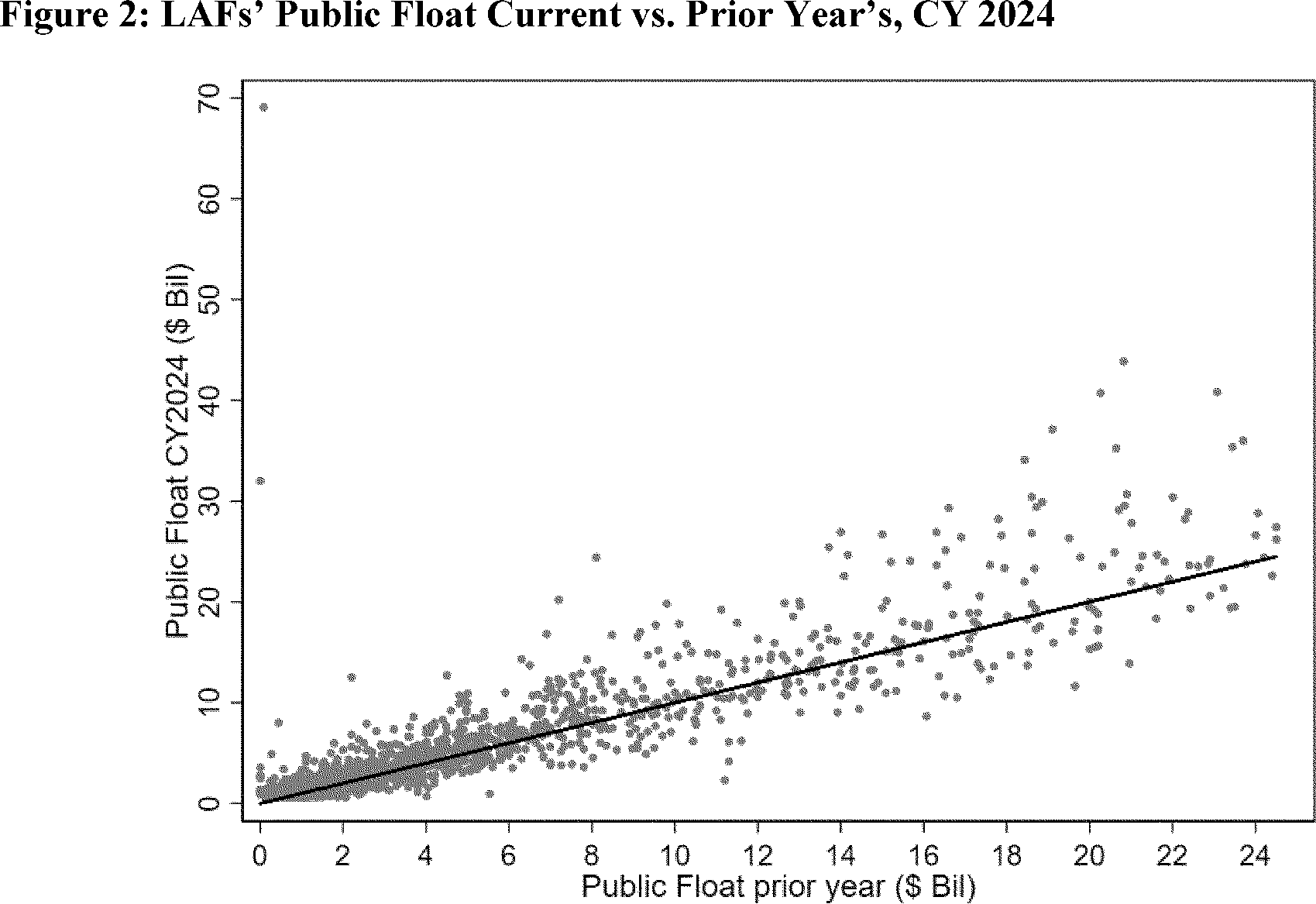

We are proposing amendments to the way a registrant determines its public float for purposes of the LAF definition. Under the current rules, a registrant assesses whether it meets LAF status as of the end of each fiscal year based on its public float as of the last business day of an issuer's most recently completed second fiscal quarter, using either the closing price or the average of the bid and ask prices on that day. As a result, a registrant may become an LAF at the end of its fiscal year based on a single day of volatility, even if the registrant's overall public float may quickly stabilize below the threshold. While we recognize that the circumstances in which such swings can cause a shift in filer status may be limited or relatively rare, to the extent they do occur, the consequences can be significant in terms of regulatory burden on affected registrants. To minimize the impact of swings in share price in a limited period or on a single day, the proposed amendments would require that, before a registrant would transition either into or out of LAF status as of the end of its fiscal year, the registrant's public float, calculated based on the average of the registrant's stock price over the last 10 trading days of each of the second quarter of such fiscal year and the immediately prior fiscal year, multiplied respectively by the aggregate worldwide number of shares of the issuer's voting and non-voting common equity held by non-affiliates as of the last day of the issuer's second fiscal quarter of such fiscal year, remain either at or above, or below, the public float threshold.

By requiring that the public float threshold be met (or not met) for two consecutive years, a registrant would change filer status as of the end of its fiscal year only if its public float has been relatively stable consistently either above or below the threshold. This would mean that a registrant, and investors, would always have at least one year of visibility regarding the

( printed page 30099)

possibility of a status transition before any transition could occur. The proposed rules also clarify that meeting or not meeting the conditions of LAF status for a single year would not suffice to change filer status from NAF to LAF or vice versa. Thus, once a registrant enters a status, it would remain in that status for at least two years.

