Securities and Exchange Commission

- [Release No. 34-105596; File No. 4-631]

I. Introduction

On May 27, 2026, Nasdaq, Inc., on behalf of Nasdaq Texas LLC (“NDTX”), Nasdaq PHLX LLC (“PHLX”), and The Nasdaq Stock Market LLC (“Nasdaq”), and the following parties to the Plan to Address Extraordinary Market Volatility (“Plan”) Pursuant to Rule 608 of Regulation NMS under the Securities Exchange Act of 1934 (“Act” or “Exchange Act”) [1] : 24X National ( printed page 33775) Exchange LLC, Cboe BZX Exchange, Inc., Cboe BYX Exchange, Inc., Cboe EDGA Exchange, Inc., Cboe EDGX Exchange, Inc., Financial Industry Regulatory Authority, Inc., Investors Exchange LLC, Long-Term Stock Exchange, Inc., MEMX LLC, MIAX PEARL, LLC, New York Stock Exchange LLC, NYSE American LLC, NYSE Arca, Inc., NYSE Texas, Inc., and NYSE National, Inc., (collectively with NDTX, PHLX, and Nasdaq, “Participants”), filed with the Securities and Exchange Commission (“Commission”) pursuant to Section 11A(a)(3) of the Exchange Act [2] and Rule 608 thereunder,[3] a proposal to amend the Plan (“Twenty-Seventh Amendment”).[4] The proposal reflects changes unanimously approved by the Participants. The Twenty-Seventh Amendment proposes to amend the Plan to establish temporary price band protections to overnight trading (“Overnight Protections”) in anticipation of overnight trading by certain national securities exchanges. The Commission is publishing this notice to solicit comments from interested persons on the Twenty-Seventh Amendment.[5]

II. Description of the Plan

Set forth in this Section II is the statement of the purpose and summary of the Twenty-Seventh Amendment, along with the information required by Rule 608(a)(4) and (5) under the Exchange Act,[6] prepared and submitted by the Participants to the Commission.[7]

A. Statement of Purpose and Summary of the Plan Amendment

The Participants filed the Plan with the Commission on April 5, 2011, to create a market-wide limit up-limit down mechanism intended to address extraordinary market volatility in NMS Stocks, as defined in Rule 600(b)(65) of Regulation NMS under the Exchange Act.[8] The Plan sets forth procedures that provide for market-wide limit up-limit down requirements to prevent trades in individual NMS Stocks from occurring outside of the specified Price Bands.[9] These limit up-limit down requirements are coupled with Trading Pauses, as defined in Section I(Y) of the Plan, to accommodate more fundamental price moves. In particular, the Participants adopted this Plan to address extraordinary volatility in the securities markets, i.e., significant fluctuations in individual securities' prices over a short period of time, such as those experienced during the “Flash Crash” on the afternoon of May 6, 2010.

As set forth in more detail in the Plan, all trading centers in NMS Stocks, including both those operated by Participants and those operated by members of Participants, are required to establish, maintain, and enforce written policies and procedures that are reasonably designed to comply with the Limit Up-Limit Down requirements specified in the Plan. The Participants believe that the Limit Up-Limit Down mechanism specified in the Plan has reduced the negative impacts of sudden, unanticipated price movements in NMS Stocks (and erroneous trades in such stocks), thereby protecting investors and promoting a fair and orderly market.[10]

The Participants propose a cautious approach to extending protections to the unique conditions presented by overnight markets. The proposal is to be implemented in two phases. In the first phase, the Participants propose to apply protections based on those currently used by certain ATSs to constrain significant fluctuations in individual securities' prices over a short period of time. The Participants believe that these protections are narrowly tailored to current market conditions, and will promote market stability over an interim period.

During implementation of this first phase, Participants will gather and analyze information concerning overnight trading, and will use that information to develop recommendations for a final proposal to be implemented in the overnight session. The final proposal will be submitted to the Commission as a plan amendment that will remove the interim measures and replace them with revised overnight protections.

1. Authority To Amend Under Rule 608 of Regulation NMS

The Participants respectfully submit this amendment to the Plan pursuant to Rule 608 of Regulation NMS under the Exchange Act, which authorizes the Participants to act jointly in preparing, filing, and implementing national market system plans. Rule 608(a)(3) specifically provides that any two or more self-regulatory organizations, acting jointly, may file a national market system plan or any amendment thereto with the Commission. The Participants are self-regulatory organizations that are parties to the Plan and have the authority under Rule 608 to propose amendments to the Plan for Commission approval.

Section III(A) of the Plan provides that, except with respect to the addition of new Participants to the Plan, any proposed change in, addition to, or deletion from the Plan shall be effected by means of a written amendment to the Plan that: (1) sets forth the change, addition, or deletion; (2) is executed on behalf of each Participant; and (3) is approved by the SEC pursuant to Rule 608 of Regulation NMS under the Exchange Act, or otherwise becomes effective under Rule 608 of Regulation NMS under the Exchange Act.

Each of the Participants has approved this Twenty-Seventh Amendment in accordance with Section III(C) of the Plan. The Participants also received and incorporated feedback from the Plan Advisory Committee in preparing this proposal.

