Securities and Exchange Commission

- [Release No. 34-105549; File No. SR-Phlx-2025-50]

I. Introduction

On September 23, 2025, Nasdaq PHLX LLC (“Phlx” or “Exchange”) filed with the Securities and Exchange Commission (“Commission”), pursuant to Section 19(b)(1) of the Securities Exchange Act of 1934 (“Act”) [1] and Rule 19b-4 thereunder,[2] a proposed rule change to list and trade options on the Nasdaq Bitcoin Index. The proposed rule change was published for comment in the Federal Register on September 29, 2025.[3] On November 3, 2025, pursuant to Section 19(b)(2) of the Act,[4] the Commission designated a longer period within which to approve the proposed rule change, disapprove the proposed rule change, or institute proceedings to determine whether to disapprove the proposed rule change.[5] On December 23, 2025, the Commission instituted proceedings under Section 19(b)(2)(B) of the Act [6] to determine whether to approve or disapprove the proposed rule change.[7] On March 20, 2026, the Commission designated a longer time for Commission action on the proposed rule change.[8] The Commission received comments regarding the proposed rule change.[9] On May 15, 2026, the Exchange filed Amendment No. 1 to the proposed rule change, which replaces and supersedes the original filing in its entirety.[10] The Commission is publishing this notice and order to solicit comment on Amendment No. 1 in Sections II and III below, which Items have been prepared by the Exchange, and to approve the proposed rule change, as modified by Amendment No. 1, on an accelerated basis.

II. Self-Regulatory Organization's Statement of the Terms of Substance of the Proposed Rule Change

The Exchange proposes to list and trade Nasdaq Bitcoin Index Options, a new index that reflects the price of Bitcoin. This Amendment No. 1 replaces and supersedes the original filing in its entirety and proposes to: (1) amend the definitions for “CME CF Cryptocurrency Pricing Products Oversight Committee,” “current index value,” and “reporting authority”; (2) amend the description of the utilization of Nasdaq Bitcoin Index Options; (3) amend the minimum increment rule text and justification for the proposed minimum increment; (4) update the position limit rule with respect to reporting and justification for the proposed position and exercise limits; (5) amend the index level rule text; (6) amend the name of final settlement index; (7) amend the interval of dissemination of the BRTI; (8) amend the conditions to list and trade Nasdaq Bitcoin Index Options including the type of exemptive relief required from the CFTC; (9) add a new Section 10 related to margin; and (10) amend rule citations and data.

The text of the proposed rule change is available on the Exchange's website at https://listingcenter.nasdaq.com/rulebook/phlx/rulefilings, and at the principal office of the Exchange. ( printed page 31770)

III. Self-Regulatory Organization's Statement of the Purpose of, and Statutory Basis for, the Proposed Rule Change

In its filing with the Commission, the Exchange included statements concerning the purpose of and basis for the proposed rule change and discussed any comments it received on the proposed rule change. The text of these statements may be examined at the places specified in Item V below. The Exchange has prepared summaries, set forth in sections A, B, and C below, of the most significant aspects of such statements.

A. Self-Regulatory Organization's Statement of the Purpose of, and Statutory Basis for, the Proposed Rule Change

1. Purpose

The Exchange proposes to introduce a new index options product, Nasdaq Bitcoin Index Options. This index would enable retail and institutional investors to obtain a precise price for Bitcoin.

Nasdaq Bitcoin Index Options, as proposed, shall have a ticker symbol “QBTC” and will be based on the underlying index, CME CF Bitcoin Real Time Index (“BRTI”) [11] divided by a factor of one hundred (100) and disseminated as the “CF NQBTC Options Indicative Settlement Value.” The Exchange shall utilize a separate methodology to calculate the final settlement price. The final settlement price shall be the “CF NQBTC Options Settlement Value” which is calculated on the expiration date by observing transactions during a one-hour window from 15.00 to 16.00 New York Time, separated into twelve partitions of five minutes, each with a resulting volume-weighted median (“VWM”), which index value is expressed as the arithmetic mean of the twelve (12) VWMs, resulting in the CME CF Cryptocurrency Reference Rate—New York Variant (“BRRNY”) [12] which is then divided by a factor of one hundred (100). The purpose of utilizing the BRRNY divided by a factor of one hundred (100), known as the CF NQBTC, as the final settlement price is to provide a replicable, manipulation-resistant and representative Bitcoin benchmark that synchronizes with the traditional U.S. options market close timeframe.

Options on this new index will be cash-settled, with a European-style exercise.

Background

The BRTI [13] is a benchmark index price calculated and published once per 200 milliseconds for Bitcoin that aggregates order data from Bitcoin-USD markets operated by major cryptocurrency exchanges that conform to the CME CF Constituent Exchange Criteria.[14] The BRTI is calculated every 200 milliseconds of every day, using the Relevant Order Books [15] of all Constituent Exchanges,[16] thereby aggregating the notional value of Bitcoin across major Bitcoin spot platforms.

The BRTI is designed based on the IOSCO Principles for Financial Benchmarks.[17] The administrator of the BRTI and BRRNY is CF Benchmarks Ltd.

A trading venue is eligible as a Constituent Exchange in any of the CME CF Cryptocurrency Pricing Products [18] if it offers a market that facilitates the spot trading of the relevant cryptocurrency base asset (Bitcoin) against the corresponding quote asset (U.S. Dollars), and makes trade data and order data available through an API with sufficient reliability, detail and timeliness. Furthermore, it must meet certain criteria established by the CME CF Cryptocurrency Pricing Products Oversight Committee.[19] Should the average daily contribution of a Constituent Exchange fall below 3% for any CME CF Cryptocurrency Pricing Product, then the continued inclusion of the venue as a Constituent Exchange to the Relevant Pair shall be assessed by the CME CF Oversight Committee.

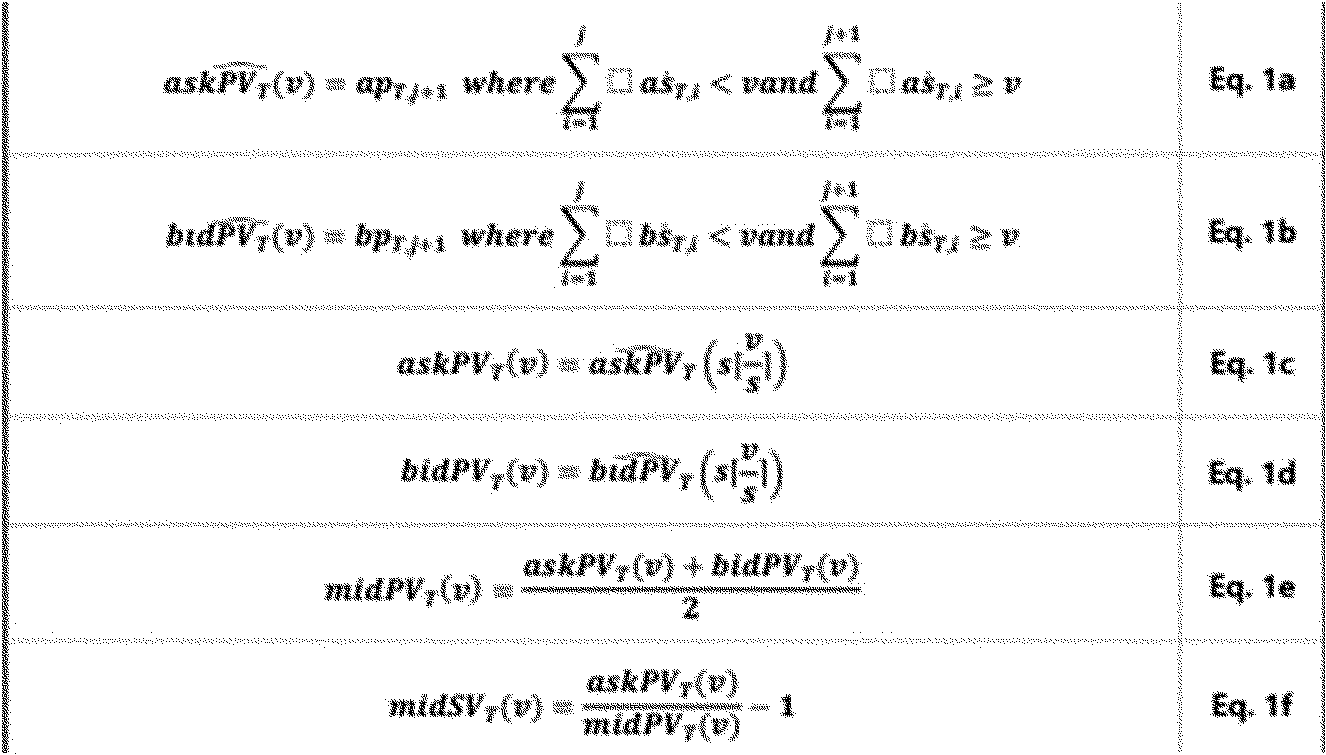

When calculated, the Relevant Order Book of each Constituent Exchange is added to a joint list of order books,[20] ( printed page 31771) which are aggregated into one consolidated order book. If the size at the bid or ask order price level exceeds the order size cap that is set by CF Benchmarks, it enters the consolidated order book with a size equal to the order size cap. The cumulative bid price-volume curve, ask price-volume curve, mid-price volume curve [21] and mid spread-volume curve are calculated from the consolidated order book at a granularity equal to the spacing parameter.

Using the above notation, the ask price-volume curve is defined as askPV, the bid price-volume curve as bidPV, the mid-price volume curve as midPV, and the mid spread-volume curve as midSV, in each case as of the effective time T, as:

At a high level, the mid-price volume curve represents the average of the marginal price at which a certain amount of Bitcoins can be sold and at which that same amount can be bought. By averaging across the mid-price volume curve, the BRTI represents a blend of such (hypothetical) transactions at various transaction sizes.[22]

The utilized depth is calculated as the maximum cumulative volume for which the mid spread-volume curve does not exceed a certain percentage deviation from the mid-price.[23] If this volume is less than the spacing parameter, the utilized depth is set to the spacing parameter. The utilized depth, v, is calculated as:

At a high level, the BRTI is calculated from the section of the mid-price volume curve for which ask limit orders at a certain depth diverge by no more than 0.5% from the mid-price at that depth. It therefore reflects a significant portion of the top of the consolidated order book (as opposed to, for instance, the best bid and ask prices only) but discards limit orders that are less likely to be matched. This makes it a meaningful representation of true Bitcoin liquidity and robust to local changes in order books. Note that utilized depth will always include crossed orders for any of the consolidated order books of the Constituent Exchanges, along with limit orders on the order books of Constituent Exchanges up to 0.5% away of the mid-price volume curve. If zero size resides in both these sections, utilized depth is set to one. The BRTI is then effectively equal to the mid-price of the consolidated order book.[24]

The mid-price volume curve is weighted by the normalized probability density of the exponential distribution up to the utilized depth. The BRTI is then given by the sum of the weighted mid-price volume curve obtained in the previous step.[25] The BRTI as of the effective time T, CCRTI, is then given by:

The order size cap is calculated from the uncapped consolidated order book. Using the above notation, the dynamic order size cap is derived as follows:

The order size cap as of the effective time T, C, is then given by:

If the Retrieval Time of the Relevant Order Book of a Constituent Exchange is at least 30 seconds older than the Calculation Time, the Constituent Exchange is disregarded in the calculation of the BRTI for that Calculation Time. If the Retrieval Times of the Relevant Order Books of all Constituent Exchanges are at least 30 seconds older each than the Calculation Time, the BRTI calculation failure occurs for that Calculation Time. All Relevant Order Books are subject to an automated screening for erroneous data.[26]

At a high level, the mid-price volume curve is weighted such that prices near the current market prices (at the mid-point) are weighted higher than prices that are far away from where trading is occurring (at the bid or offer).

Overview of the Bitcoin Industry

Bitcoin is a digital asset that is created and transmitted through the operations of the peer-to-peer Bitcoin network, a decentralized network of computers that operates on cryptographic protocols (the “Bitcoin network”). No single entity owns or operates the Bitcoin network, the infrastructure of which is collectively maintained by its user base. The Bitcoin network allows people to exchange tokens of value, called Bitcoin, which are recorded on a public transaction ledger known as the Bitcoin blockchain (the “Bitcoin blockchain”). Bitcoin can be used to pay for goods and services, or it can be converted to fiat currencies, such as the U.S. dollar, at rates determined on Bitcoin platforms that enable trading in Bitcoin or in individual end-user-to-end-user transactions under a barter system.

The Bitcoin network is commonly understood to be decentralized and does not require governmental authorities or financial institution intermediaries to create, transmit or determine the value of Bitcoin. Rather, Bitcoin is created and allocated by the Bitcoin network protocol through a “mining” process. The value of Bitcoin is determined by the supply of and demand for Bitcoin-on-Bitcoin platforms or in private end-user-to-end-user transactions.