The proposed rules also base the calculation each year on the average of the closing prices over the last 10 trading days of the second quarter of the registrant's fiscal year (or, if there is no closing price on a day, the average of the bid and ask prices that day), using the number of shares on the last day of the second quarter of the registrant's fiscal year, in order to address the risk that a single day's market volatility could result in unexpected changes to filer status. An average over 10 trading days would provide at least two calendar weeks of data, which we believe would mitigate the impact of short-term volatility, including spikes and drops in stock price that may be temporary, such as those based on short-term news and events. We are proposing that the number of shares be based on a single date in an effort to simplify the calculation.

Additionally, we believe the proposed transition criteria, by accounting for the potential for volatility, would eliminate the need for distinct criteria for transitioning out of a particular filer status as provided for in the current rules. As the Commission stated when adopting separate transition thresholds for exiting AF or LAF status, the purpose of the transition thresholds “is to avoid situations in which an issuer frequently enters and exits accelerated and large accelerated filer status due to small fluctuations in public float” which could cause confusion for issuers and investors as to the issuer's status.[139]

While we agree that addressing volatility in setting a market price-based threshold should remain an important consideration, the Commission's existing separate thresholds for exiting a filer status have contributed to the complexity of the current rules. Accordingly, we are also proposing to eliminate the separate, lower threshold for exiting LAF status in favor of a definition with a single public float criterion and a two-year lookback determination (

i.e.,

public float of $2 billion or more for two consecutive fiscal years). While the lower exit threshold was intended to maintain stability in status so that registrants with public floats near the entry threshold do not frequently move in and out of a filer status, we believe requiring the threshold be met in two consecutive years based in each year on a longer calculation window would more meaningfully address these concerns while being easier for registrants to implement and providing earlier notice of a possible change in filer status.

A potential drawback of the two-year lookback is that some registrants that would become LAFs would have to provide non-scaled disclosure even if their public float falls below the LAF threshold for a year. Conversely, a potential drawback for investors is that they would not receive the benefits of non-scaled disclosure following an NAF's single-year increase in public float, as they would with a one-year lookback. However, a registrant remaining “in status” for at least two years before potentially changing to a new filer status could provide more consistency to the disclosure regime and more comparable period-to-period information, to the benefit of both registrants and investors.

