Distribution of Continued Dumping and Subsidy Offset to Affected Domestic Producers

Pursuant to the Continued Dumping and Subsidy Offset Act of 2000, this document is U.S. Customs and Border Protection's (CBP) notice of intent to distribute assessed antidumping...

U.S. Customs and Border Protection, Department of Homeland Security.

ACTION:

Notice of intent to distribute offset for Fiscal Year 2026.

SUMMARY:

Pursuant to the Continued Dumping and Subsidy Offset Act of 2000, this document is U.S. Customs and Border Protection's (CBP) notice of intent to distribute assessed antidumping and countervailing duties (known as the continued dumping and subsidy offset) for Fiscal Year 2026 in connection with countervailing duty orders, antidumping duty orders, and findings under the Antidumping Act of 1921. This document provides instructions for affected domestic producers, or anyone alleging eligibility to receive a distribution, to file certifications to claim a distribution in relation to the listed orders and findings, and to provide CBP with the necessary information to effect payment of a distribution by electronic funds transfer.

DATES:

Certifications to obtain a continued dumping and subsidy offset under a particular order or finding must be submitted electronically at

https://www.pay.gov

or received at the address identified below by July 27, 2026. Any certification submitted electronically at

https://www.pay.gov

or received at the address identified below after July 27, 2026 will be summarily denied, making claimants ineligible for the distribution.

ADDRESSES:

Certifications must be submitted electronically athttps://www.pay.gov

or sent by mail, or an express or courier service, addressed to U.S. Customs and Border Protection, Revenue Modernization Division, Attention: CDSOA Team, 8899 E 56th Street, Indianapolis, IN 46249.

Any new or updated ACH Refund Enrollment Form must be submitted to CBP electronically athttps://www.pay.gov

under the Public Form Name, “CBP ACH Refund Enrollment Form.”

All other correspondence may be sent by mail, or an express or courier service, addressed to U.S. Customs and Border Protection, Revenue Modernization Division, Attention: CDSOA Team, 8899 E 56th Street, Indianapolis, IN 46249.

FOR FURTHER INFORMATION CONTACT:

Robin Batt, CDSOA Team, Revenue Modernization Division, 8899 E 56th Street, Indianapolis, IN 46249; telephone (317) 614-4462.

SUPPLEMENTARY INFORMATION:

Background

The Continued Dumping and Subsidy Offset Act of 2000 (CDSOA) was enacted on October 28, 2000, as part of the Agriculture, Rural Development, Food and Drug Administration, and Related Agencies Appropriations Act, 2001 (the “Act”). The provisions of the CDSOA are contained in title X (sections 1001-1003) of the Appendix of the Act (H.R. 5426).

The CDSOA amended title VII of the Tariff Act of 1930 by adding section 754 (codified at 19 U.S.C. 1675c) to provide that assessed duties received pursuant to a countervailing duty order, an antidumping duty order, or a finding under the Antidumping Act of 1921 will be distributed to affected domestic producers for certain qualifying expenditures that these producers incur after the issuance of such an order or finding. The term “affected domestic producer” means any manufacturer, producer, farmer, rancher, or worker representative (including associations of such persons) who:

(A) Was a petitioner or interested party in support of a petition with respect to which an antidumping duty order, a finding under the Antidumping Act of 1921, or a countervailing duty order has been entered;

(B) Remains in operation continuing to produce the product covered by the countervailing duty order, the antidumping duty order, or the finding under the Antidumping Act of 1921; and

(C) Has not been acquired by another company or business that is related to a company that opposed the antidumping or countervailing duty investigation that led to the order or finding (

e.g.,

opposed the petition or otherwise presented evidence in opposition to the petition). The distribution that these parties may receive is known as the continued dumping and subsidy offset.

Section 7601(a) of the Deficit Reduction Act of 2005 repealed 19 U.S.C. 1675c. According to section 7701 of the Deficit Reduction Act, the repeal takes effect as if enacted on October 1, 2005. However, section 7601(b) provides that all duties collected on an entry filed before October 1, 2007, must be distributed as if 19 U.S.C. 1675c had not been repealed by section 7601(a). The funds available for distribution were also affected by section 822 of the Claims Resolution Act of 2010 and section 504 of the Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act of 2010.

Historically, the antidumping and countervailing duties assessed and received by U.S. Customs and Border Protection (CBP) on CDSOA-subject entries, along with the interest assessed and received on those duties pursuant to 19 U.S.C. 1677g, were transferred to the CDSOA Special Account for distribution. 66 FR 48546, Sept. 21, 2001; see also 19 CFR 159.64(e). Other types of interest, including delinquency interest that accrued pursuant to 19 U.S.C. 1505(d), equitable interest under common law, and interest under 19 U.S.C. 580, were not subject to distribution. Id.

Section 605 of the

Trade Facilitation and Trade Enforcement Act of 2015

(TFTEA) (Pub. L. No. 114-125, February 24, 2016; codified as 19 U.S.C. 4401), provided new authority for CBP to deposit into the CDSOA Special Account for distribution, delinquency interest that accrued pursuant to 19 U.S.C. 1505(d), equitable interest under common law, and interest under 19 U.S.C. 580 for all surety payments received by CBP on or after October 1, 2014, on CDSOA-subject entries, as well as post-judgment interest received by CBP on those surety payments (

see28 U.S.C. 1961).

On May 30, 2025, President Trump ordered the sequester of non-exempt budgetary resources for Fiscal Year 2026 pursuant to section 251A of the

Balanced Budget and Emergency Deficit Control Act of 1985,

as amended (90 FR 24045, June 5, 2025). To implement this sequester during Fiscal Year 2026, the calculation of the Office of Management and Budget (OMB) requires a reduction of 5.7 percent of the assessed duties and interest received in the CDSOA Special Account (account number 015-12-5688). OMB has concluded that any amounts sequestered in the CDSOA Special Account during Fiscal Year 2026 will become available in the subsequent fiscal year (

see2 U.S.C. 906(k)(6)). As a result, CBP intends to include the funds that are temporarily reduced via sequester during Fiscal Year 2026 in the continued dumping and subsidy offset for Fiscal Year 2026, which will be distributed not later than 60 days after the first day of Fiscal Year 2027 in accordance with 19 U.S.C. 1675c(c). In other words, the continued dumping and subsidy offset that affected domestic producers receive for Fiscal Year 2026 will include the funds that were temporarily sequestered during Fiscal Year 2026.

( printed page 30805)

CBP has liquidated all CDSOA-subject entries. Accordingly, CBP has begun the process of reviewing the termination of special account criteria in 19 U.S.C. 1675c(e)(4) and 19 CFR 159.64(d) to identify any countervailing duty or antidumping duty orders or findings for which those termination criteria are met. Going forward, when CBP identifies such a countervailing duty or antidumping duty order or finding, CBP will publish notice of a final distribution in the

Federal Register

in accordance with 19 U.S.C. 1675c(e)(4) and 19 CFR 159.64(d). Until then, the CDSOA distribution process will be continued for an undetermined period. Consequently, the full impact of the CDSOA repeal on amounts available for distribution has been delayed for several years. It should also be noted that amounts distributed may be subject to recovery as a result of reliquidations, court actions, administrative errors, and other reasons.

