The Securities and Exchange Commission ("Commission") is proposing amendments that are intended to facilitate capital formation in the public securities markets. Specifically, t...

The Securities and Exchange Commission (“Commission”) is proposing amendments that are intended to facilitate capital formation in the public securities markets. Specifically, the proposed amendments would make Form S-3 and the ability to conduct shelf offerings available to significantly more issuers, extend certain benefits currently reserved for “well-known seasoned issuers” to a broader set of issuers, and modernize Form S-1 by expanding the ability to incorporate information by reference into that form. The proposed amendments also would make conforming changes to the registration, communication, and offering process for certain business development companies and registered closed-end investment companies that register securities on Form N-2. We also are proposing to amend the communication rules to permit broad-based advertising for certain insurance products. In addition, we are proposing certain other amendments that are intended to modernize certain rules. Finally, to mitigate the costs and complexity of conducting a registered offering, the proposed amendments would preempt State securities law registration and qualification requirements for all registered offerings.

DATES:

Comments should be received on or before July 27, 2026.

ADDRESSES:

Comments may be submitted by any of the following methods:

Send an email torule-comments@sec.gov.

Please include File Number S7-2026-17 on the subject line.

Paper Comments

Send paper comments to Vanessa A. Countryman, Secretary, Securities and Exchange Commission, 100 F Street NE, Washington, DC 20549-1090.

All submissions should refer to File Number S7-2026-17. This file number should be included on the subject line if email is used. To help the Commission process and review your comments more efficiently, please use only one method of submission. The Commission will post all submitted comments on the Commission's website (

https://www.sec.gov/rules-regulations/public-comments/s7-2026-17). Do not include personally identifiable information in submissions; you should submit only information that you wish to make available publicly. The Commission may redact in part or withhold entirely from publication submitted material that is obscene or subject to copyright protection.

Studies, memoranda, or other substantive items may be added by the Commission or staff to the comment file during this rulemaking. A notification of the inclusion in the comment file of any such materials will be made available on the Commission's website. To ensure direct electronic receipt of such notifications, sign up through the “Stay Connected” option at

www.sec.gov

to receive notifications by email.

Mark W. Green, Senior Special Counsel, or Isabel Rivera, Special Counsel, Office of Rulemaking, Division of Corporation Finance, at (202) 551-3430, Matt McNair, Senior Adviser to the Chief Counsel, Office of Chief Counsel, Division of Corporation Finance, at (202) 551-3500, Pamela Ellis, Senior Counsel; Blair Burnett, Bradley Gude, Branch Chiefs; or Brian McLaughlin Johnson, Assistant Director, at (202) 551-6792, Investment Company Regulation Office, Division of Investment Management; U.S. Securities and Exchange Commission, 100 F Street NE, Washington, DC 20549.

SUPPLEMENTARY INFORMATION:

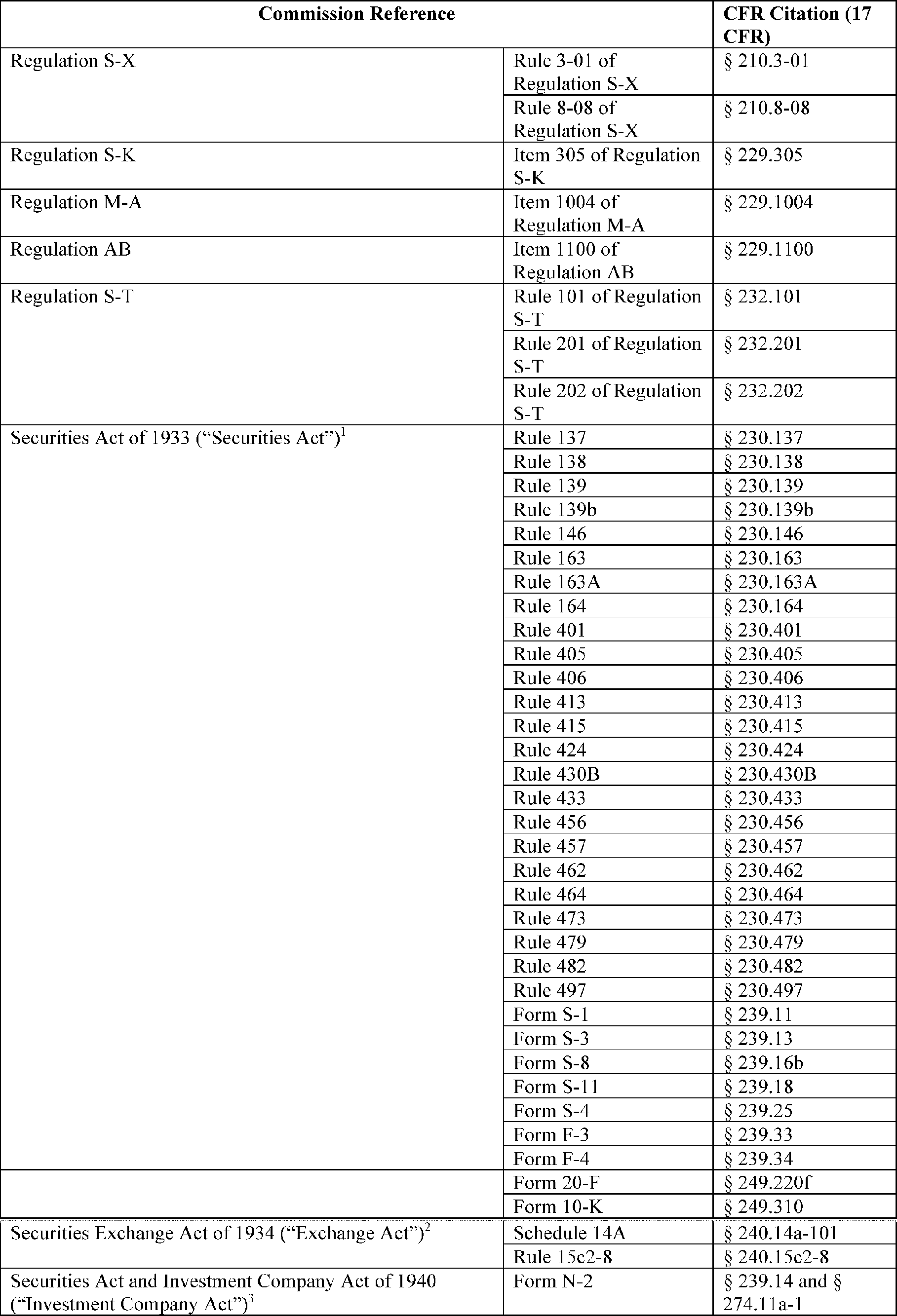

We are proposing to amend the following rules and forms:

( printed page 31023)

( printed page 31024)