To demonstrate how these proposed changes would work in practice, consider a hypothetical NAF that is assessing its annual filer status as of the last day of its fiscal year, or December 31, 2026, for a calendar-year end registrant. Assuming the proposed rules were in effect, if an NAF's public float, as determined by the average stock price over the last 10 trading days of the second quarter of each fiscal year being measured (

i.e.,

the 10 trading days ending on or before June 30), for fiscal year 2025 was $1.9 billion and for fiscal year 2026 is $2.3 billion, the registrant would remain an NAF for purposes of its December 31, 2026 Form 10-K (filed in 2027) because it crossed the LAF threshold in only one year of the two-year lookback period. That is, when performing the test as of the last day of its fiscal year, the registrant looks back to the last 10 trading days of the second quarter of the fiscal year for each of fiscal year 2026 and 2025, and in the example, it only exceeded the threshold in fiscal 2026. If the registrant then determines that its public float as of the measurement period of the second quarter for fiscal year 2027 is $1.9 billion (dropping back below the LAF threshold), the registrant would remain an NAF as of the end of fiscal 2027. The earliest it could become an LAF would be at the end of its fiscal year 2029 (assuming its public float crosses the LAF threshold for the relevant measurement period of the second quarter for both fiscal years 2028 and 2029), and if so it would be required to comply with the requirements of LAF status beginning with its Form 10-K for fiscal year 2029 filed in 2030.

On the other hand, if that registrant determines its public float for fiscal year 2027 is $2.5 billion (while the fiscal year 2026 public float remains at $2.3 billion as in the example above), it would become an LAF as of the last day of its fiscal year 2027, and would be required to comply with the requirements of LAF status beginning with its Form 10-K for fiscal year 2027 (filed in 2028). If the registrant's public float falls to $1.9 billion as of the relevant measurement period in the second quarter of fiscal year 2028, the registrant would remain an LAF for purposes of its Form 10-K for fiscal year 2028 because its public float will have been below the LAF threshold for only one fiscal year. The earliest it could become an NAF would be as of the end of its fiscal year 2029 (assuming its public float is below the LAF threshold in the relevant measurement period in the second quarters of both fiscal years 2028 and 2029), and if so would be able to transition to NAF status beginning with its Form 10-K for fiscal year 2029, filed in 2030.

As proposed, once a registrant qualifies for a change in filer status, the requirements and any applicable accommodations of the new filer status would apply beginning with the filing of its annual report on Form 10-K for the fiscal year in which the filer status was determined. As a result, the possibility of both entering LAF status and transitioning to NAF status are foreseeable further in advance than is the case currently, allowing companies to more predictably plan their disclosure controls and procedures and associated costs. Similarly, the first time an LAF's public float falls below the LAF threshold (or an NAF's public float rises above the threshold) as of one of its second fiscal quarter ends, investors would know that, even if that trend were to continue, the registrant would be required to file at least one more Form 10-K subject to the LAF disclosure requirements and deadlines (or subject to the NAF disclosure requirements and deadlines, as the case may be).

3. Seasoning

We are proposing to expand the seasoning period for LAFs—

i.e.,

the requisite period after which registrants could potentially qualify as LAFs—to 60 consecutive calendar months from when the registrant became subject to the Exchange Act reporting requirements,

( printed page 30100)

with the assessment made as of the last day of its fiscal year.[140]

Under current rules, a registrant must be an Exchange Act reporting company for at least 12 calendar months before it can be classified as an LAF.[141]

In adopting the current 12-calendar month seasoning period, the Commission noted that, along with the public float requirement, the seasoning period was “designed to include the companies that are least likely to find [accelerated deadlines] overly burdensome and where investor interest in accelerated filing is likely to be highest.” [142]

When the Commission adopted the 12-calendar month seasoning period, it was focused on existing registrants that would become subject to accelerated filing deadlines and recognized that there would be an increased burden for these issuers. Since the adoption of the acceleration of periodic reporting in 2002, Congress and the Commission have expanded the disclosure requirements for registrants, especially for LAFs. Given the additional requirements that apply to LAFs, we believe that a longer seasoning period would be appropriate before a registrant should be required to comply with non-scaled ongoing disclosure and timing requirements.