List of Orders and Findings and Affected Domestic Producers

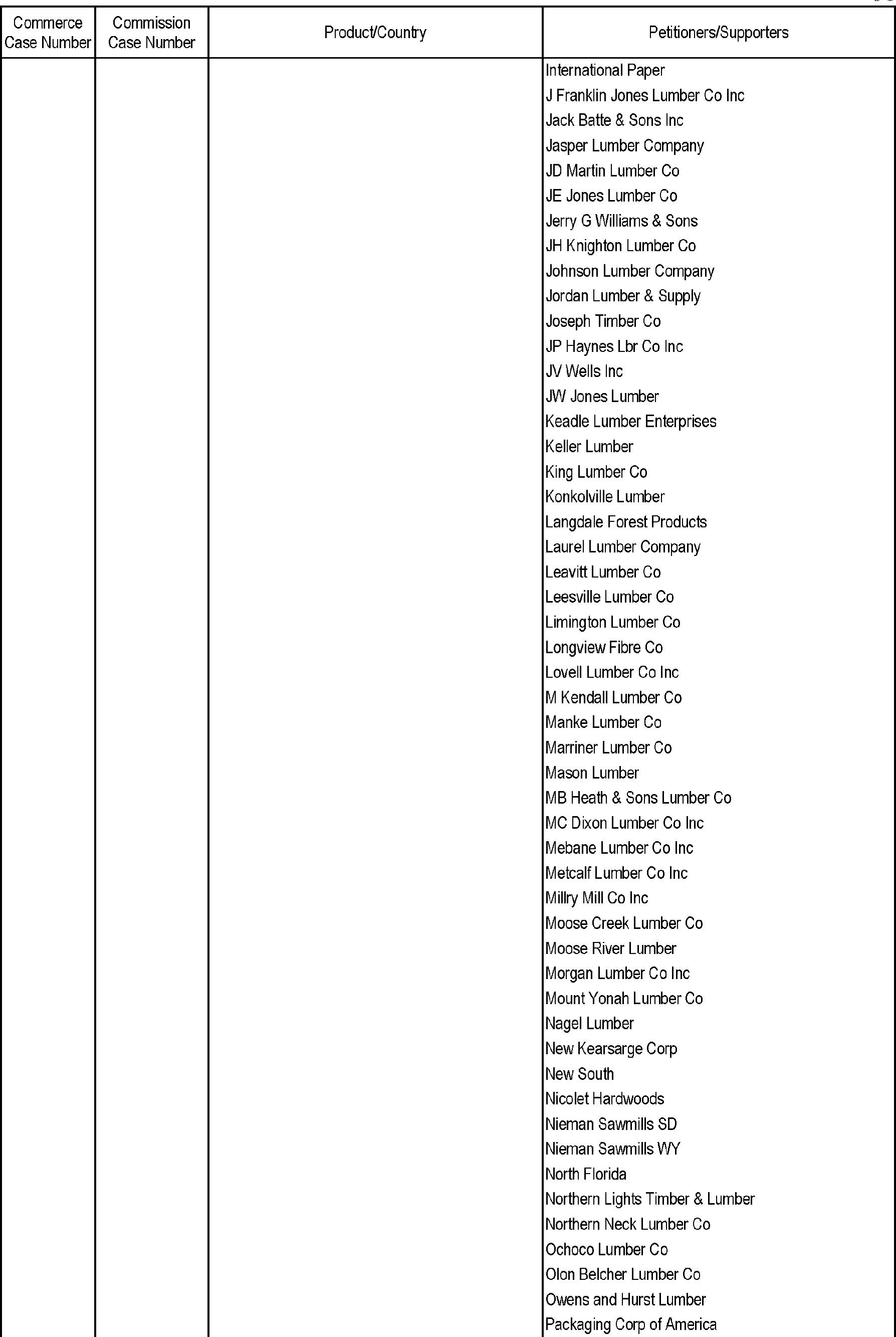

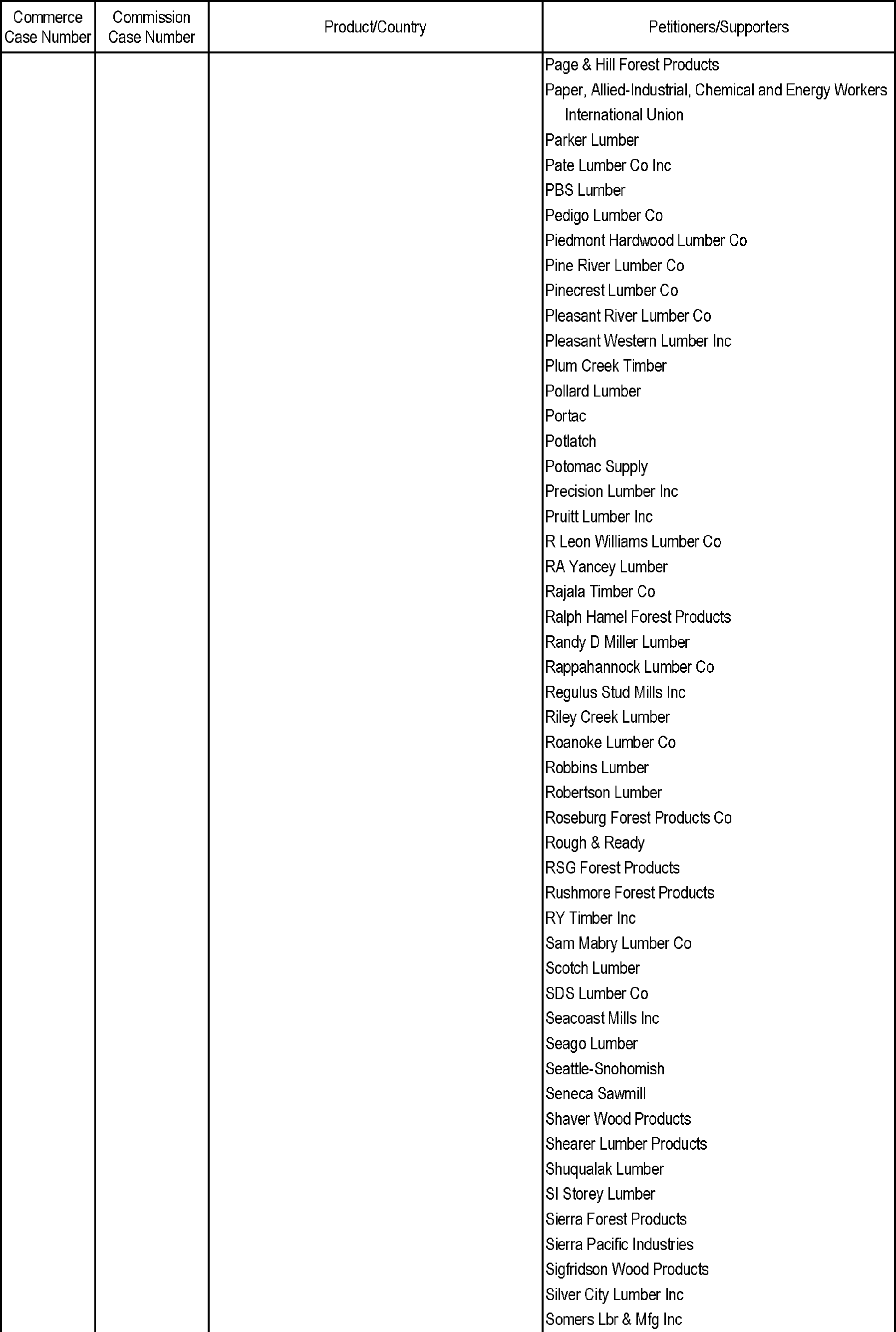

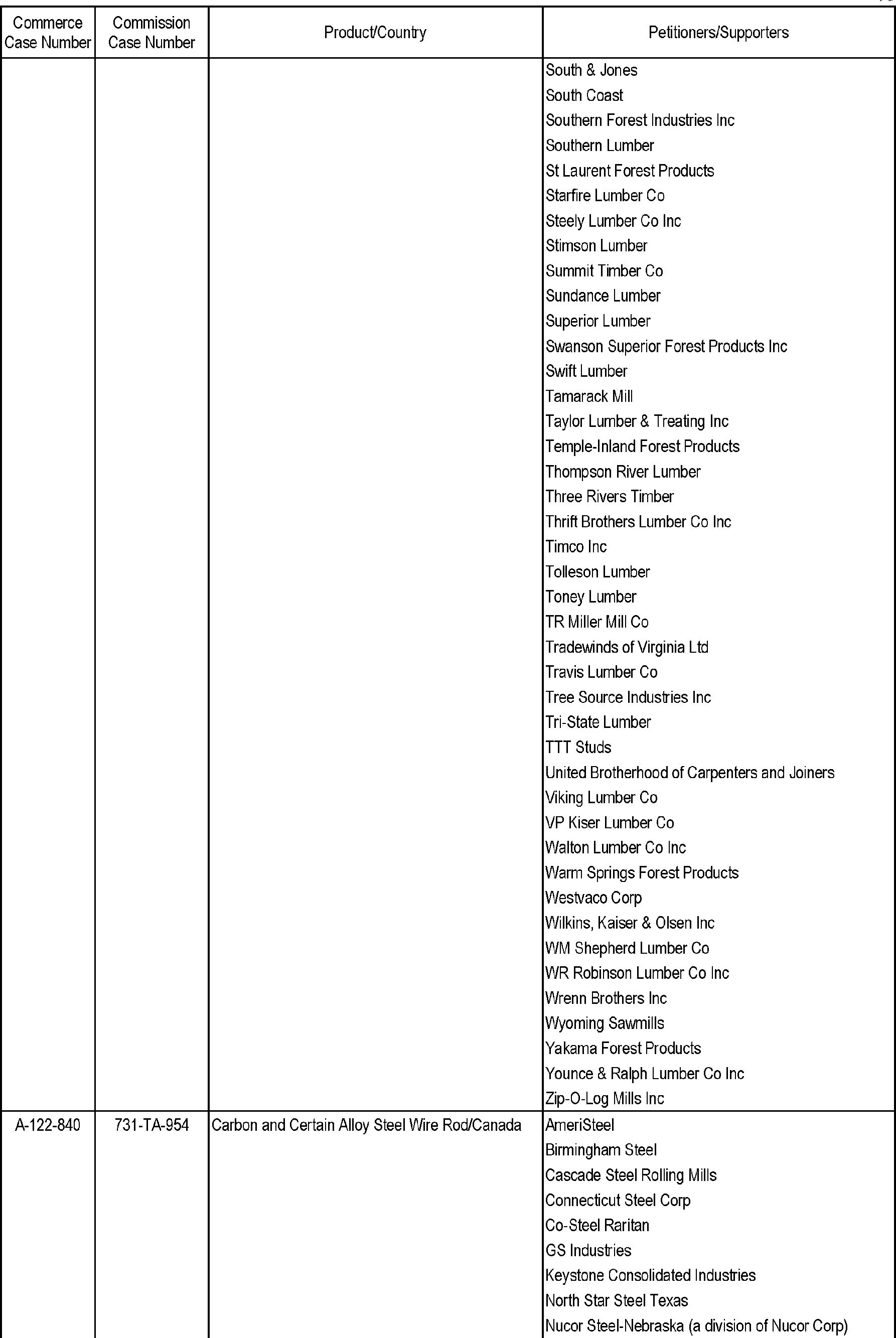

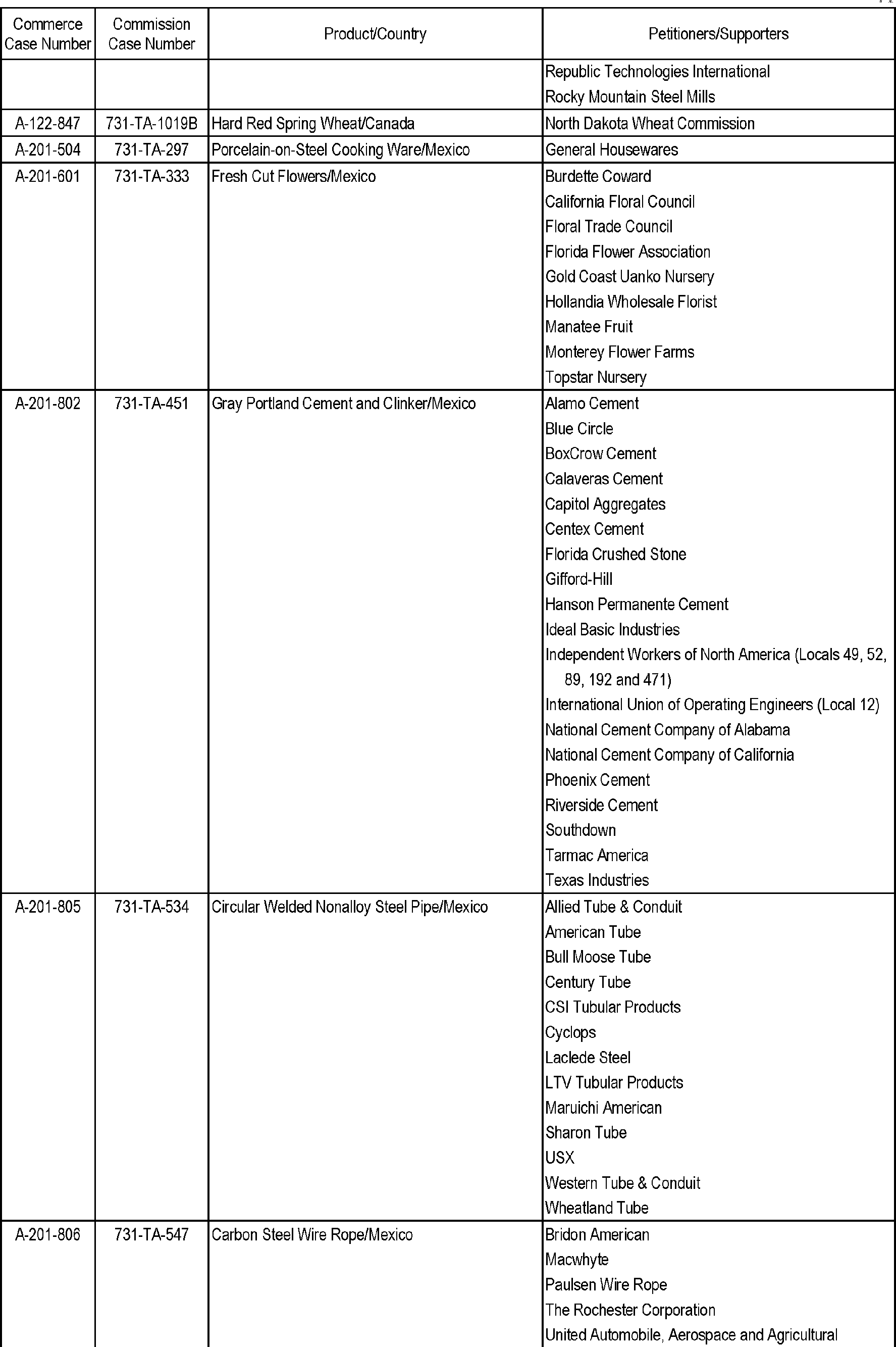

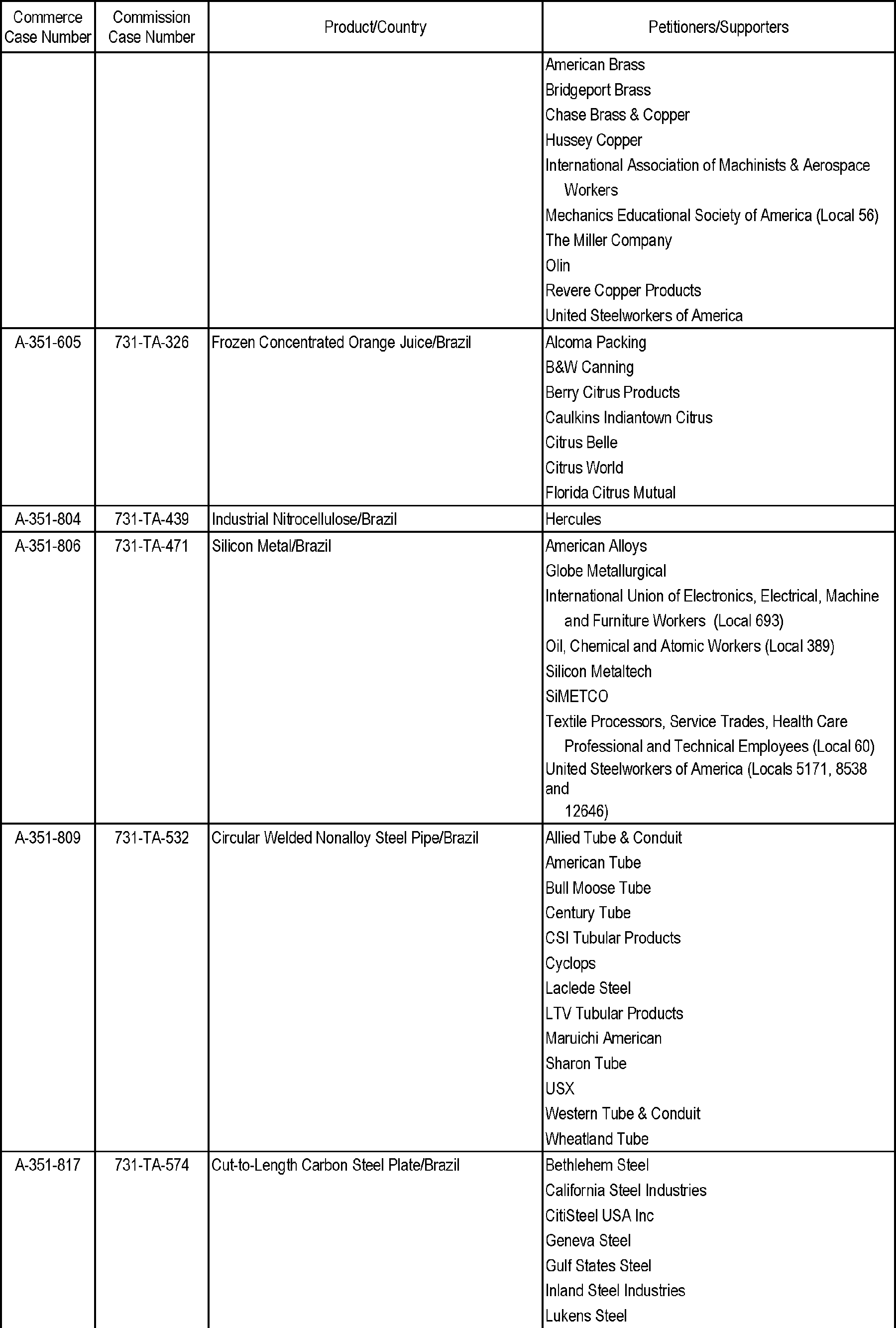

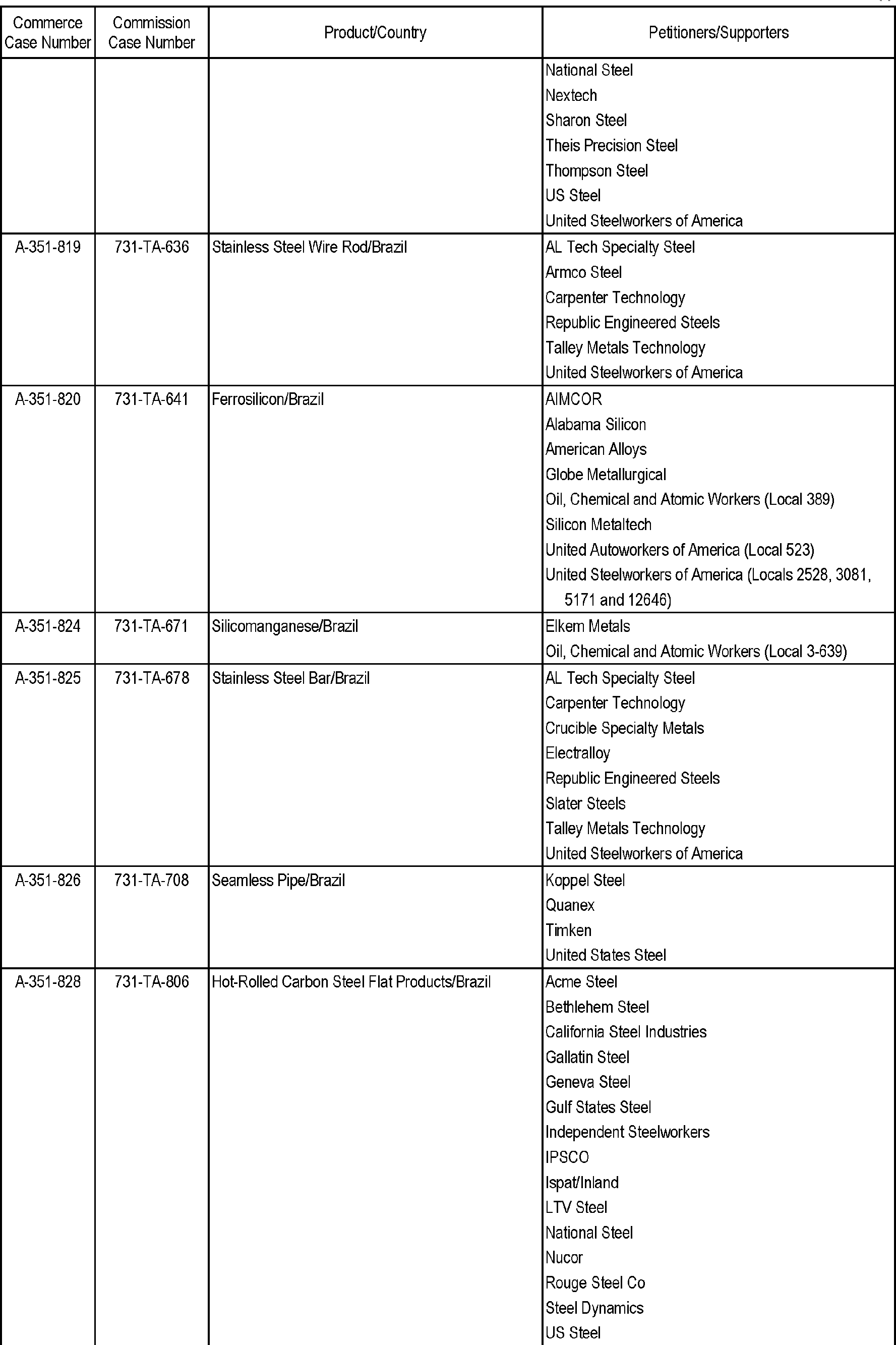

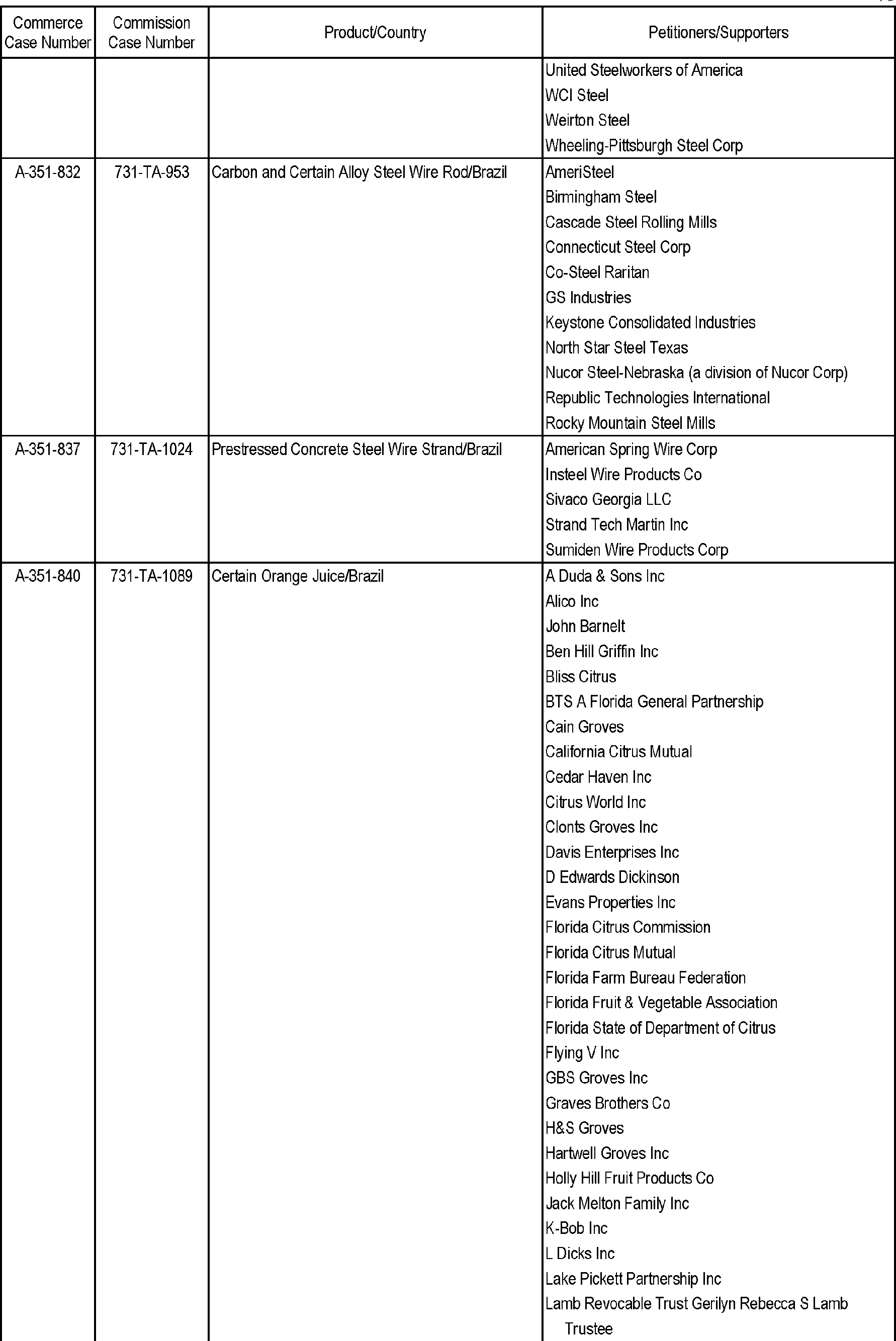

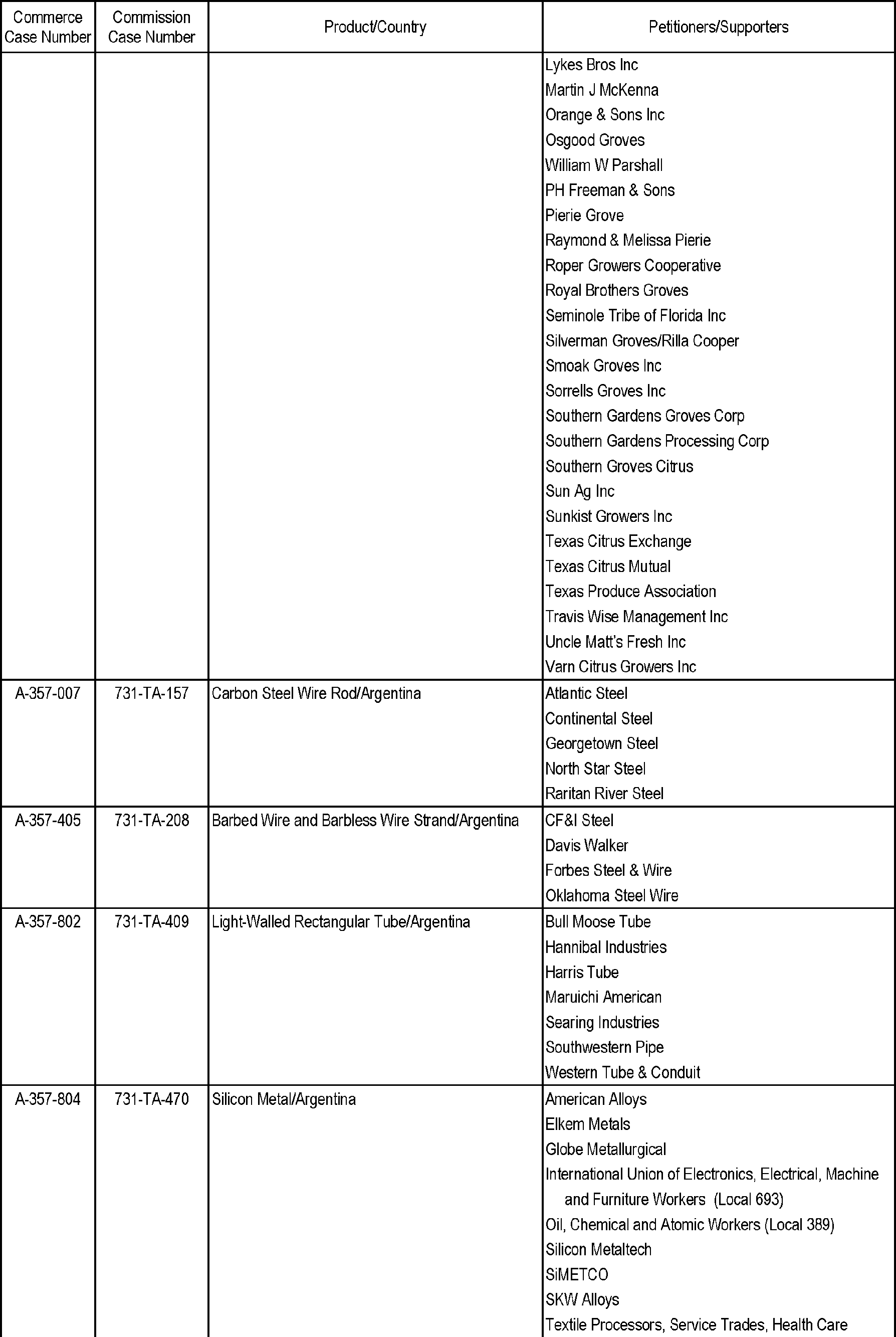

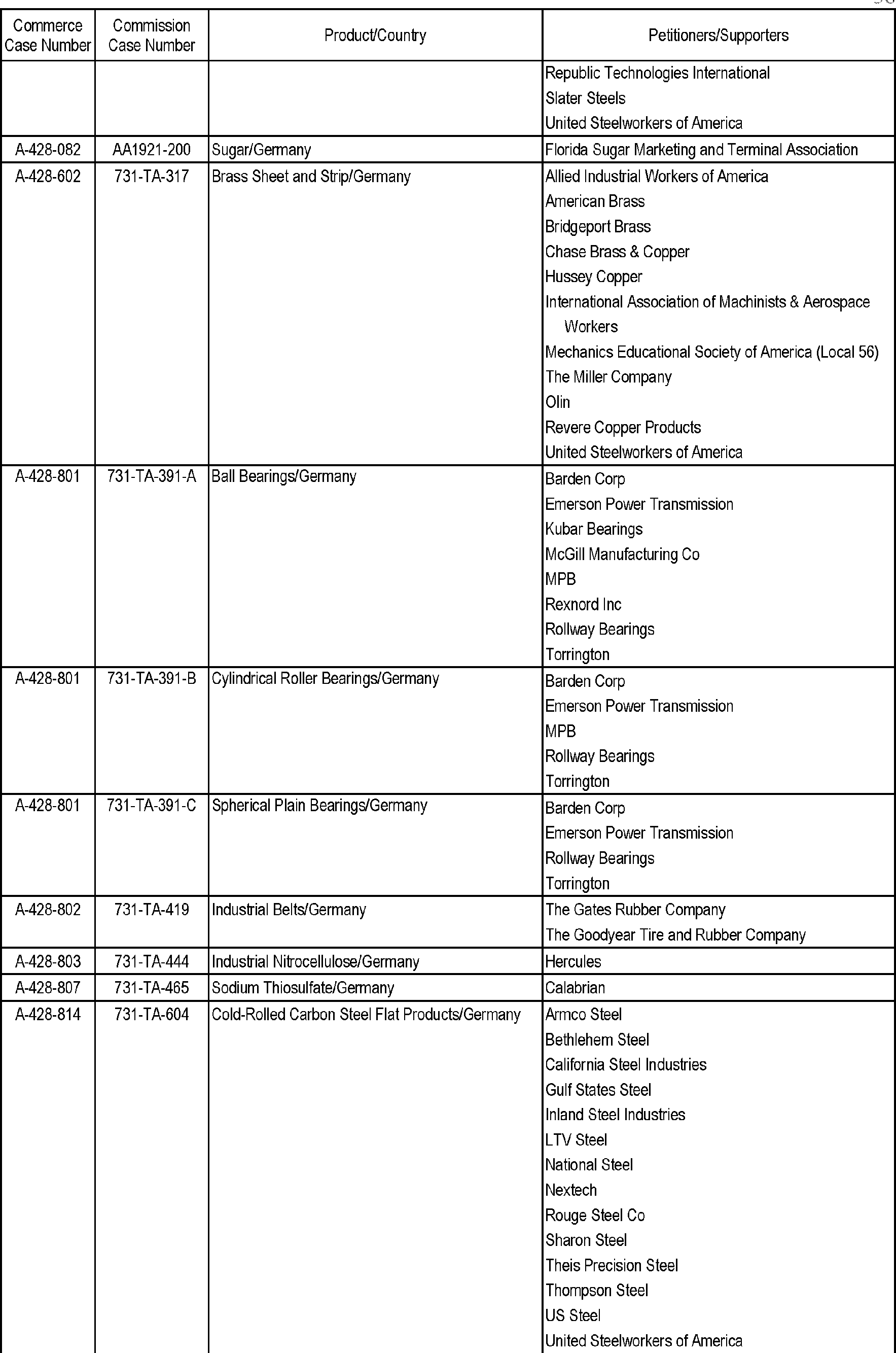

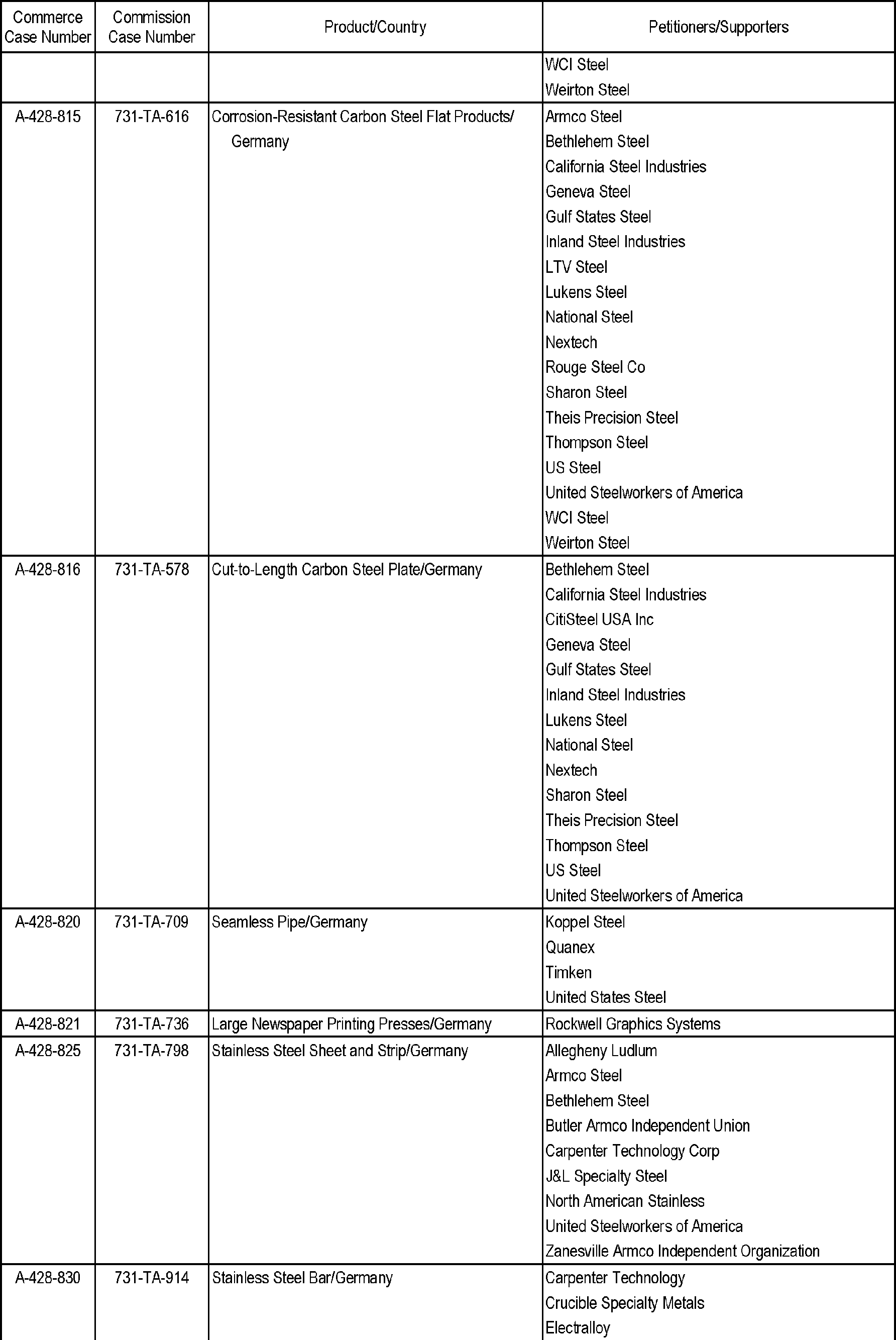

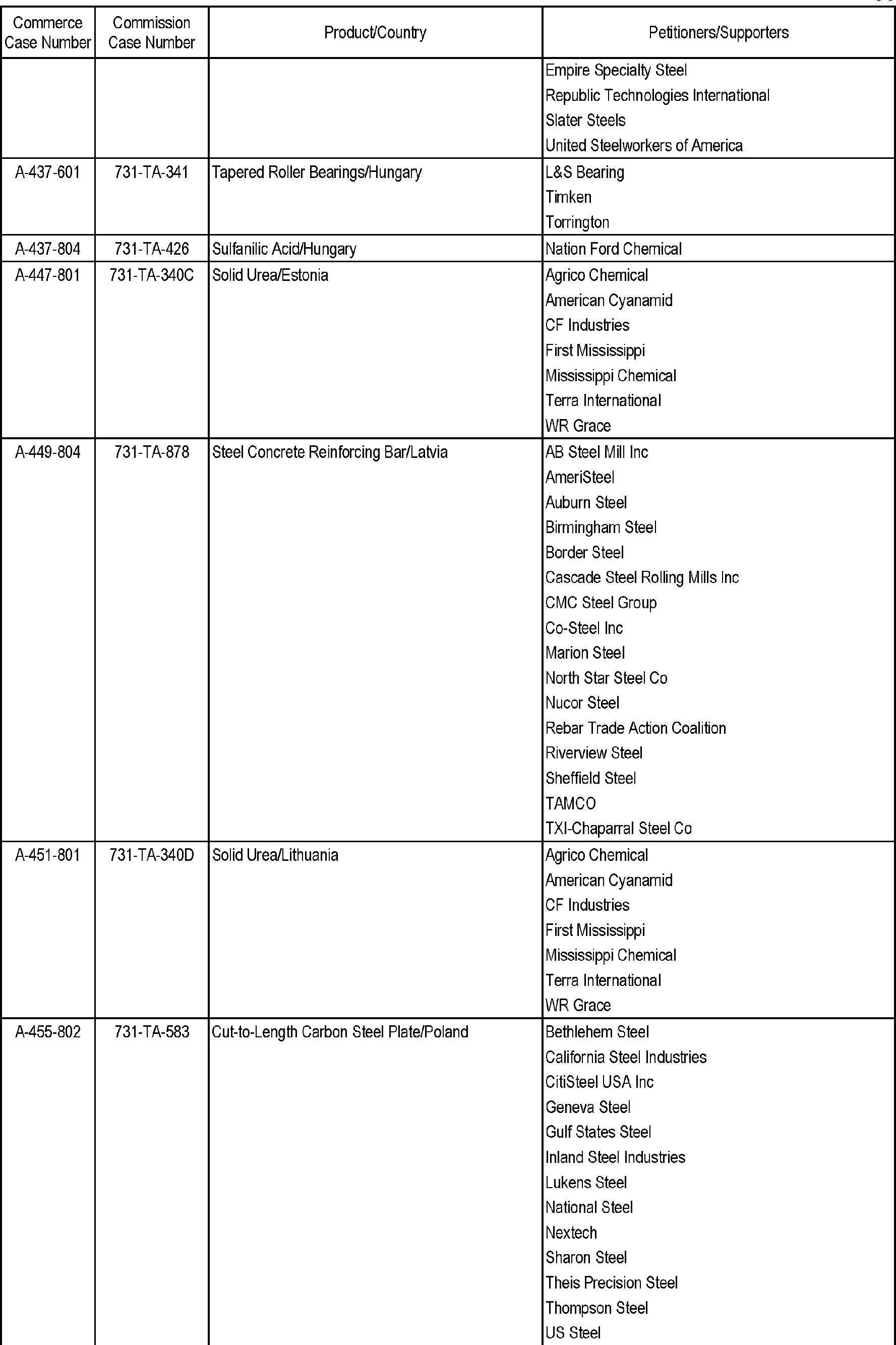

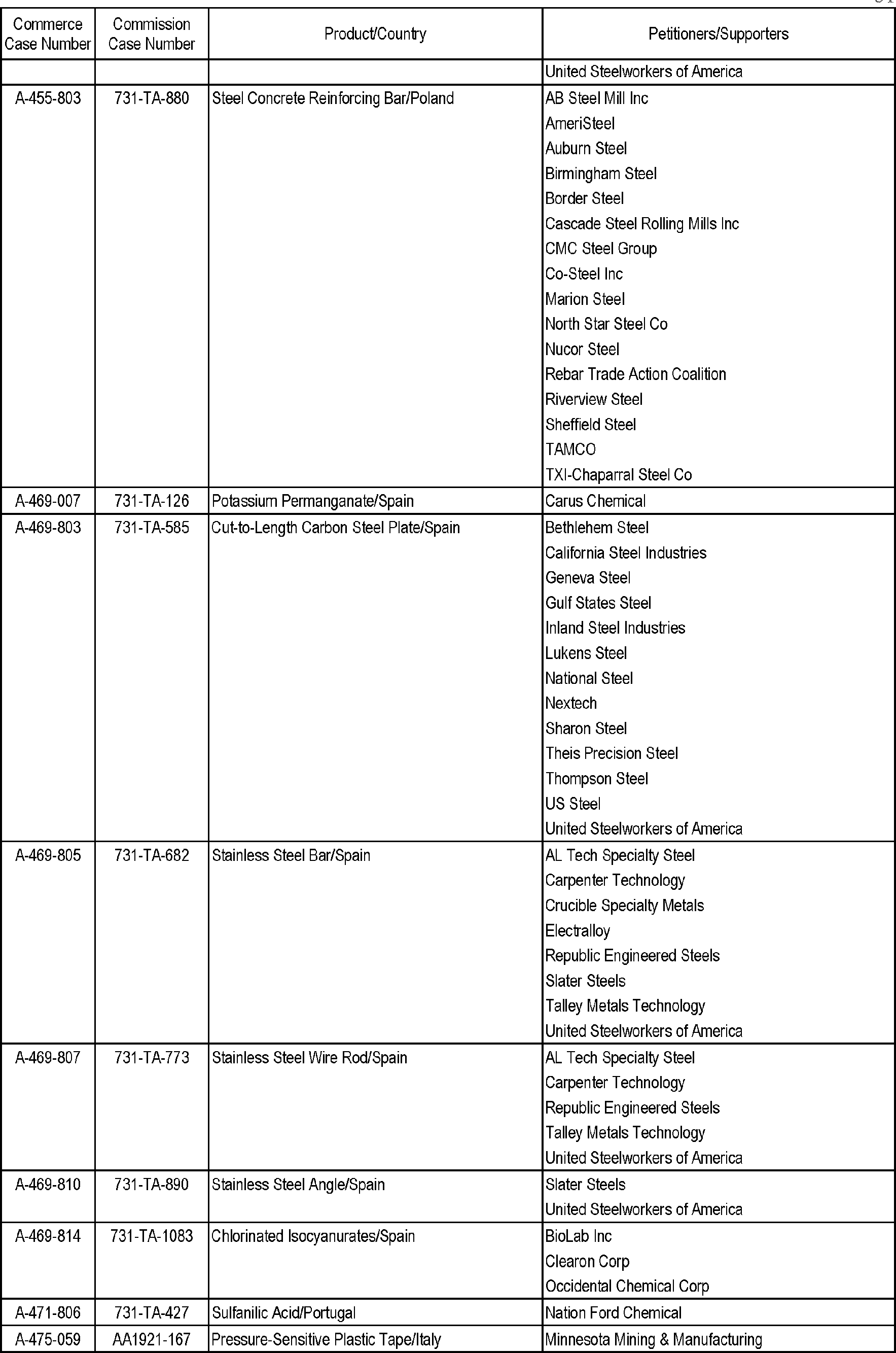

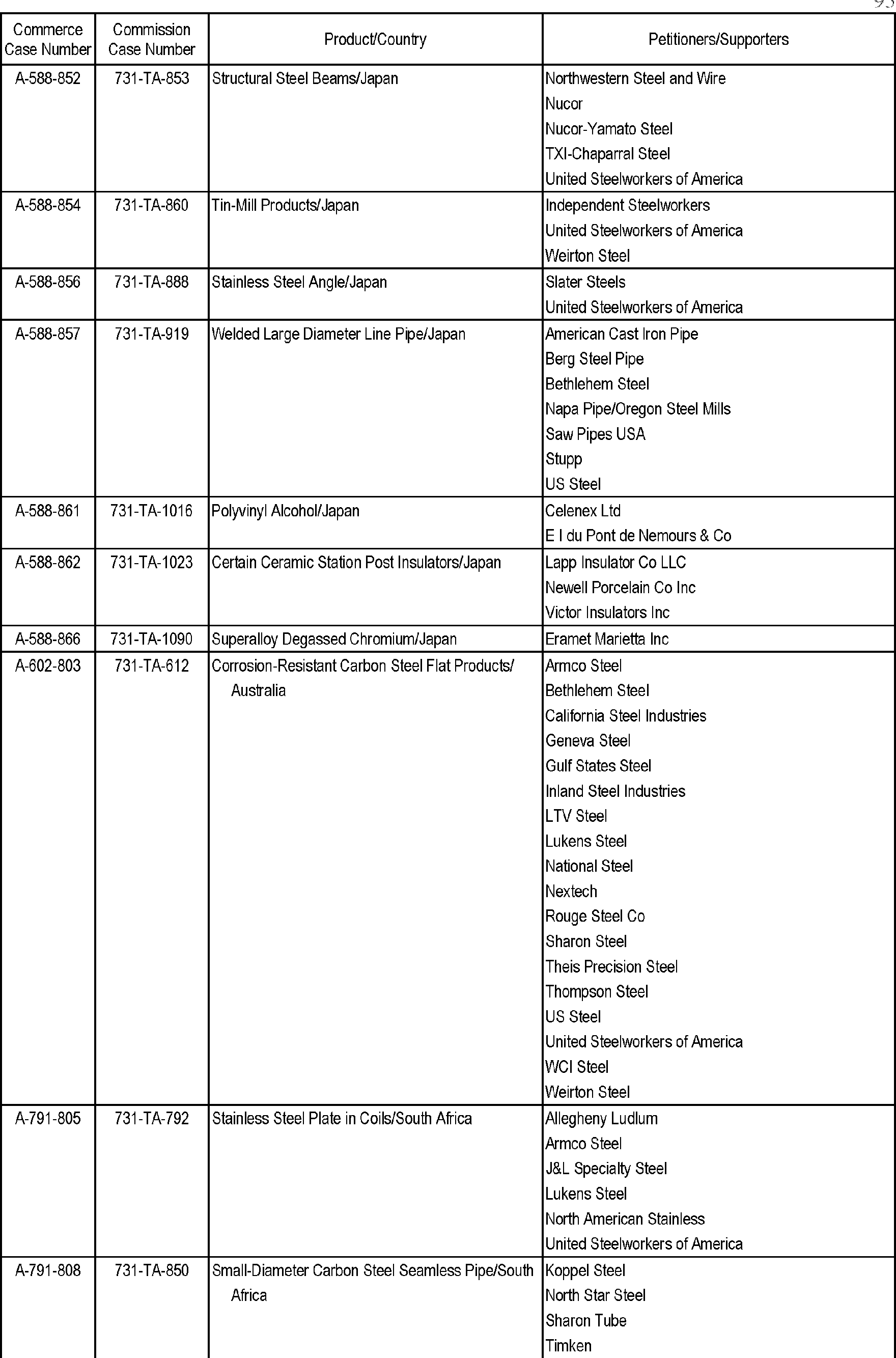

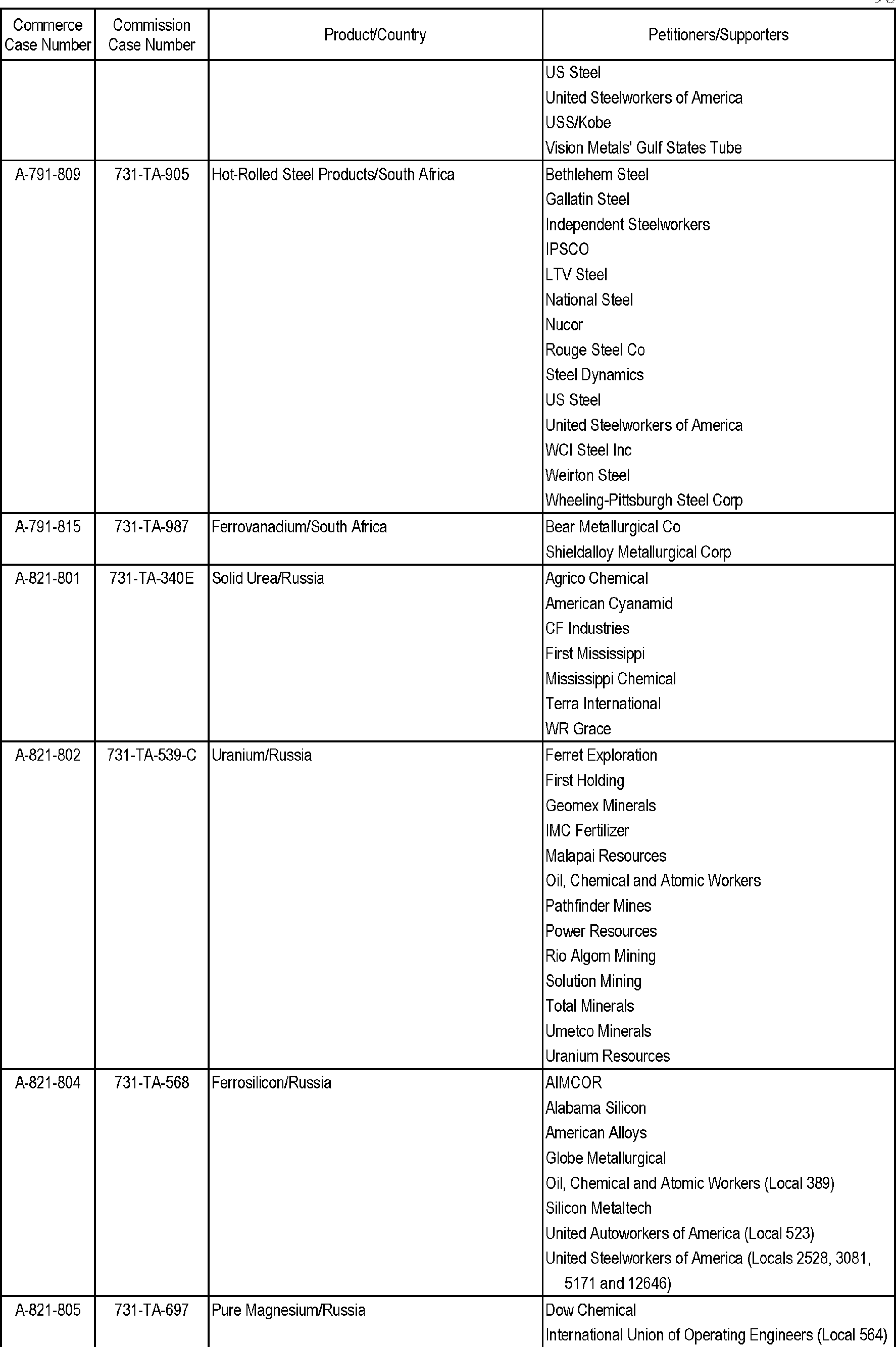

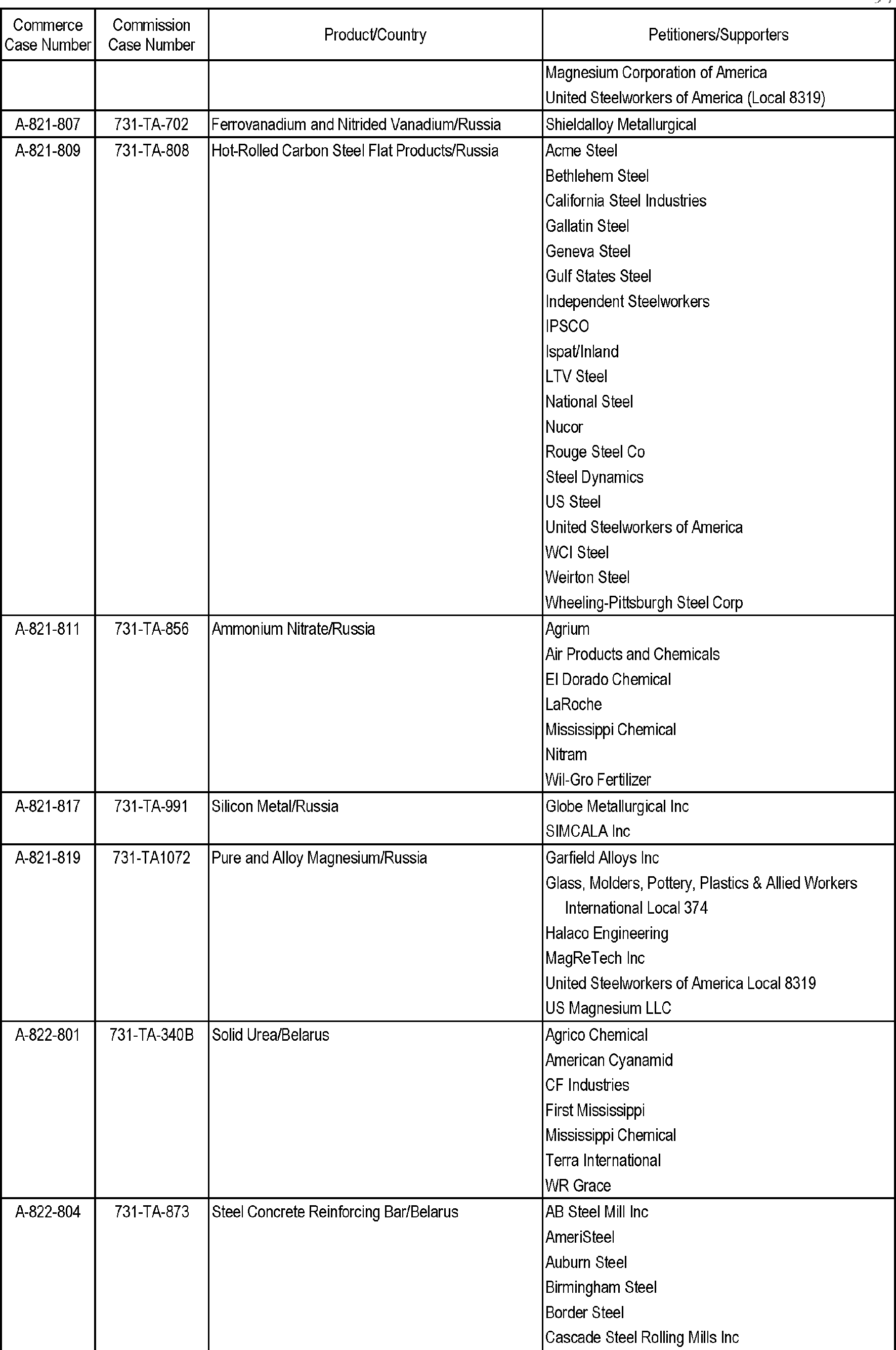

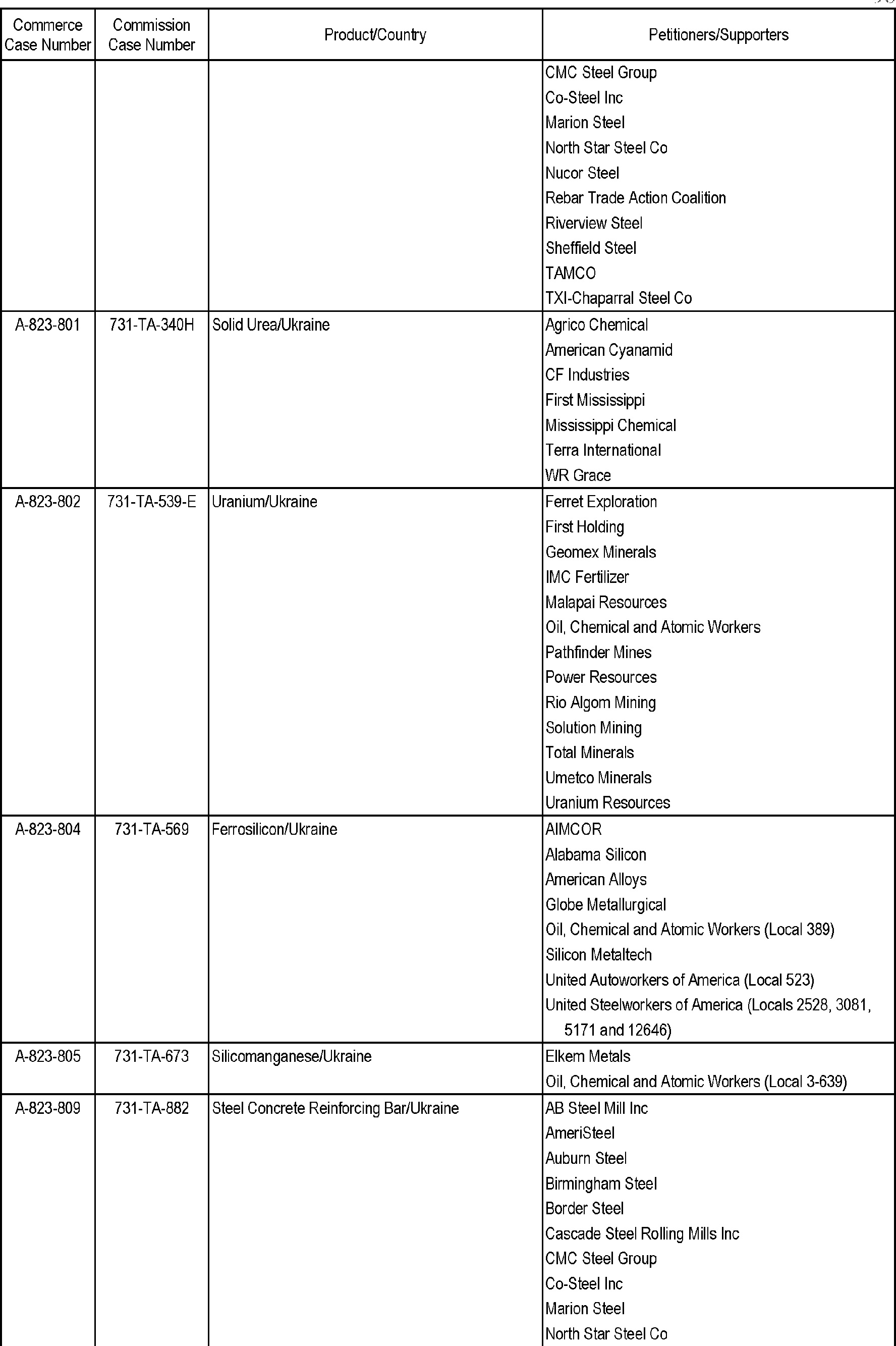

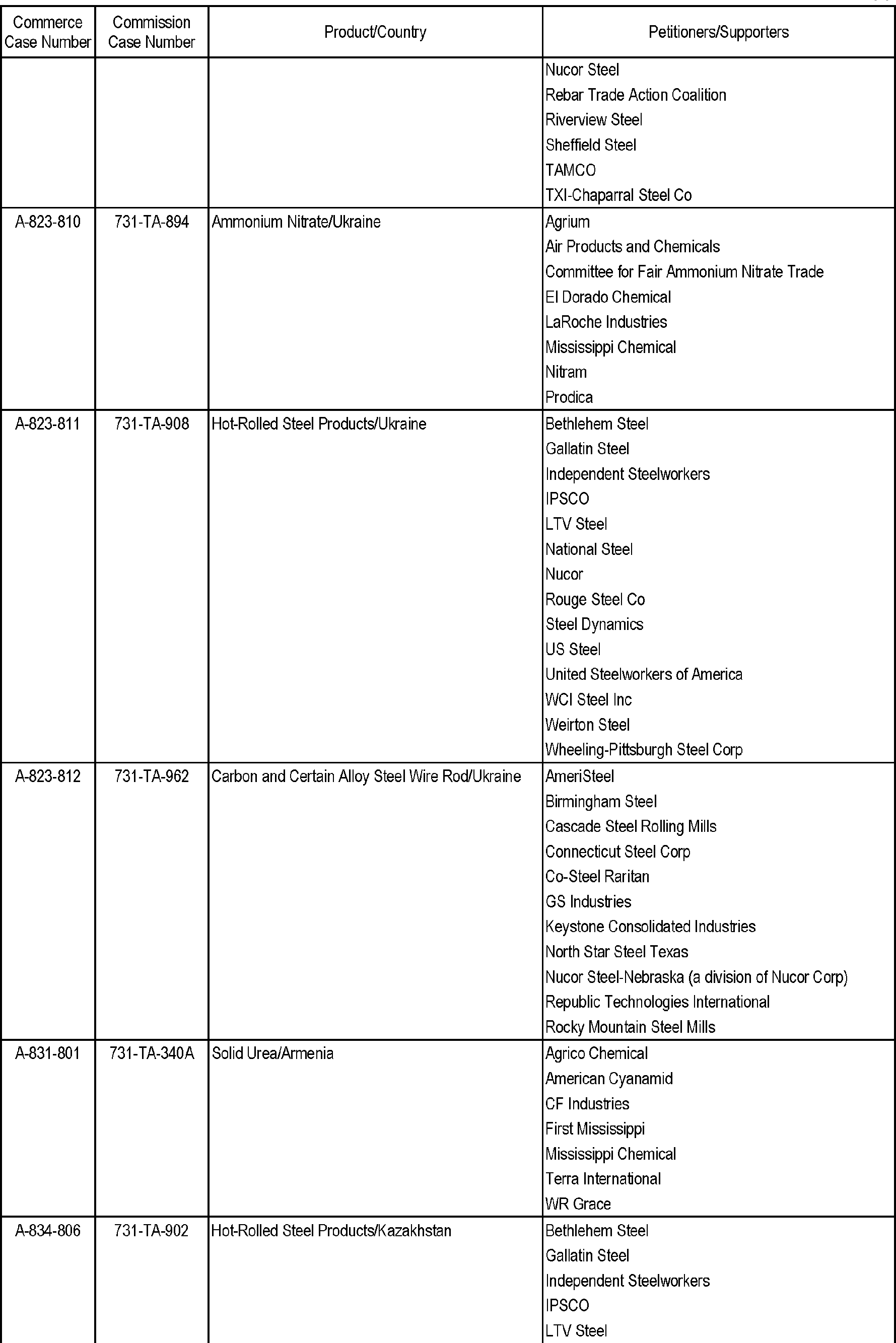

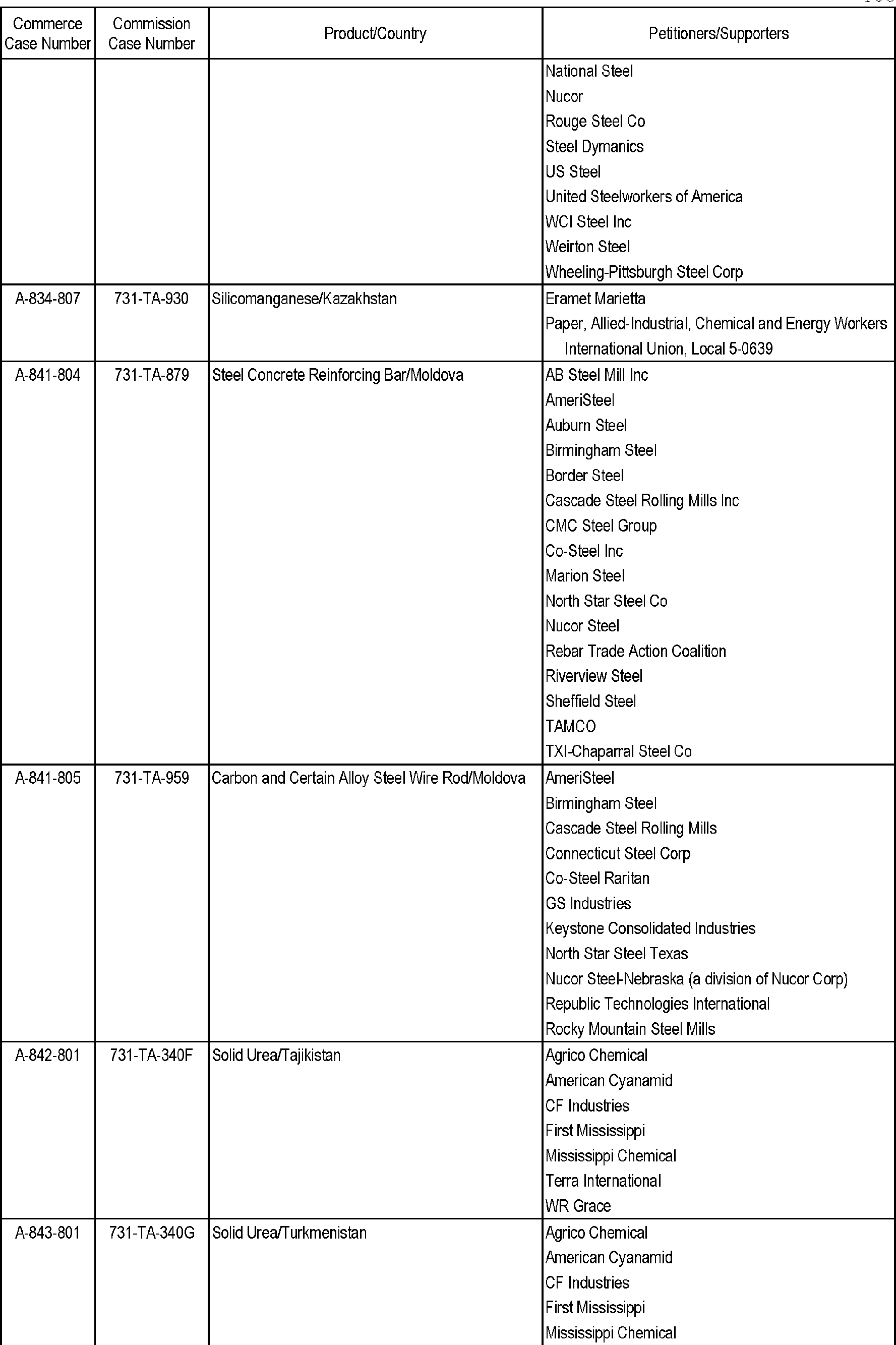

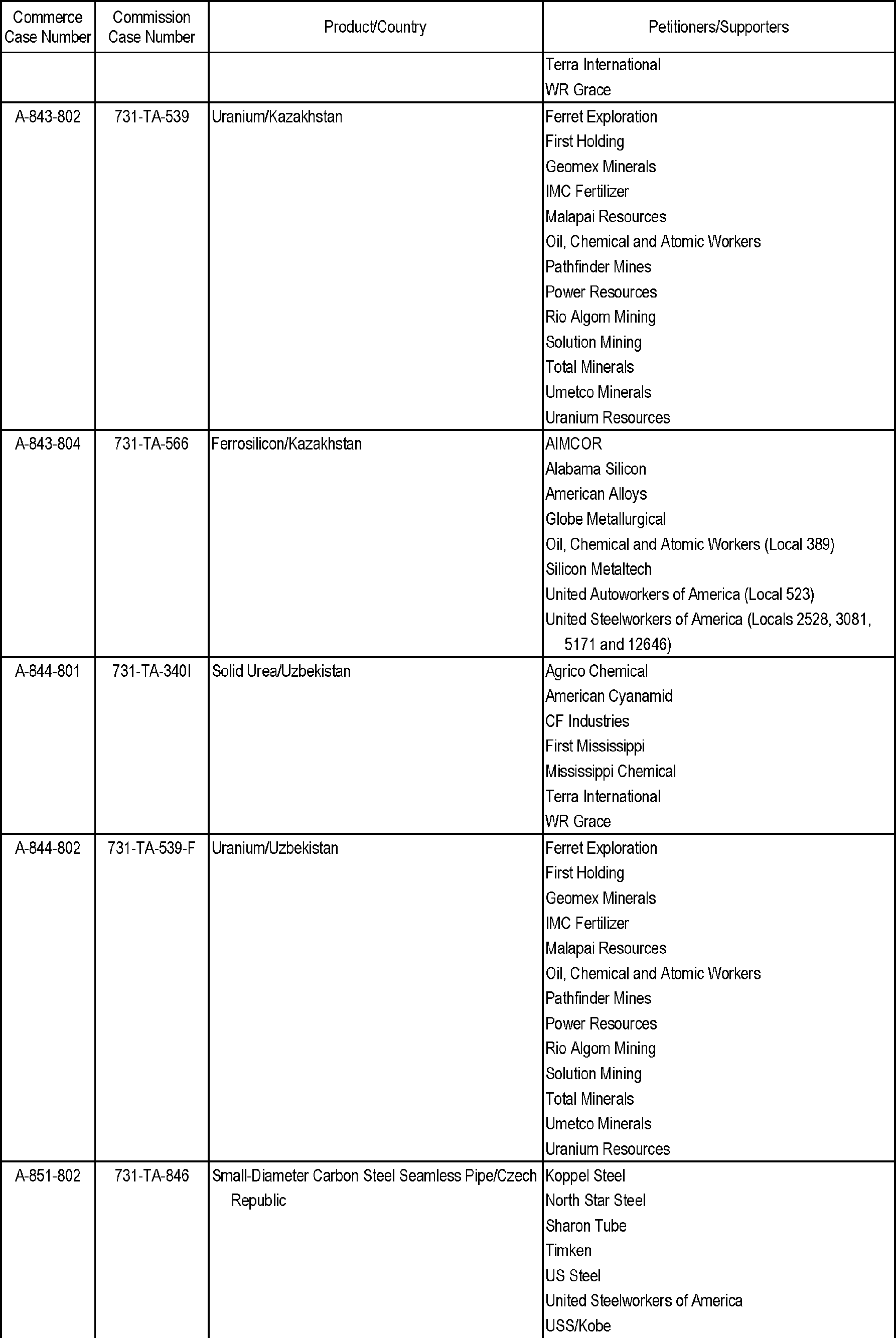

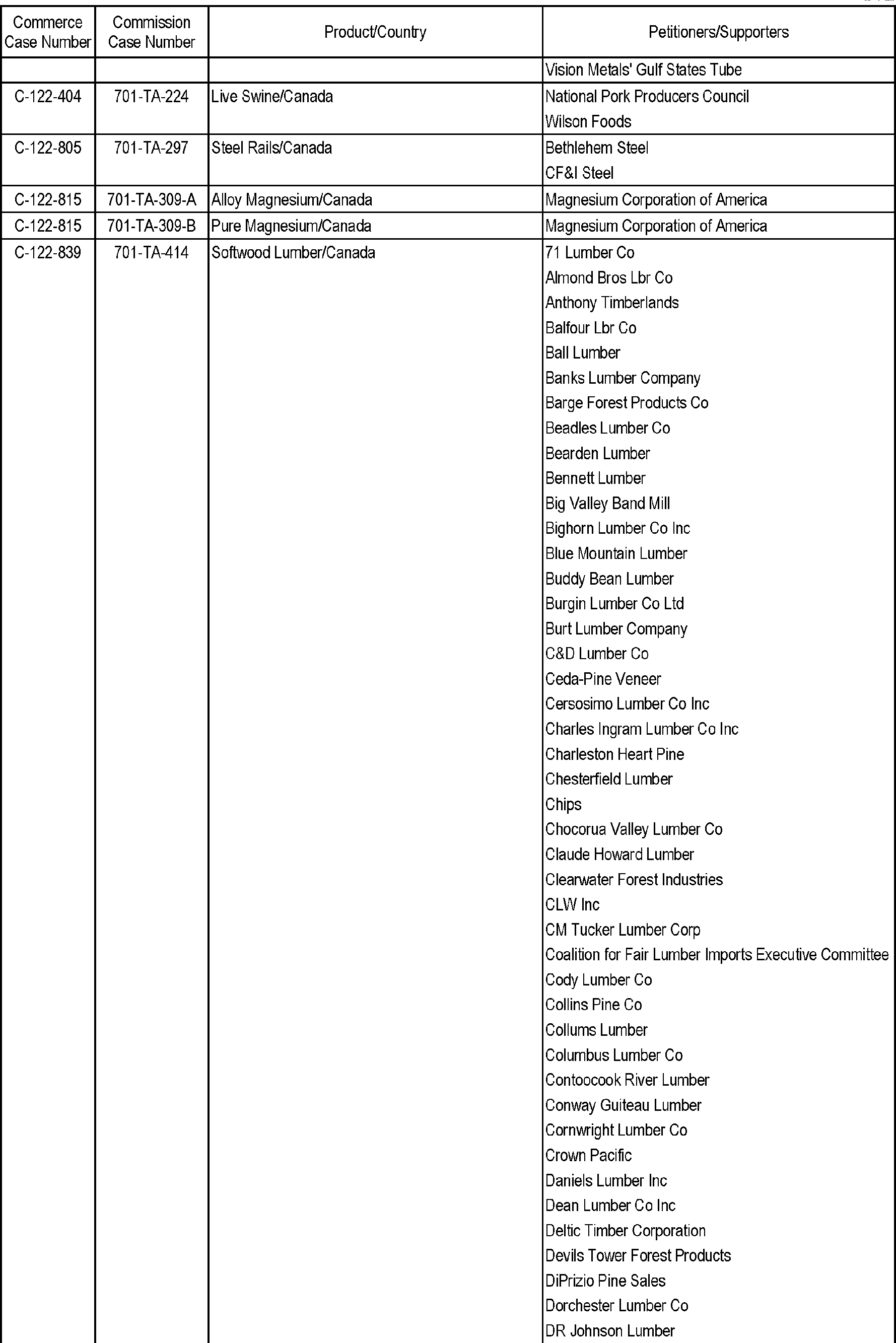

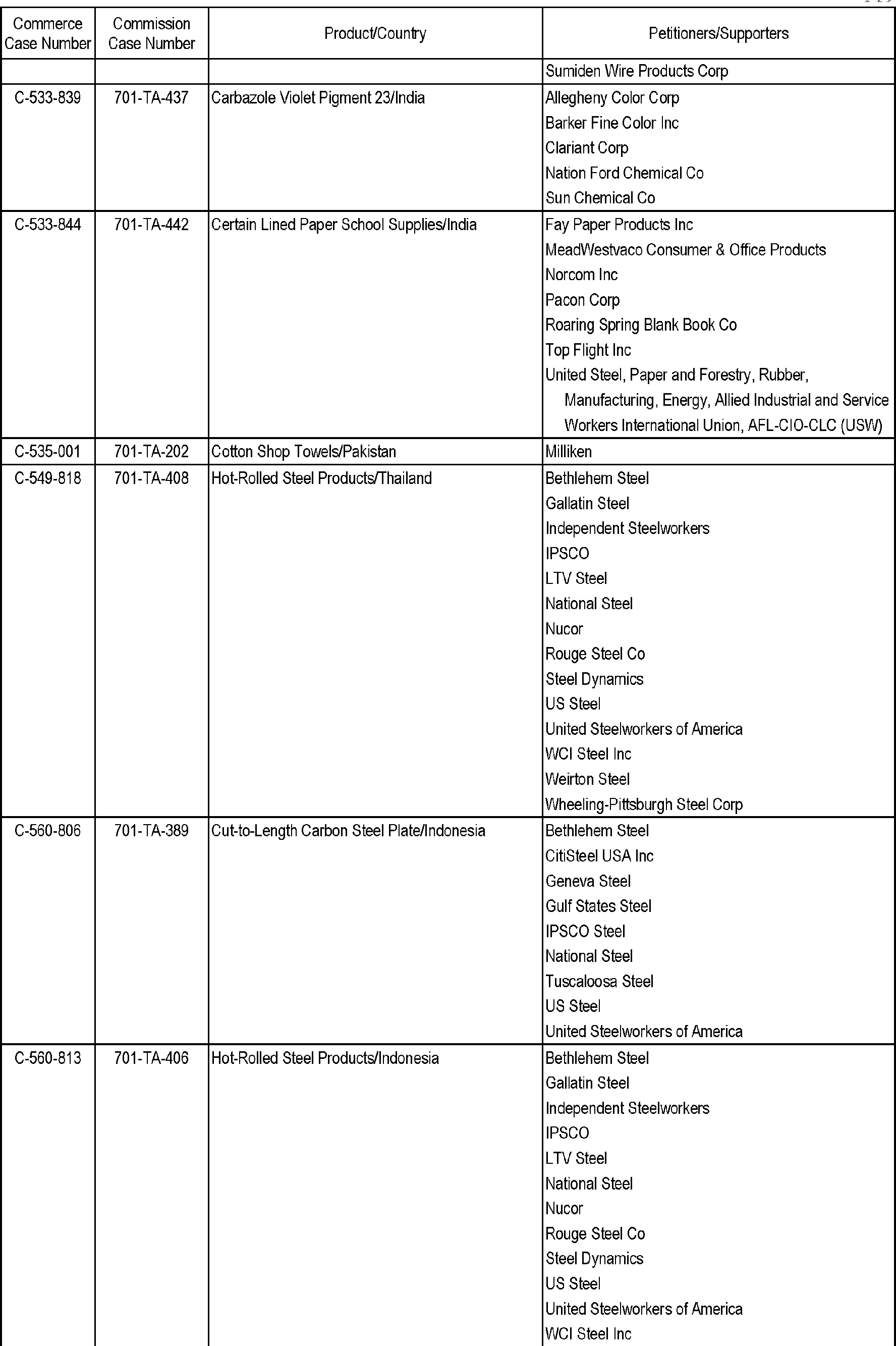

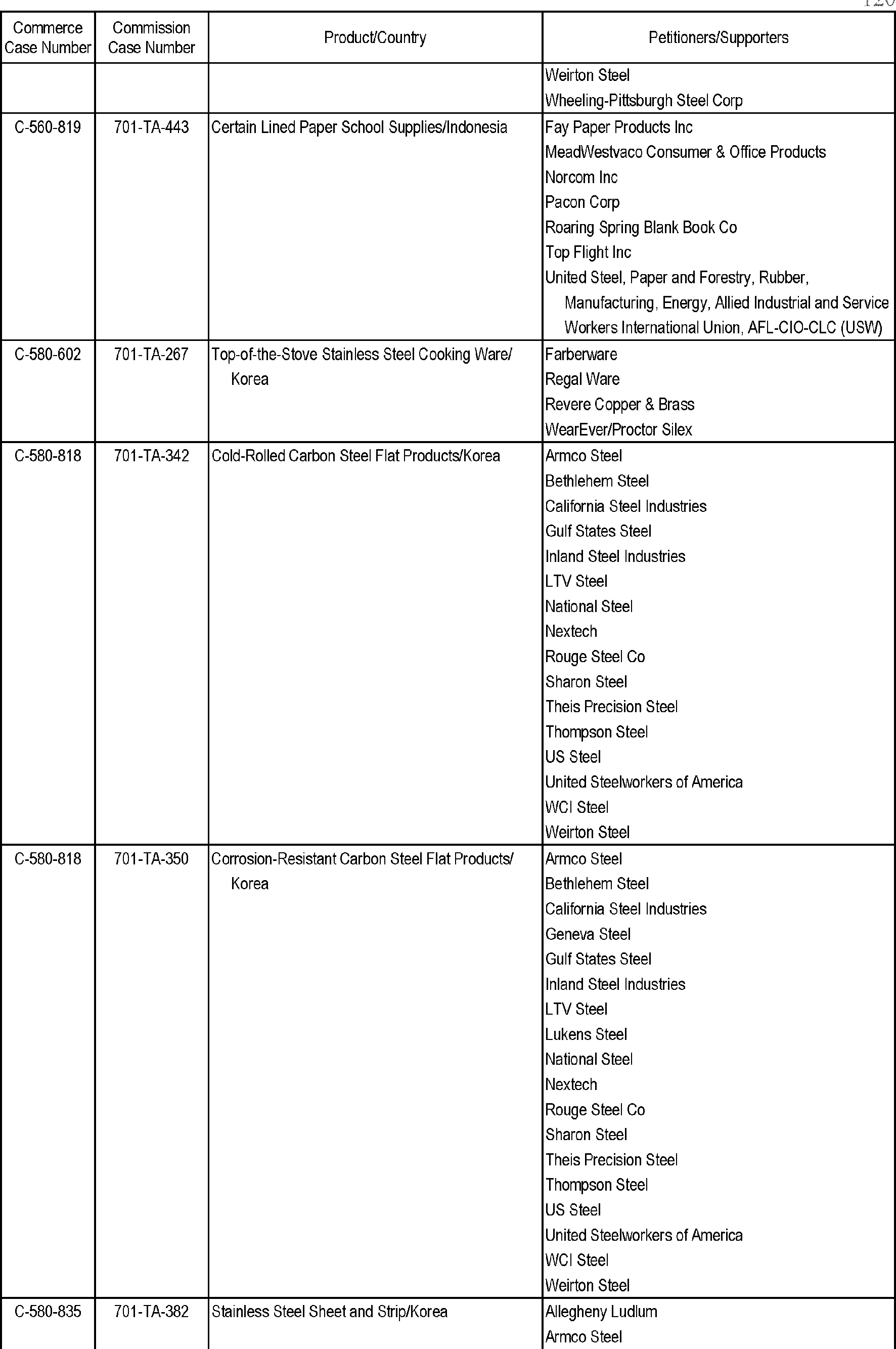

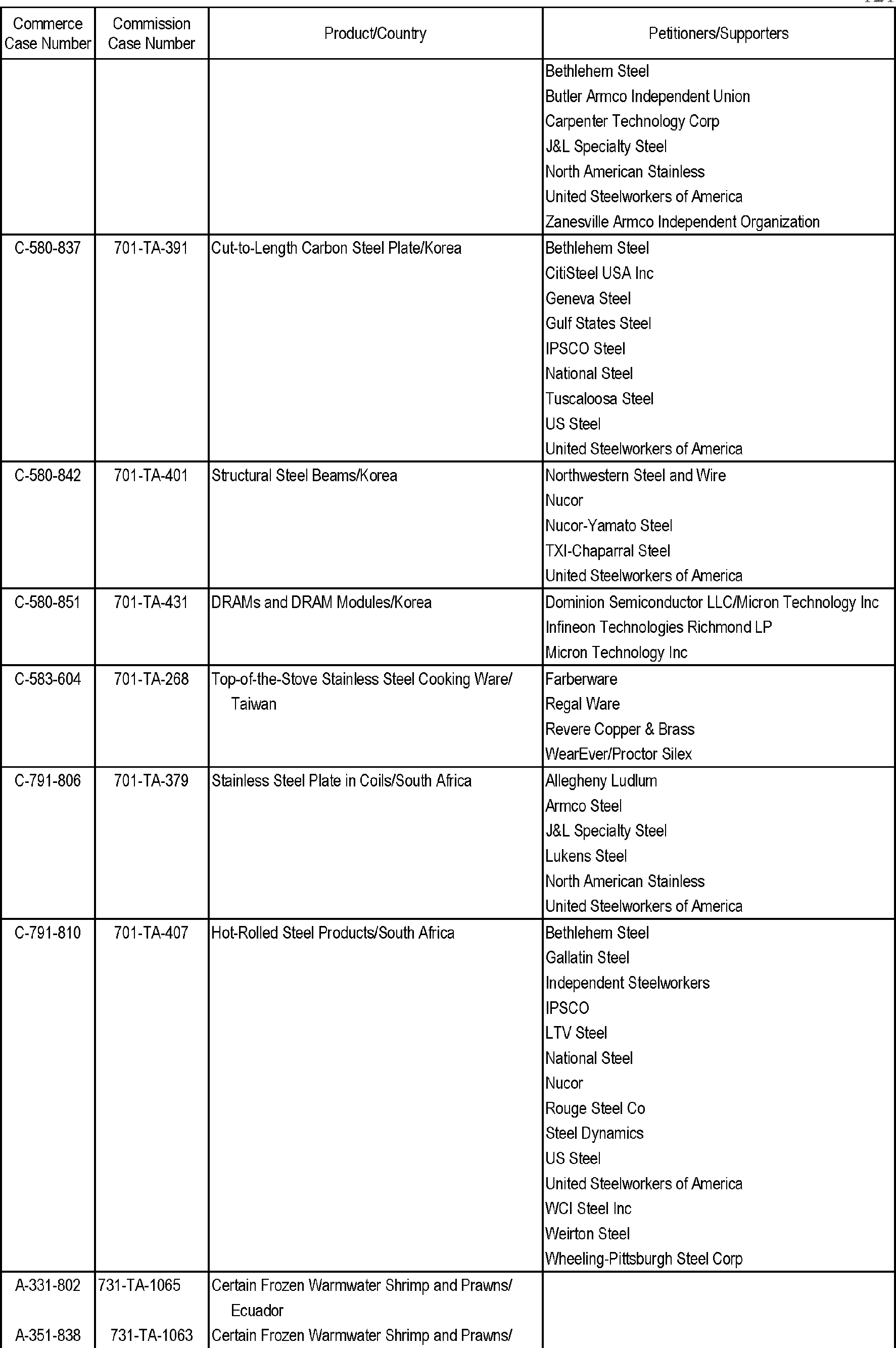

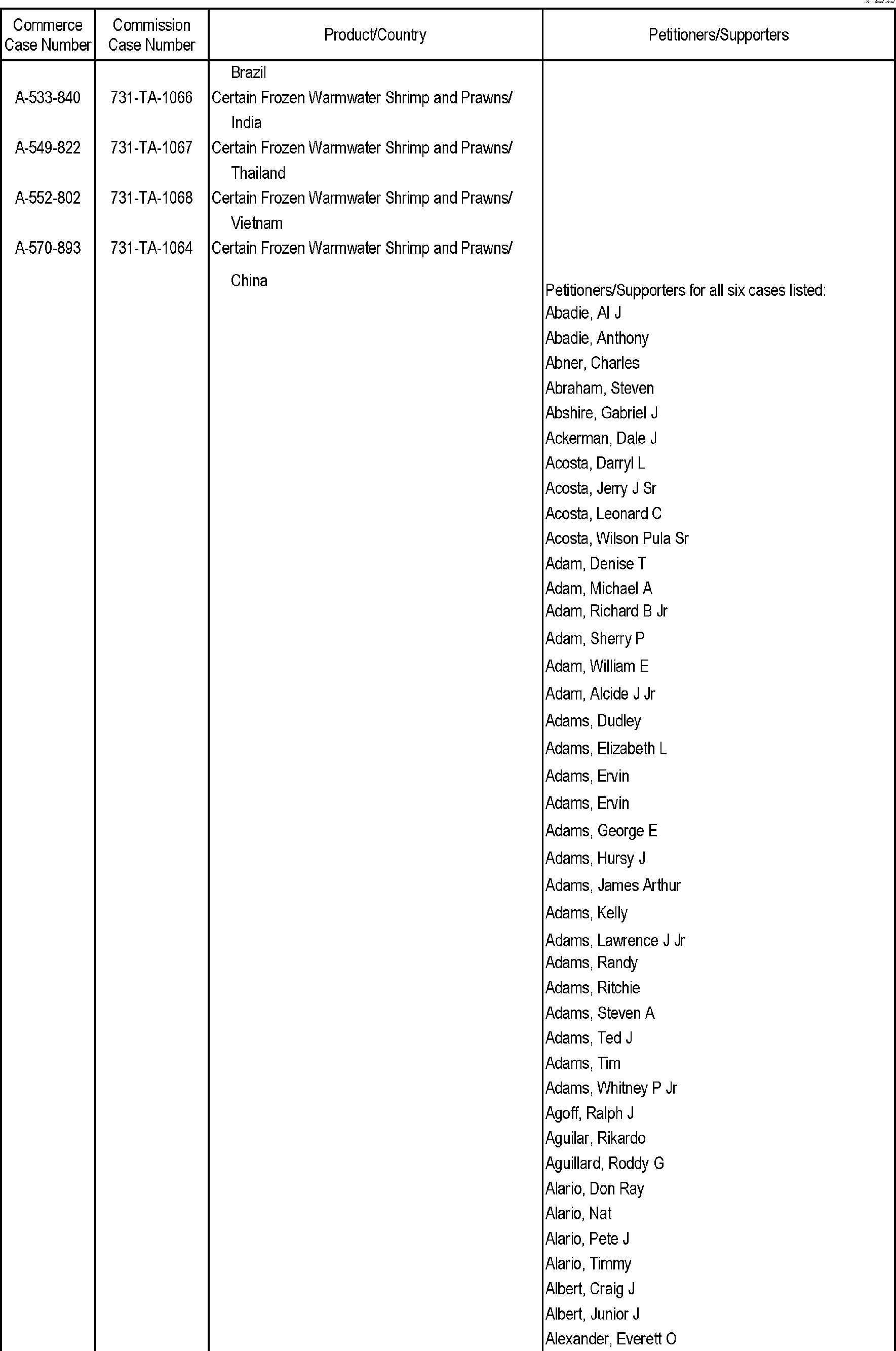

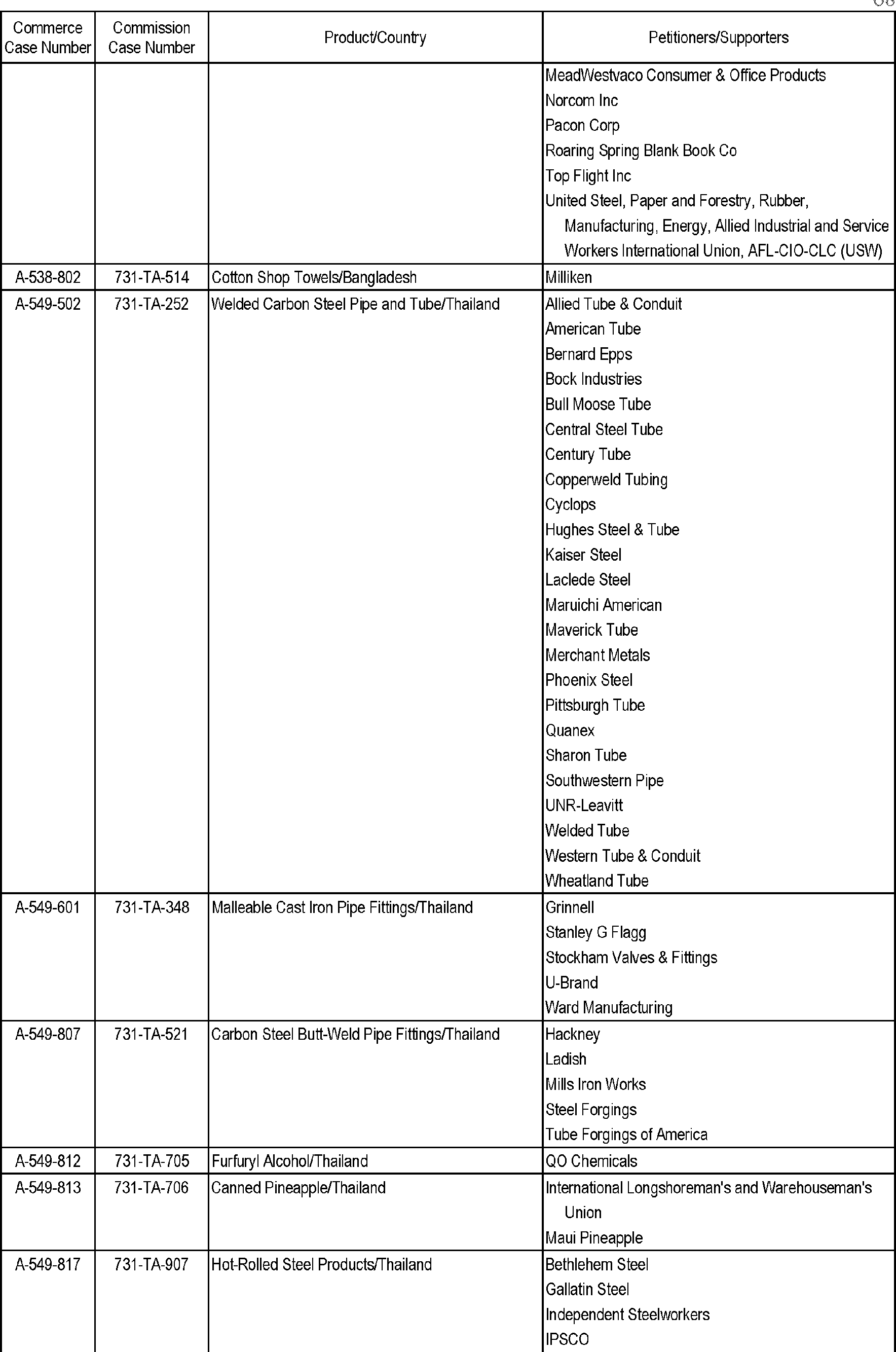

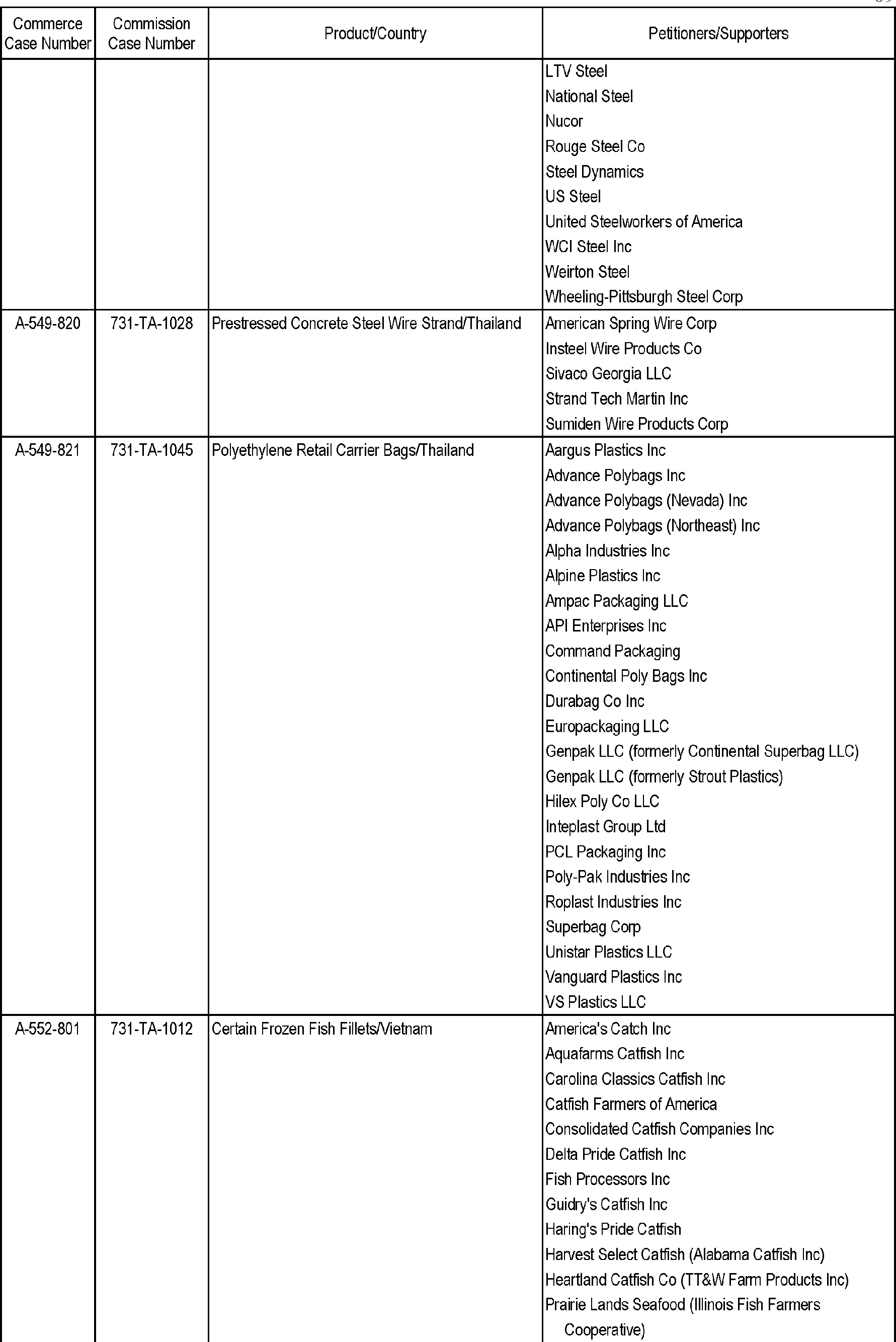

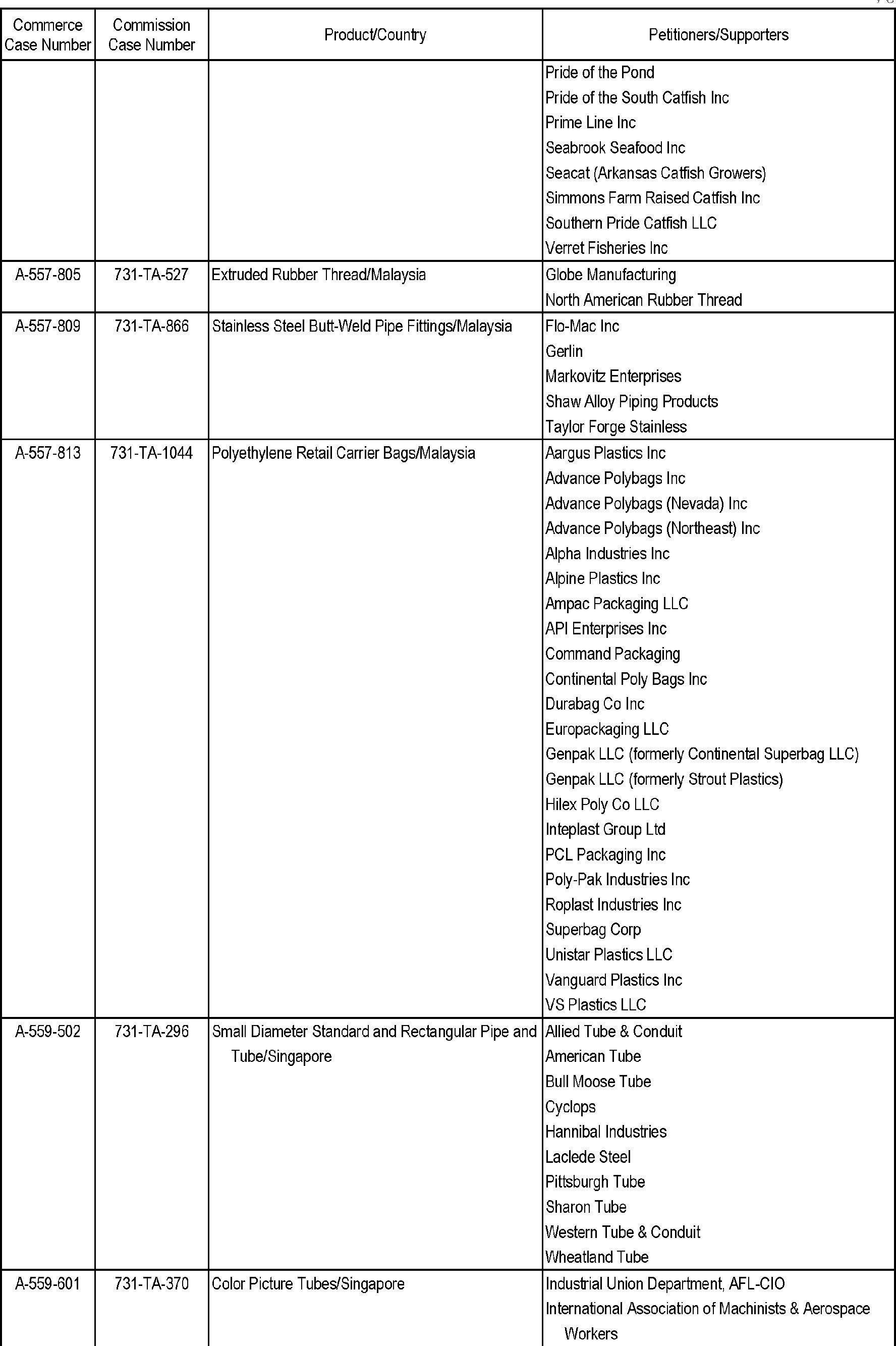

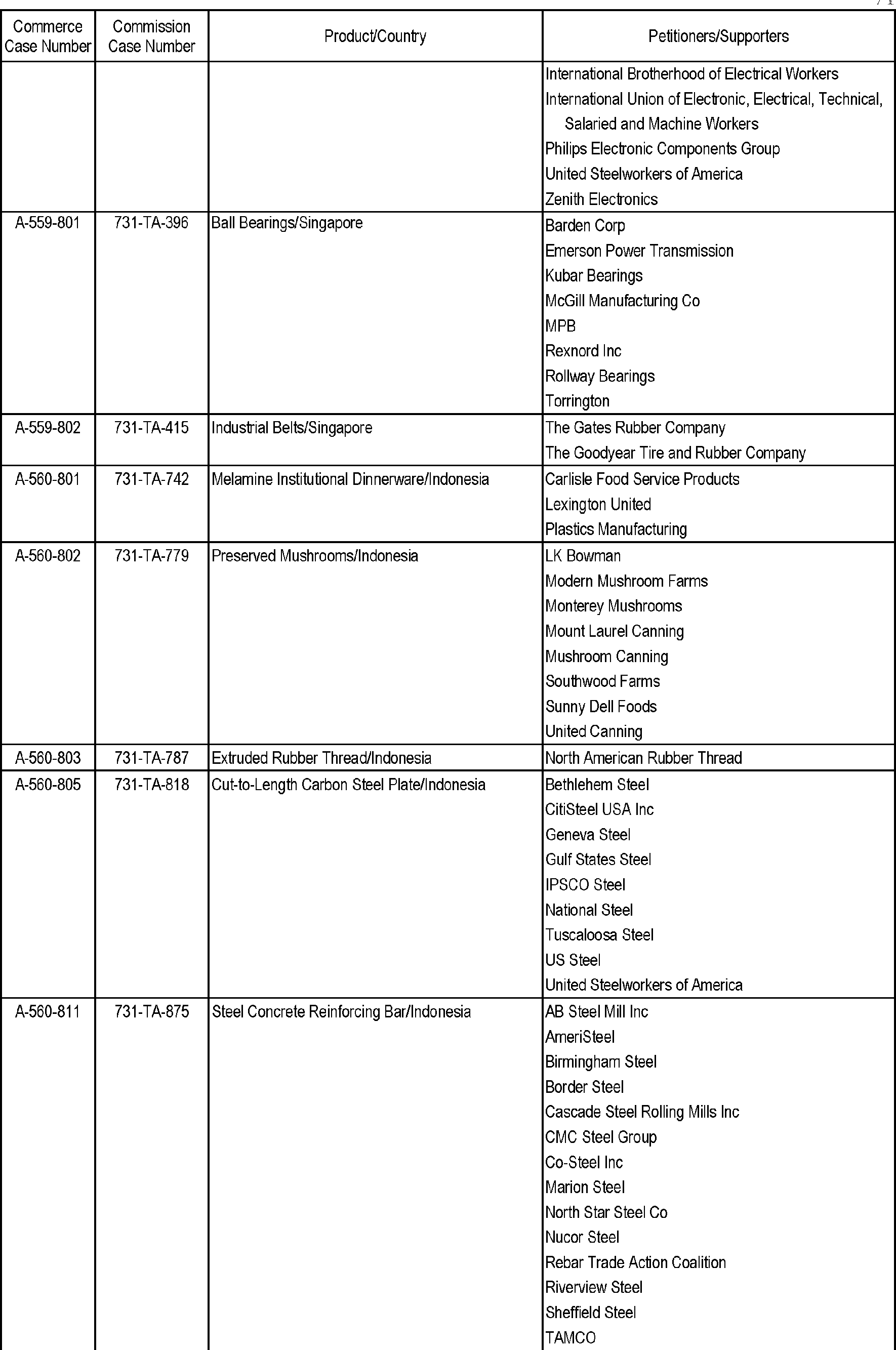

It is the responsibility of the U.S. International Trade Commission (USITC) to ascertain and timely forward to CBP a list of the affected domestic producers that are potentially eligible to receive an offset in connection with an order or finding. In this regard, it is noted that the USITC has supplied CBP with the list of individual antidumping and countervailing duty cases, and the affected domestic producers associated with each case who are potentially eligible to receive an offset. This list appears at the end of this document.

A significant amount of litigation has challenged various provisions of the CDSOA, including the definition of the term “affected domestic producer.” In two decisions, the U.S. Court of Appeals for the Federal Circuit (Federal Circuit) upheld the constitutionality of the support requirement contained in the CDSOA. Specifically, in

SKF USA Inc.

v.

United States Customs &Border Prot.,

556 F.3d 1337 (Fed. Cir. 2009), the Federal Circuit held that the CDSOA's support requirement did not violate either the First or Fifth Amendment. The Supreme Court of the United States denied plaintiff's petition for certiorari,

SKF USA, Inc.

v.

United States Customs & Border Prot., 560 U.S. 903 (2010). Similarly, in

PS Chez Sidney, L.L.C.

v.

United States,

409 Fed. Appx. 327 (Fed. Cir. 2010), the Federal Circuit summarily reversed the U.S. Court of International Trade's judgment that the support requirement was unconstitutional, allowing only plaintiff's non-constitutional claims to go forward. See

PS Chez Sidney, L.L.C.

v.

United States,

684 F.3d 1374 (Fed. Cir. 2012). Furthermore, in two cases interpreting the CDSOA's language, the Federal Circuit concluded that a producer who never indicates support for a dumping petition by letter or through questionnaire response, despite the act of otherwise filling out a questionnaire, cannot be an affected domestic producer.

Ashley Furniture Indus., Inc.et al.

v.

United States,

734 F.3d 1306 (Fed. Cir. 2013), cert. denied, 135 S. Ct. 72 (2014);

Giorgio Foods, Inc.

v.

United Stateset al.,

785 F.3d 595 (Fed. Cir. 2015).

Domestic producers who are not on the USITC list but believe they nonetheless are eligible for a CDSOA distribution under one or more antidumping and/or countervailing duty cases are required, as are all potential claimants that expressly appear on the list, to properly file their certification(s) within 60 days after this notice is published. Such domestic producers must allege all other bases for eligibility in their certification(s). CBP will evaluate the merits of such claims in accordance with the relevant statutes, regulations, and decisions. Certifications that are not timely filed within the requisite 60 days and/or that fail to sufficiently establish a basis for eligibility will be summarily denied. Additionally, CBP may not make a final decision regarding a claimant's eligibility to receive funds until certain legal issues which may affect that claimant's eligibility are resolved. In these instances, CBP may withhold an amount of funds corresponding to the claimant's alleged

pro rata

share of funds from distribution pending the resolution of those legal issues.

It should also be noted that the Federal Circuit ruled in

Canadian Lumber Trade Alliance

v.

United States,

517 F.3d 1319 (Fed. Cir. 2008),

cert. denied sub nom.United States Steel

v.

Canadian Lumber Trade Alliance,

129 S. Ct. 344 (2008), that CBP was not authorized to distribute such antidumping and countervailing duties to the extent they were derived from goods from countries that are parties to the North American Free Trade Agreement (NAFTA). Due to this decision, CBP does not list cases related to NAFTA on the Preliminary Amounts Available report, and no distributions will be issued on these cases.

Regulations Implementing the CDSOA

It is noted that CBP published Treasury Decision (T.D.) 01-68 (Distribution of Continued Dumping and Subsidy Offset to Affected Domestic Producers) in the

Federal Register

(66 FR 48546), effective on September 21, 2001, to implement the CDSOA. The final rule added subpart F to part 159 of title 19, Code of Federal Regulations (19 CFR part 159, subpart F (sections 159.61-159.64)). More specific guidance regarding the filing of certifications is provided in this notice to aid affected domestic producers and other domestic producers alleging eligibility (“claimants” or “domestic producers”).

Notice of Intent To Distribute Offset

This document announces that CBP intends to distribute to affected domestic producers the assessed antidumping and countervailing duties, section 1677g interest, and interest provided for in 19 U.S.C. 4401 that are available for distribution in Fiscal Year 2026 in connection with those antidumping duty orders, findings and countervailing duty orders that are listed in this document. As explained below, CBP is required to issue all CDSOA offset distributions made after March 22, 2024, by electronic funds transfer, unless a Department of the Treasury waiver applies.

Section 159.62(a) of title 19, Code of Federal Regulations (19 CFR 159.62(a)), provides that CBP will publish such a notice of intention to distribute at least 90 calendar days before the end of a fiscal year. Failure to publish the notice at least 90 calendar days before the end of the fiscal year will not affect an affected domestic producer's obligation to file a timely certification within 60 days after the notice is published.

See Dixon Ticonderoga

v.

United States,

468 F.3d 1353, 1354 (Fed. Cir. 2006).

Certifications; Submission and Content

To obtain a distribution of the offset under a given order or finding (including any distribution under 19 U.S.C. 4401), an affected domestic producer (and anyone alleging eligibility to receive a distribution) must timely submit a certification for each order or finding under which a distribution is sought, to CBP, indicating the producer's desire to receive a distribution. Specifically, to be eligible to obtain a distribution, certifications must be submitted electronically at

https://www.pay.gov

or received by CBP's Revenue Modernization Division Attn: CDSOA Team at 8899 E 56th Street, Indianapolis, IN 46249, no later than 60 calendar days after the date of publication of this notice of intent to distribute in the

Federal Register

. Claimants who choose to submit certifications by mail or by an express or courier service must ensure that the certification(s) are actually received by CBP at 8899 E 56th Street, Indianapolis,

( printed page 30806)

IN 46249, no later than 60 calendar days after the date of publication of this notice of intent to distribute in the

Federal Register

. A postmark date, attempted delivery date, or delivery at a location other than 8899 E 56th Street, Indianapolis, IN 46249, is not sufficient. Claimants are encouraged to submit certifications electronically at

https://www.pay.gov

under the Public Form Name, “Continued Dumping and Subsidy Offset Act of 2000 Certification” (CBP Form Number 7401) no later than 60 calendar days after the date of the publication of this notice of intent to distribute to ensure CBP's timely receipt and to avoid any potential delivery delays associated with mail or courier service. All certifications not submitted electronically at

https://www.pay.gov

or received by CBP at 8899 E 56th Street, Indianapolis, IN 46249, by the 60th day, will not be eligible to receive a distribution.

As required by 19 CFR 159.62(b), this notice provides the case name and number of the order or finding concerned, as well as the specific instructions for filing a certification under section 159.63 to claim a distribution. Section 159.62(b) also provides that the dollar amounts subject to distribution that are contained in the Special Account for each listed order or finding are to appear in this notice. However, these dollar amounts were not available in time for inclusion in this publication. The preliminary amounts will be posted on the CBP website (

https://www.cbp.gov). However, the final amounts available for disbursement may be higher or lower than the preliminary amounts.

CBP will provide general information to claimants regarding the preparation of certification(s). However, it remains the sole responsibility of the domestic producer to ensure that the certification is correct, complete, and accurate so as to demonstrate the eligibility of the domestic producer for the distribution requested. Failure to ensure that the certification is correct, complete, and accurate as provided in this notice will result in the domestic producer not receiving a distribution and/or a demand for the return of funds.

Specifically, to obtain a distribution of the offset under a given order or finding (including any distribution under 19 U.S.C. 4401), each potential claimant must timely submit a certification as detailed above containing the required information detailed below as to the eligibility of the domestic producer (or anyone alleging eligibility) to receive the requested distribution and the total amount of the distribution that the domestic producer is claiming. The certification must enumerate the qualifying expenditures incurred by the domestic producer since the issuance of an order or finding and it must demonstrate that the domestic producer is eligible to receive a distribution as an affected domestic producer or allege another basis for eligibility. Any false statements made in connection with certifications submitted to CBP may give rise to liability under the False Claims Act (see 31 U.S.C. 3729-3733) and/or to criminal prosecution.

A successor to a company that was an affected domestic producer at the time of acquisition should consult 19 CFR 159.61(b)(1)(i). Any company that files a certification claiming to be the successor company to an affected domestic producer will be deemed to have consented to joint and several liability for the return of any overpayments arising under 19 CFR 159.64(b)(3) that were previously paid to the predecessor. CBP may require the successor company to provide documents to support its eligibility to receive a distribution as set out in 19 CFR 159.63(d). Additionally, any individual or company who purchases any portion of the operating assets of an affected domestic producer, a successor to an affected domestic producer, or an entity that otherwise previously received distributions may be jointly and severally liable for the return of any overpayments arising under 19 CFR 159.64(b)(3) that were previously paid to the entity from which the operating assets were purchased or its predecessor, regardless of whether the purchasing individual or company is deemed a successor company for purposes of receiving distributions.

A member company (or its successor) of an association that appears on the list of affected domestic producers in this notice, where the member company itself does not appear on this list, should consult 19 CFR 159.61(b)(1)(ii). Specifically, for a certification under 19 CFR 159.61(b)(1)(ii), the claimant must name the association of which it is a member, specifically establish that it was a member of the association at the time the association filed the petition with the USITC, and establish that the claimant is a current member of the association.

In order to promote accurate filings and more efficiently process the distributions, we offer the following guidance:

If claimants are members of an association but the association does not file on their behalf, the association will need to provide its members with a statement that contains notarized company-specific information including dates of membership and an original signature from an authorized representative of the association.

An association filing a certification on behalf of a member must also provide a power of attorney or other evidence of legal authorization from each of the domestic producers it represents.

Any association filing a certification on behalf of a member is responsible for verifying the legal sufficiency and accuracy of the member's financial records, which support the claim, and is responsible for that certification. As such, an association filing a certification on behalf of a member is jointly and severally liable with the member for repayment of any claim found to have been paid or overpaid in error.

The association may file a certification in its own right to claim an offset for that order or finding, but its qualifying expenditures would be limited to those expenditures that the association itself has incurred after the date of the order or finding in connection with the particular case.

As provided in 19 CFR 159.63(a), certifications to obtain a distribution of an offset (including any distribution under 19 U.S.C. 4401) must be received by CBP through the submission methods detailed above no later than 60 calendar days after the date of publication of the notice of intent in the

Federal Register

. All certifications received after the 60-day deadline will be summarily denied, making claimants ineligible for the distribution regardless of whether or not they appear on the USITC list.

A list of all certifications received will be published on the CBP website (

https://www.cbp.gov) shortly after the receipt deadline. This publication will not confirm acceptance or validity of the certification but merely receipt of the certification. Due to the high volume of certifications, CBP is unable to respond to individual telephone or written inquiries regarding the status of a certification appearing on the list.

While there is no required format for a certification, CBP has developed a standard certification form to aid claimants in filing certifications. The certification form is available at

https://www.pay.gov

under the Public Form Name “Continued Dumping and Subsidy Offset Act of 2000 Certification” (CBP Form Number 7401) or by directing a web browser to

https://www.pay.gov/public/form/start/8776895/. The certification form can be submitted electronically through

https://www.pay.gov

or by mail, express or courier service at the address

( printed page 30807)

identified above. All certifications not submitted electronically must include original signatures.

Regardless of the format for a certification, per 19 CFR 159.63(b), the certification must contain the following information:

(1) The date of this

Federal Register

notice;

(2) The Department of Commerce antidumping or countervailing duty case number (for example, A-331-802);

(3) The case name (product/country);

(4) The name of the domestic producer and any name qualifier, if applicable (for example, any other name under which the domestic producer does business or is also known);

(5) The mailing address of the domestic producer (if a post office box, the physical street address must also appear) including, if applicable, a specific room number or department;

(6) The Internal Revenue Service (IRS) number (with suffix) of the domestic producer, employer identification number, or social security number, as applicable;

(7) The specific business organization of the domestic producer (corporation, partnership, sole proprietorship);

(8) The name(s) of any individual(s) designated by the domestic producer as the contact person(s) concerning the certification, together with the phone number(s), mailing address, and, if available, facsimile transmission number(s) and electronic mail (email) address(es) for the person(s). Correspondence from CBP may be directed to the designated contact(s) by either mail or phone or both;

(9) The total dollar amount claimed;

(10) The dollar amount claimed by category, as described in the section below entitled “Amount Claimed for Distribution;”

(11) A statement of eligibility, as described in the section below entitled “Eligibility to Receive Distribution;” and