The Participants believe that this amendment is consistent with Section 11A of the Exchange Act and Rule 608 thereunder. Rule 608 provides that the Commission shall approve a proposed NMS plan, or proposed amendment thereto, if it finds that such plan or amendment is necessary or appropriate in the public interest, for the protection of investors, or otherwise in furtherance of the purposes of the Act; and such ( printed page 33776) plan provides that all brokers and dealers may obtain access to transaction reports and quotations on terms that are not unreasonably discriminatory.[11] Section 11A of the Act establishes the Congressional finding that it is in the public interest and appropriate for the protection of investors and the maintenance of fair and orderly markets to assure economically efficient execution of securities transactions, fair competition among brokers and dealers and exchange markets, and the availability to brokers, dealers, and investors of information with respect to quotations for and transactions in securities.[12] Consistent with these standards, the proposed amendment would enhance the stability and integrity of the national market system by implementing price band protections during overnight trading sessions, thereby reducing the risk of extraordinary volatility and erroneous trades during periods of reduced liquidity.

2. Summary of Proposed Amendment

The Participants propose to add a new Section VIII to the Plan, entitled “Overnight Protections,” which establishes a framework for calculating and disseminating Overnight Price Bands for use during Overnight Protected Hours (defined as 9:00 p.m. Eastern Time on Sunday through Thursday to 4:00 a.m. Eastern Time on the next calendar day), and requires all trading centers that are operative during such hours to establish, maintain, and enforce written policies and procedures that are reasonably designed to prevent trades outside of such Overnight Price Bands. In Phase 2 of the proposal, Participants intend to replace the interim Section VIII proposed in this amendment with a more permanent Section VIII to govern overnight trading protections, and expect these protections to more closely resemble the LULD program in place during Regular Trading Hours, for instance by including sliding bands.

The proposed amendment for Phase 1 includes the following key aspects:

