Proposed Revisions to the Federal Reserve Policy on Payment System Risk and the Guidelines for Account and Services Requests

The Board of Governors of the Federal Reserve System (Board) is issuing a notice and request for comment on proposed revisions to the Federal Reserve Policy on Payment System Ri...

The Board of Governors of the Federal Reserve System (Board) is issuing a notice and request for comment on proposed revisions to the Federal Reserve Policy on Payment System Risk (PSR Policy), including the proposed addition of a new Part IV, to accommodate the provision by Reserve Banks of special-purpose accounts that would clear and settle certain payment activity (Payment Accounts). The Board is also proposing updates to its guidelines for Federal Reserve Banks (Reserve Banks) to utilize in evaluating requests for access to Reserve Bank account and services (Account Access Guidelines or Guidelines) to accommodate requests for access to Payment Accounts. Finally, the Board is encouraging Reserve Banks to pause decisions on requests for Reserve Bank accounts and services from institutions that are Tier 3 under the Account Access Guidelines until the Board has completed its policy development process on the Payment Account proposal.

DATES:

Comments must be received on or before July 27, 20.

ADDRESSES:

You may submit comments, identified by Docket No. OP-1878, by any of the following methods:

Mail:

Benjamin W. McDonough, Secretary, Board of Governors of the Federal Reserve System, 20th Street and Constitution Avenue NW, Washington, DC 20551.

Hand Delivery/Courier:

Same as mailing address.

Other Means: publiccomments@frb.gov.

You must include docket number in the subject line of the message.

Comments received are subject to public disclosure. In general, comments received will be made available on the Board's website at

https://www.federalreserve.gov/apps/proposals/

without change and will not be modified to remove personal or business information including confidential, contact, or other identifying information. Comments should not include any information such as confidential information that would be not appropriate for public disclosure. Public comments may also be viewed electronically or in person in Room M-4365A, 2001 C St. NW, Washington, DC 20551, between 9 a.m. and 5 p.m. during Federal business weekdays.

FOR FURTHER INFORMATION CONTACT:

Jason Hinkle, Associate Director, Zineb York, Manager, Kristopher Natoli, Manager, or Brajan Kola, Lead Financial Institution Policy Analyst, Division of Reserve Bank Operations and Payment Systems; or Corinne Milliken Van Ness, Senior Counsel, or Sumeet Shroff, Senior Counsel, Legal Division, Board of Governors of the Federal Reserve System: (202) 452-3000. For users of TTY-TRS, please call 711 from any telephone, anywhere in the United States or (202) 263-4869.

SUPPLEMENTARY INFORMATION:

I. Background

The Board is seeking comment on a proposal to revise the PSR Policy and the Account Access Guidelines to accommodate the provision of Payment Accounts by Reserve Banks.

This notice is organized into eight sections. Section I contains background on the Account Access Guidelines and the PSR Policy, a description of developments in the payments ecosystem since the Board issued the Account Access Guidelines, and an overview of the Board's Request for Information (RFI) on the Payment Account prototype. Section II provides a summary of comments on the RFI and the Board's responses. Section III.A describes the Board's proposal to offer a Payment Account and the risk-mitigating terms of the Payment Account.[1]

Section III.B summarizes the

( printed page 30628)

proposed amendments to the PSR Policy to accommodate the Payment Account. Section III.C summarizes the proposed amendments to the Account Access Guidelines (i) to accommodate the Payment Account, (ii) to update the review framework to accommodate the Payment Account, and (iii) to introduce timing expectations for reviewing certain access requests. Section IV requests comment on the proposal as a whole and sets out specific questions on which the Board is soliciting the public's input. Section V analyzes the competitive impact of the proposal. Section VI includes the Board's analysis of the proposal under the Regulatory Flexibility Act and the Paperwork Reduction Act and includes other administrative law matters. Finally, Sections VII and VIII contain the proposed amendments to the PSR Policy and the Account Access Guidelines, respectively.

A. Statutory Background, the Account Access Guidelines, and the PSR Policy

The Reserve Banks may provide accounts (accounts) and financial services (services) to institutions as authorized by federal law. Reserve Banks generally provide accounts and services to member banks, depository institutions, and branches and agencies of foreign banks pursuant to sections 13(1) and 13(14) of the Federal Reserve Act (FRA).[2]

Pursuant to section 11(j) of the FRA, the Board exercises general supervision over the Reserve Banks.[3]

In supervising and overseeing the activities of the Reserve Banks, the Board may issue guidance to the Reserve Banks regarding the provision of accounts and services. On August 15, 2022, after a public comment process, the Board adopted the Account Access Guidelines, which the Reserve Banks utilize in evaluating access requests.[4]

The Guidelines establish a transparent, risk-based, and consistent set of factors for Reserve Banks to use in reviewing access requests from legally eligible institutions. The Guidelines incorporate a tiering framework under which access requests from certain types of entities (

e.g.,

non-federally insured institutions) are subject to greater due diligence and scrutiny than access requests from other types of entities (

e.g.,

federally insured institutions). The tiering framework acknowledges the spectrum of regulatory and supervisory frameworks that apply to institutions that may request access. For example, federally insured institutions (Tier 1) are subject to a comprehensive and consistent set of federal banking regulations and, in most cases, detailed regulatory and financial information about these firms is readily available. These institutions are therefore generally subject to a less intensive and streamlined review under the Guidelines relative to institutions in higher tiers. On the other end of the spectrum, non-federally insured institutions that are not subject to prudential supervision by a federal banking agency at the institution or holding company level (Tier 3) may be subject to a supervisory or regulatory framework that is substantially different from the supervisory and regulatory framework that applies to federally insured institutions, and their access may pose the highest level of risk. Accordingly, access requests from Tier 3 institutions receive the strictest level of review under the Guidelines.

The PSR Policy addresses the risks that payment, clearing, settlement, and recording activities present to the financial system and to the Reserve Banks. In adopting the PSR Policy, the Board's objectives were to foster the safety and efficiency of payment, clearing, settlement, and recording systems, and to promote financial stability more broadly. The PSR Policy consists of three parts.[5]

Part I sets forth the Board's views and related standards regarding the management of risks in certain payment, clearing, and settlement systems. Part II of the PSR Policy outlines the methods the Reserve Banks use to provide intraday credit, also known as daylight overdrafts, while controlling credit risk posed to the Reserve Banks. Part III of the PSR Policy governs the Board's policy on overnight overdrafts in Reserve Bank accounts.

B. Developments Since Issuance of the Account Access Guidelines

The payments ecosystem continues to evolve rapidly. Technological progress, statutory developments, consumer and business preferences, and other factors are driving both the introduction of innovative financial products and services and new approaches to the traditional banking functions of payments, deposit-taking, and lending.

The Board continues to monitor developments in the payments ecosystem, including the development of new financial products and technologies. Since the Board issued the Account Access Guidelines, the types of institutions seeking accounts and services have continued to evolve. Several institutions focused on payments innovation have explained that they are interested in direct access to accounts and services, as opposed to having to rely on third-party intermediaries to access services, to reduce costs to their customers while increasing payment processing speed. These institutions have also argued that direct access to accounts and services would reduce the concentration risk created by their reliance on a limited number of third-party intermediaries for accessing services. Direct access, in their view, would reduce risks to the overall payment system. Some of these institutions have requested either a state or federal banking charter, and a few have initiated requests for accounts and services.

Many of these institutions are legally eligible for accounts and services, and they are often considered Tier 2 or Tier 3 institutions under the Board's Account Access Guidelines.[6]

Some Tier 2 and Tier 3 institutions that have requested, or expressed interest in requesting, access have voiced concern about the length of time that Reserve Banks take to review access requests and the high likelihood of denial.