Table of Contents

I. Introduction

A. Overview of the Proposed Amendments

B. Eliminating Public Float Requirements and Other Indicia of Market Following

II. Discussion of Proposed Amendments

A. Form S-3

1. Background

2. Proposed Amendments

B. The Enhanced Registration and Communication Benefits

1. Background

2. Proposed Amendments

C. Form S-1

1. Background

2. Proposed Amendments

D. Business Development Companies and Closed-End Funds

1. Background

2. Proposed Amendments

E. Registered Non-Variable Annuity Advertising

1. Background

2. Proposed Amendments

F. Preemption of State Securities Law Registration and Qualification

1. Background

2. Proposed Amendments

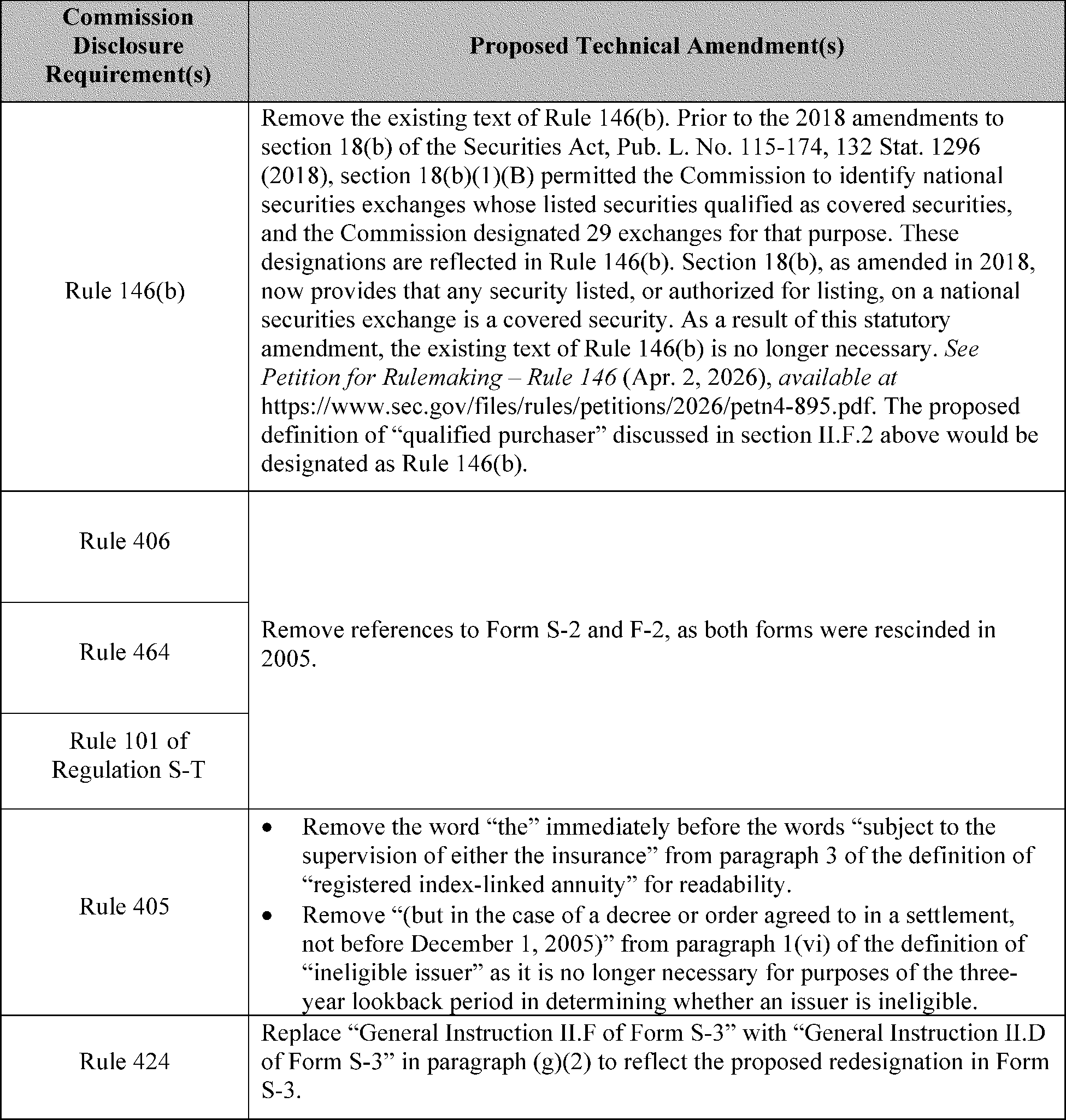

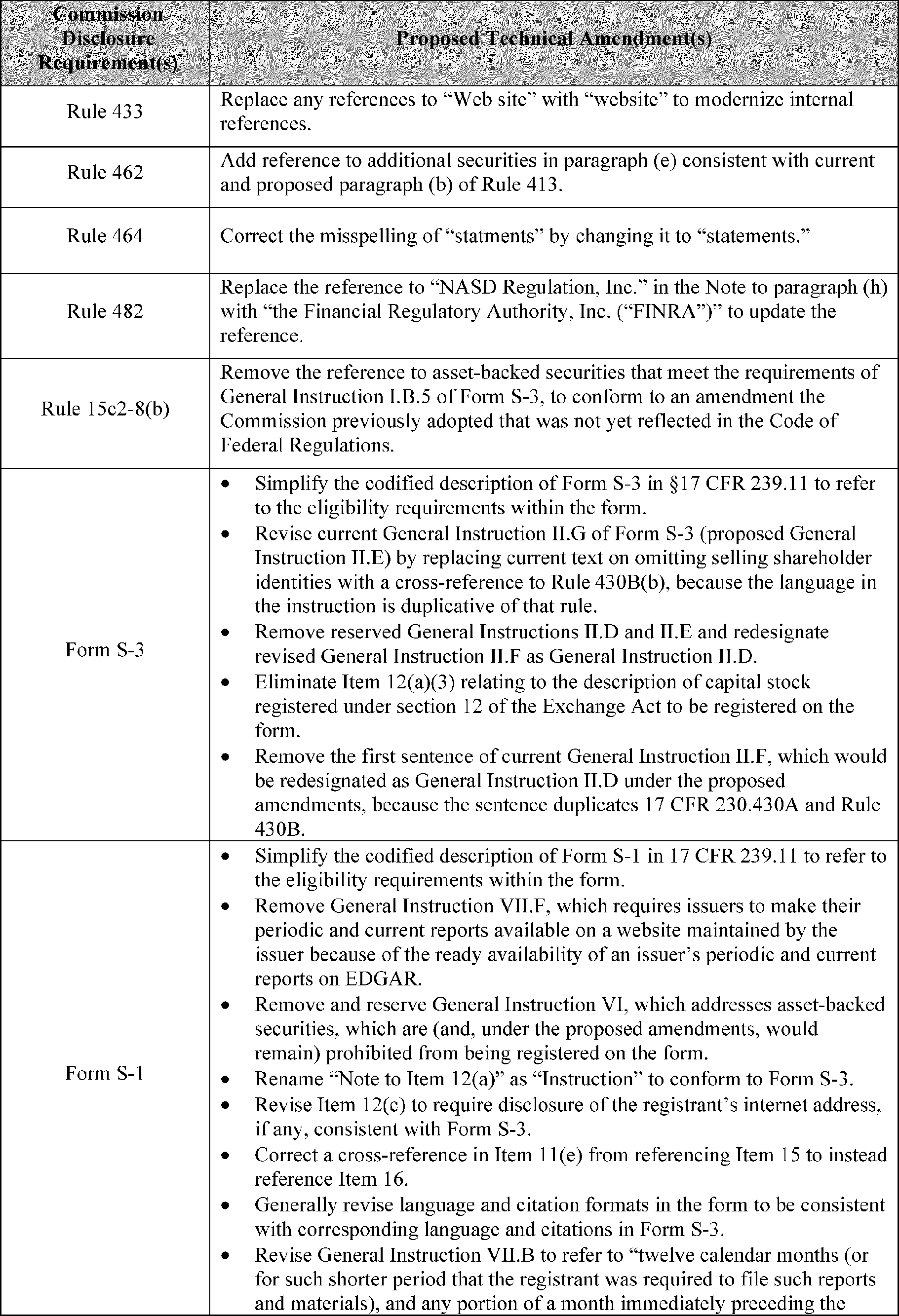

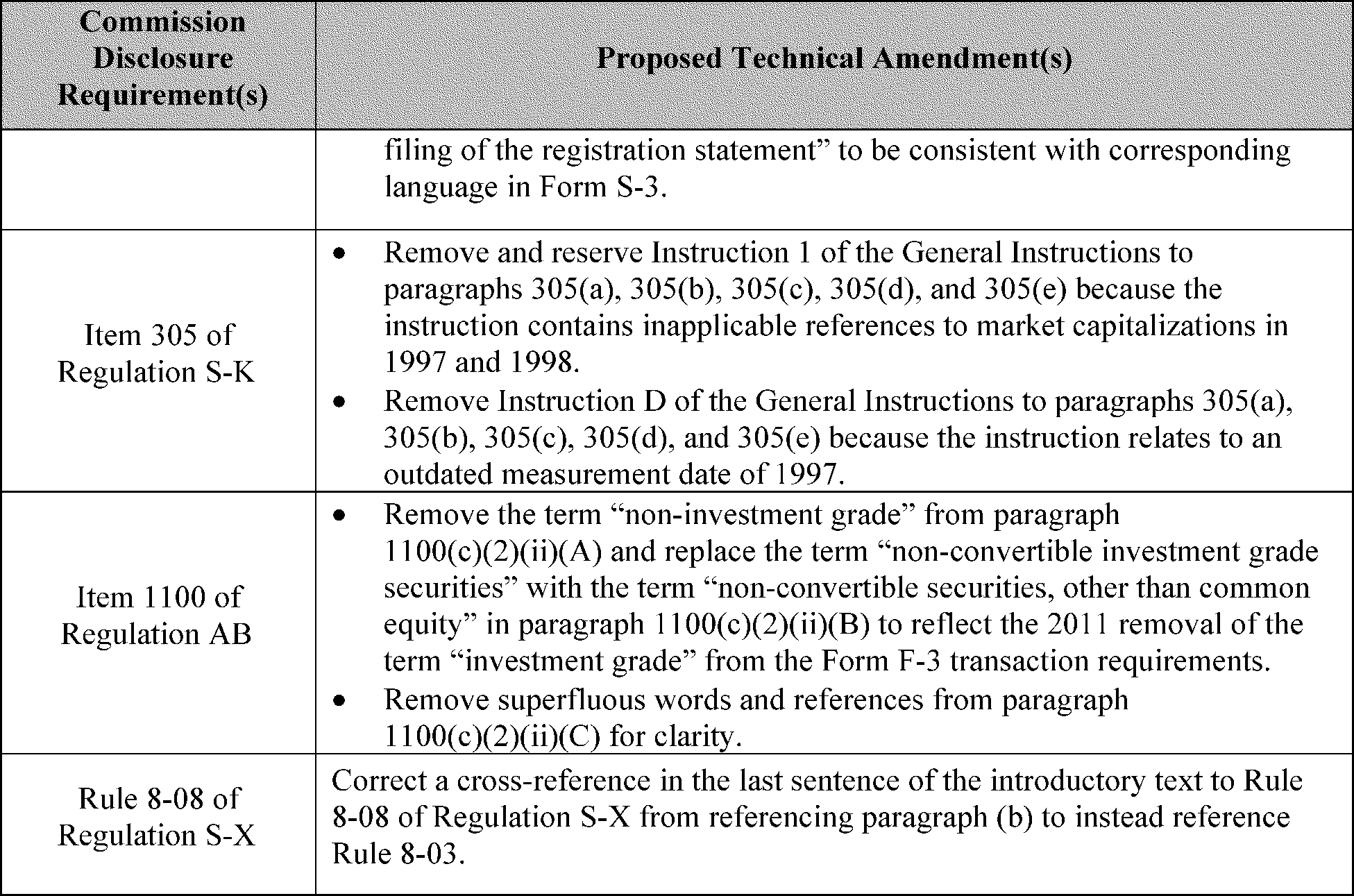

G. Other Rule Amendments

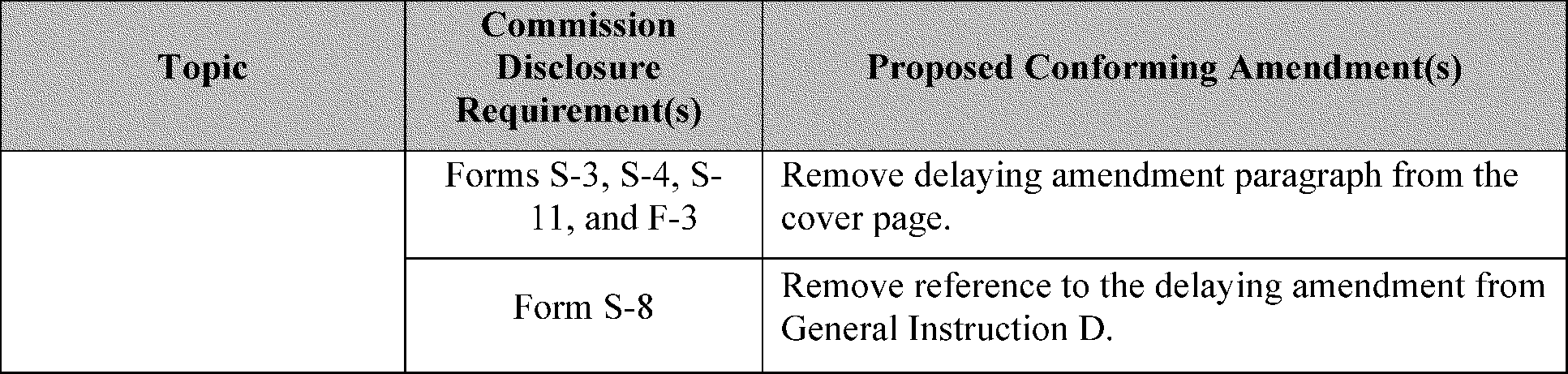

1. Delaying Amendments

2. Elimination of Certain Conditions Relating to Age of Financial Statements

3. Conforming and Technical Amendments

III. Other Matters

IV. Economic Analysis

A. Overview

B. Baseline

1. Form S-1 and Form S-3 Issuers

2. Form N-2 and Insurance Company Issuers

C. Benefits and Costs

1. Benefits and Costs of Proposed Amendments to Form S-3 Eligibility

2. Benefits and Costs of Amendments to Eligibility for the Enhanced Registration and Communication Benefits

3. Benefits and Costs of Amendments to Incorporation by Reference in Form S-1

4. Benefits and Costs of Amendments to Preempt State Regulation and Qualification

5. Business Development Companies, Closed-End Funds, and Registered Non-Variable Annuity Advertising

6. Benefits and Costs of Proposed Amendments to Rule 473 and Regulation S-X

7. Other Commission Proposals

8. Aggregate Monetized Benefits and Costs

D. Effects on Efficiency, Capital Formation, and Competition

1. Effects on Efficiency

2. Effects on Capital Formation

3. Effects on Competition

E. Reasonable Alternatives

1. Retain and Modify the Public Float-Based Conditions for Form S-3 Eligibility and WKSI Status

2. Retain WKSI Definition and Use an Alternative Measure of Whether an Issuer is “Well-Known”

F. Request for Comment

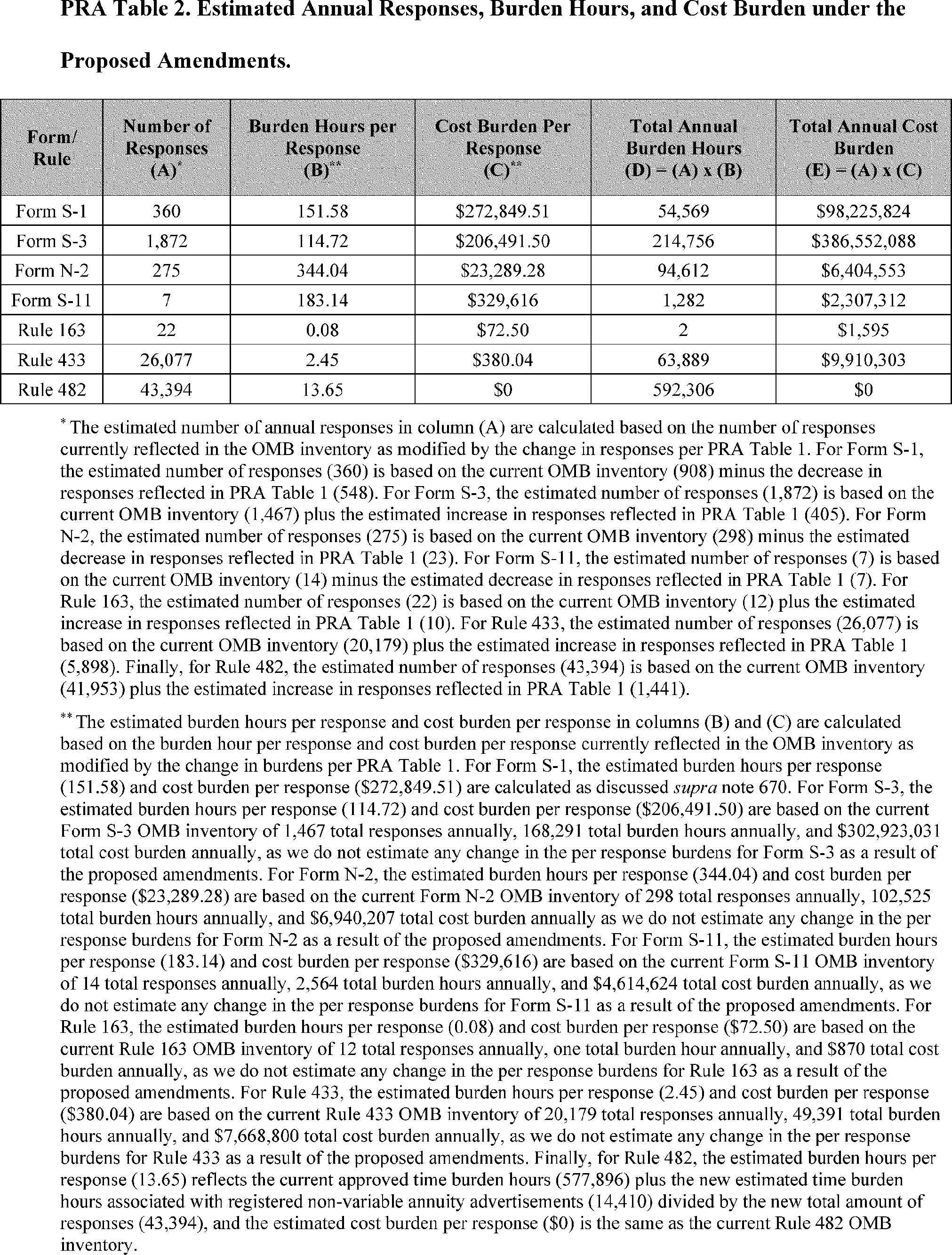

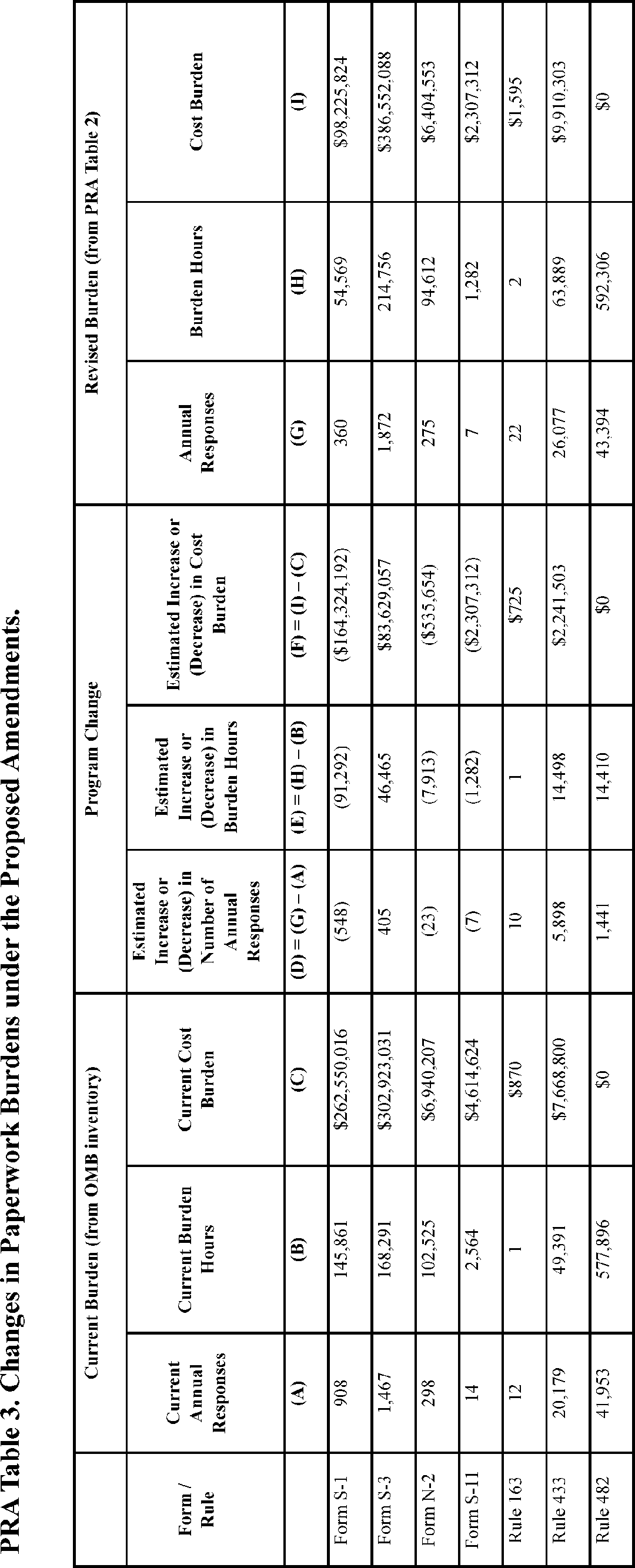

V. Paperwork Reduction Act

A. Summary of the Collections of Information

B. Summary of the Proposed Amendments' Estimated Effects on the Collections of Information

C. Incremental and Aggregate Burden and Cost Estimates

D. Request for Comment

VI. Congressional Review Act

VII. Initial Regulatory Flexibility Act Analysis and Regulatory Flexibility Act Certification

A. Initial Regulatory Flexibility Act Analysis

1. Reasons for, and Objectives of, the Proposed Action

2. Legal Basis

3. Small Entities Subject to the Proposed Amendments

4. Projected Reporting, Recordkeeping, and Other Compliance Requirements

5. Duplicate, Overlapping, or Conflicting Federal Rules

6. Significant Alternatives

B. Request for Comment

C. Certification Relating to Issuers of Registered Non-Variable Annuities

Statutory Authority

I. Introduction

We are proposing amendments that are intended to facilitate capital formation in the public securities markets. To achieve that goal, the proposed amendments would amend certain of our Securities Act rules and forms to provide issuers with greater flexibility to determine the timing and structure of their registered offerings and reduce the costs of conducting a registered offering by, among other things, simplifying and modernizing the applicable rules and forms.[4]