This change would effectively create a minimum five-year on-ramp for every new registrant, regardless of public float. While we recognize that this five-year on-ramp would, for a small subset of registrants,[143]

delay compliance with respect to non-scaled disclosure requirements, accelerated reporting deadlines, and ICFR auditor attestation as compared to the current rules, we believe allowing all newer registrants ample time to adjust to the disclosure and filing requirements of a public company may encourage more companies to go public and stay public, which may ultimately improve overall market transparency and provide investors with more investment opportunities with the greater transparency afforded by Exchange Act reporting. In addition, even if a particular requirement does not apply to a registrant, that registrant may elect to voluntarily comply, such as by obtaining an ICFR auditor attestation, if the registrant believes it would benefit the registrant to do so, such as if doing so were viewed favorably by investors.

When Congress enacted the JOBS Act, in order to encourage more companies to go and stay public, it created an on-ramp of up to five years in EGC status, reducing registrants' compliance burdens in their early years as public companies. In our experience, this on-ramp has been a meaningful accommodation to newer public companies and generally has not resulted in investor protection concerns.[144]

A similar on-ramp before a registrant would potentially enter LAF status would be consistent with and effectively expand the benefits of EGC status, and would provide all newer registrants ample time to, among other things, prepare for the increased costs and reporting burdens on company staff and enlist third party advisors or service providers needed to satisfy the non-scaled disclosure requirements and accelerated reporting timelines. Finally, providing a sixty calendar month on-ramp complements Congress' intent with its establishment of EGC status and would help to simplify filer status determinations by ensuring that all registrants that meet the statutory definition of EGCs will necessarily qualify as NAFs when making their filer status determinations.[145]

Request for Comment

(1) Does public float continue to be a reasonable indicator of which companies the markets follow most closely? Does public float continue to be a good indicator of the most significant need for more extensive public disclosure? Why or why not? As an alternative, in view of the increasing prevalence of dual class share structures, should non-publicly traded common equity securities held by non-affiliates through dual class share or other multi-class share structures be included in determining whether the threshold is met? If so, how should registrants determine the value of those securities for purposes of the determination?

(2) Does public float provide a reasonable indicator of a registrant's ability to sustain the burdens associated with LAF status under the proposed rules, including non-scaled disclosure requirements, accelerated reporting timelines, and compliance with the ICFR auditor attestation requirement in section 404(b)? If not, are alternative thresholds or other measures more appropriate to evaluate a registrant's ability to sustain the burdens of being an LAF?

(3) Is the proposed LAF threshold of $2 billion in public float, which would capture approximately 93.5 percent of the total market public float and would result in approximately 20 percent of existing public companies being classified as LAFs, appropriate? If not, what other threshold should the Commission consider and why? For example, should the Commission update the threshold to $3.85 billion to mirror the increase in the S&P 500 Index? Do the proposed changes to the LAF status public float threshold and calculation methodology appropriately balance the goals of capital formation and investor protection? Should the Commission instead adopt a different threshold, and if so, what? Would the proposed approach result in any impacts to investors and the public market, including benefits or burdens that might result from the proposed scaling of disclosure associated with the revisions to the filer status categories? Would the proposed approach impact investors' ability to make informed investment and voting decisions?

(4) We have proposed to adjust the public float threshold not based on inflation, but rather to cover the registrants that comprise the vast majority of the total market public float and that are most able to comply with the highest level of burden associated with registration. Should the Commission instead update the current threshold for inflation? Alternatively, should the Commission establish a mechanism to update the proposed $2 billion public float threshold for inflation? For example, the JOBS Act requires that the revenue threshold in definition of EGC be indexed to inflation at five-year intervals. Should the proposed public float threshold be similarly indexed to inflation? Are there alternative methodologies for updating the threshold that would be preferable?