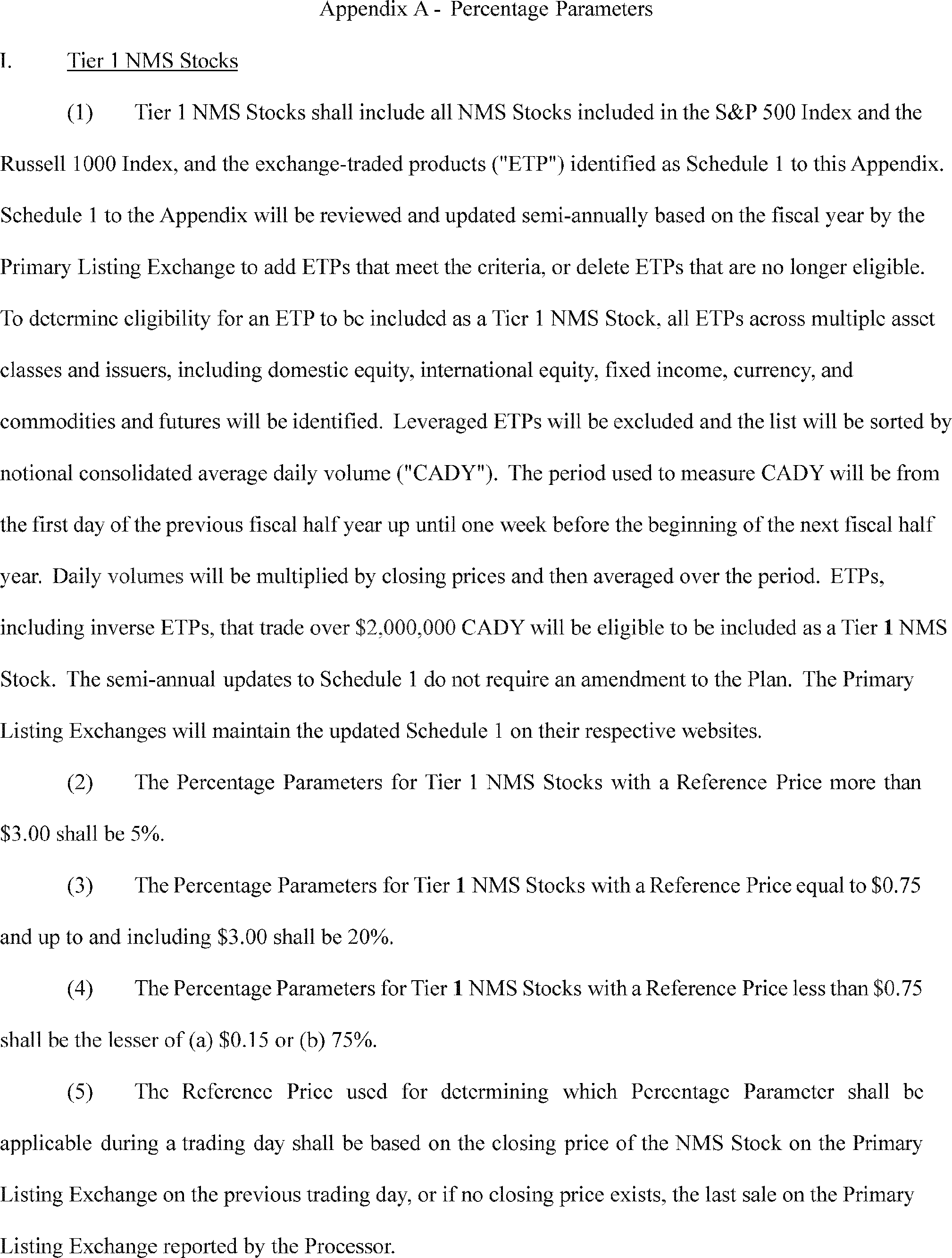

(a) Overnight Price Bands. The Primary Listing Exchange for each NMS Stock shall calculate and disseminate to the Processors an Overnight Lower Price Band and an Overnight Upper Price Band to be applied during Overnight Protected Hours for NMS Stocks. The Overnight Price Bands shall be based on two reference prices as adjusted for any relevant corporate actions, (i) the official closing price of a stock as reported by the listing market for such NMS stock and (ii) the consolidated last round lot sale as of 7:45 p.m. Eastern Time, with the Overnight Lower Price Band being 20% lower than the lower of the reference prices, and the Overnight Upper Price Band being 20% greater than the greater of the reference prices; the Overnight Percentage Parameter for a leveraged ETP shall be 20%, multiplied by the leverage ratio. For NMS Stocks with a Closing Price of less than $1.00, the minimum Overnight Upper Price Band and minimum Overnight Lower Price Band thresholds shall each be $1.00 from the applicable reference price; for NMS Stocks with a Closing Price of $1.00 or more, the minimum Overnight Upper Price Band and minimum Overnight Lower Price Band thresholds shall each be $3.00 from the applicable reference price. The Minimum Price Band for a leveraged ETP shall be multiplied by the leverage ratio of such product.

(b) Primary Listing Exchanges shall transmit the calculated Overnight Price Bands to the Processors no later than 8:55 p.m. Eastern Time, and the Processors shall disseminate such bands to the public prior to 9:00 p.m. Eastern Time.

(c) All trading centers in NMS Stocks that are operative during Overnight Protected Hours, must establish, maintain, and enforce written policies and procedures that are reasonably designed to prevent both trades and the display of prices outside the Overnight Price Bands during Overnight Protected Hours.

(d) The Primary Listing Exchange of a stock may declare a Regulatory Halt in accordance with Primary Listing Exchange rules, and, if so, shall notify the Processor.[13] During a Regulatory Halt during Overnight Protected Hours, Participants shall reject orders. Any NMS Stock subject to a Regulatory Halt during Overnight Protected Hours shall not reopen during Overnight Protected Hours.

(e) The proposed amendment also amends Section IV of the Plan to require that trading center policies and procedures comply with the overnight requirements specified in the new Section VIII.[14]

Overnight Protected Hours

The Participants have determined to implement overnight protections between the hours of 9:00 p.m. and 4:00 a.m. Eastern Time. The 9:00 p.m. Eastern Time commencement of the Overnight Protected Hours corresponds to the time at which the Processors will open for overnight trading, thereby ensuring that the limit up-limit down mechanism is operative from the moment overnight trading activity becomes available through the consolidated market data infrastructure. The 4:00 a.m. Eastern Time conclusion of the Overnight Protected Hours was selected to accommodate the well-established practice of issuers releasing earnings announcements, material corporate disclosures, and other price-sensitive information during pre-market hours in advance of the Regular Trading Session. By terminating Overnight Protected Hours at 4:00 a.m. Eastern Time, the Participants intend for market participants to be able to incorporate newly disclosed information into securities prices without the constraints of pricing bands based on the prior day's activity.

The Participants acknowledge that the application of price bands during Overnight Protected Hours has the potential to inhibit price discovery to some degree, insofar as the bands may constrain the range of prices at which transactions can occur during those hours. However, the Participants believe that this risk does not outweigh the significant investor protections afforded by the proposed amendment. In particular, the Participants' analysis [15] indicates that only a minority of NMS stocks would be materially impacted by the presence of price bands during Overnight Protected Hours, suggesting that the constraining effect on price discovery would be limited in scope and would not broadly impair the market's ability to reflect fundamental value. Moreover, to the extent that the price band mechanism may in certain instances restrain price movement during the overnight session, the Participants believe that this trade-off is justified by the protections that the amendment provides against erroneous trades and aberrant executions in a low-liquidity trading environment—protections that serve the interests of investors and the integrity of the national market system. Finally, in a circumstance in which orders are consistently being placed outside the bands or the price bands are otherwise limiting price discovery, Primary Listing ( printed page 33777) Exchanges will be able to declare a Regulatory Halt [16] to suspend trading for the remainder of the overnight session, allowing the market to resume price discovery in the more liquid environment following the end of Overnight Protected Hours.