C. Overview of Request for Information on Payment Account Prototype

On December 23, 2025, the Board published an RFI seeking public input

( printed page 30629)

on a special-purpose Payment Account prototype tailored to the needs and risks of institutions focused on payments innovation.[7]

The RFI contemplated that a Payment Account would be designed for the purpose of clearing and settling the Payment Account holder's payment activity, and that Payment Accounts would have a common set of risk-mitigating terms. Consistent with the Reserve Banks' legal authorities, only institutions that are legally eligible to maintain accounts with a Reserve Bank would be eligible to maintain a Payment Account. The Payment Account would be subject to an overnight balance limit. The Board explained that it was considering setting the overnight balance limit at the lesser of $500 million or 10 percent of the relevant Payment Account holder's total assets.[8]

Balances in a Payment Account would not receive interest. The RFI also contemplated that a Payment Account holder would not have access to Reserve Bank credit, either through the discount window or through intraday credit. Given the lack of access to intraday credit, Payment Account holders would only have access to services with automated controls to prevent overdrafts: Fedwire® Funds Service, the FedNow® Service, the National Settlement Service (NSS), and the Fedwire Securities Service for transfers free of payment.[9]

Payment Account holders would not be permitted to act as correspondent banks, and a Payment Account could not be used to settle a respondent institution's activity.[10]

The Board also noted that it was exploring additional risk controls and conditions to cover areas such as risks to the payment system or risks associated with illicit finance.

The RFI explained that, consistent with a Payment Account's lower residual risk profile given its mitigating terms, a request for a Payment Account would generally receive a more streamlined review than a request for a Master Account from the same institution. Accordingly, the RFI proposed that a Reserve Bank generally would complete its review of a Payment Account request within 90 calendar days following receipt of all documentation requested by the Reserve Bank.[11]

The Board received 72 comment letters on the RFI. Commenters represented several types of institutions and organizations, including (1) non-traditional institutions, including those focused on payments or crypto, along with their trade associations; and (2) traditional banks, including community banks, and their trade associations. Comments on the Payment Account tended to divide along industry lines. Non-traditional institutions generally supported the proposal, with many seeking access to a wider range of services or fewer controls. Traditional banks and related trade associations generally expressed concerns with the proposal, with many favoring additional restrictions or controls.

A. Eligibility

1. Summary of Comments

Several commenters requested the Board clarify legal eligibility to access accounts and services. One commenter asserted that legal eligibility remains a source of confusion and asked the Board to specifically address eligibility by institution type. Another commenter asked the Board to clarify that the establishment of a Payment Account does not alter the statutory eligibility for a Master Account.

Some commenters argued that legal eligibility should be further limited. Several commenters stated that a Master Account should be limited to Tier 1 institutions, and a few commenters stated that a Payment Account should also be limited to Tier 1 institutions. One commenter stated that Payment Account eligibility should be limited to Tier 1 and Tier 2 institutions. Another commenter stated that Master Account eligibility should be limited to Tier 1 and Tier 2 institutions, and that Tier 3 institutions should only be eligible for a Payment Account.

Some commenters discussed whether the Board could expand legal eligibility. One commenter requested that the Board expand eligibility for a Payment Account to money transmitter license holders that meet certain requirements. Another commenter advocated for all regulated stablecoin providers to be eligible for a Payment Account, arguing that nonbank stablecoin providers will be at a competitive disadvantage if they are not eligible for a Payment Account. Another commenter argued that providing access to stablecoin issuers should not be done without clear Congressional authorization. A few commenters noted that decisions by other agencies to grant charters to institutions with novel business models would effectively expand the institutions eligible to request a Payment Account. One commenter emphasized that any expansion of legal eligibility for Reserve Bank account access should be addressed by Congress through legislation, and another commenter supported Congressional action to expand eligibility to nonbank payment providers.

2. Board Response

Federal law—as enacted by Congress—dictates the entities that are eligible to maintain an account at a Reserve Bank. Currently, any institution that satisfies the legal eligibility requirements for an account under the FRA or other federal law is eligible to request a Master Account. Under the proposal, these same institutions (

i.e.,

those that satisfy the legal eligibility requirements for an account) would have the option of requesting either a Payment Account or a Master Account.

B. General Design of the Payment Account

1. Summary of Comments

Most of the comment letters received provided views about the extent to which the Payment Account's design would support an eligible institution's payment activity, the use cases it would best facilitate, and the use cases it might not facilitate.

Commenters noted that the Payment Account's design could address some, but not all, of eligible institutions' core payment needs. Many indicated that direct access to services, particularly the Fedwire Funds Service and the FedNow Service, could reduce costs for smaller institutions and consumers when considering current transaction fees associated with correspondent banking. The Payment Account was viewed as suitable for more routine, pre-funded payments by businesses and consumers.

( printed page 30630)

Some of the examples of use cases provided by commenters included instant access to wages or refunds, person-to-person or business-to-business transfers, pay-by-bank at checkout, payments related to stablecoins or other tokenized assets and, potentially, the U.S. dollar leg of cross-border transactions. Multiple commenters expressed particular interest in the benefits of the Payment Account for tokenization and stablecoins. They argued that a Payment Account could enable effective development of tokenization platforms that facilitate the transfer and settlement of tokenized securities in central bank money. Other commenters focused on how a Payment Account would improve stablecoin issuer operations through better reserve management and issuance and redemption. Additionally, several commenters noted that a Payment Account could improve functionality by fostering stablecoin-dollar fungibility and improving interoperability and settlement between different stablecoins. Some commenters noted improvement in general treasury management as a potential benefit of the Payment Account.

Several commenters asserted that excluding direct access to FedACH Services (FedACH) would significantly limit the use cases that the Payment Account could satisfy because of ACH's prominence in payroll, bill payments, and business-to-business payments. In addition to pre-funding ACH credit originations, some commenters expressed a willingness to maintain a minimum amount of balances or otherwise post collateral to mitigate the credit risk of other types of ACH transactions (for example, when a Payment Account receives a debit transaction, which would pull funds out of a Payment Account). At least one commenter suggested that Payment Account holders should be restricted from receiving any debit transaction.

Additionally, commenters offered varied opinions about how access to other Federal Reserve services, such as NSS and the Fedwire Securities Service, would affect the use cases the Payment Account could or could not support. While one commenter suggested that allowing Payment Account holders to access Fedwire Securities Service's delivery-versus-payment functionality could facilitate movement of Treasury securities, particularly for stablecoin issuers and entities engaged in repo and reverse repo transactions, another commenter stated that Payment Account holders should not have access to either the Fedwire Securities Service or NSS. Finally, one commenter noted that the Payment Account's prohibition on correspondent-respondent relationships could limit the services Payment Account holders could provide to third parties.

2. Board Response

While the Board recognizes several commenters' desire for Payment Account holders to have access to the full range of services, the Board believes that doing so would undermine the objectives of Payment Accounts as special-purpose accounts designed to minimize risk. The Board's goal is to support private-sector innovation in payments while ensuring that the risks identified in the Account Access Guidelines continue to be managed prudently. The Board believes that, on balance, this proposal would create a structured framework that would facilitate innovation in areas where providing Payment Account holders with direct access to the Fedwire Funds Service, the FedNow Service, NSS, and the Fedwire Securities Service for transfers free of payment would provide meaningful value. The Board understands that some commenters do not believe Payments Accounts should have access to NSS or do not identify use cases for NSS access; the Board believes, however, that the proposed Payment Account terms mitigate potential risk associated with granting access to NSS. Therefore, given the goal of supporting private-sector innovation, the Board believes it is appropriate to make access to NSS an option for a Payment Account holder.

