The Securities and Exchange Commission ("Commission") proposes to rescind amendments to its rules under the Securities Act of 1933 ("Securities Act") and Securities Exchange Act...

The Securities and Exchange Commission (“Commission”) proposes to rescind amendments to its rules under the Securities Act of 1933 (“Securities Act”) and Securities Exchange Act of 1934 (“Exchange Act”) that require registrants to provide certain climate-related information in their registration statements and annual reports.

DATES:

Comments should be received on or before August 3, 2026.

ADDRESSES:

Comments may be submitted by any of the following methods:

Send an email torule-comments@sec.gov.

Please include File Number S7-2026-19 on the subject line.

Paper Comments

Send paper comments to Vanessa A. Countryman, Secretary, Securities and Exchange Commission, 100 F Street NE, Washington, DC 20549-1090.

All submissions should refer to File Number S7-2026-19. This file number should be included on the subject line if email is used. To help the Commission process and review your comments more efficiently, please use only one method of submission. The Commission will post all comments on the Commission's website (

https://www.sec.gov/rules-regulations/public-comments/s7-2026-19). Do not include personally identifiable information in submissions; you should submit only information that you wish to make available publicly. The Commission may redact in part or withhold entirely from publication submitted material that is obscene or subject to copyright protection.

Studies, memoranda, or other substantive items may be added by the Commission or staff to the comment file during this rulemaking. A notification of the inclusion in the comment file of any such materials will be made available on the Commission's website. To ensure direct electronic receipt of such notifications, sign up through the “Stay Connected” option at

www.sec.gov

to receive notifications by email.

David Russo, Senior Counsel, in the Office of the General Counsel, at 202-551-5100, U.S. Securities and Exchange Commission, 100 F Street NE, Washington, DC 20549.

SUPPLEMENTARY INFORMATION:

The Commission is proposing to withdraw certain previously adopted but not yet effective amendments to the following rules and forms:

( printed page 33297)

I. Overview

II. Adoption of The Final Rules And Subsequent Litigation

III. Discussion of Proposed Rescission

A. Overview of Basis for Rescission: Lack of Authority and Reevaluation of Policy Grounds

B. The Final Rules Exceed the Commission's Statutory Authority

1. Scope of the Commission's Disclosure Authority

2. The Final Rules Exceed the Limitations on Mandatory Disclosures

3. The Final Rules Should Be Rescinded in Their Entirety

C. Policy Reasons for Rescinding the Final Rules

1. The Final Rules Are Unnecessary and Inconsistent With a Registrant-Specific, Materiality-Based Approach to Disclosure That Best Serves the Interests of Registrants and Investors

2. The Final Rules Stray Well Beyond the Policy Concerns of the Federal Securities Laws

3. The Final Rules Impose Significant Costs on Public Companies and Their Shareholders That Are Not Justified by the Informational Benefits They Provide to Some Investors

4. The High Costs of the Final Rules Are at Odds With the Commission's Policy Objectives of Facilitating Capital Formation and Promoting Public Company Status

IV. Economic Analysis

A. Introduction

B. Economic Baseline

1. Affected Parties

2. Current Regulatory Framework

3. Current Market Practices

C. Benefits and Costs

1. Benefits

2. Costs

3. Aggregate Monetized Benefits and Costs

D. Anticipated Effects on Efficiency, Competition, and Capital Formation

E. Reasonable Alternatives

F. Request for Comment

V. Paperwork Reduction Act

VI. Initial Regulatory Flexibility Act Analysis

A. Reasons for, and Objectives of, the Proposed Action

B. Legal Basis

C. Small Entities Subject to the Proposed Amendments

D. Projected Reporting, Recordkeeping, and Other Compliance Requirements

E. Duplicative, Overlapping, or Conflicting Federal Rules

F. Significant Alternatives

G. Request for Comment

VII. Congressional Review Act

VIII. Other Matters

Statutory Authority

I. Overview

We propose to rescind the climate-related disclosure rules adopted by the Commission in 2024 (“Final Rules”).[3]

Congress gave the Commission certain specific powers within the Federal securities laws. Among those powers, the Commission's governing statutes authorize the agency to except from or add to the mandatory items of disclosure specified in the Securities Act and the Exchange Act.[4]

This authority, however, is limited by the text and context of these statutes. Furthermore, even when acting pursuant to an explicit grant of authority, it is incumbent on the Commission to implement a disclosure regime that elicits material information

( printed page 33298)

for investors while being mindful of the costs imposed on registrants to collect and disclose that information. When the Commission loses sight of these considerations, it risks not only imposing undue costs on registrants [5]

and impeding capital formation, but also harming the very investors it seeks to protect.

The Final Rules were a dramatic overreach of the Commission's statutory authority and, independently, unsound as a matter of policy. Based on an incorrect view of the scope of its authority, the Commission determined that it was appropriate to prescribe dozens of pages of highly specific disclosure rules solely about climate-related matters [6]

and apply the bulk of those rules to virtually all public companies, regardless of size, industry, or specific circumstances.

The Final Rules also discounted the role of market forces in the flow of information between registrants and investors. Disclosures mandated by the Commission are only some of the information registrants provide to the marketplace. Investors and analysts often demand additional information about a wide range of topics depending on their particular investment strategies or non-investment interests. Registrants in turn may voluntarily provide such information depending on the nature of their business and the investor base they wish to attract. We expect this market-driven flow of information will continue following a rescission of the Final Rules, but it is not the Commission's role to require disclosure of particular information because it is useful for any one investment strategy or desired by some political interests for the purpose of influencing business practices. Rather, in exercising its authority to

mandate

disclosure within the statutory limits imposed by Congress, the Commission should seek to adopt rules that elicit information pursuant to the standard of materiality established by the Supreme Court: information that a reasonable investor would consider important in buying or selling securities.[7]

Accordingly, as discussed in more detail in the sections that follow, we propose to rescind the Final Rules in their entirety because they exceed the statutory limits on the Commission's disclosure authority. Furthermore, even if the Commission had authority to adopt the Final Rules, several independent policy reasons support their rescission, including that:

The Final Rules are unnecessary and inconsistent with a registrant-specific, materiality-based approach to disclosure;

The Final Rules stray well beyond the policy concerns of the Federal securities laws;

The Final Rules impose substantial costs that are not justified by the informational benefits they may provide to some investors; and

The Final Rules are at odds with the Commission's policy objectives of facilitating capital formation and promoting public company status.

II. Adoption of the Final Rules and Subsequent Litigation

On March 21, 2022, the Commission proposed rules that would require registrants to include extensive new climate-related disclosures in their registration statements and periodic reports, including detailed information about the impact and management of climate-related risks, GHG emissions, scenario analysis, internal carbon prices, and certain climate-related financial statement effects.[8]

The Proposing Release was highly contentious,[9]

and in response, the Commission received a large number of comments from a variety of market participants, environmental lobbying groups, and members of the public expressing starkly divergent views about the proposed rules.[10]

Some commenters supported the proposed rules, stating that climate-related risks can have material impacts on a company's financial position or performance.[11]

Commenters in support of the proposed rules indicated, among other things, that adoption of mandatory, climate-related disclosure rules would improve the timeliness, quality, and reliability of climate-related information, which would facilitate investors' cross-company comparisons of climate-related risks and lead to more accurate securities valuations.[12]

Many other commenters opposed the proposed rules and requested either that the Commission not adopt the proposal or make significant revisions in the Final Rules.[13]

Some commenters asserted that the Commission lacked statutory authority to adopt the proposed rules.[14]

Others stated that existing voluntary reporting practices were sufficient to serve the needs of investors and markets such that the proposed rules were unnecessary.[15]

Opposing commenters further stated that the proposed rules were overly prescriptive, that they were not bound in every instance by a materiality qualifier, that their adoption would result in the disclosure of a large volume of immaterial information that would be confusing to investors, and that mandating such disclosure requirements would impose a significant burden on registrants while resulting in few additional benefits for investors.[16]

On March 6, 2024, the Commission approved the Final Rules by a 3-2 vote. While the Final Rules included changes from the proposal in response to commenter concerns, the adopted regulations continued to include numerous, highly prescriptive disclosure requirements. To house the extensive new disclosure requirements, the Final Rules created a new subpart 1500 of Regulation S-K [17]

and a new Article 14 of Regulation S-X.[18]

Among other things, the Final Rules require a registrant to consider and possibly disclose the following detailed items:

If a registrant is a large accelerated filer (“LAF”), or an accelerated filer (“AF”) that is not otherwise exempted, and its Scope 1 emissions and/or its Scope 2 emissions metrics [19]

are material, certain disclosure about those emissions, including:

The volume of the emissions disclosed separately and each expressed

( printed page 33299)

in the aggregate, in terms of CO2

e [20]

and, if any constituent gas of the disclosed emissions is individually material, such constituent gas disaggregated from other gases;

Scope 1 emissions and/or Scope 2 emissions in gross terms by excluding the impact of any purchased or generated offsets;

The methodology, significant inputs, and significant assumptions used to calculate the GHG emissions;

The organizational boundaries used when calculating the registrant's disclosed GHG emissions, including the method used to determine those boundaries;

The operational boundaries used, including the approach to categorization of emissions and emissions sources; and

The protocol or standard used to report the GHG emissions, including the calculation approach, the type and source of any emission factors used, and any calculation tools used to calculate the GHG emissions; [21]

If a registrant's use of internal carbon pricing is material, the price per metric ton of CO2

e and the total price, including how the total price is estimated to change over certain time periods; [22]

Any climate-related risks that have materially impacted or are reasonably likely to have a material impact on the registrant, including on its strategy, results of operations, or financial condition; [23]

Any oversight by the board of directors of climate-related risks, regardless of the materiality of those risks, and any role by management in assessing and managing the registrant's material climate-related risks; [24]

Any processes the registrant has for identifying, assessing, and managing material climate-related risks and, if the registrant is managing those risks, whether and how any such processes are integrated into the registrant's overall risk management system or processes; [25]

and

If a registrant has set a climate-related target or goal that has materially affected or is reasonably likely to materially affect the registrant's business, results of operations, or financial condition, certain disclosures about such target or goal, including material expenditures and material impacts on financial estimates and assumptions as a direct result of the target or goal or actions taken to make progress toward meeting such target or goal.[26]

With respect to financial statement disclosures:

The capitalized costs, expenditures expensed, charges, and losses incurred as a result of severe weather events and other natural conditions, such as hurricanes, tornadoes, flooding, drought, wildfires, extreme temperatures, and sea level rise, subject to applicable one percent and de minimis disclosure thresholds; [27]