This calibration of the Overnight Protected Hours appropriately balances the Plan's dual objectives of preventing extraordinary volatility and facilitating price discovery: during the overnight session, when liquidity is reduced and the risk of erroneous trades or transitory gaps in liquidity is heightened, the price band mechanism will prevent trades at prices far removed from a security's recent fundamental value, thereby protecting investors who might otherwise execute transactions at aberrant prices. This is in contrast to the pre-market session, when fundamental corporate information is being disseminated and absorbed by the market, and the price discovery process will be allowed to function without impediment. Accordingly, the Participants believe that the proposed Overnight Protected Hours window removes impediments to, and perfects the mechanism of, the national market system by extending proven investor protections to a trading environment that presents the types of risks that the Plan was designed to address, while preserving the market's capacity to efficiently incorporate material new information during the pre-market period.

Overnight Price Band Calculation

The Participants have designed the Overnight Price Bands to balance the Plan's dual objectives of preventing extraordinary volatility and facilitating price discovery during overnight trading sessions. The Overnight Price Bands are calculated using two reference prices: the Closing Price and a more recent Consolidated Price representing an execution in the post-market. The use of dual reference prices is designed to mitigate the risks associated with reliance on a single closing price that may become stale or unrepresentative of current market conditions by the time overnight trading commences. Material information is frequently disseminated after the close of the Regular Trading Session, and post-market trading activity may result in prices that differ meaningfully from the Closing Price.

If the Overnight Price Bands were anchored to just one price, the bands could be misaligned with prevailing market sentiment, potentially resulting in price bands that are too restrictive impeding legitimate price discovery based on post-market developments. By incorporating the Consolidated Price, the Overnight Price Bands dynamically account for post-market trading activity, ensuring that the bands reflect a price at which market participants have demonstrated a willingness to transact, which is aligned with ATS practice, while also incorporating the Closing Price to reflect market sentiment during Regular Trading hours. This dual-reference methodology grounds the Overnight Price Bands in demonstrated market sentiment across both the Regular Trading Session and post-market hours, providing maximum flexibility in the protections while ensuring those protections remain appropriately calibrated to actual market conditions. The Participants believe that this approach is consistent with the protection of investors and the maintenance of fair and orderly markets, and removes impediments to, and perfects the mechanism of, the national market system.

The Participants selected a Percentage Parameter of 20% for Overnight Price Bands to align with the 20% static band protections currently in place for overnight trading on ATSs, while differing from ATS approach by using two reference prices in calculating those bands. Furthermore, the Participants expect that during the initial period of overnight trading hours (commonly referred to as “23/5 trading”), when market participants are adjusting to the new structure, applying the same Percentage Parameters to all stocks in the Overnight trading session will be easier for participants to understand, balancing the interest of protecting investors with ensuring transparent market practices.

The Overnight Price Bands are also subject to minimum price band thresholds [17] to ensure that a minimum range of permissible trading prices remains available during overnight hours. These minimum thresholds prevent the Overnight Price Bands from becoming so narrow as to unduly restrict trading activity or impede legitimate price movements, particularly for lower-priced securities where the application of percentage-based parameters alone could result in price bands of only a few cents. The Participants believe that establishing minimum price band thresholds appropriately balances investor protection against extraordinary volatility with the preservation of fair and orderly markets by ensuring that overnight trading can continue to occur within a reasonable price range, consistent with the purposes of Section 11A of the Exchange Act and Rule 608 thereunder.

Primary Listing Exchange and Processor Obligations

This proposed amendment requires the Primary Listing Exchange of an NMS Stock to calculate the price bands and disseminate them to the Processors, who will then disseminate those bands to the market. This was chosen as the approach in Phase 1 because the Processors are currently testing and implementing extensive updates [18] and the Participants agreed that the most effective way to implement Overnight Protections would be to reduce the burden on the Processors that would have come from calculating the bands themselves. Phase 1 is designed to require minimal work from the Processors. The Processors, however, will then disseminate the bands to the public over trade and quote multicast channels via existing fields in the LULD messages starting at approximately 8:55 p.m. Eastern Time, in line with their current role during Regular Trading Hours.

Overnight Halts

At this time, the Participants have determined not to implement automatic Trading Pauses during Overnight Protected Hours, similar to ATSs which also do not implement automatic trading pauses during overnight trading sessions (ATSs simply reject orders that fall outside their bands). This approach reflects the Participants' careful consideration of the distinct characteristics of overnight trading, including significantly reduced liquidity, lower trading volumes, and fewer active market participants relative to Regular Trading Hours. During the Regular Trading Session, automatic Trading Pauses serve to provide market participants with a brief opportunity to reassess their trading interest and supply additional liquidity following a significant price movement, after which trading resumes with an auction to ( printed page 33778) facilitate orderly price discovery. Instead of implementing a similar process of automatic Trading Pauses followed by an auction for the Overnight Protected Hours, Primary Listing Exchanges would instead retain discretion to announce Regulatory Halts, in accordance with Primary Listing Exchange rules, during Overnight Protected Hours, which would remain in place for the duration of the overnight trading session. The Participants have elected not to reopen trading halts with auctions during Overnight Protected Hours because they expect that there will be insufficient liquidity in the initial phase of the overnight trading session for an efficient auction to occur. Without confidence in the standard method of reopening trading following a halt, and without sufficient information to create a different method, the Participants believe that it is in the best interests of the market not to reopen trading following a halt in the overnight session.