New Bitcoins are created and rewarded to the miners of a block in the Bitcoin blockchain for verifying transactions. The Bitcoin blockchain is a shared database that includes all blocks that have been solved by miners and it is updated to include new blocks as they are solved. Each Bitcoin transaction is broadcast to the Bitcoin network and, when included in a block, recorded in the Bitcoin blockchain. As each new block records outstanding Bitcoin transactions, and outstanding transactions are settled and validated through such recording, the Bitcoin blockchain represents a complete, ( printed page 31773) transparent and unbroken history of all transactions of the Bitcoin network.

History of Bitcoin

The Bitcoin network was initially contemplated in a whitepaper that also described Bitcoin and the operating software to govern the Bitcoin network. The whitepaper was purportedly authored by Satoshi Nakamoto. However, no individual with that name has been reliably identified as Bitcoin's creator, and the general consensus is that the name is likely a pseudonym for the actual inventor or inventors. The first Bitcoins were created in 2009 after Nakamoto released the Bitcoin network source code (the software and protocol that created and launched the Bitcoin network). The Bitcoin network has been under active development since that time by a loose group of software developers who have come to be known as core developers.

Overview of Bitcoin Network Operations

In order to own, transfer or use Bitcoin directly on the Bitcoin network (as opposed to through an intermediary, such as an exchange), a person generally must have internet access to connect to the Bitcoin network. Bitcoin transactions may be made directly between end-users without the need for a third-party intermediary. To prevent the possibility of double-spending Bitcoin, a user must notify the Bitcoin network of the transaction by broadcasting the transaction data to its network peers. The Bitcoin network provides confirmation against double-spending by memorializing every transaction in the Bitcoin blockchain, which is publicly accessible and transparent. This memorialization and verification against double-spending is accomplished through the Bitcoin network mining process, which adds “blocks” of data, including recent transaction information, to the Bitcoin blockchain.

Overview of Bitcoin Transfers

Prior to engaging in Bitcoin transactions directly on the Bitcoin network, a user generally must first install on its computer or mobile device a Bitcoin network software program that will allow the user to generate a private and public key pair associated with a Bitcoin address commonly referred to as a “wallet.” The Bitcoin network software program and the Bitcoin address also enable the user to connect to the Bitcoin network and transfer Bitcoin to, and receive Bitcoin from, other users.

Each Bitcoin network address, or wallet, is associated with a unique “public key” and “private key” pair. To receive Bitcoin, the Bitcoin recipient must provide its public key to the party initiating the transfer. This activity is analogous to a recipient for a transaction in U.S. dollars providing a routing address in wire instructions to the payor so that cash may be wired to the recipient's account. The payor approves the transfer to the address provided by the recipient by “signing” a transaction that consists of the recipient's public key with the private key of the address from where the payor is transferring the Bitcoin. The recipient, however, does not make public or provide to the sender its related private key.

Neither the recipient nor the sender reveals their private keys in a transaction because the private key authorizes transfer of the funds in that address to other users. Therefore, if a user loses his or her private key, the user may permanently lose access to the Bitcoin contained in the associated address. Likewise, Bitcoin is irretrievably lost if the private key associated with them is deleted and no backup has been made. When sending Bitcoin, a user's Bitcoin network software program must validate the transaction with the associated private key. The resulting digitally validated transaction is sent by the user's Bitcoin network software program to the Bitcoin network to allow transaction confirmation.

Some Bitcoin transactions are conducted “off-blockchain” and are therefore not recorded in the Bitcoin blockchain. Some “off-blockchain transactions” involve the transfer of control over, or ownership of, a specific digital wallet holding Bitcoin or the reallocation of ownership of certain Bitcoin in a digital wallet containing assets owned by multiple persons, such as a digital wallet maintained by a digital assets platform. In contrast to on-blockchain transactions, which are publicly recorded on the Bitcoin blockchain, information and data regarding off-blockchain transactions are generally not publicly available. Therefore, off-blockchain transactions are not truly Bitcoin transactions in that they do not involve the transfer of transaction data on the Bitcoin network and do not reflect a movement of Bitcoin between addresses recorded in the Bitcoin blockchain. For these reasons, off-blockchain transactions are subject to risks as any such transfer of Bitcoin ownership is not protected by the protocol behind the Bitcoin network or recorded in, and validated through, the blockchain mechanism.

Summary of a Bitcoin Transaction

In a Bitcoin transaction directly on the Bitcoin network between two parties (as opposed to through an intermediary, such as a custodian), the following circumstances must initially be in place: (i) the party seeking to send Bitcoin must have a Bitcoin network public key, and the Bitcoin network must recognize that public key as having sufficient Bitcoin for the transaction; (ii) the receiving party must have a Bitcoin network public key; and (iii) the spending party must have internet access with which to send its spending transaction.

The receiving party must provide the spending party with its public key and allow the Bitcoin blockchain to record the sending of Bitcoin to that public key. After the provision of a recipient's Bitcoin network public key, the spending party must enter the address into its Bitcoin network software program along with the number of Bitcoin to be sent. The number of Bitcoin to be sent will typically be agreed upon between the two parties based on a set number of Bitcoin or an agreed upon conversion of the value of fiat currency to Bitcoin. Since every computation on the Bitcoin network requires the payment of Bitcoin, including verification and memorialization of Bitcoin transfers, there is a transaction fee involved with the transfer, which is based on computation complexity and not on the value of the transfer and is paid by the payor with a fractional number of Bitcoin.

After the entry of the Bitcoin network address, the number of Bitcoin to be sent and the transaction fees, if any, to be paid, will be transmitted by the spending party. The transmission of the spending transaction results in the creation of a data packet by the spending party's Bitcoin network software program, which is transmitted onto the decentralized Bitcoin network, resulting in the distribution of the information among the software programs of users across the Bitcoin network for eventual inclusion in the Bitcoin blockchain.

As discussed in greater detail below, Bitcoin network miners record transactions when they solve for and add blocks of information to the Bitcoin blockchain. When a miner solves for a block, it creates that block, which includes data relating to (i) the solution to the block, (ii) a reference to the prior block in the Bitcoin blockchain to which the new block is being added and (iii) transactions that have occurred but have not yet been added to the Bitcoin ( printed page 31774) blockchain. The miner becomes aware of outstanding, unrecorded transactions through the data packet transmission and distribution discussed above.

Upon the addition of a block included in the Bitcoin blockchain, the Bitcoin network software program of both the spending party and the receiving party will show confirmation of the transaction on the Bitcoin blockchain and reflect an adjustment to the Bitcoin balance in each party's Bitcoin network public key, completing the Bitcoin transaction. Once a transaction is confirmed on the Bitcoin blockchain, it is irreversible.

Creation of a New Bitcoin

New Bitcoins are created through the mining process. The process by which Bitcoin is “mined” results in new blocks being added to the Bitcoin blockchain and new Bitcoin tokens being issued to the miners. Computers on the Bitcoin network engage in a set of prescribed complex mathematical calculations in order to add a block to the Bitcoin blockchain and thereby confirm Bitcoin transactions included in that block's data. The Bitcoin network is designed in such a way that the reward for adding new blocks to the Bitcoin blockchain decreases over time. In the future, once new Bitcoin tokens are no longer awarded for adding a new block, miners will only have transaction fees to incentivize them, and as a result, it is expected that miners will need to be better compensated with higher transaction fees to ensure that there is adequate incentive for them to continue mining.

Limits on Bitcoin Supply

Under the source code that governs the Bitcoin network, the supply of new Bitcoin is mathematically controlled so that the number of Bitcoin grows at a limited rate pursuant to a pre-set schedule. The number of Bitcoin awarded for solving a new block is automatically halved after every 210,000 blocks are added to the Bitcoin blockchain, approximately every 4 years. The fixed reward for solving a new Bitcoin block is currently 3.125 BTC per block. This amount is the result of the most recent Bitcoin halving event, which occurred in April 2024. The next Bitcoin halving is anticipated in 2028 when Bitcoin will halve to 1.5625. This deliberately controlled rate of Bitcoin creation means that the number of Bitcoin in existence will increase at a controlled rate until the number of Bitcoin in existence reaches the pre-determined 21 million Bitcoin. However, the 21 million supply cap could be changed in a hard fork. A hard fork could change the source code to the Bitcoin network, including the 21 million Bitcoin supply cap.

Final Settlement

The term “final settlement value” as defined at proposed Options 4D, Section 2(a)(9) shall be calculated as described at Options 4D, Section 8. The Nasdaq Bitcoin Index Options final settlement value is the BRRNY on the expiration date (usually a Friday), divided by a factor of one hundred (100) and published as the CF NQBTC Options Settlement Value. The BRRNY is calculated daily based on the Relevant Transactions [27] and is calculated on the expiration date for purposes of final settlement. Relevant Transactions include those that trade Bitcoin versus U.S. Dollars on a Constituent Exchange from 15:00 to 16:00 New York Time. The final settlement value is calculated and reported by the reporting authority, CF Benchmarks. The final settlement value is determined by the aggregated last reported sale price of each Constituent Exchange. Specifically, the final settlement value is calculated by combining all Relevant Transactions from each Constituent Exchange on a joint list and recording the trade price and size for each transaction. That list is partitioned into a number of equally-sized time intervals, of 5 minutes. For each partition separately, the volume-weighted median trade price is calculated from the trade prices and sizes of all Relevant Transactions across all Constituent Exchanges. The BRRNY is the equally weighted average of the volume-weighted medians of all partitions. In the event that the Nasdaq Bitcoin Index is not open for trading on the expiration date, the value of the Nasdaq Bitcoin Index shall be the last reported sale price prior to the expiration date.

The BRRNY is methodologically identical to the regulated CME CF Bitcoin Reference Rate (BRR), the most widely used benchmark price for Bitcoin, that settles the Bitcoin-USD derivatives complex listed by CME Group, and which serves as the NAV for exchange listed investment products from WisdomTree Europe, Evolve ETFs (CAN) and QR Asset Management (BRZ). The only difference between the BRRNY and the BRR is that the BRRNY references the price of Bitcoin at the closing time of U.S. markets, 16:00 New York Time, rather than the price at 16:00 London Time, referenced by the BRR.

The purpose of the BRRNY is to provide a replicable, manipulation-resistant and representative Bitcoin benchmark that synchronizes with the traditional U.S. market close. The BRRNY is a regulated Benchmark under the UK Benchmarks Regulation (BMR) regime. The BRRNY calculation methodology aggregates transactions of Bitcoins in U.S. dollars that are only conducted on the most liquid markets for which data is publicly available and operated by exchanges that meet the CME CF Constituent Exchange Criteria.[28]