The capitalized costs, expenditures expensed, and losses related to carbon offsets and renewable energy credits or certificates (“RECs”) if used as a material component of a registrant's plans to achieve its disclosed climate-related targets or goals; [28]

and

If the estimates and assumptions a registrant uses to produce the financial statements were materially impacted by risks and uncertainties associated with severe weather events and other natural conditions, such as hurricanes, tornadoes, flooding, drought, wildfires, extreme temperatures, and sea level rise, or any disclosed climate-related targets or transition plans, a qualitative description of how the development of such estimates and assumptions was impacted.[29]

In addition, registrants that are required to disclose Scopes 1 and/or 2 emissions must file an attestation report of those emissions subject to phased-in compliance dates.[30]

Further, the Final Rules require a registrant that is not required to disclose its GHG emissions or to include a GHG emissions attestation report pursuant to the Final Rules to disclose certain information if the registrant voluntarily discloses its GHG emissions in a Commission filing and voluntarily subjects those disclosures to third-party assurance.[31]

The Final Rules exempt certain registrants from disclosure in limited circumstances.[32]

Outside these limited circumstances, the Final Rules require almost every registrant to comply with the vast majority of the new disclosure requirements after a transition period.[33]

As the Adopting Release noted, nearly every registrant will be required to start complying with the Final Rules by the fiscal year beginning in 2027.[34]

Within 60 days of the Commission's adoption of the Final Rules on March 6, 2024, various parties petitioned for judicial review in multiple Federal courts of appeals.[35]

On March 19, 2024, the Commission filed a Notice of Multicircuit Petitions for Review with the Judicial Panel on Multidistrict Litigation (“JPML”), and on March 21, 2024, the JPML issued an order consolidating the petitions for review in the U.S. Court of Appeals for the Eighth Circuit (“Eighth Circuit”).[36]

On April 4, 2024, the Commission, citing its authority pursuant to the Exchange Act [37]

and the Administrative Procedure Act,[38]

entered a stay of the Final Rules and ordered that “the Final Rules [would be] stayed pending the completion of judicial review of the consolidated Eighth Circuit petitions.” [39]

On March 27, 2025, the Commission voted to end its defense of the rules. The Commission staff sent a letter to the court stating that the Commission withdraws its defense of the rules and that Commission counsel are no longer authorized to advance the arguments in the brief the Commission had filed. Thereafter, on September 12, 2025, the Eighth Circuit issued an Order holding the consolidated petitions for review in abeyance “until such time as the . . . Commission reconsiders the challenged Final Rules by notice-and-comment

( printed page 33300)

rulemaking or renews its defense of the Final Rules.” [40]

The Eighth Circuit explained that it is the Commission's “responsibility to determine whether its Final Rules will be rescinded, repealed, modified, or defended in litigation.” [41]

As a result of the current procedural posture, the Final Rules remain stayed. The court has not made any decision on the merits of any arguments presented by any petition for review of the Final Rules.

III. Discussion of Proposed Rescission

A. Overview of Basis for Rescission: Lack of Authority and Reevaluation of Policy Grounds

As noted above, we are proposing to rescind the Final Rules in their entirety because they exceed the scope of the Commission's statutory authority. In addition, even if a court were to find that the Commission had authority to adopt the Final Rules, we have independent, compelling policy reasons to rescind the rules in their entirety. The Final Rules are unnecessary and inconsistent with a registrant-specific, materiality-based approach to disclosure that best serves the interests of registrants and investors; stray well beyond the policy concerns of the Federal securities laws; impose substantial costs on public companies and their shareholders that are not justified by the informational benefits they may provide to some investors; and are at odds with the Commission's policy objectives of facilitating capital formation and promoting public company status.

B. The Final Rules Exceed the Commission's Statutory Authority

A fundamental principle of constitutional and administrative law is that an administrative agency must act within its statutory authority.[42]

An agency acts unlawfully when it exercises power beyond its authority.[43]

Agencies must respond to their own unlawful acts; as the Supreme Court recently put it, illegal agency action “presumably requires remedial action of some sort.” [44]

The proper remedy for the Commission's lack of statutory authority to adopt the Final Rules is rescission.

An agency's rulemaking power is determined by examining the text and context of the relevant statutory provisions. Statutory provisions are not read in isolation; courts look to their place in the overall statutory scheme.[45]

Courts also apply the major questions doctrine to determine the lawfulness of agency action.[46]

In the Federal securities laws, Congress required specific disclosures for registrants conducting public offerings in the United States or registering securities for trading on U.S. exchanges. When enacting the Securities Act and the Exchange Act, Congress explicitly called for disclosures of items central to an understanding of a registrant's business, operation and performance, financial condition, directors, management and control, capital structure, the rights of security holders, and the terms of a registered offering.[47]

These disclosures provide investors with operational and financial information particular to the circumstances of the registrant.

Congress also granted the Commission authority to adopt rules eliminating, substituting, or adding certain disclosures. When adopting such a rule, the Commission must follow the directives and guardrails in the text and context of the governing statutes, as discussed below.

When the Commission exercises its legal authority to adopt a disclosure rule under the statutes discussed below, in certain instances it must also determine whether the action is necessary or appropriate in the public interest.[48]

When making such a public interest determination, the Commission must “consider, in addition to the protection of investors, whether the action will promote efficiency, competition, and capital formation.” [49]

These considerations are constraints on the exercise of authority, not sources of authority.

Courts have also recognized that federalism limits the Commission's rulemaking authority in areas of corporate governance regulated by State law.[50]

Congress has traditionally left

( printed page 33301)

corporate governance to the States to regulate, and it has spoken clearly on the rare occasions when it has shifted that balance.[51]

As discussed below, the Final Rules do not satisfy the statutory criteria for adopting additional disclosure provisions under the Securities Act or Exchange Act. The disclosures compelled by the Final Rules are not within the scope of the categories of disclosures Congress required and do not comport with the directives Congress set for excepting from, substituting, or adding to those disclosures. They also improperly intrude on State corporate law without a statutory directive. Accordingly, we propose to rescind the Final Rules in their entirety.

1. Scope of the Commission's Disclosure Authority

We first examine the text and context of Congress's directions on mandatory disclosures and then consider the Commission's ability to make changes to them. The main statutory provisions discussed in the Adopting Release were sections 7(a)(1) [52]

and 19(a) [53]

of the Securities Act and sections 12,[54]

13 [55]

and 23(a)(1) [56]

of the Exchange Act.[57]

a. Text of the Disclosure Rulemaking Statutes in the Securities Act and Exchange Act

Section 7(a)(1) of the Securities Act establishes that Schedule A [58]

is the base disclosure for a registration statement and also permits the Commission to except from or add to the disclosure requirements enumerated in Schedule A. Section 7(a)(1) provides that a registration statement for a public offering “shall contain the information” and documents “specified in Schedule A” of the Securities Act.[59]

Schedule A contains 32 disclosure items, such as the business of the company, its capital structure, use of proceeds from the sale of securities, director and officer compensation, material contracts, the terms of the offering and detailed balance sheet and profit or loss statements.

Section 7(a)(1) gives the Commission the authority to except from or add to Schedule A's required disclosures in certain circumstances. The Commission may by rule provide that a class of issuers does not need to include information listed in Schedule A if the Commission finds that the information is not applicable to that class “and that disclosure fully adequate for the protection of investors is otherwise required to be included within the registration statement.” Section 7(a)(1) concludes with a provision authorizing the Commission to add disclosure requirements to Schedule A: “Any such registration statement shall contain such other information, and be accompanied by such other documents, as the Commission may by rules or regulations require as being necessary or appropriate in the public interest or for the protection of investors.” [60]

Section 12 of the Exchange Act similarly requires certain categories of disclosures while allowing the Commission to prescribe the level of detail and to alter the requirements under specified conditions. Section 12 stipulates the information to be filed and made public by a company registering a class of securities on a national securities exchange or that is required to register a class of equity securities under the Exchange Act. Section 12(b)(1) provides that a registration statement must contain 12 enumerated categories of information, such as the financial structure and nature of the business, the terms of classes of securities, the financial interests of directors and officers in the company, certain material contracts, and certain financial statements.[61]

Within those 12 categories, the Commission may require a registration statement to include “[s]uch information, in such detail,” as to the issuer and any control persons “as necessary or appropriate in the public interest or for the protection of investors . . . .” [62]

Section 12(c) gives the Commission the authority to determine that an item listed in section 12(b) is not applicable to a class of issuers. If it does, “the Commission shall require in lieu thereof the submission of such other information of comparable character as it may deem applicable to such class of issuers.” [63]

Unlike section 7(a)(1) of the Securities Act, section 12 of the Exchange Act does not otherwise permit the Commission to add to the list of disclosure items in section 12(b).

Section 13(a) of the Exchange Act provides the Commission with authority to prescribe periodic disclosure rules for issuers with securities registered under section 12.[64]

The Commission shall require such an issuer “to keep reasonably current the information and documents required to be included in or filed with” an application or registration statement [65]

and may require the issuer to file annual and quarterly reports.[66]

Any rules promulgated under section 13 must be “necessary or appropriate for the proper protection of investors and to insure fair dealing in the security.” [67]

As with section 12(c), section 13(c) instructs that if the Commission concludes “any report required under subsection (a) in inapplicable to any specified class or classes of issuers, the Commission shall require in lieu thereof the submission of such reports of comparable character as it may deem applicable . . . .” [68]

( printed page 33302)

These statutory provisions establish the Commission's power to compel disclosures in public offerings and by companies registering securities for public trading. Congress restricted the information an issuer or reporting company must disclose to items central to an understanding of the company's business or financial characteristics. These categories of information are fundamental to valuing the risks and returns of an investment in the registrant's securities.

b. The Commission's Authority To Change Mandatory Disclosures

As noted above, Congress permitted the Commission to make changes to the mandatory disclosures within certain limits. In this way, Congress contemplated developments in mandatory disclosure requirements but gave context and guidance for them in the governing statutes.

The relevant part of section 7(a)(1) of the Securities Act states that the Commission may require the disclosure of “such other information” not adequately covered by Schedule A if such item is “necessary or appropriate in the public interest or for the protection of investors.” [69]

Section 7(a)(1) also provides that the Commission may exclude from or adopt a substitute for an item in Schedule A for a class of issuers if it finds the item is not applicable and “that disclosure fully adequate for the protection of investors is otherwise required to be included within the registration statement.” [70]

Section 12(b)(1) of the Exchange Act authorizes the Commission to determine the “detail” for the twelve enumerated categories of disclosures listed by Congress for applications to register securities on an exchange or in certain other circumstances.[71]

And if one of those enumerated categories “is inapplicable to any specified class or classes of issuers,” the Commission “shall require in lieu thereof the submission of such other information of comparable character as it may deem applicable to such class of issuers,” [72]

closely tying the Commission's power to modify the required disclosures to Congress's original specifications. Under section 13(a) of the Exchange Act, the Commission has authority to prescribe rules requiring issuers with securities registered under section 12 “to keep reasonably current” the information and documents required by section 12(b)(1) for the registration statement and to file annual and quarterly reports.

