Reimagining and Improving Student Education-Federal Student Loan Program Final Regulations

The Secretary amends the regulations for the Federal student loan programs authorized under title IV of the Higher Education Act (HEA) of 1965, as amended (the title IV, HEA pro...

Office of Postsecondary Education, Department of Education.

ACTION:

Final rule.

SUMMARY:

The Secretary amends the regulations for the Federal student loan programs authorized under title IV of the Higher Education Act (HEA) of 1965, as amended (the title IV, HEA programs) to implement the statutory changes to the title IV, HEA programs included in Public Law 119-21, the Working Families Tax Cuts Act signed into law by President Trump on July 4, 2025. The Department previously referred to the Working Families Tax Cuts Act as the “One Big Beautiful Bill Act,” including in the Notice of Proposed Rulemaking published on January 30, 2026. These changes include establishing new loan limits for graduate students, professional students, and parents, and phasing out the Graduate PLUS (Grad PLUS) Program. The Working Families Tax Cuts Act also simplifies the current broken and confusing myriad of Federal student loan repayment plans by phasing out the existing Income-Contingent Repayment (ICR) plans, creating a new Tiered Standard repayment plan option, and establishing a new income-driven repayment plan known as the Repayment Assistance Plan. The Working Families Tax Cuts Act also enables borrowers in default who have previously rehabilitated a defaulted loan a second chance to rehabilitate their loan(s) and resume repayment.

DATES:

This final rule is effective on July 1, 2026.

FOR FURTHER INFORMATION CONTACT:

Tamy Abernathy, Office of Postsecondary Education, 400 Maryland Ave. SW, 5th Floor, Washington, DC 20202. Telephone: (202) 245-4595. Email:

Tamy.Abernathy@ed.gov.

If you are deaf, hard of hearing, or have a speech disability and wish to access telecommunications relay services, please dial 7-1-1.

CIP Code: Classification of Instructional Programs Code

DL: Federal Direct Loans

E.O.: Executive Order

FFEL: Federal Family Education Loan Program

FSA: Federal Student Aid

Grad PLUS: Direct PLUS Loan made to graduate or professional students

HEA: Higher Education Act of 1965, as amended

IBR: Income-Based Repayment

ICR Plan: Income-Contingent Repayment plan

NPRM: Notice of Proposed Rulemaking

OIRA: Office of Information and Regulatory Affairs

PRA: Paperwork Reduction Act of 1995

PAYE: Pay As You Earn plan

PDF: Portable Document Format

Parent PLUS: Direct PLUS Loan made to parents of dependent undergraduate students

PSLF: Public Service Loan Forgiveness

RAP: Repayment Assistance Plan

RFA: Regulatory Flexibility Act

RIA: Regulatory Impact Analysis

Title IV, HEA Programs: Student financial assistance programs authorized under title IV of the HEA

rtf: Rich Text Format

RISE: Reimagining and Improving Student Education

SAVE Plan: Saving on a Valuable Education plan

SBREFA: Small Business Regulatory Enforcement Fairness Act of 1996

txt: text format

II. Executive Summary

The Secretary implements the amendments made to the HEA relating to the Federal student loan programs made by Public Law 119-21, the Working Families Tax Cuts Act, through these final regulations.

These regulations revise the Direct Loan Program under 34 CFR part 685 by amending the annual and aggregate loan limits for graduate, professional, and parent loan borrowers. The regulations also implement two new streamlined student loan repayment plans, the Repayment Assistance Plan and the Tiered Standard repayment plan. The regulations also make conforming amendments to current regulations on consolidation, deferment, forbearance, and Public Service Loan Forgiveness (PSLF). The regulations also provide borrowers in default a second opportunity to rehabilitate their loans and resume repayment, even if they previously rehabilitated a defaulted loan.

1. Summary of Major Provisions of This Regulatory Action

These final regulations:

Amend §§ 674.39, 682.215, and 682.405 to allow loan rehabilitation up to twice per each loan borrowed under the Federal Perkins Program, Federal Family Education Loan Program, and the Direct Loan Program, up from only one.

Amend § 685.102 to include new definitions for the following terms: expected time to credential, graduate student, professional student, and program length.

Amend § 685.200 to include Direct PLUS Loan eligibility for graduate and professional students.

Amend § 685.201 to establish the limited Direct PLUS Loan eligibility for a graduate or professional student.

Amend § 685.203 to include new Direct Loan annual and aggregate limits, create a new lifetime maximum aggregate limit, establish less than full-time reduction of annual loan limits, and permit institutions to limit borrowing for specific programs.

Amend § 685.204 to clarify conditions and borrower eligibility for the unemployment deferment and the economic hardship deferment.

Amend § 685.205 to establish the modified eligibility criteria for borrowers to receive a forbearance.

Amend § 685.208 to establish the terms for the Tiered Standard repayment plan, set the minimum payment for the Tiered Standard repayment plan, and restructure each Fixed repayment plan's terms under their respective plan.

Amend § 685.209 to establish terms for the Repayment Assistance Plan and sunset ICR plans and conditions.

( printed page 23769)

Amend § 685.210 to provide information to borrowers about choosing a repayment plan.

Amend § 685.211 to establish miscellaneous repayment provisions including the minimum payment increase for the Income-Based Repayment (IBR) plan.

Amend § 685.219 to clarify that repaying under the Repayment Assistance Plan will qualify for PSLF if all other eligibility criteria are met.

Amend § 685.220 to provide terms and repayment plan eligibility for consolidation loans.

Amend § 685.221 to clarify when a borrower may be eligible for an alternative repayment plan.

Amend § 685.303 to waive the substantially equal disbursement requirement for an institution when a borrower has less than full-time enrollment for the academic year and is subject to the schedule of reductions.

The regulations in this final rule consider each change to be a discrete change and independent from the other changes. Consistent with 34 CFR 685.109, “[i]f any provision of this subpart or its application to any person, act, or practice is held invalid, the remainder of the subpart or the application of its provisions to any person, act, or practice will not be affected thereby.”