The Commission's longstanding, three-part mission is to protect investors, maintain fair, orderly, and efficient markets, and facilitate capital formation. Over the years, the Commission has engaged in various rulemakings with the express goal of facilitating capital formation.[5]

Some of those rulemakings focused specifically on facilitating capital formation with respect to registered offerings.[6]

As the Commission has recognized, the public capital markets offer several benefits to issuers and investors alike.[7]

For

( printed page 31025)

example, the Commission has noted that issuers can raise capital through the public markets on more favorable terms as compared to the private markets.[8]

This is due, in large part, to the “substantial pricing discounts that private investors often demand to compensate them for the relative illiquidity of the restricted shares they are purchasing” in exempt offerings.[9]

Both issuers and their investors benefit from this characteristic of the public markets because investors “may be less subject to the risk of dilution in the value of their shares if the companies in which they invest are able to meet more of their capital needs in the public markets.” [10]

Investors in registered offerings also enjoy additional benefits and protections. As compared to exempt offerings, issuers conducting registered offerings are required to provide their investors with more robust disclosures, and those disclosures are subject to enhanced liability standards.[11]

Although these requirements may increase compliance costs and litigation risks for issuers, those issuers ultimately may benefit from a lower cost of capital due, in part, to investors' reduced risk perception with respect to registered offerings.[12]

When pursuing the goal of facilitating capital formation, the Commission also has sought to ensure investors remain appropriately protected.[13]

To the extent there is a trade-off between efforts to facilitate capital formation and protect investors, the Commission has calibrated its rules with an eye towards balancing those two goals.

This proposal is intended to achieve the benefits associated with increased capital formation in the public securities markets. At the same time, we are committed to ensuring that investors remain appropriately protected. We recognize, however, that several aspects of our current Securities Act rules and forms, while intended to help protect investors at the time they were adopted, may now have the unintended effect of unduly inhibiting capital formation in today's markets. We believe, therefore, that it is appropriate to recalibrate certain of our rules and forms to ensure that they do not unduly restrict issuers' abilities to raise capital in a timely, efficient manner via a registered offering.

A. Overview of the Proposed Amendments

As discussed in more detail in section II below, the proposed amendments can be separated into several categories. First, we are proposing to revise Form S-3's eligibility requirements to allow a broader range of issuers to conduct offerings using the form, including delayed primary offerings (which, for purposes of this release, we refer to as “shelf offerings”) [14]

and at the market (“ATM”) primary offerings. Notably, the proposed amendments would eliminate the following eligibility requirements in Form S-3:

The issuer must have filed all the material required to be filed pursuant to section 13, 14, or 15(d) of the Exchange Act for a period of at least 12 calendar months immediately preceding the filing of the registration statement (which we refer to as the “One-Year Seasoning” requirement); and

The aggregate value of the issuer's voting and non-voting common equity held by non-affiliates (i.e.,

“public float”) must be $75 million or more to offer an unlimited amount of securities on Form S-3.[15]

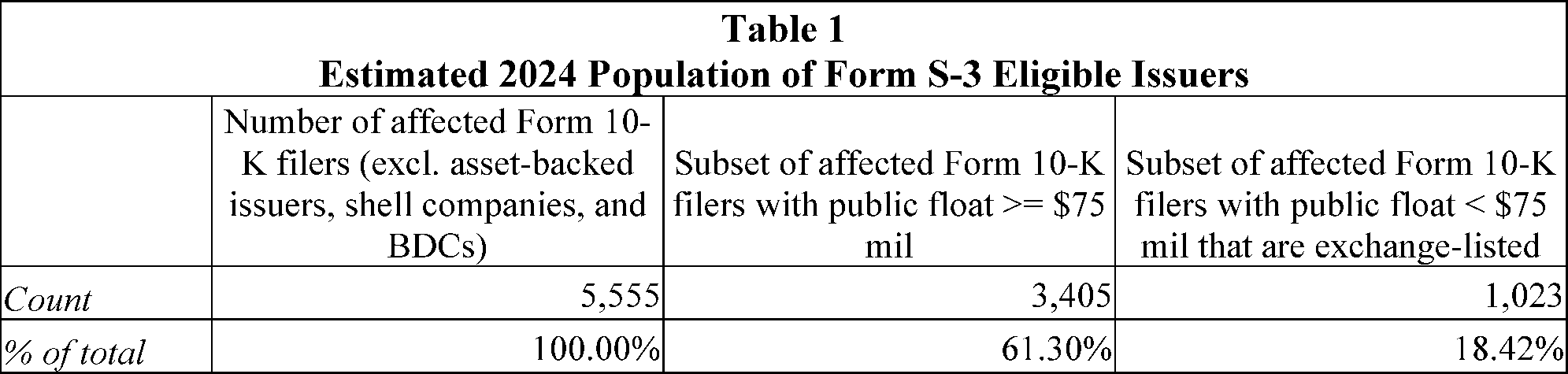

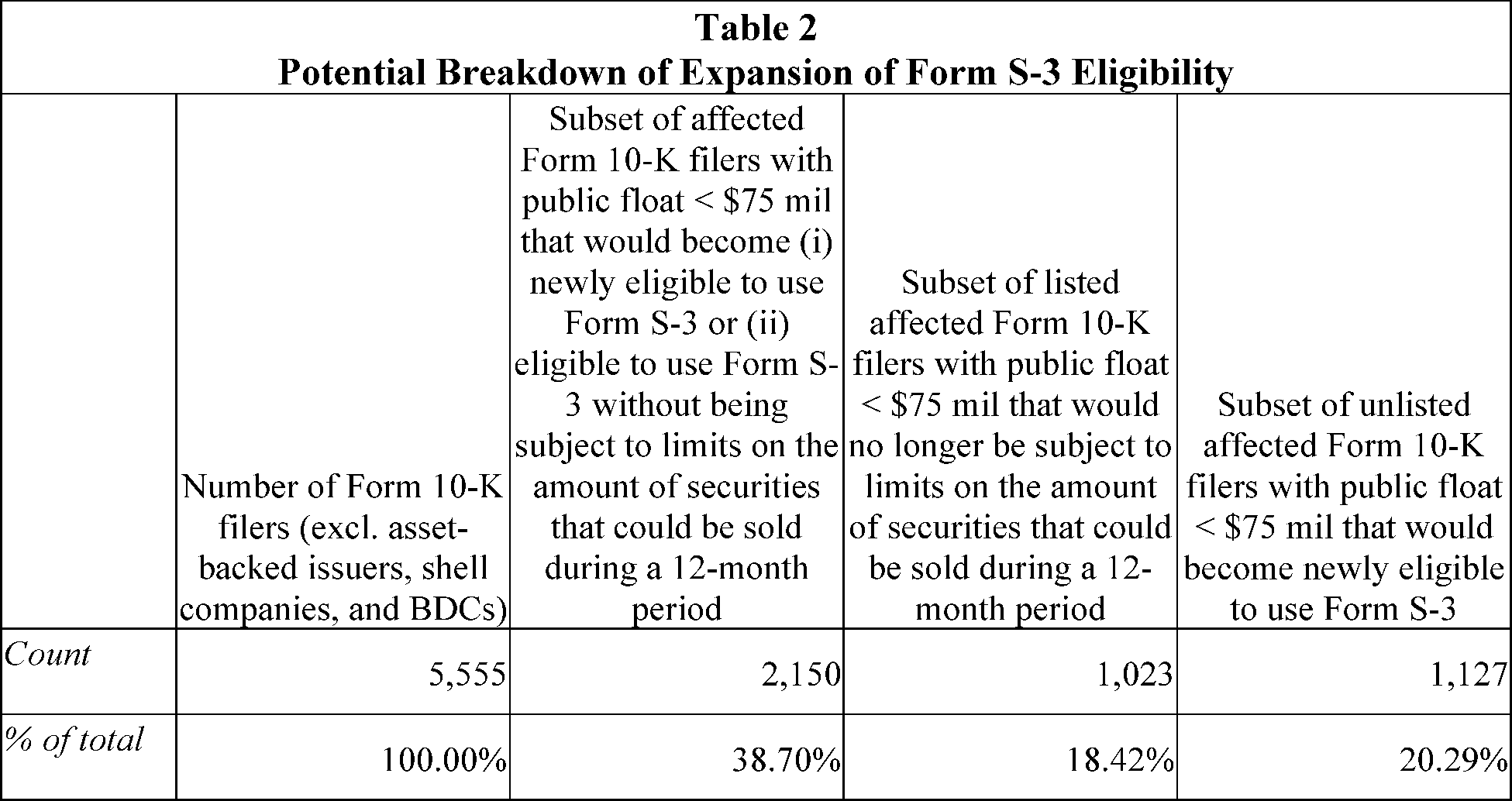

These proposed changes would significantly expand the population of issuers eligible to offer an unlimited amount of securities on Form S-3. Specifically, we estimate that there could be an increase of over 60 percent in the number of issuers eligible to offer an unlimited amount of securities on Form S-3.[16]

As discussed in section II.A below, these newly eligible issuers would benefit from the cost savings and capital raising efficiencies and flexibilities associated with the ability to use Form S-3 and conduct shelf offerings.