The Securities Act and Exchange Act work together in certain circumstances. Experience with disclosures of reporting companies under section 12 of the Exchange Act may inform the Commission about the need for or inapplicability of disclosures under section 7(a)(1) of the Securities Act. Detailed disclosures or disclosures of comparable character or current information added under section 12 for reporting companies may also guide the Commission's determination about disclosures necessary for the protection of investors in a registration statement required by the Securities Act. This interrelationship between statutory provisions provides the foundation for the Commission's existing integrated disclosure system.

The Commission's rulemaking with respect to disclosures must be “channel[ed]” by and comparable to the kinds of disclosures recited in the statutes,[73]

which refer to a registrant's business or financial characteristics. This follows from the text of the Commission's enabling statutes. As previously discussed, section 12 of the Exchange Act authorizes the Commission to specify the “detail[s]” surrounding Congress's chosen topics [74]

and to substitute those topics with others for certain issuers—provided (among other things) that those substitute disclosures are “in lieu of” Congress's specified fields and “of comparable character.” [75]

Other requirements in sections 7(a)(1), 12(b)(1), and 13(a) also guide the Commission in exercising its authority to adopt disclosure rules. The Commission must determine that a rule is “necessary or appropriate in the public interest or for the protection of investors.” That public interest determination also requires consideration of efficiency, competition, and capital formation.[76]

To be necessary, an addition to required disclosures should cover information not adequately elicited by an existing mandatory disclosure. To be appropriate, the additional disclosures must elicit information comparable to that elicited by the disclosures specified by Congress.

Courts have consistently held that the inclusion of the “words ‘public interest’ in a regulatory statute is not a broad license to promote the general public welfare. Rather, the words take meaning from the purposes of the regulatory legislation.” [77]

The purposes, in turn, are discerned from the text and context of a statute, which limits the scope of what is necessary or appropriate.[78]

For mandatory disclosures in public offerings or periodic reports, this means that any additional, substitute, or more detailed disclosure requirements must be related to the registrant's business or financial characteristics.[79]

Congress did not license the agency to act as a “roving commission to inquire into [the] evils” of corporate behavior “and upon discovery correct them.” [80]

Indeed, the

( printed page 33303)

fact that Congress required the Commission to consider efficiency, competition, and capital formation when making a public interest determination further illustrates that “public interest” was not intended to be construed in some vague, open-ended sense but rather in terms of the public interest in well-functioning securities markets.

Likewise, the words “protection of investors” do not empower the Commission to mandate any disclosure that an investor may find useful or desirable.[81]

In the Adopting Release, the Commission made general assertions that climate-related information was “important” to investors [82]

and that the Final Rules would make the disclosures more consistent, comparable, and reliable.[83]

Those considerations may play a role in the Commission's assessment of whether a potential disclosure obligation is necessary or appropriate or promotes efficiency and capital formation, but they are not a freestanding statutory authorization to expand disclosure beyond the types of information Congress specified. If they were, there would be no meaningful limits on the Commission's statutory authority.[84]

Under such a reading, the Commission could mandate disclosure about virtually any topic, however contentious, esoteric, or parochial, provided that some subset of investors may find the information relevant to their decisions to buy or sell the registrant's securities.

Expansive notions of the public interest and protection of investors do not provide a basis for straying beyond the types of business or financial characteristics that Congress specified. Generalized invocations of “importance to” and “interests of” investors or “investor demand” [85]

are not adequately grounded in the text, context, and limitations of the law to provide a basis for rulemaking. The statutes also do not mention consistency or comparability as a basis for a disclosure rule. Notwithstanding the Commission's assertions in the Adopting Release, these justifications do not authorize the Commission to “update and build on” the disclosures specified in the Federal securities laws “by requiring additional disclosures of information.” [86]

Materiality is also a key part of the Commission's application of legal authority when it adopts disclosure rules. Information is material if there is a substantial likelihood that a reasonable investor would consider it important or significant in deciding whether to buy or sell a security.[87]

The common interest of reasonable investors is in information regarding the financial performance of a company, the pricing of securities, and the prospect for economic and financial return from the disclosing company.[88]

Accordingly, materiality is a concept inherently rooted in financial considerations.

While “materiality” is not referenced in the statutory provisions that were relied upon to promulgate the Final Rules and does not itself provide a separate basis for a disclosure obligation, this concept bears directly on the Commission's consideration of investor protection, efficiency, and capital formation. Immaterial disclosures do not further the “public interest” or “protection of investors”—indeed, they are likely to frustrate such objectives. The materiality standard filters out information that a reasonable investor would not consider important, protects investors from being buried in an avalanche of trivial information, and prevents the registrant from having to collect and disclose every minor detail about its operations.[89]

Therefore, assuring that mandatory disclosures elicit material information is frequently part of the Commission's required determination that such disclosures advance the goals of investor protection, efficiency, and capital formation.

The Commission's accepted past practices illustrate these limits on its authority in operation. Current Regulation S-K, for example, contains instances of the Commission exercising its authority to adopt disclosure rules based on enumerated items of disclosure in Schedule A of the Securities Act and section 12(b)(1) of the Exchange Act. For example, Schedule A requires disclosures about securities held by officers, directors, promoters, and large shareholders and their intention to subscribe to purchases under the registration statement (paragraph 7) and the purposes for which the offered securities will supply funds (paragraph 13), but Schedule A does not explicitly require disclosures about shareholders intending to sell securities pursuant to the registration statement. Item 507 of Regulation S-K [90]

requires disclosures about the names of selling shareholders, their material relationships with the issuer, and the amount they plan to sell, but these disclosures are “channel[ed]” by the kinds of disclosures recited in paragraphs 7 and 13 of Schedule A.[91]

As another example, to address concerns with managerial self-dealing, paragraphs 14, 20, 22, and 24 of Schedule A and section 12(b)(1)(D) through (F) require disclosures of remuneration to officers, directors, underwriters, and “other persons” over certain dollar amounts and the interests of directors, officers, and large shareholders in the securities of the issuer and material contracts they have with the issuer. Item 404 of Regulation S-K,[92]

which requires disclosure about

( printed page 33304)

transactions with related persons, is not identical to the enumerated items in Schedule A, but it is channeled by Schedule A's disclosures concerning managerial self-dealing. Similarly, Item 404 spells out certain details related to the section 12(b)(1) disclosures.[93]

The ability to require substitute or added disclosures also enables the Commission to adapt current disclosure rules for novel financial assets or transaction structures that qualify as securities or securities transactions, subject to the same directives and guardrails discussed above. For example, instead of remuneration or payments to officers, directors, and promoters, the Commission could substitute “information of comparable character.” [94]

When read in the context of the mandatory disclosures in sections 7(a)(1) and 12(b)(1), it is clear that these statutes do not authorize the Commission to mandate any and all information that it deems desirable. Nor does section 13(a) give the Commission a general, freestanding power to mandate ongoing disclosures.[95]

Rather, disclosure rules adopted by the Commission must be “channel[ed]” by [96]

and comparable to the disclosures Congress specified in the Acts, which concern the registrant's business or financial characteristics. Despite suggestions to the contrary in the Adopting Release, the Commission is not free to construct a new disclosure regime out of whole cloth. In adopting the Final Rules, the Commission did not sufficiently adhere to these limits or determine the best interpretation of the relevant statutes.[97]

Instead, the Commission relied on an impermissibly broad reading of its statutory authority.

2. The Final Rules Exceed the Limitations on Mandatory Disclosures

The Final Rules did not respect the limitations on the Commission's authority and are fundamentally different from the types of enumerated disclosures found in the Commission's governing statutes. Those enumerated disclosures refer to a company's business or financial characteristics. By contrast, the Final Rules mandate highly specific and granular information on the sole topic of climate-related matters, such as operational and governance practices and internal metrics (including GHG emissions) that many registrants may not track or use for business purposes.[98]

These disclosure obligations do not fit within the powers conferred by the statutes discussed above. While the Commission in certain other circumstances has required disclosures that are tailored to specific risks facing the disclosing company in a particular industry,[99]

no prior example comes close to the breadth of disclosures required by the Final Rules, which apply across the board. The Final Rules are not comparable to the disclosures called for by the Commission's governing statutes, which refer to a company's business or financial characteristics.

The subject of each new disclosure mandated by the Final Rules, by contrast, was climate-related risks and strategies for managing those risks, as well as the financial statement effects of severe weather events and other natural conditions. Many of these disclosures were only secondarily or remotely about the past or immediate effects of climate-related matters on the operations, revenue, expenses, capital structure, liquidity, management or controlling shareholders of the registrant. For example, the Final Rules require disclosure about climate-related impacts on third parties (such as suppliers, purchasers, or counterparties to material contracts) [100]

as well as transition risks—defined expansively to include, among other things, “the actual or potential negative impacts on a registrant's business . . . attributable to regulatory, technological, and market changes, . . . changes in law or policy, reduced market demand for carbon intensive products, . . . [and] competitive pressures associated with the adoption of new technologies, and reputational impacts . . . .” [101]

The Final Rules also require the disclosure of internal analysis and metrics, such as scenario analysis [102]

and internal carbon prices.[103]

As discussed above, the Commission's disclosure authority under its governing statutes must be construed in light of the text and context of the surrounding statutory provisions. Nothing in these provisions expressly empowers the agency to burden public companies and their shareholders with such detailed (and costly) disclosures about one particular topic. Indeed, the scope of the Final Rules stands in stark contrast to the more limited and targeted disclosures the Commission has previously required on environmental matters, as discussed in section III.C.1.a.

Nor does the inclusion of materiality qualifiers salvage the Final Rules from their legal defects. While the Adopting Release claimed that such qualifiers would limit the scope, and therefore the burdens, of the Final Rules, as discussed in more detail in section III.C.3, the use of such qualifiers in such a complex, interconnected, and highly prescriptive set of disclosure requirements does not adequately cabin those requirements within the bounds of the Commission's authority. In particular, while the requirement to disclose Scope 1 and Scope 2 GHG emissions is qualified by materiality,[104]

it nonetheless requires covered registrants to devote significant time and resources to measure their emissions and determine whether they are material, including establishing organizational boundaries and operational boundaries and adopting a specific reporting protocol or standard.[105]

Only after it has invested potentially significant resources to perform this exercise can a registrant make a determination about whether such metrics are material and therefore must be disclosed.[106]

Rather than limiting the costs and burdens of the Commission's emissions reporting requirements, the rule's materiality qualifier effectively compels covered registrants to track and evaluate a metric

( printed page 33305)

they may not otherwise use for business purposes.