2. Summary of Costs and Benefits

As further detailed in the

Regulatory Impact Analysis

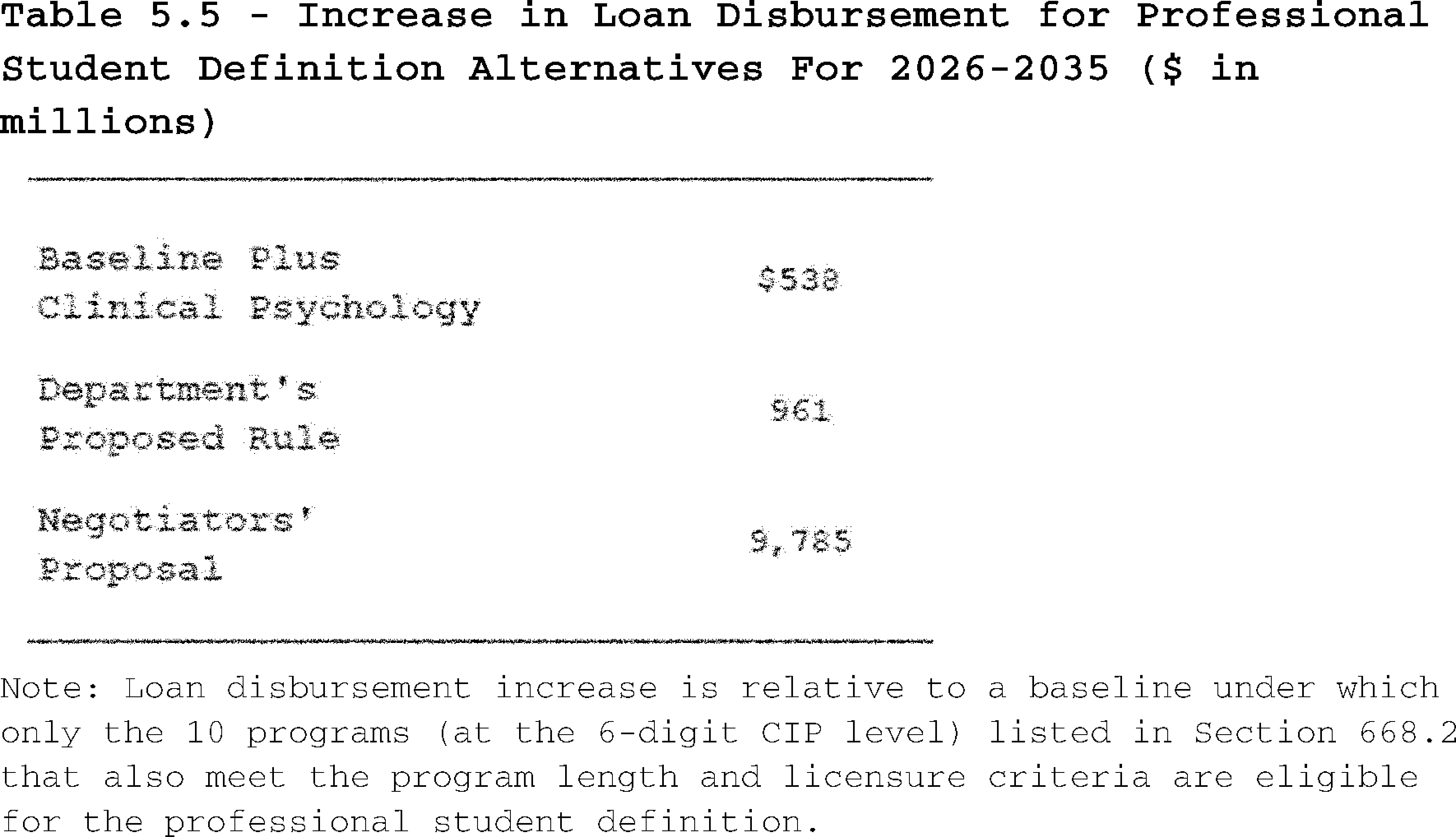

(RIA), the Department estimates a net budget impact compared to the President's Budget baseline for FY 2026 of −$409.3 billion from cohorts 1994 to 2035 for all provisions except the professional student definition. This is equivalent to an annualized reduction in transfers of −$42.3 billion at 3 percent discounting and −$44.3 billion at 7 percent discounting. The professional student definition had an estimated net budget impact of $537 million for loan cohorts 2027-2036 compared to the President's Budget for PB2027 baseline, equivalent to $51 million and $52 million at 3 percent and 7 percent discounting, respectively. Additionally, we estimate annualized cost related to paperwork burden ($25.0/$37.2 million), administrative updates to Government systems ($10.4/$12.1 million), systems maintenance and operation costs ($7.4/$7.8 million) and staffing ($5.5/$6.0 million) at 3 percent and 7 percent discounting, respectively.

As also further detailed in the RIA, these final regulations provide benefits to students, borrowers, and taxpayers. These benefits include potentially lower tuition costs for students, simplified repayment terms for student loan borrowers, and lower costs for taxpayers.

III. Purpose of This Regulatory Action

This regulatory action seeks to effectuate regulations that address the statutory changes made by the Working Families Tax Cuts Act.

IV. Background

Public Law 119-21, which the Department refers to as the “Working Families Tax Cuts Act,” was signed into law by President Trump on July 4, 2025. This landmark legislation makes extensive statutory changes to fix broken and unnecessarily complex aspects of the Federal student loan programs, specifically, in the areas of loan limits, repayment plans, and related provisions in title IV of the HEA. Among other changes, the Working Families Tax Cuts Act sets a new lifetime borrowing cap ($257,500 for most borrowers), eliminates the authority to disburse new Graduate PLUS Loans, limits borrowing under the PLUS program for parents, maintains current annual limits under the Federal Direct Stafford Loan Program for undergraduate and graduate students, increases annual Federal Direct Stafford loan limits for professional degree students, establishes aggregate limits for graduate students, professional degree students, and parents of undergraduates, and reduces annual loan amounts for students enrolled less than full-time. For repayment, the Working Families Tax Cuts Act simplifies and streamlines the current confusing patchwork of repayment plan options for future borrowers to two flexible options: a new Tiered Standard repayment plan for fixed monthly payments over a 10 to 25-year term, and a new income-driven plan called the Repayment Assistance Plan that allows borrowers the opportunity to actually pay down their student loan debt by preventing negative amortization over the life of the loan. Confusing, outdated (and in some cases, unlawful) repayment plans are phased out, including the Income-Contingent Repayment plan (ICR), Pay As You Earn plan (PAYE), and Saving on a Valuable Education plan (SAVE), which has been held as unlawful in Federal court.

See Missouri

v.

Biden,

112 F.4th 531, 538 (8th Cir. 2024).

This final rule complies with Section 492 of the HEA, which requires the Secretary to obtain public input and conduct negotiated rulemaking before issuing proposed regulations for the title IV, HEA programs. To meet those requirements and implement the new statutory directives provided for in the Working Families Tax Cuts Act, the Department convened the Reimagining and Improving Student Education (RISE) negotiated rulemaking committee (Committee). The Committee was composed of representatives from institutions, students and borrowers, State officials, financial aid administrators, loan servicers, and consumer and civil rights organizations. The Committee met over multiple sessions with the first session being from September 29 through October 3, 2025, and the second session being held November 3-6, 2025. The Committee reached consensus on the entirety of the regulatory text. In accordance with the protocols established by the Committee, the Department incorporated the regulatory amendatory text that was mutually agreed upon into a Notice of Proposed Rulemaking (NPRM) published on January 30, 2026. Building on the statutory and regulatory history, the Committee's consensus language, and the public comments received, this final rule amends Direct Loan regulations to the changes enacted in the Working Families Tax Cuts Act by revising loan limit provisions, restructuring repayment options (including IBR and adding the new Repayment Assistance Plan), updating PSLF eligibility and qualifying payment rules, and aligning consolidation, deferment, forbearance, and borrower relief provisions with the revised statutory framework.

V. Authority for This Regulatory Action

Congress passed legislation that amended statutory provisions governing programs administered by the Department, and this final rule implements those changes in the Department's regulations. The Working Families Tax Cuts Act amended portions of the HEA related to the Federal student loan programs administered by the Department. The Secretary has been granted the broad authority by Congress to implement Federal student aid programs under title IV of the HEA, including amendments made by the Working Families Tax Cuts Act.

See20 U.S.C. 1221e-3,

see

also 20 U.S.C. 1082, 3441, 3474, 3471. In order to carry out functions otherwise vested in the Secretary by law or by delegation of authority pursuant to law, and subject to limitations as may be otherwise imposed by law, the Secretary is authorized to make, promulgate, issue, rescind, and amend rules and regulations governing the manner of operations of, and governing the applicable programs administered by, the Department.

See20 U.S.C. 1221e-3. These programs include the Federal

( printed page 23770)

student loan programs authorized by the HEA.

Waiver of HEA Master Calendar Requirements

Congress may waive, modify, or rescind requirements in the HEA and Administrative Procedure Act (APA) that require the Department to follow certain processes and procedures when engaging in informal notice-and-comment rulemaking.

See, e.g., Asiana Airlines

v.

F.A.A.,

134 F.3d 393, 398 (D.C. Cir. 1998);

Methodist Hospital of Sacramento

v.

Shalala,

38 F.3d 1225, 1237 (D.C. Cir. 1998) (finding that certain parts of the APA procedural framework had been waived when Congress gave an agency direction that conflicts with and is irreconcilable with the APA).

At the same time, the court in

Asiana Airlines

made clear that the APA requires “clear intent” from Congress to justify a departure from the procedural requirements in the APA, noting that 5 U.S.C. 559 requires an explicit waiver of APA procedural requirements. Here, the Department is complying with all of the requirements for informal notice-and-comment rulemaking in 5 U.S.C. 553, so an express waiver is not needed. The explicit waiver standard in 5 U.S.C. 559 only applies to the procedural requirement of the APA and does not apply to the Master Calendar provision in Section 482(c) the HEA. Had Congress wished for the HEA Master Calendar provision to have the same rule of construction as it does for procedural requirements of the APA, we would have expected that Congress would either cross reference and incorporate 5 U.S.C. 559 into the HEA or use similar language to 5 U.S.C. 559 within Section 482(c) of the HEA. Congress knows how to create these types of special rules of construction when they want to, and they declined to do so in Section 482(c) of the HEA.