For the reasons explained in Section III.A.1 the Board is proposing to exclude access to the Fedwire Securities Service for delivery versus payment transactions. Similarly, Section III.A.2 discusses the Board's rationale for prohibiting Payment Account holders from acting as OC 1 Correspondents or OC 1 Respondents (defined in Section III.A.2) under the Reserve Banks' Operating Circular 1 (OC 1).[13]

When considering whether to provide Payment Account holders with access to FedACH, the Board considered FedACH's unique characteristics. Unlike Fedwire Funds Service or FedNow Service transactions, banks can originate both credit-push and debit-pull ACH payments, commingled into batches containing many payments that are processed together.[14]

As background, credit originations result in a debit to the account of the sending bank and a credit to the receiving bank (such as for payroll payments). Debit originations result in the reverse: a credit to the account of the sending bank and a debit to the receiving bank (such as for bill payments that a consumer authorizes in advance). If there is an issue with either a credit or debit origination, such as an incorrect payee or insufficient funds, the transaction must be returned by the receiver within a specific time frame (up to two days later for business payments and up to 60 days later for consumer payments). Additionally, a bank that originated an ACH payment could reverse the payment if it contained an error. As a result, a bank whose account was credited could have its account debited in the following days or months due to an issue with the original transaction.

With respect to access to financial services through Payment Accounts, ACH's unique characteristics materially alter the relevant considerations compared to the Fedwire Funds Service and the FedNow Service. Unlike ACH, those systems are real-time gross settlement systems with final and irrevocable settlement of credit transfers and real-time reject controls, which ultimately allows the Reserve Banks to prevent an account holder from making individual FedNow Service or Fedwire Fund Service payments that would overdraw their account. ACH is different; it employs deferred settlement, batch processing, and the provision of returns and reversals for both credit and debit transfers would require a complex, layered set of ACH controls to prevent Payment Account overdrafts. For example, today, account holders that are subject to enhanced credit risk scrutiny by the Reserve Banks can be required to prefund the value of ACH credits they originate, to protect against account overdrafts at settlement.[15]

This control could likewise be imposed on Payment Account holders in order to limit the risk of overdrafts from a Payment Account holder's origination of ACH credits, but it would only address the

( printed page 30631)

credit risk from that one discrete type of ACH transaction.

The Board believes a minimum balance or collateralization approach would not sufficiently mitigate the credit risk from ACH debits received by Payment Accounts, because the Reserve Banks do not have the ability to predict debit transactions with sufficient accuracy or limit the amount of debit transactions a Payment Account could receive to a certain threshold.[16]

The only way for Reserve Banks to sufficiently mitigate their credit risk from ACH debit transactions would be to restrict Payment Account holders from receiving any debit transactions. However, it would be unprecedented within the ACH network, and highly disruptive to the efficient operation of the network and other participants, to attempt to introduce a broad class of ACH participants that is generally not allowed to receive debit transactions but is allowed to engage in other transaction types.[17]

The ubiquity of the ACH network is in part driven by the expectation that banks can generally send and receive debits and credits to all other participants on the network at all times, and this expectation is codified in many network rules. Another essential aspect of the efficiency and ubiquity of ACH is the ability to return or reverse transactions for a range of problems after the fact. Prohibiting Payment Accounts from receiving any ACH debits would undermine a fundamental element of the ACH network by effectively eliminating the ability to process returns and reversals for ACH debit transactions originated by a class of ACH participants.[18]

Institutions need the ability to manage effectively the inherent risks of debit transactions, including fraudulent or otherwise unauthorized payments, to ensure the safety of the payment system. Restricting the ability of Payment Account holders to receive debits, which would be necessary to manage credit risk to the Reserve Banks, would dramatically reduce other institutions' ability to manage their own risks.

Further, restricting debit receipts would remove important use cases from the ACH network for Payment Account holders and their counterparties, reducing the general utility of ACH. Prohibiting Payment Accounts from receiving ACH debits therefore would mitigate credit risk to the Reserve Banks but result in unacceptable degradation to the function of the ACH network and have significant negative effects on other participants' use of the network.

Based on these considerations, the Board does not believe there is a reasonable way to allow Payment Accounts to access FedACH and effectively mitigate credit risk to the Reserve Banks without disrupting the ACH network and potentially undermining its efficiency and effectiveness.[19]

The Reserve Banks may modify their systems' controls over time. If the Reserve Banks' systems' controls were to change, the Board might reconsider the suite of services to which Payment Accounts are given access. In the interim, institutions seeking access to additional services may request a Master Account.

C. Impact on Barriers to Innovation

1. Summary of Comments

In the RFI, the Board asked about what barriers to payments innovation the Payments Account would eliminate or alleviate. Many commenters indicated that the Payment Account would alleviate or eliminate barriers to innovation in the payments system. Some of these commenters identified the reliance on intermediaries as the primary barrier that the Payment Account would address, noting that firms without Master Accounts must currently settle transactions through their existing third-party intermediaries. Commenters indicated that removing this barrier would reduce counterparty risk, decrease the costs and fees associated with accessing services through intermediaries, increase the speed of settlement, and improve the competitive environment for payment services by leveling the playing field for new entrants. One commenter noted that fintech payment providers must often rely on the banks with which they are competing to provide them with correspondent services. Relatedly, some commenters noted that having direct access to services through a Payment Account would provide them with greater operational independence and the ability to design better, more efficient processes.

A few commenters disagreed that reducing reliance on intermediaries would effectively alleviate barriers to innovation. Some commenters noted that institutions rely on intermediaries for risk mitigation, and that reducing reliance on intermediaries will shift risk-management obligations entirely onto the requesting entity itself, without reducing the overall need for risk and compliance controls. These commenters argued that this approach would move the responsibility from a supervised bank to an entity that may have less oversight, fewer resources, or a more limited compliance infrastructure.

Some commenters provided additional observations on the Payment Account's potential benefits. A few commenters noted that Payment Accounts would increase visibility into dollar activity, while another commenter noted that combined with digital settlement technologies, Payment Accounts can reduce frictions and help the U.S. dollar maintain global leadership while enabling innovation and cross-border interoperability.

2. Board Response

The Board believes that the Payment Account could support private-sector innovation by reducing (1) the uncertainty, time, and related costs of obtaining access; and (2) the reliance on intermediaries. This, in turn, could increase competition in the payments marketplace and allow institutions to design innovative and efficient services that better leverage all the capabilities of the services to which the Payment Account will have access. The Board reiterates its expectation that Reserve Banks assess access requests against the Account Access Guidelines, and this would apply to the proposed Payment Account as well. Payment Account holders would be expected to meet the Account Access Guidelines' risk-management expectations and have in place appropriate operational and risk-management frameworks.