Similarly, invoking the impact of climate-related risks on a registrant's business, results of operations, or financial condition is not sufficient, in itself, to justify the Final Rule's myriad highly specific disclosure requirements. For example, the Final Rules require registrants to provide disclosures regarding their use of transition plans,[107]

scenario analysis,[108]

and internal carbon prices, if material.[109]

The Adopting Release repeatedly asserted that such disclosures were necessary to value a registrant's securities or evaluate its financial performance,[110]

but the exceedingly granular nature of the information required by the Final Rules goes well beyond what must be disclosed in respect of the many other factors that may affect the valuation of a registrant's securities. As noted above, to be necessary, an addition to required disclosures should cover material information not adequately elicited by an existing mandatory disclosure. When climate change or other environmental issues, including transition risk, have materially affected the operations or financial performance of a specific company, existing disclosure rules require discussion of the effects. Indeed, the Commission's

Guidance Regarding Disclosure Related to Climate Change[111]

lists a variety of specific existing disclosure obligations that, depending on the particular circumstances of a company, could require disclosure of climate change matters. For example, Item 303 of Regulation S-K requires, among other things, a company to disclose and discuss any known trend or uncertainty that has had a material positive or negative consequence for the company's results of operations.[112]

The fact that existing disclosure obligations already serve to provide investors with material information about climate-related matters reinforces the conclusion that the Final Rules are not “necessary” to protect investors.[113]

Indeed, they may even serve to harm investors by eliciting information about climate-related matters that goes well beyond what a reasonable investor needs to make an informed investment decision.[114]

In addition to creating a disclosure regime far beyond the kind authorized by the Commission's enabling statutes, the Final Rules also intrude on State authority over core matters of corporate governance. “No principle of corporation law and practice is more firmly established than a State's authority to regulate domestic corporations.” [115]

Although the Final Rules purport to require issuers only to

disclose

information, the effect of their requirements is to impermissibly regulate issuers' internal affairs. The many “ifs” in the Final Rules are telling in this regard. While framed in terms of risks to and impacts on the registrant, the disclosure mandates in the Final Rules effectively provide an aspirational framework for how public companies should manage climate-related matters.

The Commission's existing rules typically require disclosure of ongoing compliance or legal matters when they are material—they do not pressure or require registrants to create and maintain dedicated risk management systems that prioritize one category of risks above all others.[116]

By contrast, the Final Rules create a highly detailed and prescriptive regime focused on a single category of risk.[117]

For example, the Final Rules require disclosure of the board of directors' role in managing climate-related risks, which overlaps with existing disclosure requirements related to the role of the registrant's board in risk oversight.[118]

In addition, while materiality qualifiers were added at the adopting stage, given the detailed nature of the requirements, the Final Rules effectively require many registrants to conduct new analyses or gather new data for the sole purpose of determining

whether

they have a disclosure obligation.[119]

To house these extensive new reporting requirements, the Commission created a new subpart 1500 of Regulation S-K as well as a new Article 14 of Regulation S-X. Each of these regulations contain detailed line item requirements related to such varied matters as transition plans,[120]

scenario analysis,[121]

internal carbon prices,[122]

GHG emissions,[123]

and the aggregate amount of carbon offsets and RECs expensed.[124]

Most of these items apply equally across all types of registrants. The anticipated response of registrants to the creation of such a detailed regime dedicated to a single category of risks is clear: all registrants will pay attention to climate-related matters and dedicate significant board, executive, and employee resources to manage them. This broad mandate interferes with the management of companies and trenches

( printed page 33306)

upon the traditional role of States in regulating corporations.[125]

On the rare occasions when Congress has intervened in corporate governance, it has given explicit direction for the Commission to do so.[126]

Congress has not done so with respect to management of climate-related matters. Such a conduct-altering regime, unrelated to managerial self-dealing,[127]

simply was not contemplated by Congress when it specified the fundamental disclosures that a registrant should provide when conducting a public offering in the United States or trading in U.S. markets. This effort to regulate corporate management interferes with the role of the States in regulating corporate governance and contravenes the “clear statement” rule that the Supreme Court applies when regulatory actions raise federalism concerns.[128]

The past practices the Commission cited in the Adopting Release also do not justify the Final Rules. According to the Supreme Court, “[i]t is telling” when an agency that “has never before adopted a broad . . . regulation” over many decades now seeks to do so, suggesting “that the mandate extends beyond the agency's legitimate reach.” [129]

Until the Final Rules, the Commission had never before adopted a sweeping set of disclosure requirements on climate-related issues; indeed, in prior years, it specifically declined to do so.

In adopting the Final Rules, the Commission pointed as precedent to environmental disclosure requirements first adopted in the 1970s, asserting that “the Commission for the last fifty years has also required disclosure about various environmental matters.” [130]

But a complete and balanced reading of the record from the 1970s about environmental disclosures tells a different story. The dominant themes from the Commission at the time were doubts about its powers and how investors would use Commission-mandated environmental disclosures.[131]

The narrow disclosures adopted in the 1970s were in response to a specific congressional directive contained in the National Environmental Policy Act of 1969 (“NEPA”),[132]

which required the Commission and other Federal agencies to develop procedures to consider environmental values in decision-making. In 1975, in considering its obligations under NEPA, the Commission noted that “it is generally not authorized to consider the promotion of social goals unrelated to the objectives of the Federal securities laws.” [133]

It further observed that “the discretion vested in the Commission under the Securities Act and the Securities Exchange Act to require disclosure which is necessary or appropriate `in the public interest' does not generally permit the Commission to require disclosure for the sole purpose of promoting social goals unrelated to those underlying these Acts.” [134]

Rather, disclosure mandates under the Federal securities laws had to relate to the financial condition of, and matters of economic significance to, the disclosing company.[135]

The Commission therefore proposed and ultimately adopted a small number of narrow rules generally consistent with the disclosure framework in the Federal securities laws. For example, under the 1975 amendments, a reporting company must disclose material effects on capital expenditures, earnings, and competitive position from compliance with government environmental regulation.[136]

The 1975 rules did not include disclosure about environmental strategies or plans or board oversight of environmental risks; nor did they include expansive requirements that companies track and assess the environmental impact of their operations.

As recently as 2016, the Commission reconsidered its authority to require disclosures on environmental and social issues as part of a concept release on the business and financial disclosure requirements in Regulation S-K.[137]

Summarizing its 1975 conclusion on lack of statutory authority, the Commission observed that, in 1975, following extensive proceedings on these topics, the Commission concluded that it “generally is not authorized to consider the promotion of goals unrelated to the objectives of the federal securities laws when promulgating disclosure requirements, although such considerations would be appropriate to further a specific congressional mandate.” [138]

The Commission also observed that, since 1975, Congress had not given new statutory authority for disclosures in these areas.[139]

While the

( printed page 33307)

Commission in 2016 stated that the “role of sustainability and public policy information in investors' voting and investment decisions may be evolving” and solicited comment on the need for new sustainability and social disclosures, it also noted concerns about such disclosures and ultimately determined in 2020 to revise, but not significantly expand upon, the provisions adopted in 1975.[140]

In sum, until the Final Rules, the Commission has consistently declined to use its statutory authority to mandate expansive environmental disclosures; instead, the Commission has required certain targeted disclosures about regulatory compliance and legal liability that directly bear on the financial condition of the disclosing company. The rulemaking in the 1970s does not support the Commission's statutory authority to issue the Final Rules, which stray beyond those limits. It is precedent against that authority.

Finally, and for similar reasons, the major questions doctrine further demonstrates that the Commission lacked authority to promulgate the Final Rules. The Supreme Court has held that agencies must have clear authorization from Congress when embarking on a new and expansive regulation of a substantial policy area of “vast economic and political significance.” [141]

Political controversies are for Congress to resolve, not administrative agencies with limited delegated authority.[142]

In addition, when “agencies assert[ ] highly consequential power beyond what Congress could reasonably be understood to have granted,” or “claim[ ] to discover in a long-extant statute an unheralded power representing a transformative expansion [of] . . . regulatory authority,” “there is every reason to hesitate before concluding that Congress meant to confer” the power claimed.[143]

Moreover, “[w]hen an agency has no comparative expertise in making certain policy judgments, . . . Congress presumably would not task it with doing so.” [144]

Finally, an intrusion “into an area that is the particular domain of State law,” [145]

also provides a strong indicator that, “absent a clear statement” from Congress, a Federal agency has exceeded its statutory authority.[146]

These indicia that the Commission transgressed the limits of its statutory authority under the major questions doctrine are all present here. Whether and how public companies should respond to the perceived causes and effects of climate change is unquestionably of “vast economic and political significance”; [147]

answering those questions, even with respect to disclosure, requires “balancing the many vital considerations of national policy implicated in how Americans will get their energy.” [148]

And as explained above, while the Final Rules purport to require only disclosure, the effect of their requirements is to impermissibly regulate issuers' internal affairs. In this regard, the Final Rules stray into areas far beyond the Commission's comparative expertise. Moreover, by effectively mandating certain risk management practices, the Final Rules intrude on an area—corporate governance—traditionally governed by State law. Thus, the major questions doctrine applies to the Final Rules, but as explained in the preceding section, the Commission's authorizing statutes do not provide the needed clarity to justify such a dramatic expansion of regulatory authority.