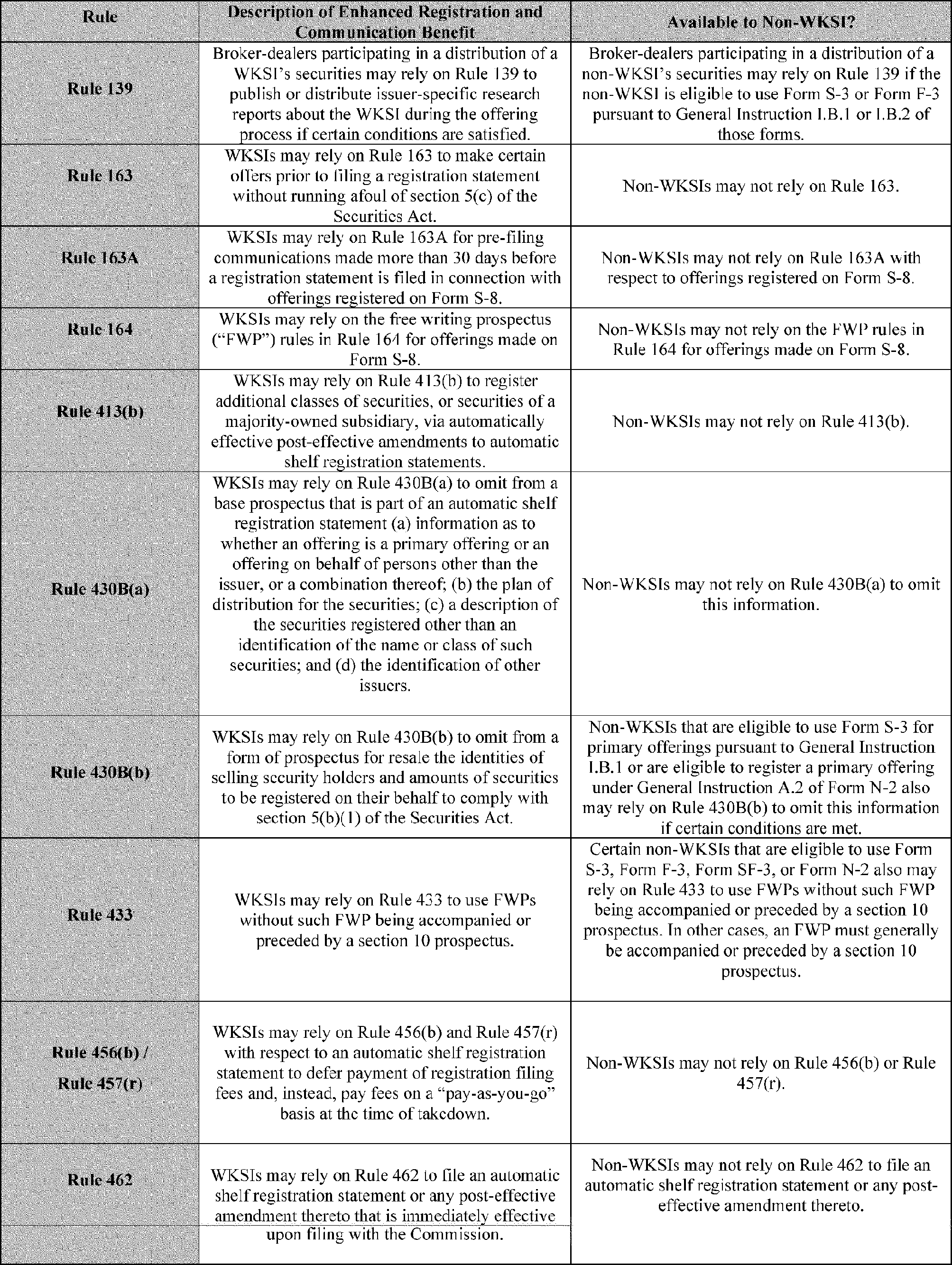

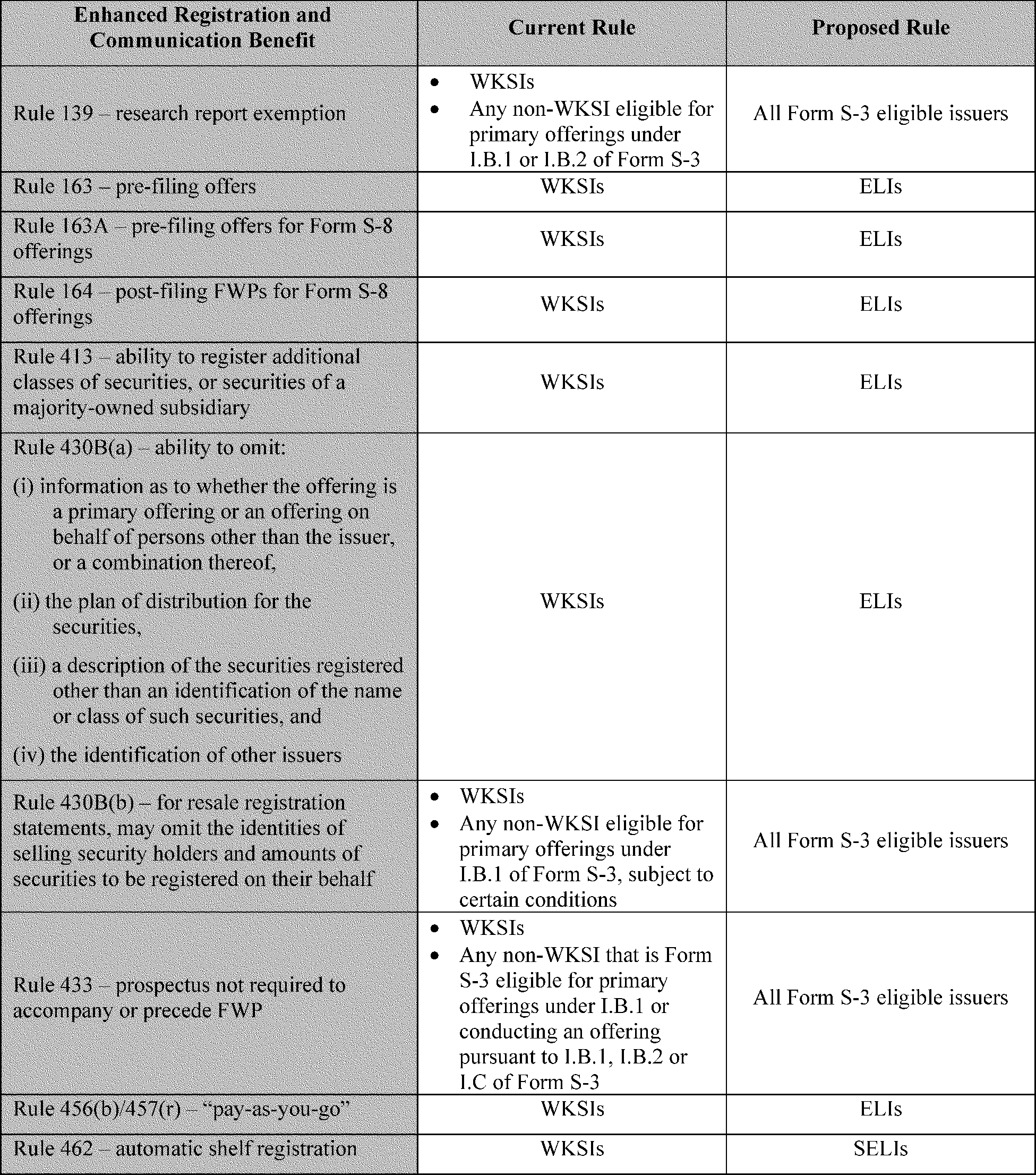

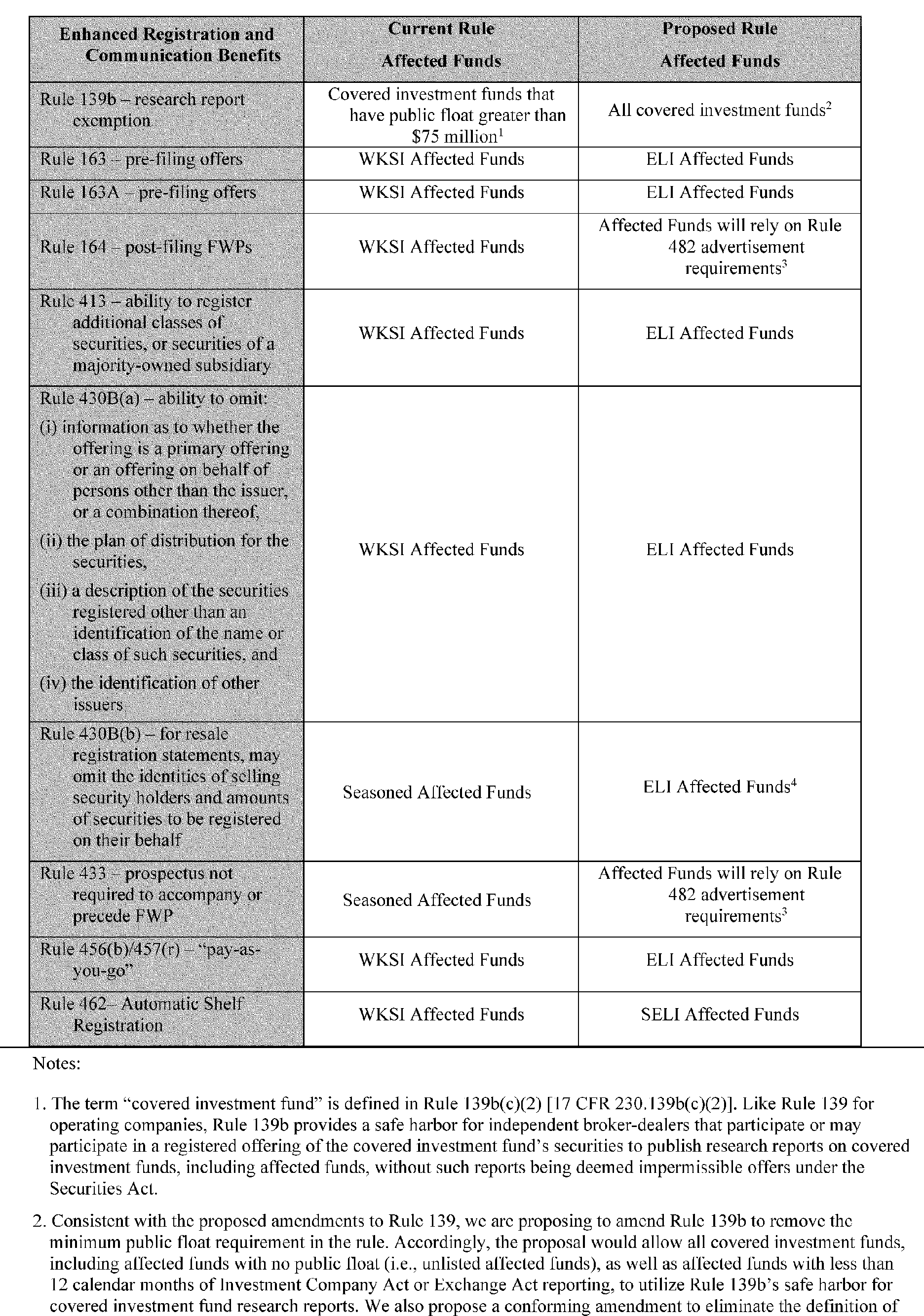

Second, we are proposing to extend certain benefits currently reserved for “well-known seasoned issuers” (“WKSIs”) and other seasoned issuers (which we refer to as the “Enhanced Registration and Communication Benefits”) to a larger set of issuers.[17]

Those benefits, which are discussed in section II.B below, are intended to further the Commission's longstanding goal of “facilitat[ing] capital formation, and possibly lower[ing] the cost of

( printed page 31026)

capital, by improving access to the public capital markets.” [18]

Currently, in order to be a WKSI (and, in turn, qualify for all of the Enhanced Registration and Communication Benefits), an issuer must, among other things, either have a public float of $700 million or more or have issued at least $1 billion aggregate principal amount of non-convertible securities, other than common equity, in primary offerings for cash, not exchange, registered under the Securities Act. Under the proposed amendments, issuers would not be required to meet either of these metrics in order to qualify for the Enhanced Registration and Communication Benefits. Instead, under the proposed amendments, issuers generally would qualify for those benefits if they are eligible to use Form S-3 and have at least one class of common equity securities listed on a national securities exchange.[19]

Thus, as a result of the proposed amendments, we estimate that there could be an increase of over 200 percent in the number of issuers eligible for all of the Enhanced Registration and Communication Benefits.[20]

Third, we are proposing to revise Form S-1 to expand issuers' abilities to incorporate by reference information filed before (

i.e.,

backward incorporation by reference) and after (

i.e.,

forward incorporation by reference) the effective date of the registration statement. As discussed in section II.C below, the ability to backward incorporate currently is limited to issuers that, among other things, have filed an annual report for their most recently completed fiscal year. The ability to forward incorporate currently is limited to issuers that, among other things, are smaller reporting companies (“SRCs”).[21]

Under the proposed amendments, issuers that meet Form S-1's requirements to incorporate by reference would be able to backward incorporate regardless of whether they had filed an annual report for their most recently completed fiscal year and forward incorporate regardless of whether they are an SRC. This would allow a greater number of issuers to enjoy the cost savings associated with incorporation by reference, with an estimated increase of up to 106 percent in the number of issuers eligible to forward incorporate on Form S-1.[22]

Fourth, in addition to the proposed amendments to the registration process for issuers that register securities on Form S-1 and Form S-3, we are also proposing to modify the registration, communication, and offering process for certain business development companies (“BDCs”) and registered closed-end investment companies (“registered CEFs”, collectively with BDCs, “affected funds”) that register securities on Form N-2, broadening their access to shelf offerings and the Enhanced Registration and Communication Benefits. These amendments would allow a greater number of affected funds to raise capital more efficiently and would provide more affected funds flexibility to manage the timing of their offerings in response to market opportunities.

Fifth, we are proposing to amend Rule 482 and other related rules to permit broad-based advertising relating to certain insurance products as discussed in more detail in section II.E below.

Sixth, under section 18(b)(3) of the Securities Act,[23]

we are proposing to define “qualified purchaser” such that State securities law registration and qualification requirements would be preempted with respect to any registered offering. As discussed in section II.F below, such preemption currently applies to registered offerings in which the securities being offered and sold are listed or approved for listing on a national securities exchange. Preemption currently does not, however, apply to registered offerings of unlisted securities. The proposed amendment, therefore, would eliminate the costs associated with complying with numerous states' registration and qualification requirements for registered offerings of unlisted securities.

Finally, we are proposing certain other amendments that are intended to modernize our rules. We discuss those proposed amendments in section II.G below.[24]

We invite and encourage interested parties to submit comments on any aspect of the proposed amendments. When commenting, please include the reasoning in support of your position or recommendation and provide any supporting documentation or data.

B. Eliminating Public Float Requirements and Other Indicia of Market Following

As noted in section I.A above, the proposed amendments would overhaul the criteria used to determine whether an issuer can use Form S-3 or the Enhanced Registration and Communication Benefits. For example, the proposed amendments would eliminate the requirements that issuers exceed a specified public float or amount of registered debt issued threshold to be eligible to offer an unlimited amount of securities on Form S-3 or to qualify for all of the Enhanced Registration and Communication Benefits. The proposed amendments also would eliminate the One-Year Seasoning requirement for Form S-3 eligibility.

These proposed amendments are intended to expand the population of issuers eligible to use Form S-3 and the Enhanced Registration and Communication Benefits. As discussed in section II.A.1 below, this goal is consistent with several prior Commission rulemakings. We recognize, however, that the proposed amendments also would, in many ways, represent a departure from the Commission's historical approach. An issuer's eligibility to use Form S-3 has, since the form's inception, depended on whether the issuer satisfies the Exchange Act seasoning and minimum public float requirements.[25]

Similarly, since the Commission adopted the Enhanced Registration and

( printed page 31027)

Communication Benefits, an issuer's ability to use those benefits has been conditioned, in part, on whether the issuer exceeds either a minimum public float or amount of registered debt issued threshold.[26]

In adopting rules and forms permitting short-form and shelf registration and the Enhanced Registration and Communication Benefits, and in periodically reconsidering the requirements issuers must meet to qualify for some of those benefits, the Commission has sought to reduce issuers' costs of raising capital while maintaining investor protection.[27]

The proposed amendments are intended to reflect the Commission's experience since it adopted or last amended the rules, including a reassessment of how best to protect investors in a manner that does not unduly limit issuers' access to short-form and shelf registration and the Enhanced Registration and Communication Benefits.

As the Commission has previously recognized, public securities offerings provide investors with benefits and protections not available in the private markets. The existing eligibility requirements, including the One-Year Seasoning and public float requirements, are intended to protect investors. Those eligibility requirements, however, also limit the number of issuers that may utilize Form S-3 and the Enhanced Registration and Communication Benefits, thus prompting some issuers to raise capital through other means, such as an exempt offering or private financing, in lieu of conducting a registered offering. Because registered offerings often ultimately benefit issuers and investors alike, we believe it is appropriate to expand significantly the population of issuers eligible to use Form S-3, conduct shelf and ATM offerings, and qualify for the Enhanced Registration and Communication Benefits so as to encourage more registered offerings, provided that appropriate investor protections are maintained.

The proposed changes to these eligibility requirements also are intended to reflect technological advancements and developments in the financial markets since the Commission adopted short-form registration, shelf registration, and the Enhanced Registration and Communication Benefits. The Commission has stated that the eligibility criteria in Form S-3 “are based on the Commission's belief that information about companies using the form already is known or is so readily available that it need not be repeated in a prospectus.” [28]

The Commission historically relied on that criteria—in particular, the Exchange Act reporting history and minimum public float requirements—as indicia of whether an issuer was widely followed and, in turn, whether information about the issuer had been sufficiently disseminated into the marketplace such that short-form registration was appropriate.[29]

The Commission relied on a similar rationale in conditioning the ability to use the Enhanced Registration and Communication Benefits on an issuer's ability to meet the specified public float or registered debt thresholds.[30]

When short-form registration was first introduced in 1967, Commission filings were submitted and available only in paper copy. The Commission attempted to facilitate broader distribution of this information by contracting with an outside company to create and distribute microfiche copies to designated Commission public reference rooms,[31]

but obtaining copies of these documents was cumbersome and expensive. Notably, an individual had to either make paper copies in the Commission's public reference rooms or order copies from service bureaus which, in turn, had to make and sell paper copies as requested.[32]

Thus, because it was difficult for investors to obtain information about an issuer, the Commission sought to ensure that, for companies using short-form registration, there was “wide dissemination of information about such companies in the market place” and that “securities analysts [would] follow companies of this size.” [33]

In the intervening years, technological developments have transformed how information is disseminated into the marketplace and facilitated widespread access to issuer information. For example, issuers today must make their Commission filings electronically through the Commission's Electronic Data Gathering, Analysis, and Retrieval system (“EDGAR”),[34]

which makes these filings immediately available to the investing public without charge.[35]

In addition, corporate news is disseminated in an electronic world, and issuers today make their Commission filings and other company information available through recognized electronic channels of distribution, including their websites and other digital technologies. Today's investors can access and follow publicly filed information about an issuer for low or no cost in real time and on demand.