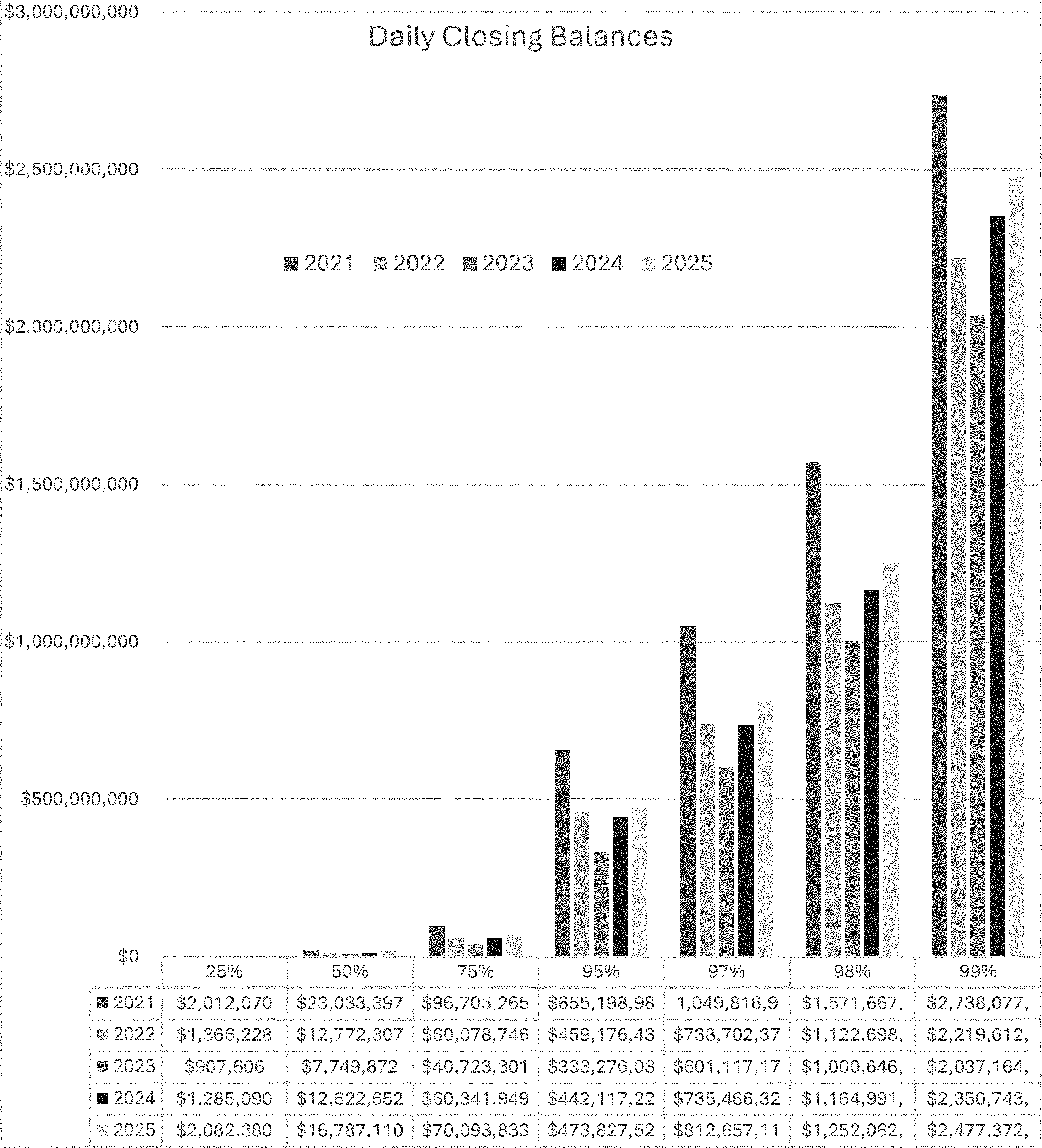

D. Limit on Closing Balances

1. Summary of Comments

Over half the comments received discussed the RFI's proposed balance limit. Although the Board received comments on the overall purpose and need for a limitation on overnight balances, a large majority of comments addressed the balance limit amount, the

( printed page 30632)

methodology for determining the limit, or both.

With respect to overall purpose and need, some commenters noted the importance of a limit to minimize the effects of Payment Accounts on the Federal Reserve's balance sheet; discourage the use of Payment Accounts as a store of value; and create an account that complements, rather than disrupts, the banking system. One commenter argued that a balance limit could support monetary policy transmission and mitigate concerns about narrow bank dynamics or deposit flight in periods of stress. Several commenters asserted that a balance limit was unnecessary because Payment Accounts would not receive interest. Two commenters suggested that, in lieu of a limit, Payment Account balances could receive interest up to a threshold level.

Regarding the limit amount, although one commenter viewed the RFI's balance limit amount as too high and another suggested a lower limit during an initial phase, a substantial number of commenters stated that the proposed limit would be too low. Commenters indicated the limit should be set at a level that accommodates the actual operating liquidity needs of account holders, and that high-volume payments business models may require a greater overnight limit to fund opening settlements. Some suggested that the limit would disproportionately impact smaller institutions. One suggested a uniform limit of $250 to $500 million and stated that the suggested level would not have a meaningful impact on the Federal Reserve's balance sheet. One commenter recommended setting the limit solely at 10 percent of total assets, rather than the

lesser

of $500 million or 10 percent of total assets. Other commenters suggested raising the balance limit to between 25 and 40 percent of total assets or a graduated asset-based limit.

Many commenters indicated that the balance limit should be calibrated to an institution's payment activity. Commenters noted that, for a payment-oriented institution, an asset-based limit may not reflect the institution's actual payment needs and that such a limit could inhibit growth. They also noted that an asset-based limit could cause inefficiencies and that an activity-based limit could promote the smooth functioning of the payment system and reduce operational risk. Commenters provided a variety of suggestions for an activity-based methodology. Some commenters recommended a balance cap commensurate with historical or near-term anticipated settlement needs and noted the need for 24/7/365 operational continuity during weekends and multi-day holiday windows. Other commenters noted the need for flexibility, including around events such as holidays and quarter ends, to meet the needs of firms that move large and concentrated amounts (such as payroll firms), and to accommodate unusual circumstances. Another commenter suggested that the asset-based limit set forth in the RFI should serve as an upper bound for an activity-based limit. Other commenters suggested stress-based limits, such as a limit based on an institution's stressed one-day liquidity needs.

Commenters also raised other suggestions regarding the balance limit. One commenter suggested establishing an institution's balance limit based on the business plan it provides to its chartering authority. Another commenter suggested establishing a limit that increases over time as a Payment Account holder demonstrates its safe payment operations. Other commenters stated that upward adjustments to an institution's limit should be subject to established public standards. Two commenters addressed stablecoin issuers specifically, with one proposing a limit of 10 percent of circulating payment stablecoin supply, and the other proposing that a balance limit should account for the likelihood that dollar-based stablecoins will displace physical currency over time.

One commenter suggested that, for smaller institutions, the Board could consider calibrating the balance limit and interest rate prohibitions by deploying them in complementary ways, which the commenter stated could preserve the Payment Account's purpose, avoid unintended incentives for intraday volatility and underfunding accounts, and better align operational resiliency with the Board's monetary policy objectives.

2. Board Response

The Board's goal in proposing a special-purpose Payment Account is to support private-sector innovation in payments while ensuring that the risks identified in the Account Access Guidelines continue to be managed prudently. As further explained in Section III.A.4, as part of a Payment Account's standard terms, the Board believes that establishing a balance limit, to be measured at the Federal Reserve's daily close of business, is important to mitigate potential risks related to financial stability and the implementation of monetary policy. Many of the comments received supported this premise.

In reviewing the comments received, the Board recognizes that calling this limit an “overnight balance limit” could result in confusion about when the limit applied, especially whether there would be a balance limit during what many businesses consider overnight hours, but when the FedNow Service or the Fedwire Funds Service is operational (

e.g.,

10 p.m. ET). To avoid any potential confusion, the Board refers to the balance limit as a “Closing Balance Limit” in this proposal. While commenters did not specifically raise questions around when the limit would apply, the Board believes that some comments about the size of the balance limit may also be addressed by clarifying the mechanics of the limit. The proposal also clarifies that the balance limit would apply solely at the close of the Federal Reserve's business hours.[20]

The Board has carefully reviewed the factors that commenters suggested should be considered in the design and implementation of the Closing Balance Limit. In particular, the Board recognizes that an asset-based limit may not reflect a payment-oriented institution's actual payment needs and that the net benefits of the Payment Account would be enhanced if the limit were calibrated to an individual institution's payment activity. However, as discussed in Section III.A.4 the Board continues to believe that having a uniform upper bound for setting the balance limit would mitigate potential risks related to financial stability and the implementation of monetary policy. As a result, the Board is proposing that the relevant Reserve Bank will set an individual Closing Balance Limit, not to exceed $1 billion, based on the Reserve Bank's analysis of the Payment Account holder's payment flows (if available), in particular at the beginning of the Federal Reserve's business day, and take into consideration periods of time when external sources of liquidity may be limited, such as during weekends and holidays.

E. Limit on Intraday Credit Access

1. Summary of Comments

Several commenters said the lack of access to intraday credit would make the Payment Account less appealing or useful for its intended purpose. For example, one commenter noted that the combination of low balance caps and the prohibition on daylight overdrafts would increase the risk of failed payments.

( printed page 30633)

Conversely, multiple commenters noted that the lack of intraday credit is an appropriate risk mitigant of the Payment Account design. Additionally, some commenters suggested that Reserve Banks implement intraday liquidity monitoring and tools to reject transactions that would result in a negative account balance, further reinforcing the goal of requiring prefunding for the Payment Account.