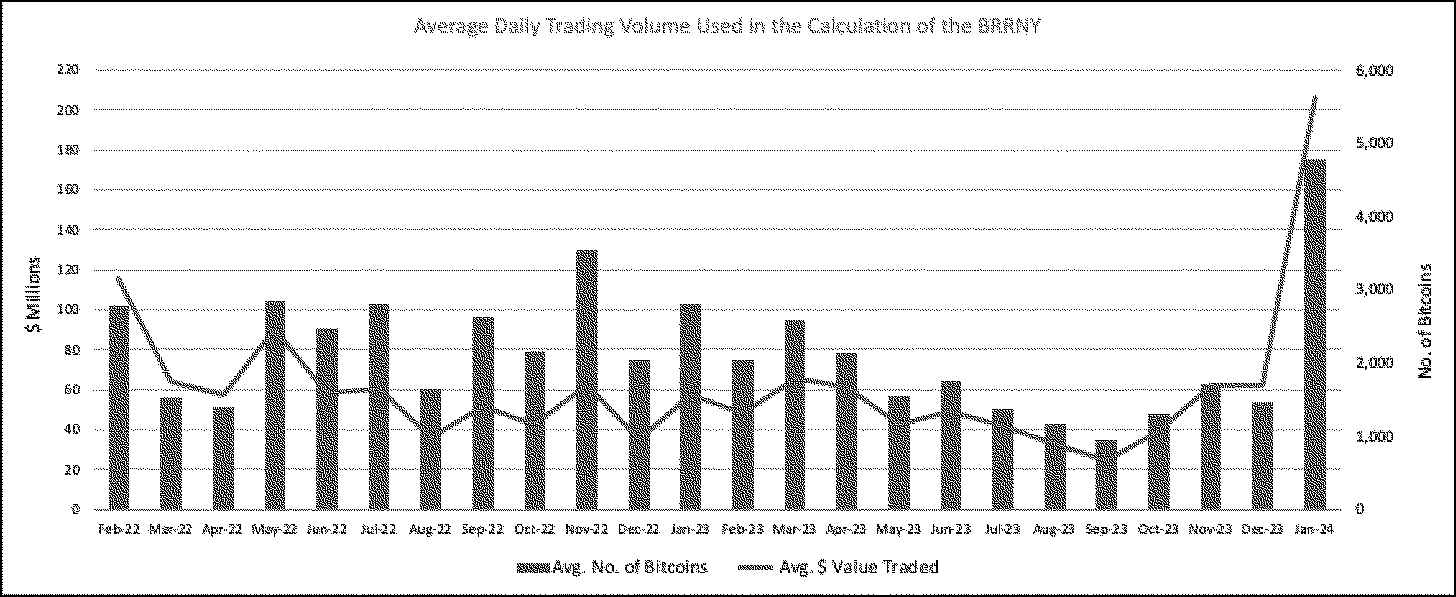

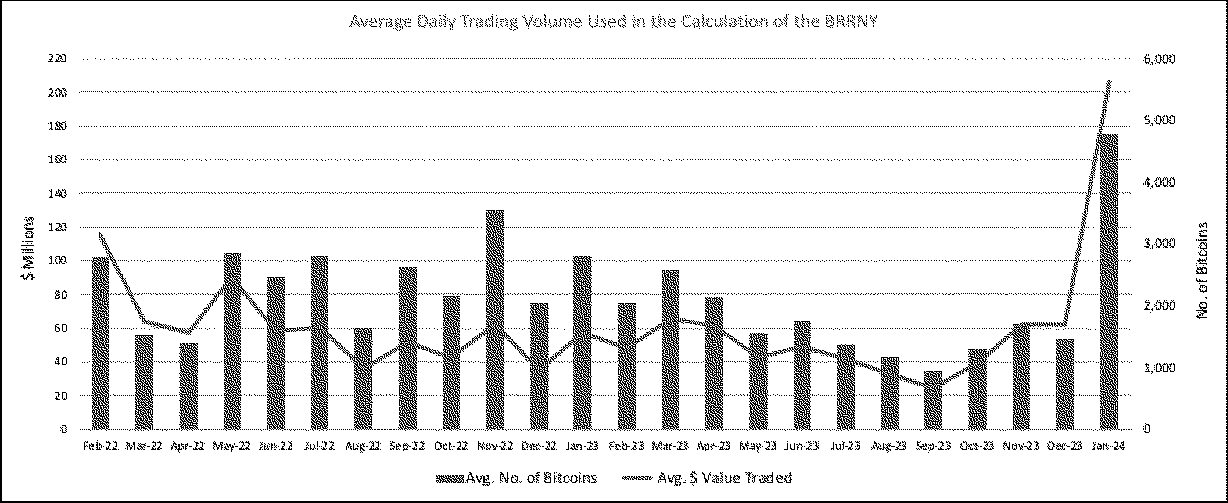

The BRRNY is a valid and robust benchmark that is calculated from input data of sufficient volume so that it is representative of the market it seeks to measure. Additionally, the BRRNY has volume sufficiency which permits it to be replicated by institutional market participants and product providers that need to warehouse price risk. The table below summarizes the total number of transactions and average number of transactions per day observed each month for the BRRNY.[29] Between February 28, 2022, and January 31, 2024 (weekdays only), on average 2,116.73 Bitcoins, or $59M were traded during each daily observation window between 15:00 and 16:00 New York Time.[30]

( printed page 31775)

This trading activity exhibits volatility that is not substantially different from that shown in traditional asset markets. The volume observed and the reliability of that volume are clearly evident to be sufficient for the calculation of a robust and reliable benchmark.

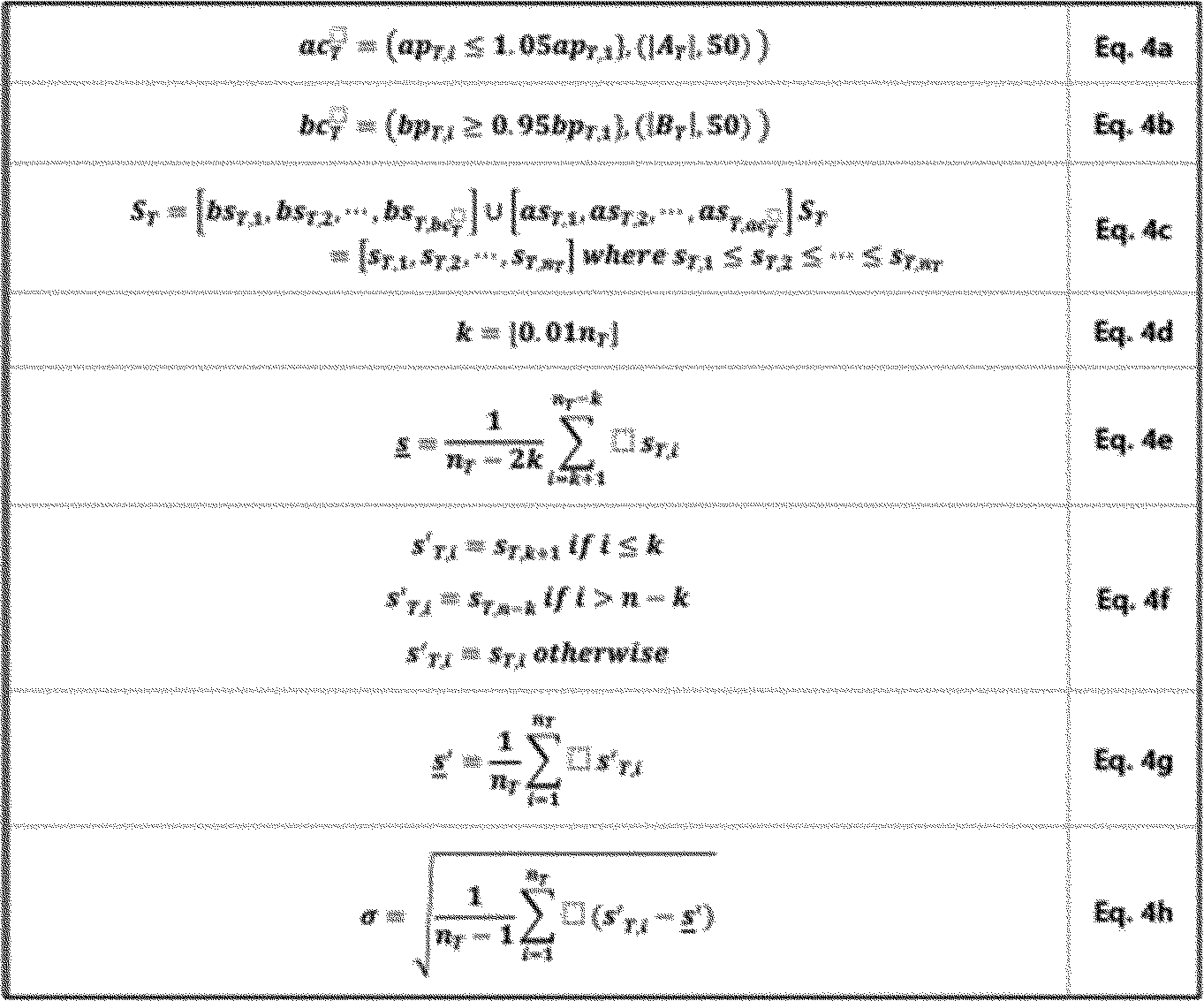

Phlx believes that Nasdaq Bitcoin Index Options will be utilized for a wide range of activities such as hedging cash portfolio risk, creating tailored or structured products that allow investor risk-mitigated participation in Bitcoin, and onshoring of risk associated with holding capital and options in non-U.S. regulated venues. To that end, the index design is fair and transparent. CF Benchmarks, the administrator of the Nasdaq Bitcoin Index, exclusively sources input data from Constituent Exchanges that meet published criteria as set out in its CME CF Constituent Exchange Criteria and CF Benchmarks conducts a thorough review of any exchange under consideration for inclusion as a Constituent Exchange.[31] The BRRNY methodology takes an observation period and divides it into equal partitions of time. The volume-weighted median of all transactions within each partition is then calculated. The benchmark index value is determined from the arithmetic mean of the volume-weighted medians, equally weighted. As a result, individual trades of large size have limited effect on the index level as they only influence the level of the volume-weighted median for that specific partition. Further, a cluster of trades in a short period of time will also only influence the volume-weighted median of the partition or partitions they were conducted in, thereby limiting impact. Use of volume-weighted medians as opposed to volume-weighted means ensures that transactions conducted at outlying prices do not have an undue effect on the value of a specific partition because trades of large size or clusters of trades over a short period of time will not have an undue influence on the index level. CF Benchmarks applies equal weight to transactions observed from Constituent Exchanges. With no pre-set weights, the BRRNY is not readily subject to manipulation. Using the arithmetic mean of partitions of equal weight further denudes the effect of trades of large size at prices that deviate from the prevailing price having undue influence on the benchmark level.[32]