(12) For certifications not submitted electronically through

https://www.pay.gov,

an original signature by an individual legally authorized to bind the producer.

Qualifying Expenditures That May Be Claimed for Distribution

Qualifying expenditures that may be offset under the CDSOA encompass those expenditures incurred by the domestic producer after issuance of an antidumping duty order or finding or a countervailing duty order (including expenditures incurred on the date of the order's issuance), and prior to its termination, provided that such expenditures fall within certain categories. See 19 CFR 159.61(c). The CDSOA repeal language parallels the termination of an order or finding. Therefore, for duty orders or findings that have not been previously revoked or were not revoked prior to October 1, 2007, expenses must be incurred before October 1, 2007, to be eligible for offset. For duty orders or findings that were revoked prior to October 1, 2007, expenses must be incurred before the effective date of the revocation to be eligible for offset. For example, assume for case A-331-802, Certain Frozen Warm-Water Shrimp and Prawns from Ecuador, that the order date is February 1, 2005, and that the revocation effective date is August 15, 2007. In this case, eligible expenditures would have to be incurred on or after February 1, 2005, up to and including August 14, 2007; expenditures incurred on or after August 15, 2007, cannot be included as eligible qualifying expenditures for A-331-802.

For the convenience and ease of the domestic producers, CBP is providing guidance on what the agency takes into consideration when making a calculation for each of the following categories:

(1) Manufacturing facilities (Any facility used for the transformation of raw material into a finished product that is the subject of the related order or finding);

(2) Equipment (Goods that are used in a business environment to aid in the manufacturing of a product that is the subject of the related order or finding);

(3) Research and development (Seeking knowledge and determining the best techniques for production of the product that is the subject of the related order or finding);

(4) Personnel training (Teaching of specific useful skills to personnel, that will improve performance in the production process of the product that is the subject of the related order or finding);

(5) Acquisition of technology (Acquisition of applied scientific knowledge and materials to achieve an objective in the production process of the product that is the subject of the related order or finding);

(6) Health care benefits for employees paid for by the employer (Health care benefits paid to employees who are producing the specific product that is the subject of the related order or finding);

(7) Pension benefits for employees paid for by the employer (Pension benefits paid to employees who are producing the specific product that is the subject of the related order or finding);

(8) Environmental equipment, training, or technology (Equipment, training, or technology used in the production of the product that is the subject of the related order or finding, that will assist in preventing potentially harmful factors from affecting the environment);

(9) Acquisition of raw materials and other inputs (Purchase of unprocessed materials or other inputs needed for the production of the product that is the subject of the related order or finding); and

(10) Working capital or other funds needed to maintain production (Assets of a business that can be applied to its production of the product that is the subject of the related order or finding).

Amount Claimed for Distribution

In calculating the amount of the distribution being claimed as an offset, the certification must indicate:

(1) The total amount of any qualifying expenditures previously certified by the domestic producer, and the amount certified by category;

(2) The total amount of those expenditures which have been the subject of any prior distribution for the order or finding being certified under 19 U.S.C. 1675c; and

(3) The net amount for new and remaining qualifying expenditures being claimed in the current certification (the total amount previously certified as noted in item “(1)” above minus the total amount that was the subject of any prior distribution as noted in item “(2)” above). In accordance with 19 CFR 159.63(b)(2)(i)-(iii), CBP will deduct the amount of any prior distribution from the producer's claimed amount for that case. Total amounts disbursed by CBP under the CDSOA for some prior Fiscal Years are available on the CBP website.

Additionally, under 19 CFR 159.61(c), these qualifying expenditures must be related to the production of the same product that is the subject of the order or finding, with the exception of expenses incurred by associations which must be related to a specific case. Any false statements made to CBP concerning the amount of distribution being claimed as an offset may give rise to liability under the False Claims Act (see 31 U.S.C. 3729-3733) and/or to criminal prosecution.

Eligibility To Receive Distribution

As noted, the certification must contain a statement that the domestic producer desires to receive a distribution and is eligible to receive the distribution as an affected domestic producer or on another legal basis. Also, the domestic producer must affirm that

( printed page 30808)

the net amount certified for distribution does not encompass any qualifying expenditures for which distribution has previously been made (19 CFR 159.63(b)(3)(i)). Any false statements made in connection with certifications submitted to CBP may give rise to liability under the False Claims Act (see 31 U.S.C. 3729-3733) and/or to criminal prosecution.

Furthermore, under 19 CFR 159.63(b)(3)(ii), where a domestic producer files a separate certification for more than one order or finding using the same qualifying expenditures as the basis for distribution in each case, each certification must list all the other orders or findings where the producer is claiming the same qualifying expenditures.

Moreover, as required by 19 U.S.C. 1675c(b)(1) and 19 CFR 159.63(b)(3)(iii), the certification must include information as to whether the domestic producer remains in operation at the time the certifications are filed and continues to produce the product covered by the particular order or finding under which the distribution is sought. If a domestic producer is no longer in operation, or no longer produces the product covered by the order or finding, the producer will not be considered an affected domestic producer entitled to receive a distribution.

In addition, as required by 19 U.S.C. 1675c(b)(5) and 19 CFR 159.63(b)(3)(iii), the domestic producer must state whether it has been acquired by a company that opposed the investigation or was acquired by a business related to a company that opposed the investigation. If a domestic producer has been so acquired, the producer will not be considered an affected domestic producer entitled to receive a distribution. However, CBP may not make a final decision regarding a claimant's eligibility to receive funds until certain legal issues which may affect that claimant's eligibility are resolved. In these instances, CBP may withhold an amount of funds corresponding to the claimant's alleged pro rata share of funds from distribution pending the resolution of those legal issues.

The certification must be executed and dated by a party legally authorized to bind the domestic producer and it must state that the information contained in the certification is true and accurate to the best of the certifier's knowledge and belief under penalty of law, and that the domestic producer has records to support the qualifying expenditures being claimed (see section below entitled “Verification of Certification”). Moreover, as provided in 19 CFR 159.64(b)(3), all overpayments to affected domestic producers are recoverable by CBP, and CBP reserves the right to use all available collection tools to recover overpayments, including but not limited to garnishments, court orders, administrative offset, enrollment in the Treasury Offset Program, and/or offset of tax refund payments. Overpayments may occur for a variety of reasons, including but not limited to: reliquidations, court actions, settlements, insufficient verification of a certification in response to an inquiry from CBP, and administrative errors. With diminished amounts available over time, the likelihood that these events will require the recovery of funds previously distributed will increase. As a result, domestic producers who receive distributions under the CDSOA may wish to set aside any funds received in case it is subsequently determined that an overpayment has occurred. CBP considers the submission of a certification and the crediting of the distribution amount to the appropriate account by electronic funds transfer or the negotiation of any distribution checks received as acknowledgements and acceptance of the claimant's obligation to return those funds upon demand.

Review and Correction of Certification

A certification that is submitted electronically at

https://www.pay.gov

or received by CBP at 8899 E 56th Street, Indianapolis, IN 46249, within 60 calendar days after the date of publication of this notice in the

Federal Register

, may, at CBP's sole discretion, be subject to review before acceptance to ensure that all informational requirements are complied with and that any amounts set forth in the certification for qualifying expenditures, including the amount claimed for distribution, appear to be correct. A certification that is found to be materially incorrect or incomplete will be returned to the domestic producer within 15 business days after the close of the 60-calendar-day filing period, as provided in 19 CFR 159.63(c). CBP must receive a corrected certification from the domestic producer and/or an association filing on behalf of an association member within 10 business days from the date of the original denial letter. Failure to receive a corrected certification within 10 business days will result in denial of the certification at issue. The return of a certification for correction does not preclude CBP from taking other actions related to the incorrect or incomplete initial certification. It is the sole responsibility of the domestic producer to ensure that the certification is correct, complete, and accurate so as to demonstrate the eligibility of the domestic producer to the distribution requested. Failure to ensure that the certification is correct, complete, and accurate will result in the domestic producer not receiving a distribution and/or a demand for the return of funds, in addition to other potential legal and administrative consequences.

Verification of Certification

Certifications are subject to CBP's verification. The burden remains on each claimant to fully substantiate all elements of its certification. As such, claimants may be required to provide copies of additional records for further review by CBP. Therefore, parties are required to maintain, and be prepared to produce, records adequately supporting their claims for a period of five years after the filing of the certification (19 CFR 159.63(d)). The records must demonstrate that each qualifying expenditure enumerated in the certification was actually incurred, and they must support how the qualifying expenditures are determined to be related to the production of the product covered by the order or finding. Although CBP will accept comments and information from the public and other domestic producers, CBP retains complete discretion regarding the initiation and conduct of investigations stemming from such information. In the event that a distribution is made to a domestic producer from whom CBP later seeks verification of the certification and sufficient supporting documentation is not provided as determined by CBP, then the amounts paid to the affected domestic producer are recoverable by CBP as an overpayment. CBP reserves the right to use all available collection tools to recover overpayments, including but not limited to garnishments, court orders, administrative offset, enrollment in the Treasury Offset Program, and/or offset of tax refund payments. CBP considers the submission of a certification and the crediting of the distribution amount to the appropriate account by electronic funds transfer or the negotiation of any distribution checks received as acknowledgements and acceptance of the claimant's obligation to return those funds upon demand. Failure to repay overpayments upon demand may result in administrative consequences. Additionally, the submission of false statements, documents, or records in connection with a certification or verification of a certification may give

( printed page 30809)

rise to liability under the False Claims Act (see 31 U.S.C. 3729-3733) and/or to criminal prosecution.

Disclosure of Information in Certifications; Acceptance by Producer

The name of the claimant, the total dollar amount claimed by the party on the certification, as well as the total dollar amount that CBP actually disburses to that affected domestic producer as an offset, will be available for disclosure to the public, as specified in 19 CFR 159.63(e). To this extent, the submission of the certification is construed as an understanding and acceptance on the part of the domestic producer that this information will be disclosed to the public and a waiver of any right to privacy or non-disclosure. Additionally, a statement in a certification that this information is proprietary and exempt from disclosure may result in CBP's rejection of the certification.

Distribution Made by Electronic Funds Transfer

Pursuant to 31 U.S.C. 3332 and 31 CFR part 208, as amended by 89 FR 12955 (February 21, 2024), CBP is required to issue all CDSOA offset distributions made after March 22, 2024, by electronic funds transfer, unless a Department of the Treasury waiver applies. Claimants are likewise required by 31 U.S.C. 3332(g) and 31 CFR 208.8 to provide CBP with the information necessary to effect payment by electronic funds transfer. Therefore, an individual who is legally authorized to bind the domestic producer must complete an ACH Refund Enrollment Form designating the bank account and associated routing number for CBP to make payment of any CDSOA offset distribution(s) by electronic funds transfer into the designated bank account. The ACH Refund Enrollment Form must also include the domestic producer's federally assigned taxpayer identification number (with suffix), or employer identification number (with suffix), or social security number; this number is also present on the domestic producer's CDSOA certification(s).

This ACH Refund Enrollment Form is accessible online at

https://www.pay.gov

under the Public Form Name, “CBP ACH Refund Enrollment Form.” Any newly completed ACH Refund Enrollment Form, including any updates to a previously submitted ACH Refund Enrollment Form, must be submitted to CBP electronically at

https://www.pay.gov,

no later than October 1, 2026. This deadline to submit the ACH Refund Enrollment Form does not change or otherwise extend the 60-day deadline to timely submit a certification for each order or finding under which a CDSOA distribution is sought. ACH Refund Enrollment Forms will not be accepted by postal mail or email submission. A claimant who previously submitted an ACH Refund Enrollment Form to CBP in a prior fiscal year is not required to submit a new ACH Refund Enrollment Form if there have been no changes to the information therein (

i.e., when there is no change to the designated bank account and associated routing number for CBP to make payment of any CDSOA offset distribution(s) via electronic funds transfer and no change in the domestic producer's assigned taxpayer identification number, employer identification number, or social security number). Questions related to this ACH Refund Enrollment Form should be submitted by email to

gmb.achrefundsupport@cbp.dhs.gov

or by calling CBP at (317) 298-1200, extension 1178.

There are limited circumstances specified in 31 CFR 208.4 wherein the Department of the Treasury may waive the requirement that payment be made by electronic funds transfer, to permit payment by paper check. For example, 31 CFR 208.4(a)(7) permits waiver when the agency does not expect to make multiple payments to the same recipient within a one-year period on a regular, recurring basis but only if the payments are made to an individual or a small business concern where “small business concern” has the meaning given the term in section 3 of the Small Business Act at 15 U.S.C. 632 and its implementing regulations. Additionally, 31 CFR 208.4(a)(4) permits waiver of the electronic funds transfer requirement when the payment is to a recipient within an area designated by the President or an authorized agency administrator as a disaster area.