2. Board Response

The lack of access to intraday credit is a central feature of the Payment Account as proposed. Although providing intraday credit can foster the smooth operation of the payment system, the Board is proposing to design the Payment Account to minimize its operational complexities and risk profile. This design would enable the Reserve Banks to provide timely, direct access to accounts and services to institutions with novel and diverse business models and risk profiles. Prohibiting access to intraday credit would facilitate this goal by minimizing credit risk to the Reserve Banks, thus reducing the complexity of the risk assessment required for Payment Account requests.

If an institution desires access to intraday credit, the institution should consider requesting a Master Account, which may provide access to a broader range of services but would likely be subject to greater due diligence and scrutiny relative to a request for a Payment Account from the same institution.[21]

As discussed in Section III.A.1, consistent with some commenters' suggestions, the Board notes that Payment Accounts would only be permitted access to those services for which the Reserve Banks have automated tools to reject transactions that would result in a negative account balance.[22]

F. Effect of Providing Payment Accounts on the Risks Identified in the Account Access Guidelines

1. Summary of Comments

Commenters expressed differing views on the effect that providing Payment Accounts would have on the risks identified in the Account Access Guidelines. Some commenters stated that the design features of the Payment Account, such as no daylight overdrafts and the Closing Balance Limit, inherently limit credit and liquidity risks. They further stated that direct access to the payment system could reduce settlement risk by shortening settlement chains and lowering reliance on intermediaries that can amplify the impacts of operational outages or liquidity constraints during stress events. However, other commenters cautioned that providing direct access to institutions not subject to the same regulatory regime as federally insured depository institutions could result in heightened risks related to operational resiliency, financial stability, and Bank Secrecy Act (BSA)/Anti Money Laundering (AML) compliance.

Further, a few commenters expressed concerns that the design of the Payment Account would increase risks to the payment system as interconnectedness between Payment Account holders may create systemic risk and suggested setting exposure limits for single counterparties. Many of these commenters provided recommendations for additional requirements or terms to which Payment Account holders could be subject, such as submitting stress-testing plans and back-up liquidity arrangements, and suggested that strong supervision, consistent application across Reserve Banks, and the ability to revoke access if risks emerge would be essential safeguards. Similarly, other commenters emphasized the importance of explicit and enforceable expectations for operational resilience, governance, cyber maturity, and compliance to ensure that the Payment Account does not weaken the safety, soundness, or integrity of the payments system.

Lastly, commenters expressed divergent views on liquidity and capital requirements for Payment Account holders. Some argued that Payment Account holders should be subject to additional liquidity and capital controls to manage risk, particularly given their potential lack of operational maturity or limited experience with supervisory oversight. Conversely, other commenters recommended that the Federal Reserve tailor such controls to individual institutions and avoid imposing onerous requirements that may impede adoption.

2. Board Response

The Board recognizes commenters' concerns regarding potential risks associated with the Payment Account design. The Board acknowledges that providing direct access to financial services requires careful attention to the risk profile of requesting institutions and the potential for systemic implications.

The Board does not believe the Payment Account would increase systemic risk. The Board believes that the Payment Account's design would result in an appropriately low residual risk profile. In particular, the core design features of the Payment Account—including payment service limitations, no access to Reserve Bank intraday credit, the Closing Balance Limit, no interest on balances, and no access to the discount window—would generally mitigate the risks that Payment Account holders pose to the Reserve Banks, the payment system, and monetary policy implementation. If necessary, a Reserve Bank would retain discretion to impose additional restrictions on the use of a Payment Account or, if necessary, to terminate the account.

G. Payment Account Risk Associated With Illicit Finance

1. Summary of Comments

Just over half of the comment letters discussed risks related to BSA, AML, and countering the financing of terrorism (CFT) and related illicit finance issues. While nearly all of these commenters acknowledged the importance of the Board considering illicit finance risk in the context of the Payment Account, and for Payment Account holders to have rigorous BSA/AML/CFT programs, there was significant divergence among commenters in the criteria and conditions Reserve Banks should apply when evaluating illicit finance risks under Principle 5 of the Account Access Guidelines. Several commenters supported Reserve Banks relying on institutions' primary state or federal supervisors to supervise and assess an institution's BSA/AML/CFT compliance, while other commenters supported Reserve Banks having a stronger BSA/AML/CFT supervisory role over, or imposing additional BSA/AML/CFT conditions on, Payment Account holders.

Among the commenters supporting a stronger role for the Federal Reserve, some argued that the Reserve Banks should ensure that Payment Account holders are compliant with BSA/AML and Office of Foreign Assets Control (OFAC) requirements through periodic examinations. Others proposed that Reserve Banks impose additional controls, such as prohibiting nested transactions or imposing transaction limits until a Payment Account holder demonstrates compliance over an extended period. Among the commenters who supported the Federal Reserve relying on the primary federal or state supervisor, many noted that state-chartered institutions are required to maintain BSA/AML compliance programs and argued that the Federal

( printed page 30634)

Reserve should use compliance with these program requirements as evidence of the adequacy of an institution's BSA/AML program to avoid creating duplicative compliance regimes. Some commenters also raised the concern that by imposing additional conditions or controls, the Federal Reserve might hold Payment Account holders to higher standards relative to traditional institutions to which the Federal Reserve has historically provided accounts and services through Master Accounts. Other commenters raised concerns that newly chartered institutions may not have history or experience with effective BSA/AML/CFT compliance programs.

A few commenters discussed how new technologies either present new types of illicit finance risk, including, for example, in the form of agentic artificial intelligence (AI) in payments, or new opportunities for combatting these risks, including, for example, through the use of blockchain technology or AI.

2. Board Response

The Board agrees that all account holders, including any Payment Account holders, must mitigate illicit activity risks of their account access by complying with federal laws and regulations enacted to combat money laundering and the financing of terrorism. In practice, these means Reserve Bank accountholders must demonstrate their management of the illicit finance risks of their account access by having robust BSA/AML and OFAC compliance programs that meet the relevant regulatory and supervisory requirements, including those administered by the Financial Crimes Enforcement Network (FinCEN) and OFAC.

Most institutions that are legally eligible to maintain an account, including a Payment Account, with a Reserve Bank meet the definition of a “bank” for purposes of the BSA and, as a result, are required to maintain a comprehensive AML program that includes customer due diligence, transaction monitoring, and suspicious activity reporting.[23]

All U.S. persons, including all institutions eligible to maintain an account with a Reserve Bank, are required to comply with OFAC sanctions requirements. Institutions eligible to maintain an account with a Reserve Bank are also generally subject to examination by a primary state or federal supervisor to assess and determine their BSA/AML and OFAC compliance.

The Board does not believe that a Payment Account would present materially different illicit finance risk than a Master Account because both accounts can be used to clear and settle payments. As discussed in Section III.A.3, however, the Board is proposing to include a term for the Payment Account that confirms and reinforces that Board's expectation that the Payment Account holder demonstrates that it effectively mitigates the illicit finance risk of its account access. This term would clarify that Reserve Banks may implement illicit finance risk account terms or mitigating controls for Payment Accounts just as they may with Master Accounts.

Under Principle 5 of the Account Access Guidelines, Reserve Banks are expected to evaluate whether provision of an account and services to an institution would create undue risk by facilitating activities such as money laundering, terrorism financing, fraud, cybercrimes, economic or trade sanctions violations, or other illicit activity (illicit finance). The Guidelines note that the Reserve Bank should incorporate into its risk assessment, to the extent possible, the assessments of an institution by its state and/or federal supervisors. In addition, the Guidelines indicate that the Reserve Bank should confirm that the institution has compliance program(s) consisting of the BSA/AML components set out in the Guidelines and in relevant regulations and are designed to support compliance with OFAC regulations.

