Securities and Exchange Commission

- [Release No. 34-96144; File No. SR-MRX-2022-22]

Pursuant to section 19(b)(1) of the Securities Exchange Act of 1934 (“Act”),[1] and Rule 19b-4 thereunder,[2] notice is hereby given that on October 14, 2022, Nasdaq MRX, LLC (“MRX” or “Exchange”) filed with the Securities and Exchange Commission (“SEC” or “Commission”) the proposed rule change as described in Items I, II, and III, below, which Items have been prepared by the Exchange. The Commission is publishing this notice to solicit comments on the proposed rule change from interested persons.

I. Self-Regulatory Organization's Statement of the Terms of Substance of the Proposed Rule Change

The Exchange proposes to amend MRX's Pricing Schedule at Options 7, Section 7.

The text of the proposed rule change is available on the Exchange's website at https://listingcenter.nasdaq.com/rulebook/mrx/rules, at the principal office of the Exchange, and at the Commission's Public Reference Room.

II. Self-Regulatory Organization's Statement of the Purpose of, and Statutory Basis for, the Proposed Rule Change

In its filing with the Commission, the Exchange included statements concerning the purpose of and basis for the proposed rule change and discussed any comments it received on the proposed rule change. The text of these statements may be examined at the places specified in Item IV below. The Exchange has prepared summaries, set forth in sections A, B, and C below, of the most significant aspects of such statements.

A. Self-Regulatory Organization's Statement of the Purpose of, and Statutory Basis for, the Proposed Rule Change

1. Purpose

On May 2, 2022, MRX initially filed this proposal to amend its Pricing Schedule at Options 7, Section 7, to assess market data fees, which had not been assessed since MRX's inception in 2016.[3] The proposed changes are designed to update data fees to reflect their current value—rather than their value when it was a new exchange six years ago—based on increased market share. Newly-opened exchanges often charge no fees for market data to attract order flow to an exchange, and later amend their fees to reflect the true value of those services.[4] Allowing newly- ( printed page 65274) opened exchanges time to build and sustain market share before charging for their market data encourages market entry and promotes competition.

This Proposal reflects MRX's assessment that it has gained sufficient market share to compete effectively against other 15 options exchanges without waiving market data fees. Such fees are assessed by options exchanges that compete with MRX—indeed, MRX is the only options exchange (out of the 16 current options exchanges) not to assess them today.

As explained in further detail below, MRX in 2022 is in the same position as NYSE National in 2020, when it sought approval for the “NYSE National Integrated Feed.” [5] The Commission approved the NYSE National Integrated Feed based on a finding that it “was subject to significant substitution-based competitive forces” based on “NYSE National's consistently low percentage of market share, the relatively small number of subscribers to the NYSE National Integrated Feed, and the sizeable portion of subscribers that terminated their subscriptions following the proposal of the fees.” [6]

The three factors cited in the Commission's approval order for NYSE National are present in MRX today. First, MRX has a consistently low percentage of market share, starting at approximately 0.2 percent when it opened as an Exchange and ending in approximately 1.8 percent today. Second, only a small number of firms purchase market data from MRX relative to its affiliated options exchanges. Third, a sizeable portion of subscribers—approximately 15 percent—have terminated their subscriptions following the implementation of the proposed fees, demonstrating that customers can and do exercise choice in deciding whether to purchase the Exchange's market data feeds.

Disapproval of the Proposal—given that the three factors cited in the Commission's approval order for NYSE National two years ago are present in MRX today—would result in differential treatment of similarly-situated exchanges. Under such circumstances, disapproval of the Proposal should be rejected as arbitrary and capricious.

Disapproval would also place a substantial burden on competition. MRX would be uniquely disadvantaged as the only options exchange unable to charge for its market data. If the Commission were to disapprove this Proposal, that action, and not market forces, would determine whether MRX is successful in its competition with other options exchanges.