The assertion of regulatory power under the Final Rules represents a “transformative expansion in [the Commission's] regulatory authority.” [149]

For example, the Final Rules require LAFs and AFs to disclose their Scope 1 emissions and/or Scope 2 emissions, if material, separately, each expressed in the aggregate, in terms of CO2

e.[150]

In addition, the Final Rules require registrants to provide disclosures regarding their use of transition plans,[151]

scenario analysis,[152]

and internal carbon prices, if material,[153]

as well as descriptions of their board of directors' oversight of climate-related risks, regardless of materiality.[154]

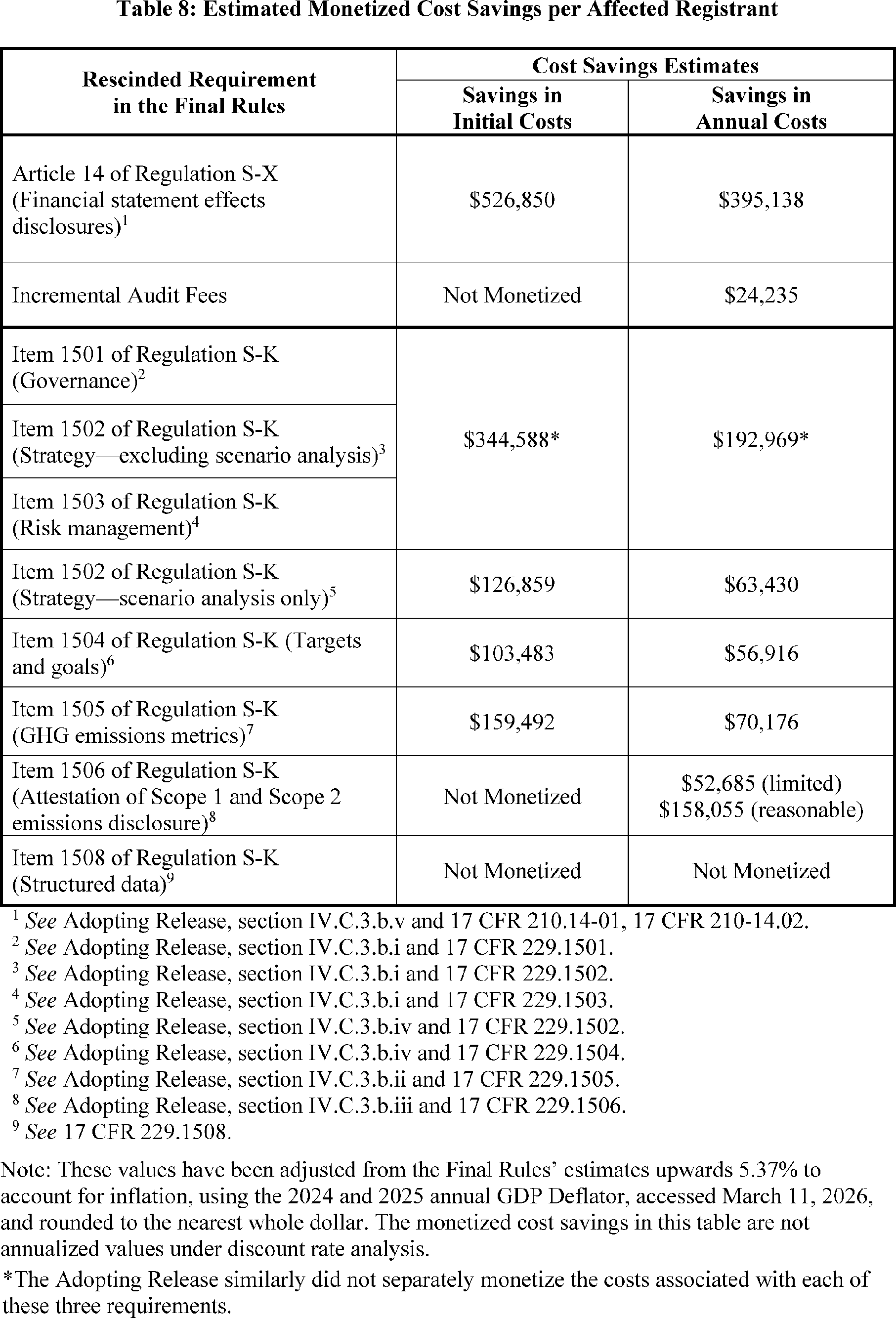

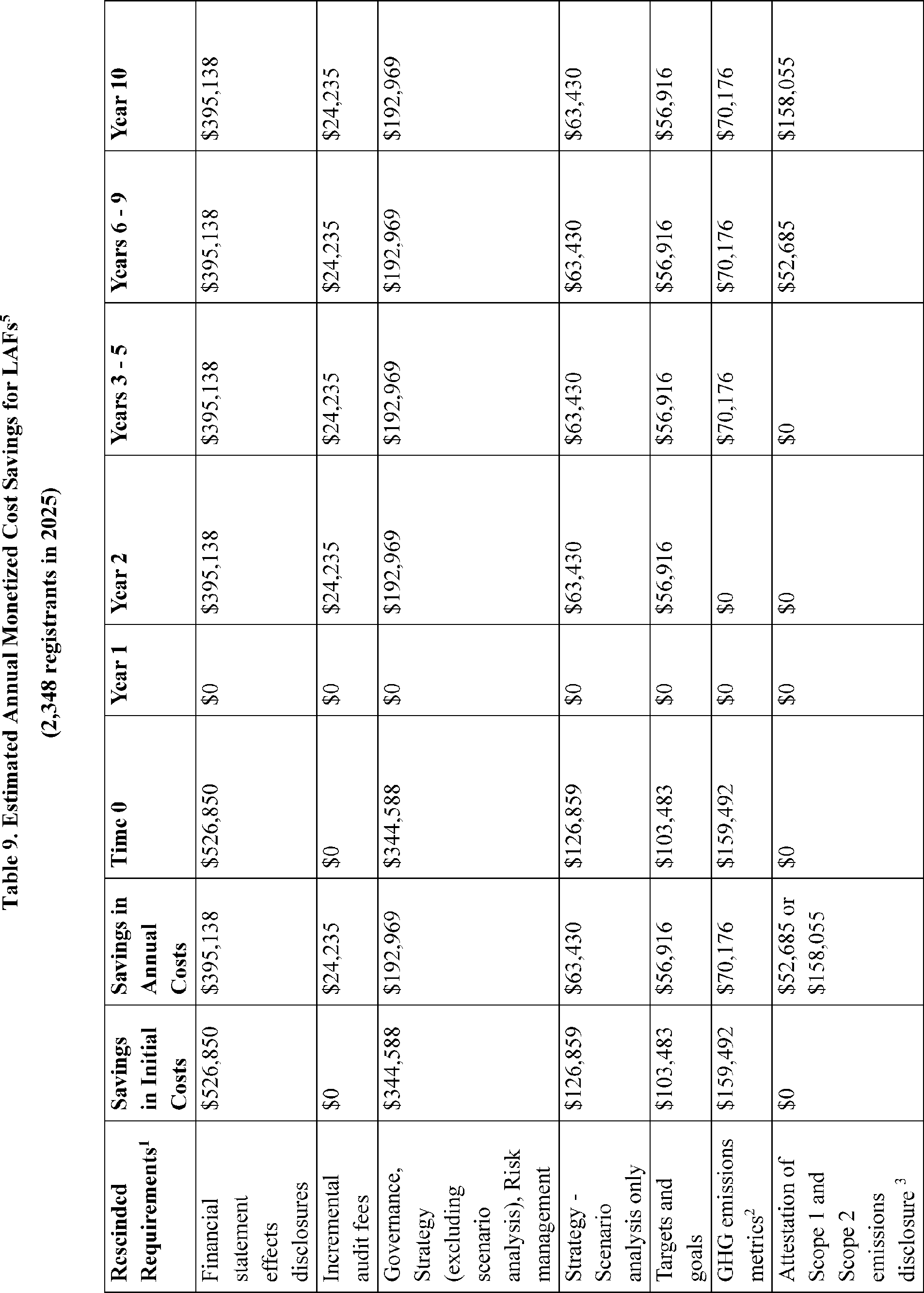

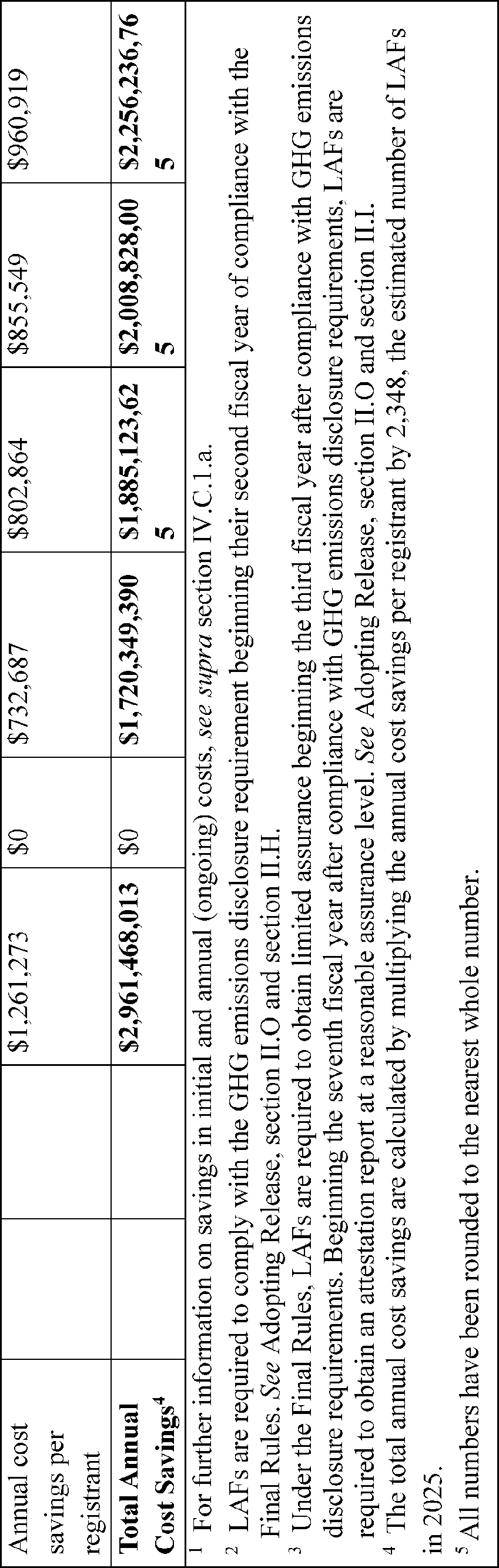

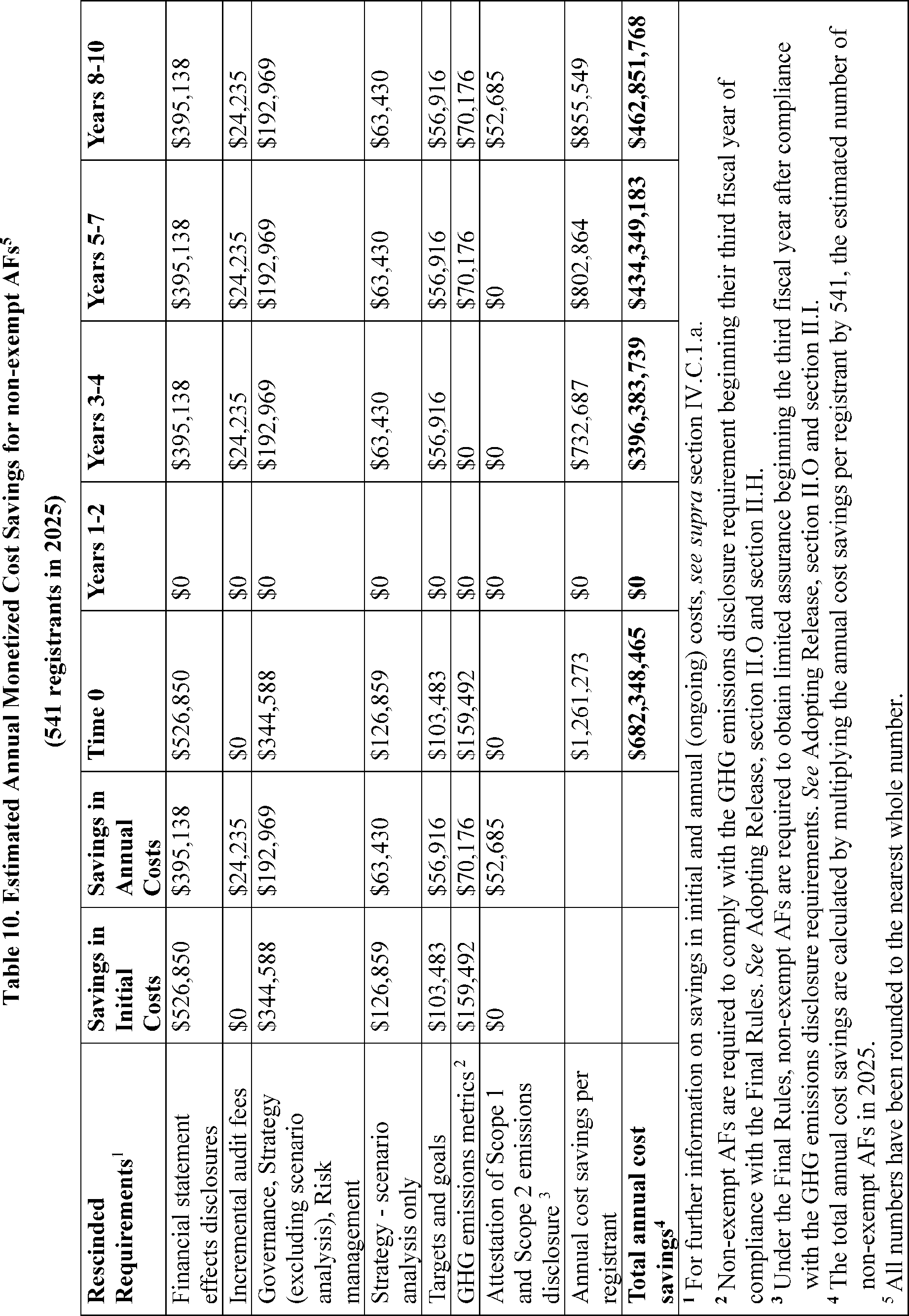

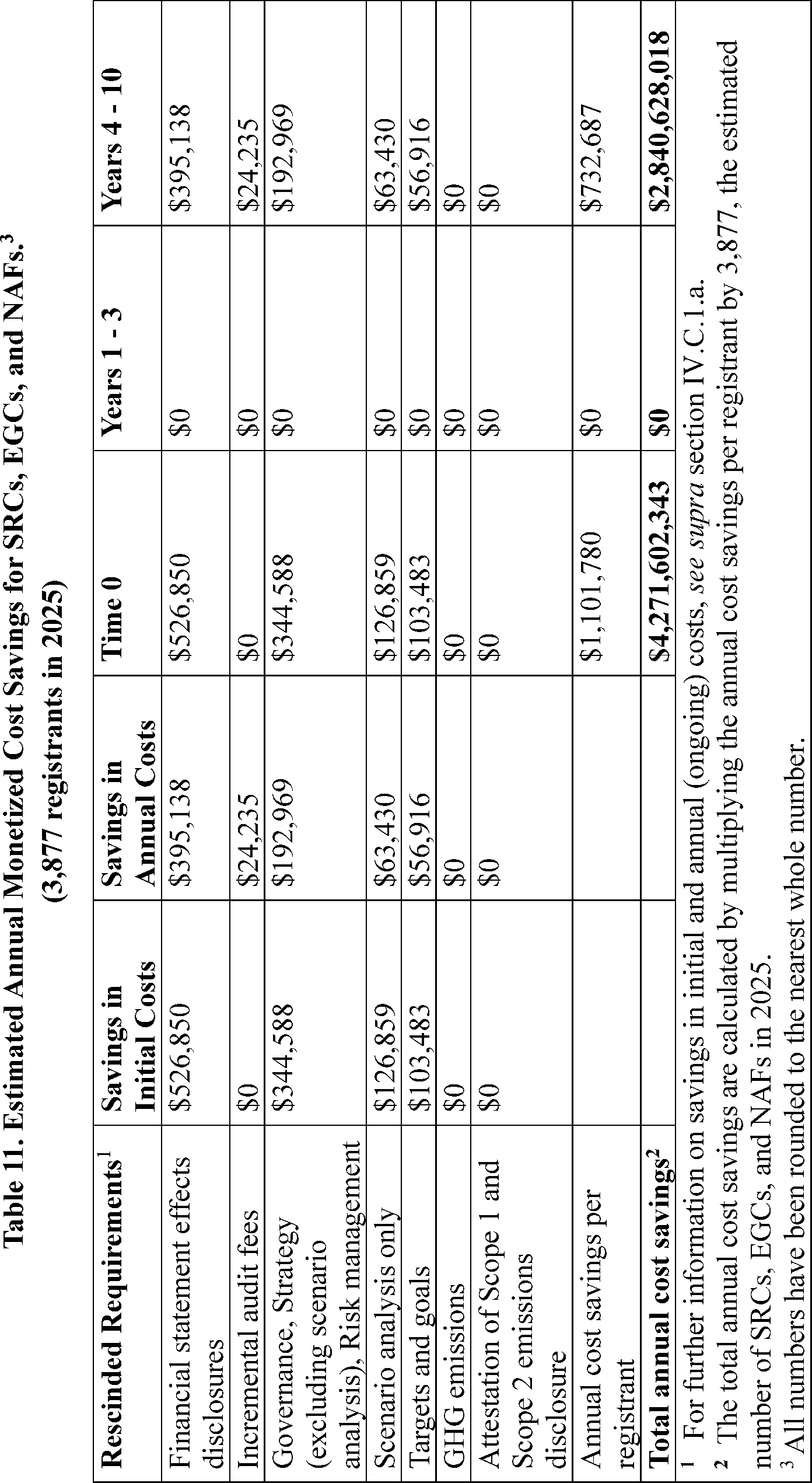

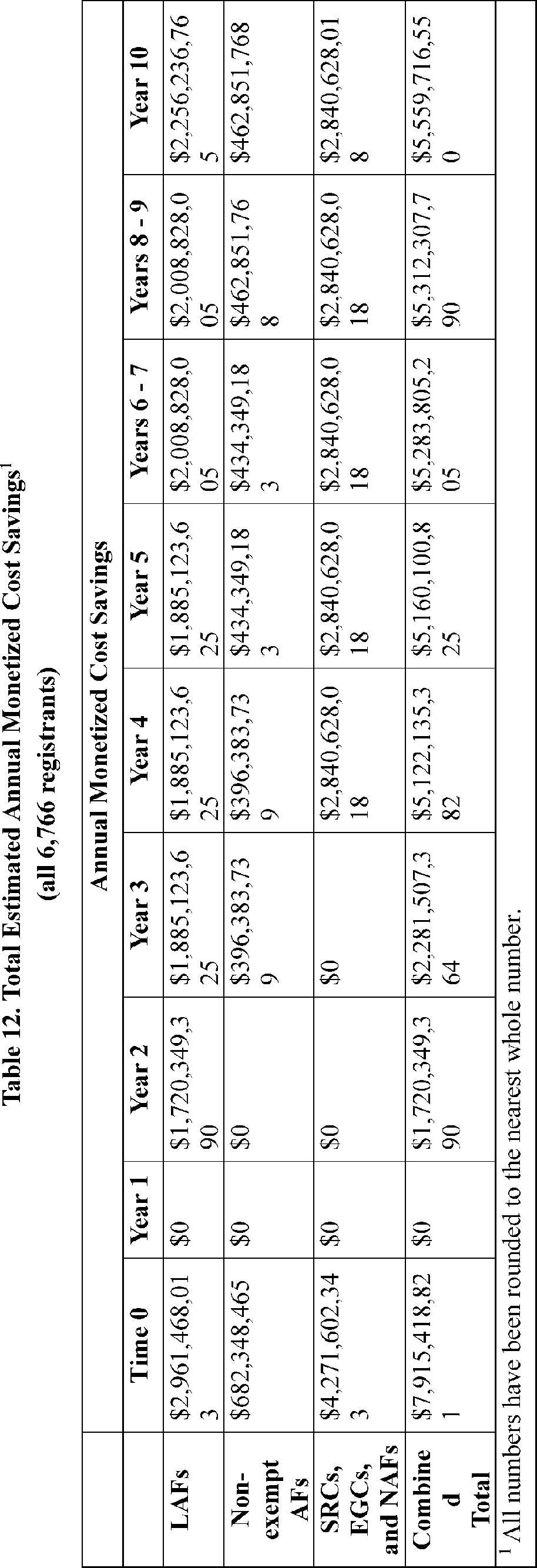

The scope of that expansion is reflected in the costs that the Commission estimated the Final Rules will impose on registrants. The Commission estimated that annual compliance costs per registrant averaged over the first ten years of compliance could range from less than $197,000 to over $739,000.[155]