Absent an explicit rule of construction in the HEA, we rely on the ordinary tools of statutory interpretation to glean the meaning of the statute. The Harmonious-Reading Canon provides that statutes should, when possible, be interpreted in a way that renders them compatible, not contradictory, but such an approach is not always possible if context and other considerations (including the application of other canons) make it impossible to do so, another approach to statutory interpretation, such as the General/Specific Canon must be applied.

See

Scalia & Garner,

Reading Law,

155 (2012). The General/Specific Canon dictates that, in cases where a general prohibition is contradicted by a specific permission or a general permission that is contradicted by a specific prohibition, the more specific of the two provisions controls.

Id.

at 158. Because, as discussed below, the Working Families Tax Cuts Act contains provisions with effective dates that cannot possibly be implemented in regulation in accordance with the HEA's master calendar requirements, and as such, implicitly provides a limited waiver of the HEA's master calendar requirement, so far as it is necessary to promulgate regulations that give effect to those provisions.

See Dorsey

v.

United States,

567 U.S. 260, 274 (2012) (stating that an agency's compliance with an existing statute “cannot justify a disregard of the will of Congress as manifested either expressly or by necessary implication in a subsequent enactment” (

quoting Great Northern R. Co.

v.

United States,

208 U. S. 452, 465 (1908)).

Here, the Working Families Tax Cuts Act was enacted on July 4, 2025. The Working Families Tax Cuts Act directs the Department to implement roughly a dozen provisions by July 1, 2026. Many of these provisions are not self-executing and could not be implemented absent the Department promulgating regulations to provide details for institutions on how to comply with the Working Families Tax Cuts Act. Congress gave the Secretary discretion within the Working Families Tax Cuts Act to implement the provisions impacting the title IV, HEA programs and knew that its commands were not self-executing when directing the Secretary to take action. Congress expected the Secretary to act via rulemaking before July 1, 2026, to enable these provisions to actually go into effect.

The master calendar in the HEA provides that regulatory changes initiated by the Secretary affecting the title IV, HEA programs must be published in final form by November 1st in order for them to go into effect by July 1st of the following year. 20 U.S.C § 1089(c)(1). Section 492 of the HEA requires the Department to undertake negotiated rulemaking as part of any regulation under title IV of the HEA. In order to conduct negotiated rulemaking and meet APA requirements, the Department must have a public hearing (providing notice to the public), solicit nominations from the public to serve on a negotiated rulemaking Committee, select non-Federal negotiators, hold negotiations, develop an NPRM, publish an NPRM (with at least a 30-day comment period), and then publish a final rule that responds to any substantive comments received. The fastest possible timeframe in which the negotiated rulemaking process for the rulemaking packages assigned to the RISE Committee could have occurred is 149 days, which is irreconcilable with the timeline allowed by the enactment of the Working Families Tax Cuts Act, due to the fact that there were 120 days from July 4, 2025, (the day the Working Families Tax Cuts Act was enacted), through and including November 1, 2025, (the publication date of the final rule required by the master calendar).

It would not have been possible for the Department to undertake every step of the negotiated rulemaking process by November 1, 2025, in order to implement the provisions that become effective in the Working Families Tax Cuts Act by July 1, 2026, which is the statutory effective date. Congress was aware of this temporal impossibility when they passed the Working Families Tax Cuts Act, yet Congress decided that these provisions would still go into effect on July 1, 2026. Because these provisions are not self-implementing and cannot go into effect unless the Department promulgates a final rule, the Working Families Tax Cuts Act implicitly waives the master calendar.

With important details unanswered by the plain text of the Working Families Tax Cuts Act, it is clear that the policy scheme set forth in the HEA made by the Working Families Tax Cuts Act cannot be implemented absent regulatory action by the Department. At the same time, even though the requirements of negotiated rulemaking are onerous, it is possible to undergo negotiated rulemaking and publish a final rule at least 30 days prior to the effective date of these Working Families Tax Cuts Act provisions on July 1, 2026. Therefore, the Working Families Tax Cuts Act does not waive negotiated rulemaking nor any provision in the APA. For provisions in the Working Families Tax Cuts Act that become effective July 1, 2027, and beyond, Congress did not implicitly repeal the master calendar because it is possible for the Department to publish a final rule that complies with the master calendar to implement those provisions.

Severability

“It is axiomatic” that a regulation may be invalid in part but not in whole or as applied to one set of facts but not another.

Ayotte

v.

Planned Parenthood of N. New England,

546 U.S. 320, 329 (2006). If a court finds one part of a regulation is unlawful, the “normal rule” is to enjoin only that part.

Id.

(quoting

Brockett

v.

Spokane Arcades, Inc.,

472 U.S. 491, 504 (1985). It is the Department's intent that if any provision of this subpart or its

( printed page 23771)

application to any person, act, or practice is held invalid, the remainder of the subpart or the application of its provisions to any person, act, or practice shall not be affected thereby. Statutes and regulations are severable if the separate provisions are “wholly independent of each other” and can operate independently.

Brockett

v.

Spokane Arcades, Inc.,

472 U.S. 491, 502 (1985). That is the case here. No part herein will be affected if another part is found to be unlawful. Nor does the Department believe courts or regulated parties would be unable to apply the rule if one part is held invalid.

C.f. Dep't of Educ.

v.

Louisiana,

603 U.S. 866, 868 (2024) (per curiam) (denying the government's request to stay a preliminary injunction against an entire rule where only parts were found to be invalid because “schools would face in determining how to apply the rule for a temporary period with some provisions in effect and some enjoined”). In particular, the Department believes that the classification degrees between “professional” or “graduate” degrees is severable. For the reasons discussed in the rule, the Department is confident in how we classified the degrees that commenters and negotiators argued were “professional.” However, if a court disagrees with our analysis, we believe and intend that this portion of the regulation is entirely severable and does not substantially impact any other portion of the regulation or any other part of this final rule. Relatedly, if a court disagrees with the Department's classification of a particular degree or degrees, the Department intends for its classification of all other degrees to survive and remain in effect.

VI. Analysis of Public Comment and Changes

On January 30, 2026, the Secretary published an NPRM for these regulations in the

Federal Register

(91 FR 4254) (January 30, 2026). The Department received 80,793 comments on the proposed regulations. The Department has grouped the comments by the regulatory section and by similar themes. We discuss substantive issues under the sections of the regulations to which they pertain. In instances where individual submissions appeared to be duplicates or near-duplicates of comments prepared as part of a write-in campaign, the Department posted one representative sample comment along with the total comment count for that campaign to

www.Regulations.gov,

which continues to be our standard practice. We considered these comments along with all the other comments received. In instances where individual submissions were bundled together (submitted as a single document or packaged together), the Department posted all the substantive comments included in the submissions along with the total comment count for that document or package to

www.Regulations.gov.

Generally, we do not address minor, non-substantive changes (such as renumbering paragraphs, adding a word, or typographical errors) within this final rule. Additionally, we generally do not address changes or comments recommended by commenters that the statute does not authorize the Secretary to make (such as forgiving all student loans), or comments pertaining to operational processes. Analysis of the comments and of any changes in the regulations since publication of the NPRM (91 FR 4254) follows.

1. Process for Out-of-Scope Comments

The Department does not typically address comments that are out of scope. For purposes of this final rule, out-of-scope comments are those that are not addressed in the NPRM (91 FR 4254) altogether. Generally, comments that are outside of the scope of the NPRM (91 FR 4254) are comments that do not discuss the content or impact of the proposed regulations or the Department's evidence or reasons for the proposed regulations.

Public Comment Period

Comments:

Several commenters requested the Department extend the comment period and some requested we hold hearings so that students, educators, and employers in counseling fields can testify regarding real world impact of the proposed regulations on the mental health profession, students, and the public.