New exchanges commonly waive data fees to attract market participants, facilitating their entry into the market and, once there is sufficient depth and breadth of liquidity, “graduate” to compete against established exchanges and charge fees that reflect the value of their services. If MRX is incorrect in its assessment, that error will be reflected in MRX's ability to compete with other options exchanges.[7]

The Exchange proposes to amend fees for the following market data feeds within Options 7, Section 7: (1) Nasdaq MRX Depth of Market Data Feed (“Depth of Market Feed”); [8] (2) Nasdaq MRX Order Feed (“Order Feed”); [9] (3) Nasdaq MRX Top of Market Feed (“Top Feed”); [10] (4) Nasdaq MRX Trades Feed (“Trades Feed”); [11] and (5) Nasdaq MRX Spread Feed (“Spread Feed”).[12] Prior to the initial filing of these proposed price changes on May 2, 2022, no fees had been assessed for these feeds.

In addition to the proposed fees for each data feed, the Exchange proposes an Internal Distributor Fee [13] of $1,500 per month for the Depth of Market Feed, Order Feed, and Top Feed, an Internal Distributor Fee of $750 per month for the Trades Feed, and an Internal Distributor Fee of $1,000 per month for the Spread Feed. If a Member subscribes to both the Trades Feed and the Spread Feed, both Internal Distributor Fees would be assessed.

The Exchange also proposes to assess an External Distributor Fee of $2,000 per month for the Depth of Market Feed, Order Feed, and Top Feed, an External Distributor Fee of $1,000 per month for the Trades Feed, and an External Distributor Fee of $1,500 per month for the Spread Feed.

MRX will also assess Professional [14] and Non-Professional [15] subscriber fees. ( printed page 65275) The Professional Subscriber will be $25 per month, and the Non-Professional Subscriber will be $1 per month. These subscriber fees (both Professional and Non-Professional) cover the usage of all five MRX data products identified above and would not be assessed separately for each product.[16]

MRX also proposes a Non-Display Enterprise License for $7,500 per month. This license would lower costs for internal professional subscribers and lower administrative costs overall by permitting the distribution of all MRX proprietary direct data feed products to an unlimited number of internal non-display Subscribers without incurring additional fees for each internal Subscriber, or requiring the customer to count internal subscribers.[17] The Non-Display Enterprise License is in addition to any other associated distributor fees for MRX proprietary direct data feed products.

2. Statutory Basis

The Exchange believes that its proposal is consistent with section 6(b) of the Act,[18] in general, and furthers the objectives of Sections 6(b)(4) and 6(b)(5) of the Act,[19] in particular, in that it provides for the equitable allocation of reasonable dues, fees, and other charges among members and issuers and other persons using any facility, and is not designed to permit unfair discrimination between customers, issuers, brokers, or dealers.

The proposed changes to the pricing schedule are reasonable in several respects. As a threshold matter, the Exchange is subject to significant competitive forces in the market for order flow, which constrains its pricing determinations. The fact that the market for order flow is competitive has long been recognized by the courts. In NetCoalition v. Securities and Exchange Commission, the D.C. Circuit stated, “[n]o one disputes that competition for order flow is `fierce.' . . . As the SEC explained, `[i]n the U.S. national market system, buyers and sellers of securities, and the broker-dealers that act as their order-routing agents, have a wide range of choices of where to route orders for execution'; [and] `no exchange can afford to take its market share percentages for granted' because `no exchange possesses a monopoly, regulatory or otherwise, in the execution of order flow from broker dealers'. . . .” [20]

The Commission and the courts have repeatedly expressed their preference for competition over regulatory intervention to determine prices, products, and services in the securities markets. In Regulation NMS, while adopting a series of steps to improve the current market model, the Commission highlighted the importance of market forces in determining prices and SRO revenues, and also recognized that current regulation of the market system “has been remarkably successful in promoting market competition in its broader forms that are most important to investors and listed companies.” [21]