The Participants believe that permitting the Primary Listing Exchanges to announce Regulatory Halts during Overnight Protected Hours aligns with the Plan's fundamental purpose of promoting a fair and orderly market. Under this framework, the Overnight Price Bands will continue to operate as a safeguard against trades occurring at prices that deviate significantly from a security's recent fundamental value, thereby preventing extraordinary volatility and protecting investors from executing transactions at aberrant prices. When an event occurs that a Primary Listing Exchange, in accordance with Primary Listing Exchange rules, determines merits a Regulatory Halt, the Primary Listing Exchange will have the authority, but not the obligation, to announce a Regulatory Halt if, in its judgment, such action is warranted to maintain a fair and orderly market. This discretionary approach permits the Primary Listing Exchange to evaluate the totality of the circumstances, including any material information that may be affecting the security's price, and which may also include, in certain circumstances, prevailing liquidity conditions, before determining whether a halt is necessary and appropriate.

The Participants believe this framework is consistent with Section 11A of the Securities Exchange Act of 1934 and Rule 608 thereunder because it preserves the core investor protections of the limit up-limit down mechanism while the Participants analyze data on overnight trading, thereby removing impediments to, and perfecting the mechanism of, the national market system.

Ministerial Amendments

The Participants have proposed ministerial changes to update the addresses of certain Participants in Section II(A) of the Plan.

The Participants have also proposed a change to the definition of Regular Trading Hours, in Section I(S) to conform to the amended citation in Regulation NMS for the definition of Regular Trading Hours.[19]

3. Proposed Overnight Trading Protections Based on Current ATS Protections in Anticipation of 23/5 Exchange Trading

The Commission has recently approved applications by 24X National Exchange LLC, NYSE Arca Inc., and Nasdaq to conduct trading on a near-continuous 23/5 basis.[20] These approvals represent a significant expansion of exchange trading into periods that have historically been characterized by lower liquidity, wider spreads, and the potential for increased price volatility due to the release of overnight news and developments in foreign markets. The Processors are preparing to commence overnight trading on December 6, 2026.[21]

The 20% Percentage Parameter proposed in this amendment reflects the existing price protection mechanisms employed by ATSs that currently operate in the overnight trading space. ATSs that currently facilitate overnight trading have generally adopted 20% trading bands as a market-wide price protection standard, although those bands are based on a single static price,[22] unlike the two reference prices in this proposal.[23] The Participants expect that adopting a band percentage consistent with these established ATS practices will facilitate a smoother transition for market participants as overnight trading expands to national securities exchanges. By aligning the Overnight Price Bands with protections conceptually familiar to broker-dealers, institutional investors, and retail participants who have engaged in overnight trading through ATSs, the proposed amendment reduces operational complexity and minimizes the risk of market disruption that could arise from the introduction of materially different price protection standards. The Participants submit that this alignment serves the public interest and the protection of investors by establishing uniform expectations across trading venues, thereby promoting confidence in the integrity of overnight trading and supporting the orderly expansion of 23/5 trading to the national market system.

The Participants believe that the application of protections to these newly approved overnight trading sessions is necessary and appropriate and in the public interest, for the protection of investors and for the maintenance of fair and orderly markets. The fundamental purpose of the Plan—to prevent trades in individual NMS Stocks from occurring at prices that are not reflective of a fair and orderly market—applies with equal, if not greater, force during overnight periods when market conditions may exacerbate the risk of sudden, unanticipated price movements similar to the “Flash Crash.” The LULD mechanism is intended to reduce the negative impacts of sudden, unanticipated price movements in NMS Stocks, thereby protecting investors and promoting a fair and orderly market. Previously conducted data and analysis have demonstrated that the LULD mechanism has been largely effective at reducing the negative impacts of such price movements,[24] and the Participants believe protections should extend to overnight trading sessions where similar risks—or heightened risks due to reduced liquidity—may arise.

