Securities and Exchange Commission

- [Release No. 34-95529; File No. SR-CboeBZX-2022-038]

Pursuant to Section 19(b)(1) of the Securities Exchange Act of 1934 (the “Act”),[1] and Rule 19b-4 thereunder,[2] notice is hereby given that on August 5, 2022, Cboe BZX Exchange, Inc. (the “Exchange” or “BZX”) filed with the Securities and Exchange Commission (the “Commission”) the proposed rule change as described in Items I, II, and III below, which Items have been prepared by the Exchange. The Commission is publishing this notice to solicit comments on the proposed rule change from interested persons.

I. Self-Regulatory Organization's Statement of the Terms of Substance of the Proposed Rule Change

Cboe BZX Exchange, Inc. (the “Exchange” or “BZX”) proposes to amend Rule 11.28(a) to extend the MOC Cut-Off Time from 3:35 p.m. Eastern Time to 3:49 p.m. Eastern Time. The text of the proposed rule change is provided in Exhibit 5.

The text of the proposed rule change is also available on the Exchange's website ( https://markets.cboe.com/us/equities/regulation/rule_filings/bzx/), at the Exchange's Office of the Secretary, and at the Commission's Public Reference Room.

II. Self-Regulatory Organization's Statement of the Purpose of, and Statutory Basis for, the Proposed Rule Change

In its filing with the Commission, the Exchange included statements concerning the purpose of and basis for the proposed rule change and discussed any comments it received on the proposed rule change. The text of these statements may be examined at the places specified in Item IV below. The Exchange has prepared summaries, set forth in sections A, B, and C below, of the most significant aspects of such statements.

A. Self-Regulatory Organization's Statement of the Purpose of, and Statutory Basis for, the Proposed Rule Change

1. Purpose

Exchange Rule 11.28 (Cboe Market Close, a Closing Match Process for Non-BZX-Listed Securities) provides Members an optional closing match process for non-BZX-Listed securities, known as Cboe Market Close (“CMC”). Currently, per Rule 11.28(a) (Order Entry) Members [3] may enter, cancel, or replace Market-on-Close (“MOC”) orders designated for participation in CMC beginning at 6:00 a.m. Eastern Time [4] up to 3:35 p.m. (“MOC Cut-Off Time”). The Exchange now proposes to move the MOC Cut-Off Time from 3:35 p.m. to 3:49 p.m. The Exchange is not proposing to make any other changes to the CMC process.

By way of background, on May 5, 2017, the Exchange filed a proposed rule change to adopt CMC, a match process for MOC orders in non-BZX listed securities and on December 1, 2017, filed Amendment No. 1 [5] to that proposal (the “Original Proposal”).[6] On January 17, 2018, the Commission, acting through authority delegated to the Division of Trading and Markets,[7] approved the Original Proposal (“Approval Order”).[8] On January 31, 2018, NYSE Group, Inc. (“NYSE”) and the Nasdaq Stock Market LLC (“Nasdaq”) filed petitions for review of the Approval Order (“Petitions for Review”). Pursuant to Commission Rule of Practice 431(e),[9] the Approval Order was stayed by the filing with the Commission of a notice of intention to petition for review.[10] On March 1, 2018, pursuant to Commission Rule of Practice 431, the Commission issued a scheduling order granting the Petitions of Review of the Approval Order, and provided until March 22, 2018, for any party or other person to file a written statement in support of, or in opposition to, the Approval Order.[11] On April 12, 2018, NYSE and Nasdaq submitted written statements opposing the Approval Order and BZX submitted a statement in support of the Approval Order.[12] On October 4, 2018, BZX filed Amendment No. 2 [13] to the Original Proposal.

The Commission conducted a de novo review of the CMC proposal and associated public record, including ( printed page 52093) Amendment No. 2, the Petitions for Review, and all comments and statements submitted by certain exchanges, issuers, and other market participants,[14] to determine whether the proposal was consistent with the requirements of the Act and the rules and regulations issued thereunder that are applicable to a national securities exchange.[15] The Commission noted that under Rule 700(b)(3) of the Commission's Rule of Practice, the “burden to demonstrate that a proposed rule change is consistent with the Exchange Act and the rules and regulations issued thereunder . . . is on the self-regulatory organization that proposed the rule change.” [16]

Importantly, after reviewing the entire record, the Commission concluded that BZX met its burden to show that the proposed rule change was consistent with the Act, and pursuant to its January 21, 2020, order, set aside the Approval Order and approved BZX's CMC proposal, as amended (“Final Approval Order”).[17] Notably, the Commission stated that the record “demonstrate[d] that Cboe Market Close should introduce and promote competitive forces among national securities exchanges for the execution of MOC orders” [18] and that “the record demonstrate[d] that Cboe Market Close should not disrupt the closing auction price discovery process nor should it materially increase the risk of manipulation of official closing prices”.[19] For the reasons discussed more fully below, the Exchange believes that when applying the Commission's analysis in the Final Approval Order to the current proposal, such review would similarly conclude that this proposal is consistent with the Act and should be approved.