Congress directed the Commission to “rely on `competition, whenever possible, in meeting its regulatory responsibilities for overseeing the SROs and the national market system.' ” [22] As a result, the Commission has historically relied on competitive forces to determine whether a fee proposal is equitable, fair, reasonable, and not unreasonably or unfairly discriminatory. “If competitive forces are operative, the self-interest of the exchanges themselves will work powerfully to constrain unreasonable or unfair behavior.” [23] Accordingly, “the existence of significant competition provides a substantial basis for finding that the terms of an exchange's fee proposal are equitable, fair, reasonable, and not unreasonably or unfairly discriminatory.” [24] In its 2019 guidance on fee proposals, Commission staff indicated that they would look at factors beyond the competitive environment, such as cost, only if a “proposal lacks persuasive evidence that the proposed fee is constrained by significant competitive forces.” [25]

History of MRX Operations

Over the years, MRX has amended its transactional pricing to attract order flow to the Exchange.[26] In June 2019, ( printed page 65276) MRX commenced offering complex orders.[27] With the addition of complex order functionality, MRX offered Members certain order types, an opening process, auction capabilities and other trading functionality that was nearly identical to functionality available on ISE.[28] The added functionality attracted order flow, which has enhanced the value of its market data and is the basis for these proposed fee changes.

Market Data Products Are Subject to Significant Substitution-Based Competitive Forces

An Exchange can show that a product is “subject to significant substitution-based competitive forces” by introducing evidence that customers can substitute that product with products offered by other exchanges.

NYSE National was able to prove exactly this when it sought approval for the “NYSE National Integrated Feed” [29] in 2020. NYSE National at the time of its filing was in a similar position to MRX today—the exchange had an approximately 1.9% market share of executed volume of equity trades.[30] The Commission approved the proposal to establish fees for NYSE National based on a finding that the exchange “was subject to significant substitution-based competitive forces.” Citing NetCoalition I,[31] the Commission stated that “whether a market is competitive notwithstanding potential alternatives depends on factors such as the number of buyers who consider other products interchangeable and at what prices.” [32] Noting that “many market participants . . . do not subscribe to . . . the NYSE National Integrated Feed, even when the feed is offered without charge,” the Commission concluded that “NYSE National's consistently low percentage of market share, the relatively small number of subscribers to the NYSE National Integrated Feed, and the sizeable portion of subscribers that terminated their subscriptions following the proposal of the fees,” demonstrated that the exchange “was subject to significant substitution-based competitive forces” in setting fees such that the proposed rule change was consistent with the Act.[33]

MRX today is in essentially the same position as NYSE National in 2020, and all three of the factors cited in the Commission's approval order for NYSE National are present in MRX today. First, MRX has a consistently low percentage of market share, starting at approximately 0.2 percent when it opened as an Exchange and ending in approximately 1.8 percent today. Second, only a small number of firms purchase market data from MRX relative to its affiliated options exchanges. Third, a sizeable portion of subscribers—approximately 15 percent—have terminated their subscriptions following the implementation of the proposed fees, demonstrating that customers can and do exercise choice in deciding whether to purchase the Exchange's market data feeds.

As of May 2, 2022, the date that MRX initially proposed these market data fees, MRX reported that two customers had terminated their market data subscriptions.[34] As of now, a total of five firms have cancelled, amounting to approximately 15 percent of the 34 customers that had been taking MRX feeds in the first quarter of 2022.[35]

Commission Staff have requested additional information pertaining to: (i) the types of feeds available to these customers prior to termination, (ii) the characteristics of the customers that terminated their feeds, and (iii) whether such customers traded on the Exchange.

With respect to the types of data feeds accessed, two of the five customers had access to all five feeds: the Depth of Market Data, the Order Feed, the Top Feed, the Trades Feed, and the Spread Feed. The three remaining customers had access to only two feeds: the Order Feed and the Top Feed. All five customers cancelled all feeds that they had access to.

With respect to the types of customers cancelling feeds, three of the five were either data vendors or technology suppliers. Data vendors purchase exchange data and redistribute it to downstream customers, while technology suppliers incorporate exchange data into software solutions, which are sold to downstream customers. The remaining two firms engage in options trading, either on their own behalf or that of a customer.