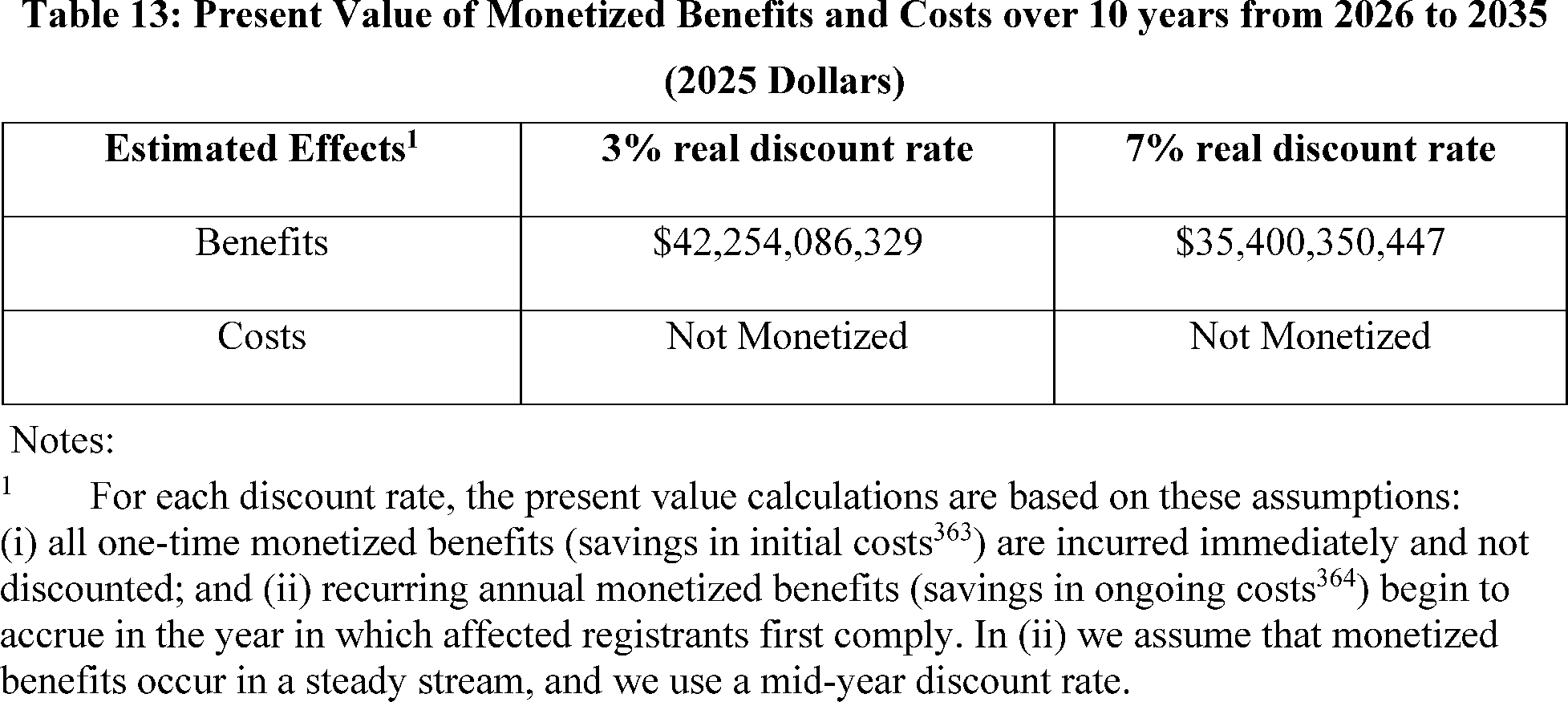

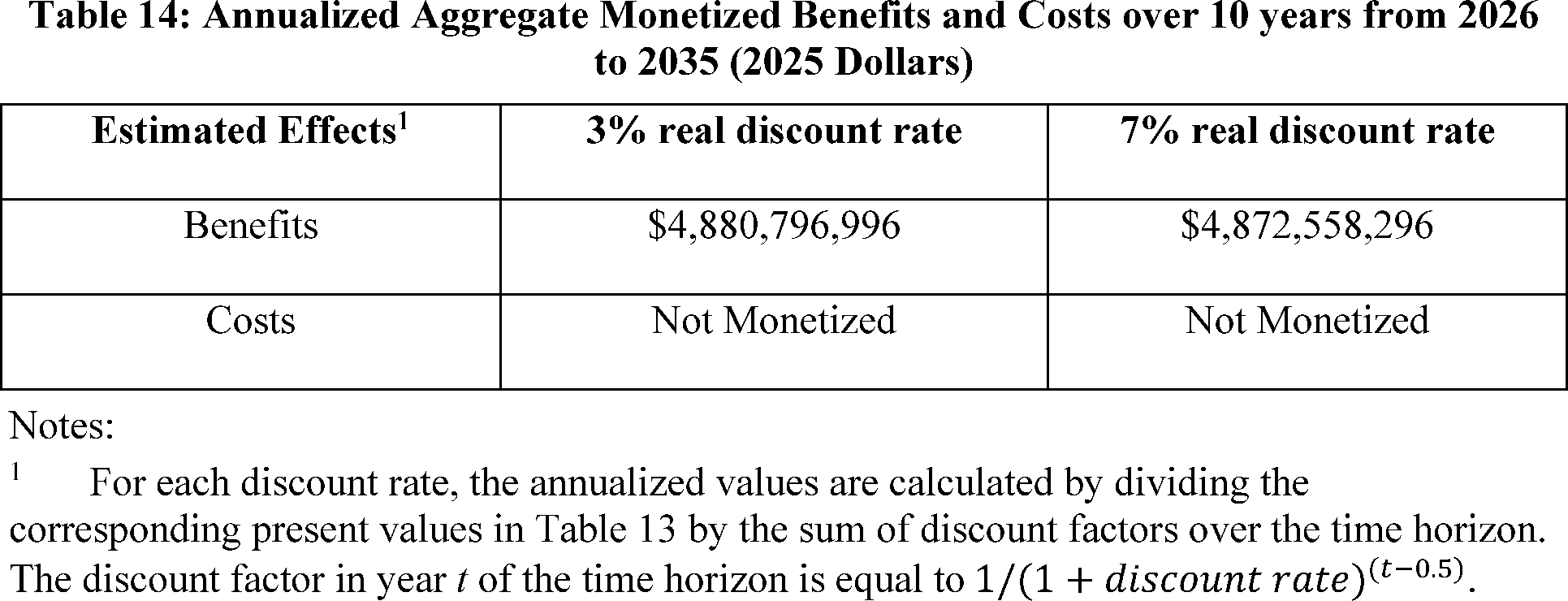

Updating these figures for inflation and aggregating them across all affected registrants, we estimate that rescinding the Final Rules could generate annualized savings of about $4.9 billion

( printed page 33308)

per year over the next 10 years for all affected registrants.[156]

As discussed in section III.B.1 and section III.B.2, Congress has not given the Commission power to write regulations requiring such detailed and extensive disclosure of climate-related information, let alone to essentially regulate issuers' internal affairs through onerous disclosure requirements. To the contrary, questions about the country's response to climate change generally and about climate-related disclosures by public companies specifically continue to be important and contentious. Congress is clearly aware of the potential and claimed risks posed by climate change, yet it has not legislated directly nor instructed the Commission to adopt regulations in response.[157]

Instead, Congress has declined to enact climate-related disclosure legislation.[158]

In evaluating an agency's assertion of statutory authority, the Supreme Court has instructed that courts “must be guided to a degree by common sense as to the manner in which Congress is likely to delegate a policy decision of such economic and political magnitude to an administrative agency.” [159]

Common sense would say that the Securities and Exchange Commission is not the right agency to deal with the question of how public companies can or should respond to climate change and related matters. The Commission clearly has no expertise, scientific or otherwise, related to climate-related risks or the criteria or analytical frameworks to be used in evaluating such risks.[160]

Congress has created an agency—the Environmental Protection Agency—and tasked that agency with collecting reports from major emissions sources and making them available to the public.[161]

In adopting the Final Rules, the Commission acted well “outside its wheelhouse.” [162]

Common sense suggests that Congress would not allocate authority over climate change and related matters to the Commission.

In light of the controversy, costs, and intrusions into the operations of public companies that would be generated by mandatory climate-related disclosure rules, this is a choice for Congress, not the Commission, to make. That conclusion is reinforced by the mismatch between the Commission's area of expertise and the subject matter of climate change. Further, Congress has not authorized the Commission to interfere in the corporate governance of registrants with respect to climate change. Congress has continued to leave such corporate governance matters to the States. The Commission's asserted basis for the Final Rules does not satisfy the clear evidence of congressional authorization required by the major questions doctrine. “Agencies have only those powers given to them by Congress, and `enabling legislation' is generally not an `open book to which the agency [may] add pages and change the plot line.' ” [163]

3. The Final Rules Should Be Rescinded in Their Entirety

Even if the Commission had authority to adopt some of the Final Rules, the Final Rules should nevertheless be rescinded in their entirety. Although the Commission stated in the Adopting Release that it intended for the Final Rules to operate independently,[164]

upon reconsideration, we now conclude that the individual items of disclosure in the Final Rules are pieces of a larger whole and cannot operate sensibly without the others. For example, the text of the Final Rules sometimes explicitly connects one part of the rules to others.[165]

In addition, parts of the Adopting Release demonstrate the functional inter-relationship between different disclosure requirements. For example, the Adopting Release states that the financial statement disclosures “facilitate investors' assessment of particular types of” climate-related risk and that there is “significant overlap” between the narrative and financial statement disclosures.[166]

As another example, Rule 14-02(e)(1) requires disclosure of costs, expenditures, and losses for carbon offsets and RECs.[167]

The Adopting Release states that these disclosures are directly connected to “a registrant's plans to achieve its disclosed climate-related targets or goals”[168]

and “will complement the disclosures required by the amendments to Regulation S-K and will anchor the disclosures required outside the financial statements to those required within the financial statements.” [169]

As a result, disclosure under these items is unlikely to be sensible to investors in the absence of the other disclosures mandated by the Final Rules.

C. Policy Reasons for Rescinding the Final Rules

In addition to (and independent of) the legal authority defects discussed above, there are strong policy arguments for rescinding the Final Rules in their entirety. As the Supreme Court has stated, “[a]gencies are free to change their existing policies as long as they provide a reasoned explanation for the change.” [170]

On reconsideration, we have determined that the Adopting Release gave inappropriate weight to several of the main justifications for adopting the Final Rules, and we now reach a different policy judgment regarding the need for, and appropriateness of, the Final Rules. Consequently, we propose to rescind the Final Rules in their entirety.

Several independent policy judgments support a rescission of the Final Rules. First, the Final Rules deviate from the Commission's “long-standing commitment to a principles-based, registrant-specific approach to disclosure” that is “rooted in materiality and facilitate[s] an understanding of a

( printed page 33309)

registrant's business, financial condition and prospects[.]” [171]

The Final Rules' sharp departure from these important tenets provides investors, at great cost, with an avalanche of information that is unlikely to be material to the decision-making of a reasonable investor. Second, the Final Rules require registrants to provide costly and lengthy disclosures about climate-related matters, a divisive social and political issue that is well outside the policy concerns of the Federal securities laws. In so doing, the Final Rules inappropriately intrude on corporate decision-making. Third, the Final Rules impose substantial costs on public companies and their shareholders that are not justified by the informational benefits they may provide to some investors. Finally, imposing those same high costs on registrants is at odds with the Commission's policy objectives of facilitating capital formation and promoting public company status.