CBP's Revenue Modernization Division, Attn: CDSOA Team, must be notified, in writing, if a domestic producer believes one of the waiver criteria applies to it and if the domestic producer seeks payment of its CDSOA distribution by paper check. The domestic producer's written waiver request must include sufficient information to identify the domestic producer, the associated CDSOA certification(s), and the specific waiver provision within 31 CFR 208.4 upon which the domestic producer is relying. The burden is on the domestic producer to demonstrate that its circumstances satisfy the waiver criteria within 31 CFR 208.4.

Notably, some waiver provisions require the domestic producer to submit a written waiver request to the Department of the Treasury. For example, a domestic producer who is an individual with a qualifying hardship due to a mental impairment (31 CFR 208.4(a)(1)(iv)) or an individual living in a remote geographic location lacking the infrastructure to support electronic financial transactions (31 CFR 208.4(a)(1)(v)) must submit a written waiver request to the Department of the Treasury using the procedure set forth in 31 CFR 208.4(b). Additional information is available from the Department of the Treasury's Electronic Payment Solution Center at 1-877-874-6347 for domestic producers who are individuals seeking a waiver under 31 CFR 208.4(a)(1)(iv) or 31 CFR 208.4(a)(1)(v).

If an electronic funds transfer waiver request is rejected and/or if a domestic producer does not provide CBP with the information necessary to effect payment by electronic funds transfer, then the Department of the Treasury may disburse the domestic producer's CDSOA distribution to a Treasury-sponsored account or to an account to which the domestic producer is receiving other Federal payments as set forth in 31 CFR 208.8.