Further, although Commission filings have been available to the investing public electronically, free of charge, through EDGAR since the mid-1990s and were available to investors in 2005 when the Commission adopted the Enhanced Registration and Communication Benefits and in 2007 when the Commission last considered eliminating the public float requirement

( printed page 31028)

in Form S-3,[36]

we believe such information has become even more widely accessible in the intervening years. Whereas only 71 percent of U.S. adults used the internet in 2007 and only 47 percent had a broadband connection at home,[37]

today 96 percent use the internet and 79 percent have a broadband connection at home.[38]

In addition, today approximately 91 percent of Americans own a smartphone compared to just 35 percent in 2011.[39]

Thus, a greater number of investors can retrieve investment information from nearly anywhere and nearly anytime. Moreover, the Commission improved investor access to this information in 2019 by requiring active hyperlinks to information incorporated by reference into registration statements and prospectuses.[40]

As a result, today's investors can now more easily and rapidly access Commission filings on EDGAR and via issuer websites, as well as other issuer-related information that is available through other electronic channels, at significantly lower cost than in the past.[41]

Because of the ease with which investors may obtain Exchange Act disclosure documents and other information about an issuer, we believe that eligibility to use Form S-3 and the Enhanced Registration and Communication Benefits should not depend on the extent of an issuer's market following, including analyst coverage (

e.g.,

by reference to its public float or initial Exchange Act seasoning).[42]

Instead, we believe a more appropriate criterion is whether investors can readily obtain issuer-specific information that is incorporated by reference into a prospectus and the related registration statement to make an informed investment decision. If an issuer is current and timely with respect to its Exchange Act reporting obligations, then an investor's ability to obtain such issuer-specific information will not depend on the length of the issuer's Exchange Act reporting history or the amount of the issuer's public float. In the pre-EDGAR era, it may have been important to include eligibility requirements for short-form registration that “assure[d] that sufficient information about registrants using the form [was] available to the investing public through the Exchange Act reporting system.” [43]

Today, however, the public availability of all issuers' Exchange Act reports in EDGAR effectively addresses the concerns that animated those requirements. We believe, therefore, that eligibility for Form S-3 and the Enhanced Registration and Communication Benefits no longer should be conditioned on an issuer's Exchange Act reporting history, public float, or amount of registered debt issued.

That said, consistent with the Commission's investor protection mandate, we are not proposing to expand eligibility to use Form S-3 or the Enhanced Registration and Communication Benefits to all issuers. For example, under the proposed amendments, issuers would be eligible to use most of the Enhanced Registration and Communication Benefits only if they are eligible to use Form S-3 and are exchange-listed. Further, although use of Form S-3 would not be conditioned on an issuer having satisfied the One-Year Seasoning requirement under the proposed amendments, use of the form would be conditioned on an issuer being current and timely with respect to all the material required to be filed pursuant to sections 13(a), 14(a), 14(c), and 15(d) of the Exchange Act during the preceding 12 calendar months, or such shorter period that the issuer was required to file such reports and materials. The proposed amendments also would prohibit issuers from using Form S-3 (and, therefore, the Enhanced Registration and Communication Benefits) if they are within a category of issuers we believe pose greater investor protection concerns, including those issuers that potentially present the highest risk of non-compliance with Securities Act and Exchange Act disclosure requirements. We discuss each of these aspects of the proposed amendments in more detail below.

II. Discussion of Proposed Amendments

A. Form S-3

We are proposing to amend Form S-3 to revise its eligibility requirements. In addition, we are proposing certain other amendments to Form S-3 that would simplify and modernize the form. Taken together, these proposed amendments are intended to allow a greater number of issuers the flexibility to access the public securities markets quickly by using Form S-3 while also ensuring that investors remain appropriately protected. Form S-3, as it would read under the proposed amendments, is attached to this release as Appendix B.

1. Background

a. Eligibility To Use Form S-3 and Conduct Shelf Offerings

Form S-3 is a short-form registration statement that eligible issuers can use to register offerings under the Securities Act. The ability to use Form S-3 can confer significant advantages on eligible companies seeking to raise capital through the public markets. Notably, an issuer that is Form S-3 eligible for primary offerings is permitted to conduct shelf offerings—that is, offerings made on a delayed basis—under Rule 415.[44]

Rule 415 provides

( printed page 31029)

issuers with considerable flexibility to access the public securities markets from time to time in response to changes in the market and the issuer's capital needs. Issuers that are eligible to conduct shelf offerings under Rule 415 are permitted to register securities offerings prior to planning any specific offering and, once the registration statement is effective, issue securities in one or more offerings without waiting for further Commission or staff action.

By having more control over the timing of their offerings, eligible issuers can take advantage of desirable market conditions, thus allowing them to raise capital on more favorable terms (such as a higher equity price or lower debt interest rate). As a result, the ability to sell securities “off the shelf” as needed gives issuers a financing alternative that may be more advantageous for them than other available methods, such as private placements with securities priced at discounted values based in part on their relative illiquidity.

One of the primary advantages of Form S-3 is the ability to omit from the prospectus included in a registration statement at the time of effectiveness (the “base prospectus”) certain information, including, for WKSIs, information as to whether an offering is a primary or secondary offering, the plan of distribution for the securities, a description of the securities to be offered other than an identification of the name or class of such securities, and the identification of other issuers.[45]

An issuer can instead provide this information at the time that it is actually conducting an offering, after its terms have been determined. The ability to omit information from the base prospectus at the time of effectiveness, therefore, enables issuers to conduct shelf offerings.

In addition, Form S-3 permits the required information to be backward and forward incorporated by reference to a company's disclosure in its Exchange Act filings. The ability to forward incorporate allows for automatic updating of the registration statement.[46]

By contrast, a company without the ability to forward incorporate must file a prospectus supplement to update information or, in certain cases, file a post-effective amendment to its registration statement to prevent information in the registration statement from becoming outdated and to update for fundamental changes to the information set forth in the registration statement.[47]

Issuers that are ineligible to file on Form S-3 often register their offerings on Form S-1, which has far fewer eligibility requirements than Form S-3.[48]

Issuers filing registration statements on Form S-1 are not permitted to register shelf offerings under Rule 415 and therefore cannot register securities in advance of an actual offering. Thus, as compared to conducting a shelf offering on Form S-3, it is more challenging (and, in some instances, likely not feasible) for Form S-1 registrants to take advantage of favorable market opportunities, as they must prepare and file a registration statement at the time of an expected offering and await Commission or staff action before offering or selling securities. Further, Form S-1 permits certain issuers to backward incorporate. Form S-1 currently does not, however, permit issuers other than SRCs to forward incorporate, which therefore requires a company to update the registration statement through prospectus supplements and post-effective amendments.[49]

To use Form S-3, an issuer must meet the form's registrant requirements,[50]

which generally pertain to the issuer's reporting history under the Exchange Act, as well as at least one of the form's transaction requirements.[51]

Form S-3's registrant requirements (which are enumerated in General Instruction I.A of Form S-3) specify that to use the form, an issuer must satisfy each of the following:

U.S. Issuer.

The issuer must be organized under the laws of the United States or any State or territory or the District of Columbia and have its principal business operations in the United States or its territories.[52]

Exchange Act Reporting.

The issuer must have a class of securities registered pursuant to section 12(b) or 12(g) of the Exchange Act or be required to file reports pursuant to section 15(d) of the Exchange Act.[53]

One-Year Seasoning.

The issuer must have been subject to the requirements of section 12 or 15(d) of the Exchange Act for a period of at least 12 calendar months immediately preceding the filing of the registration statement.[54]

Current in Exchange Act Reporting.

The issuer must have filed all the material required to be filed pursuant to section 13, 14, or 15(d) of the Exchange Act for a period of at least 12 calendar months immediately preceding the filing of the registration statement.[55]

Timely in Exchange Act Reporting.

The issuer must have filed in a timely manner all reports required to be filed during the 12 calendar months and any portion of a month immediately preceding the filing of the registration statement, other than specified reports on Form 8-K.[56]

Certain Failures to Make Payments and Defaults.

The issuer must have not, since the end of the last fiscal year for which certified financial statements of the issuer and its consolidated subsidiaries were included in a report filed pursuant to section 13(a) or 15(d) of the Exchange Act: (a) failed to pay any dividend or sinking fund installment on preferred stock; or (b) defaulted (i) on any installment or installments on indebtedness for borrowed money, or (ii) on any rental on one or more long-term leases, which defaults in the aggregate are material to the financial position of the issuer and its consolidated and unconsolidated subsidiaries, taken as a whole.[57]

Electronic Filings.

The issuer must have filed with the Commission all required electronic filings.[58]

Interactive Data Files.

The issuer must have submitted electronically to the Commission all Interactive Data

( printed page 31030)

Files [59]

required to be submitted pursuant to 17 CFR 232.405 during the 12 calendar months and any portion of a month immediately preceding the filing of the registration statement on Form S-3 (or for such shorter period of time that the issuer was required to submit such files).[60]

Foreign issuers, other than foreign governments, also can use Form S-3 if they satisfy all the registrant requirements, other than the “U.S. Issuer” eligibility requirement, and file the same Exchange Act reports as a domestic issuer.[61]

In addition, successor issuers are permitted to use Form S-3 if they meet certain conditions.[62]

Form S-3's transaction requirements (which are enumerated in General Instruction I.B of Form S-3) specify that the form can be used for primary offerings only under the following circumstances:

General Instruction I.B.1—Primary Offerings by Certain Registrants.

An issuer may register any primary offering of its securities on the form if, among other requirements, the issuer's public float is $75 million or more.

If an issuer does not have a public float of at least $75 million, it may nevertheless register the following primary offerings on Form S-3:

○

General Instruction I.B.2—Primary Offerings of Non-Convertible Securities Other than Common Equity.

An issuer may register a primary offering of non-convertible securities other than common equity, provided the issuer: (1) has issued at least $1 billion in non-convertible securities, other than common equity, in primary offerings for cash registered under the Securities Act over the prior three years; (2) has outstanding at least $750 million of non-convertible securities, other than common equity, issued in primary offerings for cash registered under the Securities Act; (3) is a wholly-owned subsidiary of a WKSI; or (4) is a majority-owned operating partnership of a real estate investment trust (“REIT”) that qualifies as a WKSI.

○

General Instruction I.B.4—Rights Offerings, Dividend or Interest Reinvestment Plans, and Conversions or Warrants and Options.

An issuer may register securities to be offered upon exercise of outstanding rights, under a dividend or interest reinvestment plan, or upon the conversion of outstanding convertible securities or the exercise of outstanding warrants or options, if certain conditions are met.

○

General Instruction I.B.6—Limited Primary Offerings by Certain Other Registrants.

An issuer that is not a shell company may register any primary offering if it is exchange-listed and the aggregate market value of securities sold by or on behalf of the issuer under the instruction during the 12 months immediately prior to, and including, the sale is no more than one-third of the issuer's public float.

Form S-3's transaction requirements specify that the form can be used for resale offerings only under the following circumstances:

General Instruction I.B.1—Primary Offerings by Certain Registrants.[63]

An issuer may register resales of outstanding securities if the issuer has a public float of at least $75 million.

General Instruction I.B.3—Transactions Involving Secondary Offerings.

If an issuer does not have a public float of at least $75 million, resales of outstanding securities can be registered on Form S-3 if the securities are listed on a national securities exchange or quoted on the automated quotation system of a national securities association.[64]

In addition, General Instruction I.B.5 provides that Form S-3 may not be used to register offerings of asset-backed securities, as defined in 17 CFR 229.1101(c).

Finally, Form S-3 has instructions that specify circumstances under which certain subsidiaries are eligible to use the form.[65]

In addition to the permissible offerings by subsidiaries identified in General Instruction I.B.2 (with respect to wholly-owned subsidiaries of WKSIs and majority-owned operating partnerships of REITs that qualify as WKSIs), General Instruction I.C provides that majority-owned subsidiaries may register certain offerings on Form S-3 if:

the issuer-subsidiary itself meets the registrant requirements and the applicable transaction requirement; [66]

the parent of the issuer-subsidiary meets the registrant requirements and the conditions of General Instruction I.B.2 are met; [67]

the parent of the issuer-subsidiary meets the registrant requirements and the applicable transaction requirement, and provides a full and unconditional guarantee, as defined in17 CFR 210.3-10 (“Rule 3-10 of Regulation S-X”), of the payment obligations on the securities being registered, and the securities being registered are non-convertible securities, other than common equity; [68]

the parent of the issuer-subsidiary meets the registrant requirements and the applicable transaction requirement, and the securities of the issuer-subsidiary being registered are full and unconditional guarantees, as defined in Rule 3-10 of Regulation S-X, of the payment obligations on the parent's non-convertible securities, other than common equity, being registered; [69]

or

the parent of the issuer-subsidiary meets the registrant requirements and the applicable transaction requirement, and the securities of the issuer-subsidiary being registered are guarantees of the payment obligations on the non-convertible securities, other than common equity, being registered by another majority-owned subsidiary of the parent where the parent provides a full and unconditional guarantee, as defined in Rule 3-10 of Regulation S-X, of such non-convertible securities.[70]

For convenience, throughout the remainder of this release, we refer to the offerings involving parent or subsidiary guarantees permitted under General Instructions I.C.3, I.C.4, and I.C.5 as “Guarantee-Related Offerings.”

b. History of Short-Form Registration

The Commission first introduced short-form registration “in the nature of

( printed page 31031)

an experiment” with Form S-7 in 1967.[71]

Unlike other forms, Form S-7 permitted eligible issuers to omit certain information about the issuer, such as property descriptions, pending legal proceedings, and director and executive compensation. To use the form, issuers had to have a class of equity securities registered under section 12(b) or (g) of the Exchange Act and had to be current and timely in their Exchange Act reporting for at least five years.[72]

Issuers also had to satisfy other qualitative criteria related to business continuity,[73]

board stability,[74]

solvency,[75]

financial performance,[76]

and dividend coverage.[77]