In implementing the Guidelines, the Reserve Banks have identified several account terms or risk mitigating controls available to Reserve Banks to mitigate illicit finance risk. For example, during its review of an access request, a Reserve Bank may, in its discretion, require information to augment that received from supervisory assessments of an institution's BSA/AML and OFAC compliance programs or otherwise identified by the Reserve Bank during its review. Additionally, a Reserve Bank may determine, in its discretion, that terms or risk mitigating controls are necessary to reduce the illicit finance risk associated with the provision of an account and services to an institution. A Reserve Bank may implement such requirements for a Master Account and would be able to do so for a Payment Account as well. Section III.A.3 provides examples of these informational requests, terms, and risk mitigating controls.

H. Payment Account Request Process

1. Summary of Comments

Commenters expressed divergent opinions on whether the 90-day review timeline for Payment Account access requests would provide adequate time for the Reserve Banks to assess risks. Views generally fell into three categories: (1) commenters who viewed the timeline as a significant improvement that would support innovation; (2) commenters who expressed concern that the timeline was insufficient for thorough risk assessment; and (3) commenters who supported the timeline in principle but raised concerns about consistent enforcement and implementation.

Many commenters viewed the 90-day review timeline as a significant improvement over the time it sometimes takes Reserve Banks to review requests for Master Accounts, a process which some commenters described as opaque. These commenters noted that the timeline would materially shorten review times and lower the cost of entry and uncertainty for eligible institutions seeking an account and services. One commenter characterized the timeline as a catalyst for innovation.

Conversely, some commenters expressed concern that 90 days would provide insufficient time for proper risk assessment. One commenter argued that reviews must be risk-based and take as long as necessary. Another commenter questioned whether the sufficiency and effectiveness of BSA/AML programs could be properly assessed within an expedited 90-day review period.

Several commenters questioned whether the Reserve Banks would adhere to the 90-day timeline in a consistent way. These commenters suggested that without additional clarity on eligibility expectations and procedural standards, the Payment Account may not be successful. One commenter noted that the absence of procedural standards has the potential to render the 90-day timeline ineffective because the RFI did not define what constitutes a complete account request and would allow for extensions. Another commenter cautioned that the possibility of open-ended extensions could create uncertainty that functions as a de facto denial and recommended that extensions be strictly time-limited and permitted only in exceptional circumstances.

( printed page 30635)

Several commenters discussed how, if at all, a Reserve Bank's provision of a Payment Account should influence the Reserve Bank's potential future provision of a Master Account to the Payment Account holder. A few commenters argued for a clearly defined pathway from a Payment Account to Master Account; some advocated for a defined on-ramp from one to the other. Conversely, other commenters argued against such a pathway and stated Payment Account holders should undergo the same level of review as Master Account requests do under the Guidelines.

To address these concerns, commenters made several recommendations. One commenter advocated for clearly defined timeline triggers for the 90-day review, including transparent pause and clock-stop rules to enhance consistency and transparency. Another commenter acknowledged that limited extensions may be appropriate for complex cases but maintained that reviews should generally conclude within three to six months. Some commenters suggested that the Board publish a standardized request checklist and release periodic summary statistics on approvals, denials, and typical timelines.[24]

One commenter suggested that the Board establish a specific timeline for Master Account access requests similar to the 90-day timeline proposed for Payment Accounts, arguing that such a timeline would provide greater transparency and reduce uncertainty in the application process.

2. Board Response

The Board believes the terms of the Payment Account would create a lower residual risk profile relative to a Master Account and thereby support the proposed 90-day review timeframe. Having a clear expected timeframe would create a transparent process and would help foster consistent evaluation of Payment Account access requests across all twelve Reserve Banks.

With respect to illicit finance risk, the Board does not have reasonable evidence to support the assertion that Payment Accounts would pose unique illicit finance risk. The Board believes that the Reserve Banks' experience reviewing access requests would facilitate adequate reviews of Payment Account requests in the proposed timeframe. In addition, the Board has added a term to the Payment Account to provide institutions greater clarity on what information a Reserve Bank may request an institution provide in order to support the Reserve Bank's analysis of illicit finance risk.[25]

The Board acknowledges concerns about extensions and consistent enforcement of the timeline. Consistent with the RFI, the Board is proposing that if a Reserve Bank requires additional time beyond the 90-day period to complete its review, the Reserve Bank would be expected to consult with the Board before extending the review period. As further explained in Section III.C.4, the Board believes the consultation process provides an appropriate mechanism for ensuring consistent application of the proposed review timelines. Further, the Board, in conducting its general supervision of the Reserve Banks, would monitor the extent to which Reserve Banks were processing Payment Account requests in accordance with the Guidelines.

In response to comments suggesting that the Payment Account be designed as an on- ramp to a Master Account, the Board believes that the provision of a Payment Account should not be an indication of any future provision of a Master Account. A request for a Master Account by a Payment Account holder would require a full review under the Account Access Guidelines. Although the Reserve Bank would have reviewed the Payment Account holder's request for a Payment Account under the Guidelines, the Reserve Bank would have done so in light of the Payment Account's standard terms, which substantially limit the range of risks posed. However, the Board acknowledges that a Reserve Bank's experience with a Payment Account holder could inform its review of a request for a Master Account.

In response to a comment about providing timelines for Master Account requests, the Board proposes that requests from Tier 1 institutions be reviewed generally within 45 calendar days, as discussed further in Section III.C.4.

I. Other Comments

1. Summary of Comments

Several trade associations requested the Board extend the RFI's 45-day comment period for an additional 30 days. The Board received one comment requesting that the Board deny the trade associations' extension request.

Several commenters discussed the need for consumer and privacy protections for Payment Account holders that facilitate retail transactions. These commenters expressed differing views on the appropriate level of protection, with some advocating for additional safeguards and others recommending that such protections be tailored to the payment activity or commensurate with the Payment Account holder's overall size or risk profile.

Additionally, one commenter mentioned structural inequities between traditional banks and non-traditional banks, noting that Payment Account holders would gain direct access to the Federal Reserve payment infrastructure without incurring the regulatory costs and investments that traditional banks have made, undermining competitive fairness. Another commenter suggested that the proposal could dilute the payments franchise of insured institutions with Master Accounts and that mid-size and community banks would face acute competitive pressure.

2. Board Response

The Board believes the 45-day comment period was reasonable and sufficient for commenters to review the RFI and provide meaningful input. The Board also believes it is appropriate to issue this notice, which provides more information on the proposal, so that the public has sufficient detail to consider and comment upon the proposed Payment Account.

With respect to other commenters' focus on consumer and privacy protections, the Board expects all accountholders to comply with applicable laws and regulations governing consumer protection.

III. Proposal

A. Proposal To Offer a Payment Account

The Board is proposing to set forth standard and transparent terms for the provision of Payment Accounts by Reserve Banks. The Board is proposing to create a Payment Account to support private-sector payments innovation while prudently managing the risks identified in the Account Access Guidelines.

The Board encourages Reserve Banks to pause decisions on access requests from Tier 3 institutions until the Board has completed its policy development process on the Payment Account

( printed page 30636)

proposal.[26]

A pause will allow time for the public to provide input on the proposal, and it will give the Federal Reserve the opportunity to consider this input. A pause also will ensure greater transparency, consistency, and certainty for institutions that are seeking access during this period. The Board requests that Reserve Banks implement this temporary pause until the Board has completed its policy development process with respect to the Payment Account.[27]

While eligible institutions from any tier may request a Payment Account, the Board anticipates that most Payment Account requesters would be Tier 2 or Tier 3 institutions. As explained above, access to an account and services by non-federally insured institutions (Tiers 2 and 3) presents greater and more heterogenous risks than federally insured institutions (Tier 1).[28]

Accordingly, the Board believes it is necessary that the Payment Account be designed with ex ante controls and standard terms to mitigate these risks.