With respect to trading, the three data vendors/technology suppliers do not trade on their own behalf or on the behalf of any downstream customs, although their customers may do so. The Exchange understands that these three firms cancelled due to insufficient demand from their downstream customers for MRX data. The two remaining firms, which do engage in options trading, have not traded on MRX, but are active traders on other Nasdaq options exchanges.[36]

Detailed information supporting the first step in the analysis of substitution-based competitive forces—low market share—is set forth in Chart 1, which shows the January 2022 market share for multiply-listed options by exchange. Of the 16 operating options exchanges, none currently has more than a 13.1% market share, and MRX has the smallest market share at 1.8%. Customers widely distribute their transactions across exchanges according to their business needs and the ability of each exchange to meet those needs through technology, liquidity and functionality. Average market share for the 16 options exchanges is 6.26 percent, with the median at 5.8, and a range between 1.8 and 13.1 percent.

Market share is the percentage of volume on a particular exchange relative to the total volume across all exchanges, and indicates the amount of order flow directed to that exchange. High levels of market share enhance the value of market data.

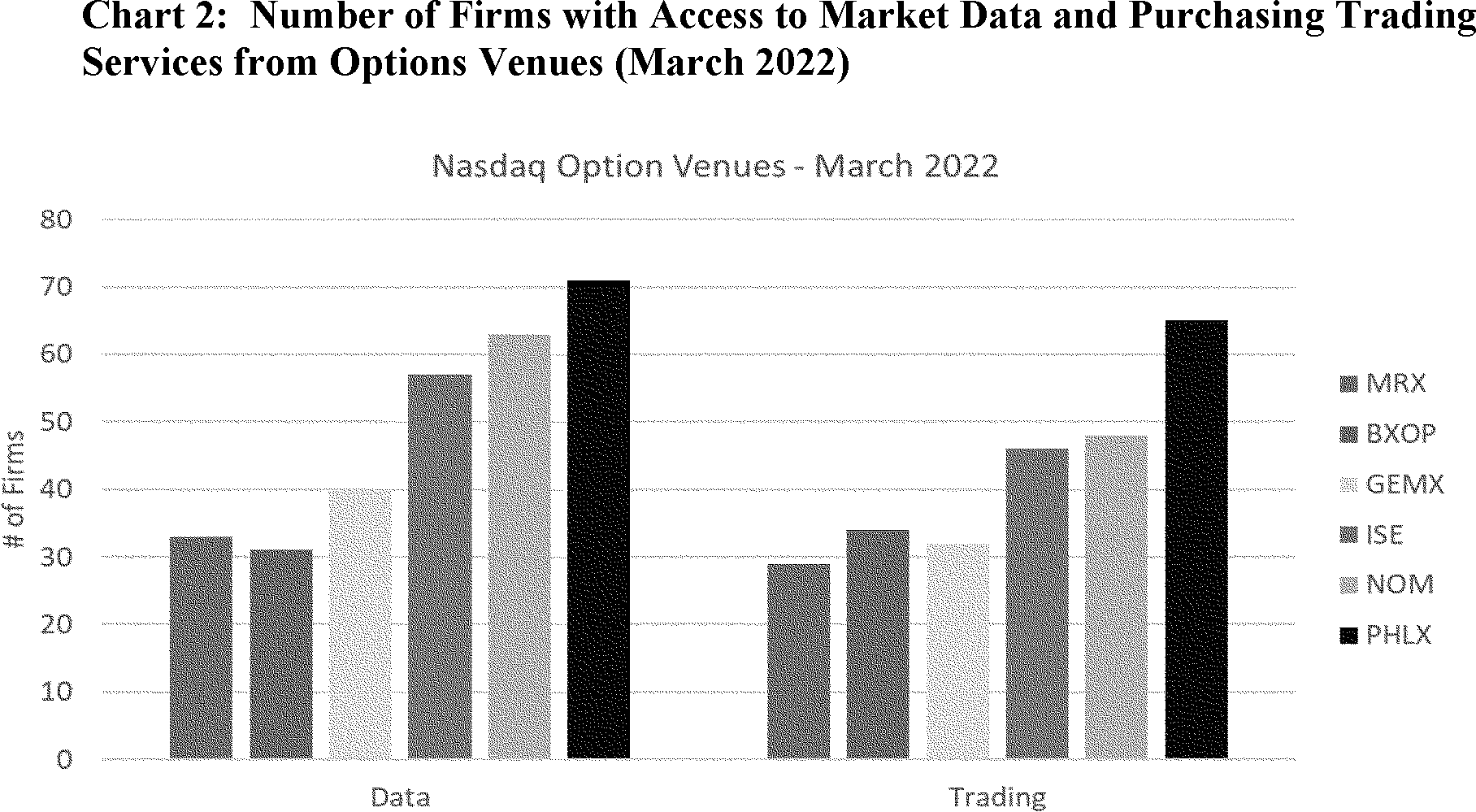

The second step in this analysis—demonstrating that only a small number of firms purchase market data relative to affiliated options exchanges—is shown in Chart 2, which compares the number of firms with access to market data from MRX to the number of firms purchasing market data from the four MRX-affiliated options exchanges, GEMX, ISE, The Nasdaq Stock Market LLC (“NOM”) and Nasdaq PHLX, LLC (“Phlx”).

Chart 2 shows that 34 firms subscribed to at least one market data product from MRX in the first quarter of 2022. This is the second lowest number of firms purchasing market data from the Nasdaq-affiliated options exchanges.

The third step in this analysis—showing that a sizable number of customers terminated subscriptions following the proposal of the fees—is confirmed by the five customer cancellations. As explained above, all five customers terminated all feeds available to them. Although not all customers took all of the MRX feeds, each one of these feeds was cancelled by at least one customer, demonstrating that customers can and do exercise ( printed page 65278) choice with respect to each feed. These cancellations reduced the number of firms with access to at least one MRX market data feed from 34 to 29, an approximately 15 percent reduction in usage, demonstrating that firms can and do exercise choice in determining whether to purchase market data from the Exchange.