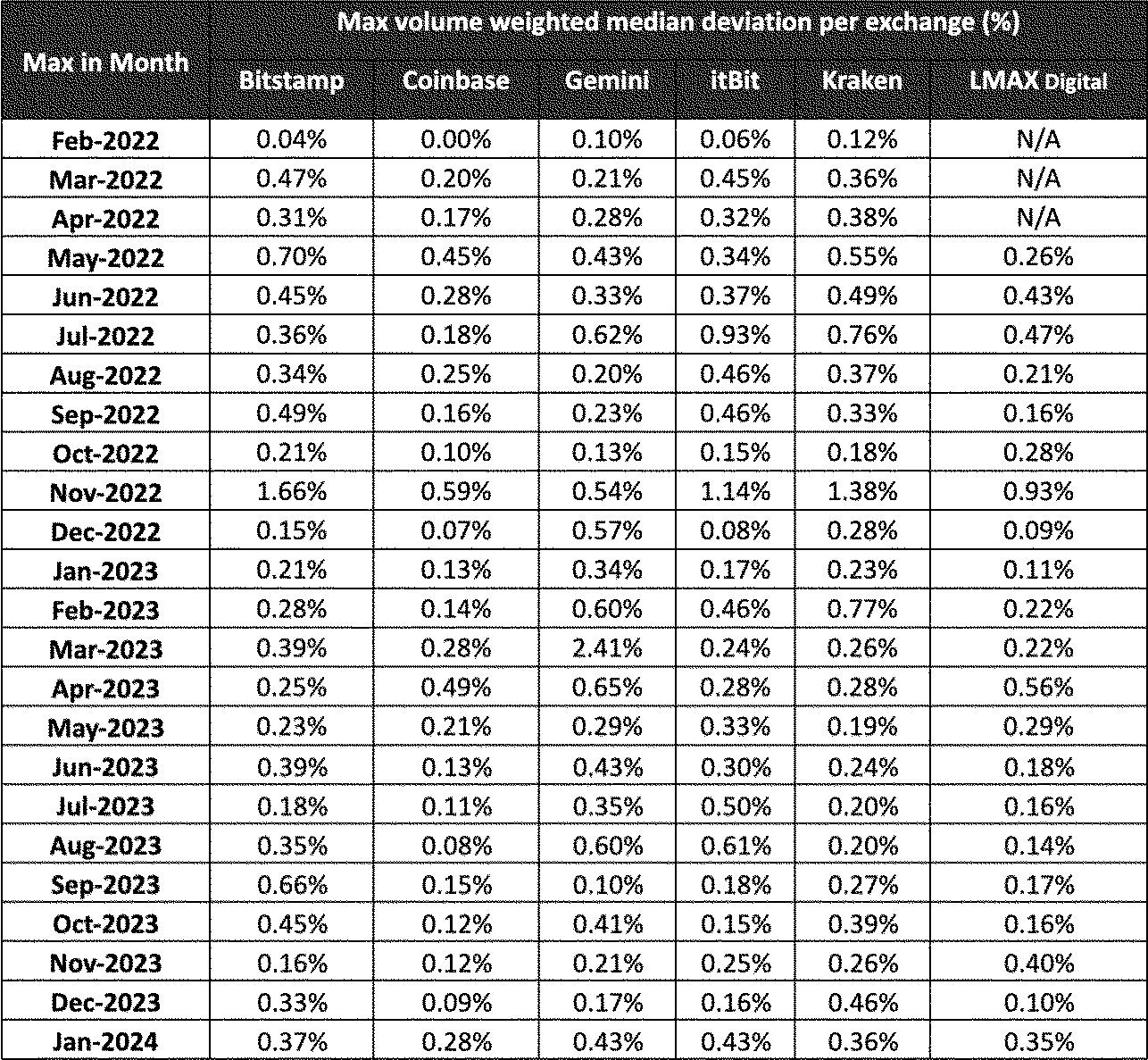

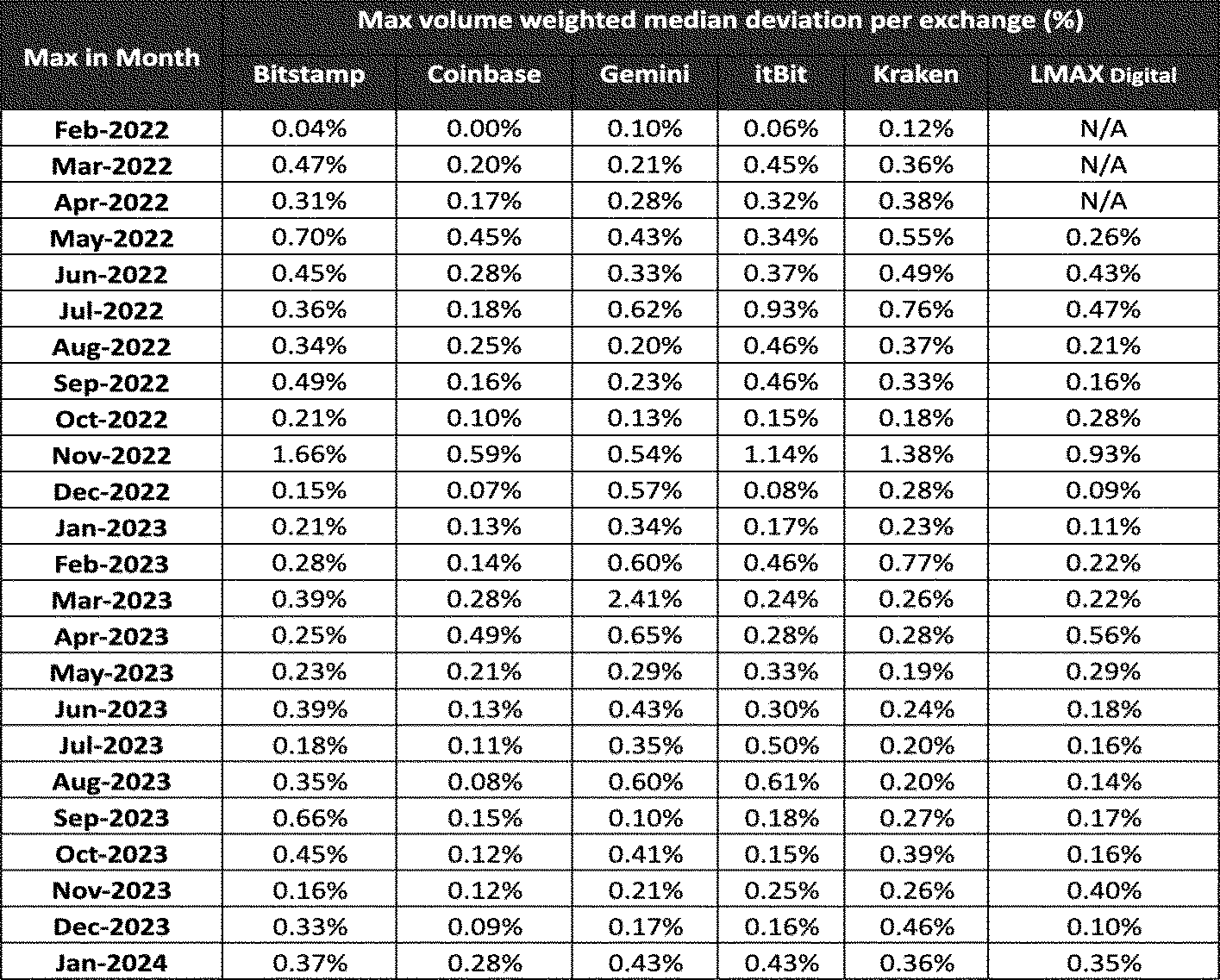

The BRRNY methodology incorporates a procedure for potentially erroneous data. In the event of an instance of index calculation in which a Constituent Exchange's volume-weighted median transaction price exhibits an absolute percentage deviation from the volume-weighted median price of other Constituent Exchange transactions greater than the Potentially Erroneous Data Parameter [33] (10%), then transactions from that Constituent Exchange are deemed potentially erroneous and excluded from the index calculation. All instances of data excluded from a calculation trigger an alert that is investigated by CF Benchmarks. By way of example, between February 28, 2022, and January 31, 2024, the Potentially Erroneous Data Parameter of the methodology for the BRRNY has never been triggered. Analysis of the highest volume-weighted median per exchange during the observation period produced the results in the table below. The results illustrate that during the observation period, no Constituent Exchange's input data needed to be excluded due to exhibiting potential manipulation and indeed no individual cryptocurrency exchange exhibits a deviation percentage above 2.41% during this period.

( printed page 31776)

CF Benchmarks has implemented a benchmark surveillance program for the investigation of alerts. Instances of suspected benchmark manipulation are escalated through appropriate regulatory channels in accordance with CF Benchmarks' obligations under the UK Benchmarks Regulation (UK BMR). As a regulated Benchmark Administrator, CF Benchmarks is subject to supervision by the UK FCA.[34]

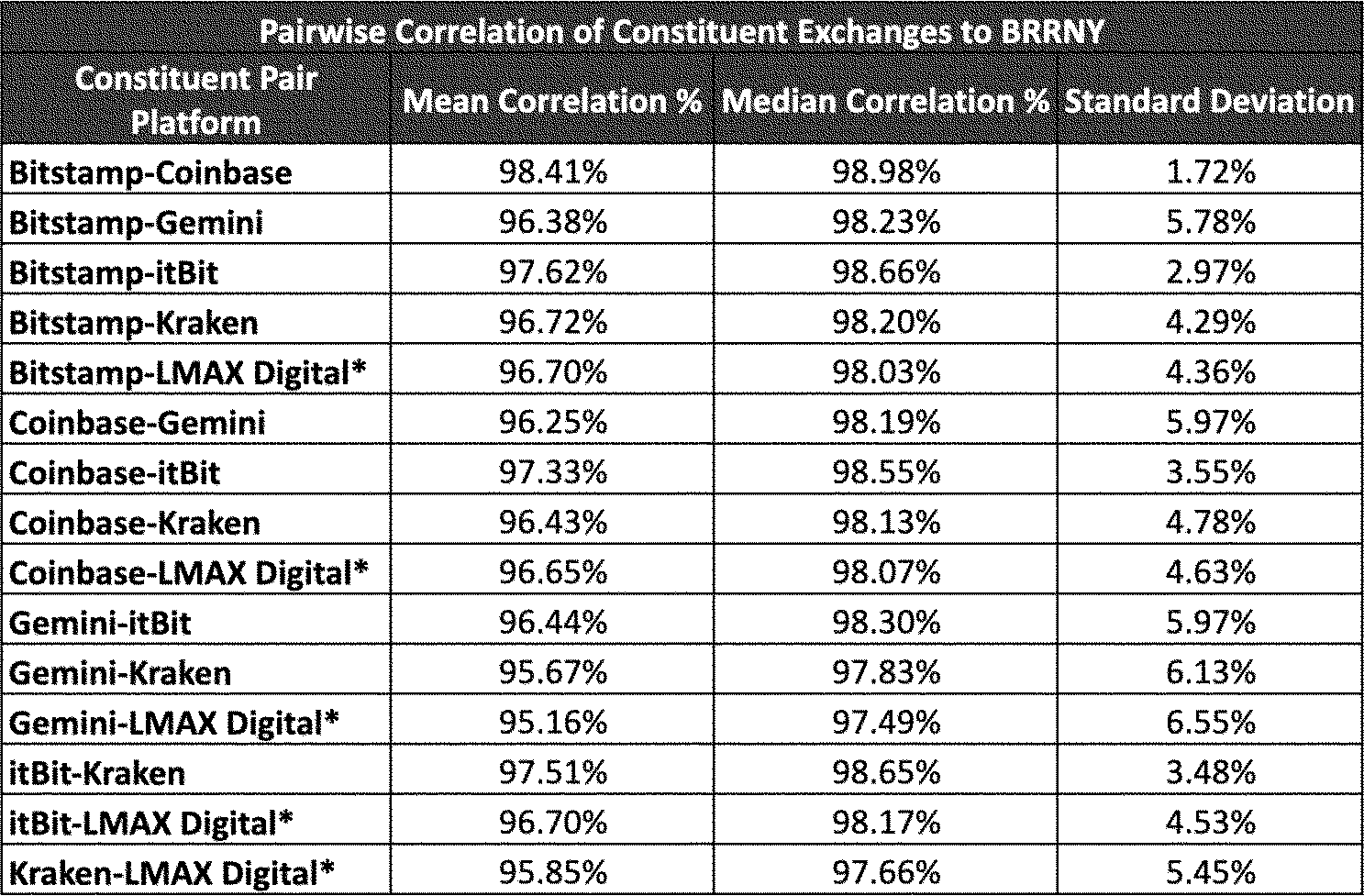

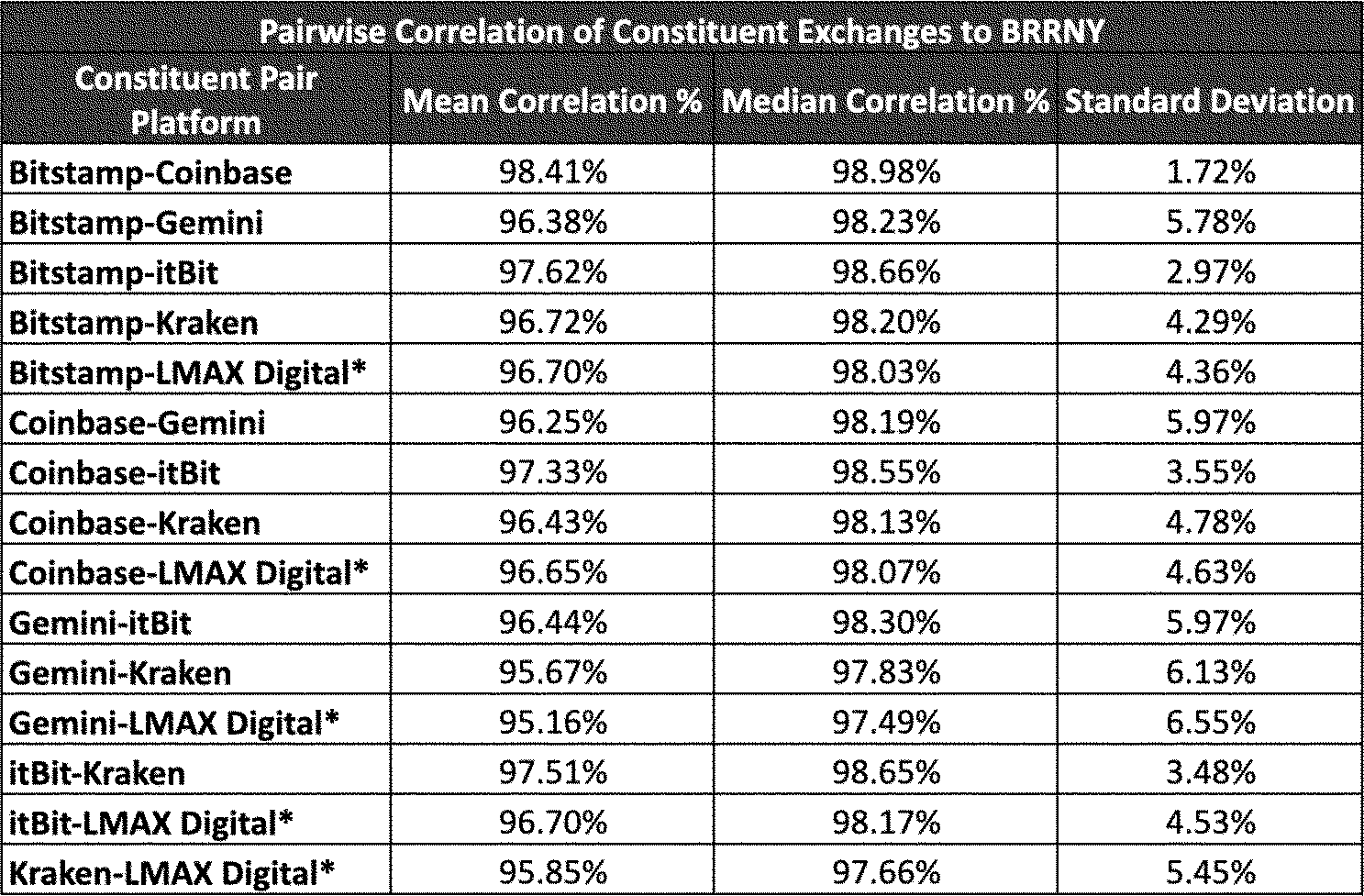

In terms of this correlation of prices among Constituent Exchanges as shown in the table above, an analysis was undertaken of the pair-wise correlation of prices from Constituent Exchanges on a per-minute basis (the price difference between transactions for each minute at each exchange) during the observation period. The results are shown in the table below.