( printed page 30101)

(5) Would the proposed average public float calculation period (consisting of the registrant's stock price over the last 10 trading days of the second quarter of each relevant fiscal year) and the proposed use of the number of shares held by non-affiliates as of the last day of the second fiscal quarter achieve the intended goal of avoiding a result where a company's public float determination is anomalous due to short-term volatility? Why or why not? Should it be more or fewer than 10 trading days? Should the number of shares be based on the average number of shares during the same 10 trading day period instead of at the last day of the second fiscal quarter or should the number of shares be based on the number of shares as of a date selected by the registrant within a given period (such as any date within the last 10 trading days of the second fiscal quarter)? Why or why not? Are there costs or benefits associated with extending the public float calculation methodology to 10 trading days?

(6) We considered multiple calculation windows for the public float calculation, including: retaining the existing calculation date of the last trading day of the second fiscal quarter; allowing a registrant to choose a date within a given period (such as any date within the last 10 trading days of the second fiscal quarter); or reducing the number of days comprising the average to, for example, the last five trading days of the second fiscal quarter. Are any of these or other alternatives preferable to the proposed 10-day average methodology, and if so, why?

(7) Is the proposed LAF threshold effective for all types of issuers, or should the threshold differ for certain types of issuers? For example, should LAF status for investment companies (

i.e.,

BDCs and face-amount certificate companies) use a different public float threshold, a different seasoning period, or a different approach altogether (

e.g.,

a threshold based on assets or annual investment income)? If so, what threshold would be appropriate for investment companies?

(8) Is a 60-calendar month on-ramp (seasoning period) before LAF status can attach to a registrant appropriate? Would this create a beneficial on-ramp for newer public companies before they could be subject to LAF status? Would a shorter period, such as 24 calendar months, or no seasoning period at all, be more appropriate considering that public companies that meet the proposed public float threshold to be an LAF likely have the resources to comply with the more extensive requirements? Do the very largest new registrants need a 60-calendar month seasoning period, or should certain registrants be required to comply with LAF requirements sooner? If a seasoning period is adopted, should the largest new registrants nevertheless be required to comply sooner with certain of the LAF requirements, such as auditor attestation on ICFR? If so, what would be an appropriate time period for such registrants? Are the proposed mechanics around assessment of the seasoning period sufficiently clear, or would any modification to the proposed amendments or any clarifying guidance be needed?

(9) In order to minimize variation in disclosure obligations and ensure a level of predictability, the proposal contemplates a two-year period after transitioning into or out of LAF status during which a registrant's filer status cannot change. Should we adopt this two-year minimum period, as proposed? Would this have the intended effect of providing registrants and investors with some consistency and predictability as to the disclosure and other requirements a registrant is subject to? Is comparability with respect to a registrant's disclosure over a two-year (or longer) period an important consideration for investors? Would another period be more appropriate? Alternatively, should we consider other ways of addressing these concerns? For example, under the current rules a registrant must fall below a separate, lower threshold to exit AF status than to enter that status; should we retain this approach? If so, why and what lower threshold would be appropriate for exiting LAF status?

(10) Are there any other issues relating to filer status transitioning that the Commission should clarify or address in any final rules? For example, if a registrant deregisters its securities and later re-enters the reporting system, should that registrant be considered a new registrant for purposes of the 60-calendar month seasoning period?

(11) When an issuer qualifies for a new filer status, which under the proposal would only happen at the end of a fiscal year, should the requirements and/or accommodations of that new status apply to the issuer beginning with the annual report for the fiscal year in which the change in filer status occurred, as proposed? Should issuers have the option to apply a change in filer status earlier than as proposed?

B. Non-Accelerated Filer Amendments

We are proposing to define “non-accelerated filer” to mean an issuer [146]

that is not an LAF. As proposed, every registrant would be an NAF beginning at the time of its initial public offering or registration and for at least five years following, as a result of the proposed 60 consecutive calendar months on-ramp requirement before a registrant could become an LAF. An issuer would then remain an NAF unless and until it had an aggregate worldwide market value of the voting and non-voting common equity held by its non-affiliates, or public float, of at least $2 billion for two consecutive years. After an NAF qualifies as an LAF and thereby loses its NAF status, it could regain its NAF status if its public float is less than $2 billion for two consecutive years.