A Payment Account, as the Board proposes to define it, would be a special-purpose account available to institutions that are legally eligible to maintain accounts with a Reserve Bank (regardless of their tier) for the purpose of clearing and settling payments activity for the institution and its customers.[29]

Payment Accounts would be a new, optional way for institutions to request access to accounts and services. As further described in this notice, the Payment Account's standard terms would reduce its residual risk profile facilitating a more streamlined review relative to the review of an access request from the same institution. Institutions seeking to access intraday credit or a broader set of services; to act as an OC 1 Correspondent or OC 1 Respondent (defined in Section III.A.2); or to maintain larger closing balances would retain the option of requesting a Master Account or to be an OC 1 Respondent.[30]

The Payment Account's terms would be set out in the Account Access Guidelines, the PSR Policy, the Board's Regulation A (12 CFR part 201), and the Board's Regulation D (12 CFR part 204). For convenience, the Board has included a summary of all the proposed Payment Account terms below:

Topic

Term

Implementing

document

Eligibility 31

Institutions that are legally eligible under the Federal Reserve Act or other federal statute to maintain an account at a Reserve Bank and receive services

Federal law.

Closing Balances 32

Closing balance limits would be set by the Reserve Bank for an individual Payment Account based on expected payment activity in the account, not to exceed $1 billion. There would be no limit on intraday balances in a Payment Account

PSR Policy.

Intraday Credit 33

Payment Accounts would not be permitted to access intraday credit. Transactions that would cause an overdraft would be automatically rejected

PSR Policy

Available Services 34

Only those services for which the Reserve Banks can automatically reject transactions that would cause an overdraft would be permitted to settle in a Payment Account (

i.e.,

currently, the Fedwire Funds Service, the FedNow Service, NSS, and the Fedwire Securities Service for securities transfers free of payment)

PSR Policy.

Correspondent Prohibition 35

A Payment Account holder may not act as a “Correspondent” as defined in the Reserve Bank Operating Circular No. 1 (OC 1) by permitting other legally eligible institutions to settle their services activity directly in the Payment Account

PSR Policy.

Respondent Prohibition 36

A Payment Account holder may not act as a “Respondent” as defined by OC 1 by settling its services activity directly in another institution's Master Account

PSR Policy.

Illicit Finance Risk 37

A Payment Account holder may be required to provide (ad hoc or periodically) information to demonstrate its compliance with BSA/AML and OFAC requirements 38

PSR Policy.

Discount Window 39

Payment Account holders would not be permitted to access credit from the discount window

Regulation A.

Interest on Balances 40

Balances in a Payment Account would not receive interest

Regulation D.

Excess Balance Account (EBA) Participation 41

A Payment Account holder would not be permitted to participate in an EBA

Regulation D.

Review Timeline 42

Review of Payment Account requests would generally be completed within 90 calendar days of receiving all requested documents

Account Access Guidelines.

Under

the proposal, Payment Accounts would have a consistent set of terms to mitigate the risks posed to the Reserve Banks (Principle 2 of the Guidelines), the payment system (Principle 3 of the Guidelines), financial stability (Principle 4 of the Guidelines), and the implementation of monetary policy (Principle 6 of the Guidelines). A Reserve Bank might also require a Payment Account holder to submit information to demonstrate its compliance with BSA/AML and OFAC requirements, which would mitigate illicit finance risk (Principle 5 of the

( printed page 30637)

Guidelines). Beyond the Payment Account's specified terms, the Reserve Banks would retain discretion to impose additional restrictions on a Payment Account, or to remove access to service or close an existing account, on a case-by-case basis, in the same manner and to the same extent as they can with Master Accounts.

Under the proposal, requests by Tier 2 and Tier 3 institutions for Payment Accounts, with their standard terms and resulting lower residual risk profile, would typically be reviewed by Reserve Banks in a shorter period than Master Account requests from the same institution. However, to the extent a Reserve Bank identifies any risk that it cannot evaluate in the proposed 90-day review period, the Reserve Bank would consult with the Board about extending the review period.[43]

While the Board believes that the Payment Account terms permit a streamlined review relative to a request for a Master Account from the same institution, Reserve Banks would still be expected to use the Account Access Guidelines, including its tiered review framework, to review all access requests, regardless of account type.

Payment Accounts and Master Accounts would be distinct Reserve Bank account types. As described further below, Payment Accounts would have a standard set of risk-mitigating terms designed to create a lower residual risk profile. Conversely, Master Accounts do not have a standard set of risk-mitigating terms (although Reserve Banks have discretion to impose terms on Master Accounts). Accordingly, the Board is proposing to define Master Accounts to clarify that they are separate from Payment Accounts. The proposed definition simply memorializes the existing characteristics of a Master Account. Institutions would not be permitted to have both a Payment Account and a Master Account simultaneously, which is consistent with existing Reserve Bank practice.[44]

A Payment Account holder that wants a Master Account would have to submit a new access request to its Reserve Bank, which would review the request in accordance with the Account Access Guidelines. The Board has considered comments suggesting that a Payment Account should be an on-ramp to a Master Account.[45]

Although the Reserve Bank would have reviewed the Payment Account holder's request for a Payment Account under the Guidelines, it would have done so in light of the Payment Account's unique terms, which substantially limit the range of risks posed by the Payment Account. Further, since Reserve Banks have the discretion to determine whether to grant a master account, as well as to tailor the terms of a Master Account to an institution's risk profile, conducting a full review according to the Account Access Guidelines would be necessary to ensure appropriate calibration of those terms. Holding a Payment Account would not indicate likely approval of a Master Account request, and a Reserve Bank would maintain its discretion to impose terms on the provision of any Master Account. Nevertheless, the Board recognizes that the Reserve Bank may be informed by its review of a Payment Account holder's request for a Payment Account and subsequent experience with the Payment Account holder when reviewing its request for a Master Account.

1. Terms To Mitigate Risk to the Reserve Banks

The Board is proposing several terms for Payment Accounts to manage risks to the Reserve Banks (and by extension to the American public).[46]

First, Payment Account holders would not be permitted access to intraday credit under the Board's proposed revisions to Part II of the PSR Policy, which governs the amount of intraday credit, if any, that an institution may receive from a Reserve Bank.[47]

In general, the Reserve Banks, at their discretion, may provide intraday credit to institutions with accounts at Reserve Banks to foster the smooth operation of the payment system.[48]

The Board, however, believes it would be imprudent for the Reserve Banks to extend intraday credit to Payment Account holders.

As described in the PSR Policy, an institution's eligibility for either

uncollateralized

or

collateralized

intraday credit (

i.e.,

a positive net debit cap) depends, in part, on the institution meeting certain creditworthiness standards.[49]

These eligibility requirements reflect the fact that all recipients of intraday credit, including collateralized intraday credit, pose some credit risk to the Reserve Bank.[50]

The Board has intentionally designed the Payment Account to minimize its operational complexity and risk profile to provide direct access to a basic account and services to a broader population of institutions with novel and diverse business models and risk profiles in a timely manner. Prohibiting access to intraday credit is central to the Board achieving this goal.

Several additional considerations support making intraday credit inaccessible to Payment Account holders. For one, institutions seeking Payment Accounts are unlikely to be subject to the resolution regimes that accompany federal deposit insurance. Resolution of federally insured depository institutions follows clear, consistent, and well-established rules for paying Reserve Banks and other creditors of a failed institution.[51]

Insolvency regimes applicable to uninsured Payment Account holders may be new or may involve the application of rarely invoked state and federal laws. Moreover, uninsured Payment Account holders likely would not be subject to a framework of prudential supervision and regulation that is as robust as that applied to federally insured depository institutions. Finally, data available to Reserve Banks may vary across Payment Account holders. Current credit risk monitoring at Reserve Banks relies mostly on supervisory information received from within the Federal Reserve System or from other federal regulators, and similar information on the full range of potential Payment Account holders may not be readily available. Consideration of the risks associated with providing credit to institutions subject to alternative regulatory and resolution regimes would require a level of analysis and due diligence that is likely infeasible in the

( printed page 30638)

expedited review period for Payment Account requests.

The Board has considered the comments that addressed the RFI's proposal not to permit Payment Accounts intraday credit access. For the reasons explained above and in Section II.E.2, the Board is proposing that Payment Accounts would not have access to intraday credit, either uncollateralized or collateralized. As such, an institution would need to prefund all transactions settling in its Payment Account. If an institution desires access to intraday credit, the institution should request a Master Account.