Since the Original Proposal various exchanges have extended the MOC cut-off times for their closing auctions, moving them closer to 4:00 p.m.[20] Additionally, closing price match services offered by off-exchange venues have grown in popularity,[21] including alternative trading systems (“ATS”) that offer a MOC cut-off time as close as 30-seconds before the primary exchanges' cut-off times, as well as MOC cut-off times aligned with those of NYSE, NYSE Arca, and Nasdaq.[22] As the market structure for closing auctions and closing price match offerings has continued to evolve, and in response to customer feedback and to better compete with off-exchange venues, the Exchange is proposing this rule change to align CMC's MOC Cut-Off time more closely with the other exchanges and off-exchange venues.

The Exchange notes that Members have requested a MOC Cut-Off Time that is closer to the end of Regular Trading Hours [23] so that they may retain control of their trading for a longer period and be better able to manage their trading at the close.[24] Generally speaking, notional trading and trading volatility are typically at their highest towards the end of Regular Trading Hours. Accordingly, market participants often prefer to trade as close to 4:00 p.m. as possible, because doing so can provide them with more time to seek better priced liquidity for their orders in a variety of ways, including but not limited to, finding contra-side liquidity in the marketplace and trading directly against such interest, or guaranteeing a customer order at a price better than the national best bid or offer by committing capital to an order and filling it in a principal capacity, as well as continuing to trade orders algorithmically into the close, thus reducing the size of their outstanding orders that they may decide to commit to CMC or the primary auctions.

Additionally, Members have indicated that extending the MOC Cut-Off Time to 3:49 p.m. will help to make CMC a more comparable alternative to NYSE and Nasdaq, which have MOC cut-off times of 3:50 p.m.[25] and 3:55 p.m.,[26] respectively. For reasons discussed directly above, cut-off times closer to 4:00 p.m. are beneficial to market participants, and by extending CMC's MOC Cut-Off Time to 3:49 p.m., CMC will be better positioned to serve as a viable option for market participants to consider when deciding which venues to route their MOC orders, thus enhancing intermarket competition.

The Exchange also notes that today's market participants, including users of CMC,[27] are technologically equipped [28] ( printed page 52094) to handle a 3:49 p.m. MOC Cut-Off time. As a general mater, today's market participants, including CMC users, rely on electronic smart order routers, order management systems, and trading algorithms, which make routing and trading decisions on an automated basis, in times typically measured in microseconds. In this regard, the Exchange believes that if a CMC user receives a message that their MOC order was not matched in CMC,[29] such CMC user will have more than enough time to reroute their MOC order to the primary exchange. Importantly, the Exchange discussed the proposed change with both current CMC users and potential new CMC users to gauge whether a MOC Cut-Off Time one-minute closer to the NYSE cut-off time, and six-minutes closer to the Nasdaq cut-off time, would present operational or technological challenges, and confirmed that CMC users can in fact manage the proposed change.

2. Statutory Basis

The Exchange believes the proposed rule change is consistent with the Act and the rules and regulations thereunder applicable to the Exchange and, in particular, the requirements of Section 6(b) of the Act.[30] Specifically, the Exchange believes the proposed rule change is consistent with the Section 6(b)(5) [31] requirements that the rules of an exchange be designed to prevent fraudulent and manipulative acts and practices, to promote just and equitable principles of trade, to foster cooperation and coordination with persons engaged in regulating, clearing, settling, processing information with respect to, and facilitating transactions in securities, to remove impediments to and perfect the mechanism of a free and open market and a national market system, and, in general, to protect investors and the public interest. Additionally, the Exchange believes the proposed rule change is consistent with the Section 6(b)(5) [32] requirement that the rules of an exchange not be designed to permit unfair discrimination between customers, issuers, brokers, or dealers.

In particular, the Exchange believes that moving the MOC Cut-Off Time to 3:49 p.m. would remove impediments to and perfect the mechanism of a free and open market and a national market system because it would allow Members to retain control over their orders for a longer period, thereby assisting market participants in managing their trading at the close. As discussed more fully above, market participants may prefer to trade as close to 4:00 p.m. as possible, because doing so can provide them with more time to seek better priced liquidity for their orders in a variety of ways, as well as give them more time to determine the size of their outstanding orders that they may decide to commit to CMC or the primary auctions.