Discussion:

Prior to publishing the NPRM (91 FR 4254), the Department solicited public input through a public hearing held on August 7, 2025, from 9:00 a.m. to 4:00 p.m. Eastern Time, including a lunch break from 12:00 p.m. to 1:00 p.m. All individuals who requested to speak were accommodated during the hearing. The Department also solicited public comments for 30 days and received 1,846 comments on the public hearing notice, which informed the development of the proposed regulations.

Following the public hearing, the Department convened a negotiated rulemaking Committee in fall 2025, consistent with the requirements of the HEA. The Department selected non-Federal negotiators representing affected constituencies and stakeholders. This negotiated rulemaking process provided additional opportunities for stakeholders to offer feedback prior to publication of the NPRM (91 FR 4254).

After publication of the NPRM (91 FR 4254), the Department provided a 30-day public comment period, which is consistent with the Department's obligations under the APA. During that period, the Department received 80,793 public comments, many of which included detailed and substantive feedback. The Department carefully reviewed these comments to determine whether clarification or revisions to the final regulations were appropriate.

Although some commenters requested that the Department extend the comment period or hold additional hearings, the Department believes that the opportunities for stakeholder engagement, including the public hearing, negotiated rulemaking sessions, and the NPRM (91 FR 4254) comment period provided the public with sufficient opportunity to comment on the proposed regulations.

Changes:

None.

General Agreement With the Regulations

Comments:

Many commenters supported the Department's proposed rule and its broader efforts to reform the Federal student loan system. Commenters stated that the current system has created long-term financial challenges for many borrowers and that such reforms are necessary to better align repayment structures with borrowers' financial realities. These commenters noted that excessive student loan debt may affect borrowers' ability to achieve financial stability, including purchasing homes, starting families, or pursuing certain career opportunities. Commenters supported reforms that would simplify repayment options, improve borrower protections, and provide borrowers with clearer and more manageable repayment options for their Federal student loans.

Discussion:

The Department appreciates the commenters' support for the proposed rule and their perspectives regarding the need to improve the Federal student loan system. As discussed in the NPRM (91 FR 4255), the Department proposed these regulatory changes to implement the Working Families Tax Cuts Act's statutory requirements and to improve the clarity and administration of Federal student loan programs. Simplifying repayment choices and improving borrower protections helps borrowers better understand their repayment obligations and remain in good standing on their loans.

Changes:

None.

( printed page 23772)

Comments:

Several commenters supported provisions in the regulations that would limit or restructure certain Federal student loan programs, including changes affecting borrowing limits and loan availability. These commenters stated that unlimited or excessive borrowing may contribute to rising tuition prices and may result in borrowers taking on debt that is difficult to repay relative to actual earnings. Some commenters noted that certain graduate programs may lead to relatively modest salaries and suggested that establishing reasonable borrowing limits may encourage students to make more informed borrowing decisions and encourage institutions to control educational costs.

Discussion:

The Department acknowledges commenters' views regarding borrowing limits and the relationship between borrowing levels and expected earnings. The Department notes that the regulatory provisions in this rulemaking implement the statutory changes in the Working Families Tax Cuts Act and are intended to support responsible borrowing while maintaining access to Federal student loans. Taken together with the other important changes made to the title IV, HEA programs, the new regulatory framework established in these final rules supports program integrity while continuing to provide the financial assistance needed by students pursuing higher education.

Changes:

None.

Comments:

Other commenters discussed the importance of maintaining access to Federal student aid programs for individuals seeking to pursue or advance their education. These commenters stated that Federal student loan programs play an important role in allowing students to obtain professional credentials and access career opportunities that may otherwise be financially out of reach. Some commenters also emphasized the importance of ensuring that borrowers have access to repayment options that are understandable and accessible so that borrowers can successfully remain in repayment and avoid default. Several commenters encouraged the Department to establish clear guidance and implementation support for borrowers and institutions.

Discussion:

The Department supports continued access to Federal student aid for students with financial need and helping borrowers successfully repay their loans and avoid default. The Department believes these regulations balance the need to provide financial support through the Federal student loan programs to students who may otherwise be unable to access postsecondary education while also providing necessary restrictions to prevent accumulation of debt a borrower may never be able to repay. The Department will continue to provide guidance and support to borrowers and institutions to facilitate implementation of the regulatory changes, including additional details on the two new repayment plans that streamline repayment. The Department believes that the changes made in these final regulations will help improve title IV, HEA program administration and improve a borrower's understanding of their repayment obligations.

Changes:

None.

General Opposition to the Regulations

Comments:

Some commenters opposed the proposed regulatory changes described in the NPRM (91 FR 4254). Commenters stated that the proposed regulations could weaken borrower protections, increase financial hardship, and make repayment less affordable. Commenters also expressed concern that these changes could disproportionately affect borrowers with low incomes and borrowers from historically underserved communities. Some commenters asserted that the proposed changes could discourage individuals from pursuing higher education or entering certain professions.

Discussion:

The Department appreciates the commenters' views regarding the potential impact of the proposed regulatory changes on borrowers. However, the Department proposed these changes to implement the Working Families Tax Cuts Act statutory requirements and to improve the administration and sustainability of the Federal student aid programs. The Department believes the final regulations implement the law while appropriately balancing borrower support with program integrity considerations.

Changes:

None.

Comments:

Several commenters stated that the proposed changes could increase financial hardship for borrowers who are also caregivers, experiencing unemployment, illness, or other economic disruptions. Commenters expressed concern that limiting borrower relief options could reduce borrowers' ability to manage temporary financial challenges.

Discussion:

The Department recognizes that borrowers may experience periods of financial hardship and acknowledges the importance of certain safeguards in the repayment process that could provide flexibility. The Department notes that the Federal student loan programs continue to include repayment options designed to help borrowers manage repayment obligations based on their financial circumstances. Depending on the borrower's personal circumstances, borrowers may enroll in various income-driven repayment plans, forbearance, or deferments in accordance with the HEA.

Changes:

None.

Comments:

Some commenters stated that the proposed regulatory changes could discourage individuals from pursuing higher education due to concerns about Federal student loan borrowing limits, repayment affordability, and financial risk.

Discussion:

The final regulations are consistent with the Working Families Tax Cuts Act's statutory requirements to curb excessive borrowing and support the improved administration of the Federal student loan programs. Contrary to the commenters' claims, the changes in this final rule, such as the simplification of the confusing myriad of borrower repayment plans, other complicated requirements, and implementation of the new Repayment Assistance Plan, address long-standing past criticisms and failures of the Federal student loan programs.

Changes:

None.

Comments:

A commenter requested that the Department align implementation of these regulations with the Administration's broader goal of supporting American workers.

Discussion:

The proposed regulations implement the statutory framework enacted in the Working Families Tax Cuts Act and are intended, among other objectives, to promote affordability, reduce the risk of unmanageable borrowing burdens, and deliver measurable results, thereby complementing and supporting key elements of the Administration's America's Talent Strategy to reindustrialize the United States.

Changes:

None.

Negotiated Rulemaking

Comments:

Some commenters expressed concerns about the integrity, security, and reliability of the public comment submission process and questioned whether comments would be reviewed in a transparent and impartial manner. Commenters stated that some stakeholders may fear professional repercussions for submitting dissenting views, which could chill participation. Several commenters who submitted comments anonymously requested assurances that comments would be protected, verified, and meaningfully

( printed page 23773)

considered and asked the Department to identify the offices responsible for reviewing comments, the criteria used to evaluate comments, and how the Department would demonstrate that input was weighed objectively and in good faith.

Discussion:

The Department reviewed all comments, including comments that were submitted anonymously, that were received by the deadline in response to the NPRM and conducted a multi-step review process in which every comment was read, cataloged, and analyzed based on the issues raised and the supporting rationale and evidence provided. In addition, Department staff with relevant subject-matter expertise, including staff from the Office of Postsecondary Education, Office of the General Counsel, Office of the Under Secretary, Office of the Chief Economist, and Federal Student Aid, conducted a comprehensive review and analysis to identify significant comments submitted in response to the NPRM. The Department's responses in this preamble reflect careful consideration of those issues and concise general statements explaining how stakeholder input informed the Department's policy determinations.