The rationale for this short-form registration statement was that the omitted information was already available through the issuer's Exchange Act reports, making its inclusion in the registration statement unnecessary.[78]

Over time, the Commission has periodically amended its rules and forms to broaden the availability of short-form registration and shelf offerings. In the Commission's 1969 Disclosure Policy Study led by Commissioner Francis Wheat (often referred to as the “Wheat Report”), the Commission recommended a “substantial expansion” of short-form registration.[79]

In response, the Commission broadened short-form eligibility by decreasing Form S-7's five-year Exchange Act reporting requirement to three years and eliminating or easing certain qualitative criteria.[80]

That same year, the Commission further expanded short-form registration by adopting Form S-16, which increased the scope of offerings available to issuers eligible to use Form S-7.[81]

Specifically, Form S-16 allowed these issuers to register secondary offerings of securities listed on a national securities exchange, conversions of convertible securities, and warrant exercises.[82]

Unlike Form S-7, Form S-16 allowed incorporation by reference of an issuer's Exchange Act reports, including forward incorporation, and required fewer disclosures.[83]

In 1976, the Commission again amended Form S-7 to extend its availability—and, by extension, that of Form S-16—to a larger number of issuers.[84]

The amendments made Form S-7 available to issuers with a class of

debt

securities registered under section 12(b) as well as issuers with a section 15(d) reporting obligation. They also permitted use by successor issuers and certain majority-owned subsidiaries of Form S-7 eligible parents, while broadening eligibility by reducing the Exchange Act reporting timeliness requirement from three years to one year. In addition, the amendments eliminated the board stability and dividend coverage requirements and eased the financial performance requirement.[85]

The Commission also retained certain safeguards—including the requirement that issuers have filed all Exchange Act reports for 36 months—“to assure that sufficient information about registrants using the form is available to the investing public through the Exchange Act reporting system.” [86]

In 1978, the Commission further expanded the scope of short-form registration by amending Form S-16 to permit primary cash underwritten offerings by any Form S-7 eligible issuer with a public float of at least $50 million.[87]

The amendments also allowed offerings by majority-owned subsidiaries whose securities were fully and unconditionally guaranteed by a parent meeting the $50 million public float threshold. The Commission characterized these amendments as “extremely important,” noting that they were expected to “reduce registration costs and thus the costs of raising capital, facilitate timely access to the capital markets, make more meaningful the periodic reporting requirements of the Exchange Act and eliminate needless duplication of disclosure which results in increased costs to investors.” [88]

At the same time, the Commission explained that the $50 million public float requirement was intended to limit eligibility to “a small top tier of companies . . . which usually provide high quality corporate communication documents, including [Exchange] Act reports, and whose corporate information is widely disseminated because members of this class of registrants are widely followed by debt and equity analysts.” [89]

( printed page 31032)

In 1982, the Commission replaced Forms S-7 and S-16 with Forms S-2 and S-3 as part of adopting the “integrated disclosure system.” [90]

Form S-2 allowed any issuer that had been an Exchange Act reporting company for at least 36 months (and had timely filed its reports during the prior 12 calendar months) to register any transaction, other than an exchange offer, on a short-form basis.[91]

Similar to Form S-7, instead of providing all required disclosures directly in the prospectus, issuers that qualified to use the form could choose to either (i) deliver a copy of the annual report to security holders with the prospectus or (ii) present issuer-oriented information comparable to that required to be included in such annual report in the prospectus. In either case, the more complete issuer information required by the form was incorporated by reference into the prospectus from the issuer's most recent annual report on Form 10-K. Form S-2 did not permit forward incorporation; accordingly, updating amendments (which required Commission or staff action to become effective) had to be filed for ongoing offerings.[92]

As initially adopted, Form S-3 permitted registration of any primary or secondary offering if the issuer had, among other requirements: (1) been subject to Exchange Act reporting for at least 36 months; (2) timely filed its Exchange Act reports for the 12 months prior to filing the registration statement; and (3) at least $150 million in public float, or, alternatively, at least $100 million in public float if the annual trading volume of such stock was at least three million shares.[93]

An issuer also could register certain specific transactions on Form S-3 without regard to public float, including primary offerings of investment grade non-convertible debt or preferred stock, secondary offerings of a class of securities listed on a national securities exchange or quoted on the Nasdaq interdealer quotation system, rights offerings to shareholders, offerings of securities issuable upon exercise of warrants or upon conversion of other outstanding securities, and offerings pursuant to dividend and interest reinvestment plans.[94]

The Commission adopted Form S-3 “in reliance on the efficient market theory,” [95]

with registrant and transaction requirements designed to “relat[e] short-form registration to the existence of widespread following in the marketplace.” [96]

Based on commenter input, the Commission explained that “a test based on the registrant's [public] float . . . is an appropriate measure of marketplace following” and determined that “a [public] float of $150 million is the appropriate level at which short-form registration should be allowed.” [97]

c. History of Shelf Registration

At the same time it adopted Forms S-2 and S-3 in 1982, the Commission also adopted Rule 415 as a “temporary rule.” [98]

Rule 415 conditionally permitted shelf registration and codified Commission staff practice that had informally permitted shelf registration prior to that time.[99]

The Commission permanently adopted Rule 415 in 1983 after it concluded that the rule “has operated efficiently and has provided registrants with important benefits in their financings, most notably cost savings.” [100]

In doing so, the Commission acknowledged commenters' concerns regarding the “adequacy of disclosure and due diligence” [101]

and addressed those concerns by “limiting the Rule to primary offerings of securities qualified to be registered on Form S-3 or F-3 and to traditional shelf offerings.” [102]

The Commission noted that “[t]he integrated disclosure system addresses concerns about the quality and timeliness of disclosure by ensuring that the marketplace is provided with a continuous stream of high quality corporate information about registrants widely followed in the marketplace.” [103]

The Commission further stated that “[f]or registrants not eligible to use short form registration, . . . concerns about disclosure and due diligence outweigh the benefits of Rule 415.” [104]

( printed page 31033)

In 1992, the Commission amended Form S-3 to make it and, by extension, shelf registration, available to a broader group of issuers and classes of transactions.[105]

It increased the pool of eligible issuers by shortening the requisite Exchange Act reporting history from 36 to 12 months for most issuers and reducing the public float requirement from $150 million to $75 million.[106]

In proposing these amendments, the Commission cited the success of Form S-3 and the integrated disclosure system over the previous 10 years, which had “achieved their intended effects of providing issuers efficient access to the public securities markets without compromising investor protection” and “improvement in the quality of ongoing Exchange Act reporting.” [107]

Among other things, the Commission noted that the amendments “would provide significant cost savings, efficiency and flexibility for many issuers” and, with respect to the expanded access to shelf registration, “allow[ ] significantly greater numbers of issuers the flexibility to access the public securities markets on demand without having to obtain additional clearance from the Commission's staff,” which would “remove unnecessary regulatory obstacles to capital raising.” [108]

The 1992 amendments also permitted shelf registration of debt, equity, and other securities on an unallocated basis and provided for immediate effectiveness of Form S-3 registration statements for dividend and interest reinvestment plans.[109]

The Commission suggested that unallocated offerings may promote greater use of shelf offerings, especially for common stock offerings. In this regard, the Commission noted “[t]he limited use of shelf registration for common stock,” which it attributed to “concerns by registrants about the market effects from the overhang created by such registration, as well [as] concerns that the market would view even a registration statement for possible future sales of common stock as signaling management's view that the price of the stock has reached a peak.” [110]

The Commission addressed these concerns by allowing issuers to identify the types of securities covered by the registration statement without having to identify the specific amount (either number of shares or dollar amount) of each category to be offered (these registration statements are commonly referred to as “universal shelf registration statements”).

The Commission further liberalized the shelf registration process in several ways in a 2005 rulemaking titled “Securities Offering Reform.” [111]

First, the Commission permitted a new category of issuers, referred to as WKSIs, greater flexibility in registering their securities offerings by allowing them to file shelf registration statements on Form S-3 that are automatically effective upon filing with the Commission.[112]

Second, the Commission adopted rules allowing WKSIs using automatic shelf registration statements to pay filing fees at any time (

i.e.,

either in advance of a takedown or on a “pay-as-you-go” basis at the time of each takedown).[113]

The “pay-as-you-go” model enabled WKSIs to file shelf registration statements without specifying a total dollar amount of securities to be offered. Third, the Commission eliminated a provision in Rule 415 that limited the amount of securities that could be registered for certain primary offerings on Form S-3 to an amount reasonably expected to be offered and sold within two years.[114]

Fourth, WKSIs were permitted to add new classes of securities or securities of an eligible subsidiary to an already effective automatic shelf registration statement by post-effective amendment.[115]

Finally, the amendments eliminated certain limitations imposed on ATM offerings by seasoned issuers.[116]

To further enhance issuers' access to the public markets, the Commission in 2007 again amended the eligibility requirements of Form S-3.[117]

These amendments allowed an even greater number of issuers to conduct primary securities offerings on the form, and, in turn, to conduct shelf offerings. Significantly, under these amendments, an issuer could use Form S-3 to conduct primary shelf offerings without regard to the size of its public float or the rating of its debt to be offered if it satisfied the form's registrant requirements, was not a shell company, was exchange-listed, and did not sell more than the equivalent of one-third of its public float in primary offerings over any period of 12 calendar months.

In further extending Form S-3 eligibility to a broader group of issuers and allowing the use of Form S-3 without regard to an issuer's public float, the Commission stated its “belie[f] that extending Form S-3 short-form registration to additional issuers should enhance their ability to access the public securities markets.” [118]

The Commission also noted “that such a measure would greatly enhance smaller public companies' access to capital in the securities markets, with far less burden and cost.” [119]

In adopting these amendments, the Commission emphasized “the great advances in the electronic dissemination and accessibility of company disclosure transmitted over the internet in the last several years.” [120]

The Commission, therefore, was “persuaded that the technological advances that have revolutionized communications between companies and the market should allow us to ease the Form S-3 eligibility standards without undermining investor protection or the integrity of the markets.” [121]

Nonetheless, the Commission stated that it was not prepared at that time “to allow unlimited use of this form for

( printed page 31034)

primary offerings by companies who do not have at least $75 million in public float.” [122]

In that regard, the Commission noted certain concerns related to allowing smaller public companies to use shelf registration. Those concerns included “that the securities of smaller public companies are comparatively more vulnerable to price manipulation than the securities of larger public companies, and may also be more prone to financial reporting error and abuses” and “that the disclosure obligations and liability imposed by the federal securities laws on smaller public companies are comparable, but not identical, to the largest reporting companies.” [123]

In part due to those concerns, the Commission stated that only a “modest expansion of Form S-3 . . . eligibility” was warranted at that time.[124]

The Commission further explained, however, that it “may revisit the appropriateness of the form restrictions at a later time if our experience with this revised requirement suggests issuer eligibility for primary offerings on Form S-3 . . . should be further revised.” [125]

The Commission has not further expanded shelf offerings or Form S-3 eligibility since 2007.

d. Public Views on Expanding Form S-3 Eligibility

Over the years, some market participants have advocated for expanding Form S-3 eligibility to reduce compliance costs in connection with registered offerings and to promote capital formation. Those commentators have proposed different methods for accomplishing this objective.

For example, in 2006, the Commission's Advisory Committee on Smaller Public Companies recommended allowing all Exchange Act reporting companies that had been reporting for at least one year and were listed on a national securities exchange or quoted in the over-the-counter market to use Form S-3.[126]

In response to a 2011 Commission proposing release, one commenter recommended eliminating Form S-3's transaction requirements and permitting its use by issuers that had reliably filed Exchange Act reports for at least one year.[127]

Participants at the Commission's 2012 Government-Business Forum on Small Business Capital Formation recommended permitting “all public companies (regardless of public float or exchange-traded status) to utilize Form S-3 for primary and secondary offerings” or eliminating the one-third limit under General Instruction I.B.6 for exchange-listed issuers.[128]

In 2015, another commentator supported making Form S-3 available to any issuer current in its Exchange Act reporting obligations, regardless of public float.[129]

At the “Small Cap Policy Roundtable: Reassessing the Framework for Small Public Companies” hosted by the Commission's Office of the Advocate for Small Business Capital Formation, some participants recommended reconsideration of: (1) the One-Year Seasoning requirement and the requirement to have a Form 10-K on file to use Form S-3; (2) the $75 million public float requirement in General Instruction I.B.1 and raising the related one-third limit in General Instruction I.B.6; (3) whether failing to file a Form 8-K should result in a 12-month ineligibility to use Form S-3; and (4) whether it makes sense to lose Form S-3 eligibility over a limited omission of XBRL tags.[130]

Also in 2025, the New York City Bar Association recommended that all exchange-listed issuers be permitted to register offerings in any amount on Form S-3.[131]

More recently, a participant at the Commission's annual Small Business Forum recommended that the Commission consider shortening the One-Year Seasoning requirement, eliminating or reducing the $75 million public float requirement in General Instruction I.B.1, and eliminating or reducing the 12-month ineligibility that results from a late Form 8-K filing.[132]

Various others commentators have recommended modernizing the registration process or shelf eligibility without specifying the manner for doing so.[133]

There also have been legislative attempts to expand access to Form S-3 by allowing all exchange-listed issuers to register any offering on the form, regardless of public float, and to allow non-exchange-listed issuers to register on Form S-3 primary offerings of up to one-third of their public float.[134]

Opponents of these proposals, however, cautioned that such changes could “allow companies to avoid SEC staff review and risk increased fraud and market manipulation, particularly for non-exchange traded companies.” [135]

( printed page 31035)

2. Proposed Amendments

We are proposing to amend Form S-3's registrant requirements and to eliminate the form's transaction requirements [136]

to simplify and expand eligibility, thereby allowing significantly more issuers to avail themselves of the form's flexibility to access the public securities markets on demand.[137]

With respect to the registrant requirements, the proposed amendments would eliminate the “One-Year Seasoning,” “Certain Failures to Make Payments and Defaults,” “Electronic Filings,” and “Interactive Data Files” eligibility requirements described above.[138]

The proposed amendments would retain the “Current in Exchange Act Reporting” and “Timely in Exchange Act Reporting” requirements and would add two new registrant requirements prohibiting a subset of “ineligible issuers,” as that term is defined in Rule 405, and certain other types of issuers (as discussed in section II.A.2.a.v below) from using Form S-3.