Additionally, the Exchange believes that a MOC Cut-Off Time fifteen-minutes (15) prior to NYSE's cut-off time, and twenty-five-minutes (25) prior to Nasdaq's cut-off time, is no longer necessary. Rather, the Exchange notes that today's market participants are technologically equipped [33] to handle a 3:49 p.m. MOC Cut-Off time. As discussed above, today's market participants rely on electronic smart order routers, order management systems, and trading algorithms, which make routing and trading decision on an automated basis, in times often measured in microseconds. As such, Members are technologically equipped to efficiently respond to CMC's publication of matched shares and should they so choose, reroute any unmatched MOC orders to the respective primary closing auction. As noted above, the Exchange discussed the extension of the MOC Cut-Off Time with CMC users and confirmed that the proposed MOC Cut-Off Time will not present them with any operational or technological issues.

Furthermore, the Exchange believes that the extension of cut-off times by the primary exchanges since CMC's proposal, as well as the growth of off-exchange venues [34] with cut-off times in such close proximity to the end of Regular Trading Hours is indicative of Members' desires for such offerings. Logically, such a change in market structure would not have occurred if Members did not already possess the operational and technological wherewithal to effectively manage the multitude of cut-off times offered by the exchanges and off-exchange venues.

Moreover, the Exchange believes that the proposed rule change will remove impediments to and perfect the mechanism of a free and open market and a national market system because extending the MOC Cut-Off Time to 3:49 p.m. would more closely align the CMC MOC Cut-Off Time to the cut-off times in place for the other exchanges.[35] For the reasons discussed more fully above, the primary exchanges' cut-off times are beneficial to market participants because of their proximity to 4:00 p.m. By moving the MOC Cut-Off Time closer to the other exchanges' cut-off times, CMC can become a comparable alternative for Members to route their unpriced MOC orders. Importantly, even with a MOC Cut-Off Time closer to the primary exchanges' cut-off times, CMC removes any perceived impact on the primary listing markets' close by publishing the number of matched order shares, by security, in advance of the primary markets' cut-off time. The total matched shares would still be disseminated by the Exchange free of charge via the Cboe Auction Feed, albeit at the new proposed MOC Cut-Off Time of 3:49 p.m. Because of the speeds and widespread use of market technology, this information can still be used by the primary markets' closing processes, and as discussed above, CMC users will still have ample time [36] to reroute any MOC orders not matched via CMC to reach the primary market to be included in their closing auction process.

Additionally, the proposed rule change would more closely align CMC's MOC Cut-Off Time with that of off-exchange venues that offer cut-off times aligned with those currently offered by the primary exchanges, and as little as ( printed page 52095) 30-seconds prior to market close.[37] As such, the Exchange believes that the proposed rule change is supported by both ample precedent as well as current market structure, and should not present any new or novel issues that market participants must consider when managing their trading and determining which exchange or off-exchange venue to route their MOC orders.

Price Discovery [38]

The Exchange believes that the proposed rule change is consistent with the Section 6(b)(5) requirements.[39] As previously noted by the Exchange,[40] CMC accepts and matches only unpriced MOC orders. By matching only unpriced MOC orders, and not Limit-On-Close (“LOC”) orders and executing those matched MOC orders that naturally pair off with each other and effectively cancel each other out, CMC is designed to avoid impacting price discovery. While the proposed rule change would have CMC accept MOC orders up to 3:49 p.m., such extension will not change this underlying functionality. As previously noted by the Exchange,[41] matched MOC orders are merely recipients of price formation and do not directly contribute to the price formation process. Indeed, in its Final Approval Order for CMC, even the Commission noted that unpriced, paired-off MOC orders do not directly contribute to setting the official closing price of securities on the primary listing exchanges but, rather, are inherently the recipients of price formation information.[42]

Moreover, the Exchange believes that even if extending the MOC Cut-Off Time to 3:49 p.m. reduces the number of MOC orders routed to a security's primary listing market, CMC is designed to remove any perceived adverse impact on the primary listing markets' close because the total matched shares would still be disseminated by the Exchange free of charge via the Cboe Auction Feed prior to the primary exchanges' cut-off times. Additionally, because of the technological capabilities of today's market participants discussed more fully above, this information can still be incorporated by the primary markets' closing processes, and CMC users will still have ample time [43] to reroute any MOC orders not matched via CMC to the primary markets to be included in their closing auction processes.