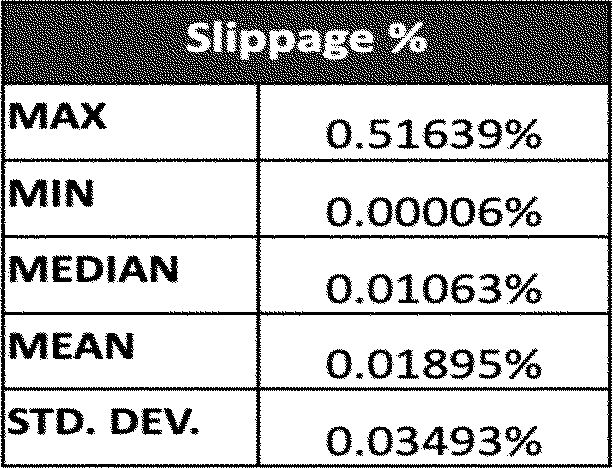

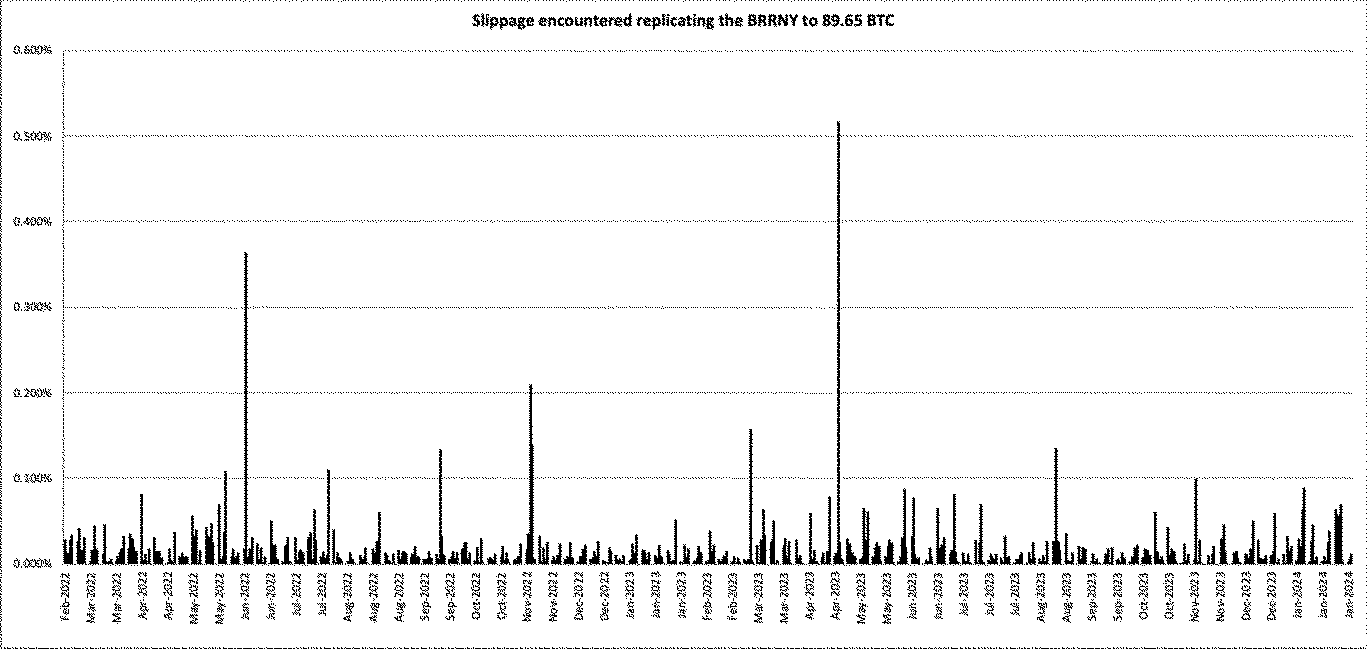

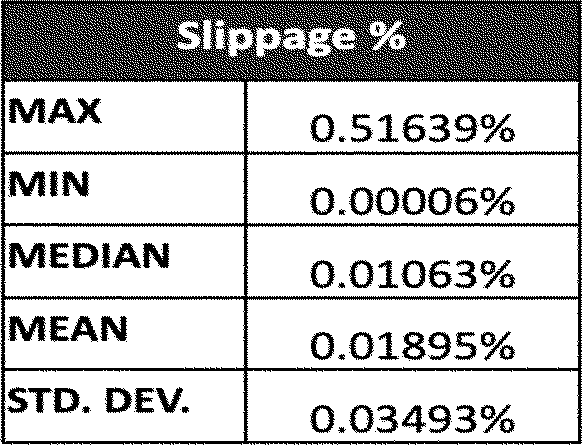

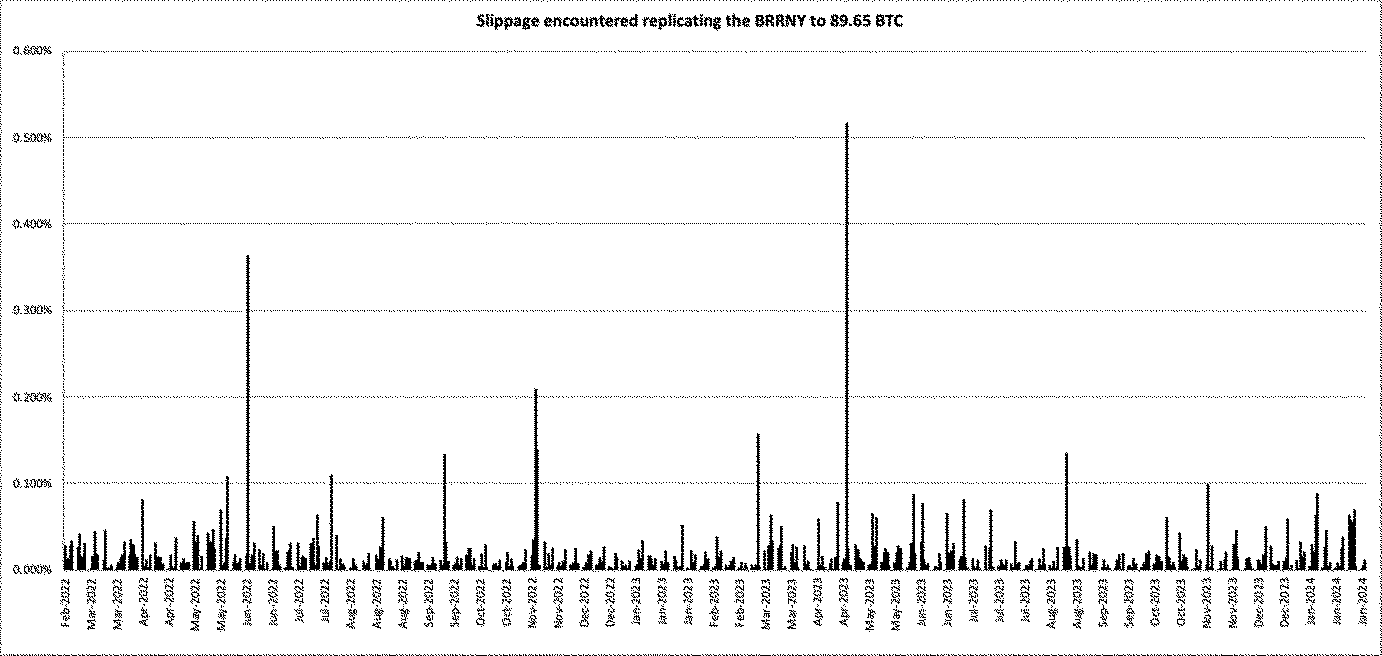

With respect to replicability, a simple replication simulation was thereby conducted of BRRNY to demonstrate the extent of slippage [35] that implementation of the BRR would probably encounter. The methodology was as follows for weekdays only.

Trades are executed on n (6) Constituent Exchanges, during a 3,600-second window.

One trade is executed every second and the price achieved is assumed to be the last execution price observed in that second. Its associated volume is assumed to be the volume executed during that second.

If no trade is completed in any single-second period, then the price achieved is assumed to be the price achieved in the previous second, but the associated volume from the previous second is not added to the volume executed in the latest second.

The results of this simulation are displayed below.

Summary data for the above simulation is provided below.

As evidenced above, the BRRNY can be replicated with a high degree of confidence and usually with slippage of no more than 1 basis point (0.01%). On only 6.76% of days would slippage have been greater than 5 basis points (0.05%). Indeed, even on the most volatile day, slippage was approximately one half of one percent, 51.6 basis points (0.516%). Furthermore, in the 24-month period under observation slippage would have been in double-digit basis points only 10 times.

As evidenced by the foregoing data, the BRTI is representative of the underlying market, resistant to manipulation, and replicable by market participants.

Regulatory Framework

The proposed product is a cash-settled index option that permits holders to receive U.S. dollars representing the difference between the current Bitcoin spot markets as represented by the BRRNY and the exercise price of the option. Like the Spot Bitcoin ETPs,[36] the Nasdaq Bitcoin Index Options do not hold physical Bitcoin.

Since January 2024, shares of Spot Bitcoin ETPs based on Bitcoin have been listed and traded on national securities exchanges.[37] Phlx's proposal to list and trade Nasdaq Bitcoin Index Options would allow market participants that hold shares of Spot Bitcoin ETPs to hedge or modify their exposure on a national securities exchange, within a single regulatory regime,[38] thereby fostering innovation and competition in the rapidly evolving market for digital asset derivatives.

Section 2(a)(1)(A) of the Commodity Exchange Act (the “CEA”) [39] provides the Commodity Futures Trading Commission (the “CFTC”) with exclusive jurisdiction over, among other things, options on commodities traded on a designated contract market, swap execution facility, or other board of trade, exchange, or market. The Exchange believes that the proposed Nasdaq Bitcoin Index Options should be permitted to trade on a national securities exchange provided the Exchange requests and obtains exemptive relief from the CFTC that would: (1) provide the Exchange with exemption from any applicable requirements of the CEA and the CFTC and regulations, including the requirements applicable to a Designated Contract Market under Section 5 of the CEA [40] and Part 38 [41] of the CFTC's regulations; and (2) provide the Commission, with the CFTC, with jurisdiction over the proposed Nasdaq Bitcoin Index Options; and (3) provide ( printed page 31778) exemptive relief to allow the proposed Nasdaq Bitcoin Index Options to clear through The Options Clearing Corporation (“OCC”) in its capacity as a clearing agency registered with the SEC pursuant to Section 17A of the Act.[42]

The Exchange acknowledges that it will not be permitted to list and trade the proposed Nasdaq Bitcoin Index Options unless and until the CFTC grants all necessary exemptive relief [43] from the requirements of the CEA and the rules and regulations thereunder, with the condition that the SEC exercise jurisdiction with the CFTC over the proposed Nasdaq Bitcoin Index Options. In addition, the Exchange acknowledges that it will not be permitted to list and trade the proposed Nasdaq Bitcoin Index Options until the CFTC issues exemptive relief to allow OCC to clear the proposed options in its capacity as a clearing agency registered with the SEC pursuant to Section 17A of the Exchange Act.[44] Finally, the Exchange acknowledges that it will not be permitted to list and trade the proposed Nasdaq Bitcoin Index Options until the OCC receives approval to update The Characteristics and Risks of Standardized Options (the “Options Disclosure Document” or “ODD”) to reflect the risks attendant to trading Nasdaq Bitcoin Index Options.

As proposed, the Nasdaq Bitcoin Index Options would transact on an SEC-regulated exchange, therefore, the SEC's jurisdiction should not be superseded or limited with respect to prosecuting fraud and manipulation relating to the proposed index options which would be transacted on Phlx. If the CFTC grants the Exchange's request for exemptive relief, the CFTC would retain enforcement jurisdiction relating to the sale of the commodity.

Phlx will not list the Nasdaq Bitcoin Index Options until such time as it obtains an exemption from the CFTC such that the Commission has jurisdiction with the CFTC over the Nasdaq Bitcoin Index Options. Further, Phlx shall not list the Nasdaq Bitcoin Index Options until all conditions set forth in any exemptive relief granted by the CFTC have been satisfied. Finally, the Exchange would not list the Nasdaq Bitcoin Index Options until such time as OCC has received approval to update the ODD to reflect the risks attendant to trading Nasdaq Bitcoin Index Options.

Amendments to Exchange Rules

The proposal is designed to ensure that Nasdaq Bitcoin Index Options are listed and traded under the same terms that apply to other index options that are currently traded on the Exchange. The Exchange proposes to create a new Options 4D, titled “Nasdaq Bitcoin Index Options,” with rules that would apply specifically to the listing and trading of Nasdaq Bitcoin Index Options.