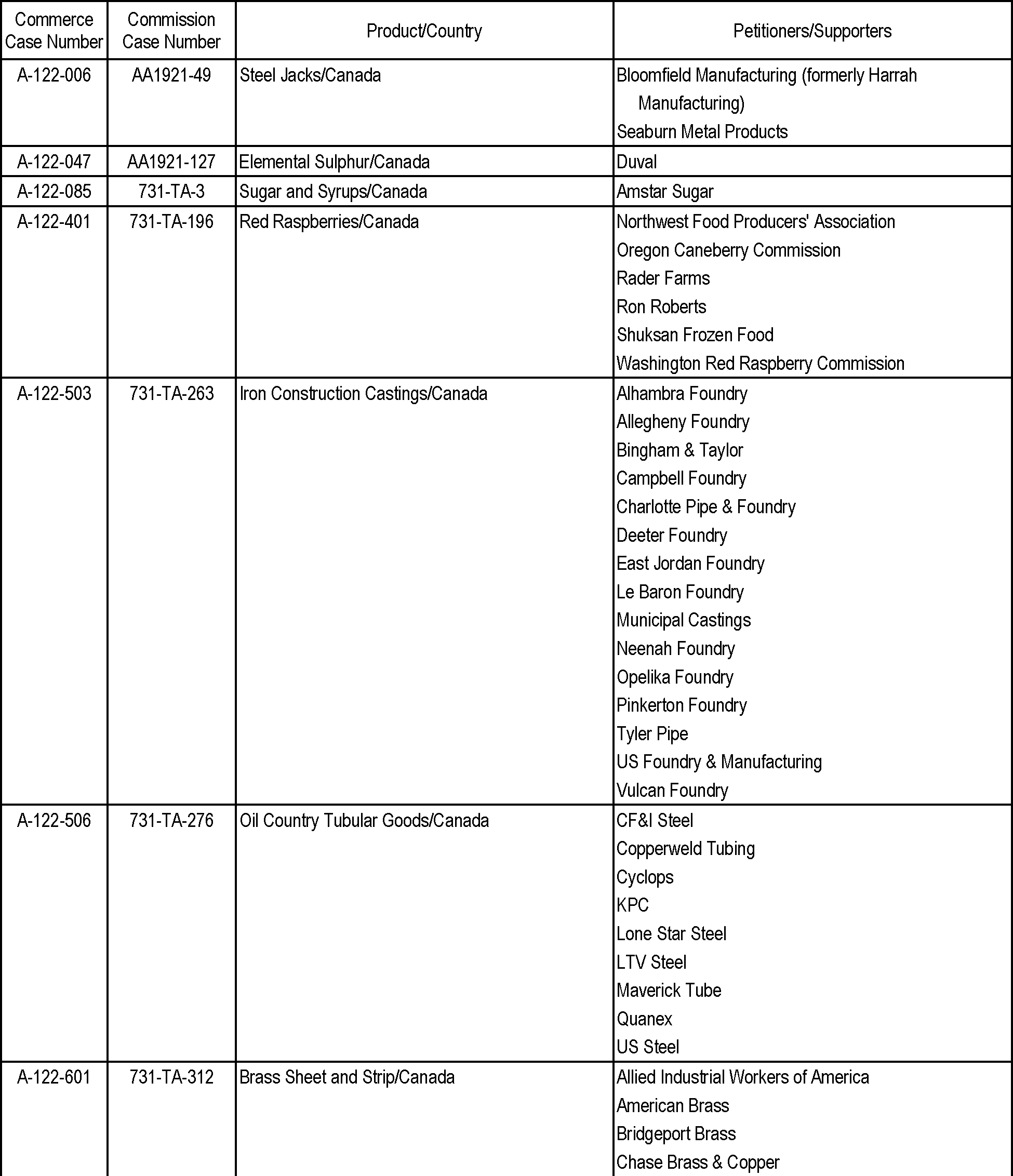

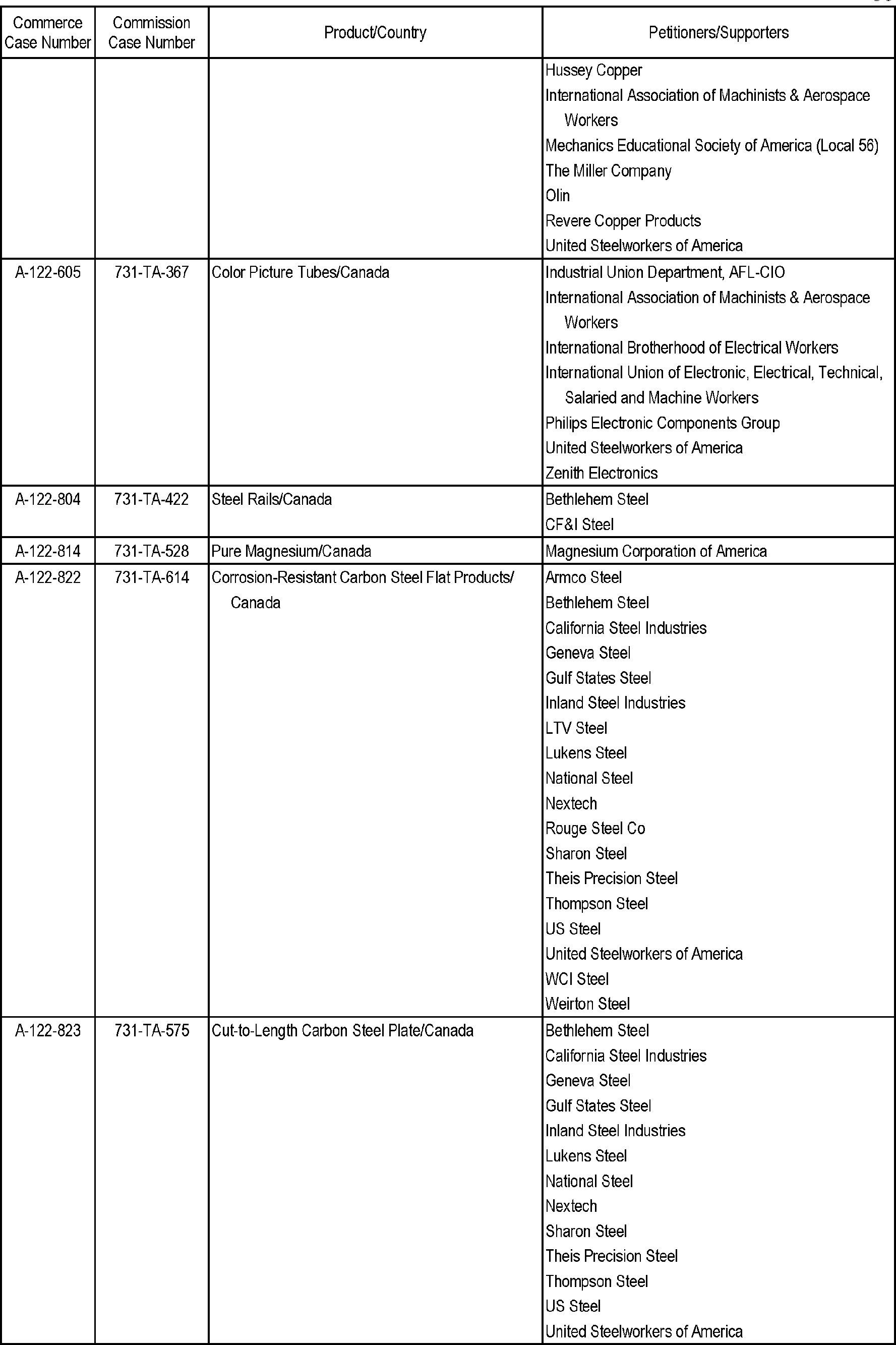

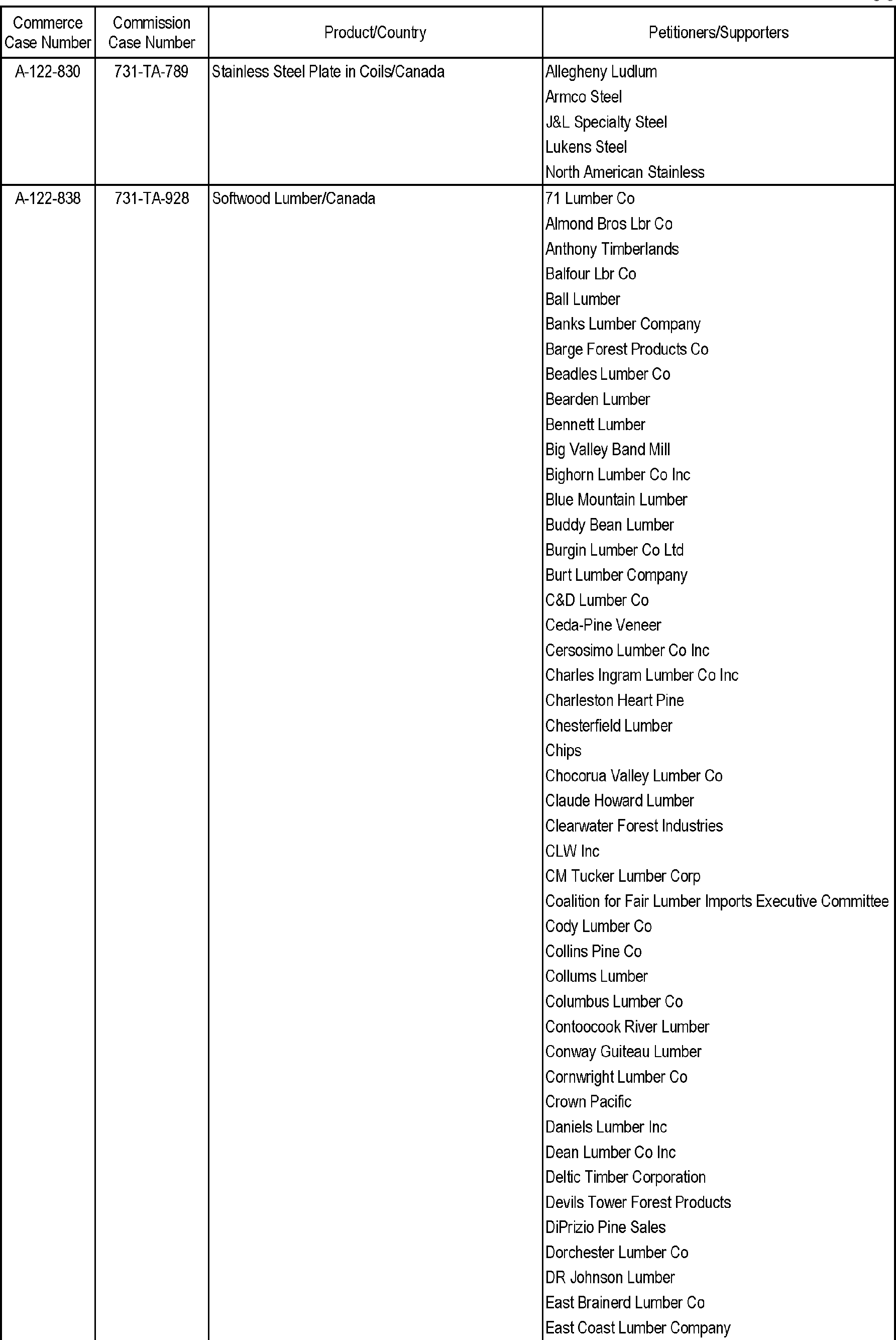

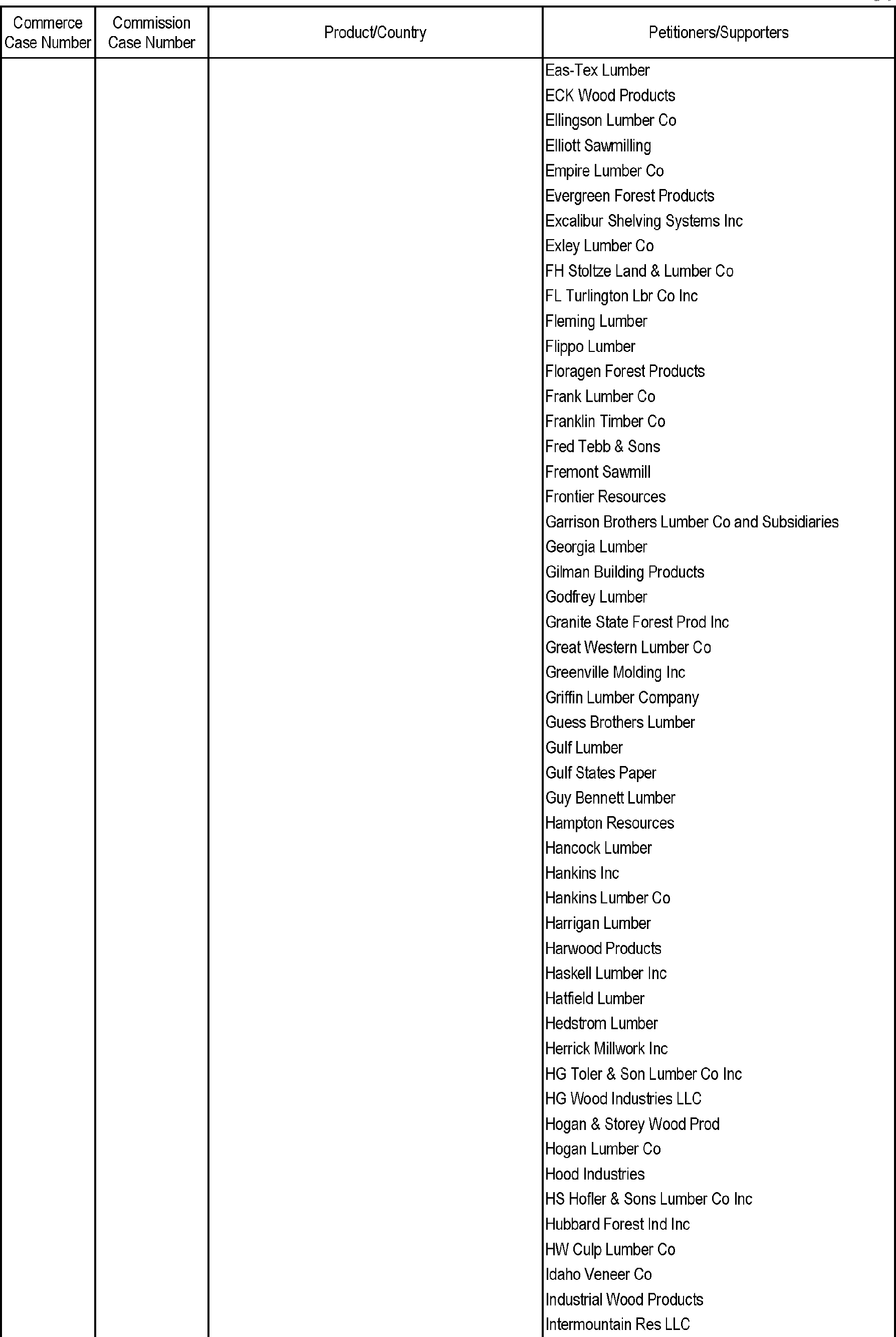

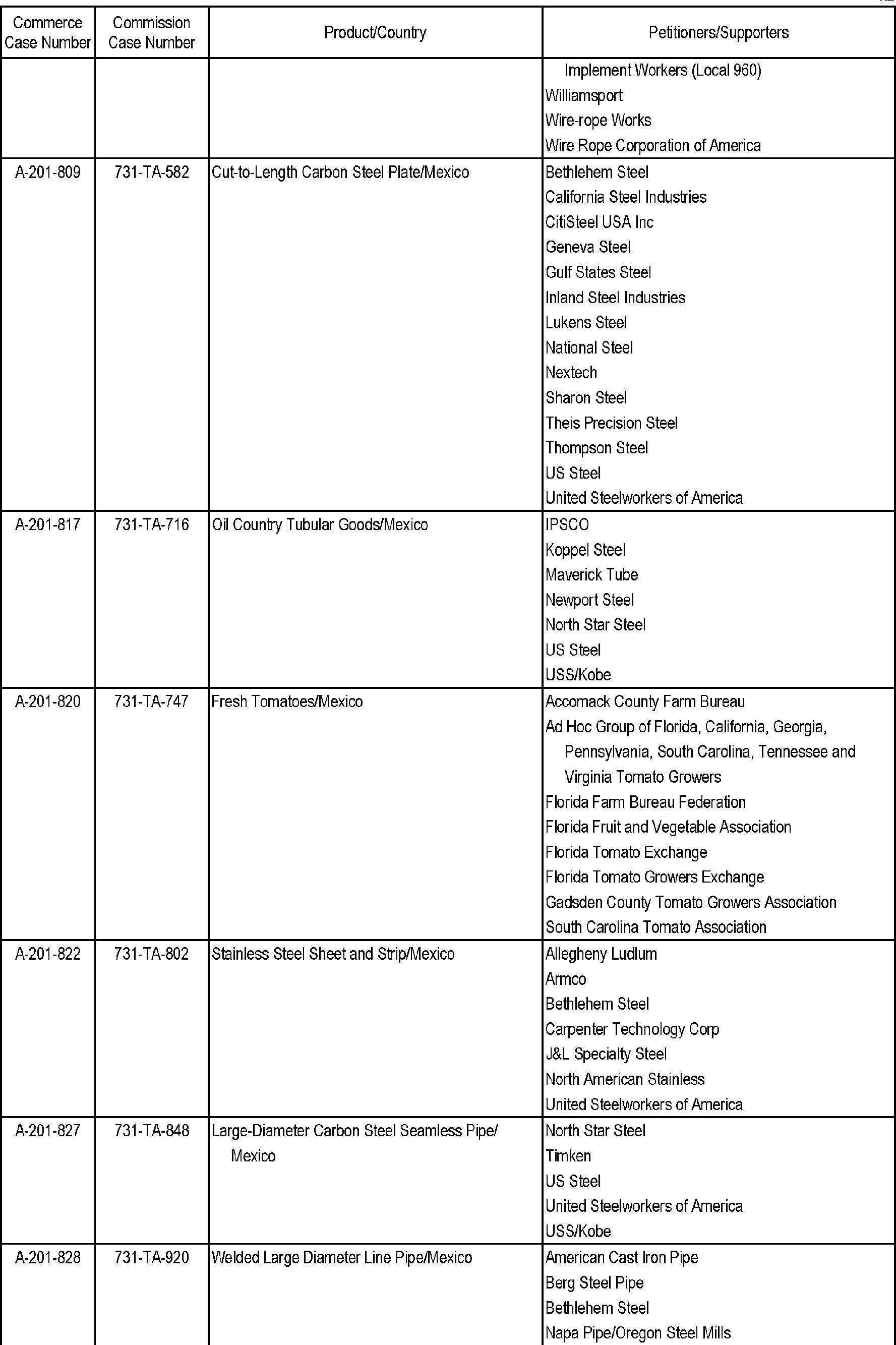

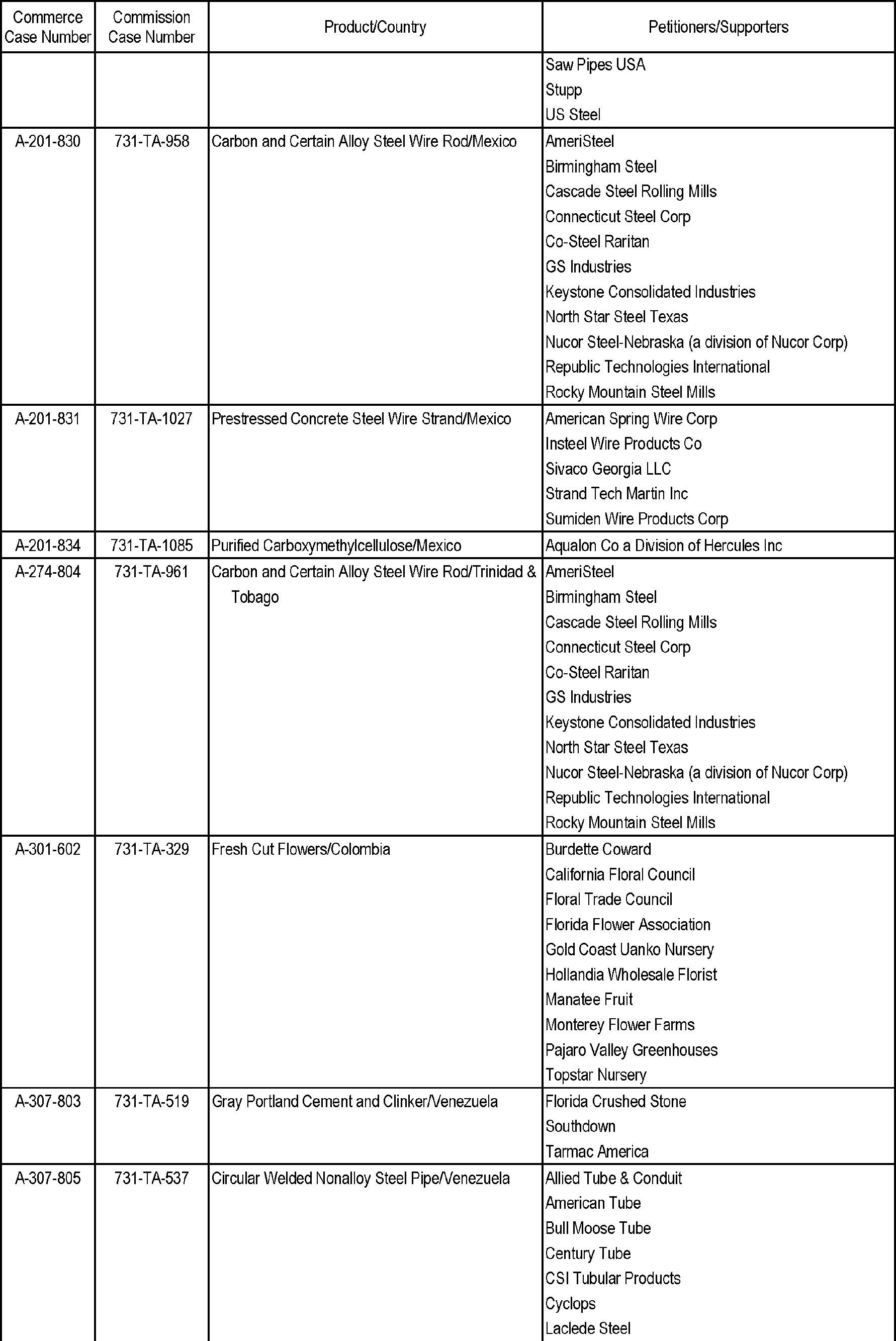

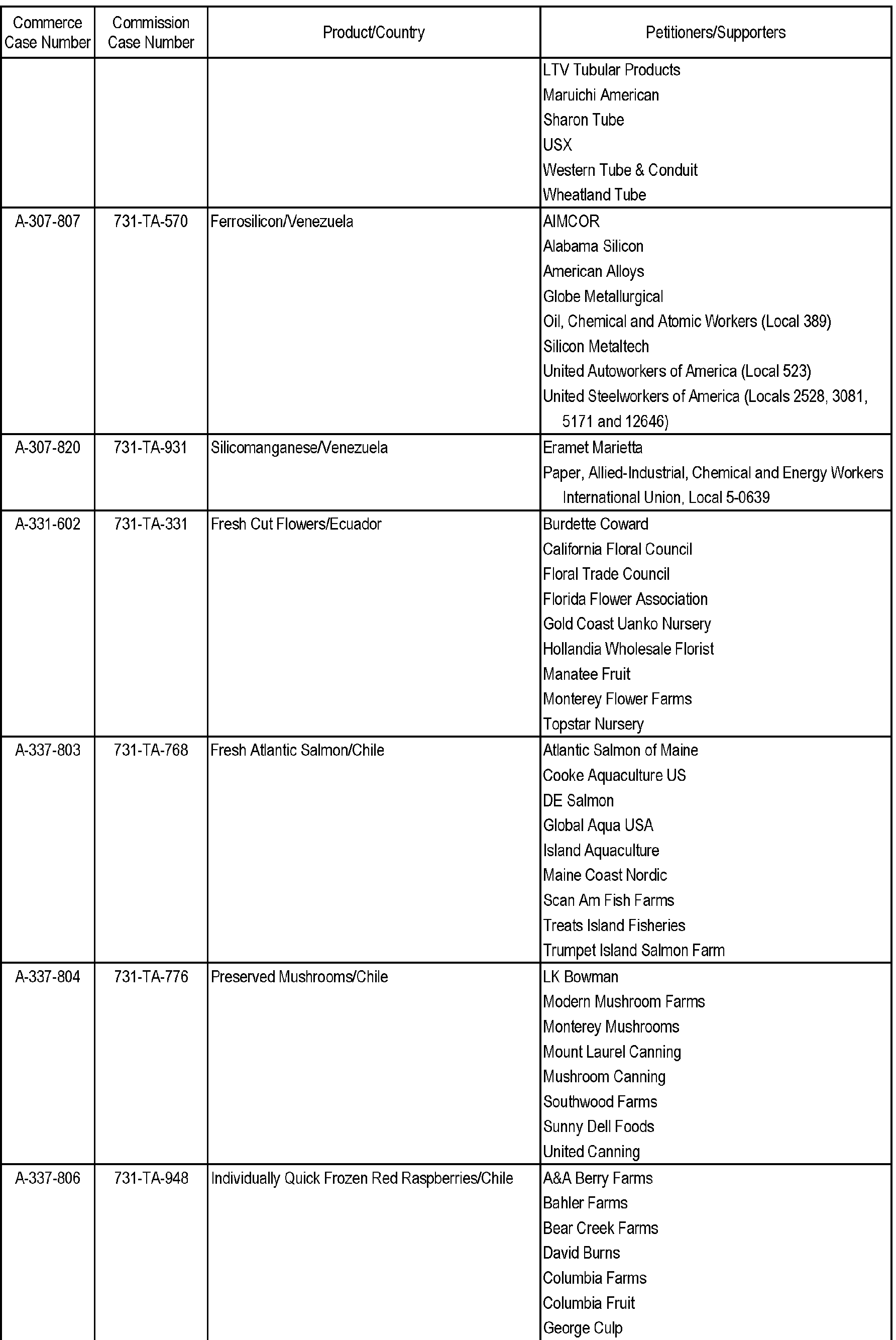

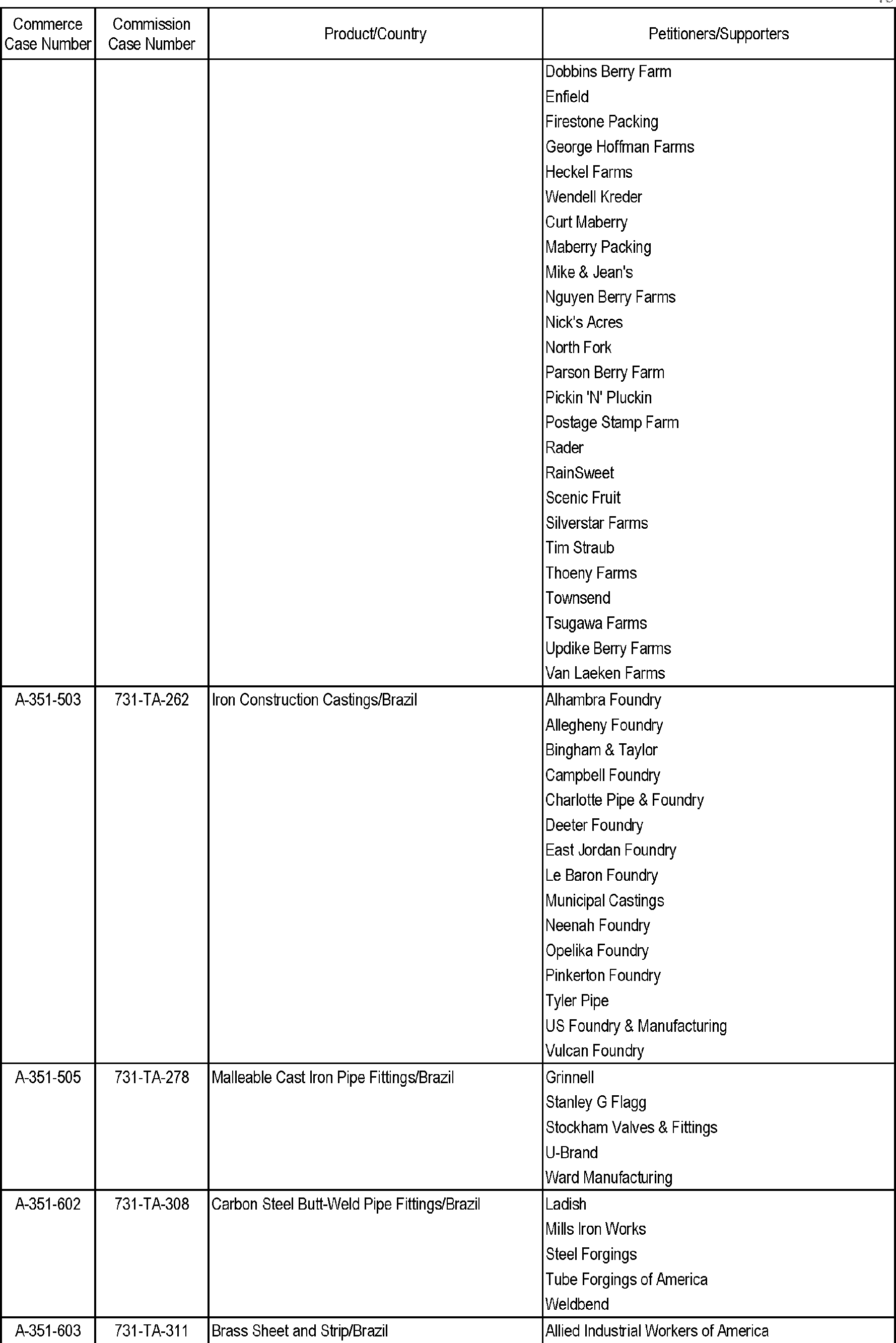

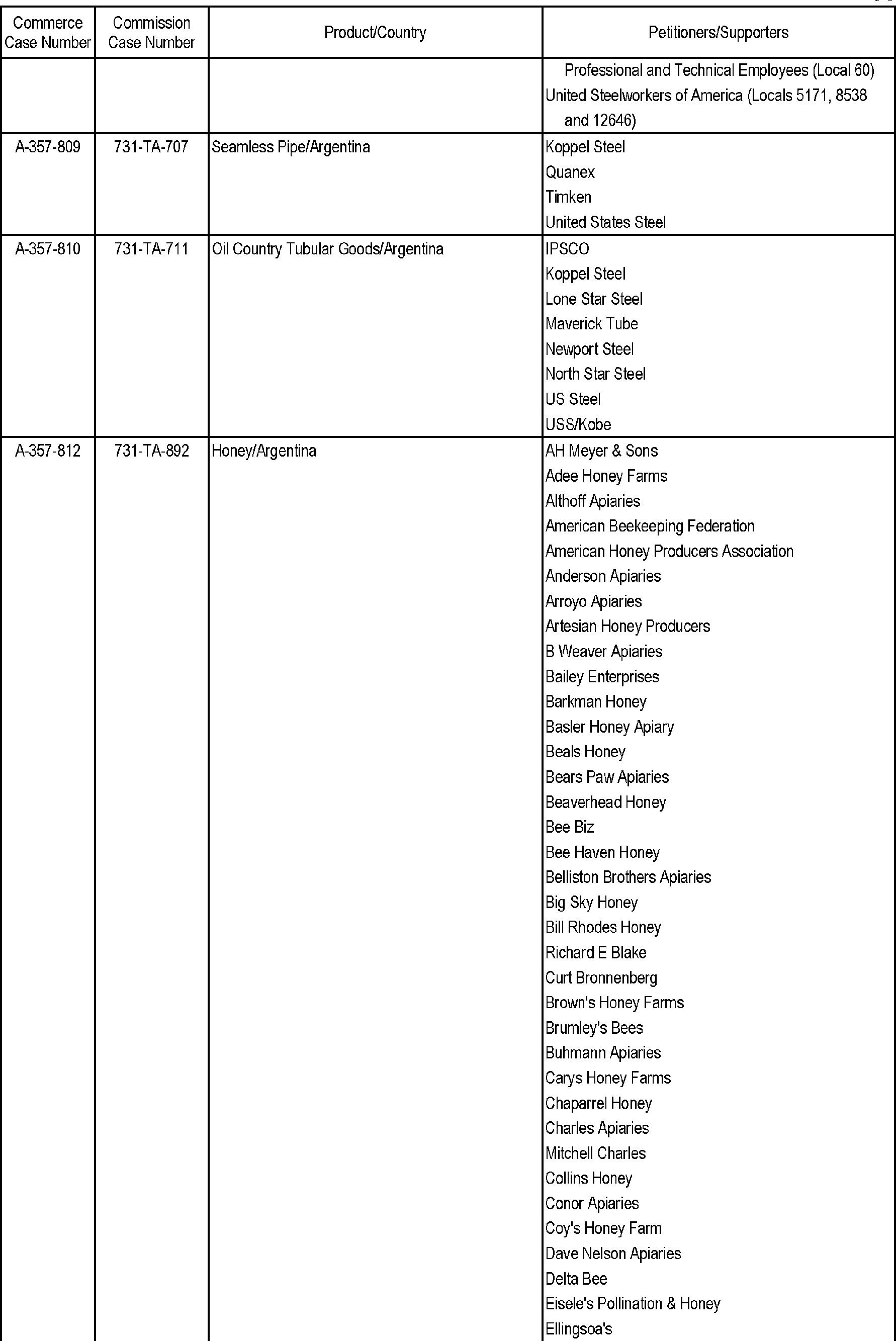

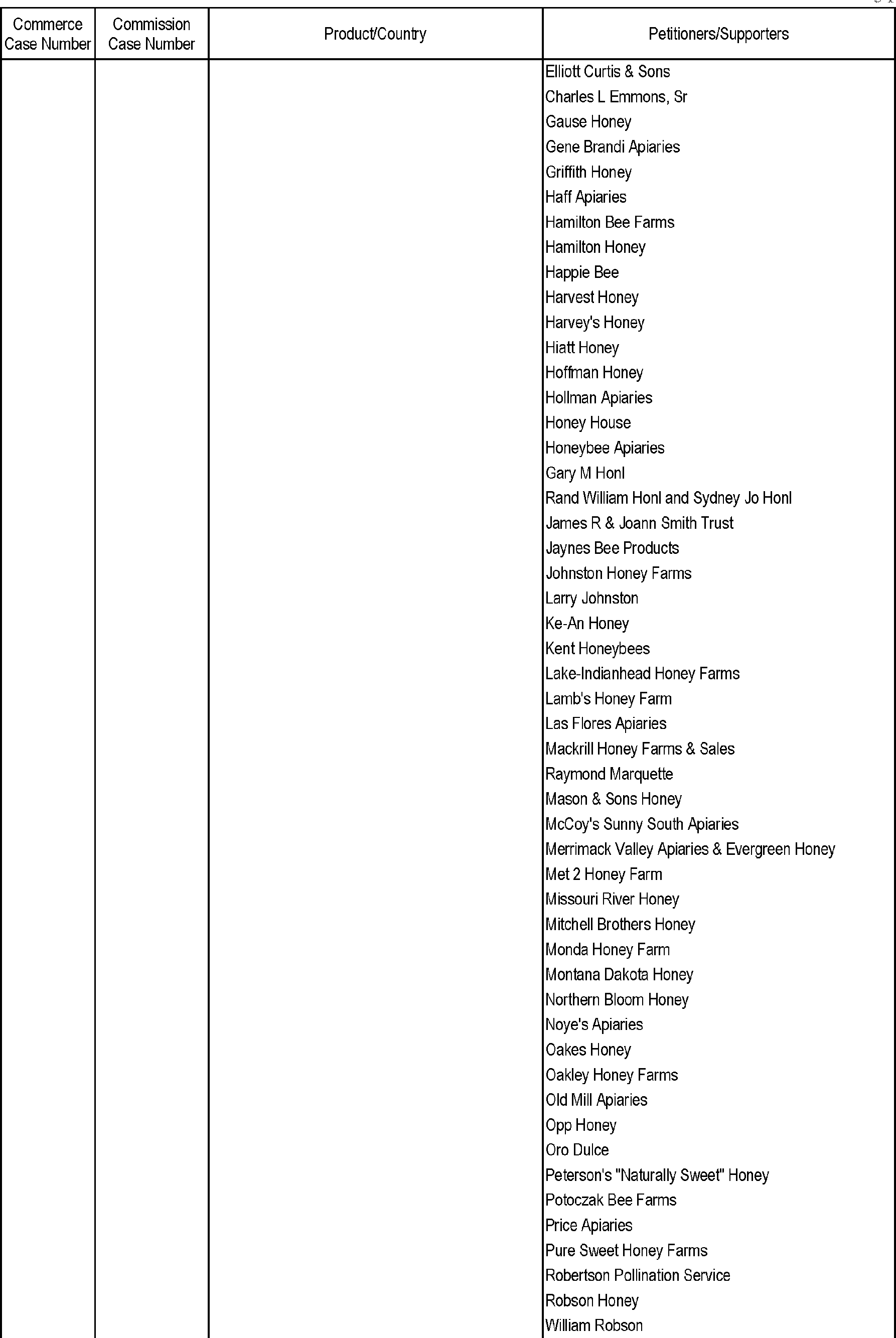

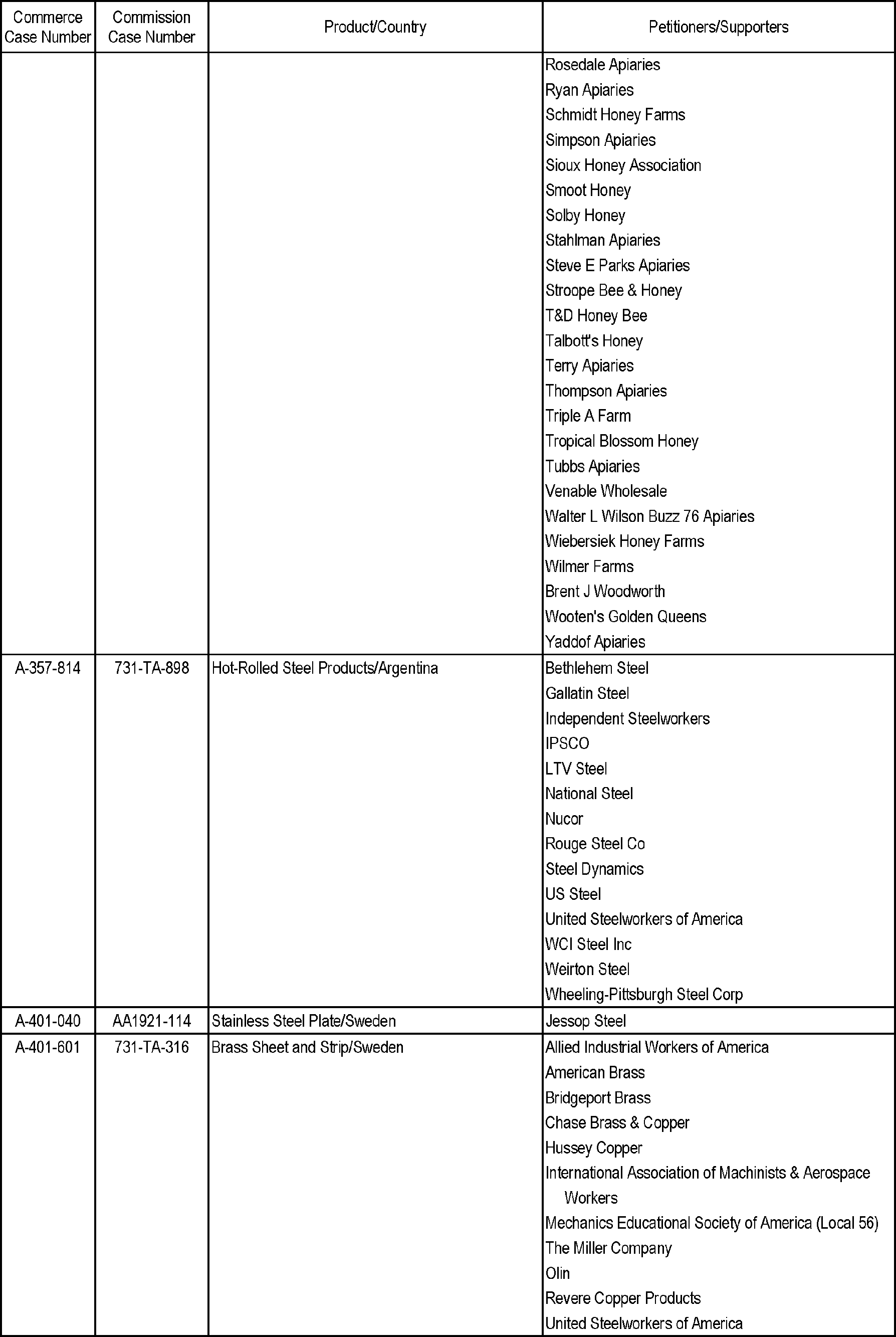

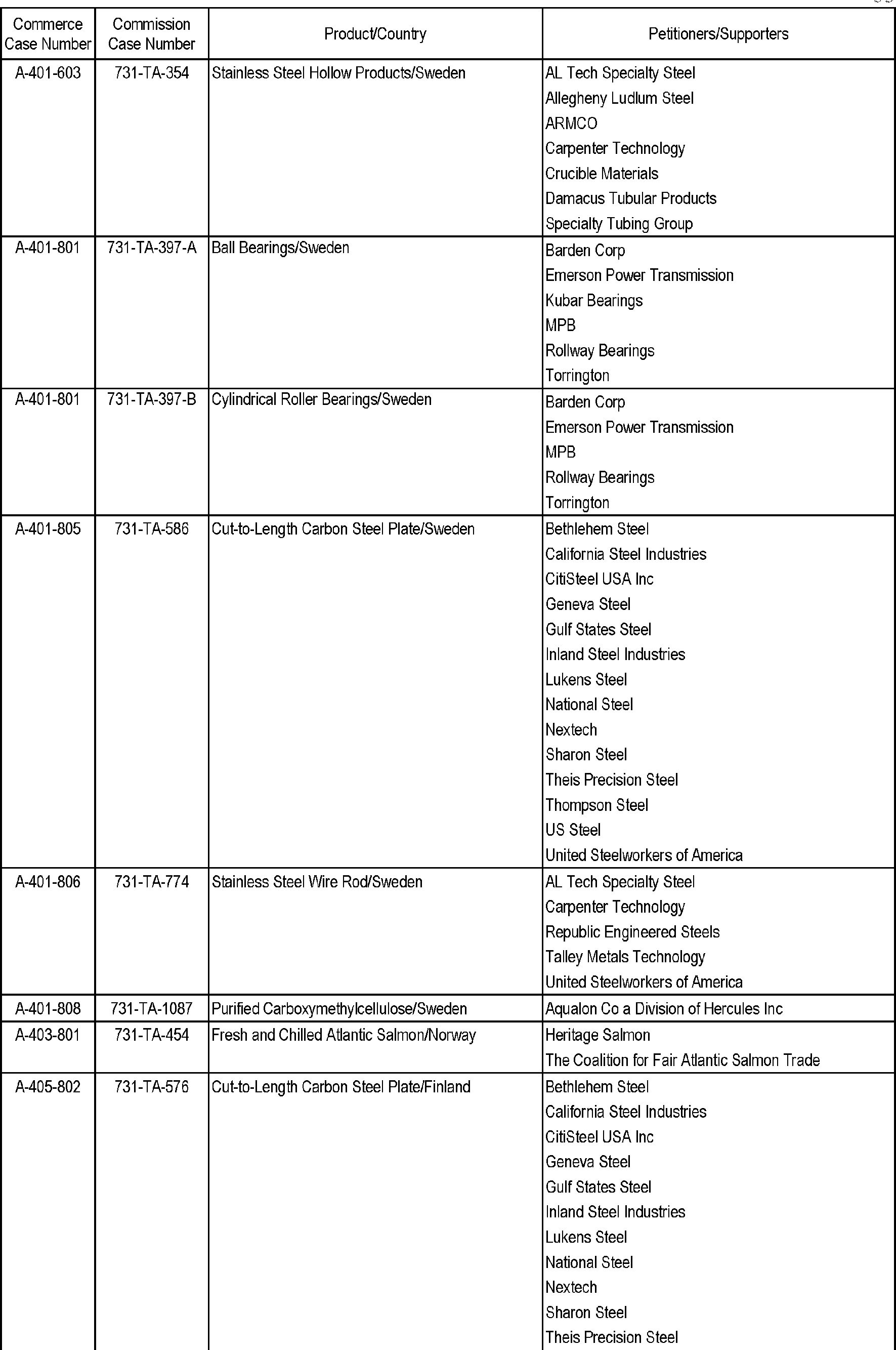

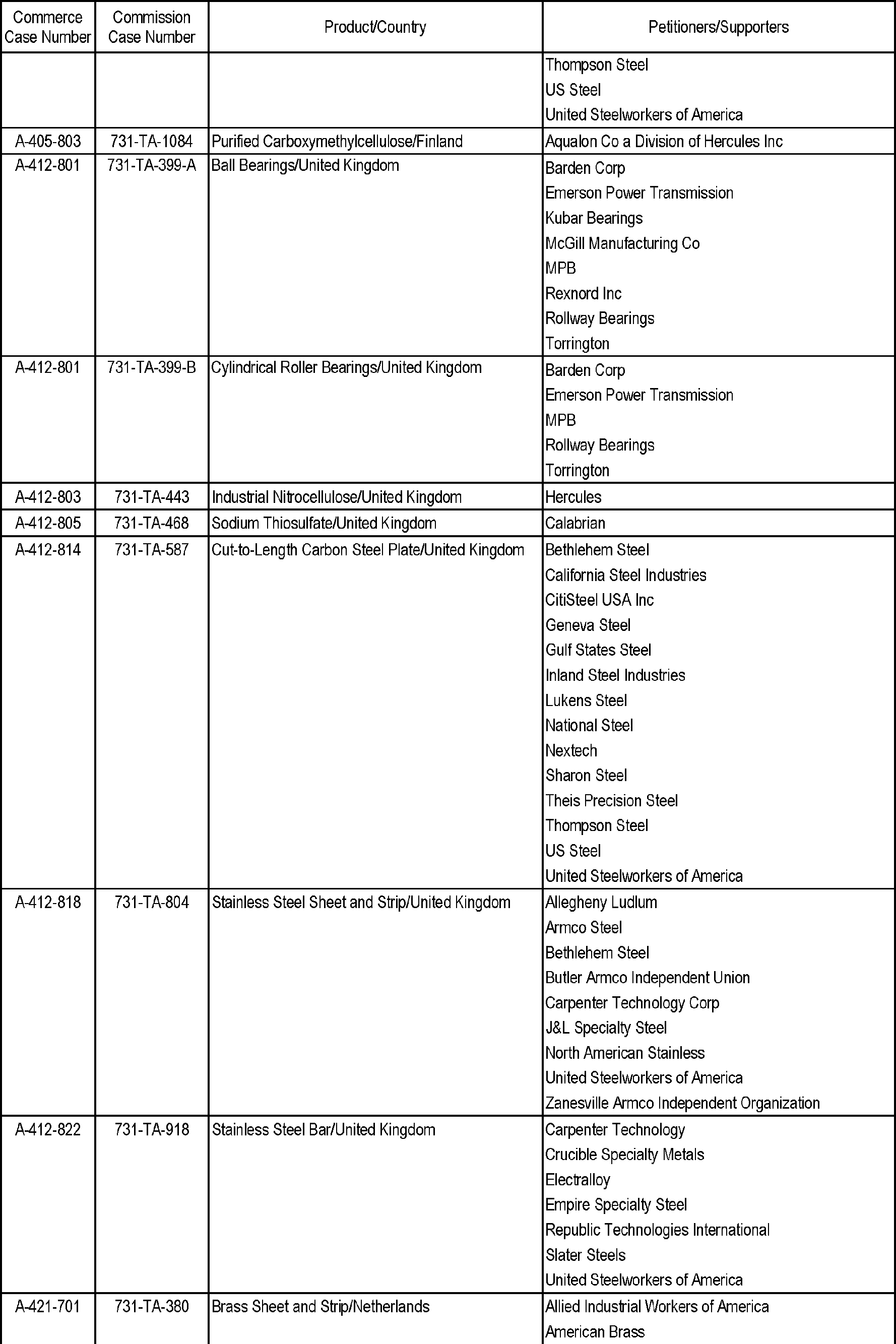

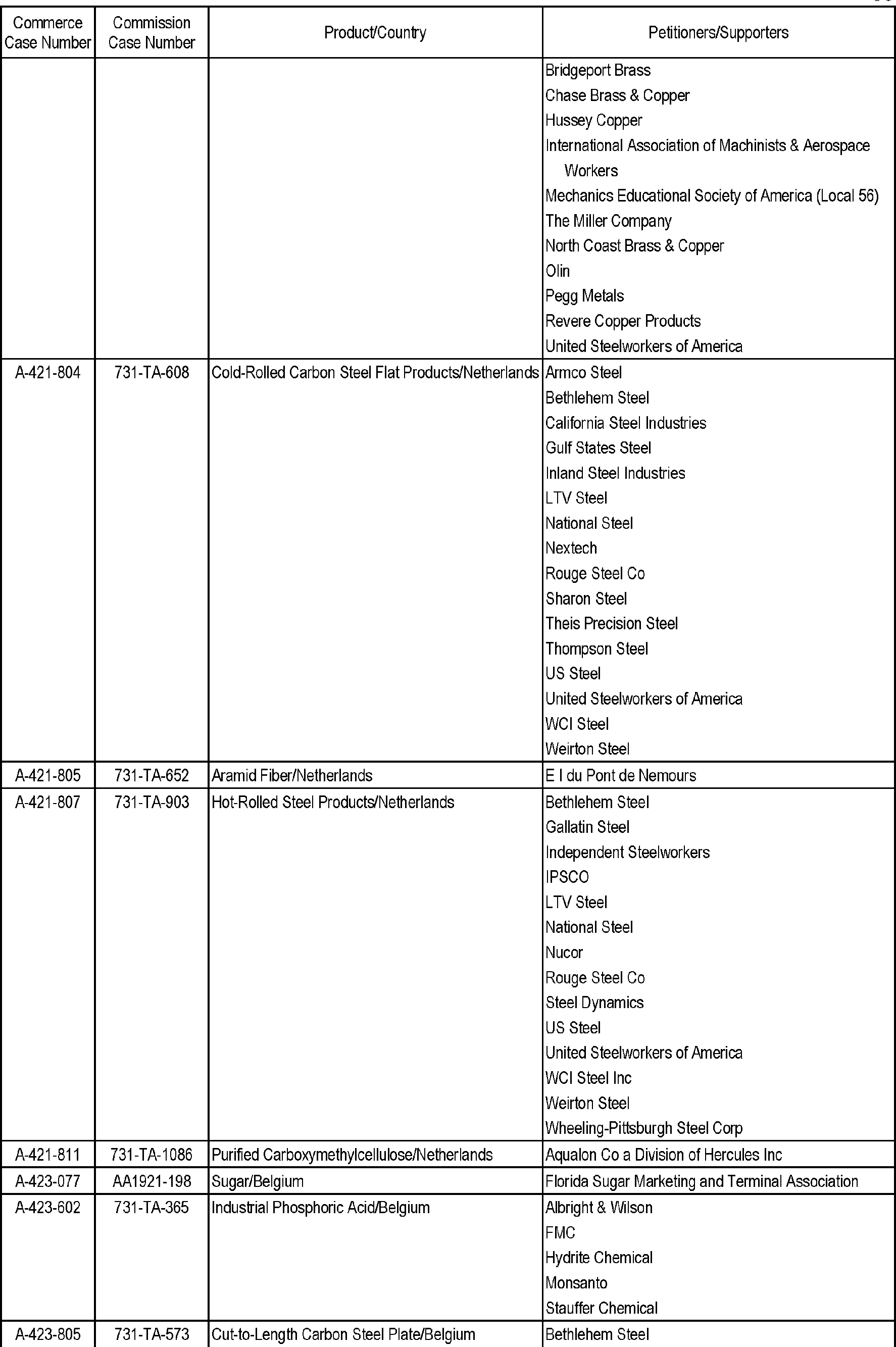

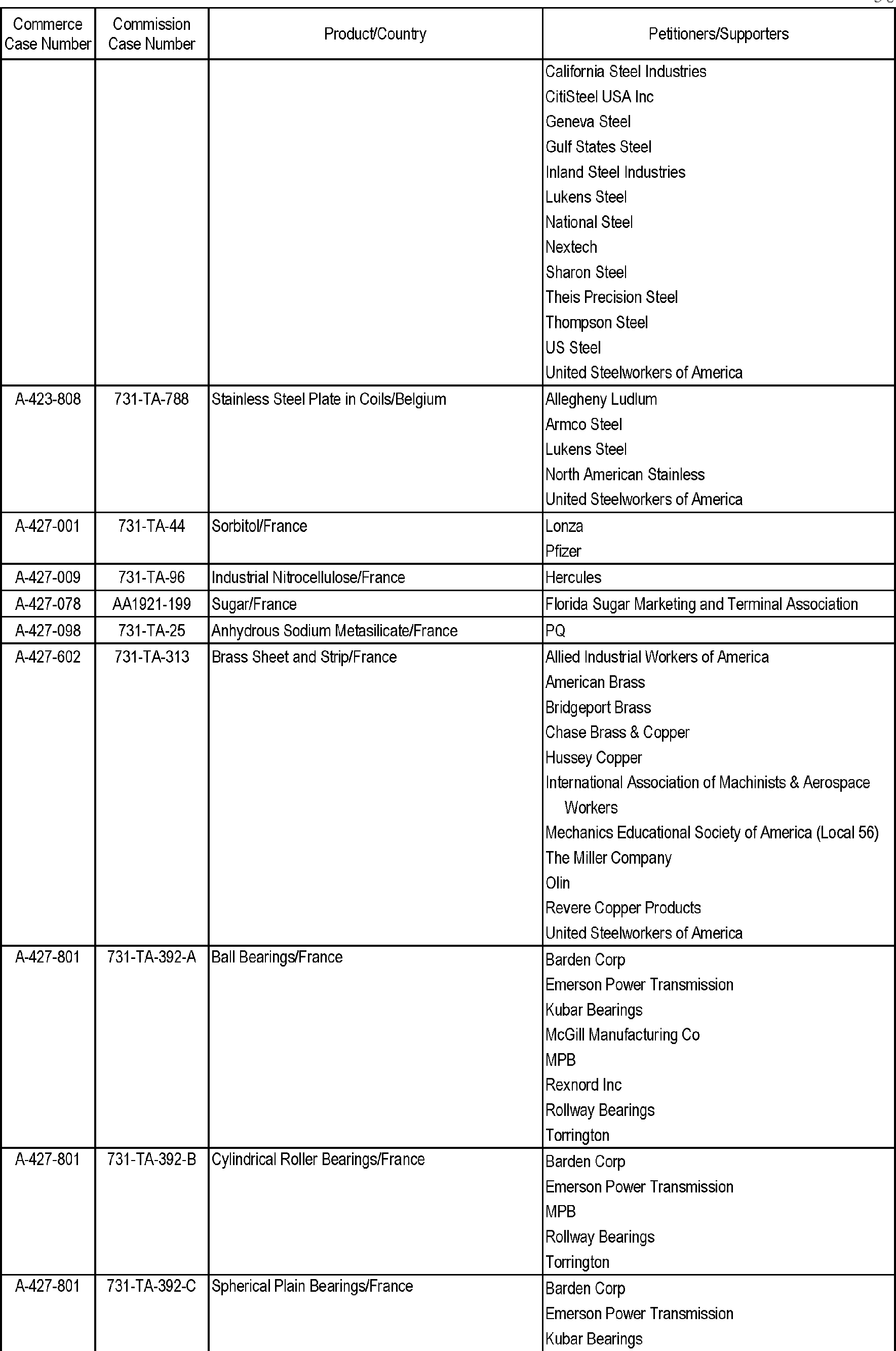

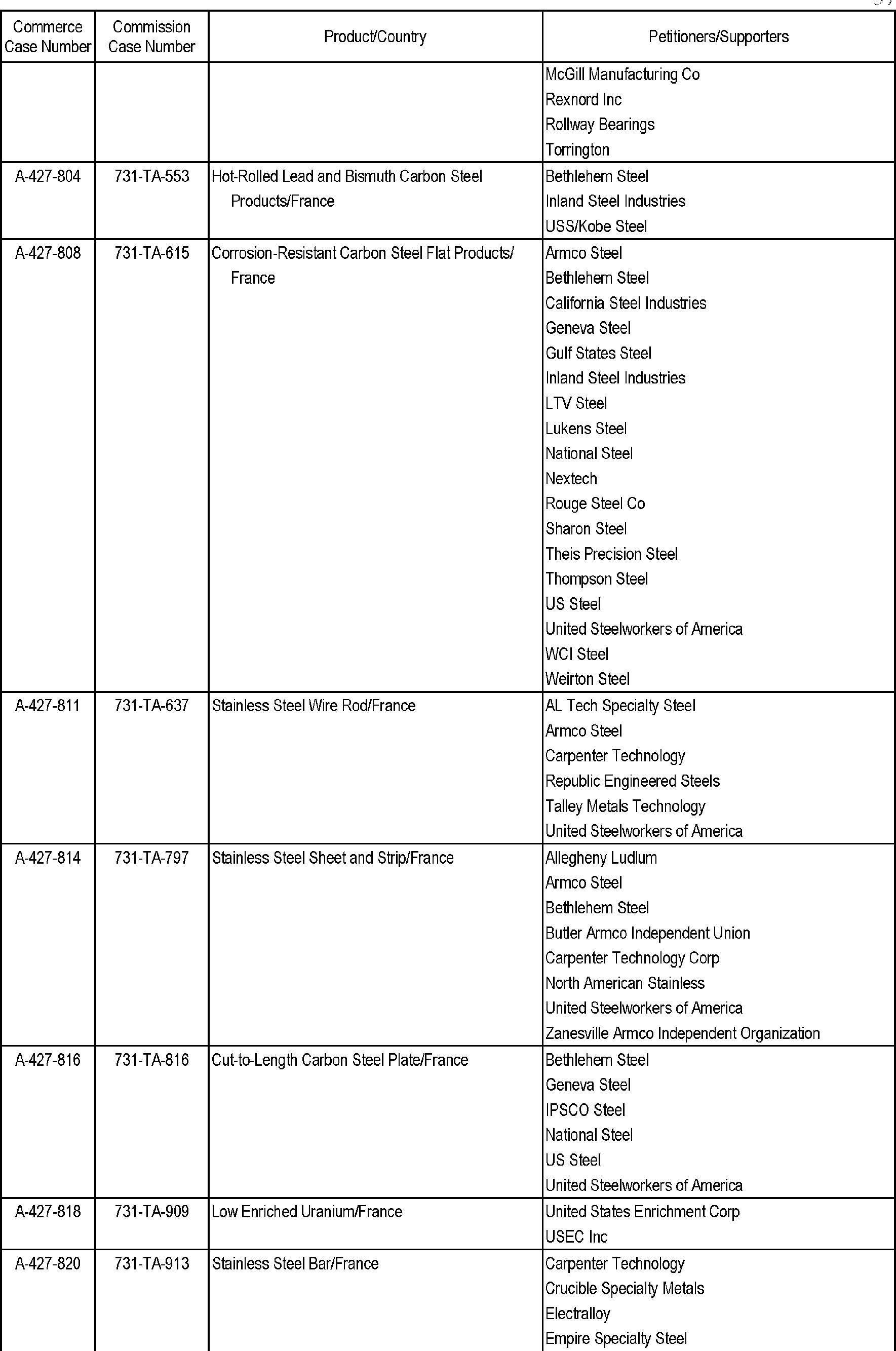

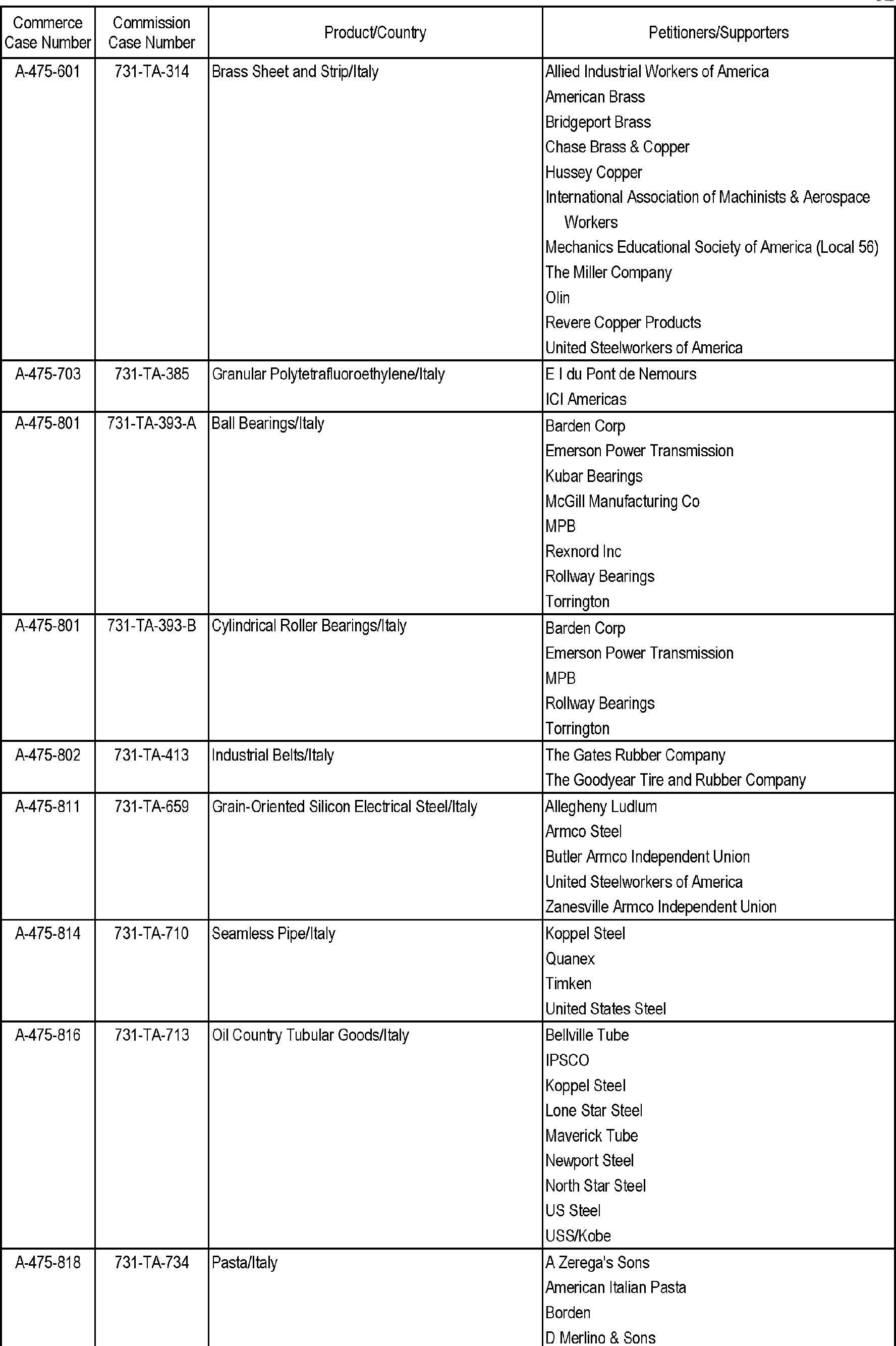

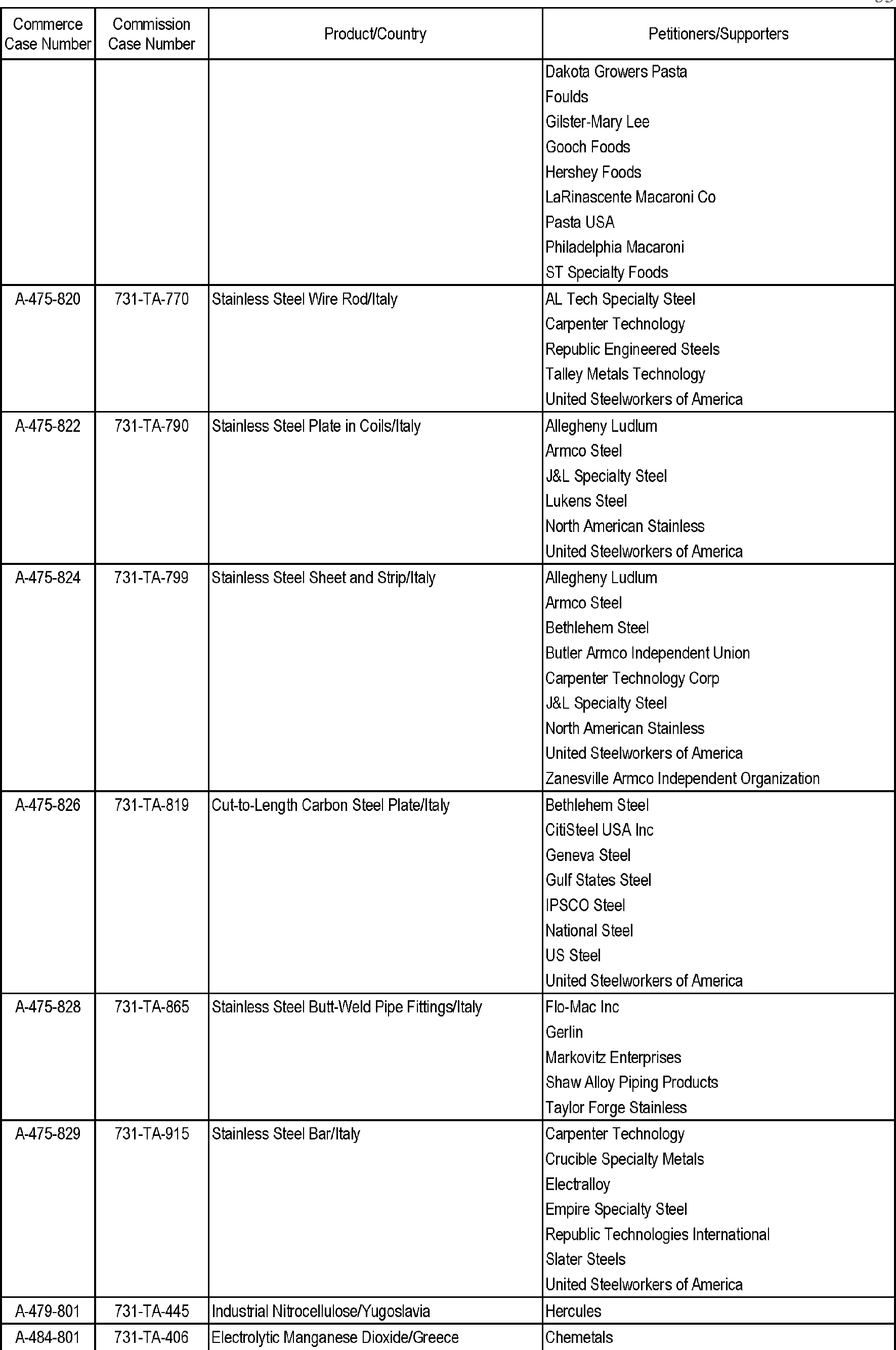

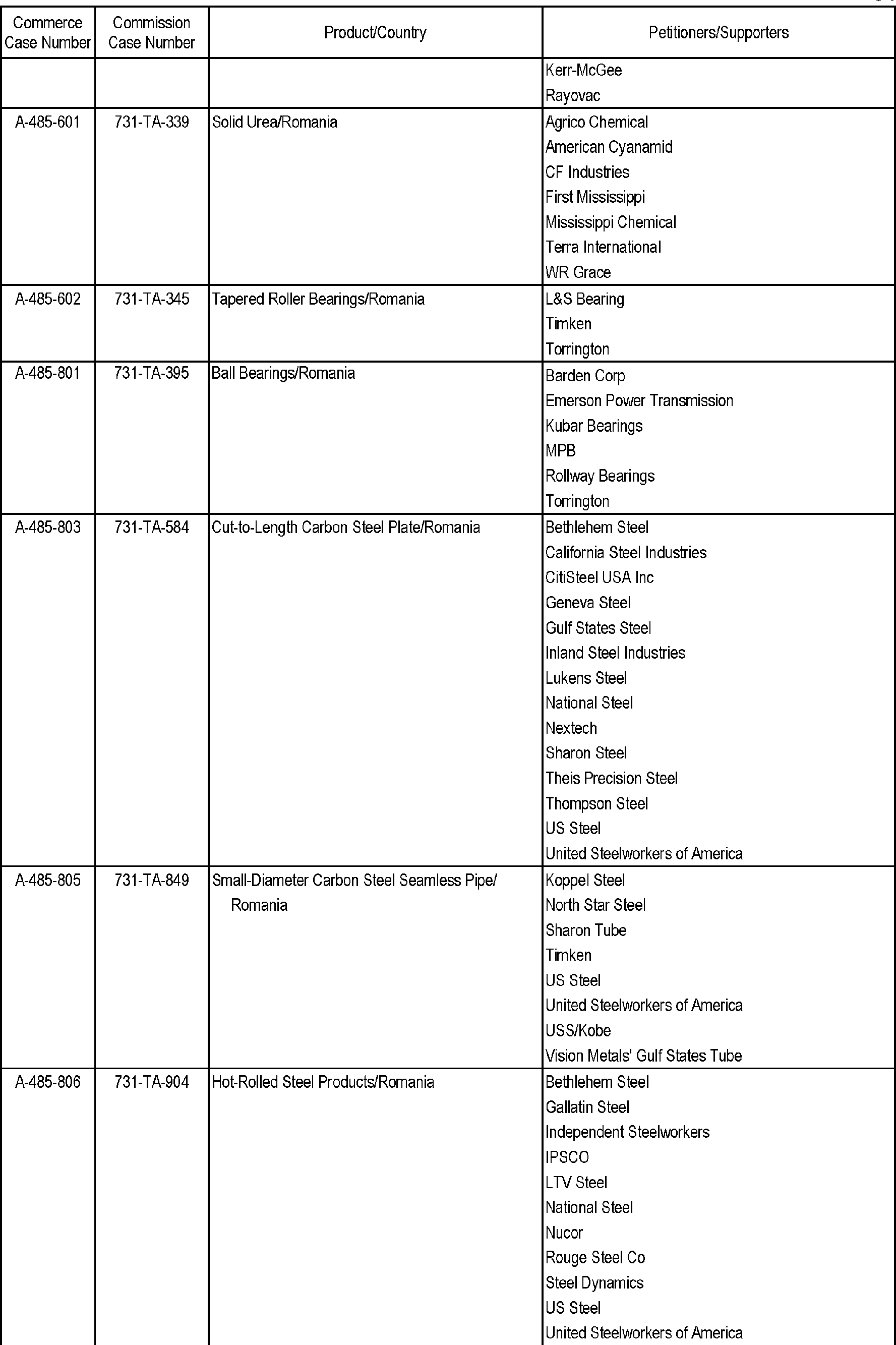

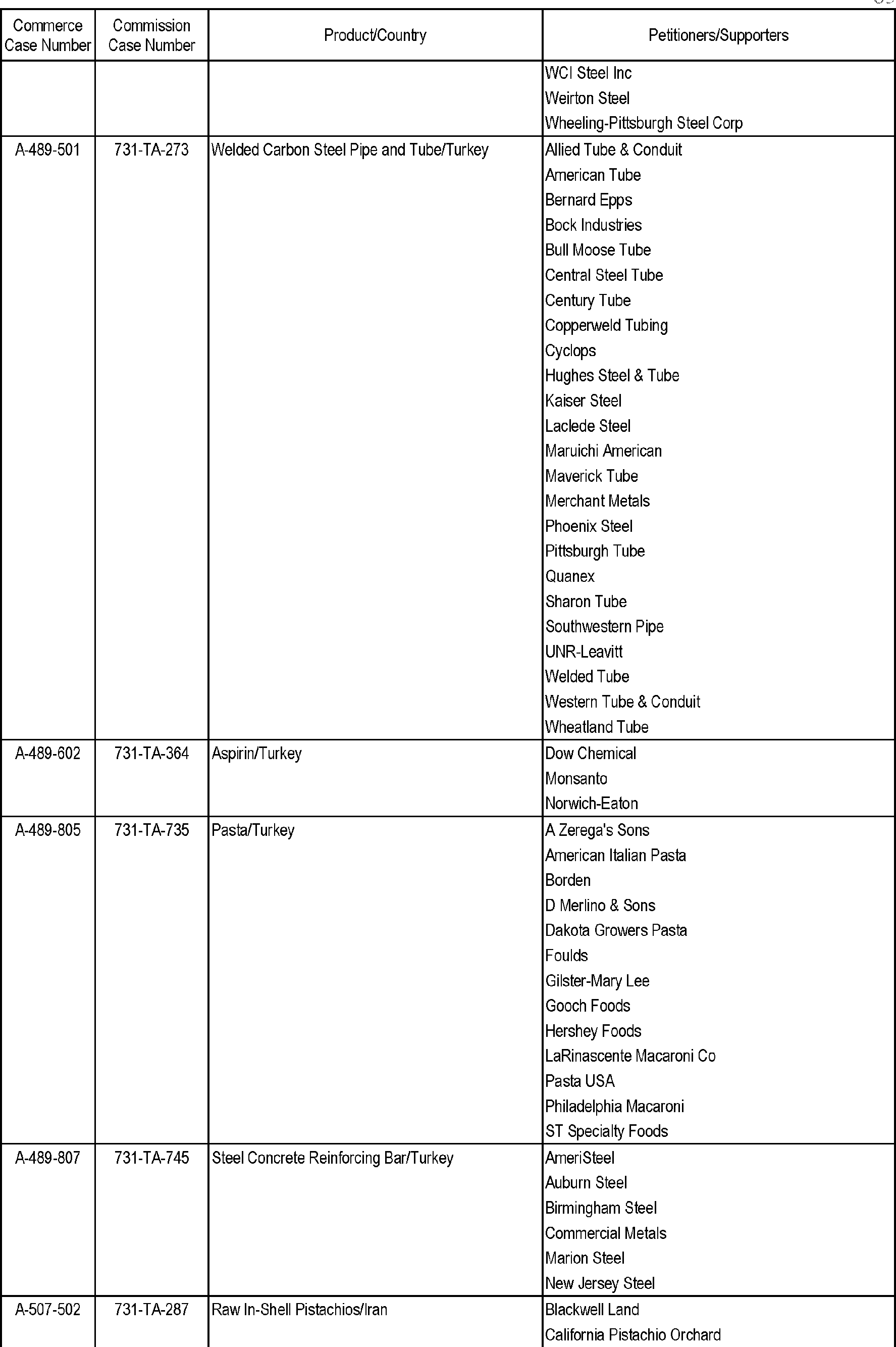

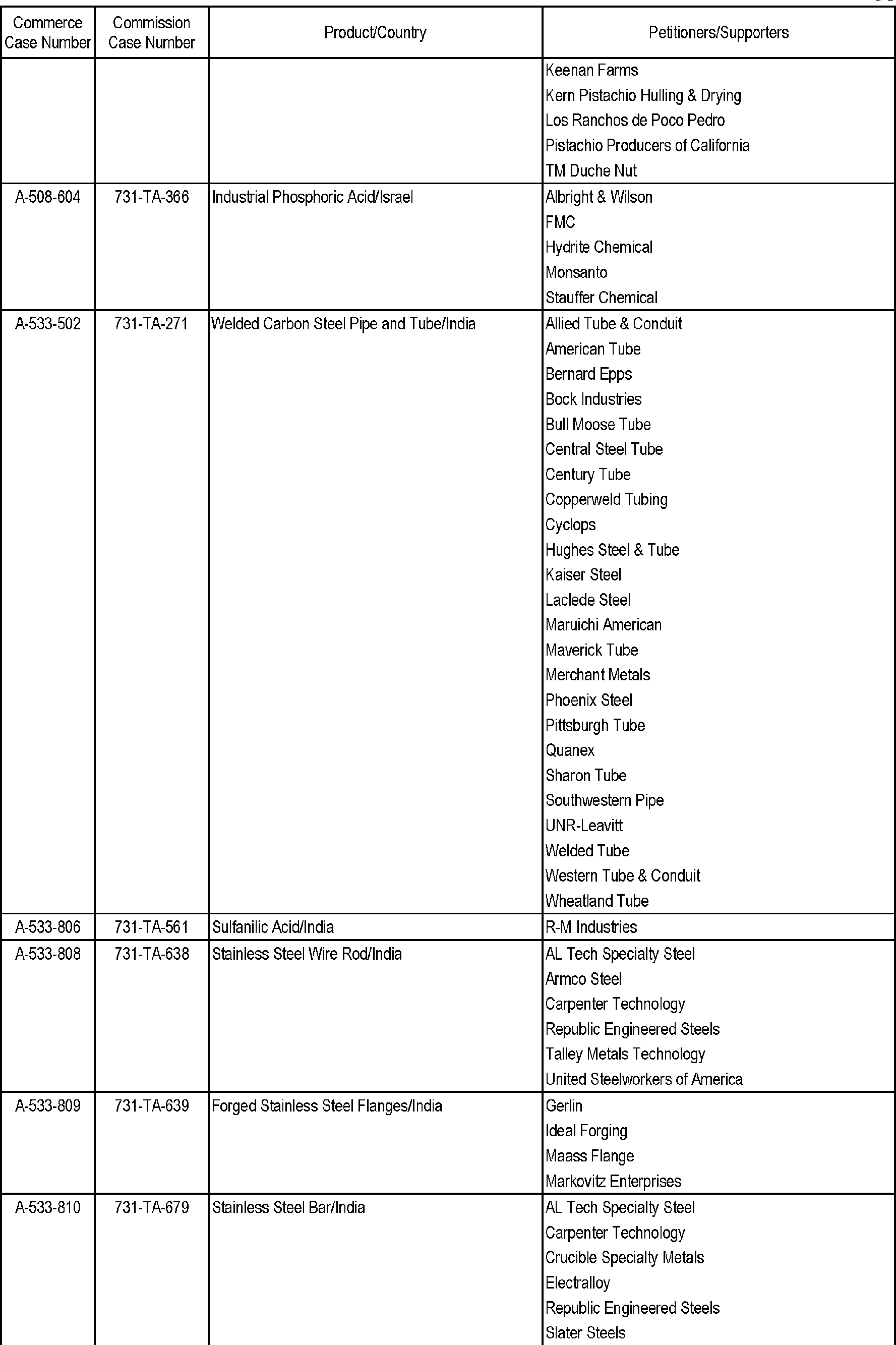