Fragmentation [44]

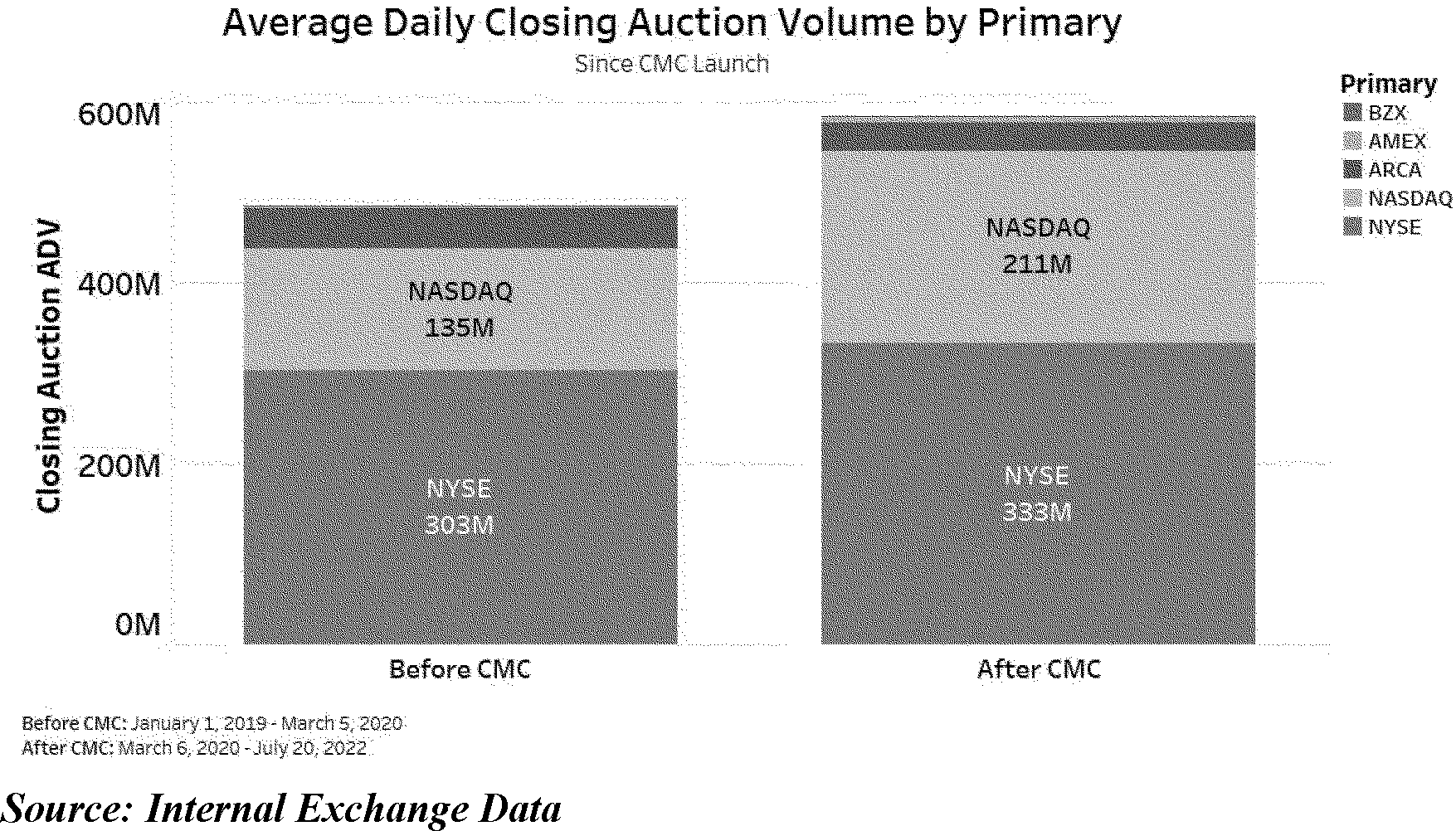

Another matter addressed by the Commission in their review of the Initial Proposal was fragmentation, and whether CMC would fragment the markets beyond what currently occurs through off-exchange close price matching venues.[45] Importantly, as illustrated in the chart below, an analysis by the Exchange shows that the closing auction volume on both NYSE and Nasdaq has increased since the launch of CMC on March 6, 2022. As such, the Exchange believes that the initial fragmentation concerns raised by commenters during the Initial Proposal have not materialized, and that merely extending the MOC Cut-Off Time, while leaving all other CMC functionality intact, will not result in increased market fragmentation.