MRX lists no proprietary options products that are entirely unique to MRX. Firms can substitute MRX market data with feeds from exchanges that provide a high degree of functionality, including complex orders. Full market data options are available, for example, from Cboe,[37] MIAX,[38] and NYSE Arca Options.[39] Because MRX does not list options on products that are exclusively available on MRX, consumers can substitute MRX data with data from any exchange that lists such multiply-listed options, or through OPRA. Moreover, all broker-dealers involved in order routing must take consolidated data from OPRA, and proprietary data feeds cannot be used to meet that particular requirement. As such, all proprietary data feeds are optional.

This analysis must be viewed in the context of a field with relatively low barriers to entry. MRX, like many new entrants to the field, offered market data for free to establish itself and gain market share. As new entrants enter the field, MRX can also expect competition from these new entrants. Those new entrants, like MRX, are likely to set market data fees to zero, increasing marketplace competition.

The Proposal is not unfairly discriminatory. The five market data feeds at issue here—the Depth of Market Feed, Order Feed, Top Feed, Trades Feed, and Spread Feed—are used by a variety of market participants for a variety of purposes. Users include regulators, market makers, competing exchanges, media, retail, academics, portfolio managers. Market data feeds will be available to members of all of these groups on a non-discriminatory basis.

With respect to the proposed Non-Display Enterprise License, enterprise licenses in general have been widely recognized as an effective and not unfairly discriminatory method of distributing market data. Enterprise licenses are widely employed by options exchanges, and the proposal here is typical of such licenses.

After 6 years, MRX proposes to assess market data fees, just as all other options exchanges do now.[40] These fees will not impede access to MRX, but rather will allow MRX to continue to compete and grow its marketplace so that it may continue to offer a robust trading architecture, a quality opening process, an array of simple and complex order types and auctions, and competitive transaction pricing. If MRX is incorrect in its assessment of the value of its services, that assessment will be reflected in MRX's ability to compete with other options exchanges.