We also propose to extend to NAFs the disclosure requirements and other accommodations currently applicable to SRCs and EGCs.[147]

While we estimate that the proposed NAF filer status would account for approximately 81 percent of reporting companies currently, they would account for only 6.5 percent of total market public float. We therefore believe it is appropriate and in the public interest to leverage the accommodations and requirements that have been effective for registrants that are currently SRCs and/or EGCs, which compose over 52 percent of current registrants, in resetting our disclosure framework to be better tailored to market following. We anticipate that this change will help rebalance the costs and benefits associated with public company status with the intention of facilitating more companies going and staying public, which will ultimately increase transparency in the market to the benefit of investors, while still maintaining investor protections. We further anticipate that reducing the burdens of periodic disclosure may enable management teams to better focus on business operations.[148]

We recognize that this approach will result in the loss of some information, loss of auditor attestation of ICFR, and longer reporting deadlines for certain registrants that currently qualify as

( printed page 30102)

LAFs or AFs but would qualify as NAFs under the proposed rules. However, we believe that the material information necessary for investors to make sound investment and voting decisions will continue to be required from and provided by NAFs under the proposed rules. NAFs would also continue to be subject to annual, other periodic and current reporting requirements, including required disclosure of audited financial statements as well as MD&A of the registrant's financial condition and results of operations, and management's assessment of and report on the effectiveness of the registrant's ICFR, which would continue to provide transparency to investors and assist them in making informed investment and voting decisions.

1. Non-Accelerated Filer Definition

Under the current rules, the term “non-accelerated filer” is not defined. The term is used informally and widely to refer to a registrant that is neither an LAF nor an AF, which typically means a registrant with under $75 million in public float.[149]

Currently, an NAF can also be an SRC, an EGC, or both. We are proposing to define a new regulatory category termed “non-accelerated filer,” which we propose to define in Securities Act Rule 405 and Exchange Act Rule 12b-2 as “an issuer that is not a large accelerated filer.” As a result, the default status for any Exchange Act reporting company (other than asset-backed issuers, pursuant to an exception we are proposing in Rule 405 and Rule 12b-2) would be an NAF; until a company meets the proposed new conditions for becoming an LAF, it would remain an NAF.[150]

In addition, under the proposed rules, NAFs would be subject to essentially the same requirements and accommodations that are applicable to SRCs and EGCs under the current rules.[151]

By expanding NAF filer status under the proposed amendments, more registrants would qualify as NAFs and therefore would not be required to comply with the ICFR auditor attestation requirement.[152]

With these amendments, we further propose to eliminate the “accelerated filer” [153]

and “smaller reporting company” [154]

categories, and the corresponding definitions in Item 10 of Regulation S-K,[155]

Rule 405,[156]

and Rule 12b-2,[157]

since they will no longer be necessary given the expansion of NAF status.[158]

Because the proposed amendments would extend to NAFs the disclosure accommodations currently available to EGCs, the proposed amendments would generally make separate reliance on those JOBS Act provisions [159]

for EGCs unnecessary.[160]

The proposed changes would establish a clearly demarcated on-ramp for registrants to grow and gain experience as reporting companies before becoming subject to the more detailed and expansive disclosure obligations applicable to LAFs. As noted above, the Commission has long considered how best to apply a disclosure regulation framework to companies that vary widely in size and resources to comply with complex securities laws and rules. During its history, the Commission has established various categories, such as “small business issuers,” “smaller reporting companies,” and “accelerated filers,” in tailoring disclosure and reporting requirements based on the needs of investors with an awareness of the potential burdens associated with registrants' ability to comply with those requirements. In the JOBS Act, Congress similarly sought to address some of these concerns for newly public companies by establishing the EGC filer status and reaffirmed the need for the Commission to consider ways to further streamline the requirements for the benefit of new and smaller companies in the FAST Act.[161]

Accordingly, we believe that the consolidation of SRC and EGC accommodations into a single regulatory filer status and the elimination of the AF status as a standalone status is in the public interest and consistent with the protection of investors.