With respect to the transaction requirements, the proposed amendments would eliminate those requirements, including the requirement in General Instruction I.B.1 that the issuer have a public float of $75 million or more to offer an unlimited amount of securities for cash on Form S-3. As such, any issuer that meets the proposed registrant requirements would be eligible to use Form S-3 for any primary or secondary offering of the issuer's securities.[139]

Each of the proposed amendments is discussed, in turn, below.[140]

a. Form S-3 Registrant Requirements

i. Exchange Act Reporting (One-Year Seasoning, Current, and Timely Requirements)

We propose to eliminate the One-Year Seasoning requirement (which currently is in General Instruction I.A.3(a)) that requires an issuer to have been an Exchange Act reporting company for at least 12 calendar months prior to filing a Form S-3 because, as discussed in section I.B above, we believe an investor's ability to obtain issuer-specific information in Exchange Act reports does not depend on the length of an issuer's reporting history. Rather, the ability to obtain such information depends on whether an issuer is current and timely with respect to its reporting obligations. Under the proposed amendments, an issuer would immediately become eligible to use Form S-3 upon having a class of securities registered pursuant to section 12(b) or 12(g), or becoming subject to section 15(d), of the Exchange Act.[141]

Although we are proposing to eliminate the One-Year Seasoning requirement, we are proposing to retain the Current and Timely in Exchange Act Reporting requirements.[142]

Specifically, proposed General Instruction I.A.1.a would set forth the requirement that an issuer be subject to the Exchange Act's reporting requirements, and proposed General Instructions I.A.1.b and c, respectively, would set forth the Current and Timely in Exchange Act Reporting requirements. Accordingly, under the proposed amendments, Form S-3 eligibility would be contingent on (among other things) an issuer being subject to the Exchange Act's reporting requirements and having timely filed all reports and other materials required to be filed under sections 13(a), 14(a), 14(c), and 15(d) of the Exchange Act, other than specified reports on Form 8-K, during the preceding 12 calendar months and any portion of a month immediately preceding the filing of a Form S-3, or, if an issuer had been subject to such requirements for less than 12 calendar months, during the time the issuer had been required to file such reports and materials.[143]

( printed page 31036)

We continue to believe issuers must be current and timely with respect to their Exchange Act reports at the time of filing a registration statement on Form S-3 because short-form and shelf registration are premised on the availability of information about an issuer.[144]

If an issuer is not current in its Exchange Act reporting obligations, then the issuer-specific information that may be needed to make an investment decision would not be available. Moreover, where Exchange Act reports that are required to be incorporated by reference into a Form S-3 have not been filed, the issuer likely would not be in compliance with section 10 of the Securities Act.[145]

Further, we believe that conditioning Form S-3 eligibility on the timely filing of Exchange Act reports establishes a compelling incentive for issuers to timely file their Exchange Act reports, thereby helping ensure continuous availability of issuer-specific information even after the shelf registration statement has become effective and in the period during which an issuer conducts its offerings and at other times.

Consistent with the Commission staff's current practice of not objecting to use of Form S-3 when an untimely filing has been made under certain limited circumstances, we also propose to amend the form's instructions to provide that an issuer would remain Form S-3 eligible notwithstanding an untimely filing having been made during the relevant lookback period so long as: (a) the filing was made within seven calendar days of the original due date (where 17 CFR 240.12b-25 (“Rule 12b-25”) applies, the seven calendar days would be calculated from the filing's original due date and not from the end of the time period prescribed under Rule 12b-25 [146]

) and (b) the issuer made only one untimely filing during the relevant lookback period.[147]

We want to encourage issuers to make their Exchange Act filings on a timely basis. At the same time, however, we believe loss of Form S-3 eligibility can be a disproportionately harsh consequence for a single untimely filing during a 12-month period. Accordingly, we propose to permit issuers to remain Form S-3 eligible when the conditions described herein are satisfied. We believe a seven-day period provides a reasonable amount of time to file the missed report or other material while helping ensure investors receive necessary information within a reasonable timeframe.

The One-Year Seasoning requirement may make registered offerings less attractive or feasible for new Exchange Act reporting companies. Currently, such issuers must file a new Securities Act registration statement on Form S-1 for any registered offerings conducted during their first year of being an Exchange Act reporting company despite having already filed a Securities Act or Exchange Act registration statement through which the issuer became an Exchange Act reporting company that contained much of the same information that would be in the new Form S-1. Further, these newly public companies cannot conduct shelf offerings, making it difficult for them to take advantage of favorable market conditions to efficiently raise capital from the public markets or to meet unexpected capital needs during this one-year period. Eliminating the One-Year Seasoning requirement would allow issuers to use Form S-3 and conduct shelf offerings immediately after becoming an Exchange Act reporting company.[148]

We recognize that eliminating the One-Year Seasoning requirement may raise concerns about extending Form S-3 eligibility to issuers without a demonstrated ability to comply with their Exchange Act reporting obligations. Specifically, there may be a view that issuers are more likely to become delinquent in their Exchange Act reporting obligations during their first year as a reporting company and, therefore, they should not be able to use Form S-3 until they have demonstrated an ability to comply with the Exchange Act. Despite these concerns, we do not believe an initial seasoning period is necessary.

Consistent with the Commission's longstanding approach, the essential aspect of Form S-3 and shelf eligibility is whether requisite information about an issuer is available to investors at the time they make an investment decision. Although there is a risk that an issuer without a demonstrated ability to comply with its Exchange Act reporting obligations will become delinquent in its reporting obligations while it has an effective registration statement on Form S-3, we do not believe this possibility alone should preclude an issuer from filing a Form S-3 at a time when it is otherwise eligible to do so as there are other investor protection measures in place.[149]

To the extent an issuer were to

( printed page 31037)

become delinquent before conducting a takedown from a shelf registration statement, it would still have to assess whether the registration statement contained all of the required information and whether the prospectus contained all information required under the Securities Act.[150]

Further, as discussed below, failure to provide the material information required to be included in the registration statement would raise liability concerns under the Federal securities laws. Our proposed prohibition of certain ineligible issuers from using Form S-3, as discussed in section II.A.2.a.iv below, also may help address concerns about the types of issuers that may pose a higher risk of non-compliance with their Exchange Act reporting obligations.

Under the proposed amendments, some issuers using Form S-3 may have shorter Exchange Act reporting histories than Form S-3 eligible issuers do today. Nonetheless, we do not believe that such potential differences in issuers' Exchange Act reporting histories would pose heightened investor protection risks. As an initial matter, all Form S-3 issuers would be required to incorporate by reference (or otherwise disclose) the same issuer-related information and remain subject to the same liability standards as today.[151]

For example, currently Item 12(a)(1) of Form S-3 requires an issuer to incorporate by reference its latest annual report on Form 10-K that contains audited financial statements for the registrant's latest fiscal year for which a Form 10-K was required to be filed and any Exchange Act reports filed since the end of such fiscal year. Under the proposed amendments, an issuer that had not been required to file a Form 10-K since becoming subject to section 13(a) or 15(d) of the Exchange Act would instead incorporate by reference a Securities Act or Exchange Act filing that contains “Form 10 information” [152]

with all financial statements required by Regulation S-X. In addition, issuers would be required to provide “such further material information, if any, as may be necessary to make the required statements, in the light of the circumstances under which they are made, not misleading.” [153]

Under Item 11(a) of Form S-3 (as revised by the proposed amendments), issuers also would be required to describe any and all material changes in the issuer's affairs which have occurred since the end of the most recent fiscal year covered by the audited annual financial statements required to be included in the registration statement pursuant to Item 12(a)(1) that have not been described in a filing incorporated by reference into the registration statement. Further, to the extent an issuer had not yet been required to file a Form 10-K, Commission staff would have had the opportunity to review the information disclosed in the Securities Act or Exchange Act registration statement through which the issuer became an Exchange Act reporting company and which would be incorporated by reference into the prospectus.

Finally, other requirements under the Federal securities laws are designed to ensure investors are adequately protected and receive the information necessary to make an informed investment decision in connection with a registered securities offering. For example, under the Securities Act, anyone who acquires an issuer's securities in a registered offering has a private right of action under section 11 and a purchaser has a private right of action under section 12(a)(2). Section 11 liability exists for untrue statements of material fact or omissions of material facts required to be included in a registration statement or necessary to make the statements in the registration statement not misleading at the time the registration statement became effective.[154]

Importantly, underwriters,

( printed page 31038)

experts such as accountants, an issuer's directors, and other signatories can be held strictly liable for material misstatements or omissions; [155]

thus, these parties are incentivized to ensure an issuer's disclosures are free of material misstatements or omissions, thereby helping to protect investors.[156]

Under section 12(a)(2), sellers have liability to purchasers for offers or sales by means of a prospectus or oral communication that includes an untrue statement of material fact or omits to state a material fact necessary to make the statements made, based on the circumstances under which they were made, not misleading. Moreover, section 17(a) of the Securities Act provides, among other things, that it shall be unlawful for any person in the offer or sale of a security to obtain money or property by means of any untrue statement of a material fact or any omission to state a material fact necessary to make the statements made, in light of the circumstances under which they were made, not misleading. Thus, to the extent that there may be a higher risk of delinquency by issuers with shorter Exchange Act reporting histories, and less historical information for investors to review when an issuer has been subject to the Exchange Act's reporting requirements for a shorter period of time, the Federal securities laws generally require that issuers provide investors with information about an issuer that is necessary to make an informed investment decision and provide remedies to investors when these disclosure standards are not satisfied. We believe that investors will continue to be protected by these liability provisions of the Federal securities laws and receive material information even in the absence of an initial Exchange Act seasoning requirement.

For these reasons, we propose to eliminate the One-Year Seasoning requirement.

Request for Comment

1. We are proposing to eliminate the One-Year Seasoning requirement in General Instruction I.A.3(a) that requires an issuer to have been an Exchange Act reporting company for at least 12 calendar months before becoming eligible to use Form S-3. Should we adopt the amendment as proposed? If not, please explain why the One-Year Seasoning requirement is necessary.

2. Instead of eliminating the One-Year Seasoning requirement altogether, should we shorten the required seasoning period? If yes, what would be an appropriate seasoning period and why?

3. Notwithstanding the proposal to eliminate the One-Year Seasoning requirement, we are proposing to require issuers to be subject to the Exchange Act's reporting requirements and current and timely in their Exchange Act reporting obligations during the 12 calendar months (or such shorter period that the issuer has been subject to the Exchange Act's reporting requirements) and any portion of a month immediately preceding the filing of a Form S-3. Should we retain these requirements as proposed?

4. As discussed in section II.A.2.a.i and footnote 148 above, the proposed amendments would allow issuers to use Form S-3 and conduct shelf offerings immediately after becoming an Exchange Act reporting company. Would this aspect of the proposed amendments alter market practice with respect to initial public offerings (“IPOs”)? For example, would the proposed amendments affect the need for, or use of, an overallotment option (

i.e.,

“greenshoe”), given the proposed ability to use Form S-3 for follow-on primary offerings after the completion of the IPO? If so, are there any investor protection concerns resulting from such a change in market practice? Would the proposed amendments affect how issuers choose to go public? For example, would the proposed ability to use Form S-3 for shelf offerings immediately after becoming a reporting company affect the extent to which direct listings would be used by companies as a means of going public?

5. As discussed in footnote 55, Form S-3 currently requires (and under the proposed amendments, would continue to require) an issuer to have been timely in its Exchange Act reports “during the twelve calendar months and any portion of a month immediately preceding the filing of the registration statement.” Should we revise this standard to instead require only a 12-month (or one-year) lookback? Under this alternative approach, an issuer intending to file a Form S-3 on July 19, 2026, for example, would need to have been current and timely in its Exchange Act filings—other than specified Form 8-K reports—from July 19, 2025 through July 19, 2026 (rather than from July 1, 2025 through July 19, 2026). Why or why not?

6. We are proposing to amend Form S-3's instructions to provide that an issuer would remain eligible to use the form notwithstanding an untimely filing having been made during the relevant lookback period so long as: (a) the filing was made within seven calendar days of the original due date and (b) the issuer had only one untimely filing during the relevant lookback period. Should we adopt the amendment as proposed? Would a shorter or longer period than seven calendar days be appropriate? For example, should the period be 10 business days rather than seven calendar days? Are there other conditions that we should include in this proposed instruction?

7. Under the proposed amendments, an issuer would be required to be subject to the Exchange Act's reporting requirements. Should issuers that voluntarily comply with the reporting requirements of section 13(a) or 15(d) be eligible to use Form S-3 if they have filed all reports and materials that would otherwise be required of an issuer subject to the Exchange Act's reporting requirements?

8. Should we amend our rules to require reassessing of Form S-3 eligibility each time an issuer conducts a shelf takedown to help ensure issuers remain current and timely and investors have available all required information at the time they make an investment decision?

9. Under the proposed amendments to Item 12(a)(1) of Form S-3, an issuer that was not yet required to file a Form 10-K since becoming subject to section 13(a) or 15(d) of the Exchange Act would instead have to incorporate by reference a Securities Act or Exchange Act filing that contains Form 10 information with respect to each class of securities to be registered on Form S-3. The term “Form 10 information” would

( printed page 31039)

be defined as the information required by Form 10 to register under the Exchange Act each class of securities to be registered on the Form S-3. The proposed amendments also would provide that a filing contains Form 10 information even if it omits the information required by Item 202 of Regulation S-K with respect to a class of securities registered on this Form. Should we adopt the amendments as proposed? Is it necessary to specify that the Form 10 information need not include the information required by Item 202 of Regulation S-K? Should similar treatment be permitted for other Form 10 disclosure requirements? Why or why not?

10. We propose to amend Item 12(b) of Form S-3 to eliminate the requirement for forward incorporation by reference of proxy or information statements, or other material, filed under section 14(a) or 14(c) of the Exchange Act. We also propose to eliminate Item 12(b)'s reference to section 13(c) of the Exchange Act. Should we adopt the amendments as proposed?