B. Self-Regulatory Organization's Statement on Burden on Competition

The Exchange does not believe that the proposed rule change will impose any burden on competition not necessary or appropriate in furtherance of the purposes of the Act. For all of the reasons set forth above, the Exchange is subject to “significant substitution-based competitive forces”: (i) it has a consistently low percentage of market share, starting at approximately 0.2 percent when it opened as an Exchange and ending in approximately 1.8 percent today; (ii) only a small number of firms purchase market data from MRX relative to its affiliated options exchanges; and (iii) a sizeable portion of subscribers—approximately 15 percent—have terminated their subscriptions following the implementation of the proposed fees, demonstrating that customers can and do exercise choice in deciding whether to purchase market data.

Nothing in the Proposal burdens inter-market competition (the competition among self-regulatory organizations) because approval of the Proposal does not impose any burden on the ability of other options exchanges to compete. Each of the remaining 15 options exchanges currently sells its market data, and is capable of modifying its fees in response to the proposed changes by MRX. Moreover, allowing MRX, or any new market entrant, to waive fees for a period of time to allow it to become established encourages market entry and thereby ultimately promotes competition.

Nothing in the Proposal burdens intra-market competition (the competition among consumers of exchange data) because each customer will be able to decide whether or not to purchase the Exchange's market data, as demonstrated by the fact that a significant number of the Exchange's customers have already elected to terminate their access to such feeds.

The Exchange operates in a highly competitive market in which market participants can readily favor competing venues if they deem fee levels at a particular venue to be excessive. Because competitors are free to modify their own fees in response, and because market participants may readily adjust their order routing practices, the Exchange believes that the degree to which fee changes in this market may impose any burden on competition is extremely limited. If the changes proposed herein are unattractive to market participants, it is likely that the Exchange will lose market share.[41]

C. Self-Regulatory Organization's Statement on Comments on the Proposed Rule Change Received From Members, Participants, or Others

No written comments were either solicited or received.

III. Date of Effectiveness of the Proposed Rule Change and Timing for Commission Action

The foregoing rule change has become effective pursuant to section 19(b)(3)(A)(ii) of the Act.[42]

At any time within 60 days of the filing of the proposed rule change, the Commission summarily may temporarily suspend such rule change if it appears to the Commission that such action is: (i) necessary or appropriate in the public interest; (ii) for the protection of investors; or (iii) otherwise in furtherance of the purposes of the Act. If the Commission takes such action, the Commission shall institute proceedings to determine whether the proposed rule should be approved or disapproved.

IV. Solicitation of Comments

Interested persons are invited to submit written data, views, and arguments concerning the foregoing, including whether the proposed rule change is consistent with the Act. Comments may be submitted by any of the following methods:

Electronic Comments

- Use the Commission's internet comment form (https://www.sec.gov/rules/sro.shtml); or ( printed page 65279)

- Send an email torule-comments@sec.gov. Please include File Number SR-MRX-2022-22 on the subject line.

Paper Comments

- Send paper comments in triplicate to Secretary, Securities and Exchange Commission, 100 F Street NE, Washington, DC 20549-1090.

All submissions should refer to File Number SR-MRX-2022-22. This file number should be included on the subject line if email is used. To help the Commission process and review your comments more efficiently, please use only one method. The Commission will post all comments on the Commission's internet website ( https://www.sec.gov/rules/sro.shtml). Copies of the submission, all subsequent amendments, all written statements with respect to the proposed rule change that are filed with the Commission, and all written communications relating to the proposed rule change between the Commission and any person, other than those that may be withheld from the public in accordance with the provisions of 5 U.S.C. 552, will be available for website viewing and printing in the Commission's Public Reference Room, 100 F Street NE, Washington, DC 20549, on official business days between the hours of 10:00 a.m. and 3:00 p.m. Copies of the filing also will be available for inspection and copying at the principal office of the Exchange. All comments received will be posted without change. Persons submitting comments are cautioned that we do not redact or edit personal identifying information from comment submissions. You should submit only information that you wish to make available publicly. All submissions should refer to File Number SR-MRX-2022-22 and should be submitted on or before November 18, 2022.

For the Commission, by the Division of Trading and Markets, pursuant to delegated authority.[43]

J. Matthew DeLesDernier,

Deputy Secretary.