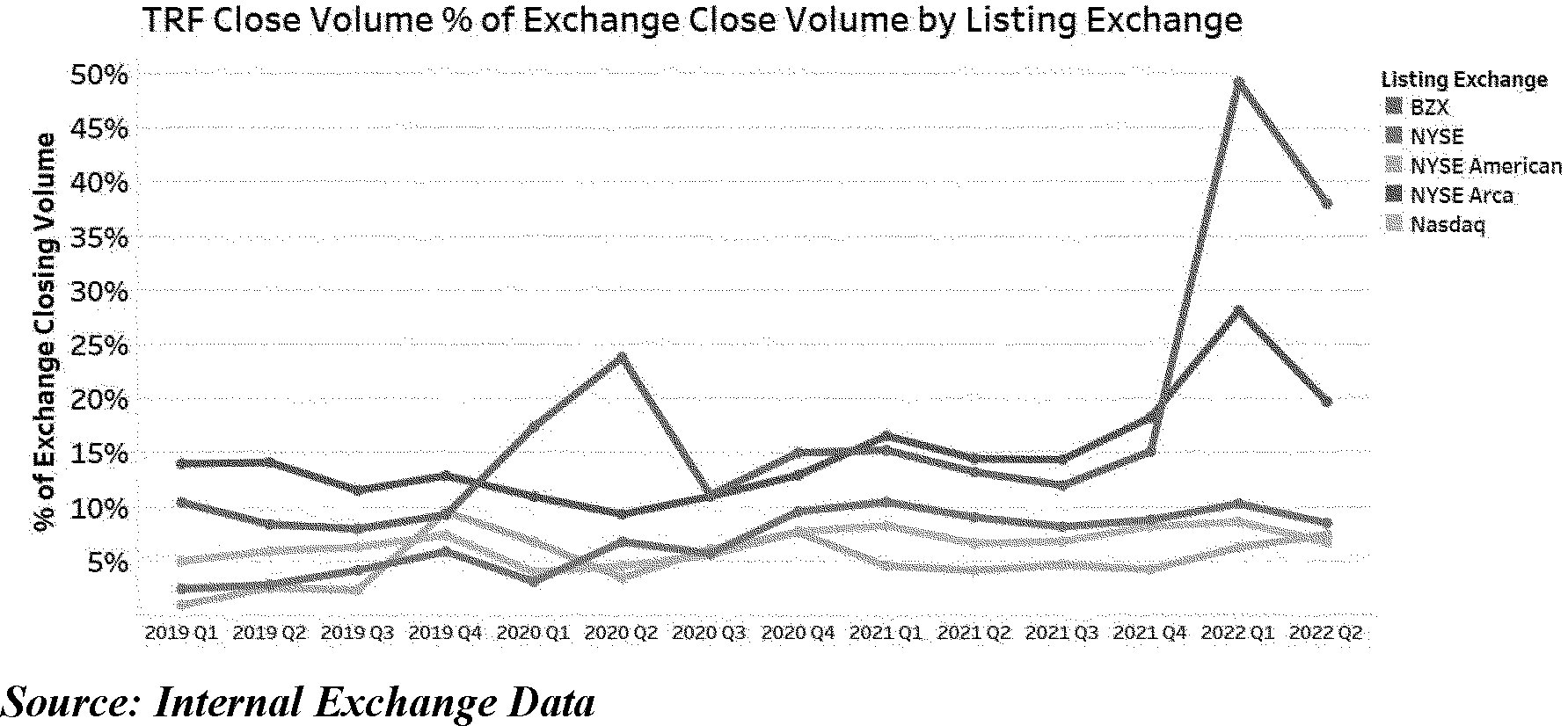

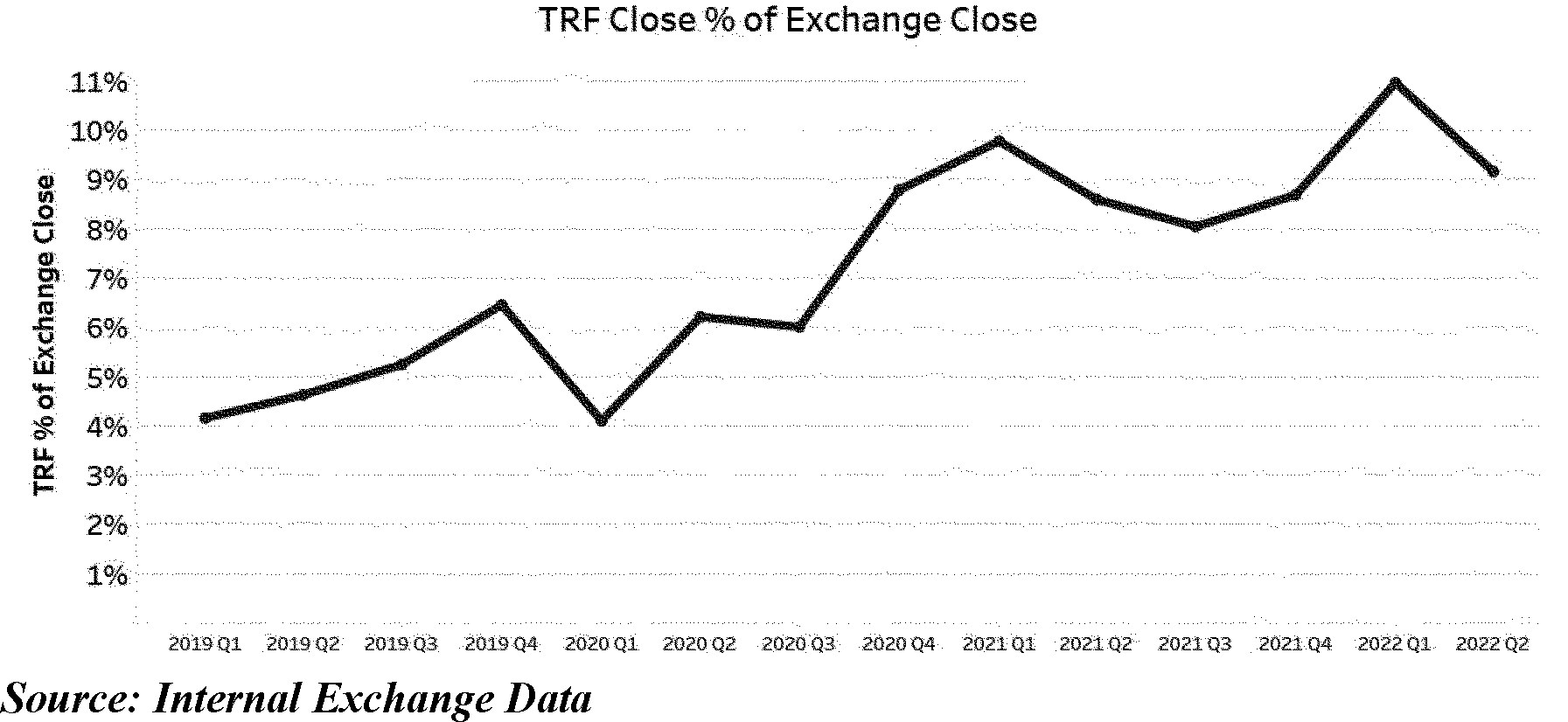

The Exchange also notes that even if the proposed rule change results in fewer MOC orders participating in the primary exchanges' closing auctions, that the fragmentation of MOC orders already occurs in today's markets on off-exchange venues. As illustrated in the first two charts below, a growing proportion of trading volume at the close occurs on off-exchange venues, where the TRF close volume, as a percent of Exchange close volume, has risen steadily since January 2019.[46] In the third chart the Exchange also studied the top ten most actively traded securities during the same time period and found that a significant portion of the total closing volume is executed off-exchange, following the dissemination of the official closing price.

Accordingly, the Exchange believes that approving this proposal will allow the Exchange to compete on a more equal playing field with off-exchange venues for closing volume already being executed away from the primary listing venues. In better competing with off-exchange venues, CMC can help increase transparency, reliability, and price discovery by encouraging market participants that would otherwise seek to match MOC orders off-exchange to re-direct their MOC orders to BZX, a public exchange. Moreover, by attracting such order flow, CMC can help to increase the amount of volume at the close executed on systems subject to the resiliency requirements of Regulation SCI.[48]

Market Complexity and Operational Risk [49]

The Exchange believes that the proposed rule change is simple and straightforward, and as such will not significantly increase market complexity or operational risk. The Exchange seeks only to extend the MOC Cut-Off Time to 3:49 p.m., leaving all other aspects of the CMC process intact. Members will not have to consider new operational requirements of monitoring and consuming a new data feed or consider the utilization of a new order type or implementation of new Exchange code. Rather, Members may continue to monitor the same data feed as they do today, the Cboe Auction Feed, and simply look for the publication of the CMC information at the new proposed MOC Cut-Off Time.

Additionally, as discussed more fully above, the Exchange discussed this proposal with current CMC users prior to submitting this proposal and learned that CMC users are technologically equipped to manage a MOC Cut-Off Time closer to the primary exchanges' cut-off times, and that they can respond to CMC's publication of matched shares and quickly reroute any unmatched MOC orders to the respective primary closing auction. Moreover, CMC is a voluntary offering, and Members may freely decide whether to participate.