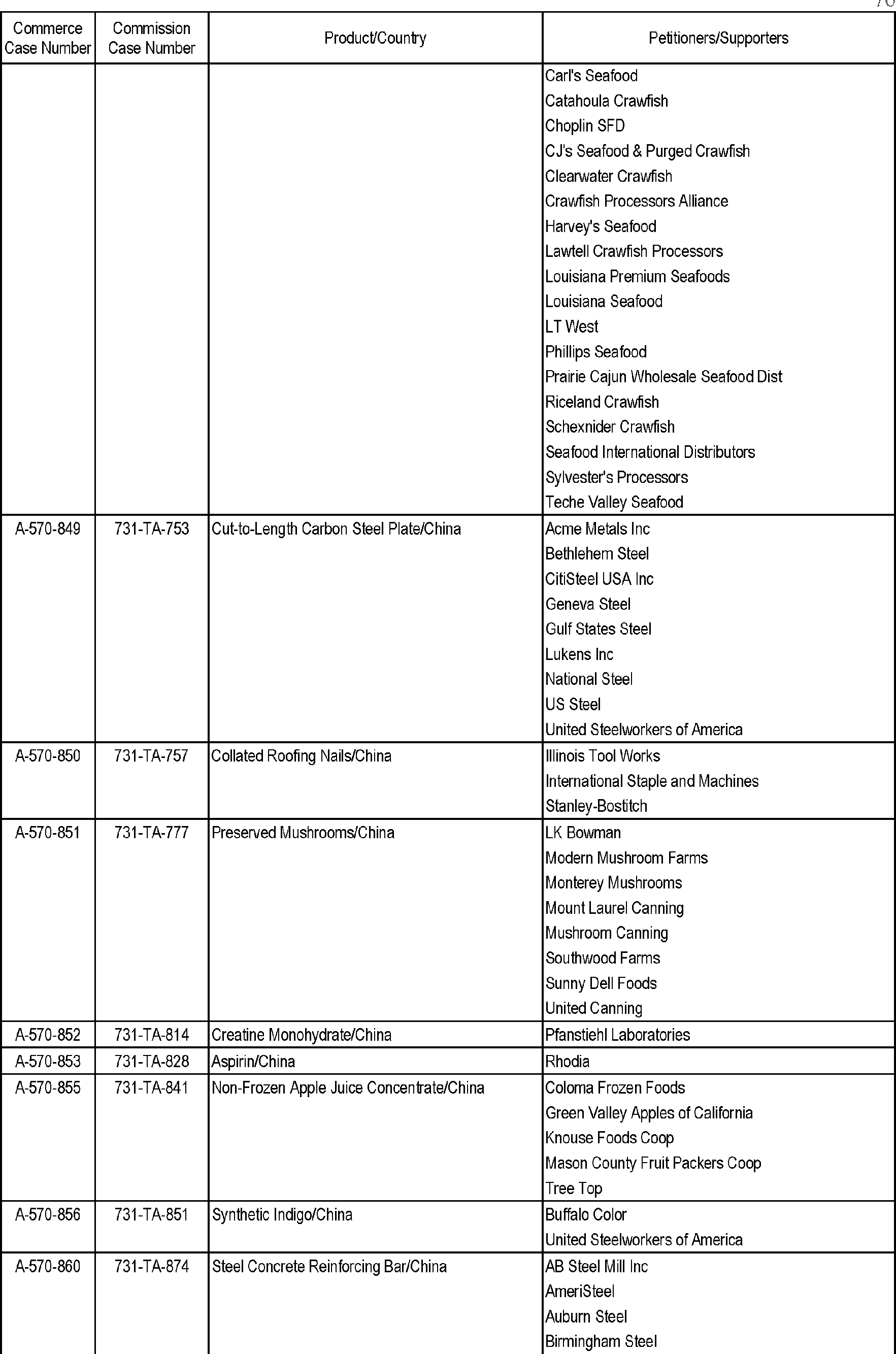

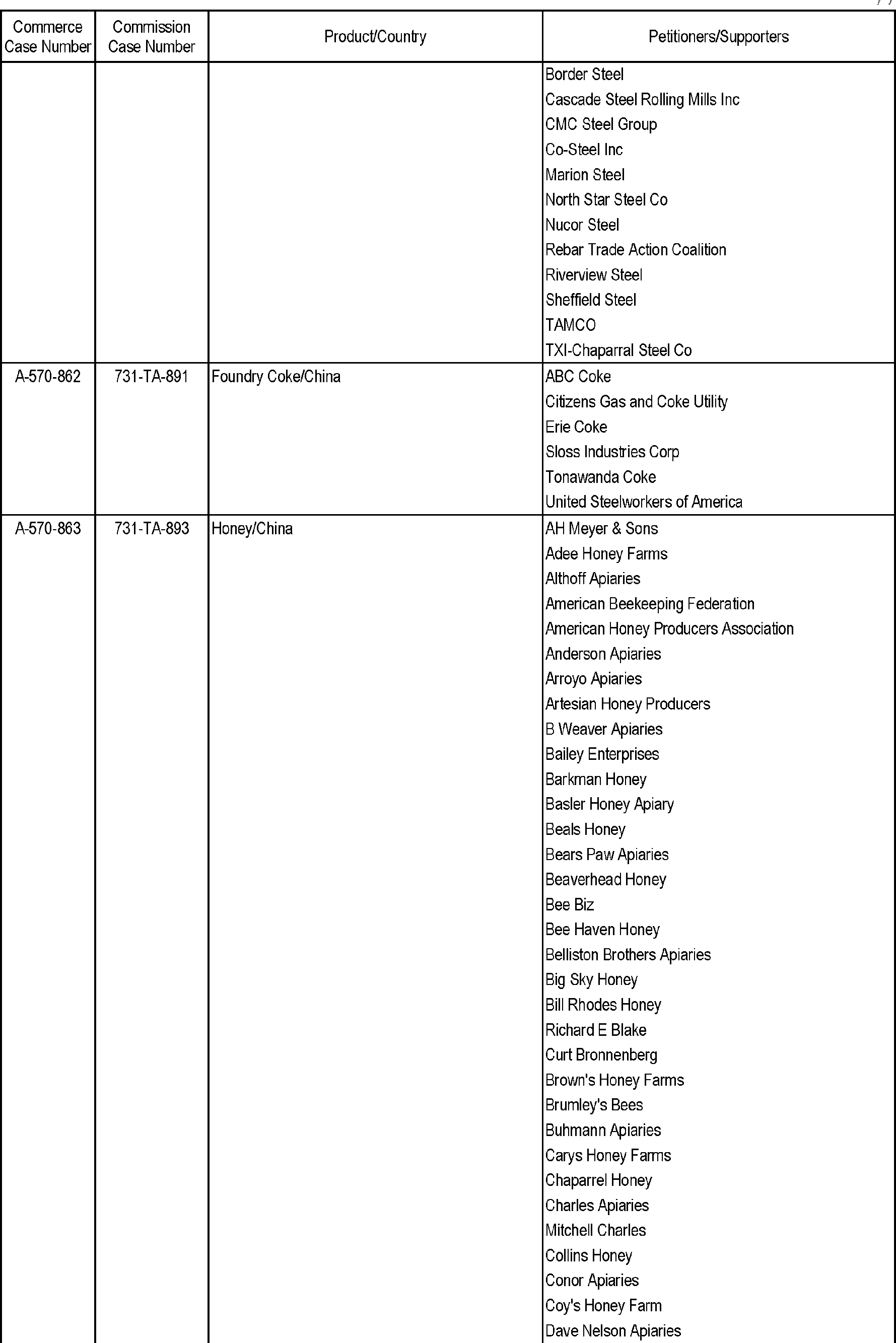

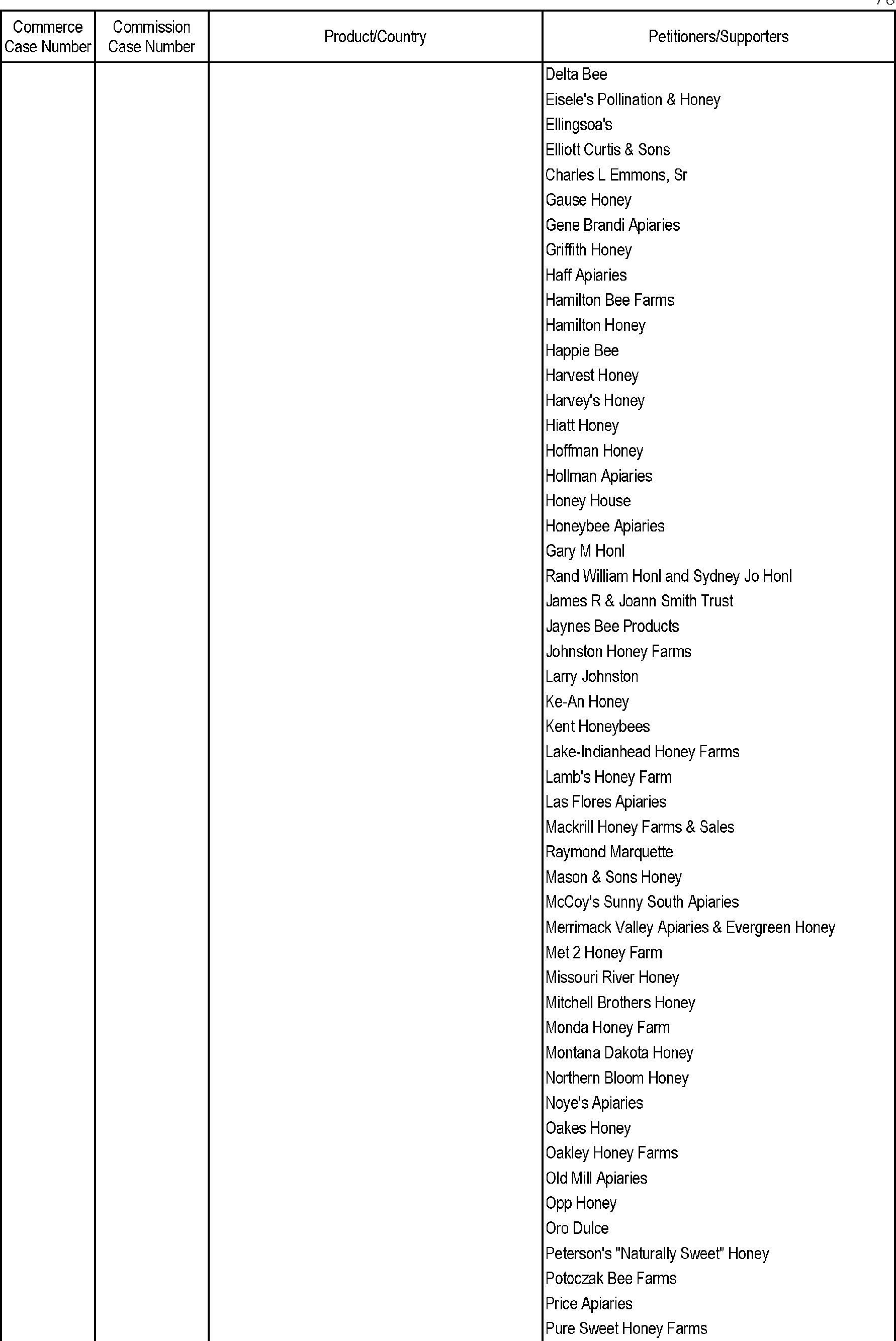

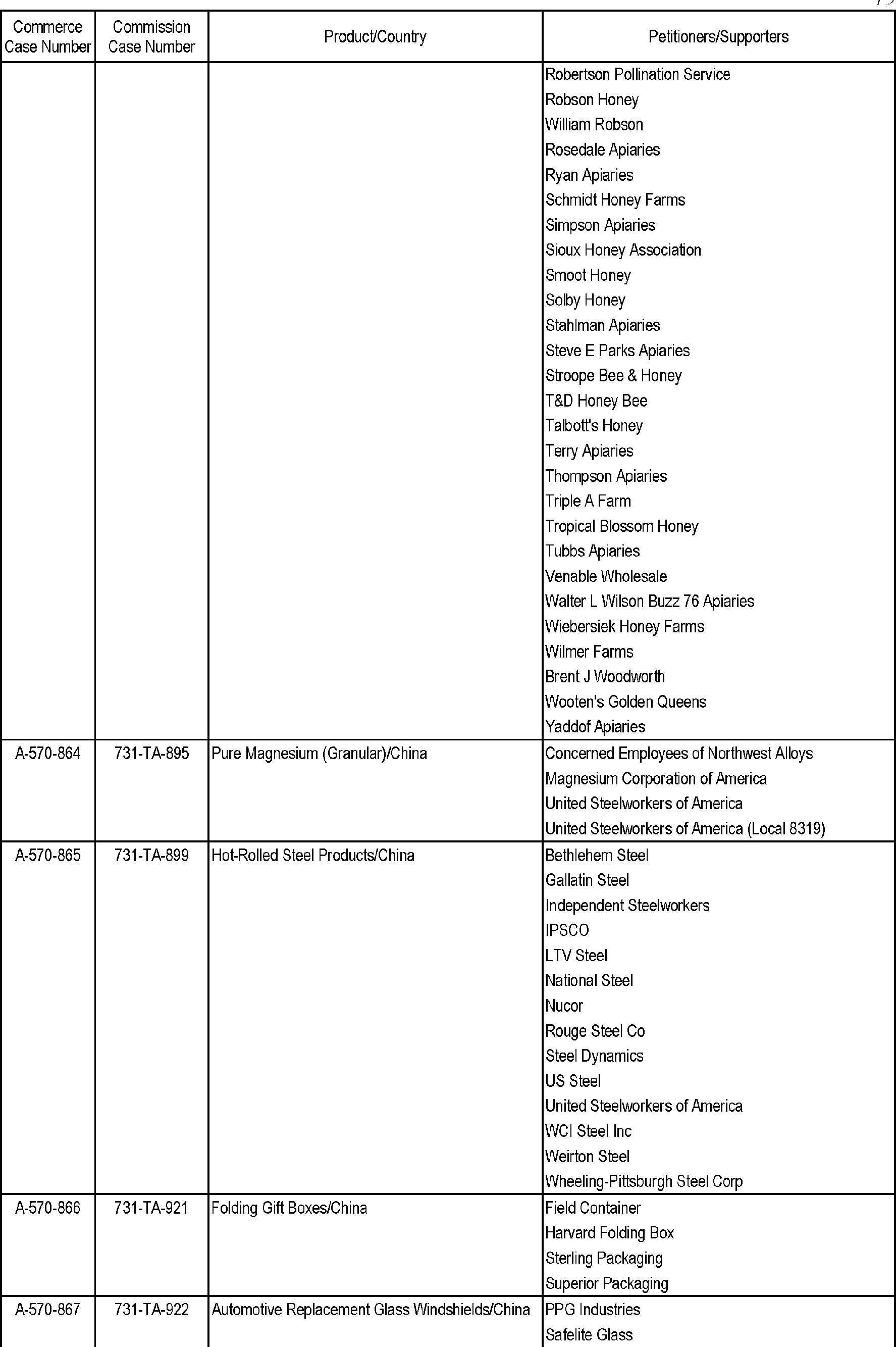

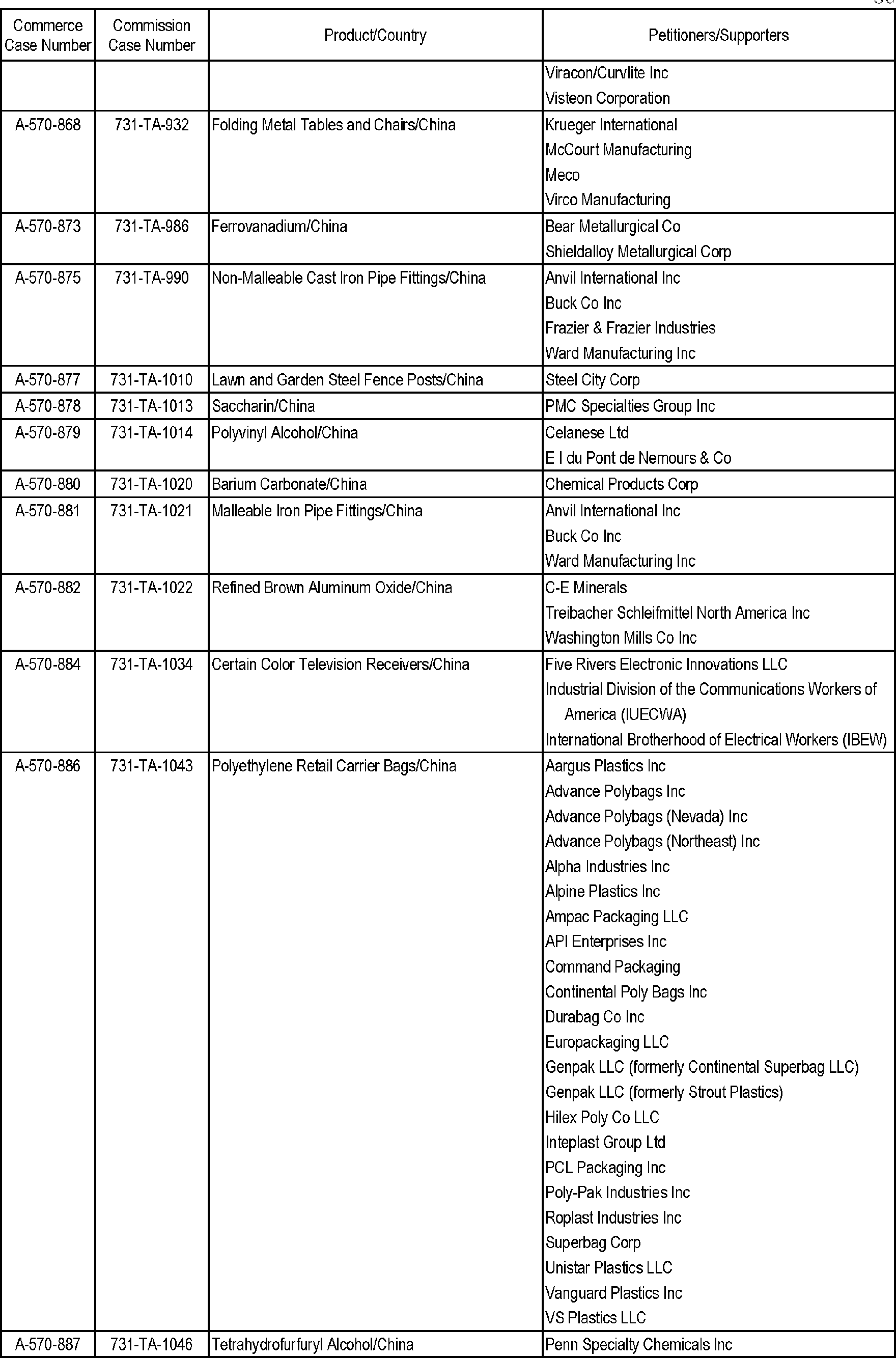

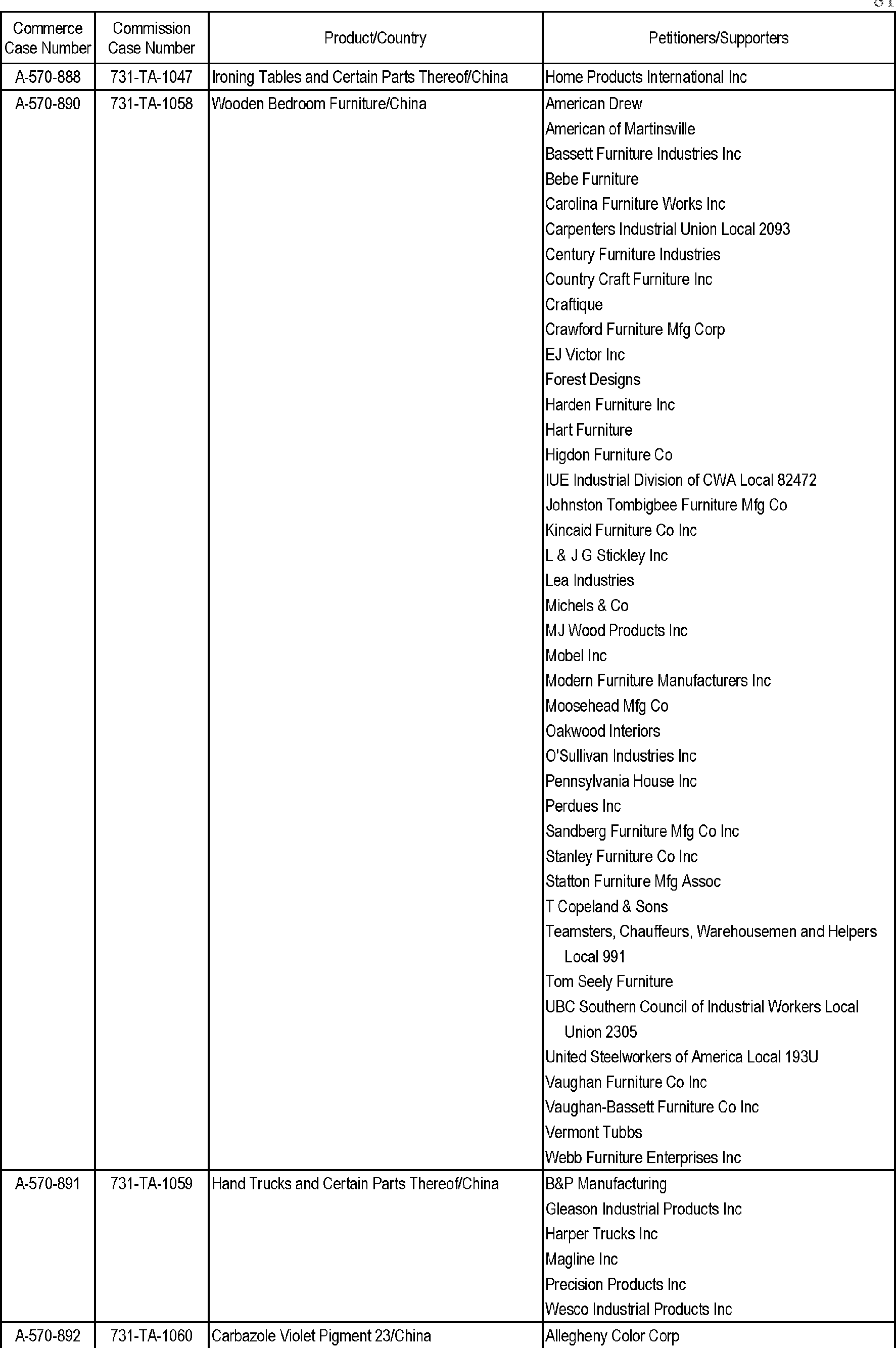

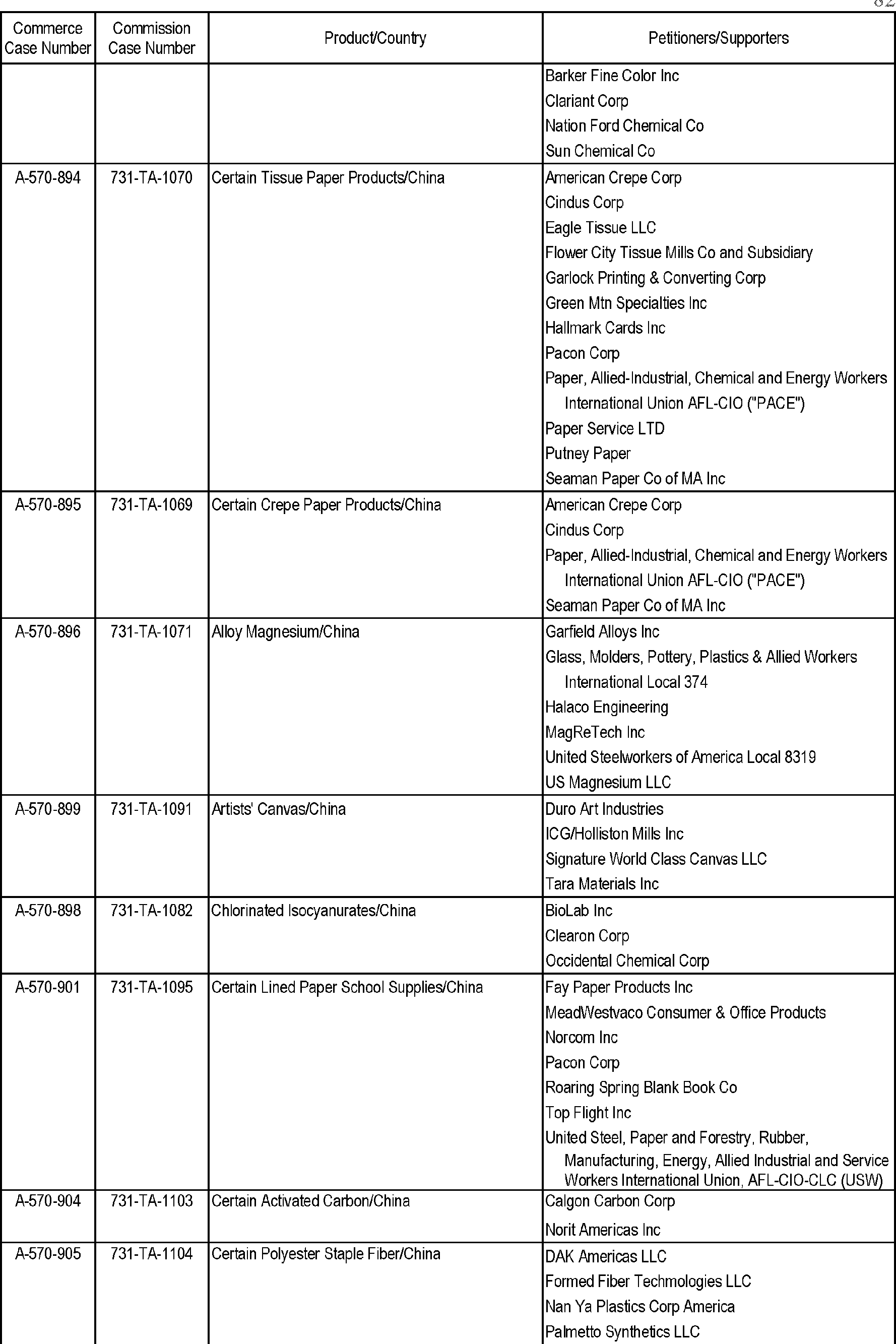

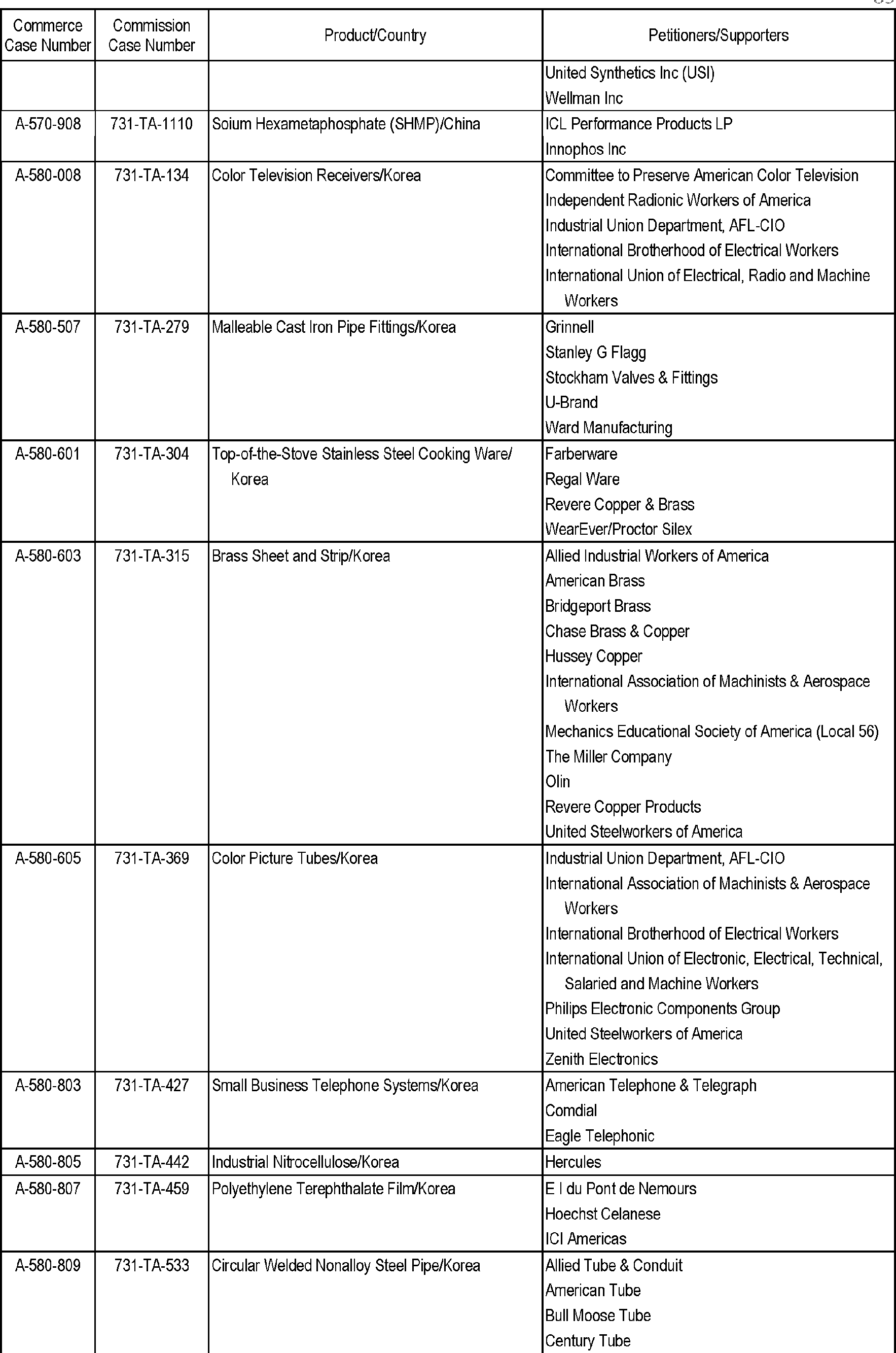

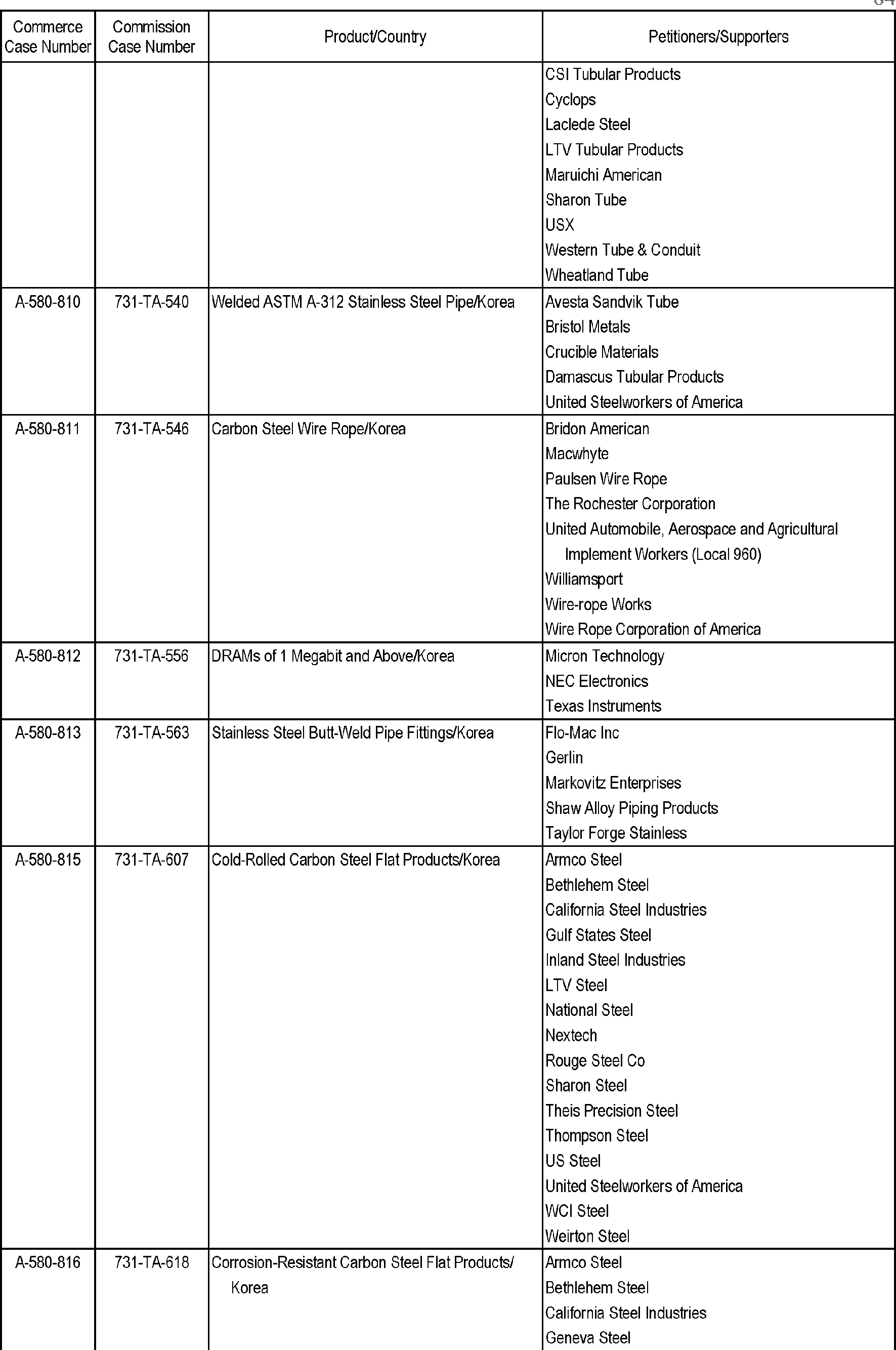

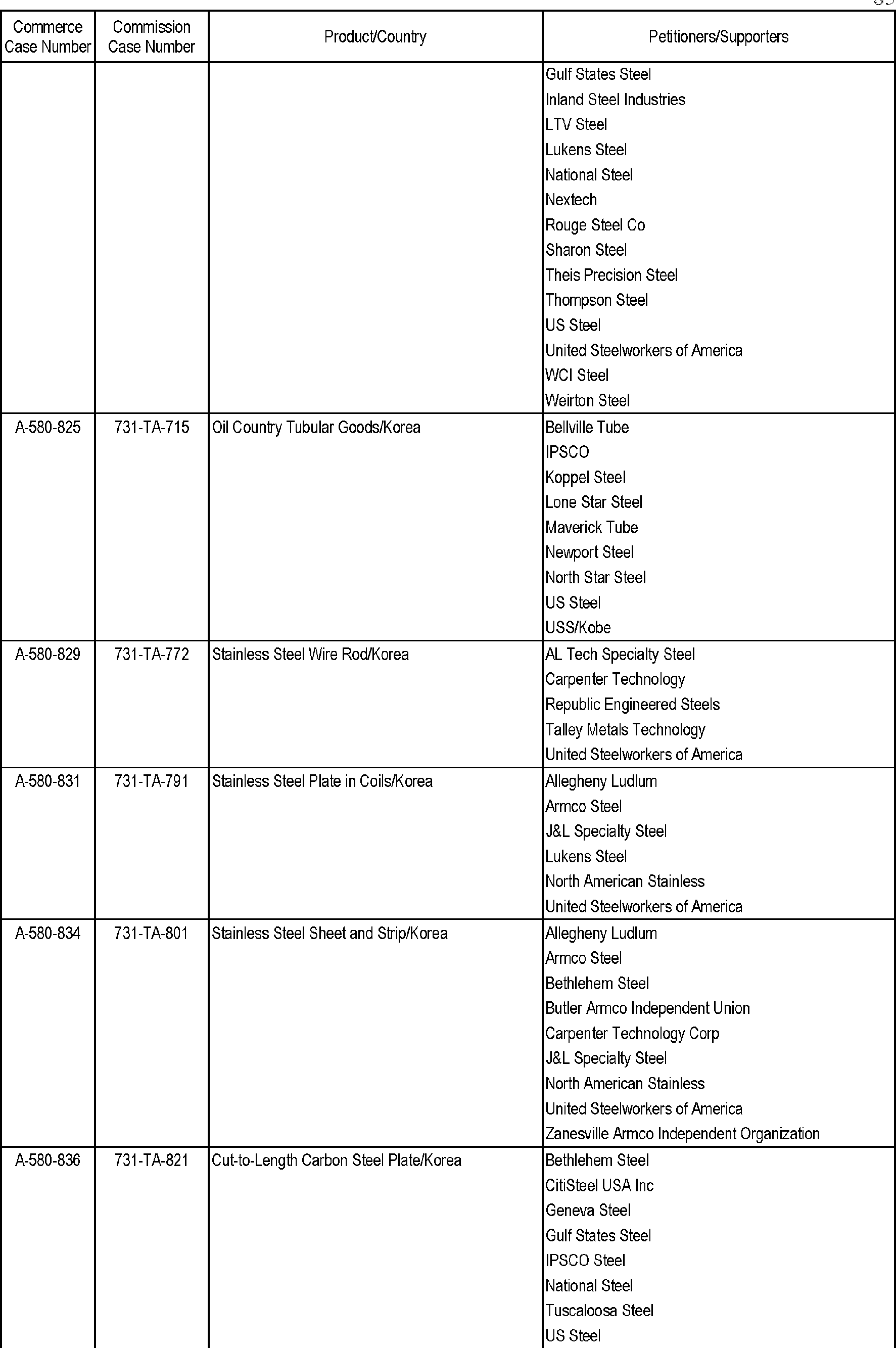

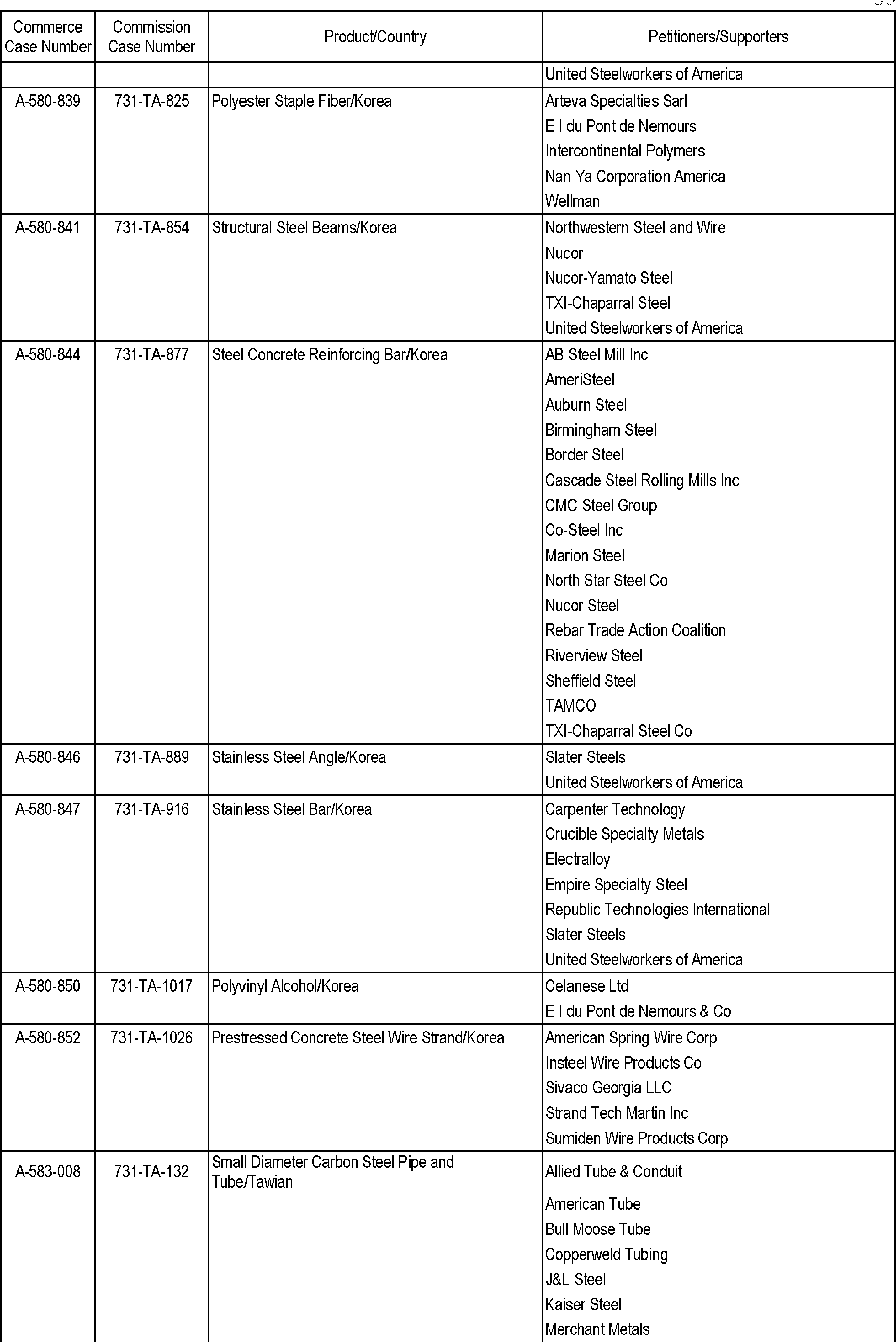

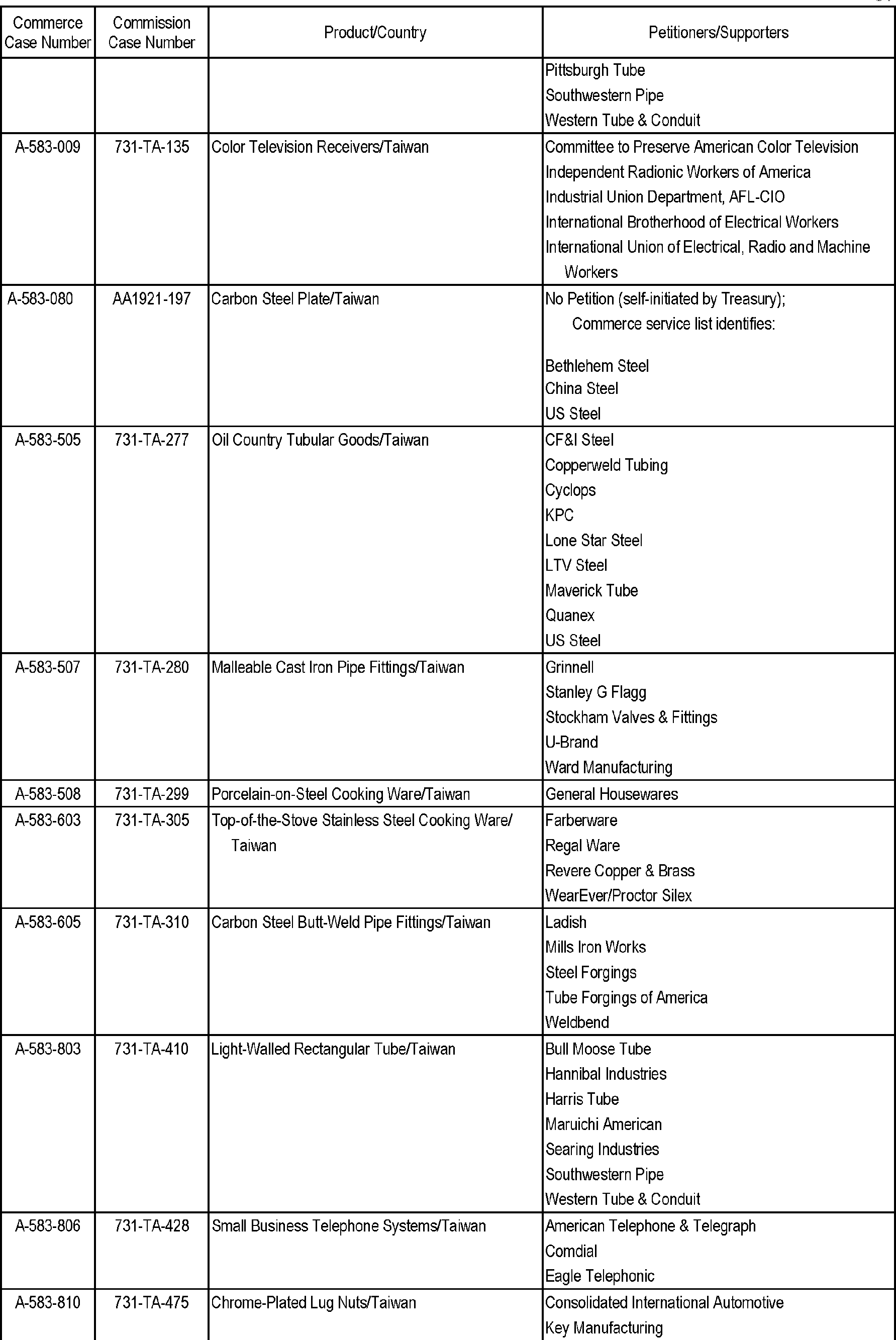

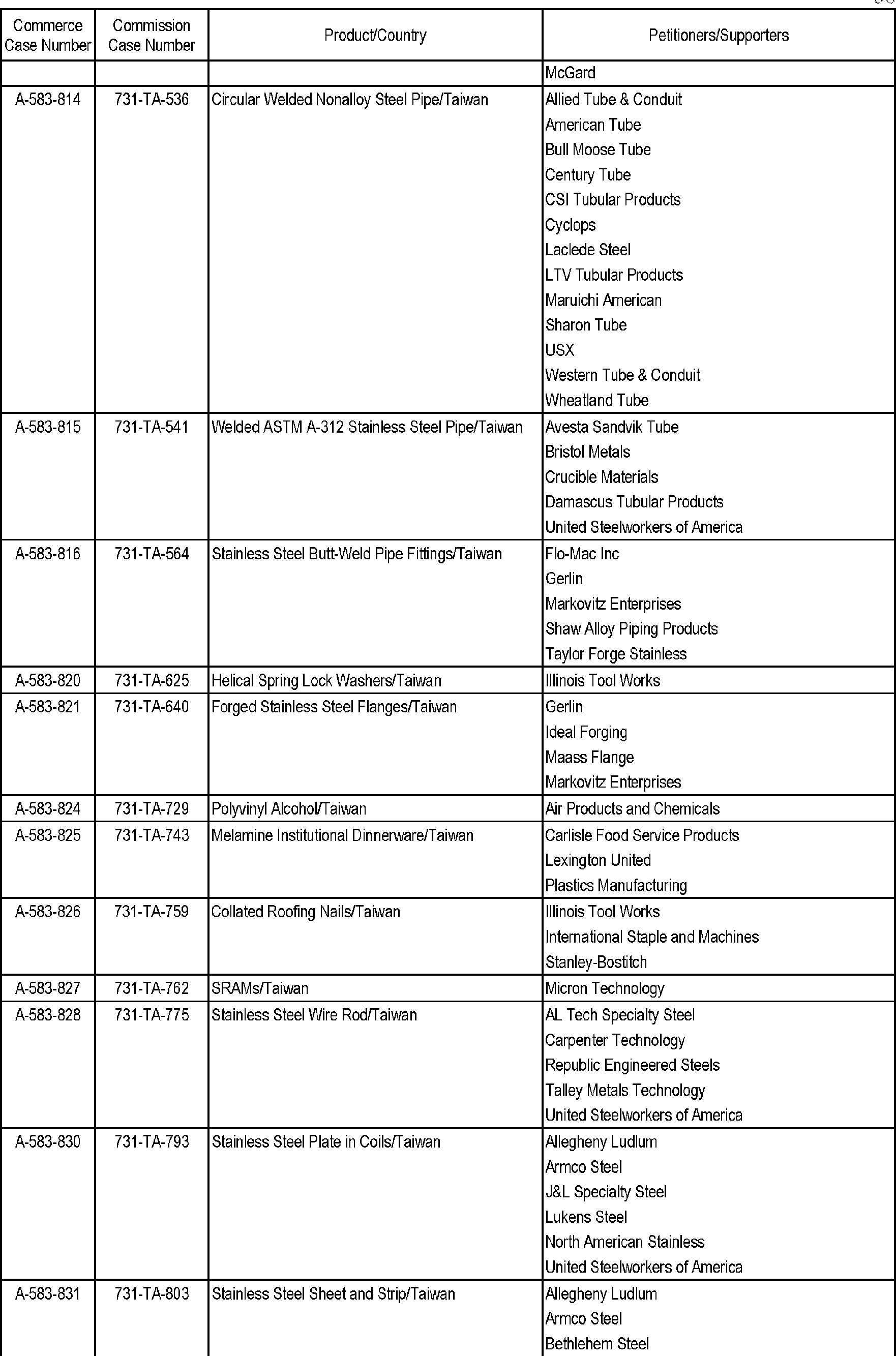

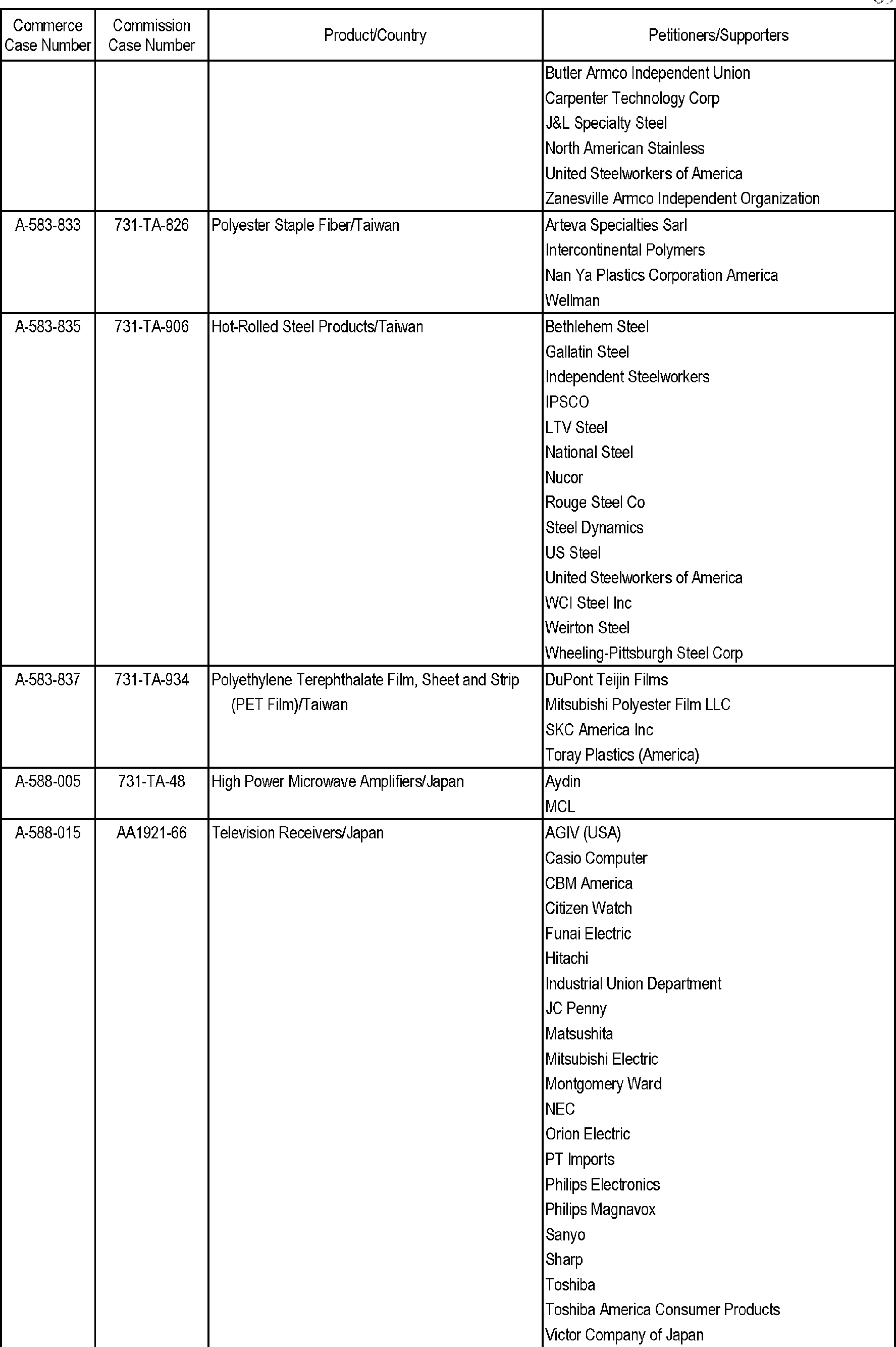

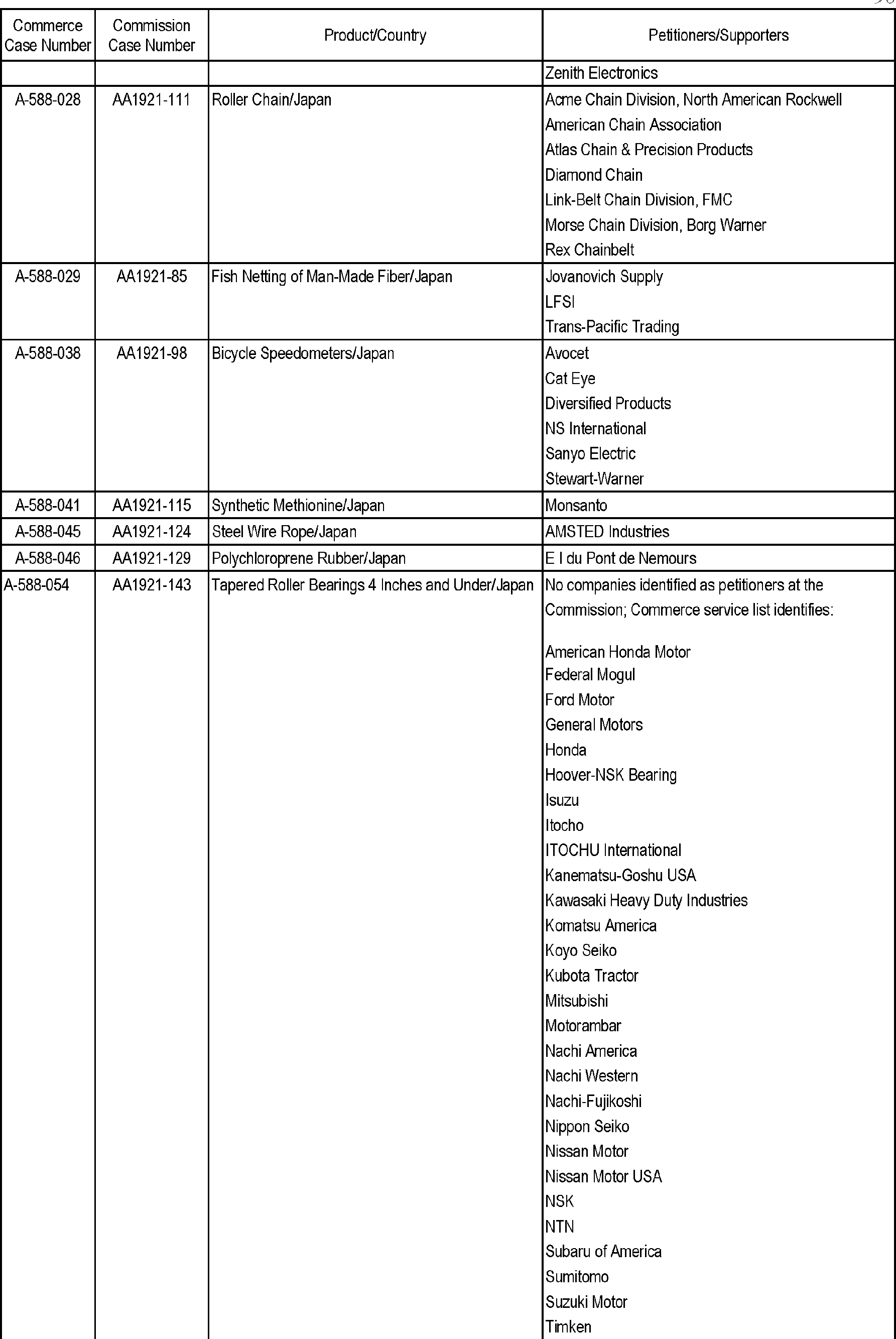

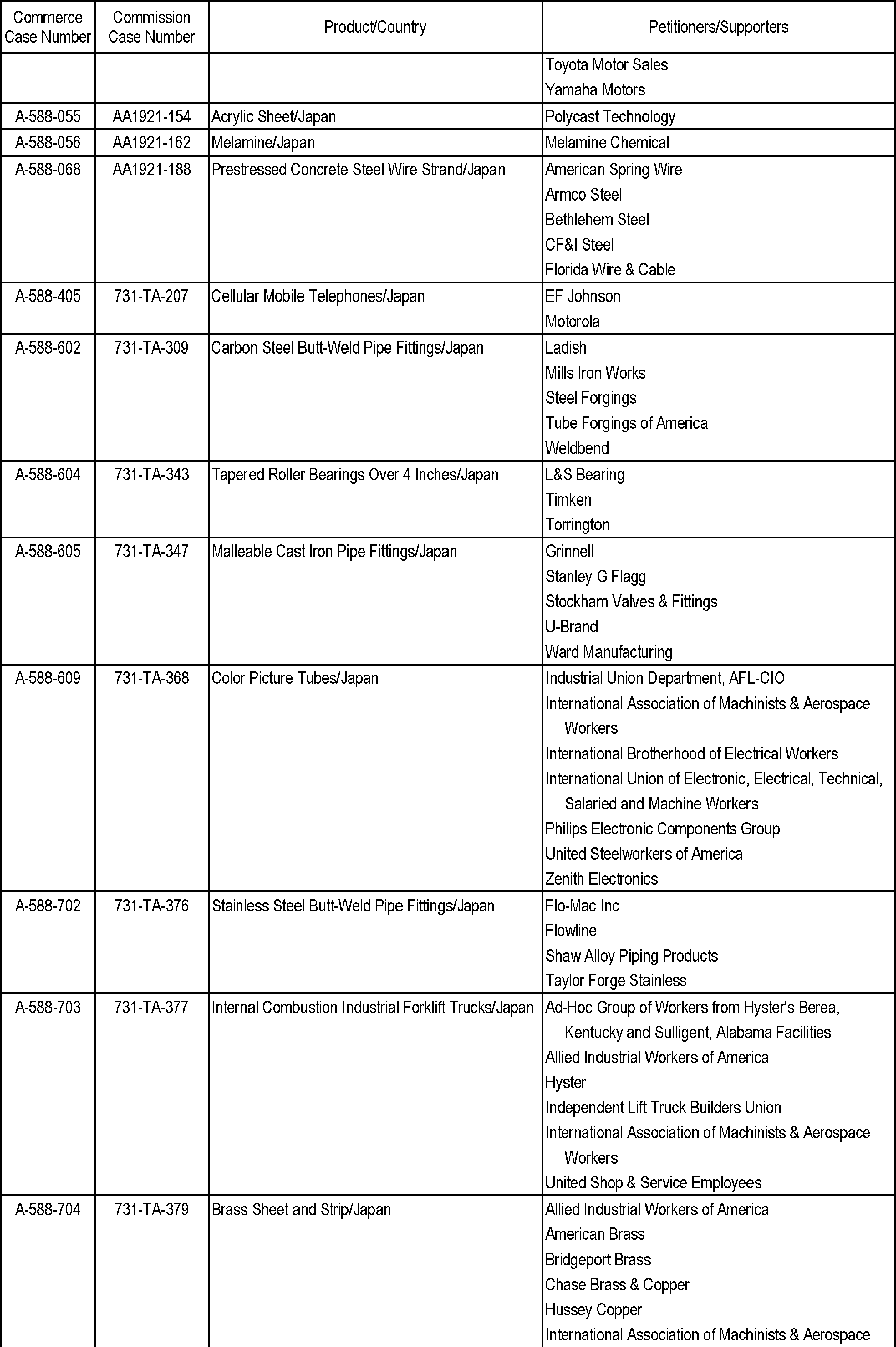

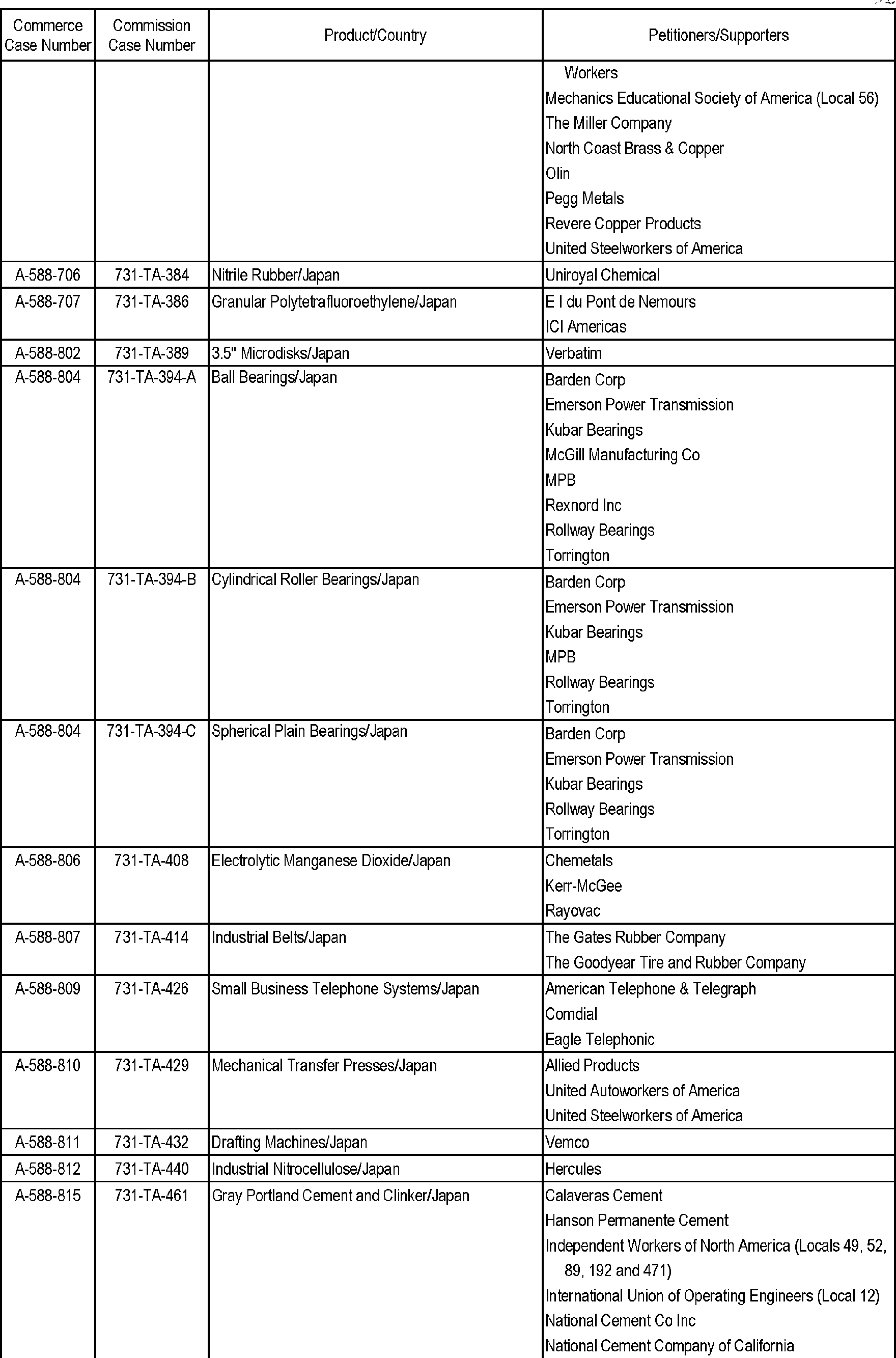

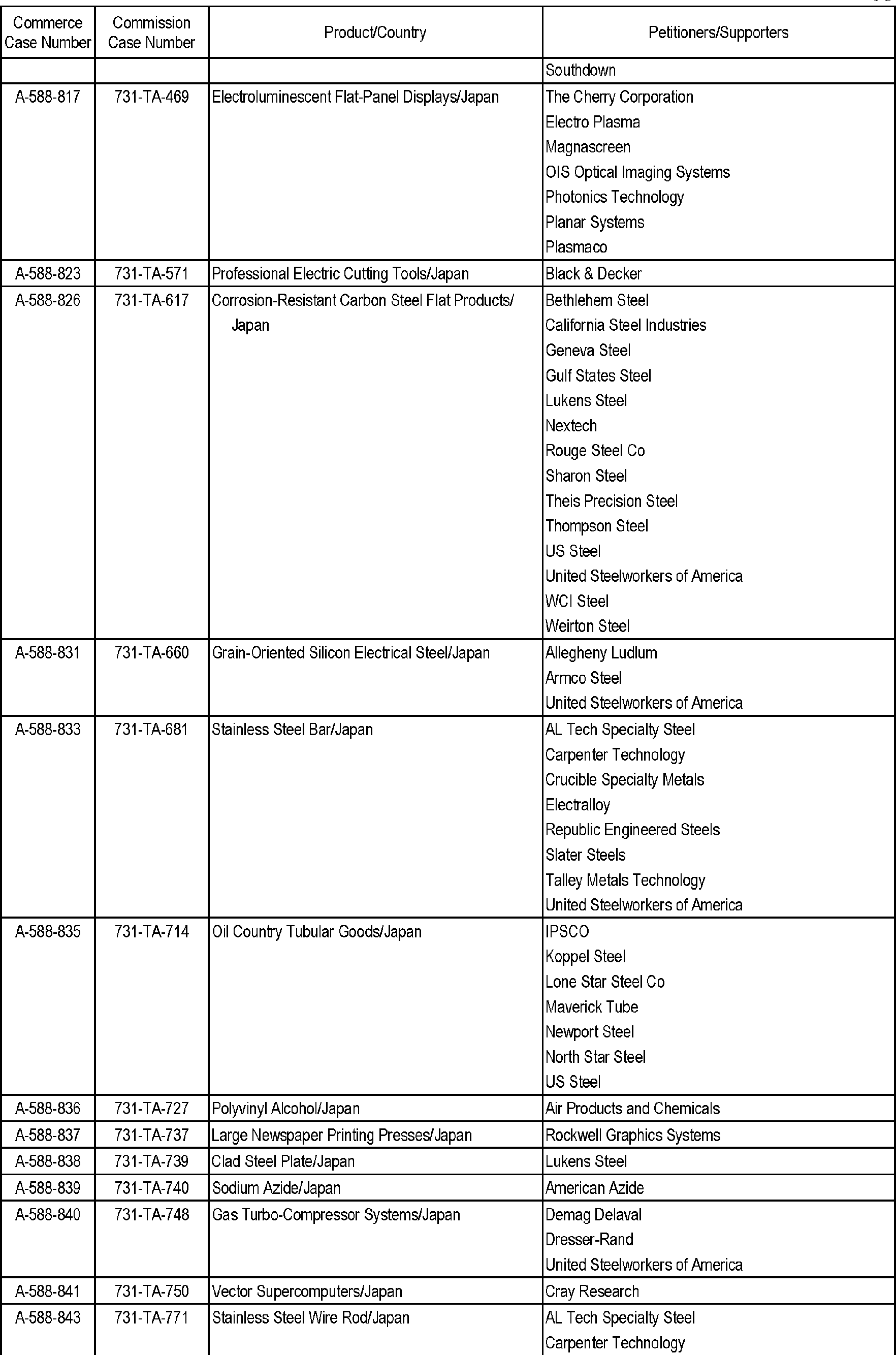

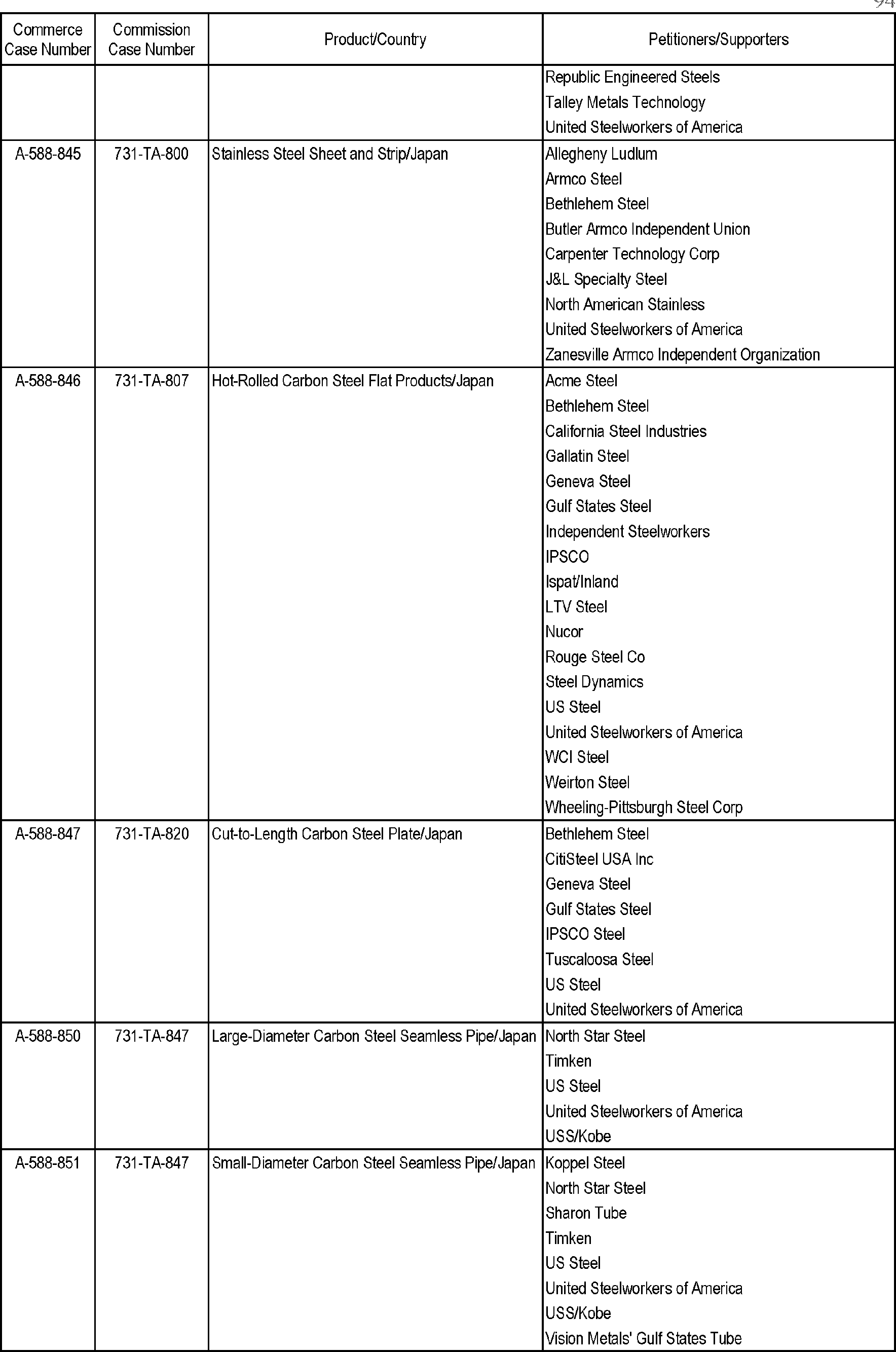

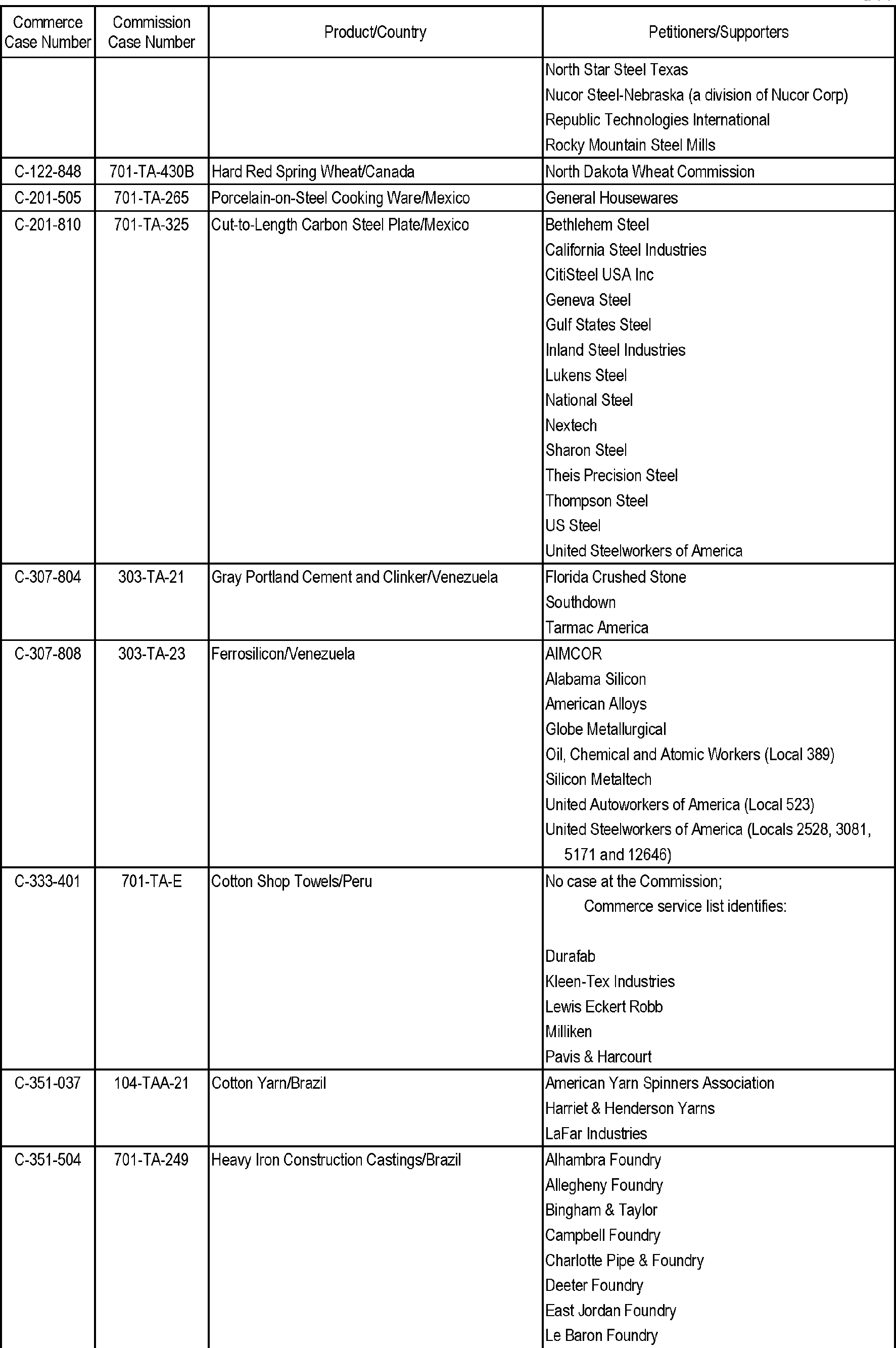

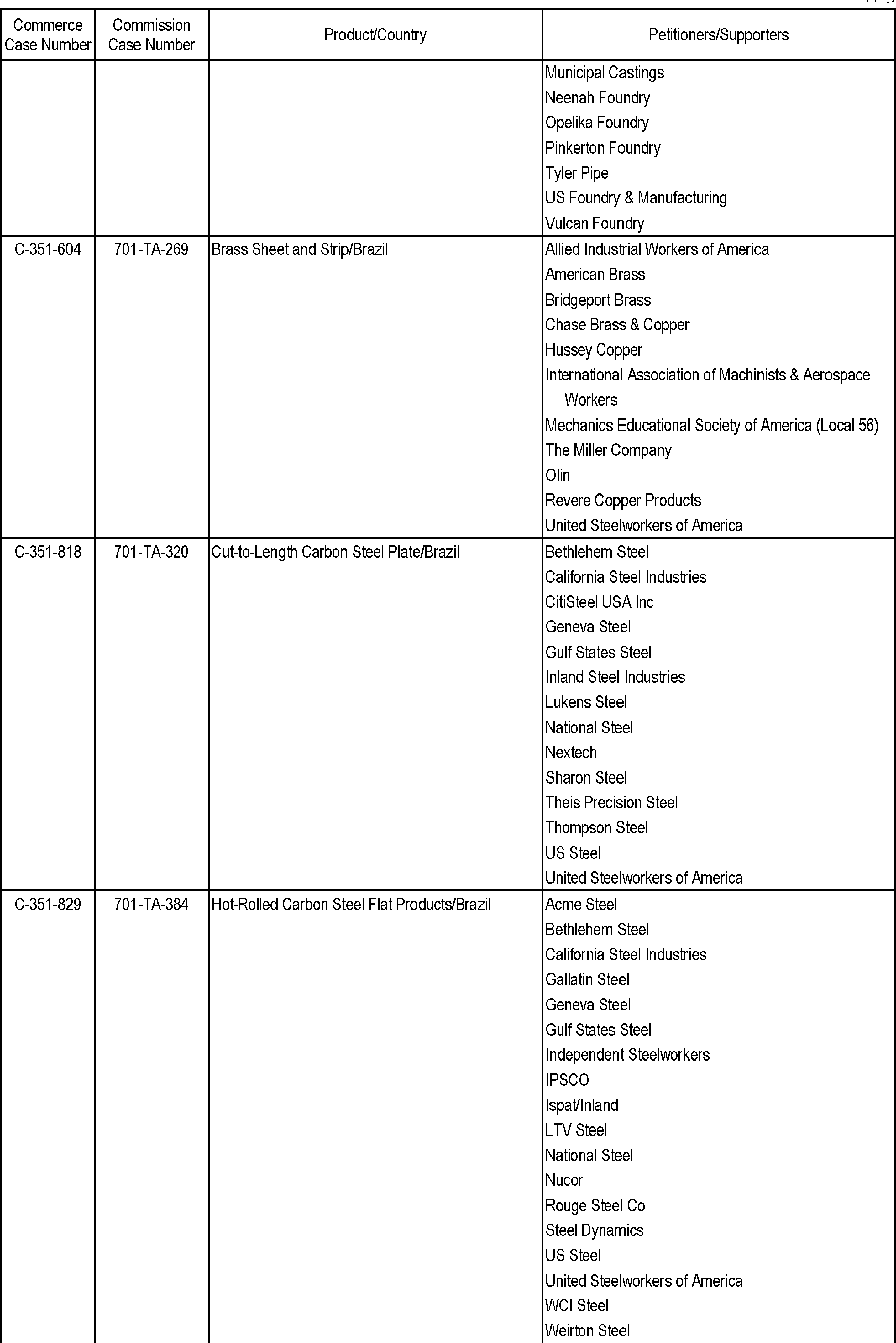