Changes:

None.

Comments:

Several commenters commended the Department for engaging in the negotiated rulemaking process and inviting public input for these significant changes. One commenter believed our proposals reflected a reasonable exercise of our authority under the negotiated rulemaking process.

Discussion:

We appreciate the commenters' support and likewise acknowledges the work of the RISE Committee in reaching consensus on regulatory text, which underlies this final rule.

Changes:

None.

Comments:

Some commenters expressed dissatisfaction with our negotiated rulemaking process. Some of these commenters believed we addressed too many complex issues at once. Other commenters believed our timeline to make the system and operational changes by the implementation date to be aggressive and unreasonable.

Discussion:

We disagree with these commenters. Since the enactment of the Working Families Tax Cuts Act, the Department has engaged with the community in a transparent manner about the statutory changes to the title IV, HEA programs. Although there were various issues under the RISE Committee's purview, the Department believes the scope and breadth of the rulemaking process was manageable. The Department often negotiates many topics during the negotiated rulemaking process. In many prior negotiations, the Department had a very wide array of topics that were negotiated—often times, all unrelated to one another. By contrast, the RISE Committee's negotiations focused exclusively on student loans and related provisions. Other changes enacted by the Working Families Tax Cuts Act, such as the establishment of Workforce Pell Grants and a new accountability standard tied to low earning outcomes, were considered by a separate negotiated rulemaking Committee.

With respect to system and operational changes, as we state in the

Analysis of Public Comments and Changes

section of this document, we generally do not address changes or comments pertaining to operational processes. However, we encourage affected parties to monitor our websites for the latest updates.

Changes:

None.

Comments:

One commenter noted that we had an inaccessible docket on

regulations.gov.

Discussion:

We disagree with the claim that the docket was inaccessible on

regulations.gov.

The Department reviewed the docket and determined the link that we published in the

Federal Register

(91 FR 4254) was to a summary that is required to be included in the docket. Specifically, the Providing Accountability Through Transparency Act of 2023 requires agencies to publish the URL where a plain language summary of the proposed rules may be found.

Throughout the public comment period, over 81,000 other commenters were able to successfully submit comments. If the commenter believed they were unable to submit a comment, we provided clear instructions in the NPRM (91 FR 4254) that if a commenter cannot otherwise submit their comments via

Regulations.gov, to contact

regulationshelpdesk@gsa.gov

or by phone at 1-866-498-2945.

Changes:

None.

Comments:

Some commenters advocated adding certain constituency groups in the negotiated rulemaking process, including certain health professionals. These commenters urged us to engage and consult with experts from different backgrounds before implementing changes.

Discussion:

On July 25, 2025, the Department published a notice in the

Federal Register

(90 FR 31836) announcing its intention to establish a negotiated rulemaking committee to prepare proposed regulations for these issues. The notice set forth a schedule for the committee meetings and requested nominations for individual negotiators to serve on the RISE Committee. As we stated in that solicitation and request for nominations, we select individual negotiators with demonstrated experience in the relevant subjects under negotiation in accordance with Section 492(b)(1) of the HEA. We established a committee that allowed significantly affected parties to be represented while at the same time keeping the Committee size manageable. As with all other Committee representatives, each of these constituencies had primary representatives and alternates. The Department believes it identified the appropriate constituency groups involved in the title IV, HEA program regulations being negotiated by the Committee. Further, interested parties had several opportunities to be involved with the rulemaking process, including by submitting written comments on the proposed rule during the comment period we established prior to negotiated rulemaking and during the public comment period on the proposed rule. In fact, the number of written comments the Department received, including those from the health professions community, demonstrates the opportunity we provided for public participation in the process. Additionally, the full negotiated rulemaking Committee reached agreement on its protocols, including the composition of the primary negotiators.

Changes:

None.

Comments:

Several commenters urged us to delay implementation of these regulations. These commenters stressed the need for more time to comply with the regulations or to allow for a transition to help make certain that affected borrowers are not harmed by these regulations.

Discussion:

As we stated in the NPRM (91 FR 4254), within the Working Families Tax Cuts Act enacted on July 4, 2025, the vast majority of the regulatory provisions have an effective date by July 1, 2026, and Congress expected the Secretary to act via rulemaking before July 1, 2026, to enable the various provisions to go into effect in accordance with statutory deadlines (91 FR 4254). Affected stakeholders will have had nearly a year since enactment of the Working Families Tax Cuts Act to assess the potential effects of the statutory provisions and to begin planning any necessary policy and operational changes.

Changes:

None.

( printed page 23774)

Legal Authority/Department Authority

Comment:

One commenter requested that the Department classify this final rule as a major rule under the Congressional Review Act and allow for full congressional review.

Discussion:

The Office of Information and Regulatory Affairs has already classified this final rule as a major rule, and as such, will have at least a 60-day review period prior to the effective date. This information is clearly reflected in the preamble in the Regulatory Analyses section.

Changes:

None.

Comments:

Some commenters noted their belief that revoking or changing the terms of a borrower's loan after they signed an agreement to those terms is dishonest and wrong. These commenters point out that when borrowers took out student loans, they signed an agreement with the understanding that the terms and conditions would remain the same.

Discussion:

We disagree with these commenters. We note that the legally binding instrument upon origination of a Federal student loan is the master promissory note (MPN). The MPN contains the legally binding terms and conditions, including a section on the Borrower's Rights and Responsibilities (BRR) stipulated under the HEA. By signing the MPN, borrowers agree to the terms and conditions of the loans while acknowledging that terms and conditions of those loans may be changed. The MPN explicitly states that its terms and conditions “are determined by the HEA and other Federal laws and regulations” and the BRR further clarifies that subsequent amendments to the HEA and other Federal laws could amend the terms of the MPN. Therefore, by signing the MPN, and as explicitly stated in the BRR section of the MPN, the borrower acknowledges amendments to the HEA may change the terms of the MPN. The borrower also acknowledges that any amendment to the HEA that changes the terms of the MPN will be applied to the borrower's loans in accordance with the effective date of the amendment. Depending on the effective date of the amendment, amendments to the HEA may modify or remove a benefit that existed at the time that a borrower signed the MPN.

This is not a new concept as Congress has changed the terms and conditions of title IV loan programs numerous times, including for borrowers who had already taken out loans. As we also explain in the PSLF final rule (90 FR 48978), the MPN disclaims the notion that terms and conditions of Federal student loans are fixed and can only be changed through the legal process. The legal process here is through the legislative changes enacted by Congress and signed by the President. Here, the statutory changes to the HEA mandate that we provide these revised terms and conditions.

Changes:

None.

Comment:

For purposes of the interim exception, one association requested clarification regarding the treatment of existing borrowers whose Direct Unsubsidized Loan MPNs expire after July 1, 2026. This commenter inquired if a current borrower signs a new MPN on or after July 1, 2026, if that borrower would remain subject to the prior terms applicable at the time of their original borrowing or by the new terms. This commenter maintained that clarification is necessary to make certain that institutions can accurately and effectively counsel borrowers.

Discussion:

As stated above, the MPN includes information in the BRR that clearly informs borrowers that any changes or amendments to the HEA could change the terms of the MPN and the MPN would still be valid. This includes MPNs that have previously been signed and are fully executable. Specifically, we note that any amendment to the HEA that changes the terms of the MPN would apply to the borrower's loans in accordance with the effective date of the amendment and that depending on the effective date of such amendment, amendments to the HEA may modify or remove a benefit that existed at the time that the borrower signed the MPN. We disagree with the commenter's characterization that a borrower who signs a new MPN would either be subject to the terms of their original MPN or the new MPN; both MPNs would have that general condition that statutory changes could amend the terms of their promissory notes, including ones that were signed prior to the Working Families Tax Cuts Act. At the same time, some borrowers who have loans that were originated before July 1, 2026, are eligible for certain legacy repayment plans that loans originated after such date are not eligible for, as explained below in this final rule. We remind institutions that if the borrower's MPN is expiring, the institution must obtain a valid MPN from the borrower before disbursing a new Direct Loan to such borrower. This does not have an impact on the eligibility for the interim exception; it is a requirement to receive additional Federal student loans if desired.