Applicability

The proposed Options 4D Rules would be applicable to Nasdaq Bitcoin Index Options. All Options Rules shall apply to Nasdaq Bitcoin Index Options, in addition to the Options 4D Rules, however where the Options 4D Rules disagree with another Options Rule not within Options 4D, a conflict shall be resolved in favor of the Options 4D Rule as it applies to Nasdaq Bitcoin Index Options.[45]

Definitions

The Exchange proposes to define certain terms for the trading of Nasdaq Bitcoin Index Options in proposed Options 4D, Section 2, titled “Definitions.” The Exchange proposes to define “aggregate exercise price,” “CME CF Bitcoin Real Time Index (“BRTI”),” “CME CF Cryptocurrency Reference Rate—New York Variant (“BRRNY”),” “CME CF Cryptocurrency Pricing Products Oversight Committee,” “Constituent Exchange,” “current index value,” “exercise price,” “European-style index option,” “final settlement value,” “index multiplier,” “Nasdaq Bitcoin Index,” “P.M.-settled Index Options,” “reporting authority,” and “underlying.” The proposed definitions are as follows:

The term “aggregate exercise price” shall mean the exercise price of the option contract times the index multiplier.

The term “CME CF Bitcoin Real Time Index (“BRTI”)” shall mean a benchmark index price calculated and published once per 200 milliseconds for Bitcoin that aggregates order data from Bitcoin-USD markets operated by Constituent Exchanges.

The term “CME CF Cryptocurrency Reference Rate—New York Variant (“BRRNY”)” shall mean the once a day benchmark index price for Bitcoin that aggregates trade data from Constituent Exchanges.

The term “CME CF Cryptocurrency Pricing Products Oversight Committee” or “Oversight Committee” shall mean the committee established jointly by Crypto Facilities or “CF” and Chicago Mercantile Exchange Inc. or “CME” to protect the integrity of the methodology and calculation process of the BRTI and the BRRNY and to address potential conflicts of interest. The role of the Oversight Committee is to provide an oversight function to review and provide challenge on all aspects of the methodology and calculation process and provide effective oversight of CF Benchmarks as the administrator of the BRTI and BRRNY.

The term “Constituent Exchange” shall mean the cryptocurrency trading venues approved by the CME CF Cryptocurrency Pricing Products Oversight Committee to serve as pricing source for the calculation of the BRTI and BRRNY.

The term “current index value” shall mean the last derived aggregated value based on the last bids and asks posted in the Bitcoin-USD markets of each Constituent Exchange comprising the BRTI divided by a factor of one hundred (100).

The term “exercise price” shall mean the specific price at which the current index value may be purchased in the case of a call or sold in the case of a put upon the exercise of the option.

The term “European-style index option” shall mean an option on an industry or market index that can be exercised only on the business day of expiration, or, in the case of an option contract expiring on a day that is not a business day, on the last business day prior to the day it expires.

The term “final settlement value” shall be calculated as described at Options 4D, Section 8.

The term “index multiplier” shall mean the amount by which the current index value is to be multiplied to arrive at the value required to be delivered to the holder of a call or by the holder of a put upon valid exercise of the contract. The index multiplier shall be $100.

The term “Nasdaq Bitcoin Index” for purposes of the Options 4D rules shall mean the BRTI divided by a factor of one hundred. The settlement value will be based on the BRRNY divided by a factor of one hundred.

The term “P.M.-settled Index Options” shall mean index options where the last day of trading shall be the business day of expiration, or, in the case of an option contract expiring on a day that is not a business day, on the last business day before its expiration date.

The term “reporting authority” shall mean the institution or reporting service designated by the Exchange as the official source for (1) calculating the level of the index and (2) reporting such level. CF Benchmarks is the “reporting authority” for the BRTI, BRRNY, the CF NQBTC Options Indicative Settlement Value and the CF NQBTC Options Settlement Value as described in Section 7 below.

The term “underlying” shall mean the Nasdaq Bitcoin Index.

Trading Sessions

Proposed Options 4D, Section 3, titled “Trading Sessions,” notes that Nasdaq Bitcoin Index Options may be effected on the Exchange between the hours of 9:30 a.m. (Eastern time) and 4:15 p.m. (Eastern time), except that on the last trading day, transactions in expiring ( printed page 31779) Nasdaq Bitcoin Index Options may be effected on the Exchange between the hours of 9:30 a.m. (Eastern time) and 4:00 p.m. (Eastern time). As is the case for all index options, General 3, Rule 1030 governs the days the Exchange will be open for business.[46] These hours are consistent with trading hours for P.M-Settled index options listed on Phlx pursuant to Options 4A, Section 12(a)(6).

Designation of an Index

Unlike other index options, Nasdaq Bitcoin Index Options need not meet the requirements of Options 4, Section 3 or Options 4A, Section 3.[47] The Exchange designates Nasdaq Bitcoin Index as a narrow based index.

Minimum Increments

As proposed, Nasdaq Bitcoin Index Options would have a minimum increment of $0.01 for all series as long as IBIT Options participate in the Penny Interval Program.[48] Nasdaq Bitcoin Index Options would be quoted and traded in U.S. dollars.[49]

Nasdaq Bitcoin Index Options is a micro-sized benchmark reflecting 1/100th of the BRRNY, designed to provide retail-accessible participation in a major reference asset. Similarly, the Nasdaq-100 Micro Index® (“XND”) options, which reflect 1/100th the value of the Nasdaq-100 Index®, currently trade in $0.01 increments on Phlx. Further, comparable penny treatment exists across the broader index options complex: Cboe Exchange Inc.'s (“Cboe”) Mini-S&P 500 Index (“XSP”) options trade in $0.01 increments, and the Mini-Russell 2000 Index (“MRUT”) options trade in $0.01 increments. The Exchange believes market demand including by retail investors, who generally prefer lower trading increments supports a lower trading increment for Nasdaq Bitcoin Index Options. The Exchange believes that more granular pricing creates narrower bid-ask spreads and increases the possible number of price points available to investors, which also lowers costs to investors. Finer increments also permit more precise pricing in line with the theoretical value of these options and thus more efficient hedging opportunities.

Position and Exercise Limits

The Exchange proposes to state at proposed Options 4D, Section 6(a) that the Nasdaq Bitcoin Index Options shall be subject to a position limit of 24,000 contracts. Today, options on the Cboe Bitcoin U.S. ETF Index (“CBTX”) and the Mini-Cboe Bitcoin U.S. ETF Index (“MBTX”) have position limits of 24,000 contracts. CBTX was trading at 1,775.00 as of April 29, 2026. The notional value of one CBTX options contract was $177,500 (index * $100) as of April 29, 2026. The notional value of one Nasdaq Bitcoin Index Options contract was $76,000 (index * $100) as of April 29, 2026. Therefore, the proposed 24,000 position and exercise limits for Nasdaq Bitcoin Index Options are appropriate because the limits represent less than half of the notional value of CBTX. If a position limit of 24,000 contracts were considered, the equivalent risk would represent 0.12% [50] of the outstanding supply of Bitcoin. This analysis demonstrates that the proposed 24,000 per same side position and exercise limit is appropriate for Nasdaq Bitcoin Index Options.

With respect to aggregation, the Exchange proposes at Options 4D, Section 6(c) that Nasdaq Bitcoin Index Options contracts shall not be aggregated with any other options contracts. Positions in Short Term Option Series, Monthly Options Series, and Quarterly Options Series in Nasdaq Bitcoin Index Options shall be aggregated with other positions in options contracts in Nasdaq Bitcoin Index and shall be subject to the overall position limit. This aggregation is consistent with aggregation for all other index options pursuant to Options 4A, Section 6(e).

Proposed Options 4D, Section 6(c) specifies that the reporting requirements for Nasdaq Bitcoin Index Options shall be those specified in Options 6E, Section 2. Options 6E, Section 2, Reporting of Options Positions, generally requires that each Phlx member and member organization file a report with the Exchange with respect to each account in which the member or member organization has an interest, each account of a partner, officer, director, or employee of such member organization, and each customer account, acting alone, or in concert with others, which has established an aggregate position of 200 or more option contracts (whether long or short) of a put class and call class on the same side of the market covering the same underlying security.

Finally, as noted in proposed Options 4D, Section 6(e), exercise limits for Nasdaq Bitcoin Index Options shall be equivalent to the position limits described in Options 4D, Section 6.

Terms of Index Options Contracts

Pursuant to proposed Options 4D, Section 7(a)(1), bids and offers shall be expressed in terms of dollars and cents per unit of the underlying index which is the Nasdaq Bitcoin Index.

Pursuant to proposed Options 4D, Section 7(a)(2), the Exchange shall determine fixed-point intervals of exercise prices for call and put options.

As proposed in Options 4D, Section 7(a)(3), strike price intervals of no less than $2.50 are generally permitted for Nasdaq Bitcoin Index Options if the strike price is less than $200. This is consistent with how other index options trade on Phlx pursuant to Options 4A, Section 12(a)(3). Further, the Exchange may also determine to list strike prices at $1 or greater, subject to certain conditions. The Exchange may list series at $1 or greater strike price intervals for Nasdaq Bitcoin Index Options and will list at least two strike prices above and two strike prices below the current value of the Nasdaq Bitcoin Index Options [sic] at about the time a series is opened for trading on the Exchange. The Exchange shall list strike prices for Nasdaq Bitcoin Index Options that are within 5 points from the closing value of the Nasdaq Bitcoin Index on the preceding day.[51] This is consistent with how other index options trade on Phlx pursuant to Supplementary Material .02 to Options 4A, Section 12.

Additional series of the same class of Nasdaq Bitcoin Index Options may be opened for trading on the Exchange when deemed necessary to maintain an orderly market, to meet customer demand or when the Nasdaq Bitcoin Index moves substantially from the initial exercise price or prices. To the extent that any additional strike prices are listed by the Exchange, such additional strike prices shall be within thirty percent (30%) above or below the closing value of Nasdaq Bitcoin Index Options.[sic] The Exchange may also open additional strike prices that are more than 30% above or below the current Nasdaq Bitcoin Index value divided by a factor of one hundred (100) provided that demonstrated customer interest exists for such series, as expressed by institutional, corporate or individual customers or their brokers. ( printed page 31780) Market-Makers trading for their own account shall not be considered when determining customer interest under this provision. In addition to the initial listed series, the Exchange may list up to sixty (60) additional series per expiration month for each series in Nasdaq Bitcoin Index Options.[52] This is consistent with how other index options trade on Phlx pursuant to Supplementary Material .03(b) to Options 4A, Section 12.

The Exchange shall not list LEAPS on Nasdaq Bitcoin Index Options at intervals less than $5.[53] This is consistent with how other index options trade on Phlx pursuant to Options 4A, Section 12(c)(1)(A).

With respect to delisting, Nasdaq Bitcoin Index Options added pursuant Options 4D, Section 7(a)(3)(A) and (B) will be reviewed by the Exchange on a monthly basis. The Exchange will review series that are outside a range of five (5) strikes above and five (5) strikes below the current value of the Nasdaq Bitcoin Index and delist series with no open interest in both the put and the call series having a: (i) strike higher than the highest strike price with open interest in the put and/or call series for a given expiration month; and (ii) strike lower than the lowest strike price with open interest in the put and/or call series for a given expiration month.[54] This is consistent with how other index options trade on Phlx pursuant to Supplementary Material .02(d) to Options 4A, Section 12.

Notwithstanding this delisting policy, customer requests to add strikes and/or maintain strikes in Nasdaq Bitcoin Index Options series eligible for delisting shall be granted.[55] If the Exchange identifies series for delisting, the Exchange shall notify other options exchanges with similar delisting policies regarding eligible series for delisting, and shall work with such other exchanges to develop a uniform list of series to be delisted, so as to ensure uniform series delisting of multiply listed Nasdaq Bitcoin Index Options.[56] This is consistent with how other index options trade on Phlx pursuant to Options 4A, Section 12(g)(2).

Notwithstanding any other provision regarding strike prices in Options 4D, Section 6, non-Short Term Options that are on Nasdaq Bitcoin Index Options that have been selected to participate in the Short Term Option Series Program (referred to as a “Related non-Short Term Option series”) shall be opened during the month prior to expiration of such Related non-Short Term Option series in the same manner as permitted in Supplementary .01 of Options 4D, Section 7 and in the same strike price intervals that are permitted in Supplementary .01 of Options 4D, Section 7.[57] This is consistent with how other index options trade on Phlx pursuant to Options 4A, Section 12(a)(3)(A).

The Exchange proposes to state that Nasdaq Bitcoin Index Options contracts may expire at three (3) month intervals, in consecutive weeks or in consecutive months. The Exchange may list: (i) up to six (6) standard monthly expirations at any one time in a class of Nasdaq Bitcoin Index Options, but will not list Nasdaq Bitcoin Index Options that expire more than twelve (12) months out.[58] This is consistent with how other index options trade on Phlx pursuant to Options 4A, Section 12(a)(4).