Furthermore, as noted throughout, both off-exchange venues and other exchanges already offer MOC cut-off times that are closer in time to the end of Regular Trading Hours. Specifically, as mentioned above, in 2018 Nasdaq received approval to move the cut-off times for the entry of MOC and Limit-On-Close (“LOC”) orders from 3:50 to 3:55 p.m.[50] Similarly, in 2018 the NYSE received approval from the SEC to extend their cut-off times for order entry and cancellation for participation their closing auction, from 3:45 p.m. to 3:50 p.m.[51] NYSE also offers discretionary-orders, which unlike MOC/LOC orders that are subject to NYSE's 3:50 p.m. cut-off, may be entered for participation in the closing auction until 3:59:50.[52] Additionally, market participants may enter MOC orders for participation in NYSE Arca's closing auction up to 3:59 p.m..[53] Finally, various off-exchange venues offer closing match processes with cut-off times aligned with those of the primary exchanges, and even as close to 30-seconds before market close, 4:00 p.m.[54]

Accordingly, the Exchange believes that market participants are well accustomed to managing the various cut-off times in today's marketplace, and in incorporating these timelines into their trading decisions. The number of exchanges and off-exchange venues with extended cut-off times indicates that market participants find value in their ability to retain control of their trading heading into the end of Regular Trading Hours, and the exchanges and off-exchange venues have responded to such demand. Certainly, market participants would not desire cut-off times closer to the end of Regular Trading Hours if they could not technologically and operationally manage their trading accordingly. Therefore, the extension of CMC's MOC Cut-Off Time should not present market participants with any novel operational or technological complexities.

Manipulation [55]

The Exchange does not expect that the proposed extension of the MOC Cut-Off Time to 3:49 p.m. will result in an increase of manipulative activity due to information asymmetries, or raise any unique manipulation concerns relative to how CMC exists today with a current MOC Cut-Time of 3:35 p.m. Specifically, any information CMC participants may be able to glean from their paired-off MOC orders, or from their unmatched MOC orders, is still limited in nature. For instance, any information that CMC participants may learn from receiving unmatched MOC order messages is still limited in nature because the CMC participant would still only know the unexecuted size of its own order.[56] Moreover, even if a ( printed page 52098) Member chose to participate in CMC only to gather information about the direction of an imbalance and use such information to manipulate the closing price, the Member's orders were still eligible for execution. Thus, in addition to any such information being of limited use, the Member's actions still do not provide them with free information unavailable to other market participants because the Member's orders were eligible to for execution, subjecting the Member to economic risk.

Furthermore, as with the current MOC Cut-Off Time, the proposed extension does not present any information asymmetries that do not already exist in today's markets, as the very nature of trading creates short term asymmetries of information to those who are parties to a trade.[57] Indeed, as noted by the Commission, any party to a trade gains valuable insight regarding the depth of the market when an order is executed or partially executed.[58] Additionally, NYSE imbalance information is already disseminated to NYSE floor brokers, who are permitted to share with their customers specific data from the imbalance feed.[59] Even in this case, though, the Commission stated that the value of such information is limited because the imbalance information does not represent overall supply and demand for a security, is subject to change, and is only one relevant piece of information.[60] Similarly, because any information gleaned by a CMC participant is limited only to the unexecuted size of their order, and relative to the depth of only the BZX pool of liquidity, the Exchange believes that the proposed extension of the MOC Cut-Off Time does not create an increased risk of manipulative trading activity.

While this proposal would result in the total shares for buy and sell orders in CMC being disseminated closer in time to the primary exchanges' cut-off times, this change does not suddenly make the value of such information more valuable or useful in terms of enhancing opportunities for gaming and manipulating the official closing price. The proposed MOC Cut-off Time is one-minute prior to NYSE's cut-off time of 3:50 p.m., and six-minutes prior to Nasdaq's cut-off time of 3:55 p.m. As noted above, today's markets are marked by technological solutions which typically operate in durations of microseconds. In this context, the separation between the CMC MOC Cut-Off Time and that of NYSE's and Nasdaq's is a substantial duration of time, during which much can change in the marketplace, thus limiting the value of information, if any, that can be gleaned from CMC's dissemination of matched shares at 3:49 p.m. Moreover, there are currently controls and processes in place to monitor for manipulative trading activity, such as the supervisory responsibilities and capabilities of exchanges and the expansive cross market surveillance conducted by FINRA. Following approval of this proposal, the Exchange, FINRA and others will continue to surveil for potential manipulative activity and when appropriate, bring enforcement actions against market participants engaged in manipulative trading activity.