The proposed amendments would transform what is currently a layered and complex set of filer statuses into a more streamlined structure, with the

( printed page 30103)

intent of simplifying the regulatory scheme. Registrants would no longer need to assess each year multiple filer status entry and exit thresholds, many of which are overlapping and often have inconsistent lines distinguishing one set of requirements from the next.

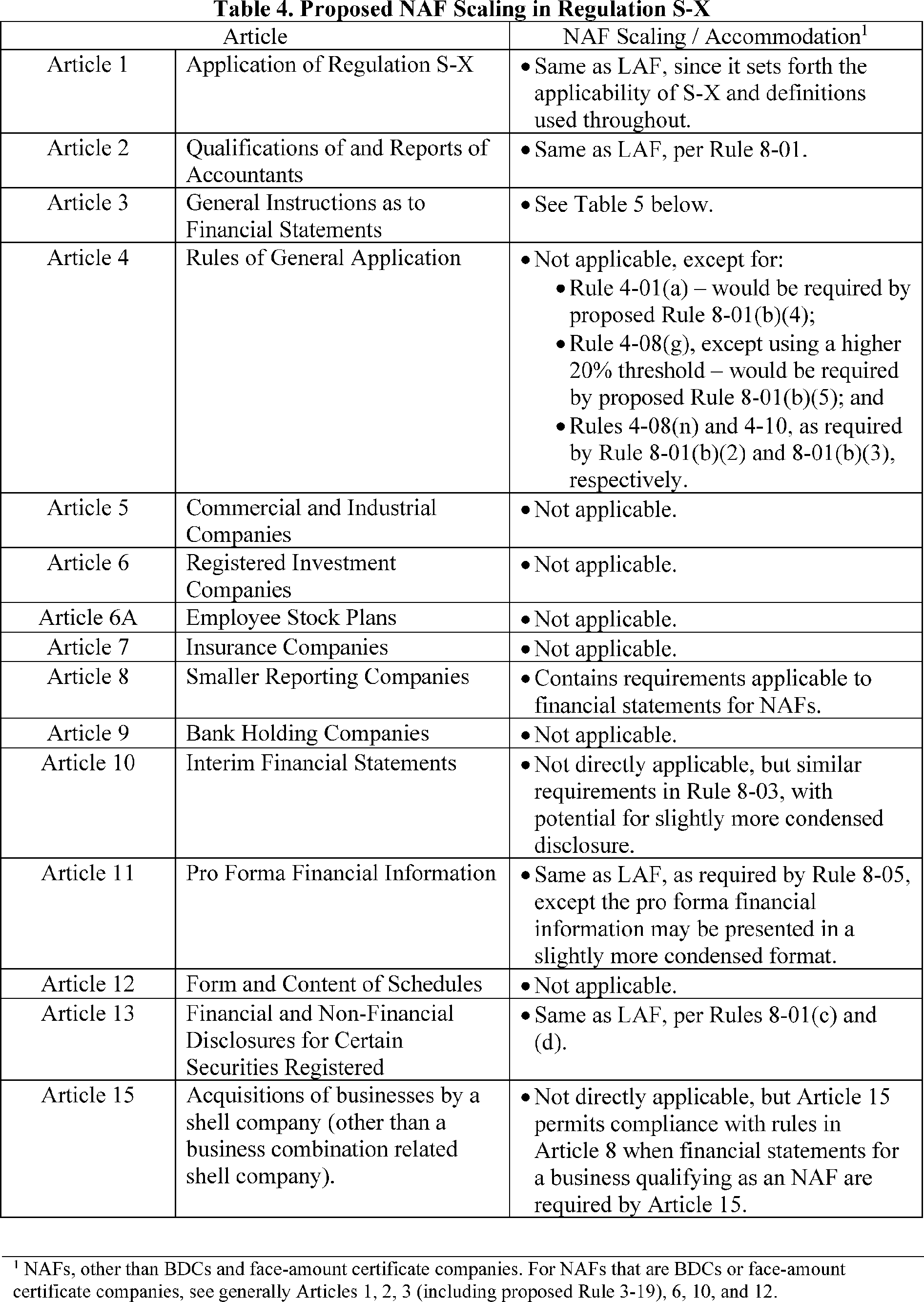

In addition, the expanded category of NAFs would be subject to fewer of the costly requirements that currently apply to LAFs and AFs. As discussed in more detail in the sections that follow, for example, NAFs would be permitted to rely on Article 8 of Regulation S-X for scaled financial disclosure and provide only two (instead of three) years of audited financial statements in their annual reports and registration statements, would be permitted to comply with scaled executive compensation disclosure requirements, and would not be subject to the ICFR auditor attestation requirement.[162]

As a result, we expect that NAFs would have reduced costs of compliance compared to LAFs and would have ample notice to prepare for accelerated filing, additional disclosure, and required auditor attestation of ICFR should they transition to LAF status.

We recognize that the proposed expansion of NAF status and application of EGC and SRC disclosure requirements would result in reduced disclosure for many registrants and their investors. While that reduction in disclosure may result in costs to investors, both investors and registrants may also benefit from more companies choosing to register their securities or to continue as public companies. This would provide more public market investment opportunities that would be subject to robust disclosure requirements, which provide greater transparency as compared to private markets. In addition, and as discussed in more detail in sections IV and V below, we believe investors and registrants would benefit from a more easily understandable filer status framework that imposes fewer compliance costs, the ultimate burdens of which are borne by a registrant's shareholders. Moreover, as discussed in more detail in section IV below, we estimate that the proposed changes would apply to registrants representing approximately 6.5 percent of total market public float, while registrants representing approximately 93.5 percent of total market public float would remain subject to LAF reporting requirements. We believe this focus on ensuring that the registrants that represent the vast majority of the market continue to comply with the most extensive requirements mitigates investor protection concerns with the proposed amendments.