Nasdaq Bitcoin Index Options would be European-style index options [59] and P.M.-settled.[60]

The Exchange believes that market participants, and in particular, retail investors, prefer P.M.-settled index options. P.M.-settlement is preferred by retail investors as it allows market participants to hedge their exposure for the full week. A.M.-settled options by contrast are based on opening prices on the day of expiration and therefore stop trading on the day prior, leaving residual risk on the day of expiration. P.M.-settlement is needed to garner retail investor support for this product.

After a particular class of Nasdaq Bitcoin Index Options has been approved for listing and trading on the Exchange, the Exchange shall from time to time open for trading series of options therein. Within each approved class of Nasdaq Bitcoin Index Options, the Exchange shall open for trading a minimum of one expiration month and series and may also open for trading series of options having not less than twelve and up to 60 months to expiration (“Long-Term Index Options Series”).[61]

Prior to the opening of trading in any series of Nasdaq Bitcoin Index Options, the Exchange shall fix the expiration month and exercise price of option contracts included in each such series.[62]

Additional series of Nasdaq Bitcoin Index Options of the same class may be opened for trading on the Exchange when the Exchange deems it necessary to maintain an orderly market, to meet customer demand or when the market price of the Nasdaq Bitcoin Index moves more than five strike prices from the initial exercise price or prices. The opening of a new series of options shall not affect the series of options of the same class previously opened. New series of Nasdaq Bitcoin Index Options may be added until the beginning of the month, in which the options contract will expire. Due to unusual market conditions, the Exchange, in its discretion, may add a new series of Nasdaq Bitcoin Index Options until the fourth business day prior to the business day of expiration, or, in the case of Nasdaq Bitcoin Index Options contract [sic] expiring on a day that is not a business day, up to the fifth business day prior to expiration.[63] This is consistent with how other index options trade on Phlx pursuant to Options 4A, Section 12.

The Exchange would also list Long-Term Option Series or “LEAPs” on Nasdaq Bitcoin Index Options. Similar to index options at Options 4A, Section 12(b)(2), the Exchange proposes that it may list LEAPs on Nasdaq Bitcoin Index Options that expire from twelve (12) to sixty (60) months from the date of issuance. There may be up to ten (10) expiration months, none further out than sixty (60) months. Strike price intervals and continuity Rules shall not apply to such options series until the time to expiration is less than twelve (12) months. Bid/ask differentials for LEAPs are specified within Options 2, Section 4(b)(4)(i)(A).[64] Also similar to index options at Options 4A, Section 12(b)(1), when new Nasdaq Bitcoin Index Options LEAPs are listed, such series would be opened for trading either when there is buying or selling interest, or forty (40) minutes prior to the close, whichever occurs first. No quotations would be posted for such options series until they are opened for trading.[65] This is consistent with how other index options trade on Phlx.

Similar to index options at Options 4A, Section 12(d), the reported level of the Nasdaq Bitcoin Index is calculated by the reporting authority, CF Benchmarks. The BRTI Index divided by a factor of one hundred (100) will be disseminated by CF Benchmarks throughout the trading day as the CF NQBTC Options Indicative Settlement ( printed page 31781) Value. The BRRNY Index divided by a factor of one hundred (100) will be disseminated by CF Benchmarks each day as the CF NQBTC Options Settlement Value.[66]

The Exchange proposes to note in Supplementary .01 to Options 4D, Section 7 that the Short Term Options Series Program listing rules at Options 4A, Section 12(b)(4) shall be applicable to Nasdaq Bitcoin Index Options. The Monthly Options Series Program at Options 4A, Section 12(b)(5) shall be applicable to Nasdaq Bitcoin Index Options. Finally, the Quarterly Options Series Program at Options 4A, Section 12(b)(3) shall be applicable to Nasdaq Bitcoin Index Options.

The Exchange proposes to describe the final settlement value of Nasdaq Bitcoin Index Options in proposed Options 4D, Section 8. Nasdaq Bitcoin Index Options would be settled in U.S. dollars on the business day following expiration. Cash settlement would be equal to the difference between the final settlement value and the strike price of the contract multiplied by an index multiplier of $100.[67]

The Nasdaq Bitcoin Index Options final settlement value would be the BRRNY on the expiration date (usually a Friday). BRRNY is calculated based on the Relevant Transactions. BRRNY will be divided by a factor of one hundred (100) and published as CF NQBTC Options Settlement Value. BRRNY is calculated daily based on the Relevant Transactions and is calculated on the expiration date for purposes of final settlement. Relevant Transactions include those that trade Bitcoin versus U.S. Dollars on a Constituent Exchange that occur from 15:00 to 16:00 New York Time that is calculated and reported by the reporting authority. The final settlement value is determined by the aggregated last reported sale price of each Constituent Exchange. Specifically, the final settlement is calculated by combining all Relevant Transactions from each Constituent Exchange on a joint list and recording the trade price and size for each transaction. That list is partitioned into a number of equally-sized time intervals, of 5 minutes. For each partition separately, the volume-weighted median trade price is calculated from the trade prices and sizes of all Relevant Transactions across all Constituent Exchanges. The BRRNY is the equally weighted average of the volume-weighted medians of all partitions. In the event that the underlying BRTI is not open for trading on the expiration date, the value of the Nasdaq Bitcoin Index shall be the last reported sale price prior to the expiration date.[68] The Exchange notes that a 1/100th version of the BRTI would be disseminated intra-day as the CF NQBTC Options Indicative Settlement Value.

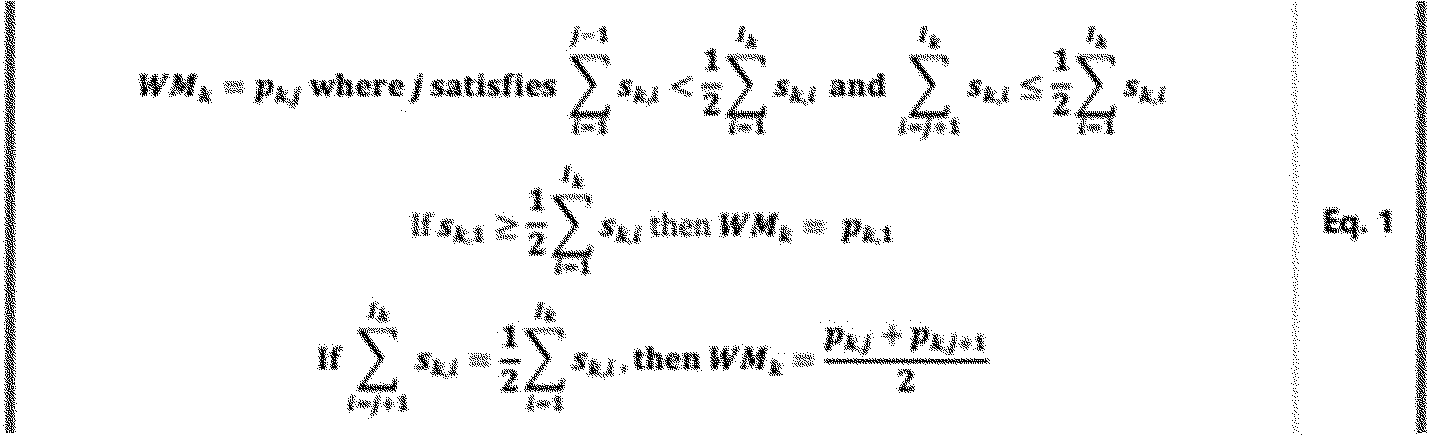

Settlement is calculated by combining all Relevant Transactions on a joint list and recording the trade price and size for each transaction. That list is partitioned into a number of equally-sized time intervals, of 5 minutes. For each partition [69] separately, the volume-weighted median [70] trade price is calculated from the trade prices and sizes of all Relevant Transactions, i.e., across all Constituent Exchanges.[71] A volume-weighted median differs from a standard median in that a weighting factor, in this case trade size, is factored into the calculation.[72] For each partition k, the volume-weighted median trade prices WM across all Relevant Transactions is calculated as:

The BRRNY is then given by the equally weighted average of the volume-weighted medians of all partitions.[73] The CME CF Cryptocurrency Reference Rate as of the effective time T, CCRR, is then given by:

Delayed data and missing data are subject to certain rules. Any Relevant Transaction for a given Calculation Day that is not available from a Constituent Exchange's API by the Retrieval Time is disregarded in the calculation of the ( printed page 31782) CME CF Cryptocurrency Reference Rate for that Calculation Day. If no Relevant Transaction occurs on a Constituent Exchange on a given Calculation Day or one or more Relevant Transactions occur but for any reason cannot be retrieved by the Calculation Agent, the Constituent Exchange is disregarded in the calculation of the CME CF Cryptocurrency Reference Rate for that Calculation Day. If, for any of the K partitions of the TWAP Period in the above Eq. 2, no Relevant Transaction occurs on any Constituent Exchange or one or more Relevant Transactions occur but for any reason cannot be retrieved by the Calculation Agent, the partition remains empty and will be disregarded in the calculation of the CME CF Cryptocurrency Reference Rate for that Calculation Day. The denominator in Eq. 2 above will then be decremented by the number of empty partitions. If one or more Relevant Transactions occur but for any reason no Relevant Transaction can be retrieved from any Constituent Exchange API by the Calculation Agent, a CME CF Cryptocurrency Reference Rate calculation failure occurs for that Calculation Day. All Relevant Transactions retrieved by CF Benchmarks for a given calculation day are subject to an automated screening for erroneous data.[74]

Similar to other index options,[75] neither the Exchange, nor any agent of the Exchange would have any liability for damages, claims, losses or expenses caused by any errors, omissions, or delays in calculating or disseminating the current settlement value or the final settlement value resulting from an act, condition, or cause beyond the reasonable control of the Exchange including but not limited to, an act of God; fire; flood; extraordinary weather conditions; war; insurrection; riot; strike; accident; action of government; communications or power failure; equipment or software malfunction; any error, omission, or delay in the reports of transactions in one or more underlying transactions in the BRRNY or any error, omission or delay in the reports of the current settlement value or the closing settlement value by the Exchange.[76] The Exchange shall post the final settlement value CF NQBTC Options Settlement Value” on its website or disseminate it through one or more major market data vendors.[77]

Today, Phlx limits its liability at Options 4A, Section 19. The Exchange proposes to expand this limitation of the Exchange's liability in connection with its administration of Phlx proprietary indices that currently exists for other indexes [78] to the Nasdaq Bitcoin Index Options. The Exchange currently lists and trades options on a number of proprietary indices, and new indices continue to be developed from time to time. There is a great deal of work involved in the daily calculation and dissemination of these indices. While much of such work is automated, manual input is still required. Thus, the potential for human error exists which exposes the Exchange to a risk of liability. Potential human errors include inputting a symbol or index value incorrectly. The Exchange's proposal promotes equitable principles of trade, and protects investors and the public interest, by defining the scope of the Exchange's liability, thereby putting investors on notice that the Exchange is not liable for negligent conduct in connection with its administration of the Nasdaq Bitcoin Index Options.

The Exchange proposes to adopt “Disclaimers” at proposed Options 4D, Section 9. As noted herein, CF Benchmarks shall be the reporting authority for Nasdaq Bitcoin Index Options.[79] Other options markets provide similar disclaimers for the reporting authority.[80] Each index has a designated Reporting Authority, which is the institution or reporting service designated by the Exchange as the official source for routinely calculating the level of each respective index. The Exchange believes that a disclaimer for a Reporting Authority promotes just and equitable principles of trade by encouraging the Reporting Authority for each index to develop and maintain indexes that may qualify for options trading on the Exchange, thereby providing investors with new investment opportunities.

The Exchange proposes to provide at proposed Options 4D, Section 9(a) that the disclaimers in paragraph (b) of Options 4D, Section 9 shall apply to the reporting authority, CF Benchmarks, as identified in Options 4D, Section 2(a)(13).

Further, proposed Options 4D, Section (b) provides that neither CF Benchmarks nor any of its affiliates make any warranty, express or implied, as to the results to be obtained by any person or entity from the use of an index it publishes, any opening, intra-day or closing value therefor, or any data included therein or relating thereto, in connection with the trading of any options contract based thereon or for any other purpose. CF Benchmarks shall obtain information for inclusion in, or for use in the calculation of, such index from sources it believes to be reliable, but CF Benchmarks does not guarantee the accuracy or completeness of such index, any opening, intra-day or closing value therefor, or any data included therein or relating thereto. CF Benchmarks hereby disclaims all warranties of merchantability or fitness for a particular purpose or use with respect to such index, any opening, intra-day, or closing value therefor, any data included therein or relating thereto, or any options contract based thereon. CF Benchmarks shall have no liability for any damages, claims, losses (including any indirect or consequential losses), expenses, or delays, whether direct or indirect, foreseen or unforeseen, suffered by any person arising out of any circumstance or occurrence relating to the person's use of such index, any opening, intra-day or closing value therefor, any data included therein or relating thereto, or any options contract based thereon, or arising out of any errors or delays in calculating or disseminating such index.