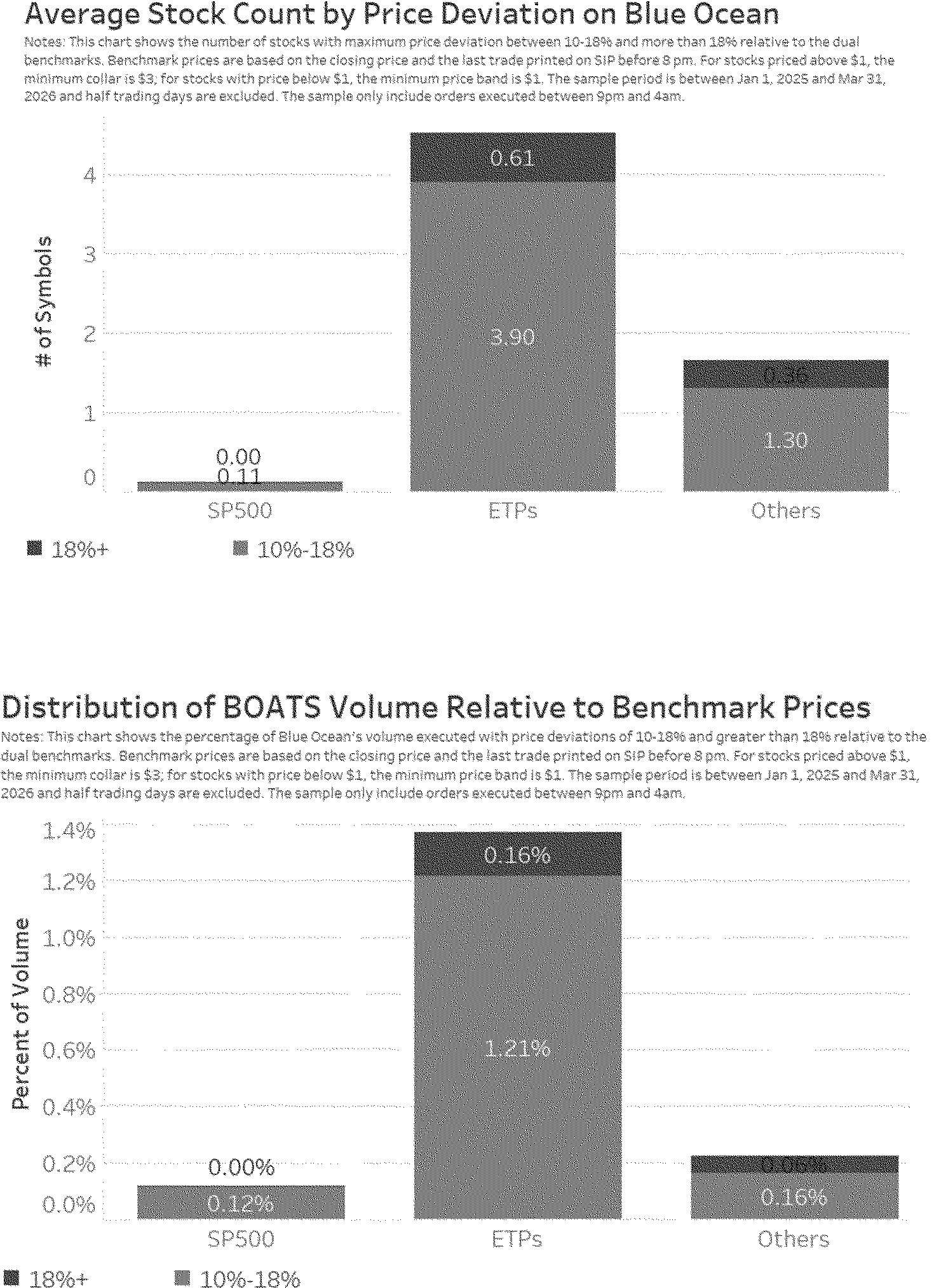

Based on an analysis of data from the ATS Blue Ocean, the Participants expect ( printed page 33779) that the impact of this proposal on actual overnight trading will be minimal, although the guardrails are valuable to the outliers. Using an approximation of the proposed overnight trading bands [25] and the closing price and the price of a stock as of 7:45 p.m. Eastern Time, an average of 0 S&P 500 stocks, 0.6 ETPs and 0.4 non-S&P 500 stocks per day, or less than 0.1% of total volume, would be impacted by the bands.

Overnight trading sessions present unique challenges for market integrity, including reduced liquidity, increased information asymmetry due to overnight news flow and global developments, and a heightened potential for erroneous trades. Implementing the proposed market protections during overnight trading sessions should limit the frequency and severity of harmful price dislocations, consistent with the purposes for which the Plan was adopted.

Indeed, the development of price band protections in the overnight trading space illustrates the organic evolution of similar safeguards in response to market need. Before national securities exchanges sought to extend their operating hours into overnight sessions, ATSs pioneered overnight trading and independently implemented price band mechanisms to protect market participants from aberrant executions during periods of reduced liquidity. The adoption of 20% price bands by ATSs operating in this space emerged as a market-driven response to the unique risks presented by overnight trading—demonstrating that sophisticated market participants recognize the necessity of such protections. Market participants who have engaged in overnight trading through ATSs have come to rely on these safeguards. These market participants have a reasonable expectation that comparable protections will accompany the expansion of overnight trading to national securities exchanges, which the Participants believe this proposed amendment will achieve, although with some differences to the ATS approach, including by using two reference prices in order to reflect relevant market activity.

4. Phased Implementation of Overnight Protections

As noted above, the Participants propose to implement Overnight Protections in two phases. The amendments to the Plan set forth herein constitute Phase 1 of this implementation. Phase 2 is anticipated to be implemented in 2027, following a ( printed page 33780) period of observation, data gathering, and assessment of overnight trading. As no national exchange currently conducts trading in the overnight session, comprehensive and reliable data on overnight trading activity remains limited, and the Participants recognize that the provisions of Phase 1 in the proposed Plan may require recalibration as empirical evidence accumulates. Phase 1 is therefore designed not only to provide meaningful protections against extraordinary volatility during overnight hours, but also to serve as a structured framework for generating the granular, real-world data necessary to evaluate and refine these overnight provisions to craft a thoughtful Phase 2.