2. ICFR and the Auditor Attestation Requirement

One significant effect of the proposed amendments would be a decrease in the number of registrants required to obtain an auditor attestation of management's assessment of the effectiveness of the company's ICFR. Sarbanes-Oxley Act section 404(b) requires the auditor that prepares or issues the issuer's audit report (other than for EGCs) to attest and report on management's assessment of the effectiveness of ICFR; however section 404(c) exempts registrants that are not LAFs or AFs from the ICFR auditor attestation requirement. By increasing the upper bound of NAF status from less than $75 million (or less than $700 million if revenues are less than $100 million) to less than $2 billion, the proposed amendments would expand by 26.7 percent the number of current registrants that would qualify as NAFs and would therefore not be subject to an ICFR auditor attestation requirement.[163]

Additionally, with respect to newly public companies, the proposed minimum five-year on-ramp (60 calendar months) before entering LAF status would allow these companies additional time to adjust to being a public company before potentially being exposed to ICFR auditor attestation costs. This in turn may incentivize some companies to go public sooner, which could open to investors additional opportunities for investments that might otherwise have stayed in the private market or which some investors may not have otherwise been able to access.

As noted, under the proposal, NAFs would remain subject to the Commission's rules under section 404(a), which require management to establish, state its responsibility to establish and maintain, and provide its assessment of, the registrant's ICFR.[164]

NAFs would also continue to be required to obtain a financial statement audit by a registered public accounting firm [165]

in which the auditor is required to obtain an understanding of ICFR as part of its risk assessment procedures.[166]

Obtaining an understanding of ICFR includes evaluating the design of controls that are relevant to the financial statement audit and determining whether the controls have been implemented.[167]

Additionally, the auditor may test the operating effectiveness of certain internal controls in connection with the financial statement audit.[168]