Margin

The Exchange proposes to apply margin requirements for the purchase and sale of Nasdaq Bitcoin Index Options that are identical to those applied for its narrow-based index options. Therefore, purchases of puts or calls with 9 months or less until expiration must be paid for in full. Writers of uncovered puts or calls must deposit/maintain 100% of the option proceeds plus 20% of the underlying index value less out-of-the-money amount, if any, to a minimum of option proceeds plus 10% of underlying index value for calls; 10% of the put exercise price for puts. Proposed Options 4D, Section 10, titled “Margin,” shall provide that the margin requirements for Nasdaq Bitcoin Index Options shall be the margin requirements set forth in Cboe Rule 10.3 for narrow-based index options.[81]

( printed page 31783)Regulatory Rules

The trading of Nasdaq Bitcoin Index Options would be subject to the same rules that presently govern the trading of index options on Phlx, including sales practice rules and trading rules. Options 10, Section 6, “Opening of Accounts,” is designed to protect public customer trading and shall apply to trading in Nasdaq Bitcoin Index Options. Specifically, Options 10, Section 6(a) prohibits members and member organizations from accepting a customer order to purchase or write an option, including Nasdaq Bitcoin Index Options, unless such customer's account has been approved in writing by an Options Principal. Additionally, Phlx Options 10, Section 8, “Suitability of Recommendations,” is designed to ensure that options, including Nasdaq Bitcoin Index Options, are only sold to customers capable of evaluating and bearing the risks associated with trading in this instrument. Further, Phlx Options 10, Section 9, “Discretionary Accounts,” permits members and member organizations to exercise discretionary power with respect to trading options, including Nasdaq Bitcoin Index Options, in a customer's account only if the customer has given prior written authorization and the account has been accepted in writing by a Registered Options Principal. Phlx Options 10, Section 9 also requires a record to be made of every option transaction for an account in respect to which a member or member organization or a partner, officer or employee of a member organization is vested with any discretionary authority, such record to include the name of the customer, the designation, number of contracts and premium of the option contracts, the date and time when such transaction took place and clearly reflecting the fact that discretionary authority was exercised. Finally, Phlx Options 10, Section 7, “Supervision of Accounts,” Phlx Options 10, Section 10, “Confirmations to Customers,” and Phlx Options 10, Section 13, “Delivery of Options Disclosure Documents and Prospectus,” will also apply to trading in Nasdaq Bitcoin Index Options.

The trading of Nasdaq Bitcoin Index Options will be subject to the trading halt procedures applicable to other index options traded on the Exchange.[82]

The Exchange believes that all Phlx and OCC members will be able to accommodate trading, clearance and settlement of Nasdaq Bitcoin Index Options because these index options will trade similar to all other index options.

Surveillance

In 2024, the Commission approved various rule changes to list and trade Spot Bitcoin ETPs.[83] The Commission noted in the Spot Bitcoin ETPs Approval Order that, “. . . one way an exchange that lists Bitcoin-based ETF can meet the obligation under Exchange Act Section 6(b)(5) that its rules be designed to prevent fraudulent and manipulative acts and practices is by demonstrating that the exchange has a comprehensive surveillance-sharing agreement with a regulated market of significant size related to the underlying or reference Bitcoin assets. Such an agreement would assist in detecting and deterring fraud and manipulation related to that underlying asset.” The Commission has recognized that the “regulated market of significant size” standard is not the only means for satisfying Section 6(b)(5) of the Act, specifically providing that a listing exchange could demonstrate that “other means to prevent fraudulent and manipulative acts and practices” are sufficient to justify dispensing with the requisite surveillance-sharing agreement.[84] For example, in approving the Spot Bitcoin ETPs, the Commission found that there were “sufficient `other means' of preventing fraud and manipulation,” including that:

[B]ased on the record before the Commission and the improved quality of the correlation analysis in the record, including the Commission's own analysis, the Commission is able to conclude that fraud or manipulation that impacts prices in spot Bitcoin markets would likely similarly impact CME Bitcoin futures prices. And because the CME's surveillance can assist in detecting those impacts on CME Bitcoin futures prices, the Exchanges' comprehensive surveillance-sharing agreement with the CME—a U.S. regulated market whose Bitcoin futures market is consistently highly correlated to spot Bitcoin, albeit not of “significant size” related to spot Bitcoin—can be reasonably expected to assist in surveilling for fraudulent and manipulative acts and practices in the specific context of the [Spot Bitcoin ETPs].[85]

As described in the Spot Bitcoin ETPs Approval Order, there is currently a regulated U.S. market with respect to spot Bitcoin, the CME Bitcoin futures (“Bitcoin Futures”) market.[86] In its Spot Bitcoin ETPs Approval Order, the Commission found there was a high price correlation between the underlying and the futures market.[87] The proposed Nasdaq Bitcoin Index Options and the various Spot Bitcoin ETPs reference the same underlying market for spot Bitcoin that trade on spot Bitcoin trading platforms.

Specifically, the Exchange has a comprehensive surveillance-sharing agreement with the CME via its common membership in ISG, which facilitates the sharing of information that is available to the CME through its surveillance of its markets, including its surveillance of the Bitcoin Futures market. Similar to the Spot Bitcoin ETPs previously approved by the SEC, Phlx's ability to obtain information regarding trading in the Bitcoin Futures market from other markets that are members of the ISG (specifically the CME) would assist Phlx in detecting and deterring misconduct.

Further, the exchanges that list Spot Bitcoin ETPs comprehensively surveil market conditions and price movements on a real time and ongoing basis in order to detect and prevent price distortions, including price distortions caused by manipulative efforts. Thus, the CME's surveillance as well as Phlx's surveillance and other equity markets that list Spot Bitcoin ETPs can reasonably be relied upon to capture the effects on the Bitcoin Futures market and Spot Bitcoin ETPs, as applicable, that are caused by a person attempting to manipulate the futures ETP or Spot Bitcoin ETPs by manipulating the price of Bitcoin futures contracts or Spot Bitcoin ETPs, whether that attempt is made by directly trading on the Bitcoin Futures market or Spot Bitcoin ETPs, or indirectly by trading outside of the Bitcoin Futures market or Spot Bitcoin ETPs. Both the Exchange and the equity markets that list and trade Spot Bitcoin ETPs are member of ISG which will facilitate the sharing of information among the Exchange and the equity ( printed page 31784) exchanges with respect to Spot Bitcoin ETPs.

The Exchange would have an adequate surveillance program in place for Nasdaq Bitcoin Index Options as it intends to apply the same program procedures that apply to the Exchange's other index options products.[88] Index products are integrated into the Exchange's existing surveillance system architecture and are thus subject to the relevant surveillance processes. This is true for both surveillance system processing and manual processes that support the Phlx's surveillance program. Additionally, the Exchange is also a member of the ISG under the Intermarket Surveillance Group Agreement. ISG members work together to coordinate surveillance and investigative information sharing in the stock futures and options markets. Both the Exchange and CME are members of ISG.[89]

The Exchange, in its normal course of surveillance, will monitor for any potential manipulation of the Nasdaq Bitcoin Index Options settlement value according to the Exchange's current procedures. The Exchange believes that its surveillance procedures currently in place will allow it to adequately surveil for any potential manipulation in the trading of Nasdaq Bitcoin Index Options.

Capacity

The Exchange represents that it has the necessary system capacity to support additional quotations and messages that will result from the listing and trading Nasdaq Bitcoin Index Options. Finally, the Options Price Reporting Authority (“OPRA”) has the necessary systems capacity to handle the additional traffic associated with the listing of Nasdaq Bitcoin Index Options. The proposal is limited to one new class and the additional traffic that would be generated from the introduction of Nasdaq Bitcoin Index Options would be manageable and well within any systems capacity capabilities.

2. Statutory Basis

The Exchange believes that its proposal is consistent with Section 6(b) of the Act,[90] in general, and furthers the objectives of Section 6(b)(5) of the Act,[91] in particular, in that it will permit trading in Nasdaq Bitcoin Index Options pursuant to rules designed to prevent fraudulent and manipulative acts and practices and promote just and equitable principles of trade. In particular, the Exchange believes the proposed rule change will further the Exchange's goal of introducing new and innovative products to the marketplace. The Exchange believes that listing Nasdaq Bitcoin Index Options will provide an opportunity for investors to hedge, or speculate on, the market risk associated with trading Bitcoin. This proposal offers market participants with choice of product structures for Bitcoin exposure and offers a flexible way to gain exposure to Bitcoin through transparent, regulated index options.

Since January 2024, Spot Commodity ETF shares based on Bitcoin have been listed and traded on national securities exchanges.[92] Phlx's proposal to list and trade Nasdaq Bitcoin Index Options would allow market participants that hold spot Bitcoin-based ETFs to hedge or modify their exposure on a national securities exchange, within a single regulatory regime,[93] thereby fostering innovation and competition in the rapidly evolving market for digital asset derivatives.

Section 2(a)(1)(A) of the Commodity Exchange Act (the “CEA”) [94] provides the Commodity Futures Trading Commission (the “CFTC”) with exclusive jurisdiction over, among other things, options on commodities traded on a designated contract market, swap execution facility, or other board of trade, exchange, or market. The Exchange believes that the proposed Nasdaq Bitcoin Index Options should be permitted to trade on a national securities exchange provided the Exchange requests and obtains exemptive relief from the CFTC that would: (1) provide the Exchange with exemption from any applicable requirements of the CEA and the CFTC and regulations, including the requirements applicable to a Designated Contract Market under Section 5 of the CEA [95] and Part 38 [96] of the CFTC's regulations; and (2) provide the Commission, with the CFTC, with jurisdiction over the proposed Nasdaq Bitcoin Index Options; and (3) provide exemptive relief to allow the proposed Nasdaq Bitcoin Index Options to clear through The Options Clearing Corporation (“OCC”) in its capacity as a clearing agency registered with the SEC pursuant to Section 17A of the Act.[97]

The Exchange acknowledges that it will not be permitted to list and trade the proposed Nasdaq Bitcoin Index Options unless and until the CFTC grants all necessary exemptive relief [98] from the requirements of the CEA and the rules and regulations thereunder, with the condition that the SEC exercise jurisdiction with the CFTC over the proposed Nasdaq Bitcoin Index Options. In addition, the Exchange acknowledges that it will not be permitted to list and trade the proposed Nasdaq Bitcoin Index options until the CFTC issues exemptive relief to allow OCC to clear the proposed options in its capacity as a clearing agency registered with the SEC pursuant to Section 17A of the Exchange Act.[99] Finally, the Exchange acknowledges that it will not be permitted to list and trade the proposed Nasdaq Bitcoin Index Options until the OCC receives approval to update The Characteristics and Risks of Standardized Options (the “Options Disclosure Document” or “ODD”) to reflect the risks attendant to trading Nasdaq Bitcoin Index Options.

As proposed, the Nasdaq Bitcoin Index Options would transact on an SEC-regulated exchange, therefore, the SEC's jurisdiction should not be superseded or limited with respect to prosecuting fraud and manipulation relating to the proposed index options which would be transacted on Phlx. If the CFTC grants the Exchange's request for exemptive relief, the CFTC would retain enforcement jurisdiction relating to the sale of the commodity.

Phlx will not list the Nasdaq Bitcoin Index Options until such time as it obtains an exemption from the CFTC such that the Commission has jurisdiction with the CFTC over the Nasdaq Bitcoin Index Options. Further, Phlx shall not list the Nasdaq Bitcoin Index Options until all conditions set forth in any exemptive relief granted by the CFTC have been satisfied. Finally, the Exchange would not list the Nasdaq Bitcoin Index Options until such time as OCC has received approval to update ( printed page 31785) the ODD to reflect the risks attendant to trading Nasdaq Bitcoin Index Options.

In light of evolving market structures in digital asset developing markets, Phlx's proposal will foster responsible innovation and competition, while ensuring that appropriate regulatory protections are in place. The proposed Nasdaq Bitcoin Index Options are in the public interest and promote responsible innovation and fair competition.

The Exchange believes that with the commencement of trading of Bitcoin as an ETF on a national securities exchange, Phlx's proposal would serve important economic functions by providing investors, speculators and multinational corporations with an important risk-shifting mechanism by allowing them to hedge the price of Bitcoin. Phlx's proposal is an innovative response to the demands of various market participants who require greater flexibility to tailor their Bitcoin positions and portfolios to satisfy their investment objectives by creating a “precise” hedge for approved Spot Bitcoin ETPs.