The Participants currently expect Phase 2 to include: (1) sliding price bands that adjust based on market activity during Overnight Protected Hours without imposing an absolute limit on prices ( e.g., sliding the Upper Price Band to a higher price if a security is in a prolonged limit state where the national best bid is equal to the Overnight Upper Price Band; (2) the Processors calculating and disseminating the Overnight Price Bands, rather than the Primary Listing Exchanges; and (3) recalibrated Overnight Percentage Parameters, which may be lower than the proposed parameters set forth in Section VIII(A)(3) of the Plan and which may differ between Tier 1 and Tier 2 NMS Stocks.

Each of these anticipated Phase 2 enhancements reflects the Participants' recognition that certain provisions in the current proposal—including the initial Overnight Percentage Parameters, the assignment of calculation and dissemination responsibilities, and the static nature of the price bands—may not be optimally calibrated for the unique liquidity and volatility conditions that characterize overnight trading sessions. The Participants believe that the phased approach is the most prudent and responsible means of addressing them these challenges, by enabling the Plan and the Commission to collect and analyze data on overnight trading before proceeding to a more complex system of overnight protections.

The Operating Committee intends to evaluate data on overnight trading and the performance of Phase 1 in 2027 and determine the appropriate timing and specifications for Phase 2. In conducting this evaluation, the Operating Committee will analyze, among other things, the interactions between the market and Overnight Price Bands across varying liquidity conditions, the incidence and causes of any trading halts declared by Listing Exchanges, the adequacy of the Overnight Percentage Parameters in mitigating extraordinary volatility without unduly constraining legitimate price discovery, and the operational performance of the Primary Listing Exchanges in calculating Overnight Price Bands and the Processors in disseminating them. The Participants are committed to a rigorous, evidence-based assessment and intend to work collaboratively with the Commission and its Staff throughout this process to identify additional data points or analytical methodologies that may enhance the evaluation. The Participants expect to include information regarding the operations of Phase 1 in the Plan's quarterly reports, commencing with the quarterly report covering the first full quarter of overnight trading. Participants expect to submit a Phase 2 proposal for consideration by the Commission with sufficient time for implementation by the fourth quarter of 2027. The Participants will report on the evidence gathered on overnight trading together with its proposal for Phase 2 revisions to overnight protections.

Just as the Plan was initially approved on a trial basis [26] to allow the Participants and the public to gain valuable practical experience with Plan operations, and subsequently made permanent following extensive data collection and analysis,[27] the Participants' proposal to implement Overnight Protections in a phased approach will enable the Operating Committee, the Commission, and the market as a whole, to observe overnight trading and the effectiveness of the Overnight Protections and compile data to inform future decisions.

The Plan has always operated on the premise that the Participants will engage in a continuous data-intensive review of the National Market System and the Plan's impact on that market. That premise carries particular force here, where the implementation of protections to Overnight Protected Hours presents novel challenges—including thinner liquidity, wider spreads, and the potential for price dislocations driven by international developments or after-hours corporate announcements—that cannot be fully anticipated or addressed through existing data alone. The current provisions of the proposal reflect the Participants' best judgment based on available information, but the Participants recognize that certain parameters and operational assignments may require adjustment once real-world evidence becomes available. The proposed two-phased approach, based on a review of the evidence prior to implementing a final proposal, is consistent with that fundamental approach, and will enable the Operating Committee and the Commission to collaborate to review new information.

The Commission has repeatedly emphasized the importance of ongoing review and assessment to ensure that the Plan continues to achieve its objective of reducing extraordinary volatility. The Participants believe that the same data-driven approach is appropriate for overnight protections, and that the restrained approach of observing the interim effects of this Twenty-Seventh Amendment during new overnight trading hours will enable the Plan to respond to market activity with overnight protections that are effective and specifically tailored to the particular circumstances that present during overnight trading.

5. Consistency With the Purposes of the Plan and the Exchange Act

The Participants believe that the proposed amendment is necessary and appropriate in the public interest, for the protection of investors, and for the maintenance of fair and orderly markets, because extending the protections afforded by the Plan to overnight hours is consistent with the fundamental purposes of the Plan. The Plan was originally adopted to address extraordinary volatility in the securities markets and to prevent trades in individual NMS Stocks from occurring outside of Price Bands selected to maintain orderly market conditions. These objectives are equally applicable—and may be more critical—during overnight trading sessions when market conditions may be less liquid and more susceptible to price dislocations. The efficacy of current LULD mechanisms in addressing extraordinary market volatility, moreover, informs the Participants' belief that it is appropriate to also establish price protections in the new overnight trading environment.

The Participants believe that the proposed amendment is consistent with Section 11A(a)(1)(C) of the Exchange Act, which directs the Commission to facilitate the establishment of a national market system that assures, among other things, economically efficient execution of securities transactions, fair competition among brokers and dealers ( printed page 33781) and among markets, and the practicability of brokers executing investors' orders in the best market.[28] Applying uniform protections across all trading centers that operate during Overnight Protected Hours promotes fair competition and ensures that investor protection does not vary based on the venue at which an order is executed during overnight hours.