Second, and consistent with the lack of intraday credit access, the Reserve Banks would only permit Payment Account holders to access, at most, services for which the Reserve Banks can automatically reject transactions that would cause an overdraft. Currently, the Reserve Banks can implement credit-limit monitoring controls to prevent overdrafts at a service-line level for the Fedwire Funds Service, the FedNow Service, and the National Settlement Service. In addition, the Reserve Banks can prevent overdrafts caused by securities transfers over the Fedwire Securities Service by limiting Payment Account holders to securities transfers free of payment.[52]

The Board acknowledges the comments suggesting that Payment Accounts be provided with access to FedACH. As discussed in detail in Section II.B.2, the Board does not believe there is a reasonable way to allow Payment Accounts to access FedACH and effectively mitigate credit risk to the Reserve Banks without disrupting the ACH network and potentially undermining its efficiency and effectiveness. If the Reserve Banks were to change the controls that apply to their payment systems such that it becomes possible to automatically reject additional types of transactions that would cause an overdraft, the Board might reconsider the suite of services to which Payment Accounts are given access, but the Board would expect to evaluate any potential expansion of Payment Account services through public comment.

In addition to credit risk, the Account Access Guidelines include an assessment of a wide range of risks to the Reserve Banks that can arise from the provision of an account and services, such as operational and cyber risks. Today, Reserve Banks mitigate cyber and operational risk through strong risk management controls and processes, including a security and resiliency assurance program that requires institutions to attest to their compliance with Reserve Bank security requirements.[53]

Payment Account holders would be subject to the same controls, processes, and attestation requirement. Given the Payment Account's proposed simplified operational and risk profile, the Board believes Reserve Banks generally should be able to assess requesters' cyber and operational risks within the proposed 90-day review period.

2. Terms To Mitigate Risk to the Payment System

The Board is proposing a usage restriction for Payment Accounts to reduce their risk to the payment system. The Board anticipates that a Payment Account holder, like a Master Account holder, would use its account to clear and settle its depositors' and other customers' payment activity. However, the Reserve Banks' OC 1 also permits a contractually defined Correspondent-Respondent relationship in which an account holder may agree to act as a Correspondent (OC 1 Correspondent) and allow its Master Account to be used to settle certain transactions and service fees for a Respondent (OC 1 Respondent).[54]

This OC 1 Correspondent-Respondent relationship creates a materially different relationship between the Reserve Bank, the OC 1 Correspondent, and the OC 1 Respondent from a traditional relationship in which a financial institution processes payments on behalf of its depositors and customers. In particular, in an OC 1 Correspondent-Respondent relationship, an OC 1 Respondent can submit payment instructions

directly

to a Federal Reserve Bank (rather than to its OC 1 Correspondent), and the debits and credits associated with those payments settle in the Master Account of the OC 1 Correspondent. The Board proposes that Payment Account holders not be permitted to act as either OC 1 Correspondents or OC 1 Respondents because these relationships pose unique and complex risks.

Under these arrangements, multiple OC 1 Respondents can settle debits and credits associated with Federal Reserve payments in a single OC 1 Correspondent's account. Assessing the risks associated with multiple institutions settling their transactions in the Master Account of a single OC 1 Correspondent involves detailed due diligence. Additionally, if an OC 1 Correspondent fails or decides to abruptly terminate its relationship with an OC 1 Respondent, the OC 1 Respondent's continued access to services could be affected and, particularly when the OC 1 Respondent is accessing FedACH as an OC 1 Respondent, could cause challenges for other participants in the payment system.

The Board believes acting as an OC 1 Correspondent should be subject to the full review associated with the provision of a Master Account. Similarly, the Board is proposing that Payment Account holders would not be permitted to act as OC 1 Respondents. The Board reiterates, however, that this would not prevent the Payment Account holder from clearing and settling activity associated with its customers' payments activity in the Payment Account subject to the Payment Account's terms.

The Board considered whether Payment Account holders should be permitted to be OC 1 Respondents. The Board recognizes that OC 1 Respondent relationships may pose lower residual risks, for example lower credit risk to the Reserve Banks, which may result in a more streamlined review than a Master Account request from the same institution under the Guidelines. OC 1 Respondent relationships only permit access to a subset of services, although FedACH is among those included, while Master Account holders may, if approved by the Reserve Bank, potentially access all services and potentially access intraday credit.[55]

Given the potential operational complexity that could arise from an institution maintaining OC 1 Respondent status, which would be subject to a one type of review and ongoing monitoring while simultaneously holding a Payment Account, which would subject to a different type of review and ongoing monitoring, the Board is proposing that Payment Account holders not be permitted to act as OC 1 Respondents. The Board also does not anticipate that Payment Account holders would be

( printed page 30639)

interested in being OC 1 Respondents when they could instead request a Master Account.

Therefore, given the Board's goals of creating a Payment Account with a relatively simple operational and risk profile, the request for which is subject to a comparatively streamlined review to that of a request for a Master Account from the same institution, the Board does not believe the risks associated with a Payment Account holder acting as either OC 1 Correspondent or OC 1 Respondent can be sufficiently mitigated. Accordingly, the proposal would not permit Payment Account holders to act as either OC1 Correspondents or OC 1 Respondents as those terms are defined in OC1.

The Account Access Guidelines' consideration of risks to the payment system includes cyber and operational risks among the payment risk considerations. As previously discussed in Section III.A.1, given the Payment Account's proposed simplified operational and risk profile and the reliance on the assessments of requesters' primary supervisors, the Board believes Reserve Banks can assess requesters' cyber and operational risks at that time within the proposed 90-day review period.

3. Terms To Mitigate Illicit Finance Risk

Under the Account Access Guidelines, provision of a Payment Account should not create undue risk to the overall economy by facilitating illicit finance. In consideration of this principle and the comments received on the RFI, the Board is proposing to set out a non-exhaustive list of terms available to a Reserve Bank, at its discretion, to mitigate illicit finance risk associated with the provision of a particular Payment Account. If requested by the Reserve Bank, a Payment Account holder would be required to provide information related to its BSA/AML and OFAC compliance. This information would assist the Reserve Bank in its initial or ongoing assessment of the illicit finance risk associated with provision of the Payment Account. The Reserve Bank could require this additional information on an ad hoc or periodic basis depending on its individualized assessment of the institution. These informational requirements could include:

Providing the Reserve Bank with an independent, third-party assessment of the Payment Account holder's BSA/AML and OFAC compliance programs;

Providing the Reserve Bank with an attestation regarding the Payment Account holder's compliance with BSA/AML and OFAC laws and regulations;

Providing the Reserve Bank with copies of audit reports of the Payment Account holder's BSA/AML or OFAC compliance programs;

Meeting regularly with the Reserve Bank to discuss noteworthy or material BSA/AML or OFAC compliance issues;

Notifying the Reserve Bank of any BSA/AML or OFAC enforcement action taken against the Payment Account holder by a regulatory or supervisory authority; or

Notifying the Reserve Bank of any material deficiencies identified regarding the Payment Account holder's BSA/AML or OFAC compliance programs.[56]

These illicit finance terms are consistent with those the Reserve Banks already use to mitigate illicit finance risks associated with Master Accounts. The Board believes potential Payment Account holders, in particular, would benefit from the transparency provided by setting out potential illicit finance terms that a Reserve Bank might impose. The Board anticipates that Payment Account requesters are more likely to be subject to weaker or more divergent supervisory regimes and are more likely to engage in new or emerging business lines. Accordingly, Payment Account requesters could pose greater and more heterogenous risk than federally insured institutions. The above non-exhaustive list of potential terms would inform potential Payment Account holders of the illicit finance mitigants that Reserve Banks may apply to Payment Accounts.[57]

4. Terms To Mitigate Risk to Financial Stability and Monetary Policy Implementation