As discussed more fully below, a responsible approach to public company disclosure demands that the Final Rules be rescinded in their entirety.[172]

1. The Final Rules Are Unnecessary and Inconsistent With a Registrant-Specific, Materiality-Based Approach To Disclosure That Best Serves the Interests of Registrants and Investors

The Final Rules are unnecessary because existing disclosure requirements already elicit information about the material effects of climate-related matters. Furthermore, the Final Rules prioritize one potential factor over others that may materially affect a registrant's operations and financial condition. Finally, recent events, such as the European Union's efforts to narrow the coverage and scope of recently adopted sustainability and due diligence directives and extend their implementation deadlines, have highlighted the flaws in mandating such highly prescriptive disclosure for an evolving area, such as climate-related matters, as in the Final Rules.

a. Existing Disclosure Obligations and Anti-Fraud Provisions Already Elicit Information About the Material Effects of Climate-Related Matters

The Final Rules should be rescinded because the Commission's existing disclosure requirements and anti-fraud provisions already elicit information about the effects of climate-related matters in a way that is tailored to reflect registrants' particular circumstances, is focused on material information for investors, and does not impose upon registrants the additional costs and burdens of the Final Rules.[173]

As the Commission highlighted in the 2010 Guidance, various disclosure requirements apply to climate-related matters when they are material to a particular company. In particular, the 2010 Guidance highlighted Regulation S-K items related to description of business, legal proceedings, risk factors, and management's discussion and analysis. The 2010 Guidance also noted that registrants must consider any financial statement implications in accordance with applicable accounting standards. As the Commission acknowledged in the Adopting Release, even prior to the adoption of the Final Rules, registrants had an obligation to consider material impacts on the financial statements regardless of whether a material impact was driven by climate-related matters.[174]

In addition to existing line item and financial statement disclosure requirements, the liability provisions of the Federal securities laws, including the anti-fraud provisions, serve to protect investors from materially misleading or incomplete disclosures about climate-related matters. For example, Sections 11 [175]

and 12 [176]

of the Securities Act impose liability for material misstatements or omissions made in connection with registered offerings conducted under the Securities Act,[177]

and Exchange Act Section 10(b) [178]

and Rule 10b-5 broadly prohibit fraudulent and deceptive practices and untrue statements or omissions of material facts in connection with the purchase or sale of any security.[179]

We recognize that the Commission previously stated that it adopted the Final Rules because of a “need to improve the consistency, comparability, and reliability of climate-related disclosures for investors.” [180]

We disagree, however, that these purported benefits justify adoption of the Final Rules. As an initial matter, any assertions about the benefits of the consistency and comparability of the disclosures elicited by the Final Rules should be discounted because those benefits are substantially compromised by the inconsistent, variable, and often speculative assumptions necessary to make many of those disclosures.[181]

As a result, the type of information elicited by the Final Rules would vary across even similarly-situated registrants, depending on, for instance, whether they engage in certain practices, how they choose to report certain information, how they determine which expenditures to include, what methodologies they use, and how they exercise judgment in assessing which financial disclosures to make.[182]

Moreover, as noted above, prior to adoption of the Final Rules, registrants were already required to disclose information about the material effects of climate-related matters in a manner better tailored to reflect registrants' particular circumstances. The benefits of more tailored and effective disclosure in this context justify any potential loss in comparability because they allow for more particularized insight into a

( printed page 33310)

registrant's management, operations and financial condition, which can contribute to better risk and return assessments by investors. By contrast, the Final Rules are more apt to create information overload for investors, including through disclosure of immaterial information, while imposing significant new costs for registrants.

In light of existing disclosure obligations, the Final Rules serve insufficient additional purpose in informing investors about the material effects of climate-related matters. Indeed, in our view, the Final Rules are likely to result in the disclosure of immaterial information, at great cost to investors.

b. The Final Rules Prioritize the Effects of Climate-Related Matters Over Other Factors That May Materially Affect a Registrant's Operations and Financial Condition

In adopting the Final Rules, the Commission departed from its existing, generally principles-based approach to disclosure that for decades has elicited information about matters, including climate-related matters, that materially affect a registrant's operations or financial condition. In our view, a disclosure regime that prioritizes a single potential factor above any other that may affect the registrant and requires disclosure at the level of granularity called for by the Final Rules is inferior to the Commission's existing approach to disclosure that already applies with equal force to climate-related matters.

The Final Rules impose a myriad of highly prescriptive regulations that mandate granular disclosures focused exclusively on climate-related matters. For example, with respect to climate-related risks only, registrants under the Final Rules would need to consider and possibly disclose: (i) how a registrant's board oversees and is informed of climate risk, regardless of materiality; [183]

(ii) how a registrant's management assesses and manages material climate risk; [184]

(iii) which management positions manage climate risk and the associated expertise of the individuals serving in those roles; [185]

(iv) the geographic location of physical climate risk; [186]

and (v) how climate risks affect items like a registrant's products or services, suppliers, climate mitigation activities, and expenditures for research and development.[187]

Similarly, the financial statement requirements prioritize the effects of severe weather events and other natural conditions by imposing relatively low percentage thresholds for when such effects must be separately reported in the notes to the financial statements. Specifically, the Final Rules require disclosure in the income statement of expenditures expensed as incurred and losses if such amounts (in the aggregate) equal or exceed one percent of the absolute value of income or loss before income tax expense or benefit (subject to a $100,000 de minimis threshold) [188]

and require disclosure of capitalized costs and charges recognized on the balance sheet if the absolute value of such amounts (in the aggregate) equals or exceeds one percent of the absolute value of stockholders' equity or deficit (subject to a $500,000 de minimis threshold).[189]

These examples, including the specified thresholds, make clear that the Final Rules cannot be justified as eliciting disclosure of

material

information. Given their exceedingly granular requirements, the Final Rules would inevitably result in the disclosure of

immaterial

information about climate-related matters.[190]

Requiring such granular disclosures about a single type of risk, trend or event is at odds with a disclosure system that is intended to elicit information about the most significant factors affecting a registrant's operations and financial condition.[191]

The Commission's disclosure regime generally does not require this level of detailed disclosure for other factors affecting a registrant's business.[192]

Requiring such attention by registrants on climate-related matters, specifically, may lead to registrants devoting an inappropriate amount of attention to managing and reporting on such matters, which may not be among the most significant factors affecting the registrant's business. The Final Rules' misplaced focus, however, is not limited to impacts on a registrant's allocation of resources. The sheer volume of disclosures responsive to the Final Rules may hurt investors' abilities to ascertain relevant information about the other factors affecting a registrant because the climate-related disclosures could overshadow material disclosures about those other factors.

Moreover, as discussed in section III.C.3, the Commission's attempt to mitigate the burdensome granularity of the adopted requirements by adding materiality qualifiers throughout the Final Rules fails to adequately mitigate their distorting effects on registrant disclosures. Given the complexity of making the materiality determinations required by the Final Rules, many registrants may err on the side of over-disclosure, burdening both investors and registrants with an avalanche of climate-related information.

Thus, in our view, the Final Rules are inconsistent with and inferior to the Commission's long-standing, registrant-specific approach to disclosure of factors materially affecting a registrant's operations and financial condition and therefore should be rescinded.

c. Recent Developments Underscore Why a Flexible, Materiality-Based Approach Is Preferable

Recent efforts to scale back, set aside, or otherwise revise various climate reporting regimes at the international level further underscore why the Commission was misguided in adopting costly and prescriptive requirements built around shifting investor preferences and reporting trends. Investors are not monolithic and have differing risk appetites, investment strategies, and analytical methods—and in some cases non-financial interests—that affect their particular investment decisions. In designing a disclosure regime, the Commission should not seek to cater to the specific informational needs of every subset of investors about each emergent topic. Rather, as the

( printed page 33311)

Supreme Court directed when delineating a materiality standard for the Federal securities laws,[193]

the Commission should look to whether the

reasonable

investor would consider the information important in buying or selling securities—and as discussed above, the common interests of reasonable investors is in information regarding the financial performance of a company, the pricing of securities, and the prospect for economic and financial return from the disclosing company.[194]

Moreover, investors generally are better served by regulatory requirements that can be adapted to registrants' specific circumstances. Such bespoke disclosures are more likely to provide material information than the one-size-fits-all disclosure approach of the Final Rules. If, over time, market forces lead to coalescence around certain disclosure practices, such practices are likely to be more responsive to the changing needs of investors than the top-down prescriptive approach of the Final Rules.

The soundness of these basic principles is well illustrated by the challenges faced by other climate-risk reporting regimes since the Final Rules were adopted. In adopting the Final Rules, the Commission observed several ongoing developments related to climate-risk reporting, which included, at the time, announcements by several jurisdictions to adopt, apply, or otherwise be informed by the International Sustainability Standards Board (“ISSB”) standards.[195]

The Adopting Release also highlighted the European Union's (“EU”) adoption of the Corporate Sustainability Reporting Directive (“CSRD”), which requires certain large and listed companies and other entities, including non-EU entities, to report on sustainability-related issues in line with the European Sustainability Reporting Standards.[196]

In taking note of such developments, the Commission acknowledged that these laws could reduce the compliance burden of the Final Rules to the extent they impose similar requirements on registrants subject to them.[197]

Since the adoption of the Final Rules only two years ago, there has been a noticeable effort to step back from these initiatives, calling into question the Commission's decision to follow them with its own highly prescriptive approach. These developments also undermine the assumption that the emergence of other reporting regimes would help to mitigate the significant costs of the Final Rules. For example, entities that set international standards for climate-risk reporting regimes, such as the ISSB and the EU, have revised their climate-related disclosure standards, having found them to be burdensome, overly complex, and/or duplicative. The ISSB has recently amended IFRS to “reduce complexity, the risk of duplicative reporting and the cost of applying specific greenhouse gas emissions disclosure requirements.” [198]

In February 2026, the EU adopted legislation revising the CSRD and the Corporate Sustainability Due Diligence Directive (“CSDDD”) to simplify rules on sustainable finance reporting and decrease compliance burdens.[199]

Specifically, the EU removed around 80% of previously covered companies from the scope of the CSRD, narrowed the scope of the CSDDD, and postponed the implementation timelines of both Directives, among other changes.[200]

These developments reinforce our determination that highly prescriptive disclosure requirements based on shifting investor preferences and reporting trends are inferior to a registrant-specific, materiality-based reporting regime focused on the information a reasonable investor would consider important in making an investment decision.

2. The Final Rules Stray Well Beyond the Policy Concerns of the Federal Securities Laws

An additional policy reason for rescinding the Final Rules is that they do not respond to a gap in investor protection in the securities disclosure regime; rather, they concern the divisive and unsettled political and social issue of climate regulation. The Commission's role is to protect investors; maintain fair, orderly, and efficient markets; and facilitate capital formation. It is not to regulate how public companies manage the effects of climate-related matters or to hijack the public company reporting regime to further social policies unrelated to the aims of the Federal securities laws. The Commission's disclosure requirements should inform investors about a registrant's operations and finances; it is not the province of the Commission to drive changes in those operations absent specific direction from Congress.[201]