Changes:

None.

Comments:

Some commenters argued that we should protect borrowers' reliance interests, especially as they relate to PSLF. These commenters believed that, at the time a borrower signed their MPN, the regulations could not be materially altered. One commenter recommended that the Department implement a grandfathering provision, whereby a borrower who was on track to receive PSLF would retain the right to remain in an income-contingent repayment plan until forgiveness or paid in full.

Discussion:

We disagree with the commenters' concerns and believe that reliance interests are not impacted here. Similar to the Department's statements in the PSLF final rule (90 FR 48979) with respect to reliance interests, a borrower would have to demonstrate their detrimental reliance and would require proof that a promise or representation was made and that promise or representation was relied upon by the borrower asserting the estoppel in such a manner as to change his position for the worse, and that the promise's reliance was reasonable and should have been reasonably expected by the promisor. See

L. Mathematics & Tech., Inc.

v.

United States,

779 F.2d 675, 678 (Fed. Cir. 1985). Much like the PSLF final rule, the borrower would fail to satisfy the required elements for a promissory estoppel claim because they expressly acknowledged and agreed to the possibility of changes to benefits that existed when they signed the MPN. The MPN disclaims the idea that the terms and conditions of a Federal student loan are unalterable, as we explain elsewhere in this document, meaning that any reliance interest is not reasonable.

We also reject the commenter's recommendation that we grandfather a borrower who was on track to PSLF so that they may retain the right to remain in an income-contingent repayment plan until forgiveness or paid in full as the statute is clear that these income-contingent repayment plans must be sunset. Borrowers on track toward receiving PSLF will have other PSLF-qualifying repayment plans available to them. Congress was clear that income-contingent repayment plans sunset and will be no longer available after July 1, 2028. The Department has no authority to alter this sunset date.

Changes:

None.

Loan Rehabilitation

Second Rehabilitation

Comments:

A significant majority of commenters expressed strong support for the provision allowing borrowers a second opportunity to rehabilitate defaulted Federal student loans

( printed page 23775)

beginning on or after July 1, 2027. Commenters characterized this as a humane and positive step that acknowledges the reality of recurring financial hardship. Commenters noted that financial situations can change due to market factors beyond a borrower's control, such as entering a workforce with low job opportunities. Supporters argued that giving borrowers a second chance encourages repayment rather than long-term default and helps bring consumers back into the economy. Several commenters stated that this change strikes an appropriate balance between personal accountability and the need for a meaningful path back to repayment.

Discussion:

The Department, effective July 1, 2027, increased the number of times a borrower may rehabilitate a defaulted Federal student loan made, insured, or guaranteed under title IV of the HEA from one time to two times to reflect the changes made by the Working Families Tax Cuts Act. The Department agrees that providing a second opportunity for loan rehabilitation is a balanced and constructive borrower protection. Allowing borrowers an additional opportunity to rehabilitate a loan may assist borrowers in resolving default and returning to repayment.

Changes:

None.

Comments:

Some commenters applauded the alignment of administrative wage garnishment (AWG) suspensions with the two rehabilitation opportunities authorized by the Working Families Tax Cuts Act, stating that suspending garnishment during voluntary payment periods is vital for a borrower's financial stability and their ability to successfully complete the rehabilitation agreement.

Discussion:

The Department agrees that expanding rehabilitation opportunities can support borrowers seeking to resolve default. Section 82003(a)(1) of the Working Families Tax Cuts Act amended Sections 428F(a)(5) and 464(h)(1)(D) of the HEA, which permit borrowers to rehabilitate a defaulted Federal student loan up to two times beginning on or after July 1, 2027. The Department also agrees that suspending AWG while a borrower makes voluntary rehabilitation payments supports the borrower's transition back to good standing. Sections 685.211(f)(11) and (12) reflect that on or after July 1, 2027, a borrower may obtain both the benefit of an AWG suspension, and the rehabilitation process itself a maximum of two times per loan.

Changes:

None.

Comments:

Commenters requested regulatory language to clarify whether restarting payments after a period of enrollment constitutes a continuation of the first rehabilitation attempt or the start of a second attempt. Specifically, these commenters proposed language stating that a rehabilitation is considered a single attempt if a borrower makes six payments, pauses for school, and then resumes to complete the final three payments.

Discussion:

Under existing regulations, a rehabilitation agreement is defined by the successful completion of the required payment series (nine payments within ten months). An attempt at rehabilitation that does not result in the loan returning to good standing does not count against the statutory limit on rehabilitations. A rehabilitation is only counted toward the limit once it is successfully completed. Therefore, if a borrower makes six payments, stops, and later enters into a new agreement to make nine payments and successfully completes the later agreement, they have still only used one of their permitted rehabilitations. The Department believes the proposed regulations at § 685.211(f)(12), which distinguish between rehabilitations completed before and after July 1, 2027, provide sufficient clarity on the limits on successful rehabilitations without the need for the additional language suggested by the commenters and the Department declines to make these changes.

Changes:

None.

Comments:

One commenter recommended that the Department clarify how the timing of a borrower signing a rehabilitation agreement should be treated in implementing the second rehabilitation opportunity established by the Working Families Tax Cuts Act. The commenter stated that borrowers who have already been making voluntary payments on a defaulted loan prior to July 1, 2027, should be able to receive the benefit of the second rehabilitation opportunity if they sign the rehabilitation agreement on or after that date, provided they have otherwise satisfied the required payment criteria. The commenter also suggested that borrowers who have already demonstrated good-faith repayment through voluntary payments should not be required to repeat the full series of rehabilitation payments solely because of when the rehabilitation agreement was signed.

Discussion:

The Department appreciates the commenters' recommendation regarding the implementation of the second rehabilitation opportunity authorized by the Working Families Tax Cut. As discussed in the NPRM (91 FR 4259), the Department's loan rehabilitation regulations implement the statutory changes that allow borrowers to rehabilitate a defaulted loan up to two times beginning July 1, 2027. The Department notes that loan rehabilitation is defined by the successful completion of the required payment series under the statute governing rehabilitation. The Department believes that the proposed regulatory structure provides sufficient clarity regarding how rehabilitation opportunities are counted and declines to make additional regulatory changes regarding the timing of rehabilitation agreements. As we also explain in the NPRM (91 FR 4288), we note that the effective date for the second rehabilitation attempt cannot begin until July 1, 2027, because the changes to the HEA regarding loan rehabilitations take effect

beginning

on July 1, 2027 [emphasis added] in accordance with the statutory deadlines contained in the Working Families Tax Cuts Act. As such, the borrower cannot begin that second rehabilitation until on or after the effective date.

Changes:

None.

Comments:

One commenter recommended that the Department require borrowers who seek to rehabilitate a defaulted loan for a second time to complete mandatory financial literacy counseling before entering into a second rehabilitation agreement. The commenter stated that counseling could help borrowers better understand the consequences of repeated default and improve long-term repayment success. The commenter suggested that such counseling could be provided by the Department or an approved third-party partner and could emphasize the importance of sustainable repayment strategies and the benefits of avoiding future default.

Discussion:

The Department appreciates the commenters' recommendation regarding mandatory financial literacy counseling for borrowers seeking a second loan rehabilitation. The Department agrees that providing borrowers with information about repayment options and the consequences of default can support successful repayment outcomes. As discussed in the NPRM (91 FR 4289), the Department intends to provide borrowers with improved guidance and information regarding repayment options as they transition out of default and into repayment. However, the Department declines to adopt a regulatory requirement mandating counseling as a condition for a second rehabilitation. The HEA establishes the

( printed page 23776)

statutory framework governing loan rehabilitation, including the requirement that borrowers make nine voluntary, reasonable, and affordable payments within ten months to successfully rehabilitate a defaulted loan. Requiring a borrower who seeks to rehabilitate a defaulted loan a second time to complete mandatory financial literacy counseling before entering into a second rehabilitation agreement is inconsistent with the HEA and no statutory basis exists to impose such a requirement for purposes of loan rehabilitation. The Department believes that the existing statutory structure, combined with borrower communications and guidance, is sufficient to support borrowers seeking to rehabilitate their loans and declines to make the commenters' proposed changes.