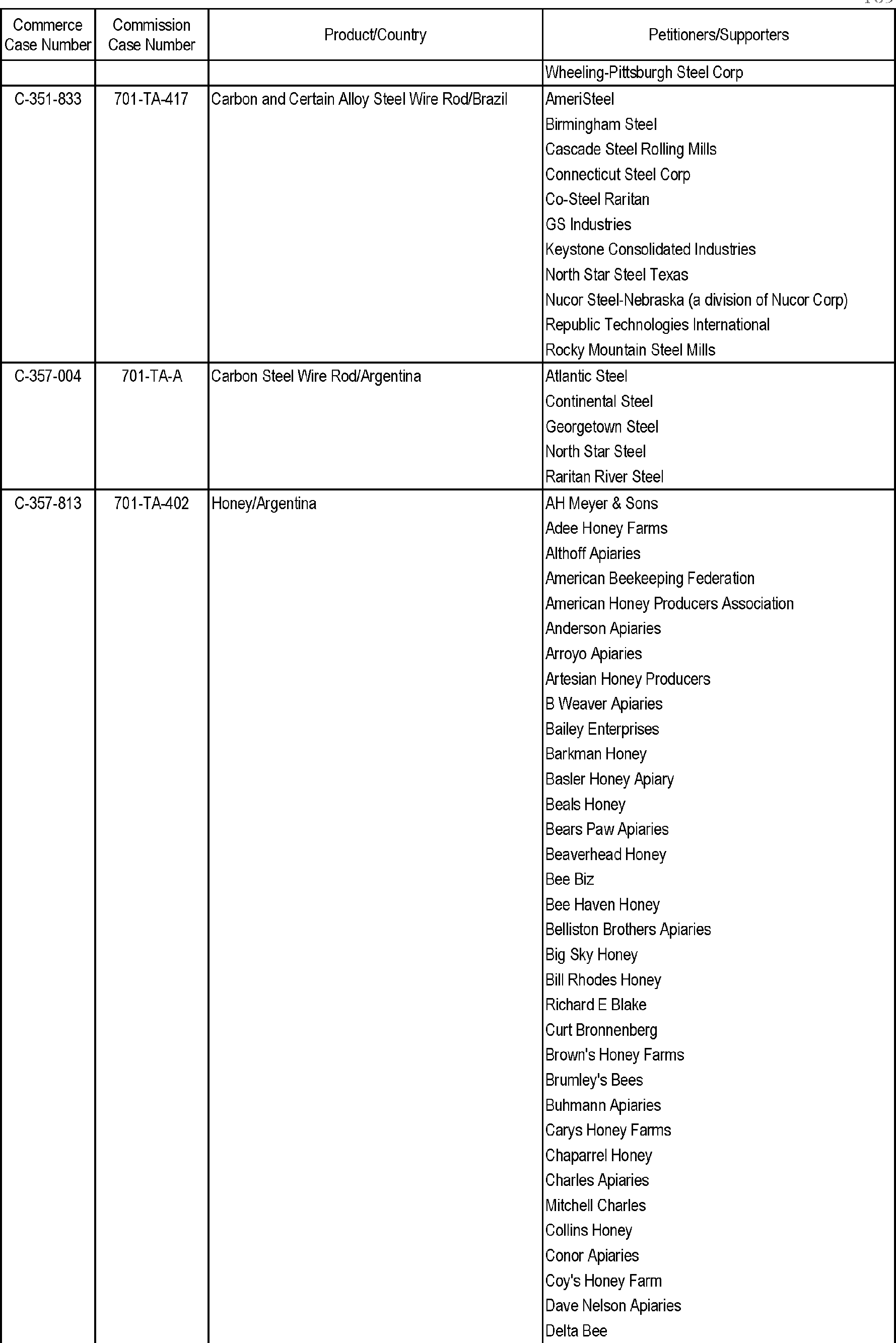

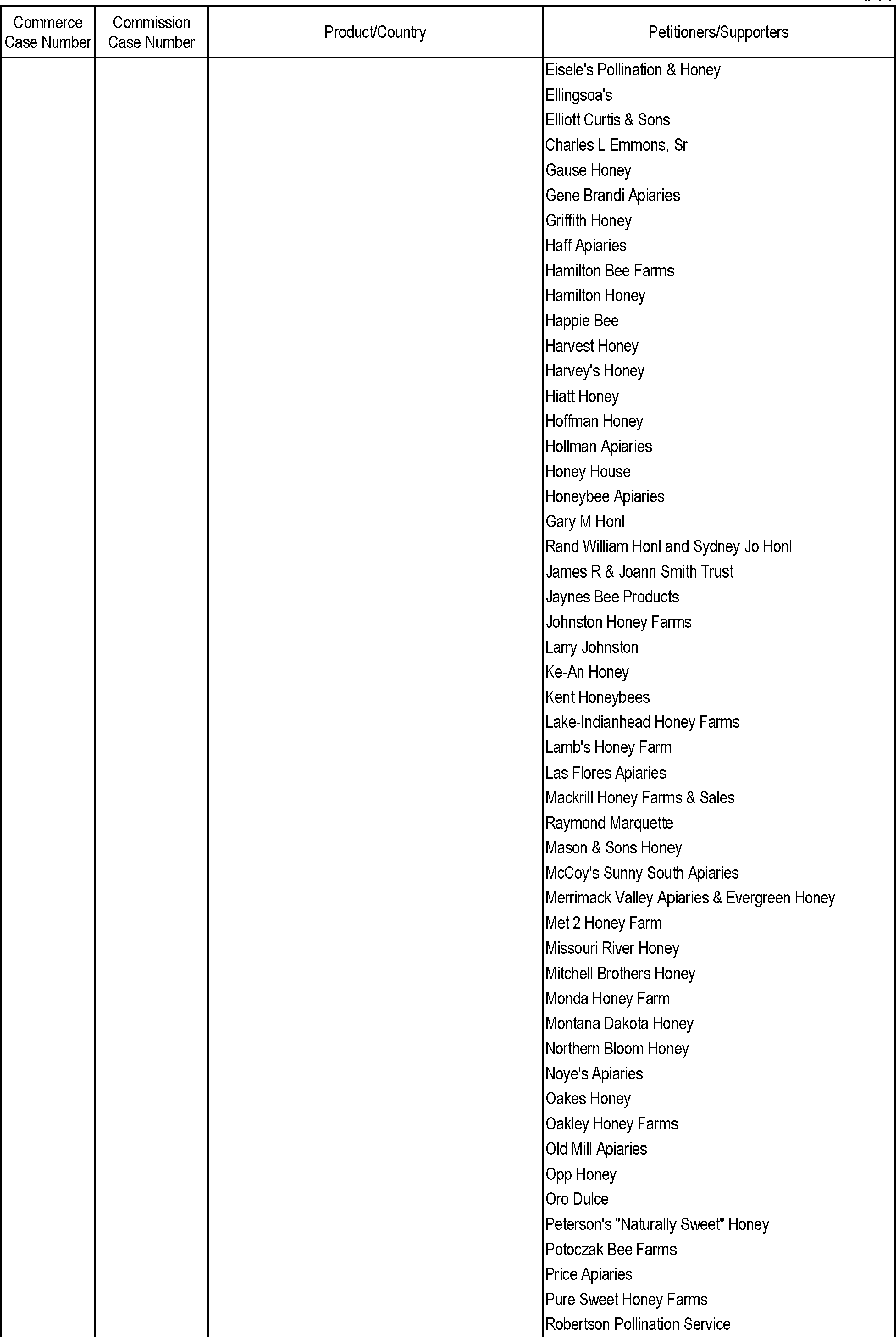

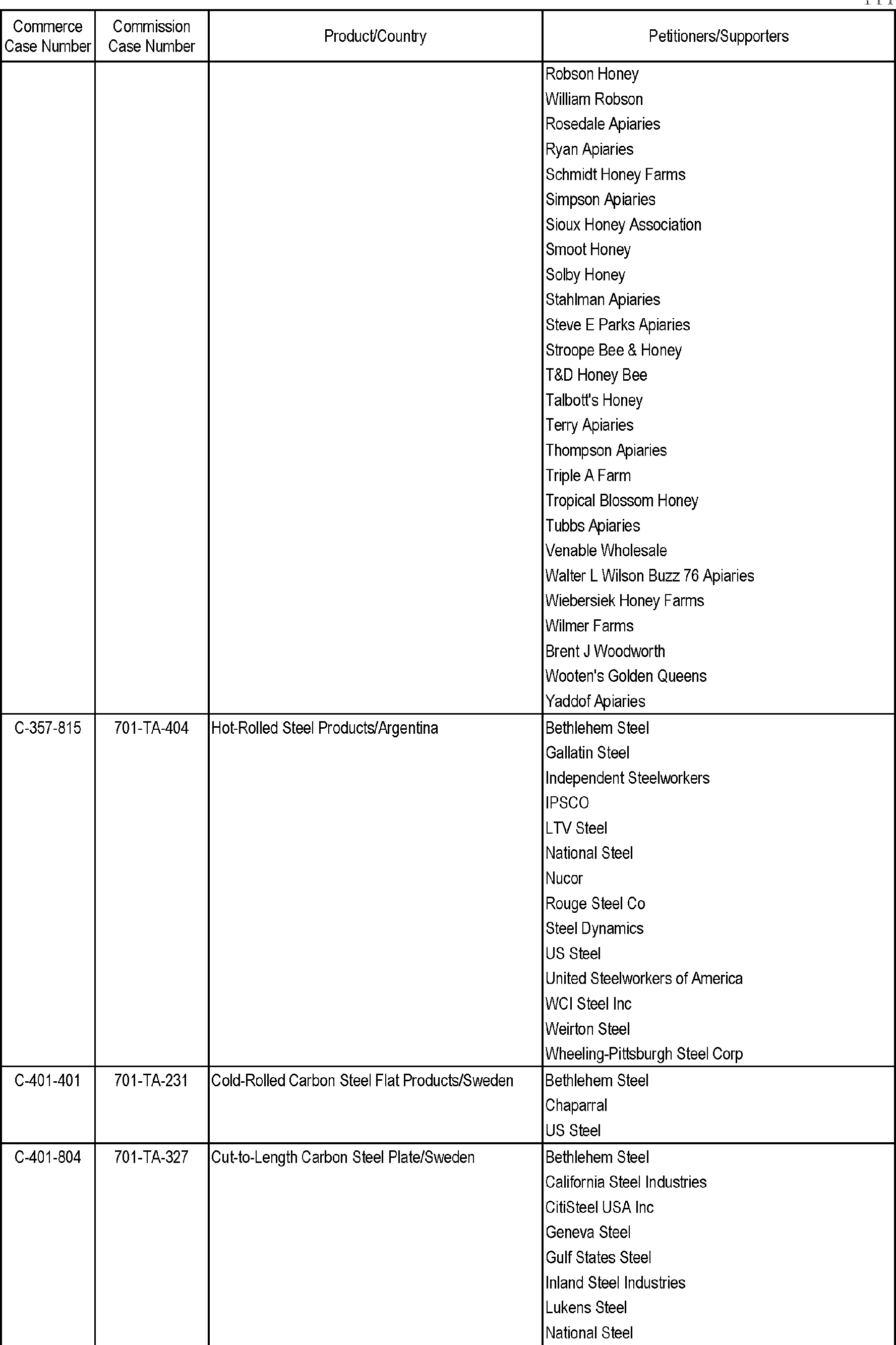

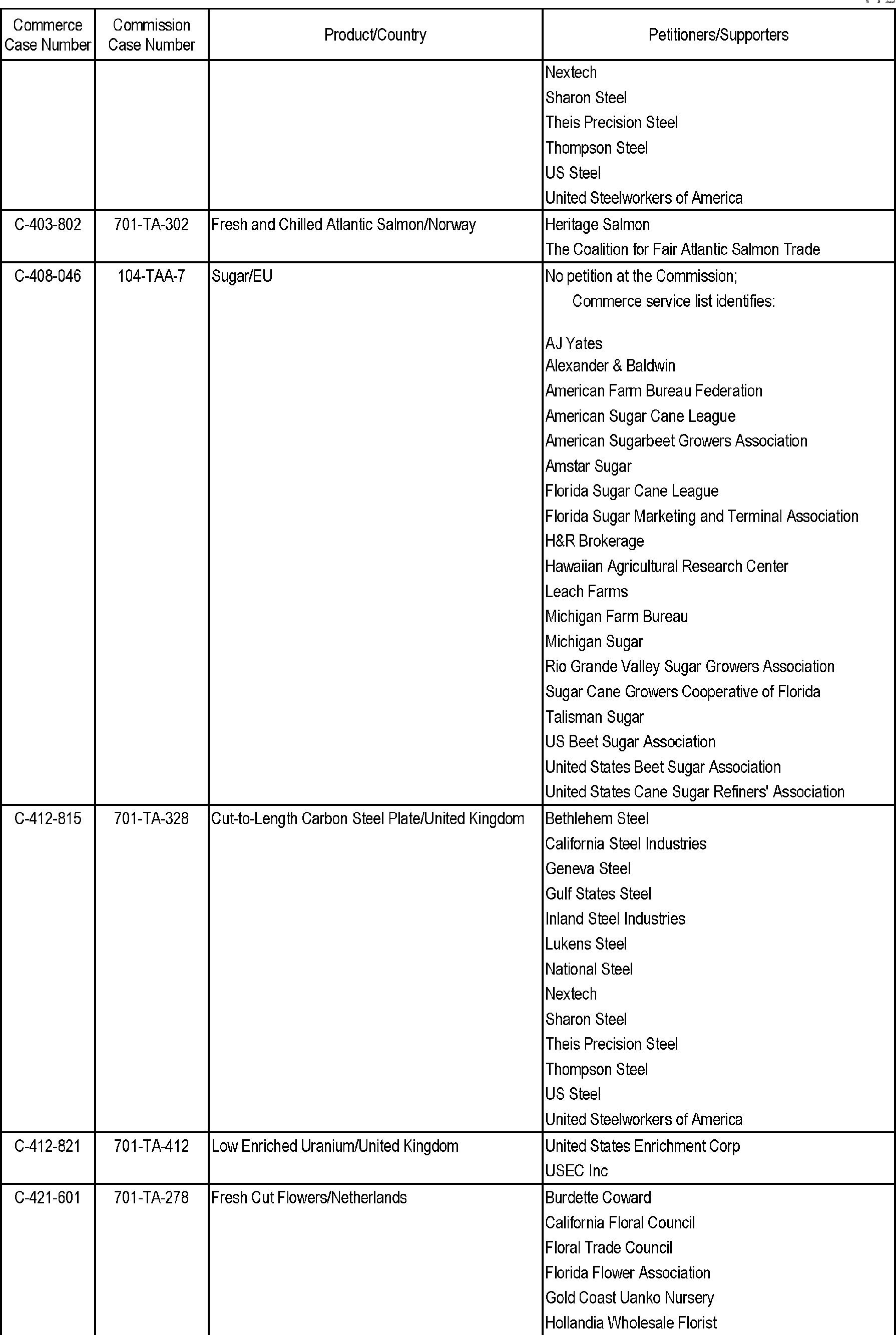

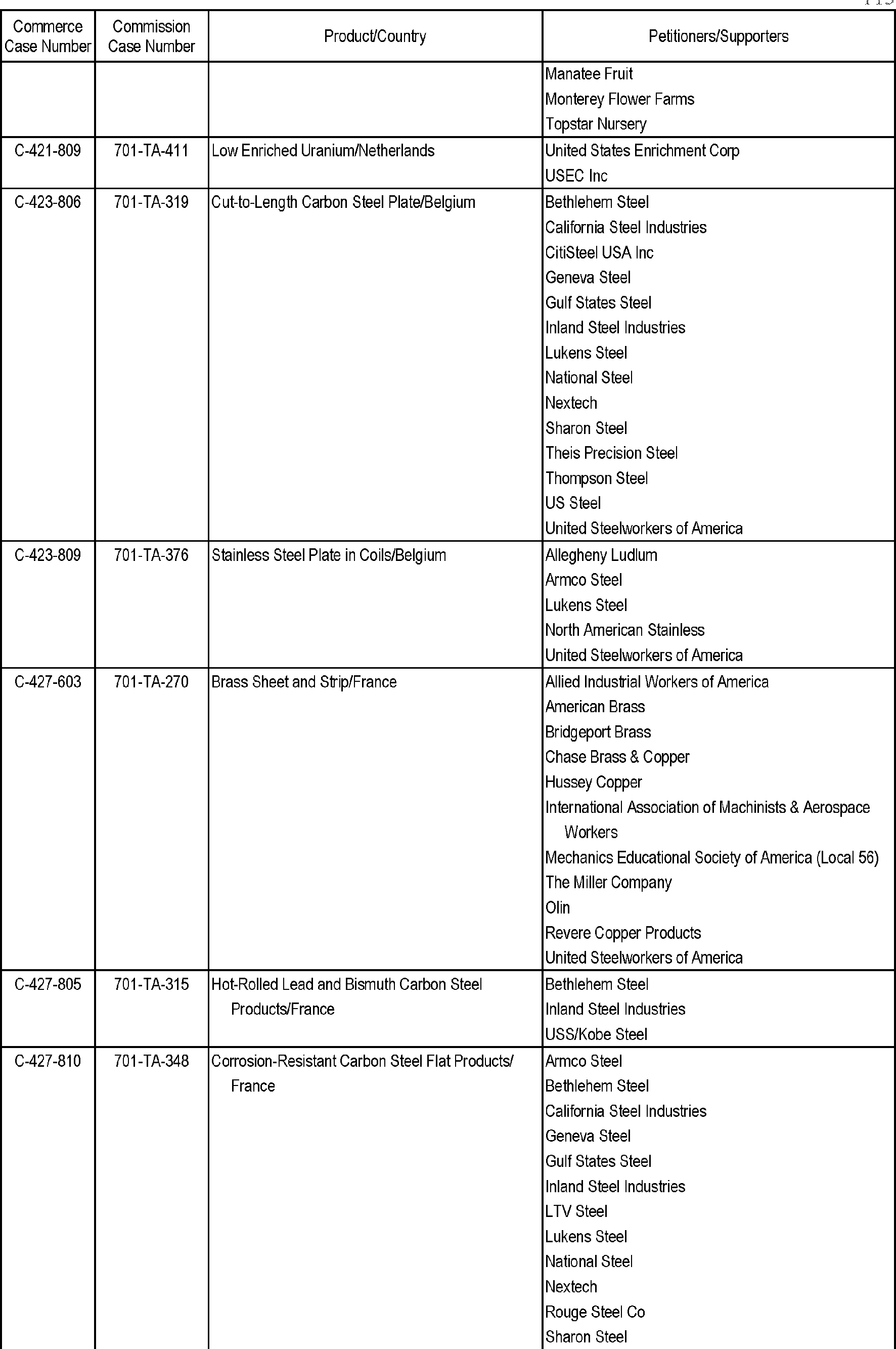

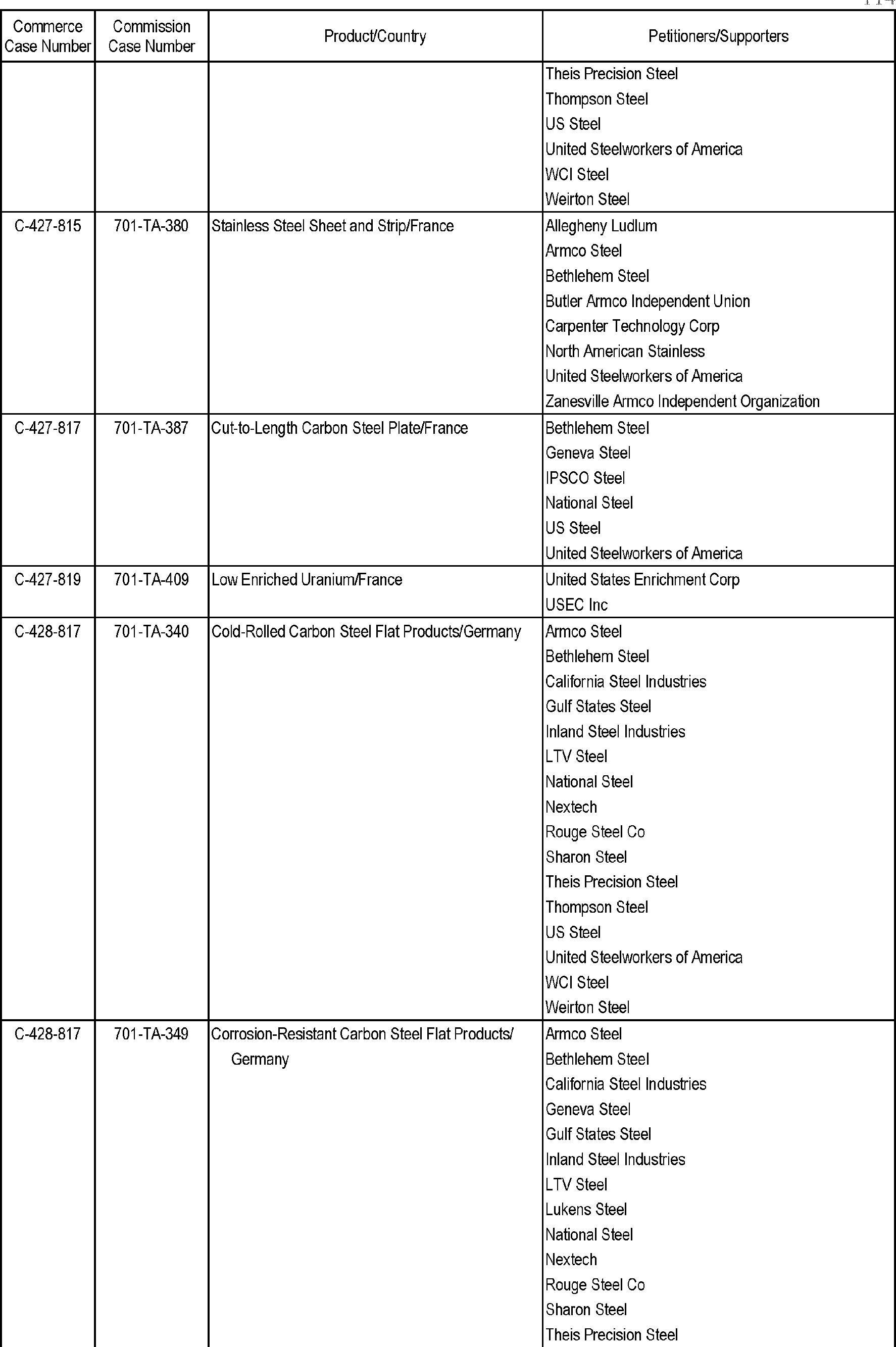

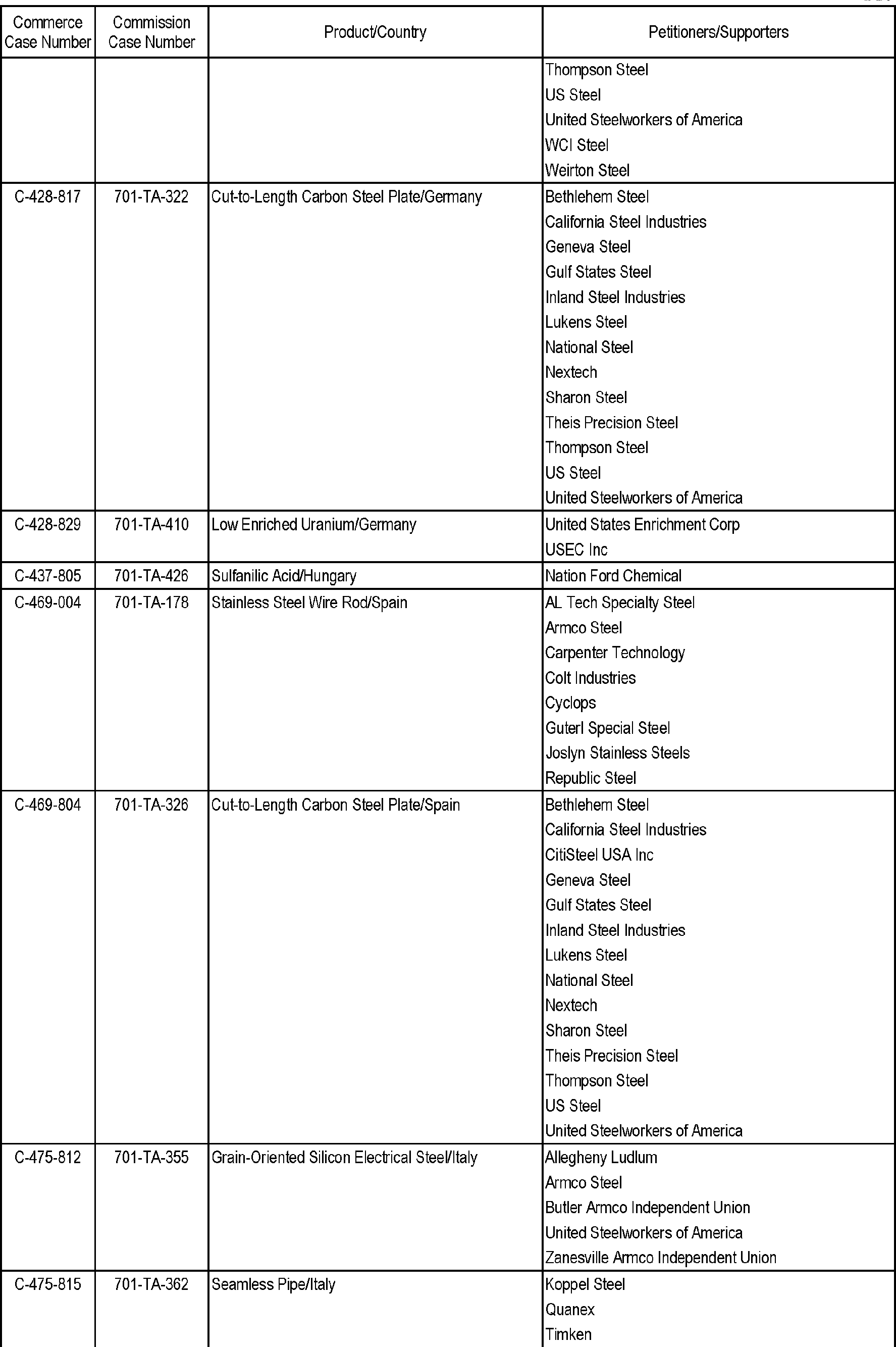

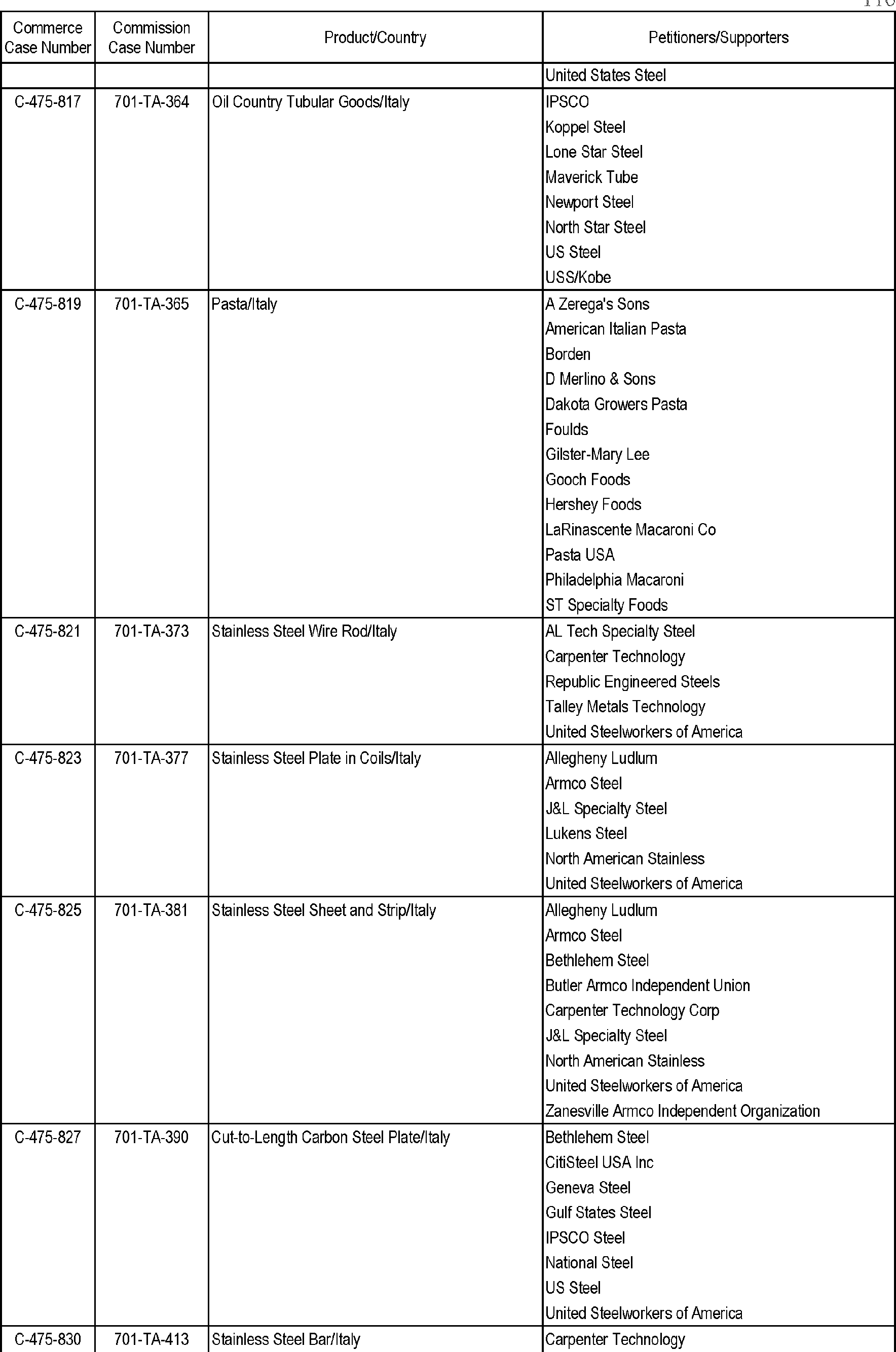

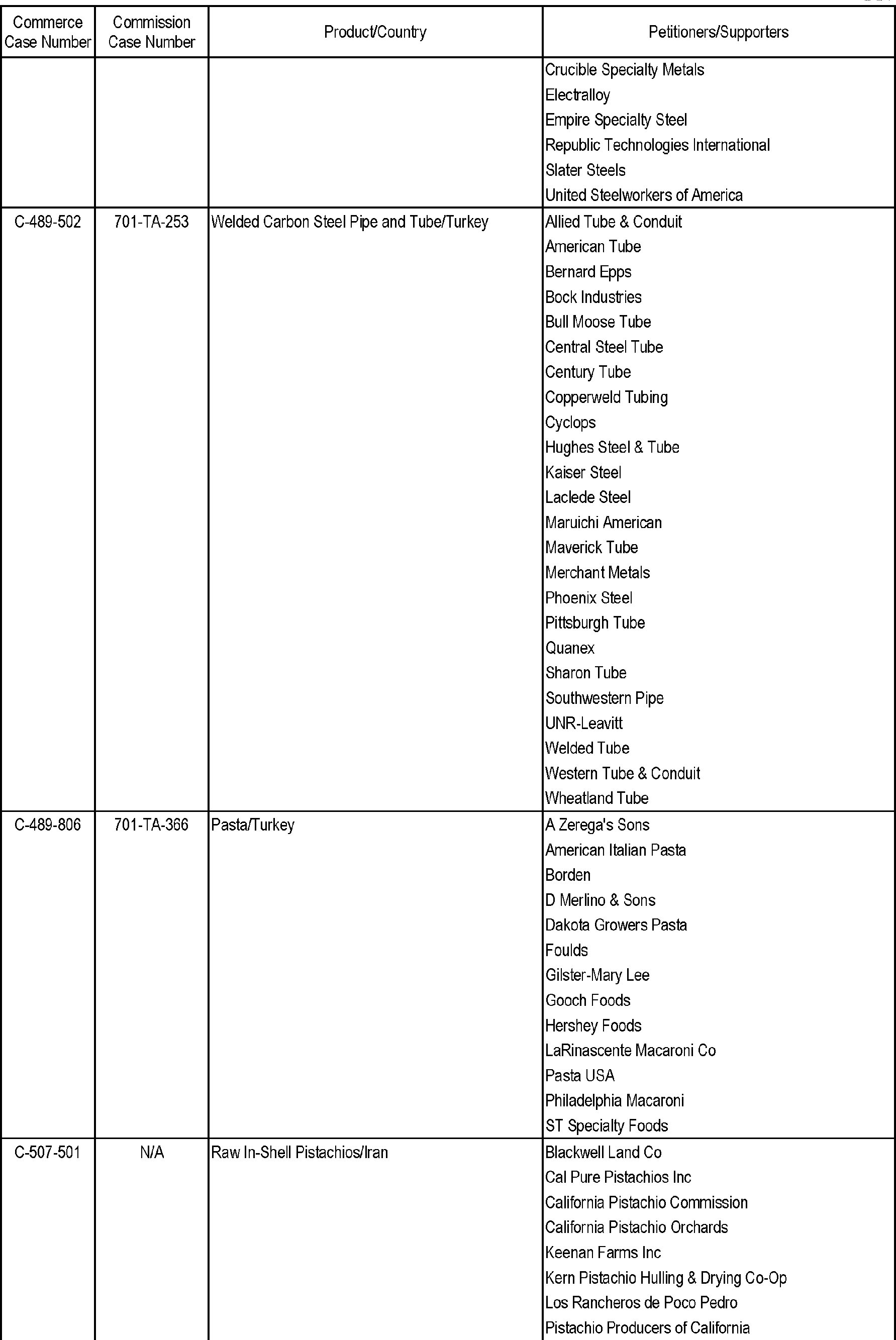

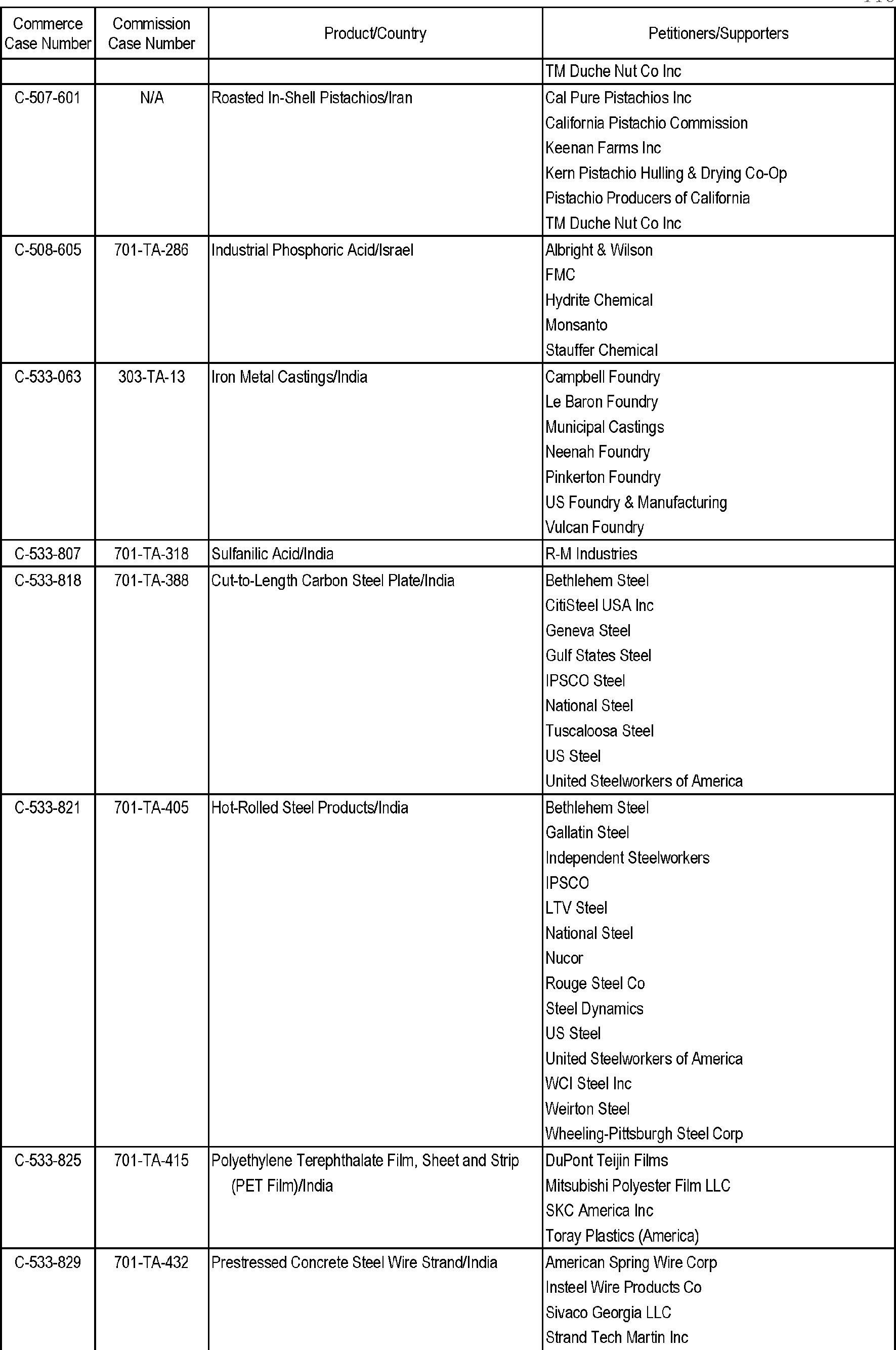

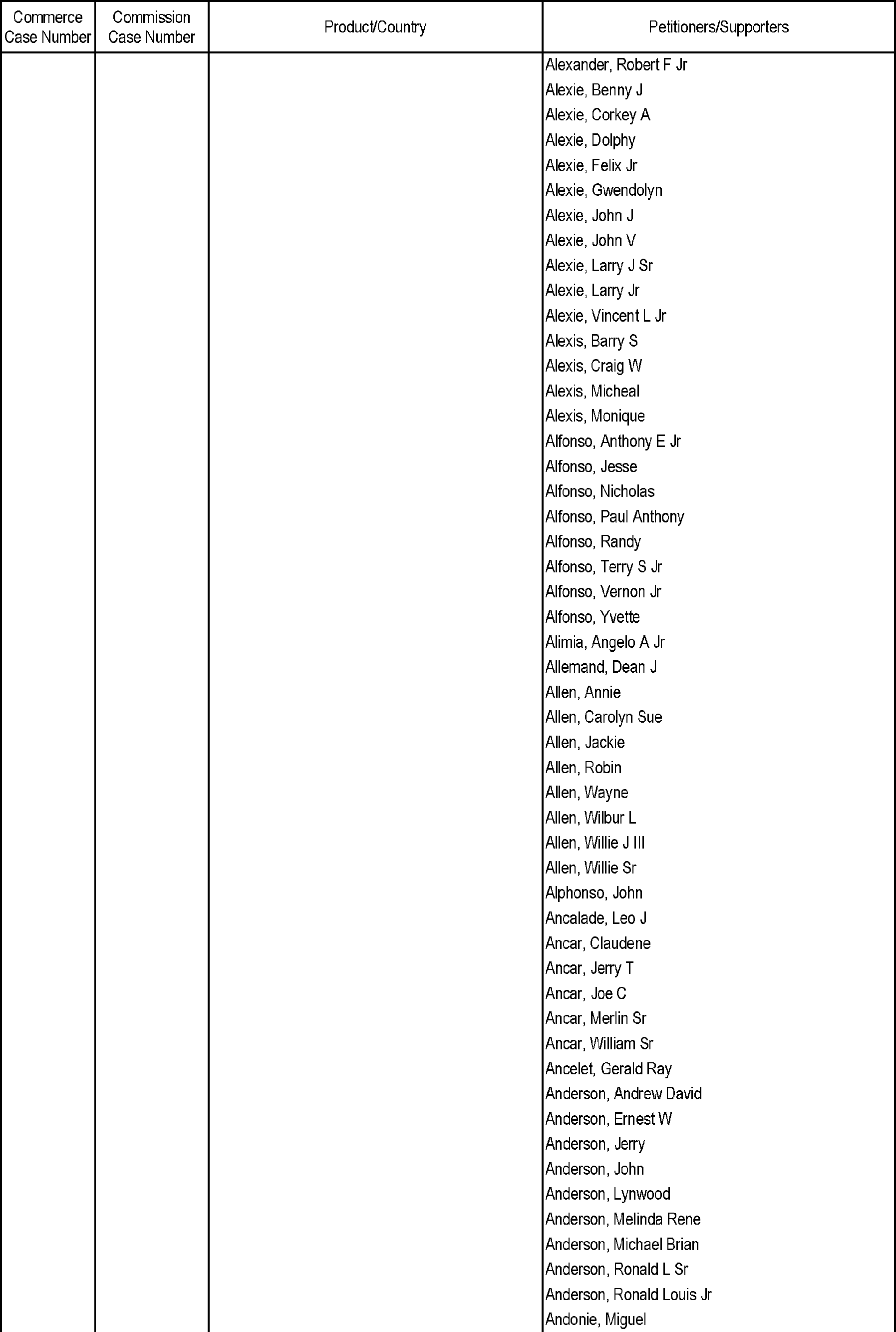

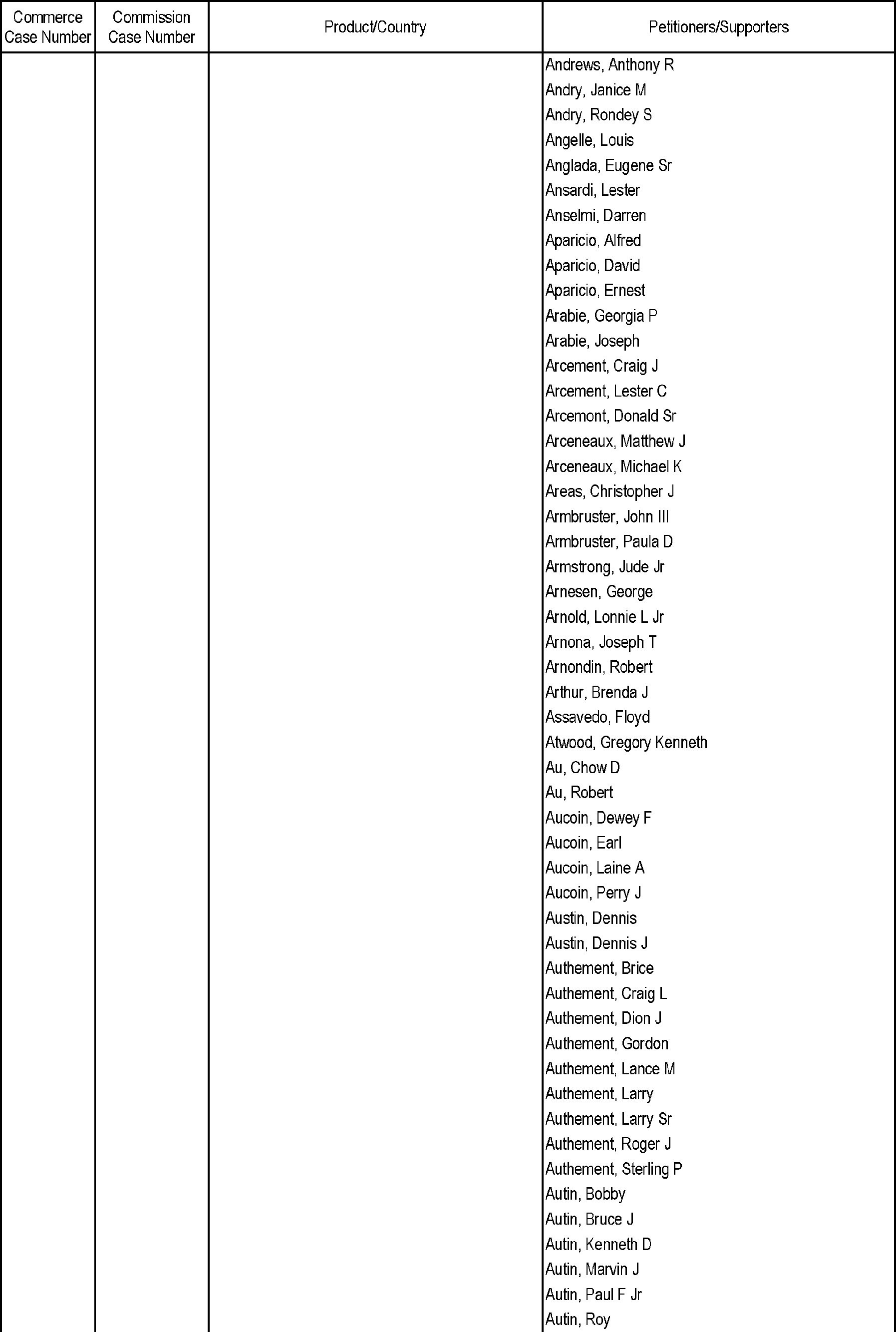

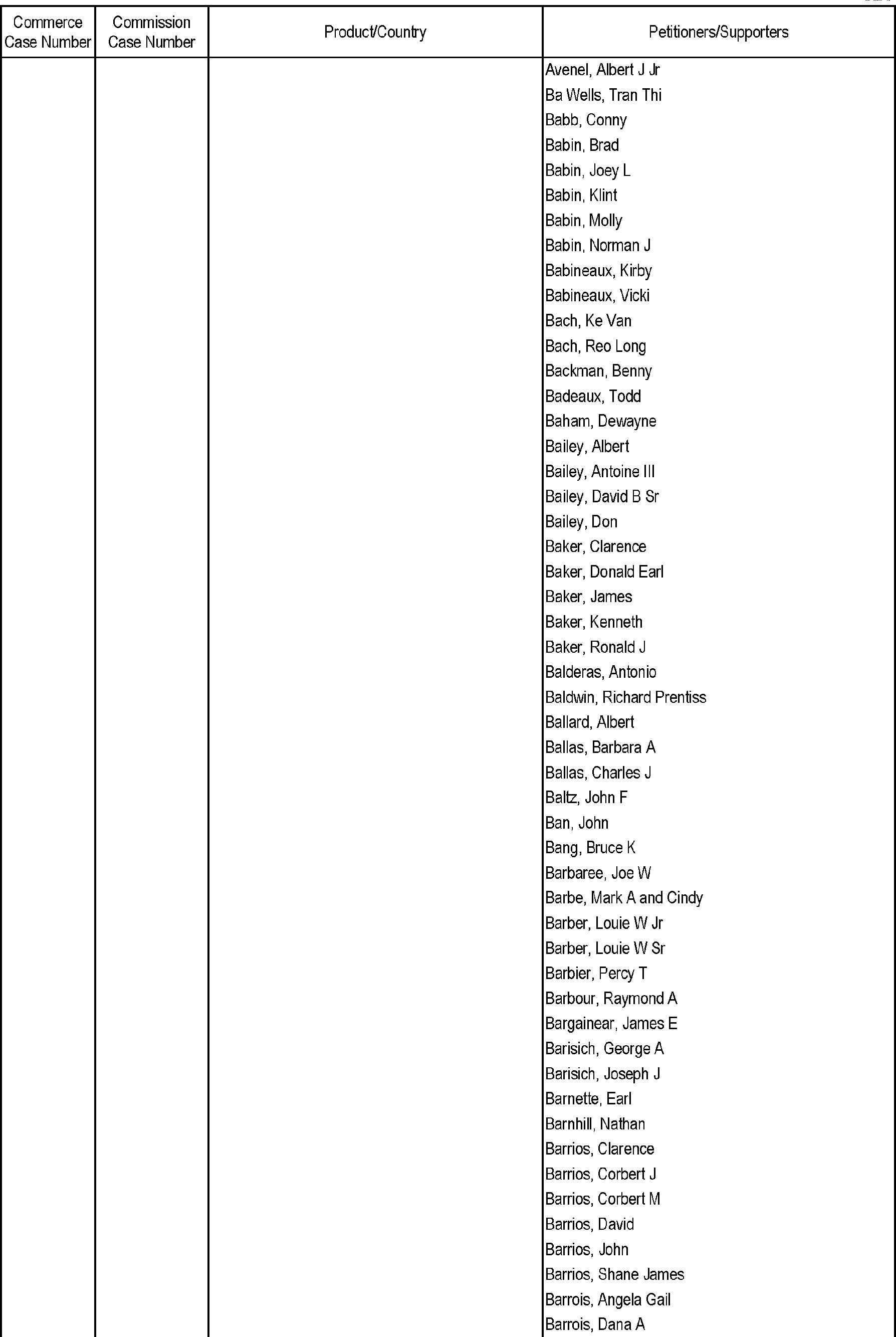

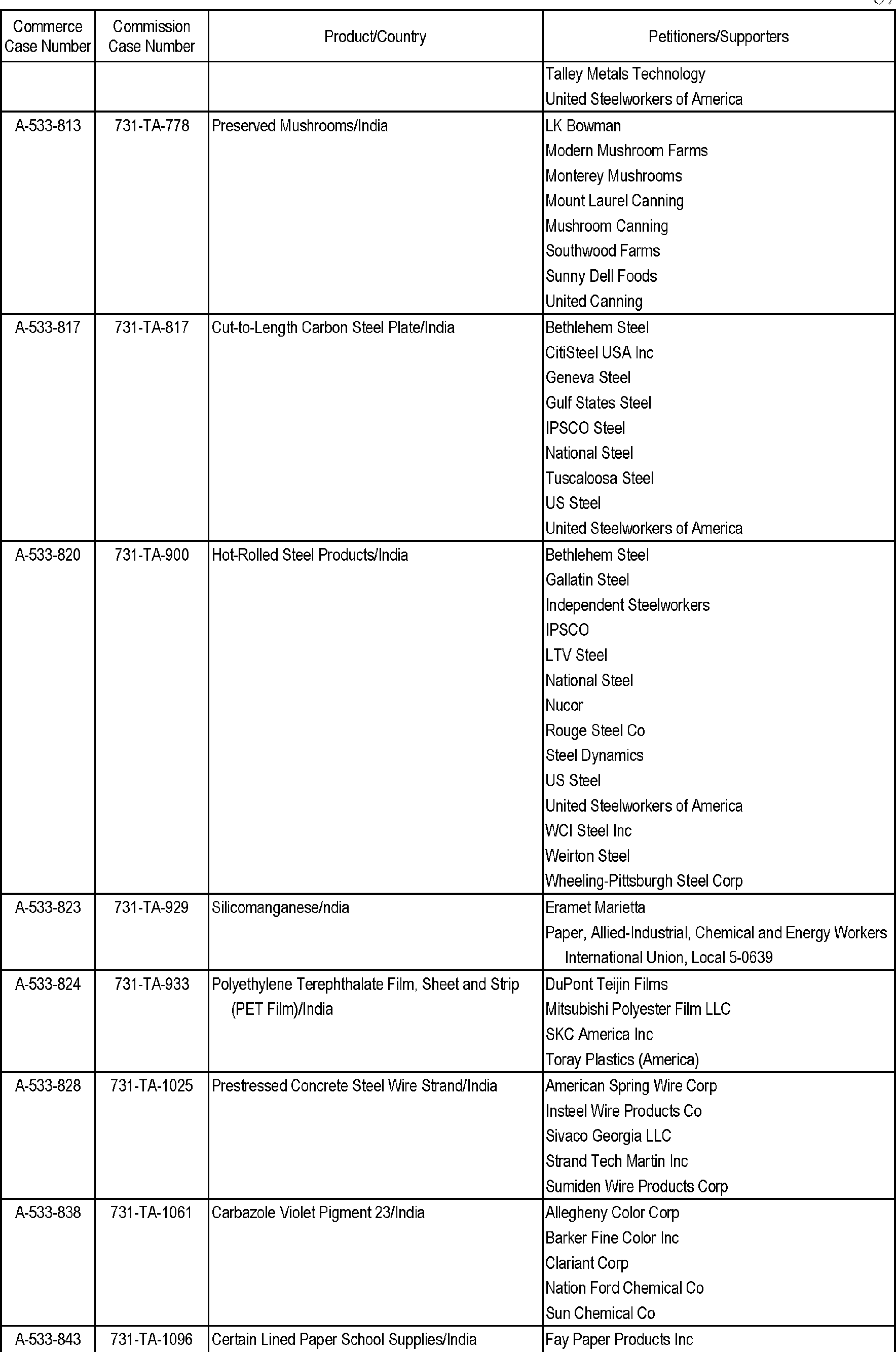

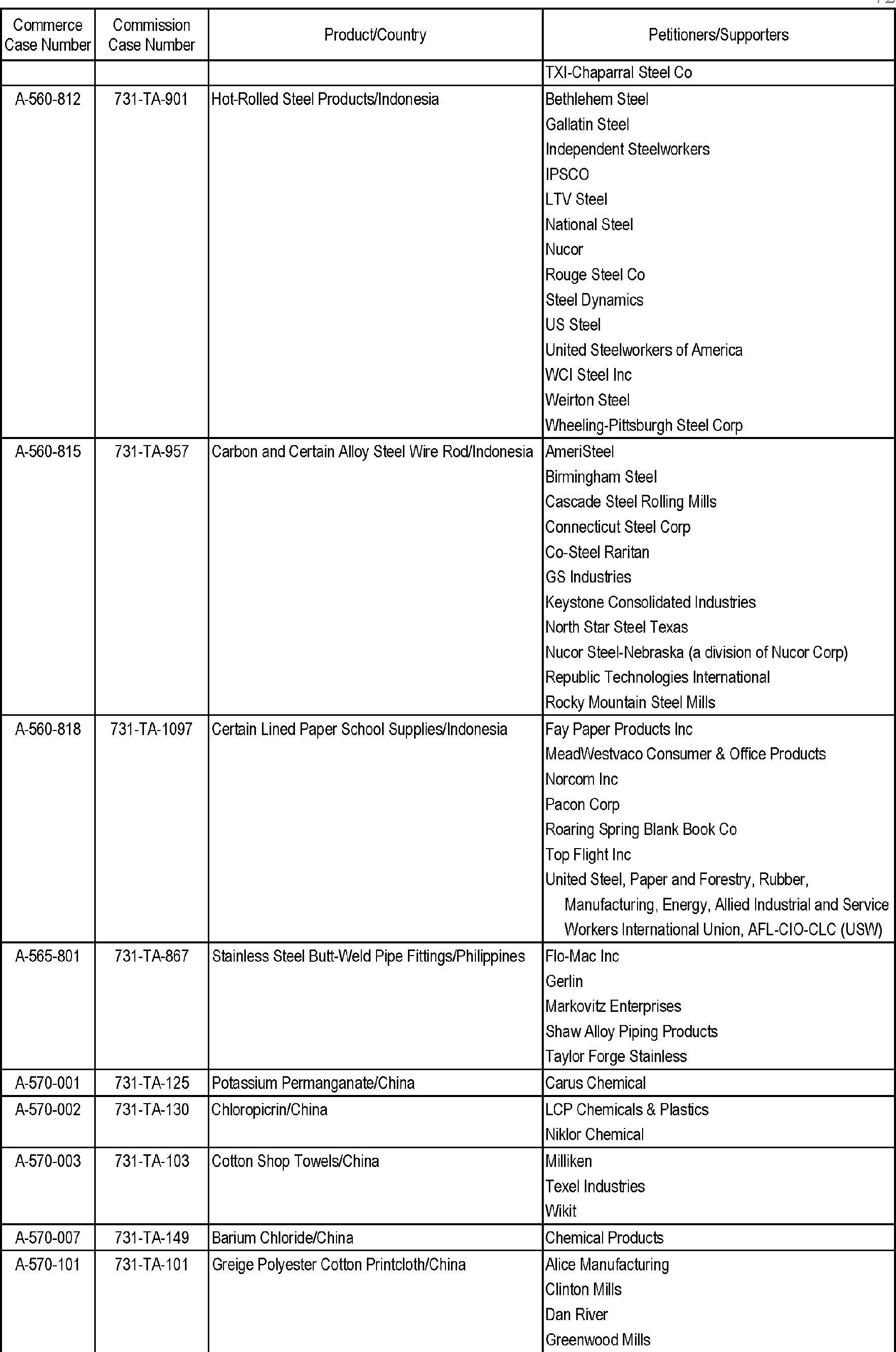

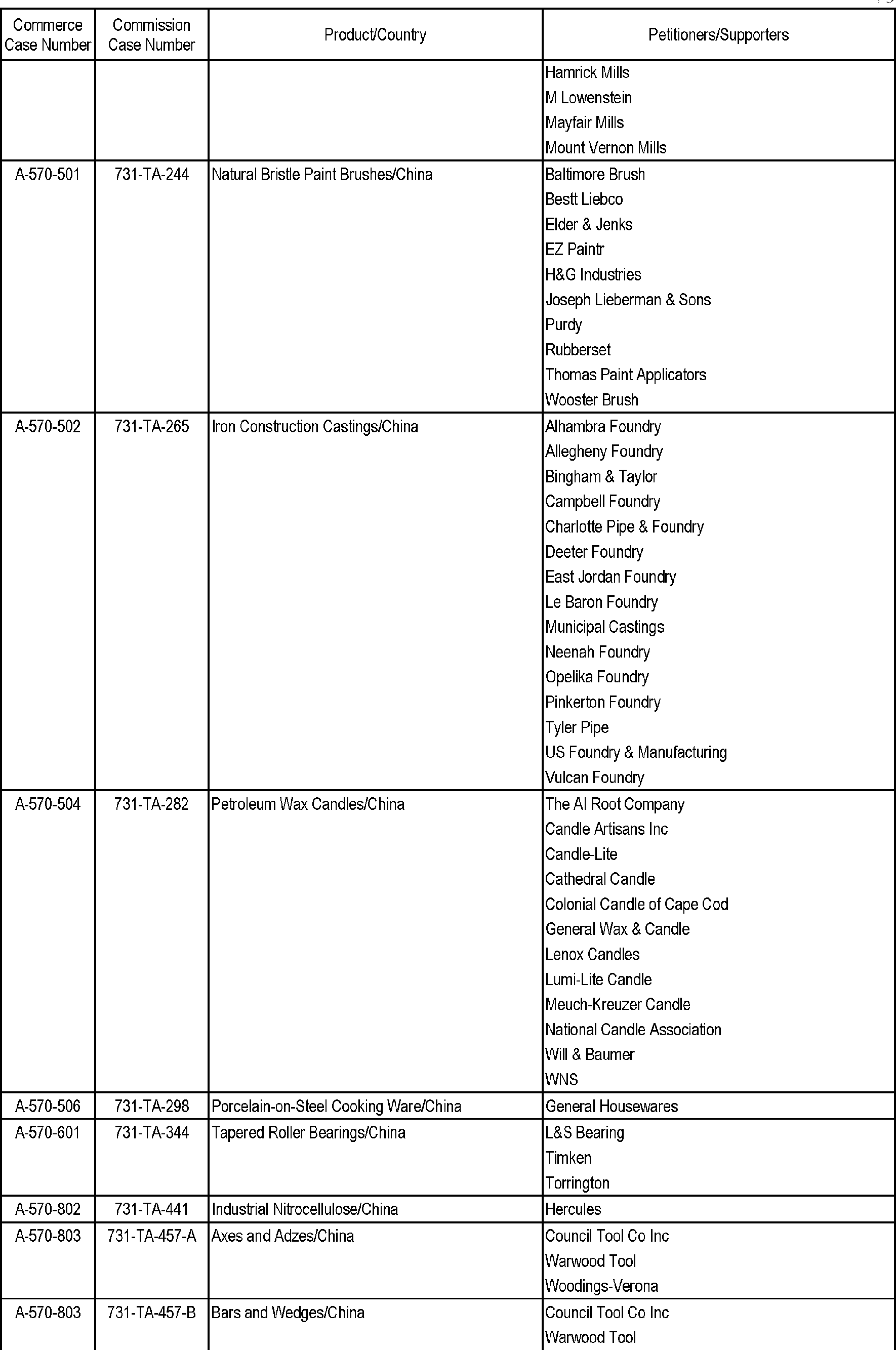

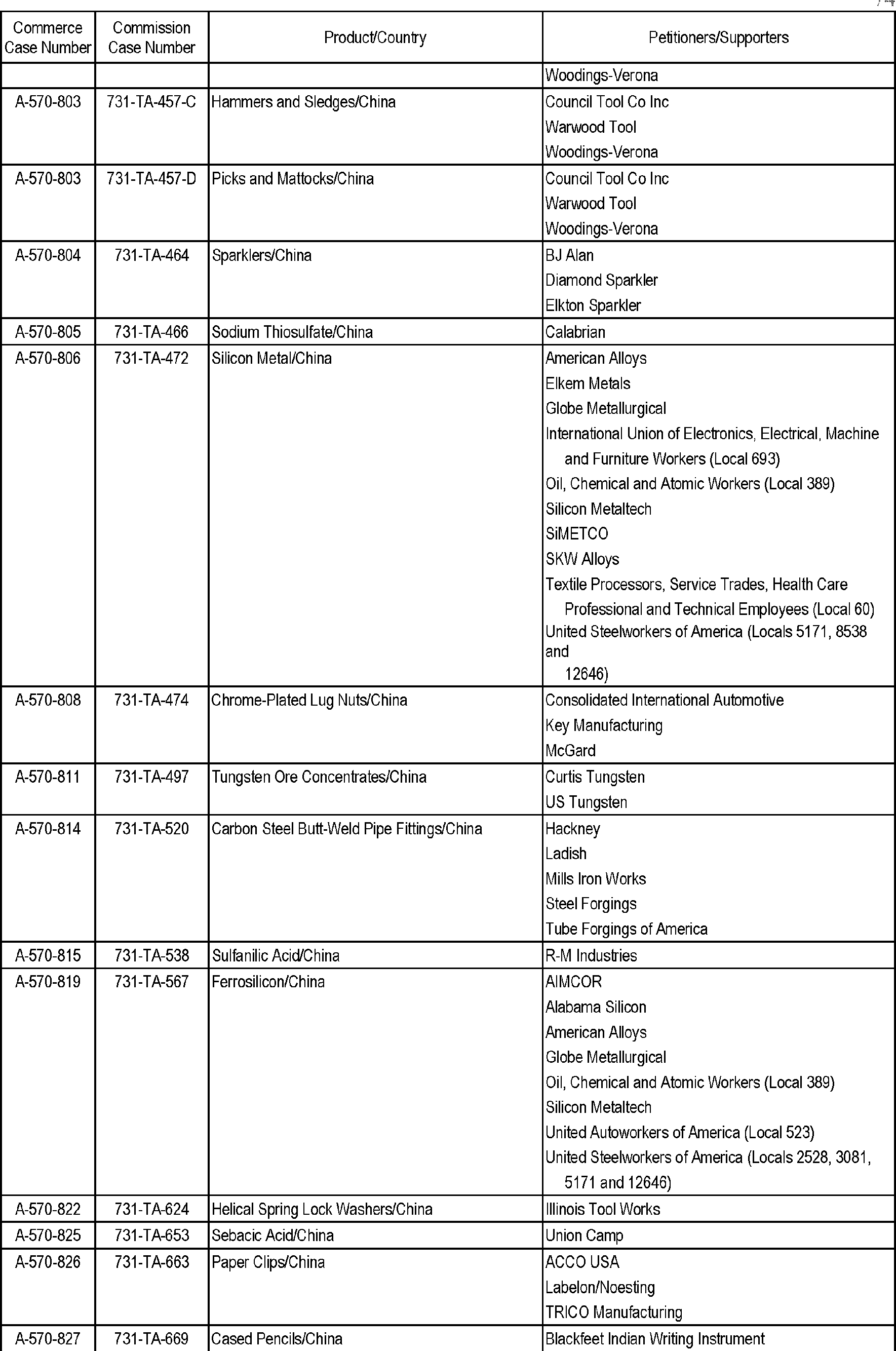

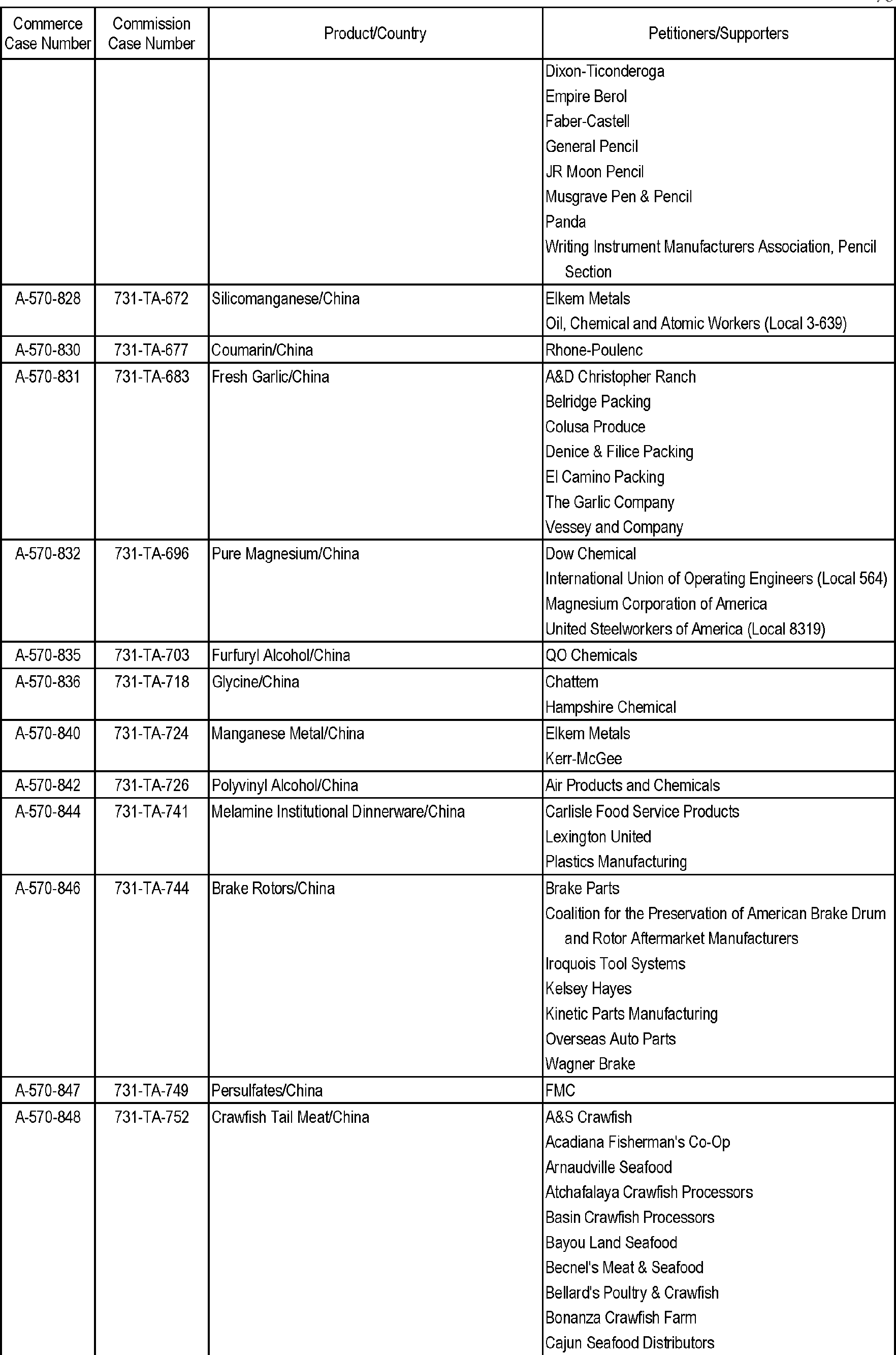

List of Orders and Findings and Related Domestic Producers

The list of individual antidumping duty orders and findings and countervailing duty orders is set forth below together with the affected domestic producers associated with each order or finding who are potentially eligible to receive an offset. Those domestic producers not on the list must allege another basis for eligibility in their certification. Appearance of a domestic producer on the list is not a guarantee of distribution.

Jeffrey Caine,

Chief Financial Officer, U.S. Customs and Border Protection.

Use this for formal legal and research references to the published document.

91 FR 30804

Web Citation

Suggested Web Citation

Use this when citing the archival web version of the document.

“Distribution of Continued Dumping and Subsidy Offset to Affected Domestic Producers,” thefederalregister.org (May 26, 2026), https://thefederalregister.org/documents/2026-10350/distribution-of-continued-dumping-and-subsidy-offset-to-affected-domestic-producers.