This Twenty-Seventh Amendment to the Plan would enhance the public interest, protect investors, and help maintain fair and orderly markets, while removing impediments to and perfecting the mechanism of the national market system in conformance with Rule 608.[29] This proposed amendment establishes guardrails for overnight trading to mitigate the risk of excessive volatility in markets and will help to prevent extreme price swings and erroneous trades, which will protect investors from excessive volatility in the new overnight trading session. The amendment appropriately balances the dual objectives of preventing extraordinary volatility and facilitating price discovery, and will thus enhance confidence in the market as a whole by demonstrating the exchange industry's thoughtful approach to implementing new market protections in the new world of 23/5 Trading.

B. Governing or Constituent Documents

The governing documents of the Processor, as defined in Section I(P) of the Plan, will not be affected by the Amendment.

C. Implementation of Amendment

The Participants will announce the operative date of the amendment (“Operative Date”), which will be subject to the completion of certain systems changes by the Processors for the Unlisted Trading Privileges (UTP) Plan and Consolidated Tape Association (CTA) Plan to ensure dissemination of overnight trading bands.

D. Development and Implementation Phases

The Participants propose to implement the proposed amendment on the Operative Date. As discussed, a separate “Phase 2” proposal will be filed with the Commission at a later date. Phase 1 overnight protections will remain in place until the operative date of such Phase 2 proposal.

E. Analysis of Impact on Competition

The Participants believe that the proposed amendment does not impose any burden on competition that is not necessary or appropriate in furtherance of the purposes of the Exchange Act. The proposed amendment to the Plan would apply to all market participants equally and would not impose a competitive burden on one category of market participants in favor of any other category of market participant. The proposed amendment would apply to trading on all trading centers that operate during Overnight Protected Hours, and all NMS Stocks (other than rights and warrants, which are excluded from the Plan) would be subject to the amended Plan's requirements. The Participants do not believe that the proposed amendment introduces terms that are unreasonably discriminatory for the purposes of Section 11A(c)(1)(D) of the Exchange Act because it would apply to all market participants equally.

F. Written Understanding or Agreements Relating to Interpretation of, or Participation in, Plan

The Participants have no written understandings or agreements relating to interpretation of the Plan. Section II(C) of the Plan sets forth how any entity registered as a national securities exchange or national securities association may become a Participant.

G. Approval of Amendment of the Plan

Each of the Participants has approved this Twenty-Seventh Amendment in accordance with Section III(C) of the Plan. The Participants also received and incorporated feedback from the Plan Advisory Committee in preparing this proposal. Each of the Plan's Participants has executed a written amended Plan.

H. Description of Operation of Facility Contemplated by the Proposed Amendment

Not applicable.

I. Terms and Conditions of Access

Section II(C) of the Plan provides that any entity registered as a national securities exchange or national securities association under the Exchange Act may become a Participant by: (1) becoming a participant in the applicable Market Data Plans, as defined in Section I(F) of the Plan; (2) executing a copy of the Plan, as then in effect; (3) providing each then-current Participant with a copy of such executed Plan; and (4) effecting an amendment to the Plan as specified in Section III(B) of the Plan.

J. Method of Determination and Imposition, and Amount of, Fees and Charges

This section is not applicable as the proposed amendment to the Plan does not involve fees or charges.

K. Method and Frequency of Processor Evaluation

Not applicable.

L. Dispute Resolution

Section III(C) of the Plan provides that each Participant shall designate an individual to represent the Participant as a member of an Operating Committee. No later than the initial date of the Plan, the Operating Committee shall designate one member of the Operating Committee to act as the Chair of the Operating Committee. Any recommendation for an amendment to the Plan from the Operating Committee that receives an affirmative vote of at least two-thirds of the Participants, but is less than unanimous, shall be submitted to the Commission as a request for an amendment to the Plan initiated by the Commission under Rule 608.

III. Solicitation of Comments

Interested persons are invited to submit written data, views and arguments concerning the foregoing, including whether the amendment is consistent with the Exchange Act and the rules thereunder. Comments may be submitted by any of the following methods:

Electronic Comments

- Use the Commission's internet comment form (https://www.sec.gov/rules/sro.shtml); or

- Send an email torule-comments@sec.gov. Please include file number 4-631 on the subject line.

Paper Comments

- Send paper comments in triplicate to Secretary, Securities and Exchange Commission, 100 F Street NE, Washington, DC 20549-1090.

All submissions should refer to File Number 4-631.This file number should be included on the subject line if email is used. To help the Commission process and review your comments more efficiently, please use only one method. The Commission will post all comments on the Commission's internet website ( http://www.sec.gov/rules/sro.shtml). Copies of the filing will be available for inspection and copying at the principal office of the Exchange. Do not include personal information in submissions; you should submit only information that you wish to make available publicly. We may redact in ( printed page 33782) part or withhold entirely from publication submitted material that is obscene or subject to copyright protection. All submissions should refer to File Number 4-631 and should be submitted on or before June 25, 2026.

For the Commission, by the Division of Trading and Markets, pursuant to delegated authority.30

Sherry R. Haywood,

Assistant Secretary.

( printed page 33783)