B. Self-Regulatory Organization's Statement on Burden on Competition

The Exchange does not believe that the proposed rule change will impose any burden on competition that is not necessary or appropriate in furtherance of the purposes of the Act. Rather, the proposed rule change seeks merely to extend the MOC Cut-Off Time from 3:35 p.m. to 3:49 p.m., enabling all Members to manage their trading for a longer period. The Exchange is not proposing to make any other changes to the CMC process. Moreover, CMC is a voluntary closing match process, and Members are not required to participate in the CMC. Additionally, the proposed rule change applies to equally to all Members. Importantly, based on feedback from CMC users, the proposed MOC Cut-Off Time will not prevent CMC's current user's from participating in CMC, as CMC's current users are technologically equipped to manage a 3:49 p.m. MOC Cut-Off Time, and should they choose to do so, reroute MOC orders not matched in CMC to the primary exchanges' closing auctions.

Furthermore, the Exchange does not believe that the proposed rule change will impose any burden on intramarket competition that is not necessary or appropriate in furtherance of the purposes of the Act. As noted above, the proposed rule change more closely aligns the CMC MOC Cut-Off Time to the cut-off times of other exchanges, while still providing CMC participants with an opportunity to reroute any of their unpaired MOC orders to the primary exchanges. In this regard, the proposed rule change may make CMC a more viable alternative to the primary auctions and should therefore promote competition amongst the exchanges. Additionally, the proposed MOC Cut-Off Time may also enable the Exchange to more effectively compete with off-exchange venues that have cut-off times much closer in time to the market close and comprise a growing percentage of closing volume.

C. Self-Regulatory Organization's Statement on Comments on the Proposed Rule Change Received From Members, Participants, or Others

The Exchange neither solicited nor received comments on the proposed rule change.

III. Date of Effectiveness of the Proposed Rule Change and Timing for Commission Action

Within 45 days of the date of publication of this notice in the Federal Register or within such longer period up to 90 days (i) as the Commission may designate if it finds such longer period to be appropriate and publishes its reasons for so finding or (ii) as to which the Exchange consents, the Commission will:

A. by order approve or disapprove such proposed rule change, or

B. institute proceedings to determine whether the proposed rule change should be disapproved.

IV. Solicitation of Comments

Interested persons are invited to submit written data, views, and arguments concerning the foregoing, including whether the proposed rule change is consistent with the Act. Comments may be submitted by any of the following methods:

Electronic Comments

- Use the Commission's internet comment form (https://www.sec.gov/rules/sro.shtml); or

- Send an email torule-comments@sec.gov. Please include File Number SR-CboeBZX-2022-038 on the subject line.

Paper Comments

- Send paper comments in triplicate to Secretary, Securities and Exchange Commission, 100 F Street NE, Washington, DC 20549-1090.

| Rank | Symbol | Primary exchange | TRF close % inc. PRP 47 |

|---|---|---|---|

| 1 | AAPL | Nasdaq | 9 |

| 2 | T | NYSE | 6 |

| 3 | BAC | NYSE | 10 |

| 4 | INTC | Nasdaq | 5 |

| 5 | MSFT | Nasdaq | 7 |

| 6 | F | NYSE | 9 |

| 7 | PFE | NYSE | 5 |

| 8 | CSCO | Nasdaq | 5 |

| 9 | CMCSA | Nasdaq | 7 |

| ( printed page 52097) | |||

| 10 | WFC | NYSE | 9 |

| Source: Internal Exchange Data. | |||

All submissions should refer to File Number SR-CboeBZX-2022-038. This file number should be included on the subject line if email is used. To help the Commission process and review your comments more efficiently, please use only one method. The Commission will post all comments on the Commission's internet website ( https://www.sec.gov/rules/sro.shtml). Copies of the submission, all subsequent amendments, all written statements with respect to the proposed rule change that are filed with the Commission, and all written communications relating to the proposed rule change between the Commission and any person, other than those that may be withheld from the public in accordance with the provisions of 5 U.S.C. 552, will be available for website viewing and printing in the Commission's Public Reference Room, 100 F Street NE, Washington, DC 20549 on official business days between the hours of 10:00 a.m. and 3:00 p.m. Copies of the filing also will be available for inspection and copying at the principal office of the Exchange. All comments received will be posted without change. Persons submitting comments are cautioned that we do not redact or edit personal identifying information from comment submissions. You should submit only information that you wish to make available publicly. All submissions should refer to File Number SR-CboeBZX-2022-038 and should be submitted on or before September 14, 2022.

For the Commission, by the Division of Trading and Markets, pursuant to delegated authority.[61]

Jill M. Peterson,

Assistant Secretary.