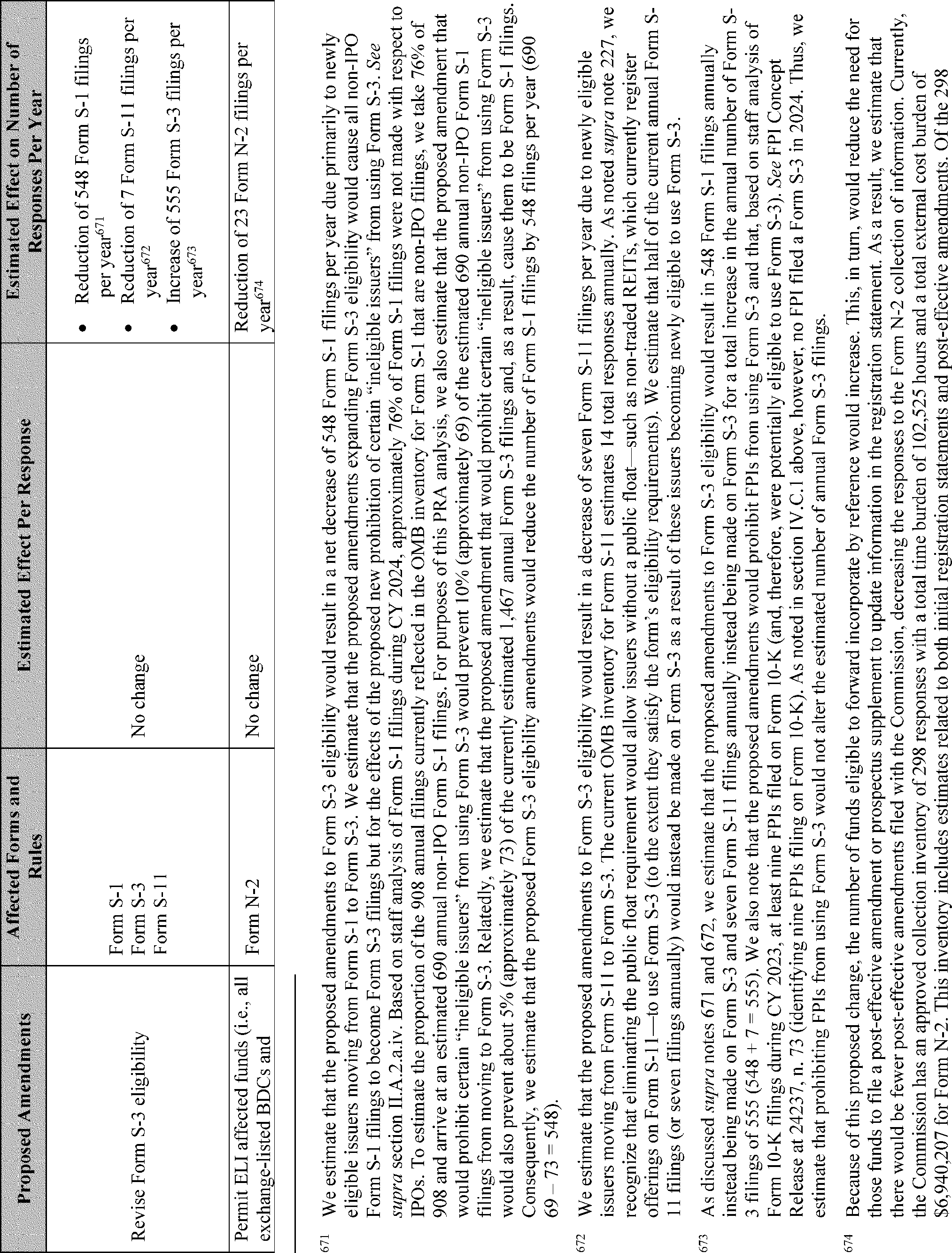

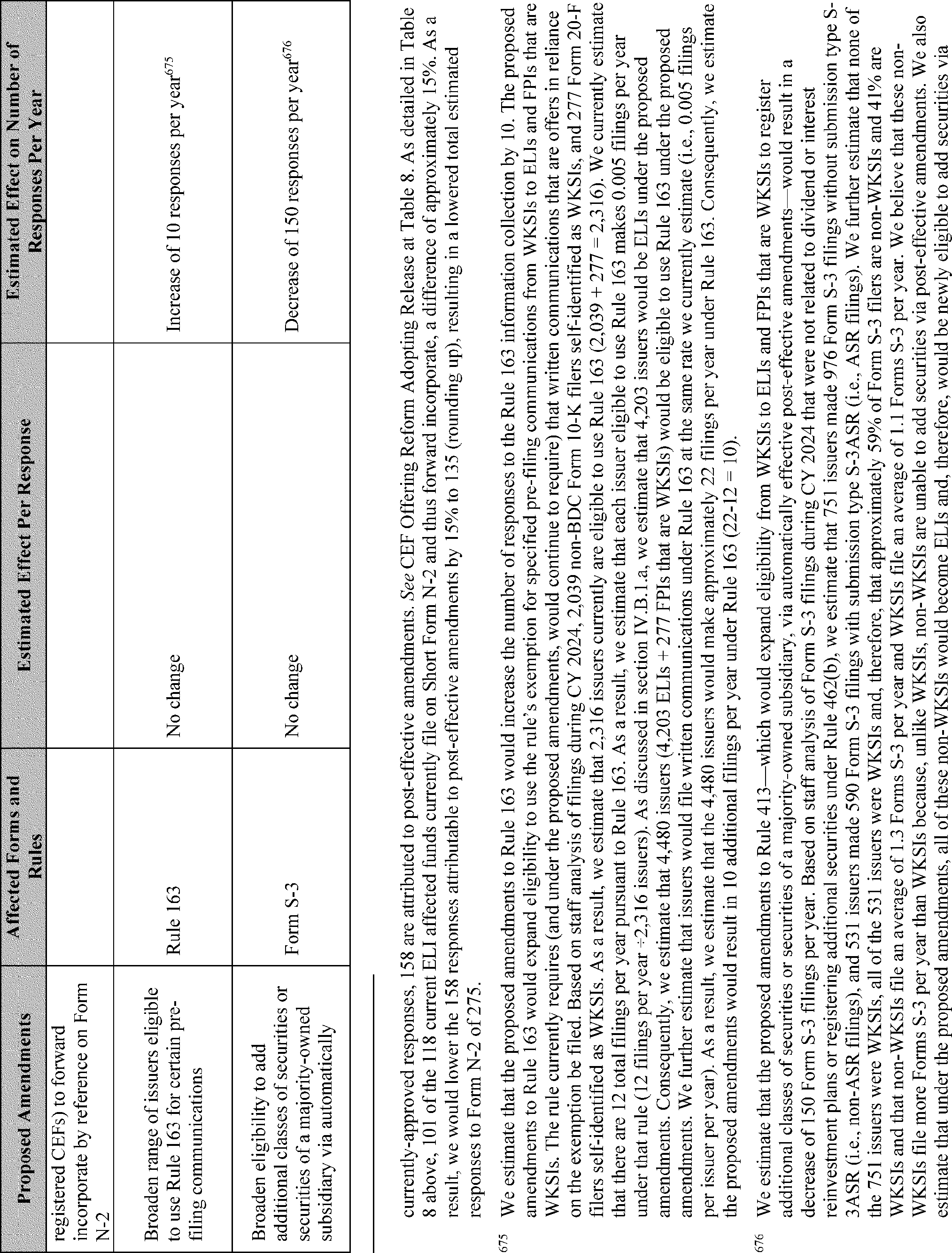

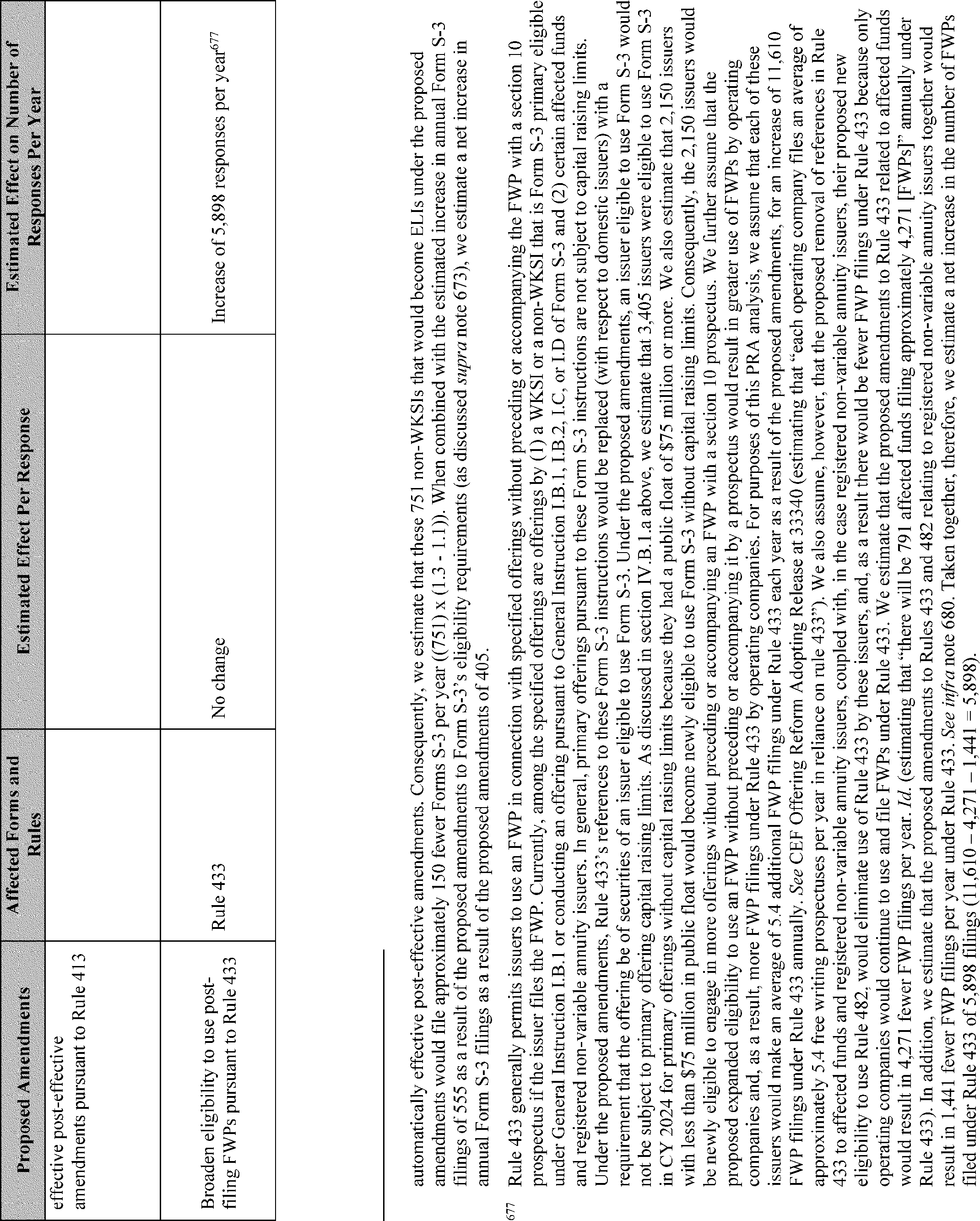

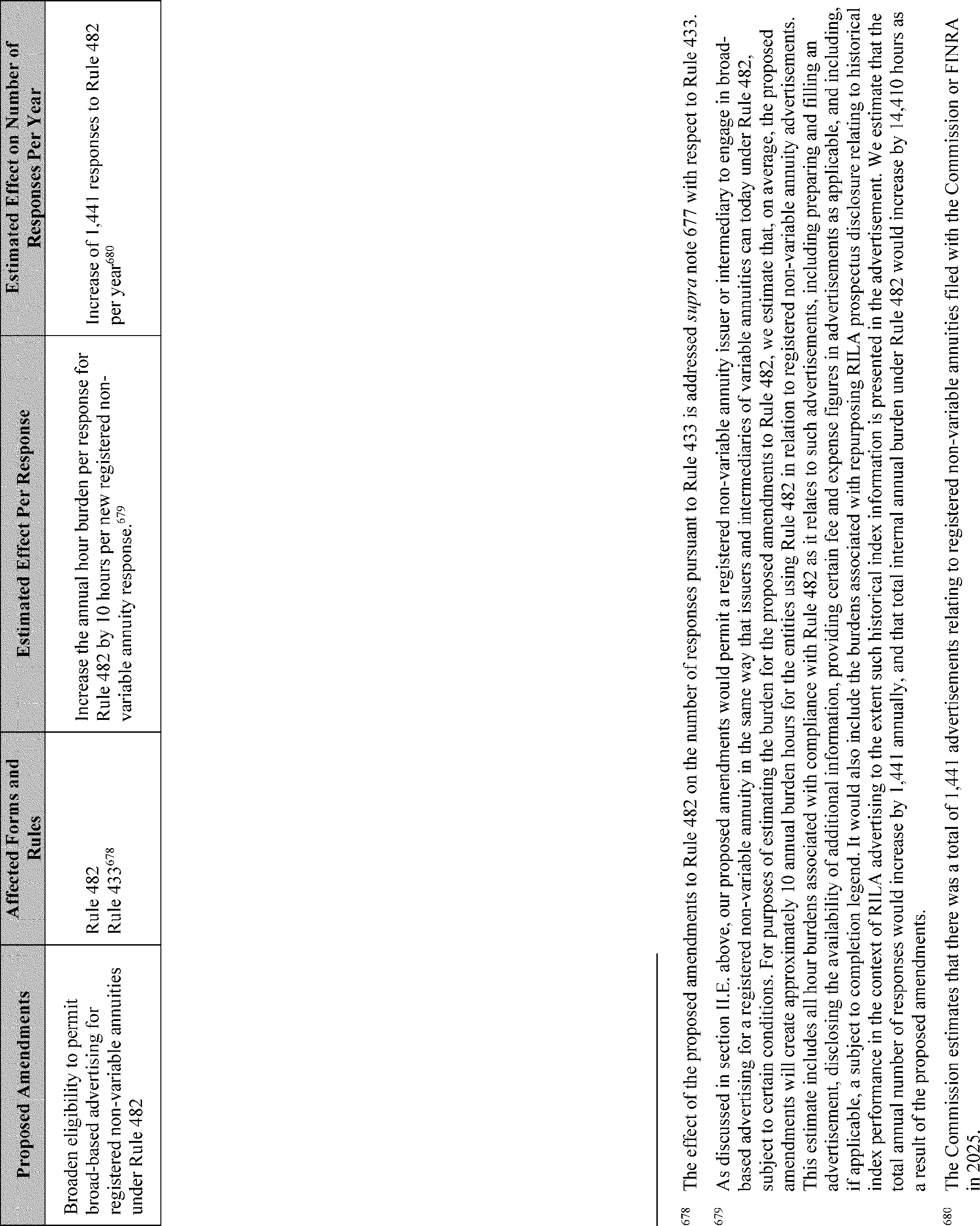

11. We propose to amend Item 12(b) of Form S-3, consistent with prior staff guidance, to clarify that all Exchange Act reports filed pursuant to sections 13(a) and 15(d) “after the date of filing the initial registration statement and prior to the termination of the offering” would be deemed to be incorporated by reference into the prospectus. Should we adopt the amendment as proposed?