Changes:

None.

Comments:

One commenter supported the statutory provision permitting borrowers to rehabilitate a defaulted loan a second time beginning July 1, 2027, stating that the additional rehabilitation opportunity could assist borrowers who previously rehabilitated their loans but later experienced circumstances that resulted in another default. However, the commenter expressed concern that the proposed regulations do not describe how borrowers eligible for a second rehabilitation opportunity will be identified or notified.

The commenter also requested that the Department include in regulatory text the clarification provided in the preamble to the NPRM that participation in the Fresh Start Initiative does not count as a rehabilitation for purposes of the statutory limit on the number of rehabilitations permitted. The commenter recommended that the Department codify this clarification in the regulations and establish outreach procedures to notify borrowers of their eligibility for a second rehabilitation opportunity.

Discussion:

The Department appreciates the commenter's support for implementing the statutory provision allowing borrowers to rehabilitate a loan a second time. As explained in the NPRM (91 FR 4259), the Department is amending the loan rehabilitation regulatory revisions to implement Section 82003 of the Working Families Tax Cut, which provides that a borrower may rehabilitate a defaulted loan no more than two times. The Department intends to implement this statutory change consistently with existing loan rehabilitation processes administered through Federal loan servicers and Department operational guidance.

Participation in the Fresh Start Initiative does not constitute a loan rehabilitation for purposes of the statutory limit, as this program purported to rely on a different legal authority. The Department does not believe additional regulatory text changes are necessary to implement this clarification and declines to make the proposed changes.

Changes:

None.

Streamlining Rehabilitation Process To Repayment

Comments:

One commenter requested that the Department align the definition of full rehabilitation to six months. The commenter noted that under current regulations, a borrower can regain eligibility for new Federal student loans after six on-time payments but must make nine on-time payments to fully rehabilitate the defaulted loan. The commenter argued that this discrepancy sets borrowers up for failure by allowing them to take on new debt before their previous default is fully resolved. Alternatively, commenters suggested that the Secretary consider at least half-time enrollment at an eligible institution as an approved “hold” on the rehabilitation process, allowing borrowers to resume their remaining three payments within 45 days of their enrollment end date without having to restart the process.

Discussion:

The Department acknowledges the commenter's concern regarding the different timelines for regaining title IV eligibility versus completing rehabilitation. However, under Section 428F(a)(1)(A), the nine-payment stipulation is a statutory requirement to successfully rehabilitate a Federal student loan before a loan is returned to non-defaulted status and the record of default is removed from a borrower's credit history.

The Department declines to reduce the number of payments required for full rehabilitation or to create a regulatory “hold” for enrollment. Section 428F(a)(1) of the HEA specifically requires a borrower to make nine payments within ten consecutive months to successfully rehabilitate a defaulted loan. The Department does not have the statutory authority to change this requirement through regulation.

Changes:

None.

Comments:

Members of Congress and other commenters requested that the Department allow payments made while a borrower is in default to count toward timed forgiveness under IDR plans. Commenters stated that for low-income borrowers, timed forgiveness is an important safeguard that prevents borrowers from remaining in repayment indefinitely. Commenters asserted that the default collections process may result in borrowers paying more through wage garnishment or offsets than they would otherwise pay under an IDR plan. Commenters noted that under current regulations at § 685.209, certain voluntary payments made during loan rehabilitation may count as qualifying payments toward forgiveness under the IBR plan. Commenters urged the Department to maintain or expand this approach so that payments made while a borrower is in default would count toward forgiveness across legacy IDR plans and the Repayment Assistance Plan. Commenters stated that this policy would help borrowers make meaningful progress toward forgiveness and reduce confusion between repayment and default systems. Some commenters also urged the Department to implement these provisions before restarting involuntary collections such as through AWG and the Treasury Offset Program (TOP).

Discussion:

The Department appreciates commenters' perspectives regarding the treatment of payments made while a borrower is in default and their relationship to forgiveness under IDR plans. The Department is amending § 685.211 to implement the statutory changes made by the Working Families Tax Cuts Act, including provisions establishing the Repayment Assistance Plan, clarifying the repayment plans that may be designated for borrowers in default, and revising the loan rehabilitation framework. These amendments are intended to provide borrowers and servicers with clearer rules governing the treatment of payments and the repayment options available to borrowers who wish to resolve their default. The Department's authority regarding how payments may count toward forgiveness under IDR plans is governed by the HEA and applicable statutory requirements that does not permit us to count such payments toward forgiveness. Consistent with the proposed regulations, the Department is focusing on clarifying the repayment framework for borrowers in default and the transition from default into repayment.

Changes:

None.

Comments:

One commenter recommended that the Department consider using reliable third-party employment and income data sources to help determine whether proposed rehabilitation payment amounts are reasonable and affordable. The commenter stated that access to up-to-date employment and salary information could help servicers

( printed page 23777)

establish rehabilitation payment amounts that better reflect borrowers' current financial circumstances and improve the sustainability of rehabilitation agreements.

Discussion:

The Department appreciates the commenters' suggestion regarding the use of additional data sources to support the determination of reasonable and affordable rehabilitation payment amounts. Under the HEA, rehabilitation payments must be based on the borrower's total financial circumstances. The Department currently permits borrowers to provide income documentation or other financial information to establish reasonable and affordable payment amounts. The Department will continue to evaluate operational tools and data sources that may assist in administering the rehabilitation process consistent with statutory requirements and borrower privacy protections. However, the Department declines to adopt specific regulatory provisions governing the use of third-party employment data at this time.

Changes:

None.

Comments:

Commenters requested that the Department simplify the loan rehabilitation process to eliminate administrative barriers for borrowers. Commenters noted that the current rehabilitation process relies heavily on manual and paper-based procedures, including submitting documentation by mail or fax, which can result in a slow process for borrowers seeking to resolve their default. Commenters recommended several operational improvements, including allowing borrowers to request and execute rehabilitation agreements online, enabling electronic submission of income documentation, allowing borrowers to track their progress toward completing rehabilitation payments, and facilitating enrollment in income-driven repayment plans following rehabilitation. Commenters also recommended that the Department improve outreach to defaulted borrowers, streamline the administrative steps required to enroll in rehabilitation, and explore approaches to make post-rehabilitation payments more manageable, including potential phase-in or transition periods for repayment amounts.

Discussion:

The Department appreciates commenters' recommendations regarding improvements to increase the effectiveness of loan rehabilitation as a path out of default. The Department is developing a number of operational improvements that complement the regulations implementing the rehabilitation improvements enacted in the Working Families Tax Cuts Act.

We agree with commenters that operational improvements to make it easier to enroll in income-driven repayment plans following rehabilitation is important to make a seamless transition to repayment for borrowers exiting default. Many borrowers who rehabilitate their loans ultimately redefault if they do not enroll in an affordable income-driven repayment plan. To that end, the final rule will enable the Secretary to create a single application for rehabilitation agreements for Direct Loans that also includes the option to sign up for an eligible IDR plan. This single application will not be available to Perkins Loan or FFEL borrowers. Borrowers who only wish to enroll in loan rehabilitation will not be forced to also sign up for IDR; however, the Department believes that giving borrowers the option to do so will make it easier for borrowers to sign up. This all-in-one application will allow borrowers to replace multiple applications with one single transaction that would allow them to become enrolled in an affordable payment plan after they successfully rehabilitate their loan. Borrowers will also have the option to sign up for auto-debit for both the rehabilitation agreement and the IDR plan, making it easy for borrowers to make payments without the need for additional actions.

Under this single, all-in-one application, the Secretary would be able to calculate the borrower's payment under the IDR plan using the Federal tax information (FTI) (with the borrower's approval under HEA, as amended by the FUTURE Act) [1]

to inform the borrower what their IDR payment would be after rehabilitation. 26 U.S.C. 6103(l)(13); 20 U.S.C. 1098h. The borrower is not required to actually enroll in the IDR plan for the Department to be able to use its authority (with borrower approval) to access FTI and calculate eligible IDR payment amounts. 20 U.S.C. 1098h. This enables the borrower to compare different IDR plans before selecting a plan or deciding not to enroll.

If the borrower elects to see the monthly payment under and IDR plan through this single application process, the Secretary now has the borrower's monthly payment.

34 CFR 685.211 requires borrowers to make 9 monthly payments that are reasonable and affordable to rehabilitate a loan. The regulations include a provision that states that “The Secretary initially considers the borrower's reasonable and affordable payment amount to be an amount equal to the payment required under the IBR plan.” [2]

The Department believes that this requirement is too narrow in that it only applies to IBR and that monthly payment amounts under any eligible IDR plan (not including SAVE/REPAYE) are reasonable and affordable. These payment plans have been designed by the Department and Congress to be affordable for borrowers. And furthermore, under the changes we are making to this provision, borrowers can pick from among any eligible plan, all of which are designed to be affordable.

When a borrower elects to have their FTI pulled for the purposes of determining an IDR monthly payment rate, the Secretary may use that derivative monthly payment rate (with the borrower's approval) as the monthly payment rate for the purposes of the rehabilitation agreement. 34 CFR 685.211(f)(1)(ii) currently calls on the borrower to submit documentation to verify income, but in this limited circumstance, the Department believes that additional documentation is generally unnecessary. As such, the Department proposes to give the Secretary the option not to require additional verification.

In some circumstances even when FTI is used to calculate the IDR rate (which becomes the reasonable and affordable rate under a rehabilitation), it may be appropriate for the Secretary to require additional documentation. This may include when the borrower represents that his or her income is higher or lower than what was reported on his or her taxes, and when their family size has changed. In these circumstances, the Secretary may have an interest in requesting additional documentation from the borrower.

If the income information is unavailable or the Secretary does not believe it is accurate, the borrower will be required to provide alternative documentation of income. This approach is consistent with and complements the regulations implementing the rehabilitation improvements enacted in the Working Families Tax Cuts Act.

In addition, Parent PLUS borrowers are no longer eligible to enroll in IDR

( printed page 23778)

plans after the statutory changes made by the Working Families Tax Cuts Act. For the purposes of the rehabilitation process, the Secretary may confirm that the borrower is not eligible if they have Parent PLUS loans. But the Secretary may follow the formulas in this final rule under 34 CFR 685.211(f) under the IDR plans as if they were eligible in order to determine the reasonable and affordable payment.

The Department's changes in these final regulations enable, but do not require, the Secretary to provide a single application. The Department intends to provide a single application to borrowers as soon as practical but notes that several operational and technical changes must be made to Department systems to make this possible. As such, the Department will not have the single application available on July 1, 2026. However, as explained in the Paperwork Reduction Act section of this preamble, the Department will make the draft application publicly available and open a 60-day and 30-day public comment period before being made available for use.

Lastly, the Department notes that borrowers who have a defaulted student loan are ineligible for any IDR plan. As such, if a defaulted borrower were to apply for an IDR plan under our current regulations, the Secretary would be required to deny the application. However, we propose changes to the regulations that allow the Secretary to hold the IDR application, when it is submitted in combination with a rehabilitation agreement application on the single application, until the borrower has either: (1) completed the rehabilitation, or (2) failed to complete the rehabilitation by not making the required nine payments in a ten month period.

When a borrower successfully completes the rehabilitation, the Secretary then approves the IDR plan and automatically enrolls the borrower into the IDR plan. The single application will also enable the borrower to sign up for auto-debit such that the Secretary may continue the auto-debit after automatically enrolling the borrower into an IDR plan. If the borrower fails to complete the rehabilitation, then the Secretary denies the IDR application because the borrower is ineligible for the plan.

As a result of these improvements to loan rehabilitation, we also make two technical corrections to paragraphs (f)(2) and (3). In (f)(2), we replace “account” with “loans” and in (f)(3), we replace “objects to” to “rejects”.

Changes:

We amend § 685.211(f)(1)(ii) to read as follows: (ii)(A) The Secretary may calculate the payment amount based on information provided orally (or through other means) by the borrower or the borrower's representative and provide the borrower with a rehabilitation agreement using that amount. (B) The Secretary may provide a single application for the purpose of enabling a borrower to apply for loan rehabilitation and income driven repayment simultaneously, and may, with the borrower's approval, calculate the payment amount for any income driven repayment plan that the borrower would otherwise be eligible for (after successful rehabilitation of the defaulted loan) to inform the borrower of the projected monthly repayment amount under such plan after the loans are rehabilitated. The Secretary may use the calculated payment required under any eligible income driven repayment plan for the purpose of determining the reasonable and affordable payment amount under this paragraph (f)(1), with the borrower's approval. Nothing in this section prohibits the Secretary from accepting an application from a borrower for an IDR plan who is currently enrolled in a rehabilitation agreement but has not yet completed such agreement by making the requisite payments and holding such application until the borrower has completed the rehabilitation. (C) The Secretary requires the borrower to provide documentation to confirm the borrower's AGI and family size, except that the Secretary may, in his or her discretion, consider such additional documentation unnecessary if the borrower approves having the payment amount calculated by the Secretary for an eligible income driven repayment plan as the borrower's reasonable and affordable payment. If the borrower's AGI or family size is not available, or if the Secretary believes that the borrower's reported AGI or family size may be inaccurate, the borrower must provide other documentation to verify income or family size. If the borrower fails to provide acceptable documentation to verify family size, the Secretary assumes a family size of one. If the borrower does not provide the Secretary with any income documentation requested by the Secretary to calculate or confirm the reasonable and affordable payment amount within a reasonable time deadline set by the Secretary, the rehabilitation agreement provided is null and void.

We also make two technical corrections to §§ 685.211(f)(2) and (3).

Comments:

Commenters generally supported the establishment of clear minimum payment amounts for rehabilitation. However, some sought clarification on the difference between FFEL and Direct Loan requirements.

Discussion:

To reflect changes made by the Working Families Tax Cuts Act that amended Section 428F(a)(1)(B) of the HEA, the Department is establishing a $10 minimum monthly payment for the rehabilitation of a defaulted Direct Loan beginning July 1, 2027. Prior to that date, the minimum payment is $5. The Department notes that, while the Direct Loan minimum monthly rehabilitation payment will increase to $10, the minimum monthly rehabilitation payment for the FFEL Program remains at $5 under § 682.405. This lack of change is because the statute did not amend the minimum monthly payment for rehabilitation of a defaulted FFEL loan. Section 428F(a)(1)(B) of the HEA was amended only with respect to a borrower who has one or more loans made under part D [

i.e.: Direct Loans] on or after July 1, 2027, that are being rehabilitated, establishing the total monthly payment for the borrower with all such loans shall not be less than $10.

When the Secretary determines the amount of a borrower's reasonable and affordable payment for loan rehabilitation, we initially proposed that the loan rehabilitation payment amount to be an amount equal to the minimum payment required under the IBR plan, except if this amount was less than $5 (or $10 beginning on or after July 1, 2027), the monthly payment was $5 (or $10 beginning on or after July 1, 2027). After further review, if the borrower avails themself of the rehabilitation agreement under § 685.211(f)(1)(ii), the loan rehabilitation payment amount will be the minimum amount under the IDR plan proactively selected by the borrower in their application. We note, however, that if a borrower's IDR monthly payment is $0, the borrower's loan rehabilitation payment amount will be $10 in accordance with the aforementioned.

Section 494(b) of the HEA and 26 U.S.C. 6103(l)(13) limits the Secretary's authority to obtain FTI from the IRS only for purposes of administering the FAFSA®, enrollment in an IDR plan, and total and permanent disability discharge determinations. However, in response to the commenters' desire to streamline the rehabilitation process as well as an on-ramp to affordable repayment, we believe we can proactively obtain the borrower's FTI for enrollment in an IDR plan with their approval. As such, we are using the IDR rate, derived from the borrower's FTI, to determine the reasonable and affordable rate for loan rehabilitation.

( printed page 23779)